a summer internship report on investment … · for more project report visit techshristi.com a ......

TRANSCRIPT

For more project report visit techshristi.com

A

SUMMER INTERNSHIP REPORT

ON

INVESTMENT PLANNING OF AHMEDABADI PEOPLE

Submitted to

L.J. Institute of Engineering and Technology

In requirement of partial fulfillment of

Master’s of Business Administration(MBA)

2 year full time Program of Gujarat Technological University

Submitted on:

14th July 2010

Submitted by:

CHIRAG BHARATKUMAR GANATRA

Batch No.: 2009 -11

For more project report visit techshristi.com

Certificate

It is hereby certified that the work incorporated in the thesis

submitted entitled “Topic” submitted by (Student’s name)

comprises the result of independent and original investigation

carried out me. The material which obtained (and used) from

other sources has been duly acknowledged in the thesis.

Date: 10TH JULY 2010

Place:A’BAD Signature of the student

It is certified that the work mentioned above is carried out

under my guidance.

Date:

Place: Signature of the faculty guide

For more project report visit techshristi.com

1.1 History of the Indian Mutual Fund Industry

The origin of mutual fund industry in India is with the introduction of the concept of mutual fund by UTI in

the year 1963. Though the growth was slow, but it accelerated from the year 1987 when non-UTI players

entered the industry.

In the past decade, Indian mutual fund industry had seen dramatic improvements, both quality wise as

well as quantity wise. Before, the monopoly of the market had seen an ending phase; the Assets Under

Management (AUM) was Rs. 67bn. The private sector entry to the fund family raised the AUM to Rs. 470

bn in March 1993 and till April 2004; it reached the height of 1,540 bn.

Putting the AUM of the Indian Mutual Funds Industry into comparison, the total of it is less than the

deposits of SBI alone, constitute less than 11% of the total deposits held by the Indian banking industry.

The main reason of its poor growth is that the mutual fund industry in India is new in the country. Large

sections of Indian investors are yet to be intellectuated with the concept. Hence, it is the prime

responsibility of all mutual fund companies, to market the product correctly abreast of selling.

The mutual fund industry can be broadly put into four phases according to the development of the sector.

Each phase is briefly described as under.

First Phase – 1964-87

Unit Trust of India (UTI) was established on 1963 by an Act of Parliament. It was set up by the Reserve

Bank of India and functioned under the Regulatory and administrative control of the Reserve Bank of

India. In 1978 UTI was de-linked from the RBI and the Industrial Development Bank of India (IDBI) took

over the regulatory and administrative control in place of RBI. The first scheme launched by UTI was Unit

Scheme 1964. At the end of 1988 UTI had Rs.6700 crores of assets under management.

For more project report visit techshristi.com

Second Phase – 1987-1993 (Entry Of Public Sector Funds

1987 marked the entry of non- UTI, public sector mutual funds set up by public sector banks and Life

Insurance Corporation of India (LIC) and General Insurance Corporation of India (GIC). SBI Mutual Fund

was the first non- UTI Mutual Fund established in June 1987 followed by Canbank Mutual Fund (Dec 87),

Punjab National Bank Mutual Fund (Aug 89), Indian Bank Mutual Fund (Nov 89), Bank of India (Jun 90),

Bank of Baroda Mutual Fund (Oct 92). LIC established its mutual fund in June 1989 while GIC had set up its

mutual fund in December 1990.

At the end of 1993, the mutual fund industry had assets under management of Rs.47, 004 crores.

Third Phase – 1993-2003 (Entry Of Private Sector Funds)

With the entry of private sector funds in 1993, a new era started in the Indian mutual fund industry, giving

the Indian investors a wider choice of fund families. Also, 1993 was the year in which the first Mutual Fund

Regulations came into being, under which all mutual funds, except UTI were to be registered and

governed. The erstwhile Kothari Pioneer (now merged with Franklin Templeton) was the first private

sector mutual fund registered in July 1993.

The 1993 SEBI (Mutual Fund) Regulations were substituted by a more comprehensive and revised Mutual

Fund Regulations in 1996. The industry now functions under the SEBI (Mutual Fund) Regulations 1996.

The number of mutual fund houses went on increasing, with many foreign mutual funds setting up funds

in India and also the industry has witnessed several mergers and acquisitions. As at the end of January

2003, there were 33 mutual funds with total assets of Rs. 1, 21,805 crores. The Unit Trust of India with

Rs.44541 crores of assets under management was way ahead of other mutual funds.

For more project report visit techshristi.com

Fourth Phase – Since February 2003

In February 2003, following the repeal of the Unit Trust of India Act 1963 UTI was bifurcated into two

separate entities. One is the Specified Undertaking of the Unit Trust of India with assets under

management of Rs.29,835 crores as at the end of January 2003, representing broadly, the assets of US 64

scheme, assured return and certain other schemes. The Specified Undertaking of Unit Trust of India,

functioning under an administrator and under the rules framed by Government of India and does not

come under the purview of the Mutual Fund Regulations.

The second is the UTI Mutual Fund Ltd, sponsored by SBI, PNB, BOB and LIC. It is registered with SEBI and

functions under the Mutual Fund Regulations. With the bifurcation of the erstwhile UTI which had in

March 2000 more than Rs.76, 000 crores of assets under management and with the setting up of a UTI

Mutual Fund, conforming to the SEBI Mutual Fund Regulations, and with recent mergers taking place

among different private sector funds, the mutual fund industry has entered its current phase of

consolidation and growth. As at the end of September, 2004, there were 29 funds, which manage assets

of Rs.1, 53,108 crores under 421 schemes.

For more project report visit techshristi.com

2. Introduction to Mutual Funds

2.1 What is a Mutual Fund?

4

A Mutual Fund is a trust that pools the savings of a number of investor who share a common financial

goal. The money thus collected is then invested in capital market instruments such as shares, debentures

and other securities. The income earned through these investments and the capital appreciations realized

are shared by its unit holders in proportion to the number of units owned by them. Thus a Mutual Fund is

the most suitable investment for the common man as it offers an opportunity to invest in a diversified,

professionally managed basket of securities at a relatively low cost.

For more project report visit techshristi.com

Definition of Mutual Fund

A mutual fund is just the connecting bridge or a financial intermediary that allows a group of

investors to pool their money together with a predetermined investment objective. The mutual

fund will have a fund manager who is responsible for investing the gathered money into specific

securities (stocks or bonds). When you invest in a mutual fund, you are buying units or portions

of the mutual fund and thus on investing becomes a shareholder or unit holder of the fund.

Mutual funds are considered as one of the best available investments as compare to others they are very

cost efficient and also easy to invest in, thus by pooling money together in a mutual fund, investors can

purchase stocks or bonds with much lower trading costs than if they tried to do it on their own. But the

biggest advantage to mutual funds is diversification, by minimizing risk & maximizing returns.

For more project report visit techshristi.com

Organization Structure of Mutual Fund Industry

To protect the interest of the investors, SEBI formulates policies and regulates the mutual

funds. It notified regulations in 1993 (fully revised in 1996) and issues guidelines from time to

time. MF either promoted by public or by private sector entities including one promoted by

foreign entities is governed by these regulations.

SEBI approved Asset Management Company (AMC) manages the funds by making

investments in various types of securities. Custodian, registered with SEBI, holds the securities

of various schemes of the fund in its custody.

According to SEBI Regulations, two thirds of the directors of Trustee Company or board of

trustees must be independent. The Association of Mutual Funds in India (AMFI) reassures the

investors in units of mutual funds that the mutual funds function within the strict regulatory

framework. Its objective is to increase public awareness of the mutual fund industry. AMFI

also is engaged in upgrading professional standards and in promoting best industry practices in

diverse areas such as valuation, disclosure, transparency etc.

For more project report visit techshristi.com

Mutual Fund Operation Flow Chart

A Mutual Fund is a trust that pools the saving of number of investors who shares a common financial goal.

The money thus collected is the invested in capital market instrument such as shares, debentures. The

income earned through these investments and the capital appreciation realized is shares by its unit

holders in proportion to the number of units owned by them. Thus a mutual fund is the most suitable

investment for the common man as it offers an opportunity to invest in a diversified, professionally

managed basket of securities at a relatively low cost.

For more project report visit techshristi.com

The risk return trade-off indicates that if investor is willing to take higher risk then

correspondingly he can expect higher returns and vise versa if he pertains to lower risk

instruments, which would be satisfied by lower returns. For example, if an investors opt for bank

FD, which provide moderate return with minimal risk. But as he moves ahead to invest in capital

protected funds and the profit-bonds that give out more return which is slightly higher as

compared to the bank deposits but the risk involved also increases in the same proportion.

Thus investors choose mutual funds as their primary means of investing, as Mutual funds provide

professional management, diversification, convenience and liquidity. That doesn’t mean mutual fund

investments risk free. This is because the money that is pooled in are not invested only in debts funds

which are less riskier but are also invested in the stock markets which involves a higher risk but can

expect higher returns. Hedge fund involves a very high risk since it is mostly traded in the derivatives

market which is considered very volatile.

For more project report visit techshristi.com

2.2 Types of Mutual Funds

Types of Funds as per Structure: -

For more project report visit techshristi.com

1) Equity Funds:

Equity funds are considered to be the more risky funds as compared to other fund types, but

they also provide higher returns than other funds. It is advisable that an investor looking to

invest in an equity fund should invest for long term i.e. for 3 years or more. There are different

types of equity funds each falling into different risk bracket. In the order of decreasing risk level,

there are following types of equity funds:

a. Aggressive Growth Funds: In Aggressive Growth Funds, fund managers aspire for maximum capital

appreciation and invest in less researched shares of speculative nature. Because of these speculative

investments Aggressive Growth Funds become more volatile and thus, are prone to higher risk than

other equity funds.

b. Growth Funds: Growth Funds also invest for capital appreciation (with time horizon of 3 to 5 years)

but they are different from Aggressive Growth Funds in the sense that they invest in companies that

are expected to outperform the market in the future. Without entirely adopting speculative

strategies, Growth Funds invest in those companies that are expected to post above average

earnings in the future.

c. Speciality Funds: Specialty Funds have stated criteria for investments and their portfolio comprises

of only those companies that meet their criteria. Criteria for some specialty funds could be to

invest/not to invest in particular regions/companies. Specialty funds are concentrated and thus, are

comparatively riskier than diversified funds... There are following types of specialty funds:

I. Sector Funds: Equity funds that invest in a particular sector/industry of the market are known

as Sector Funds. The exposure of these funds is limited to a particular sector (say Information

Technology, Auto, Banking, Pharmaceuticals or Fast Moving Consumer Goods) which is why

they are more risky than equity funds that invest in multiple sectors.

II. Foreign Securities Funds: Foreign Securities Equity Funds have the option to invest in one or

more foreign companies. Foreign securities funds achieve international diversification and

hence they are less risky than sector funds. However, foreign securities funds are exposed to

foreign exchange rate risk and country risk.

III. Mid-Cap or Small-Cap Funds: Funds that invest in companies having lower market

capitalization than large capitalization companies are called Mid-Cap or Small-Cap Funds.

Market capitalization of Mid-Cap companies is less than that of big, blue chip companies (less

For more project report visit techshristi.com

than Rs. 2500 crores but more than Rs. 500 crores) and Small-Cap companies have market

capitalization of less than Rs. 500 crores. Market Capitalization of a company can be calculated

by multiplying the market price of the company's share by the total number of its outstanding

shares in the market. The shares of Mid-Cap or Small-Cap Companies are not as liquid as of

Large-Cap Companies which gives rise to volatility in share prices of these companies and

consequently, investment gets risky.

IV. Option Income Funds*: While not yet available in India, Option Income Funds write options

on a large fraction of their portfolio. Proper use of options can help to reduce volatility, which

is otherwise considered as a risky instrument. These funds invest in big, high dividend yielding

companies, and then sell options against their stock positions, which generate stable income

for investors.

d. Diversified Equity Funds: Except for a small portion of investment in liquid money market,

diversified equity funds invest mainly in equities without any concentration on a particular

sector(s). These funds are well diversified and reduce sector-specific or company-specific risk.

However, like all other funds diversified equity funds too are exposed to equity market risk. One

prominent type of diversified equity fund in India is Equity Linked Savings Schemes (ELSS). As per

the mandate, a minimum of 90% of investments by ELSS should be in equities at all times. ELSS

investors are eligible to claim deduction from taxable income (up to Rs 1 lakh) at the time of filing

the income tax return. ELSS usually has a lock-in period and in case of any redemption by the

investor before the expiry of the lock-in period makes him liable to pay income tax on such

income(s) for which he may have received any tax exemption(s) in the past.

e. Equity Index Funds: Equity Index Funds have the objective to match the performance of a specific

stock market index. The portfolio of these funds comprises of the same companies that form the

index and is constituted in the same proportion as the index. Equity index funds that follow broad

indices (like S&P CNX Nifty, Sensex) are less risky than equity index funds that follow narrow

sectoral indices (like BSEBANKEX or CNX Bank Index etc). Narrow indices are less diversified and

therefore, are more risky.

f. Value Funds - Value Funds invest in those companies that have sound fundamentals and whose

share prices are currently under-valued. The portfolio of these funds comprises of shares that are

trading at a low Price to Earning Ratio (Market Price per Share / Earning per Share) and a low

Market to Book Value (Fundamental Value) Ratio. Value Funds may select companies from

diversified sectors and are exposed to lower risk level as compared to growth funds or specialty

For more project report visit techshristi.com

funds. Value stocks are generally from cyclical industries (such as cement, steel, sugar etc.) which

make them volatile in the short-term. Therefore, it is advisable to invest in Value funds with a

long-term time horizon as risk in the long term, to a large extent, is reduced.

g. Equity Income or Dividend Yield Funds - The objective of Equity Income or Dividend Yield Equity

Funds is to generate high recurring income and steady capital appreciation for investors by

investing in those companies which issue high dividends (such as Power or Utility companies

whose share prices fluctuate comparatively lesser than other companies' share prices). Equity

Income or Dividend Yield Equity Funds are generally exposed to the lowest risk level as

compared to other equity funds.

2. Debt/Income Funds:

Funds that invest in medium to long-term debt instruments issued by private companies, banks,

financial institutions, governments and other entities belonging to various sectors (like infrastructure

companies etc.) are known as Debt / Income Funds. Debt funds are low risk profile funds that seek to

generate fixed current income (and not capital appreciation) to investors. In order to ensure regular

income to investors, debt (or income) funds distribute large fraction of their surplus to investors.

Although debt securities are generally less risky than equities, they are subject to credit risk (risk of

default) by the issuer at the time of interest or principal payment. To minimize the risk of default, debt

funds usually invest in securities from issuers who are rated by credit rating agencies and are considered

to be of "Investment Grade". Debt funds that target high returns are more risky. Based on different

investment objectives, there can be following types of debt funds:

A. Diversified Debt Funds - Debt funds that invest in all securities issued by entities belonging to all

sectors of the market are known as diversified debt funds. The best feature of diversified debt funds

is that investments are properly diversified into all sectors which results in risk reduction. Any loss

incurred, on account of default by a debt issuer, is shared by all investors which further reduces risk

for an individual investor.

B. Focused Debt Funds*: Unlike diversified debt funds, focused debt funds are narrow focus funds that

are confined to investments in selective debt securities, issued by companies of a specific sector or

industry or origin. Some examples of focused debt funds are sector, specialized and offshore debt

funds, funds that invest only in Tax Free Infrastructure or Municipal Bonds.

For more project report visit techshristi.com

C. High Yield Debt funds: As we now understand that risk of default is present in all debt funds, and

therefore, debt funds generally try to minimize the risk of default by investing in securities issued by

only those borrowers who are considered to be of "investment grade". But, High Yield Debt Funds

adopt a different strategy and prefer securities issued by those issuers who are considered to be of

"below investment grade". The motive behind adopting this sort of risky strategy is to earn higher

interest returns from these issuers. These funds are more volatile and bear higher default risk,

although they may earn at times higher returns for investors.

D. Assured Return Funds: Although it is not necessary that a fund will meet its objectives or provide

assured returns to investors, but there can be funds that come with a lock-in period and offer

assurance of annual returns to investors during the lock-in period. Any shortfall in returns is suffered

by the sponsors or the Asset Management Companies (AMCs). These funds are generally debt funds

and provide investors with a low-risk investment opportunity. However, the security of investments

depends upon the net worth of the guarantor (whose name is specified in advance on the offer

document).In the past, UTI had offered assured return schemes (i.e. Monthly Income Plans of UTI)

that assured specified returns to investors in the future. UTI was not able to fulfill its promises and

faced large shortfalls in returns. Eventually, government had to intervene and took over UTI's

payment obligations on itself. Currently, no AMC in India offers assured return schemes to investors,

though possible.

E. Fixed Term Plan Series: Fixed Term Plan Series usually are closed-end schemes having short term

maturity period (of less than one year) that offer a series of plans and issue units to investors at

regular intervals. Unlike closed-end funds, fixed term plans are not listed on the exchanges. Fixed

term plan series usually invest in debt / income schemes and target short-term investors. The

objective of fixed term plan schemes is to gratify investors by generating some expected returns in a

short period.

3. Gilt Funds:

Also known as Government Securities in India, Gilt Funds invest in government papers (named dated

securities) having medium to long term maturity period. Issued by the Government of India, these

investments have little credit risk (risk of default) and provide safety of principal to the investors.

For more project report visit techshristi.com

However, like all debt funds, gilt funds too are exposed to interest rate risk. Interest rates and prices

of debt securities are inversely related and any change in the interest rates results in a change in the

NAV of debt/gilt funds in an opposite direction.

4. Money Market / Liquid Funds:

Money market / liquid funds invest in short-term (maturing within one year) interest bearing debt

instruments. These securities are highly liquid and provide safety of investment, thus making money

market / liquid funds the safest investment option when compared with other mutual fund types.

However, even money market / liquid funds are exposed to the interest rate risk. The typical

investment options for liquid funds include Treasury Bills (issued by governments), Commercial

papers (issued by companies) and Certificates of Deposit (issued by banks).

5. Hybrid Funds:

As the name suggests, hybrid funds are those funds whose portfolio includes a blend of equities,

debts and money market securities. Hybrid funds have an equal proportion of debt and equity in

their portfolio. There are following types of hybrid funds in India:

Balanced Funds: The portfolio of balanced funds include assets like debt securities, convertible

securities, and equity and preference shares held in a relatively equal proportion. The objectives

of balanced funds are to reward investors with a regular income, moderate capital appreciation

and at the same time minimizing the risk of capital erosion. Balanced funds are appropriate for

conservative investors having a long term investment horizon.

Growth-and-Income Funds: Funds that combine features of growth funds and income funds are

known as Growth-and-Income Funds. These funds invest in companies having potential for

capital appreciation and those known for issuing high dividends. The level of risks involved in

these funds is lower than growth funds and higher than income funds.

Asset Allocation Funds: Mutual funds may invest in financial assets like equity, debt, money

market or non-financial (physical) assets like real estate, commodities etc.. Asset allocation

funds adopt a variable asset allocation strategy that allows fund managers to switch over from

one asset class to another at any time depending upon their outlook for specific markets. In

For more project report visit techshristi.com

other words, fund managers may switch over to equity if they expect equity market to provide

good returns and switch over to debt if they expect debt market to provide better returns. It

should be noted that switching over from one asset class to another is a decision taken by the

fund manager on the basis of his own judgment and understanding of specific markets, and

therefore, the success of these funds depends upon the skill of a fund manager in anticipating

market trends.

6. Commodity Funds:

Those funds that focus on investing in different commodities (like metals, food grains, crude oil etc.) or

commodity companies or commodity futures contracts are termed as Commodity Funds. A commodity

fund that invests in a single commodity or a group of commodities is a specialized commodity fund and a

commodity fund that invests in all available commodities is a diversified commodity fund and bears less

risk than a specialized commodity fund. "Precious Metals Fund" and Gold Funds (that invest in gold, gold

futures or shares of gold mines) are common examples of commodity funds.

7. Real Estate Funds:

Funds that invest directly in real estate or lend to real estate developers or invest in shares/securitized

assets of housing finance companies, are known as Specialized Real Estate Funds. The objective of these

funds may be to generate regular income for investors or capital appreciation.

8. Exchange Traded Funds (ETF):

Exchange Traded Funds provide investors with combined benefits of a closed-end and an open-end

mutual fund. Exchange Traded Funds follow stock market indices and are traded on stock exchanges like

a single stock at index linked prices. The biggest advantage offered by these funds is that they offer

diversification, flexibility of holding a single share (tradable at index linked prices) at the same time.

Recently introduced in India, these funds are quite popular abroad.

For more project report visit techshristi.com

9. Fund of Funds:

Mutual funds that do not invest in financial or physical assets, but do invest in other mutual fund

schemes offered by different AMCs, are known as Fund of Funds. Fund of Funds maintain a portfolio

comprising of units of other mutual fund schemes, just like conventional mutual funds maintain a

portfolio comprising of equity/debt/money market instruments or non financial assets. Fund of Funds

provide investors with an added advantage of diversifying into different mutual fund schemes with even

a small amount of investment, which further helps in diversification of risks. However, the expenses of

Fund of Funds are quite high on account of compounding expenses of investments into different mutual

fund schemes.

Types of Mutual Fund Scheme

1. Open-ended Schemes: -

An open-end fund is one that is available for subscription all through the year. These do not have a fixed

maturity. Investors can conveniently buy and sell units at Net Asset Value ("NAV") related prices. The

key feature of open-end schemes is liquidity.

2. Close-ended Schemes: -

A closed-end fund has a stipulated maturity period which generally ranging from 3 to 15 years. The fund

is open for subscription only during a specified period. Investors can invest in the scheme at the time of

the initial public issue and thereafter they can buy or sell the units of the scheme on the stock exchanges

where they are listed. In order to provide an exit route to the investors, some close-ended funds give an

option of selling back the units to the Mutual Fund through periodic repurchase at NAV related prices.

SEBI Regulations stipulate that at least one of the two exit routes is provided to the investor.

3. Interval Schemes: -

Interval Schemes are that scheme, which combines the features of open-ended and close-ended

schemes. The units may be traded on the stock exchange or may be open for sale or redemption during

pre-determined intervals at NAV related prices.

For more project report visit techshristi.com

2.3 Advantages of Mutual Funds

Professional Management: -

The basic advantage of funds is that, they are professional managed, by well qualified

professional. Investors purchase funds because they do not have the time or the expertise to

manage their own portfolio. A mutual fund is considered to be relatively less expensive way to

make and monitor their investments.

Diversification: -

Purchasing units in a mutual fund instead of buying individual stocks or bonds, the investors risk is

spread out and minimized up to certain extent. The idea behind diversification is to invest in a large

number of assets so that a loss in any particular investment is minimized by gains in others.

Economies of Scale: -

Mutual fund buy and sell large amounts of securities at a time, thus help to reducing transaction costs,

and help to bring down the average cost of the unit for their investors.

Liquidity: -

Just like an individual stock, mutual fund also allows investors to liquidate their holdings as and

when they want.

Simplicity: -

Investments in mutual fund are considered to be easy, compare to other available instruments in the

market, and the minimum investment is small. Most AMC also have automatic purchase plans whereby

as little as Rs. 2000, where SIP start with just Rs.50 per month basis.

For more project report visit techshristi.com

2.4 Disadvantages of Mutual Funds

Professional Management: -

Some funds doesn’t perform in neither the market, as their management is not dynamic enough to

explore the available opportunity in the market, thus many investors debate over whether or not the so-

called professionals are any better than mutual fund or investor him self, for picking up stocks.

Costs: -

The biggest source of AMC income is generally from the entry & exit load which they charge from

investors, at the time of purchase. The mutual fund industries are thus charging extra cost under layers

of jargon.

Dilution: -

Because funds have small holdings across different companies, high returns from a few investments

often don't make much difference on the overall return. Dilution is also the result of a successful fund

getting too big. When money pours into funds that have had strong success, the manager often has

trouble finding a good investment for all the new money.

Taxes: -

When making decisions about your money, fund managers don't consider your personal tax situation.

For example, when a fund manager sells a security, a capital-gain tax is triggered, which affects how

profitable the individual is from the sale. It might have been more advantageous for the individual to

defer the capital gains liability.

For more project report visit techshristi.com

2.5 Association of Mutual Funds in India (AMFI)

With the increase in mutual fund players in India, a need for mutual fund association in India was

generated to function as a non-profit organization. Association of Mutual Funds in India (AMFI) was

incorporated on 22nd August, 1995.

AMFI is an apex body of all Asset Management Companies (AMC) which has been registered with SEBI.

Till date all the AMCs are that have launched mutual fund schemes are its members. It functions under

the supervision and guidelines of its Board of Directors.

Association of Mutual Funds India has brought down the Indian Mutual Fund Industry to a professional

and healthy market with ethical lines enhancing and maintaining standards. It follows the principle of

both protecting and promoting the interests of mutual funds as well as their unit holders.

The objectives of Association of Mutual Funds in India

The Association of Mutual Funds of India works with 38 registered AMCs of the country. It has certain

defined objectives which juxtaposes the guidelines of its Board of Directors. The objectives are as

follows:

This mutual fund association of India maintains a high professional and ethical standard in all

areas of operation of the industry.

It also recommends and promotes the top class business practices and code of conduct which is

followed by members and related people engaged in the activities of mutual fund and asset

management. The agencies who are by any means connected or involved in the field of capital

markets and financial services also involved in this code of conduct of the association.

AMFI interacts with SEBI and works according to SEBIs guidelines in the mutual fund industry.

Association of Mutual Fund in India does represent the Government of India, the Reserve Bank

of India and other related bodies on matters relating to the Mutual Fund Industry.

It develops a team of well qualified and trained Agent distributors. It implements a programme

of training and certification for all intermediaries and other engaged in the mutual fund industry.

For more project report visit techshristi.com

AMFI undertakes all India awareness programme for investors in order to promote proper

understanding of the concept and working of mutual funds.

SEBI Regulations Regarding Mutual Fund :

Mutual Funds shall be established in the form of trusts under the Indian Trust Act and

managed separately formed asset Management Company.

Money Market mutual Fund would be regulated by the RBI and Other Mutual Funds Would be

regulated by SEBI.

Fifty percent (50%) members of the board of AMC must be independent directors and must

have no connection with sponsoring organization.

The directors should have at least 10 years experience in the field of Portfolio management,

Financial Administration.

The AMC should have minimum Net Worth of RS 10 crores

An AMC can not act as the AMC for another Mutual Fund

AMCS are also allowed to do other fund based businesses such as providing investment

management services to offshore funds, other mutual funds, venture capital funds, and insurance

companies.

The minimum amount to be raised with each Closed-End scheme should be Rs. 20 crores and

for the Open-Ended scheme Rs 50 crores.

Each Scheme of the Mutual Fund is registered with SEBI before it is floated in the market.

Closed end schemes should not be kept open for subscription for more than 45 days. For open

ended schemes, the first 45 days should be considered for determining the target figure.

The initial issue expenses should not exceed 6% of the funds raised under each scheme.

For each scheme there should be a separate and responsible Fund Manager.

All Mutual Funds mu8st distribute a minimum of 90% of their profits in any given year.

For more project report visit techshristi.com

2.6 Major Mutual Fund Companies in India

CCllaassssiiffiiccaattiioonn ooff AAMMCC’’ss CCuurrrreennttllyy OOppeerraattiinngg

Bank Sponsored:

SBI Fund Management Ltd.

BOB Asset Management Co. Ltd.

Canbank Investment Management Services Ltd.

UTI Asset Management Company Pvt. Ltd.

Private Sector:

Indian:-

BenchMark Asset Management Co. Pvt. Ltd.

Cholamandalam Asset Management Co. Ltd.

Credit Capital Asset Management Co. Ltd.

Escorts Asset Management Ltd.

JM Financial Mutual Fund

Kotak Mahindra Asset Management Co. Ltd.

Reliance Capital Asset Management Ltd.

Sahara Asset Management Co. Pvt. Ltd

Sundaram Asset Management Company Ltd.

Tata Asset Management Private Ltd.

DWS Mutual Fund

JP Morgan Mutual Fund

Lotus India Mutual Fund

Tuarus Mutual Fund

PNB Mutual Fund

For more project report visit techshristi.com

Predominantly India Joint Ventures:-

Birla Sun Life Asset Management Co. Ltd.

DSP Merrill Lynch Fund Managers Limited

HDFC Asset Management Company Ltd.

Jardine Fleming Mutual Fund

Quantum Mutual Fund

Predominantly Foreign Joint Ventures:-

ABN AMRO Asset Management (I) Ltd.

Alliance Capital Asset Management (India) Pvt. Ltd.

Deutsche Asset Management (India) Pvt. Ltd.

Fidelity Fund Management Private Limited

Franklin Templeton Asset Mgmt. (India) Pvt. Ltd.

HSBC Asset Management (India) Private Ltd.

ING Investment Management (India) Pvt. Ltd.

Morgan Stanley Investment Management Pvt. Ltd.

Optimix Mutual Fund

Principal Asset Management Co. Pvt. Ltd.

Prudential ICICI Asset Management Co. Ltd.

Standard Chartered Asset Mgmt Co. Pvt. Ltd.

Institutions:

GIC Asset Management Co. Ltd.

Jeevan Bima Sahayog Asset Management Co. Ltd.

For more project report visit techshristi.com

Source (For Page-1to23): www.amfiindia.com

For more project report visit techshristi.com

3.1 Company Profile

Prudent CAS Ltd, historically known as Prudent Fund Manager established in 2000, is a

registered investment company offering fee-based money management, financial planning, and

investment advisory services. We help you build a personalized investment strategy to ensure

your financial goals are met. We focus on each client, build investment strategies tailored to

specific client needs, and regularly review those strategies to increase the likelihood of success.

What are your goals and aspirations? We'd like to know. Then we can determine an investing

strategy that helps you achieve your full potential.

We Understand - The difference between selling and marketing. Prudent believes in

understanding the customer needs and offering the product that can match his requirement

(marketing) as against just selling what product is already available. Owing to the inherent

professional expertise we first study and understand the investment requirements and

circumstances. Our experts assess the investors' need and their risk profile. Once the entire

comparative analysis is done then the best possible option is advised to the investors. The best

possible option provides the proper asset allocation to various asset classes and also the

estimated risk involved.

This helps us to provide our clients an optional basket of funds rather than selling the typical

available funds. This approach lets us set our focus on the quality work rather than the just the

quantity. Here it is worth mentioning that though we are involved in wide spectrum and heavy

quantum of activities but, if ever it comes to a choice Prudent CAS always prefers to be the best

rather then being the biggest.

For more project report visit techshristi.com

3.2 Overview of Company

Managing Director : Mr. Sanjay Shah

CEO : Mr. Shirish Patel

Director : Mr. Chirag Shah

HOD Details:

IT Head : Mr. Yogi Kanani

Accounts Head : Mr. Chirag Kothari

HR Head : Mr. Dashrathsinh Chundawat

Direct Sales : Mr. Deven Shah (Ahmadabad & North Gujarat Region)

Mr. Rohit Patel (Baroda)

Mr. Satyesh Desai (South Gujarat Region)

Indirect Sales : Mr. Jigar Parekh (North & West India)

Mr. Manoj Singh (Mumbai Region)

Mr. Bhanu P STomar (Pune Territory)

For more project report visit techshristi.com

Head Office Address : Prudent Corporate Advisory Service Ltd.

701, Sears Tower,

Gulbai Tekra,

Off. C.G.Road,

Ahmedabad 380006

Contact : Tel. No: (079) 40209600

Project Guide : Mr. Ayaj Mansuri

Mr. Chirag Modi

For more project report visit techshristi.com

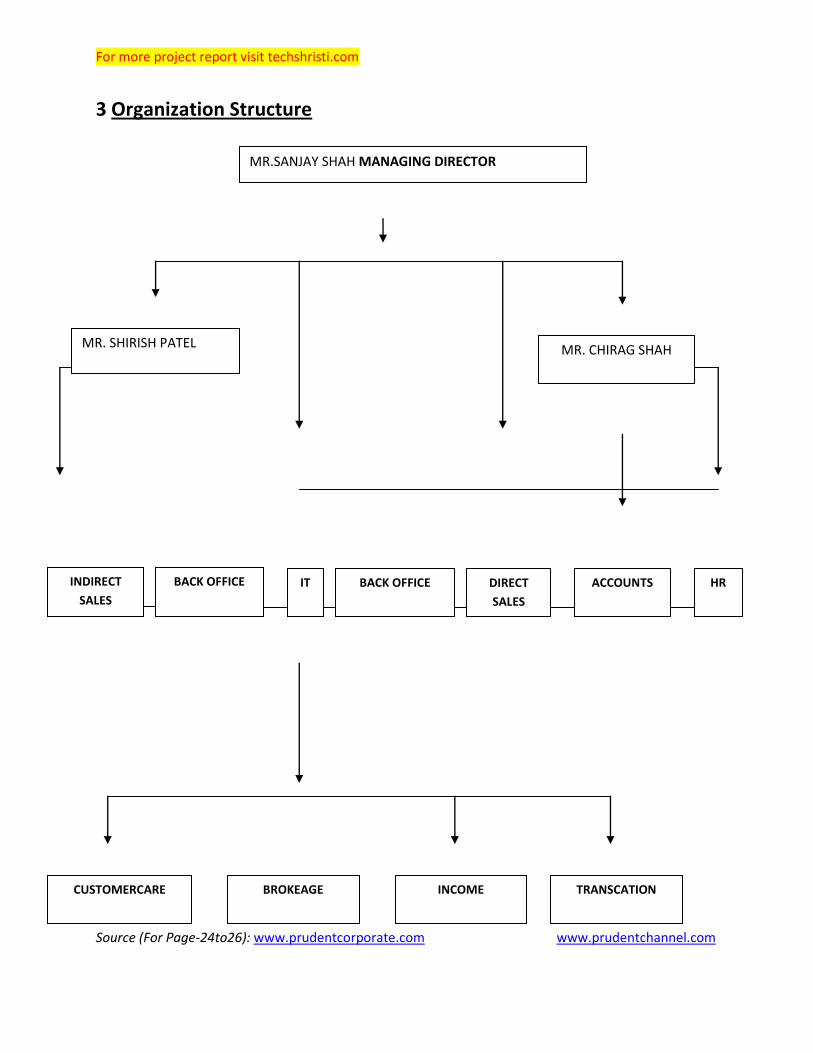

3 Organization Structure

Source (For Page-24to26): www.prudentcorporate.com www.prudentchannel.com

MR.SANJAY SHAH MANAGING DIRECTOR

MR. SHIRISH PATEL

CEO

MR. CHIRAG SHAH

DIRECTOR

INDIRECT

SALES

BACK OFFICE IT BACK OFFICE HR ACCOUNTS DIRECT

SALES

CUSTOMERCARE TRANSCATION INCOME BROKEAGE

For more project report visit techshristi.com

4. Research Methodology

I. Title of project : Investment & Tax Planning of Investors

II. Objectives :

Primary:

To know the investment planning of investors.

To know the tax planning of investors.

Secondary :

To know the Risk-Return pattern of investment.

To know the investment percentage of investor’s income.

To know what influences most preferred for investments.

To know the investors’ preferences regarding the mutual fund scheme

& pattern

To know the percentage of total investment in tax saving funds.

To compare the investment & tax planning of investors on basis of their

occupation.

“On the basis of this research company can focus on investors as per their occupation & their

investment pattern.”

III. Research Type :Basic Research

IV. Research Design :Descriptive

V. Types of Data : Primary

VI. Research Approach : Survey Research

VII. Research Instrument: Questionnaire, Mechanical instrument(

Manual & MS Excel)

VIII. Contact Method : Personnel

IX. Sample Size :360

For more project report visit techshristi.com

X. Classification of Samples :

Government Employees

Private Employees

Businessmen

Professionals

Students

XI. Sample Area : Ahmedabad City

XII. Different Tests : Chi-Test (χ2)