abbott laboratories (abt)

TRANSCRIPT

ABBOTT LABORATORIES (ABT)SHOAIB HAROON | ANGELA JIANGApril 21, 2011

Agenda Company Overview Industry Analysis Competition and SWOT Analysis MD&A Financial Analysis Valuation Recommendation

Company Overview Founded in 1900 by Dr. Wallace C.

Abbott Discovery, development, manufacture,

and sale of diversified line of healthcare products

6th largest global pharmaceutical provider

Headquartered in Abbot Park, Illinois Employees about 90,000

Data from Google Finance

Key Financials FY ‘09 Revenues: $30.76B up 4.2% Market Capitalization: $79.11B P/E: 17.19 Current Share Price: $50.80 Operating Margin: 17.31% Net Profit Margin: 13.15% RoA: 8.27% RoE: 20.45%

Data from Google Finance

Major ProductsMarket Segment

Revenues % Target End User Major Products

Pharmaceuticals

53.60 Government, retailers

Humira, TriCor, TriLipix, Synthroid

Diagnostic Products

11.60 Hospitals, blood banks, clinics

Architect, Imx, Commander, Prism

Nutritional Products

17.20 Retailers, wholesalers, third party distributors

Similac and Isomil brands

Vascular Products

8.80 Hospitals and Abbot owned distribution centers

Xience V, Multi-Link, Starclose

Other 8.90 Healthcare facilities, mail order pharmacies, public warehouses

Blood glucose monitoring meters and stripes, data management software

Revenue Sources

53.60%

17.20%

11.60%

8.80%

8.90%

Pharmaceuticals

Nutritionals

Diagnostics

Vascular

Other

Geographic Sales

U.S., 47%

Eurozone, 21%

UK, 3%

Others, 25%

Industry Drivers M&A activity and licensing activity

In-Licensing Both activities needed to maintain growth

Cost Containment Regulation

Increased use in generics Rising healthcare expenses Aging population

Biologics New manufacturing methods Different treatments

Part D Companies contributing to Medicare Donut hole

Industry Analysis Decelerating growth in recent years

Limited projects in R&D pipelines Decreasing prescription drug needs

Stabilizing growth through 2014 Consolidating industry Increasing product diversification to

maintain competition Cardiovascular and central nervous system

sales most profitable Strong revenue gains from Emerging Markets

Industry Growth

Year Sales (Billions) Growth2005 545.32006 571.5 4.80%2007 601.4 5.20%2008 625.6 4.00%2009 644.2 3.00%

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

2005 2006 2007 2008

Growth Rate for Pharmaceuticals

480500520540560580600620640660

2005 2006 2007 2008 2009

Reve

nue

(In B

illio

ns)

Year

Sales for Pharmaceuticals

Porter’s 5 Forces

Source: Company 10-K

Industry RivalryHigh

Threat of New Entrants

Low

Supplier Power High

Buyer PowerModerate

Threat of Substitutes

Low

Threat of New Entrants: Low New drugs requires large investments Consolidating industry Multiple drugs already exist for known

conditions

Supplier Power: High Manufacturers supplying active

ingredients critical to all parts of pharmaceutical industry R&D Current production

R&D requires new range of drugs Generally sold on contract basis

Buyer Power: Moderate More sales to pharmacies diversifying

target markets Focus on marketing strategy

Different effects of drugs Differentiation of products

Increase in generic prescriptions increasing buying power

Threat of Substitutes: Low Patents protecting revenues Alternative treatments not widely used

but available Generics more targeted towards OTC

medicines Multiple drugs already exist for known

conditions

Rivalry: High Top pharmaceutical companies using

M&A to keep top market share High fixed costs and exit costs Multiple drugs competing to treat same

problem Stress on marketing and sales

Competition

Company Share Price ($)

Market Cap ($mm)

Debt / Equity

2010 Revenue ($mm)

LTM EPS ($)

Johnson & Johnson (JNJ)

64.39 165,678 0.30 61,587 4.8

Sanofi-Aventis (SNY) 38.06 94,054 0.16 45,468 5.9 Medtronic, Inc. (MDT) 40.68 43,053 0.70 15,834 3.0

Boston Scientific (BSX) 7.08 10,665 0.48 7,806 (0.7) Merck Ltd. (MRK) 34.04 231 -- 117 0.9

Novartis A.G. (NVS) 57.92 61 0.38 39 0.9

Abbott (ABT) 50.80 79,360 0.84 35,167 3.0

ABT is generally larger and more leveraged than its competitors with strong EPS

Source: Capital IQ as of 4/20/11

Competition

-20.00

-15.00

-10.00

-5.00

0.00

5.00

Apr-19

-2010

May-04-

2010

May-19-

2010

Jun-03

-2010

Jun-18

-2010

Jul-05-

2010

Jul-20-

2010

Aug-04

-2010

Aug-19

-2010

Sep-03

-2010

Sep-20

-2010

Oct-05-2

010

Oct-20-2

010

Nov-04-

2010

Nov-19-

2010

Dec-06

-2010

Dec-21

-2010

Jan-06

-2011

Jan-21

-2011

Feb-07

-2011

Feb-22

-2011

Mar-09-

2011

Mar-24-

2011

Apr-08

-2011

Index: JNJ, SNY, MDT, BSX, 2 more (Market Cap) - Index Value Abbott Laboratories (NYSE:ABT) - Share Pricing

Source: Capital IQ as of 4/20/11

SWOT Analysis

Market leader in lucrative I&I space

Very diverse dyslipidemia portfolio

Strong revenue base across multiple healthcare segments

Weak pipeline with only 3 drug launches expected out to 2014

Increasing reliance on flagship drug Humira

Weak IP position; faces generic erosion

Strengths Weaknesses

Opportunities Threats Pursue M&A to strengthen

pipeline Collaboration with

AstraZeneca could reinforce Abbott’s positon in the US dyslipidemia market

Continued litigation with J&J and Bayer on patent position of Humira

New biological launches threaten market share in autoimmune disorder space

Management Discussion & Analysis Reshape business portfolio for long-term

growth Focus on acquiring early and late stage

pipeline technologies and growth platforms Solvay Pharmaceuticals (pharma) Advanced Medical Optics (vision care) Visiogen (vision care) Evalve (stuctural heart repair)

Invest $2.9bn on R&D

Source: Company 10-K

Management Discussion & Analysis Grow Pharmaceuticals business internationally

Leverage Humira in emerging markets Acquisition of Solvay Pharmaceuticals to create

presence in Eastern Europe Focus on US growth for Nutrition business

New product launches and leadership in infant formula

Improve profitability for Medical Products business Underwent thorough rebuilding process to

improve margins

Source: Company 10-K

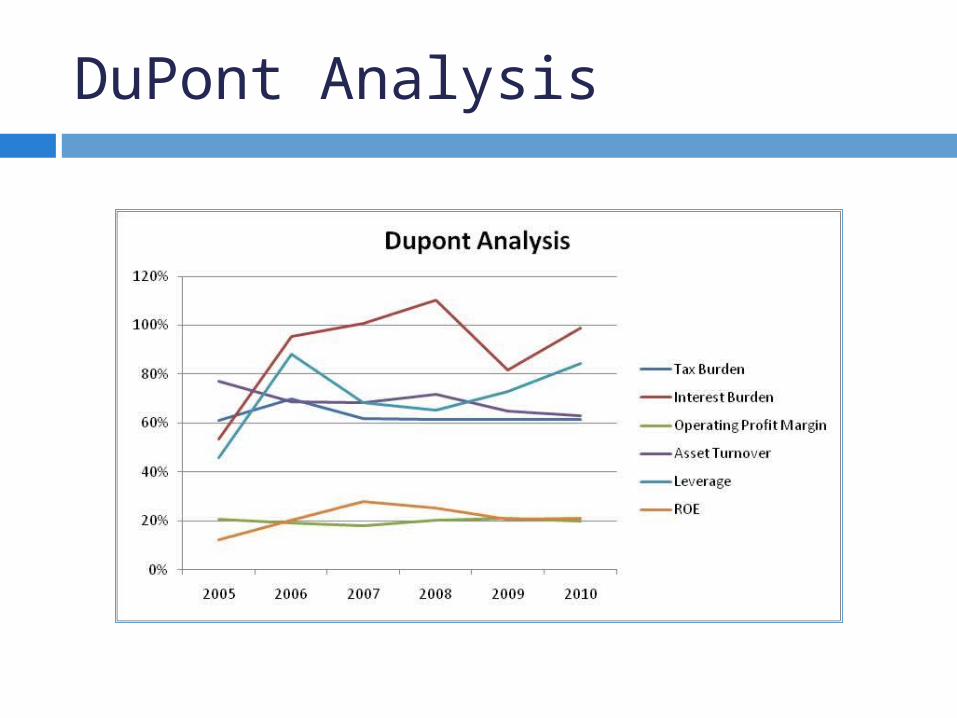

DuPont Analysis

Financial Ratios

Company Operating Margin Net Margin ROA ROE

Boston Scientific (BSX) 14.31% 7.00% 3.10% 4.92%

Johnson & Johnson (JNJ) 26.33% 19.77% 13.50% 24.88%

Medtronic, Inc. (MDT) 30.53% 20.68% 10.84% 22.06%

Merck Ltd. (MRK) 20.22% 1.87% 5.33% 1.66%

Sanofi-Aventis (SNY) 24.75% 17.07% 5.99% 11.23%

Abbott (ABT) 18.93% 12.29% 8.27% 20.45%

Industry 14.10% 10.10% 12.40% 13.80%

ABT’s margins slightly trail competitors’ but its ability to take on leverage is shown by a strong ROE

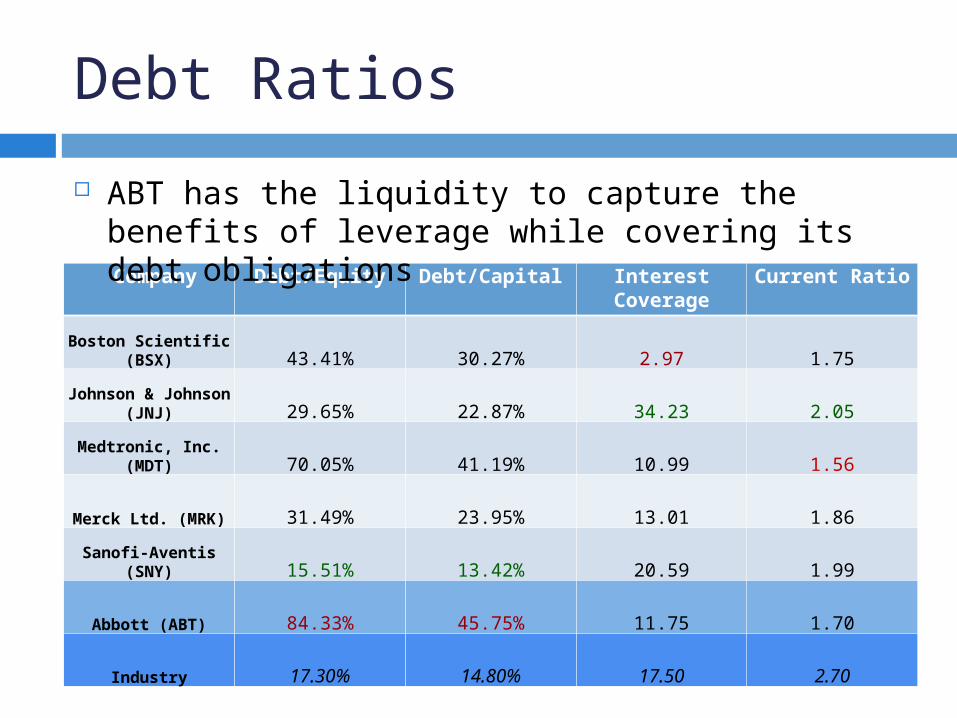

Debt Ratios

Company Debt/Equity Debt/Capital Interest Coverage Current Ratio

Boston Scientific (BSX) 43.41% 30.27% 2.97 1.75

Johnson & Johnson (JNJ) 29.65% 22.87% 34.23 2.05

Medtronic, Inc. (MDT) 70.05% 41.19% 10.99 1.56

Merck Ltd. (MRK) 31.49% 23.95% 13.01 1.86

Sanofi-Aventis (SNY) 15.51% 13.42% 20.59 1.99

Abbott (ABT) 84.33% 45.75% 11.75 1.70

Industry 17.30% 14.80% 17.50 2.70

ABT has the liquidity to capture the benefits of leverage while covering its debt obligations

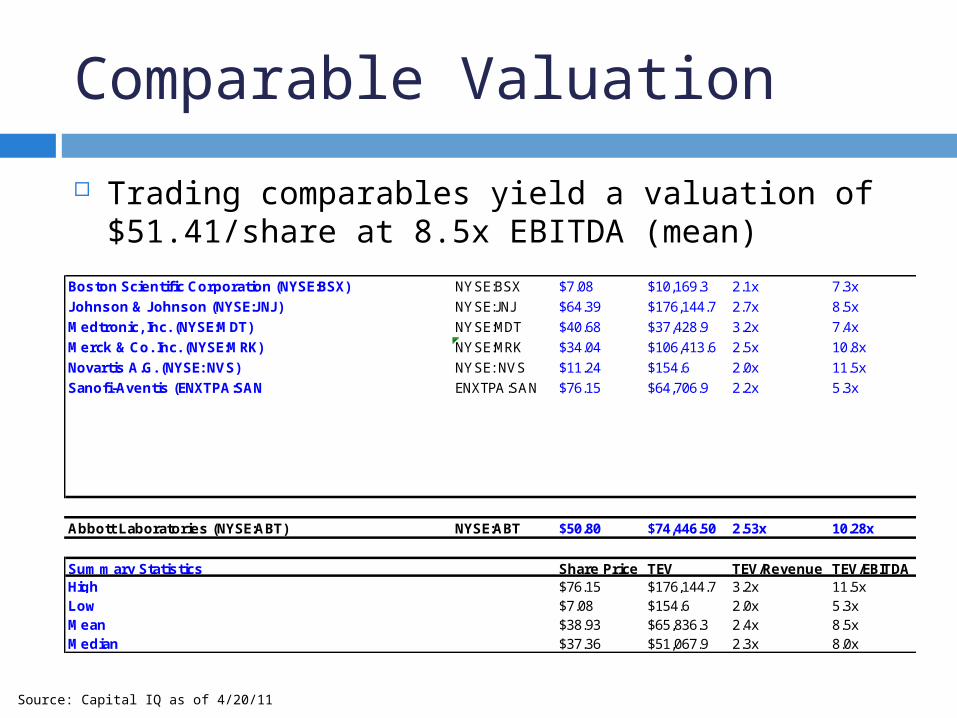

Comparable Valuation Trading comparables yield a valuation of

$51.41/share at 8.5x EBITDA (mean)

Source: Capital IQ as of 4/20/11

Boston Scientific Corporation (NYSE:BSX) NYSE:BSX $7.08 $10,169.3 2.1x 7.3xJohnson & Johnson (NYSE:JNJ) NYSE:JNJ $64.39 $176,144.7 2.7x 8.5xMedtronic, Inc. (NYSE:MDT) NYSE:MDT $40.68 $37,428.9 3.2x 7.4xMerck & Co. Inc. (NYSE:MRK) NYSE:MRK $34.04 $106,413.6 2.5x 10.8xNovartis A.G. (NYSE: NVS) NYSE: NVS $11.24 $154.6 2.0x 11.5xSanofi-Aventis (ENXTPA:SAN ENXTPA:SAN $76.15 $64,706.9 2.2x 5.3x

Abbott Laboratories (NYSE:ABT) NYSE:ABT $50.80 $74,446.50 2.53x 10.28x

Summary Statistics Share Price TEV TEV/Revenue TEV/EBITDAHigh $76.15 $176,144.7 3.2x 11.5xLow $7.08 $154.6 2.0x 5.3xMean $38.93 $65,836.3 2.4x 8.5xMedian $37.36 $51,067.9 2.3x 8.0x

DCF ValuationProjected Year Ending Dec. 31,

2011 2012 2013 2014 2015

Sales $38,332 $39,865 $41,061 $42,703 $44,839EBT $7,556 $7,694 $7,718 $7,204 $7,318Plus: Interest Expense ($494) ($678) ($494) ($910) ($1,201)EBIT $8,050 $8,372 $8,212 $8,114 $8,519Plus: Depreciation $3,085 $3,641 $3,623 $4,007 $4,572EBITDA $11,135 $12,013 $11,835 $12,121 $13,091 EBITDA Margin 29.0% 30.1% 28.8% 28.4% 29.2%

Less: Taxes 1,467 1,517 1,544 1,441 1,464 Less: Capex (1,917) (1,196) (1,232) (1,281) (1,345) Less: Changes in NWC 278 881 518 (377) (1,119)

Unlevered Free Cash Flow $8,029 $8,419 $8,542 $9,776 $11,401 Unlevered Free Cash Flow Growth Rate na 4.9% 1.5% 14.5% 16.6%

Discount Rate 11%Discounted FCFs $7,241 $6,848 $6,267 $6,469 $6,805

DCF Valuation

WACC Calculation

CAPMRisk Free Rate 3.40%Market Risk Premium 6.40%Beta 0.3Cost of Equity 4.30%

RoE 20.50%

Cost of Equity 18.88%Cost of Debt 5.50%

Capital StructureDebt 55.30%Equity 44.70%

WACC 10.87%

Terminal Value CalculationLong-term Grow th Rate 2.5%Terminal Value $139,568Discounted TV $83,301

Value / Share CalculationNPV of FCFs $33,631PV of TV $83,301

Enterprise Value $116,932

Less: Net Debt $14,341Equity Value $102,591

Shares Outstanding 1,556

Value / Share $65.93

DCF yields a valuation of $64.76/share

Valuation Summary

LT Growth Rate$65.93 1.5% 2.0% 2.5% 3.0% 3.5%

7.0% $111.24 $121.40 $133.82 $149.35 $169.319.0% $77.97 $82.91 $88.62 $95.27 $103.14

11.0% $58.78 $61.60 $64.76 $68.31 $72.3313.0% $46.32 $48.10 $50.04 $52.18 $54.5515.0% $37.59 $38.79 $40.08 $41.47 $42.99

WAC

C

DCF yields a valuation of $64.76/share

Comparables yield a valuation of $51.41/share Triangulated value of $58.67/share

Triangulated ValuePrice Weight

DCF $65.93 0.5Comps $51.41 0.5Triangulated Value $58.67

Recommendation Buy 200 shares of ABT at market

Current price: $50.80 Currently undervalued

DCF: $64.76 Comps: $51.41 Triangulated: $58.67 (Price target)