accountancy - university of nigeria, nsukka sunday.pdf · a research project submitted in partial...

TRANSCRIPT

i

OKARO, SUNDAY, CHUKWUNEDU

REG. NO: PG/MSc/05/45025

BRIDGING THE AUDIT EXPECTATION GAP: THE

PERCEPTION OF ICAN MEMBERS

ACCOUNTANCY

A THESIS SUBMITTED TO THE DEPARTMENT OF ACCOUNTANCY, FACULTY OF

BUSINESS ADMINISTRATION, UNIVERSITY OF NIGERIA ENUGU CAMPUS

Webmaster

Digitally Signed by Webmaster’s Name

DN : CN = Webmaster’s name O= University of Nigeria, Nsukka

OU = Innovation Centre

DECEMBER, 2009

ii

BRIDGING THE AUDIT EXPECTATION GAP: THE PERCEPTION OF

ICAN MEMBERS

BY

OKARO, SUNDAY, CHUKWUNEDU

REG. NO: PG/MSc/05/45025

A RESEARCH PROJECT SUBMITTED IN PARTIAL FULFILMENT OF

THE REQUIREMENTS FOR THE DEGREE OF MASTER OF SCIENCE

DEPARTMENT OF ACCOUNTANCY

UNIVERSITY OF NIGERIA,

ENUGU CAMPUS

DECEMBER, 2009

iii

TITLE PAGE

BRIDGING THE AUDIT EXPECTATION GAP: THE PERCEPTION OF

ICAN MEMBERS

BY

OKARO, SUNDAY, CHUKWUNEDU

REG. NO: PG/MSc/05/45025

A RESEARCH PROJECT SUBMITTED IN PARTIAL FULFILMENT OF

THE REQUIREMENTS FOR THE DEGREE OF MASTER OF SCIENCE

IN THE DEPARTMENT OF ACCOUNTANCY

UNIVERSITY OF NIGERIA, ENUGU CAMPUS

DECEMBER, 2009

iv

CERTIFICATION PAGE

The Work embodied in this dissertation is original and has not been submitted in

part or in full for any other diploma or degree of this or any other university.

………………… …..………………..

Okaro, S. C . Date

v

APPROVAL PAGE

This is to certify that Okaro, S.C, a postgraduate student in the department of

Accountancy with the Reg. No. PG/ M.S.c./05/45025 has satisfactorily completed the

requirements for dissertation in partial fulfillment of the requirements for the award of

master of science (M.S.c.) degree in Accountancy.

_________________________________ _____________

Dr. A.U. Nweze Date

Supevisor

_________________________________ _____________

Dr (Mrs) Regina, Gwamniru, Okafor Date

Head of Department

vi

DEDICATION

This Research work is dedicated to THE ALMIGHTY GOD whose guidance and

inspiration throughout this work was palpable.

vii

ACKNOWLEDGEMENTS

I am grateful to my supervisor Dr. A. U. Nweze for his valuable contributions and

encouragement while the work lasted. I owe a debt of gratitude to Professor, U. Modum

for her assistance and understanding. I cannot thank enough my amiable wife, B C.

Okaro (Mrs.) for her understanding and forbearance throughout the duration of the

research work. Similarly, I doff my hat for my children, Emeka, Chidinma, Chijioke,

Ifeoma and Chioma for their sacrifices to enable me pull out this work successfully. My

thanks go to all the amiable lecturers of the department of Accountancy, University of

Nigeria, Enugu campus, for equipping me academically to accomplish this task. They

include Mr. R Ugwuoke, Dr (Mrs.) Regina Okafor, Mrs, E. Onyeanu, Dr. Odo, Mrs.

Ofoegbu, Mrs. Eyisi. Mr. Ezeugwu, Mr.Emengini and Mr. Osita Aguolu. Back at Unizik,

I remain indebted to my colleagues for creating conducive work environment that aided

this work. I am particularly grateful to Professors B. Osisioma and Emma Okoye, Mr. P

Okoye, Mrs. Ogoo Okafor and Dr E Chukwuemeka. I made copious use of Unizik

library at Awka in the Course of this work. I remain grateful to the staff of this great

library. I want also to place on record my gratitude to Cynthia of Resources Application

Ltd. Enugu for editorial assistance. Finally my thanks go to many other people who in

one way or the other contributed to the success of this work but cannot be mentioned

individually for want of space. My prayer is that the good Lord should reward all of you.

viii

ABSTRACT.

This research set out to find out the perception of Members of ICAN, an important

stakeholder group, on the fresh initiatives at bridging the audit expectation gap problem.

Four hypotheses were formulated and tested in the course of this study. A survey design

approach was adopted for the study .Out of a population of 23,324, 159 ICAN

MEMBERS were randomly selected. The t- test statistic and the Chi square were used to

test the hypotheses of the study. The study found out, among others, that 24 out of the 29

methods on offer for bridging the audit expectation gap and articulated in the

questionnaire were acceptable to members of ICAN. Consequent upon the findings, it

was recommended that ICAN should commence the process of implementing some of the

methods within its purview and approved by its members as capable of ameliorating the

expectation gap problem.

ix

TABLE OF CONTENTS

PAGES

Title page … … … … … … … … … i

Certification page … … … … … … … … ii

Approval page … … … … … … … … iii

Dedication … … … … … … … … … iv

Acknowledgement … … … … … … … … v

Abstract … … … … … … … … … vi

Table of Contents … … … … … … … … vii

List of tables … … … … … … … … … xi

CHAPTER ONE

INTRODUCTION … … … … … … … … 1

1.1 Background of the Study … … … … … … 1

1.2 Statement of Research Problem … … … … … 4

1.3 Objectives of Study … … … … … … … 4

1.4 Research Questions … … … … … … … 5

1.5 Research Hypotheses … … … … … … … 5

1.6 Scope and Limitations of study … … … … … 6

1.7 Significance of Study … … … … … … … 7

1.8 Definition of Terms … … … … … … … 8

References … … … … … … … … 9

CHAPTER TWO

2.0 Review of Related Literature and Theoretical Frame work … … 10

2.1 The Nature and Dimensions of Audit expectation

Gap Problem … … … … … … … … 10

2.2 Communication Gap … … … … … … … 10

2.3 Performance Gap … … … … … … … 11

x

2.4 Causes of Performance Gap or Audit Failures … … … 13

2.5 Fresh impetus to The Audit Expectation Gap Problem … … 14

2.6 Some Current methods in issue aimed at Bridging the

Audit Expectation Gap … … … … … … 16

2.7 Fresh Initiatives/Methods aimed at bridging the Audit

Expectation Gap … … … … … … … 18

2.8 Encouragement of Joint Audit and Audit Competition … … 20

2.9 Introduction of Mandatory Rotation of Auditors … … … 21

2.10 Establishment of Financial Reporting Council … … … 23

2.11 Composition of an active Audit Committee made up of

non- executive directors and knowledgeable in

financial matters … … … … … … … 24

2.12 Separation of Audit Services from other services … … … 25

2.13 Punish Company Management who mislead their Auditors… … 27

2.14 Establishment of government oversight body to regulate

Audit Practice … … … … … … … … 28

2.15 Introduce Forensic and Value for Money Audit … … … 30

2.16 Encourage Shareholders to attend annual general meetings

and ask difficult questions … … … … … … 31

2.17 Bridging the audit expectation gap- the perception of

Chartered Accountants- experience from other countries … … 31

2.18 Review of Related Literature and Theoretical Framework-

A summary … … … … … … … … 33

References … … … … … … … … 35

xi

CHAPTER THREE

3.0 Research Design and Methodology … … … … … 36

3.1 Research Design … … … … … … … 36

3.2 Nature and Sources of Data … … … … … … 37

3.3 Population and Sample Size … … … … … … 37

3.4 Data Analysis Technique … … … … … … 39

3.5 Validation and Reliability of Instruments … … … … 41

References … … … … … … … … 42

CHAPTER FOUR

4.0 Data presentation and Analysis … … … .. … 43

4.1 Introduction … … … … … … … … 43

4.2 Presentation and Analysis … … … … … … 43

4.3 Test of Hypotheses 1 … … … … … … … 56

4.4 Test of Hypothesis 2 … … … … … … … 56

4.5 Additional Statistical Test for Hypothesis 2 … … … … 56

4.6 Test of Hypothesis 3 … … … … … … … 60

4.7 Test of Hypothesis 4 … … … … … … … 61

CHAPTER FIVE

5.0 Summary of Findings, Conclusion and Recommendations… … 62

5.1 Summary of Findings … … … … … … … 62

5.2 Conclusion … … … … … … … … 63

5.3 Recommendations … … … … … … … 66

Bibliography … … … … … … … … 68

Appendix [Questionnaire] … … … … … … 74

xii

LIST OF TABLES

2.1 Key Features and advantages of Joint Audit … … … … 20

3.1.5 Point likert Scale … … … … … … … 39

3.2. 3 Point likert Scale … … … … … … … 40

4.1. Questionnaire Administration … … … … … 43

4.2. Experience Distribution of Chartered Accountants … … … 44

4.3. Gender Distribution of Respondents … … … … … 44

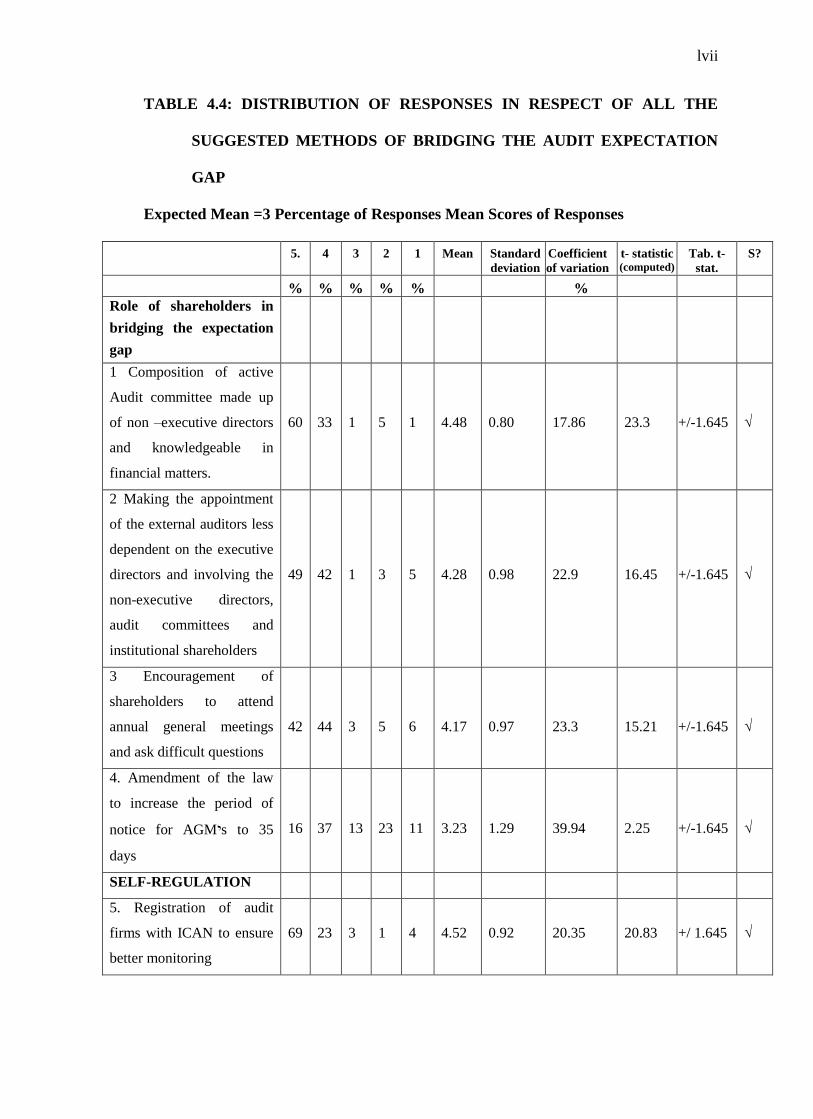

4.4 Distribution of Responses in Respect of all the suggested

methods of bridging the audit expectation Gap … … … 45

4.5. Distribution of methods that were over 75% endorsed

by respondents … … … … … … … 50

4.6 Distribution of methods that received between 50% and 75%

endorsement by respondents … … … … … … 53

4.7 Distribution of methods that received less than 50%

endorsement by respondents … … … … … … 54

4.8 Responses with negative t- calculated values … … … … 56

4.9 Chi square test result for hypothesis 2 … … … … 58

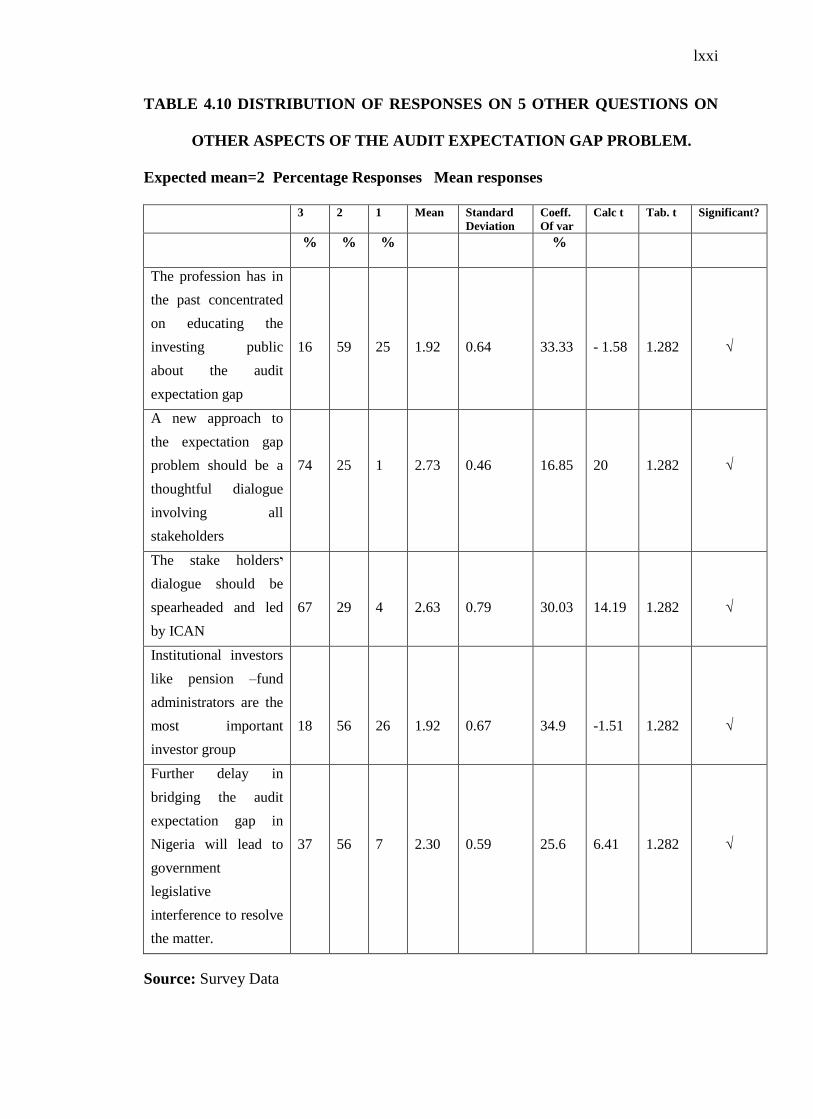

4.10. Distribution of responses on other 5 Questions on bridging

the audit expectation gap … … … … … … 59

xiii

CHAPTER ONE

INTRODUCTION

1.1 BACKGROUND OF THE STUDY

Audit expectation gap is the gap between the role of an auditor as understood by

the auditor and the users of financial statements .It is a gap between what the auditor is

doing and what the society expects him to do creating the impression that the statutory

objective of audit is not meeting the social needs of the populace. The functions

performed by the accounting profession are vital to the growth and stability of the

financial market, whether at the global level or at the local level (Egbiki, 2006: 56 - 57).

An audit has been defined as an examination of the financial statements of an

enterprise by an independent expert (the auditor) with a view to attesting that such

financial report (in his opinion) show a true and fair view of the state of affairs of that

enterprise for the period under review. The contribution of the auditor is to provide

credibility to information. This means that the information can be believed and that it can

be relied upon by outsiders. The outsiders include shareholders and government

regulators. Others are creditors and customers. Usually these third parties use the

information to make various economic decisions. An example of this decision is whether

to invest in the organization. Economic decisions are made under conditions of

uncertainty as there is always a risk that the decision maker will select the wrong

alternative and incur a significant loss. The credibility added to the information by the

auditors actually reduces the decision makers’ risk Therefore auditors reduce information

risk, which is the risk that the financial information used to make a decision is materially

misstated. The legal position is that an audit is carried out to enable an auditor form an

opinion as to the truth and fairness of financial statements presented to him by his client’s

management and to report accordingly. The accuracy of a company’s accounts is the sole

xiv

responsibility of the directors. However, the accounting profession in Nigeria and other

climes has been under intense pressure due to rising public expectations.

These expectations have been fuelled largely as a result of demise of some financial

institutions in the late 80’s to early 1990’s and very recently for banks that failed to meet

the statutory minimum recapitalization to the tune of N25 billion .Yet other banks failed

the CBN ” stress” test. In the light of these developments the heat was turned on

accountants as members of the public sought whom to blame. The wide spread news of

financial scandal and false reporting rife in the collapsed institutions have cast the

organizational controls and auditors in very poor light. It has also tended to undermine

the confidence of the public in the profession to detect and prevent corporate abuses.

Audit failures have been blamed, partly, on greed on the part of auditors. In

defense, auditors have often replied that they are not primarily responsible for detecting

frauds and errors. However, shareholders, depositors and most of the general public

remain unimpressed as they query the value of a watchdog that cannot bark let alone bite.

Most people cannot seem to accept the legally defined status. They would wish to see an

auditor’s certificate as an assurance that all that needs to be known about the financial

transactions of a company have been disclosed to the auditor. In the same vein, an

auditor’s signature should be taken to mean that all is well with the health of the

institution concerned and that there has been no fraud or other malfeasance. This,

however, is often not the case.

Two components of the audit expectation gap have been identified –

communication gap and performance gap. Communication gap has to do with what the

auditors think is their role and what the members of the public perceive should be the role

of auditors. Performance gap, on the other hand, occurs when public expectations are

xv

reasonable but the auditor’s performance does not fulfill them. This means that there is a

short fall in the auditor’s performance. (Okafor and Okaro, 2009: 11).

In the past, attempts have been made to bridge the gap by the profession. For

example attempts have been made to educate users of the limitations of the modern audit

process. As part of the process of educating the user of audited accounts, the modern

audit report usually tries to delineate clearly the respective responsibilities of the directors

of a company and that of the auditor in respect of audited financial statements. The

profession has also tightened the noose on self regulation bringing to book erring

members of the profession. The mandatory continuing professional education whereby

members of professional accounting bodies are compulsorily required to attend

professional seminars has also ensured that members’ skills are updated and horned up.

However, like a sore thumb, the gap appears to have remained as wide as ever. At

the local level, the recent scandal in Cadbury Nigeria Plc whereby profits were overstated

by a whopping sum of over N13 billion, and the subsequent indictment of the accounting

firm of Akintola Williams Delloite for audit failure, has further aggravated the

expectation gap conundrum.

The international community has not been spared either. The collapse of the energy

giant Enron in the United States of America in 2002 as a result of what was obviously a

case of audit failure and wobbly accounting standards has again ignited a global search

for tools to at least narrow the expectation gap.

The literature is awash with fresh suggestions and initiatives aimed at tackling the

problem of expectation gap. ICAN MEMBERS are a very important stakeholder group in

the search for a solution to the expectation gap problem. Their cooperation or lack of it

can have a tremendous effect on the resolution or otherwise of the problem. This work is

xvi

therefore an attempt to document in Nigeria, the perception of ICAN MEMBERS as to

the initiatives for bridging the audit expectation gap problem.

1.2 STATEMENT OF RESEARCH PROBLEM

The global search for a solution to the audit expectation gap problem has become

strident. The credibility of the accounting profession appears to be at its lowest ebb. In

the United States of America, the profession has lost its self regulatory status .In this

circumstance, the profession is bestirring itself and the result is a welter of fresh

suggestions and initiatives aimed at solving the expectation gap problem. Some of the

suggestions appear mundane while some others at best appear controversial. One U.K

research study even concluded that expectation gap problem cannot be eliminated. There

is the belief that the accountancy profession has resisted change in auditing for so long

that it was unlikely to change of its own initiative. In the light of the above, what is the

perception of ICAN MEMBERS in Nigeria as to the fresh suggestions and initiatives

aimed at addressing the expectation gap problem?

1.3 OBJECTIVES OF STUDY

This study has the general objective of ascertaining the perception of ICAN

MEMBERS in Nigeria on the vexed issue of bridging the audit expectation gap. The

specific objectives of this study are as follows

1. To ascertain the perception of ICAN MEMBERS in Nigeria as to the suggestions

for bridging the expectation gap.

2. To test the popularity, among ICAN MEMBERS in Nigeria, of the suggestion that

convocation of all stakeholders dialogue to negotiate the issues involved in the

audit expectation gap problem has become necessary

xvii

3. To elicit the opinion of ICAN MEMBERS in Nigeria as to whether undue delay

by the Accounting profession in Nigeria may lead unwittingly to government

legislative interference.

4. To enquire into the attitude of ICAN MEMBERS in Nigeria as regards enlisting

the co-operation of rival accounting professionals in Nigeria in the search for

solution to the audit expectation gap problem.

1.4 RESEARCH QUESTIONS

This study will be approached in such a way that it will, among others, answer the

following questions

1. What is the perception of ICAN MEMBERS in Nigeria about the efficacy of the

suggestions for bridging the audit expectation gap?

2. What is the opinion of ICAN MEMBERS in Nigeria to the suggestion that the

convocation of a stake holder’s dialogue to negotiate the issues involved has

become desirous?

3. Are ICAN MEMBERS in Nigeria worried that any further delay by the

accounting profession in Nigeria to find a lasting solution to the expectation gap

problem may lead to government legislative interference to resolve it?

4. Are ICAN MEMBERS willing to enlist the cooperation of rival professional

accountancy bodies in Nigeria to confront the monster of audit expectation?

1.5 RESEARCH HYPOTHESES

To achieve the above objectives, the following hypotheses are formulated for the

research study.

1. The acceptability of the 29 methods itemized in the questionnaire and aimed at

bridging the audit expectation gap, to ICAN MEMBERS in Nigeria is not mixed.

xviii

2. The attitude of ICAN MEMBERS in Nigeria towards the suggestion that the

Institute of Chartered Accountants of Nigeria should partner with rival

accountancy bodies to monitor performance of professional accounting firms is

not negative.

3. ICAN MEMBERS in Nigeria perception of the idea of an all inclusive stake

holder’s conference to negotiate the issues involved in bridging the audit

expectation gap is not positive.

4. ICAN MEMBERS in Nigeria attitude to the suggestion that further delay in bridging

the audit expectation gap might lead to government legislative interference to

resolve the issue is not positive..

1.6 SCOPE AND LIMITATIONS OF THE STUDY

The scope of this study is on the perception of ICAN MEMBERS in Nigeria on the

thorny issue of bridging the audit expectation gap given fresh initiatives in this regard.

This study will focus on Nigeria. Accordingly, ICAN MEMBERS in Nigeria will be the

target of this study and will be sought at MCPE’S, Zonal and annual conferences.

Particular care will be taken to ensure that ICAN MEMBERS from the various ethnic and

interest groups are covered in the sample. As Abuja has become the melting point of

Nigeria’s ethnic groups, the researcher will, among others, sample the opinion of ICAN

MEMBERS gathering in Abuja either for MCPE or Annual Conference. The study is

being carried out in 2008.

In a research work of this nature difficulties are bound to be encountered. There

was paucity of local literature as the researcher was threading on an area that has not been

over flogged. Finance constituted another problem limiting the ability of the researcher to

travel more extensively in search of relevant data and opinion. Some ICAN MEMBERS

filled the questionnaires in a hurry, because of their busy schedules, thus affecting the

xix

quality of their answers. Time was of the essence in this research and this also affected

the researcher.

On the whole, however, the researcher was still able to use his wealth of experience

to navigate successfully through the difficulties and produce a work that will stand the

test of time.

1.7 SIGNIFICANCE OF THE STUDY.

The problem of audit failures globally had tended to exacerbate the problem of

audit expectation gap. As a result the search for a solution has become frenetic. ICAN

MEMBERS, especially as auditors, stand at the centre of this effort at a panacea.

Chronicling the perception of ICAN MEMBERS in Nigeria as to some of the

methods/suggestions on offer for bridging the gap will have the following significance

among others, the Institute of Chartered Accountants of Nigeria will benefit immensely

from this work as the perception of the rank and file of the Institute about bridging the

gap will be documented. The management and members of the Institute can then speak

with one voice in any future negotiations aimed at bridging the audit expectation gap.

Members of the public will be better informed on this enigmatic subject. Government of

Nigeria will be better placed to articulate its own strategy, as the regulatory stakeholder

group, in any discourse on this subject matter. This will apply with equal force to the

investing public. Academics will also have a field day as this work will open a floodgate

for further researches on other aspects of this all important subject matter as it affects

Nigeria. Finally, the International community will have the benefit of Nigeria’s

experience as the global search for solution to the audit expectation gap cankerworm

gathers momentum.

xx

1.8 DEFINITION OF TERMS

The following operational terms germane to this study are hereby defined:

(1) The Institute of Chartered Accountants of Nigeria: The first professional

accountancy body in Nigeria chartered by an Act of Parliament in 1965 and

charged with regulating the practice of Accountancy profession in Nigeria.

(2) ICAN MEMBERS: These are members of the Institute of Chartered Accountants

of Nigeria.

(3) Rival Accountancy Professionals in Nigeria: These are members of other

Accountancy bodies in Nigeria notably members of The Association of National

Accountants of Nigeria.

(4) MCPE: Mandatory Continuing professional Education whereby members of the

Institute of Chartered Accountants of Nigeria are compulsorily required to attend

professional seminars in order to keep abreast of developments in Accountancy

profession

(5) ICAN Disciplinary Tribunal: A quasi judicial body charged with trying erring

members of the Institute of Chartered Accountants of Nigeria.

xxi

REFERENCES

Egbiki, H (2006), “Whistle Blowing Culture Imperative for Anti-Corruption

Crusade” The Guardian, 17 July, pp. 56-57

Okafor, G.O and S.C. Okaro (2009), “Stemming the Tide of Audit Failures

in Nigeria”, ICAN STUDENTS’ JOURNAL, 13(1):11-17

.

xxii

CHAPTER TWO

2.0 REVIEW OF RELATED LITERATURE AND THEORETICAL

FRAMEWORK

2.1 THE NATURE AND DIMENSIONS OF THE AUDIT EXPECTATION GAP

PROBLEM

Audit expectation gap is the gap between the role of an auditor as perceived by

the auditor and the expectations of users of financial statements. It is a gap between what

the auditor is doing and what the society expects him to do creating the impression that

the statutory objective of audit is not responsive to the social needs of the populace. The

problem of expectation gap is dual: communication gap and the performance gap.

2.2 COMMUNICATION GAP

One survey 0f users’ expectation worldwide revealed the following:

a) Going Concern:

Users of Financial statements believe that auditors should comment on the going

concern assumptions in the financial statements.

b) Fraud and Illegal Acts:

Users expect an unqualified opinion to assure them that no fraud or illegal acts

have taken place.

c) Warning of impending collapse:

Users expect an unqualified opinion to guarantee that a business will not fail, at

least, in the short run.

d) Accuracy:

Users expect financial statements to be accurate.

xxiii

e) Management Performance

Many users would like to see the auditor express an opinion on both the

performances of the company and management.

f) Independence

g) Users demand that the auditor remains objective and independent of management.

h) Duty of Care

Users believe that the auditor has a duty of care to any one who relies upon his

opinion.

Communication gap persists partly because most users cannot come to terms with

the legally defined status of an audit. Another reason is that users are a motley crowd

with differing expectations about what an audit should accomplish.

2.3 PERFORMANCE GAP.

Performance gap occurs when public expectations are reasonable but the auditor’s

performance does not fulfill them. That means that there is a short fall in the auditor’s

performance. An audit has been defined as an independent examination of financial

statements of enterprises where such an examination is conducted with a view to

expressing an opinion on whether those statements give a true and fair view. An audit, it

was posited, had the primary purpose of enabling an auditor form an opinion as to the

truth and fairness of financial statements presented to him by his client’s management

and to report accordingly. Other incidental objectives of an audit include;

i The detection of errors and frauds through the moral effect of regular audit visits

upon the conduct of the client staff. Each time an auditor used the term “true and

fair view” in his report, he is saying;

ii As to his examination, that independence is unquestionable; no limitation has

reduced the scope of his audit below the level considered minimal, all records

xxiv

required by him were made available to and utilized by him, and he had exercised

every professional care and skill throughout his examination.

iii As to the client’s internal control and accounting methods, that they are adequate,

accounting principles and procedures have been found acceptable, accounting

policies and their application have been consistent, and the books of account have

been brought into agreement with the financial statements;

iv As to the financial statements and appended notes that proper terminology had

been employed, the statements are comparable in form and content with those of

similar organizations, all major post-balance sheet events and unusual large-scale

transactions are disclosed, no misstatement or misrepresentation is reflected in the

statement, all facts and conditions are included without which the statement might

be interpreted as misleading, and any material departure from accepted

accounting principles is identified in the auditor’s report.

v. As to statutory requirement, that the financial statements conform to the

requirements of all existing statutes and regulations, and all disclosures required

by law are made (Osisioma, 2004: 40).

It has been suggested that given the rapid changes occurring in the business

environment and the increasing sophistication of the average consumer of financial

services that the subsisting audit performance has proved inadequate. It is also argued

that the rise of consumerism demand that audit procedures be reviewed to make it more

responsive to the needs of the multiplicity of users of financial statements .This has to do

with audit objectivity and effectiveness. It has also been suggested that the auditor can no

longer hide behind professional excuses to cover their inefficiencies.

xxv

2.4 CAUSES OF PERFORMANCE GAP OR AUDIT FAILURES.

Audit failure or ineffectiveness can arise as a result of many factors. These include;

i Lack of independence and objectivity on the part of the auditor and ethical failure.

ii Negligence in carrying out the audit process and

iii Environmental/cultural influences.

At the root of an audit engagement is the independence of the auditor. Lack of

independence on the part of the auditor will colour his objectivity and cast aspersions on

the credibility of his audited financial statements. The company and allied matters Act of

1990 recognised this and made elaborate arrangements to ensure the independence of the

auditor. Such arrangements are covered in sections 357, 262 and 363 of the Act. Ethics

has been defined as the study of moral judgment and standards of conduct. It is suggested

that ethical framework should be defined by five fundamental principles of integrity,

objectivity, professional competence and due care, confidentiality and professional

behaviour. The Institute of Chartered Accountants of Nigeria’s code for members

identifies certain situations that could result in ethical conflicts. These include:

i. Pressure from an overbearing supervisor, manager, director or partner.

ii. Pressures to act contrary to technical and/or professional standards.

iii. Divided loyalty as, for example, between the member’s superior and the required

professional standard.

iv. Publication of misleading information advantageous to the client but not to the

auditor.

Opinions seem to suggest that Nigerian auditors may not be truly independent. It

has been suggested that some auditors are unable to distance themselves from

overbearing board or management so as not to incur their wrath and put their appointment

at risk (Onosode, 2001:7). Another reason adduced for apparent lack of independence of

xxvi

the Nigerian auditor is that an unsatisfied Board will always find a way of effecting the

removal of the auditor at the annual general meeting, the provisions of CAMA

notwithstanding. It has also been said that the Nigerian auditor is not psychologically free

as a result of the fact that the distinction between shareholders and management has

become so often blurred that the appointment, remuneration and dismissal of auditors are

effectively decided by management, who are the very people auditors may wish to

criticize in the course of their duties .The pervasive atmosphere of fraud and dishonesty

in Nigeria has no doubt taken its tool on audit effectiveness. The Nigerian culture doesn’t

seem to encourage efficient management of public and private funds. In such situations it

is possible that some auditors may have compromised their positions. One opinion is that

audit failures are made in the board rooms of accountancy firms as audit work is

routinely falsified given time budget pressures (Mitchel, 2002:1). It has also been

suggested that the root cause of the global audit crisis is greed and weak moral fiber on

the part of some auditors. Many directors and other key staff may not always have been

transparent and honest in their dealing with auditors.

2.5 FRESH IMPETUS TO THE AUDIT EXPECTATION GAP PROBLEM.

A school of thought believes that audit failures are few in relation to the huge

number of audit opinions given across the world each year (Lerner, 2002:22). The

problem, however, is that such failure often does have disastrous consequences for many

stakeholders. Recent corporate failures/problems across the globe have again brought to

the fore the problem of audit expectation gap. The Enron, WorldCom, Global Crossing,

sunbeam and waste in the US are good examples. In the UK similar incidents like the

collapse of BCCI, Independent insurance and Equitable life, the Maxwell and Poly peck

affairs, stand in bold relief. In Germany Metal gessells shaft and over 700 American

companies have been forced to restate their accounts in four years. Back home in Nigeria,

xxvii

the massive collapse of banks in the 1990’s and early 2000’s, the overstatement of Lever

Brothers PLC profits by inflation of stock figures over some years and the failure of due

diligence search in AP PLC to uncover a debt of N20billion is still very fresh in our

minds.

In 2006, Cadbury plc confirmed “a significant and deliberate” overstatement of

the company’s financial position over a number of years which resulted in the company

posting a loss of over a billion Naira in its 2006 financials while at the same time making

a one-time exceptional charge in 2006 of over N13 billion in respect of the profit and

balance sheet overstatements. This considerably diminished the company’s reserves. SEC

has since waded into the saga revealing a classic case of audit failure. AWD, the auditors

of the company had been very much around for forty years. No doubt cozy relationship

may have crept in between the directors and the auditors. The auditors in this case also

acted as its reporting accountant in the rights issue of N5 billion. Some of the findings

and conclusions of SEC in respect of the auditors of Cadbury include;

i. A balance of N7.7 billion was credited to the company’s account in 2005 without

confirmation of the bank balances from any of the banks by the auditor.

ii. The auditors failed to follow up available leads which ought to put them on

enquiry in respect of the company’s accounts.

iii. The auditors sent management letters on the company’s 2001 to 2005 accounts

but failed or refused to note the lapses in the accounts when satisfactory response

was not forthcoming from the management of the company.

iv. The audit partner was negligent

The audit committee of the company, another corporate audit watchdog, was also

severely indicted.

xxviii

In such situations the question in the lips of the members of the public has always

been “where were the auditors”? This has greatly exacerbated the expectation gap

problem leading to fresh initiatives at finding a solution.

2.6 SOME CURRENT METHODS IN USE AIMED AT BRIDGING THE

AUDIT EXPECTATION GAP.

In the past and currently, the profession is using a lot of instruments of self-

regulation to ensure audit quality. These instruments include:

i. Peer review

ii. Rotation of auditors and concurring review

iii. Professional ethics and

iv. Continuing professional education

Peer review involves a review, every three years, of the work of one accounting

firm by another accounting firm of comparable size. The purpose of peer review is to

provide assurance to the public that a firm performing auditing and accounting services

has an effective quality control system that provides reasonable assurance that its auditors

are complying with statements of accounting standards. Peer reviews are aimed at

evaluating quality control by testing compliance of the firm’s auditing and accounting

engagements. Rotation of audit partners and concurring review by a fellow partner are

measures to improve the quality of services provided to clients. When an audit partner

has been in charge of an audit engagement for a period of five to seven consecutive years,

a new audit partner is assigned. The audit report and financial statement of public held

companies are also subject to concurring review by a partner other than the audit partner

in charge of the engagement.

Each professional accountancy body maintains a code of professional conduct

and, when appropriate, makes changes to the code. Any allegation against a member of

xxix

wrong doing is investigated by an investigating panel. Disciplinary action is visited on

any member found guilty .This include suspension or expulsion from the professional

body. Most professional accountancy bodies around the world require their members to

complete certain hours of continuing professional education annually. The idea is to

ensure that members maintain and even enhance their professional competence as well as

keep abreast with current developments. However, aspersions have been cast on the

ability of the accounting profession to effectively regulate its members on its own. For

example, there have been reports of attempts at voluntary peer review by local accounting

firms in Nigeria which came to grief as a result of intense competition among the firms

for client (Randle, 1998:19). There is also the believe that the profession has resisted

change in auditing for so long that it was unlikely to change of its own accord.

One method of bridging the audit expectation gap which has gained currency is

that of spelling out the respective responsibilities of the directors of a company and that

of its auditors in the preamble to the auditor’s report. Typically in such statements,

shareholders are reminded that the responsibility for preparation and fair presentation of

the financial statements including responsibility for designing, implementing and

maintaining internal control rests squarely with the directors. Auditors, on the other hand,

have the responsibility of expressing an opinion on the financial statements so produced

by the directors after performing procedures aimed at obtaining audit evidence about the

amounts and disclosures in the financial statements. Auditors also perform procedures

aimed at assessing the risks of material misstatement of the financial statements whether

due to fraud or error.

xxx

2.7 FRESH INITIATIVES/METHODS AIMED AT BRIDGING THE AUDIT

EXPECTATION GAP.

The following suggestions have been made recently by various stakeholders as a

fresh initiative to confront head long the expectation gap problem;

i. Encouragement of joint and cross audits.

ii. Introduction of mandatory rotation of auditors

iii. Establishment of Financial reporting council in conjunction with the Nigerian

accounting standards Board and in line with the World Bank model with strict

rules on auditing and accounting standards and monitoring and sanctions.

iv. Separation of audit relationship from provision of other services.

v. Appointment of a government oversight body to conduct inspection of registered

accounting firms on a continuous basis.

vi. Strengthening of the mandatory continuing professional educational

requirements of professional accountancy bodies.

vii. Involvement of audit committee, non- executive directors and institutional

shareholders in the appointment of external auditors.

viii. Encouraging other types of audit like forensic audit and revenue audit alongside

statutory audits.

ix. Widen legislation to penalize top company management that mislead their

auditors.

x. Encourage audit choice and competition.

xi. Encourage rotational audit whereby auditors would change after say (3) years

xii. Prohibition of audit staff from taking up employment with clients for a period of

not less than (3 years) after an audit-the so-called cooling off period.

xxxi

xiii. Composition of an active audit committee made up of non- executive directors and

knowledgeable in financial matters.

xiv. Strict enforcement of professional ethics by the institute

xv. Widen by legislation the statutory responsibilities of auditors to include detection

of material fraud.

xvi. Fuller disclosure of audit and consulting fees in the annual report and accounts.

xvii. Proceedings of ICAN investigating and disciplinary tribunal to be done in the full

glare of the media and the press.

xviii. The auditor’s report in addition to stating clearly the respective responsibilities of

directors and auditors in respect of the audited financial statements should refer to

the existence of a detailed management letter which could be referred to by users

of audited financial statements.

xix. Encouragement of shareholders to attend annual general meetings and ask

difficult questions. Amend the law to increase the period of notice for AGM’s to

35 days

xx. All recognized accounting bodies in Nigeria should team up to form a

professional monitoring body for the audit firms

xxi. Strengthen the work of the public practice section of ICAN.

xxii. Have a full time staff complement in the Institute charged with monitoring audit

firms and independent of the firms.

xxiii. Continued corporate advertisement by the Institute to enlighten the public about the

statutory duties of auditors.

xxiv. The new corporate governance code of SEC should have the force of law and be

vigorously enforced

xxv. Bar holding company auditors from auditing the subsidiary companies.

xxxii

xxvii. Encourage concurring review by partners independent of the engagement

partners.

xxviii. Introduce legislation compelling finance director and CEO’s of public companies

to certify the accuracy of financial statements produced by a company.

xxix. Encourage production of principle based accounting standards as opposed to rule

based ones.

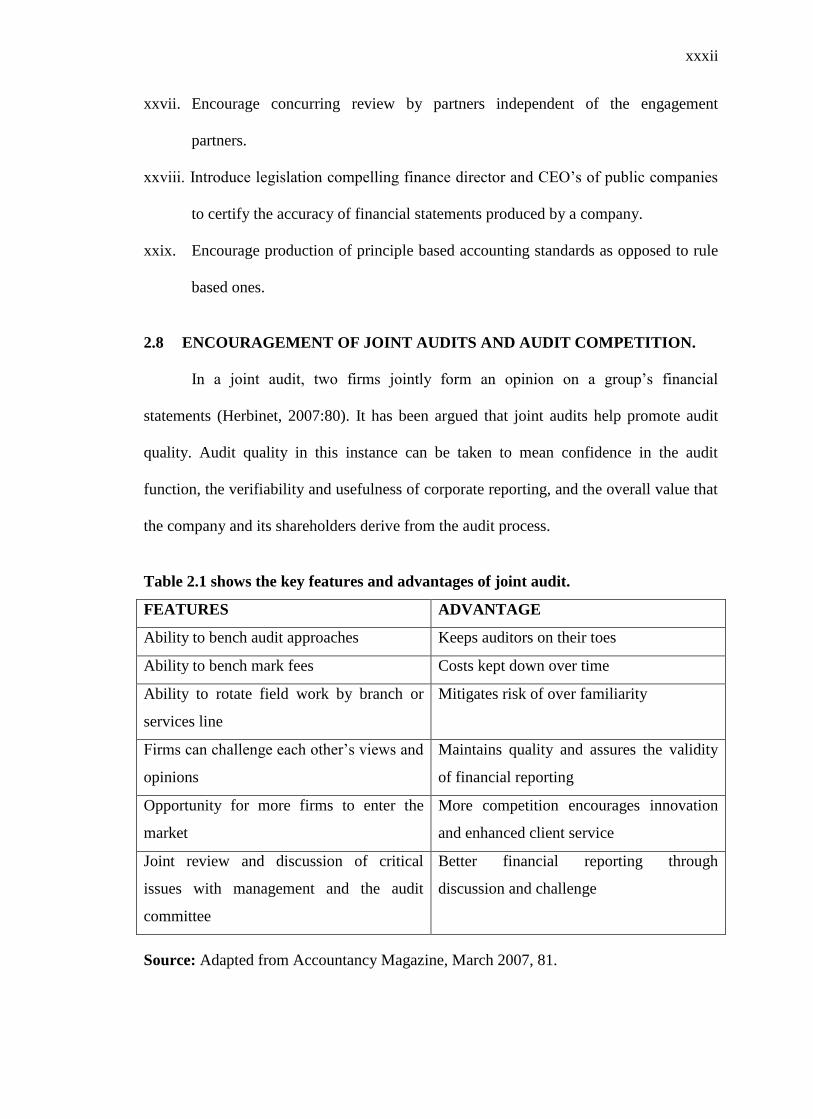

2.8 ENCOURAGEMENT OF JOINT AUDITS AND AUDIT COMPETITION.

In a joint audit, two firms jointly form an opinion on a group’s financial

statements (Herbinet, 2007:80). It has been argued that joint audits help promote audit

quality. Audit quality in this instance can be taken to mean confidence in the audit

function, the verifiability and usefulness of corporate reporting, and the overall value that

the company and its shareholders derive from the audit process.

Table 2.1 shows the key features and advantages of joint audit.

FEATURES ADVANTAGE

Ability to bench audit approaches Keeps auditors on their toes

Ability to bench mark fees Costs kept down over time

Ability to rotate field work by branch or

services line

Mitigates risk of over familiarity

Firms can challenge each other’s views and

opinions

Maintains quality and assures the validity

of financial reporting

Opportunity for more firms to enter the

market

More competition encourages innovation

and enhanced client service

Joint review and discussion of critical

issues with management and the audit

committee

Better financial reporting through

discussion and challenge

Source: Adapted from Accountancy Magazine, March 2007, 81.

xxxiii

However, joint audits are not without its critics. One argument is that it

significantly increases costs and time necessarily spent on coordination and discussions

by firms and company management. Others argue that joint audits are no longer

fashionable. The issue of greater audit choice in the accountancy market has also come to

the fore as the debate rages on how to ensure greater audit quality. It is clear that globally

and also in Nigeria, that only four firms dominate the accountancy market and thus limit

competition and choice. Solutions being touted to ameliorate the global phenomenon

include allowing external investment in and a change in the ownership structure of audit

firms as well as requirement for more information to shareholders regarding the

reselection of auditors. It is also suggested that audit firms should come within the ambit

of SEC code on corporate governance.

2.9 INTRODUCTION OF MANDATORY ROTATION OF AUDITORS.

Perhaps, the most controversial proposal on ameliorating the incidence of audit

failure in Nigeria is the issue of mandatory rotation of auditors on audit engagements.

Proponents of this line of thought believe that audit firms should be rotated, say every

three years. For example after auditing Cadbury Plc for three years, Akintola Williams

Delloitte should hand over to say Price Water House Coopers. The idea ensures that

employees of the client firm and the audit firm would not get too acquainted (Asein,

2007:20). This ensures that objectivity is maintained and the audit exercise will be

thorough as to be able to add credibility to the stewardship report of directors. It is argued

that mandatory rotation of audit firms would have some impact since a firm expecting to

be replaced in a year or two’s time will be very careful not to leave behind any

embarrassing compromises (Swinson, 2002:66). This observation accords with NDIC

observation that many Nigerian bank auditors qualified their reports only at the last audit

before they were replaced. Other arguments for rotation include;

xxxiv

a) It is inexpensive to implement compared with other quality control measures

b) It will result in a” periodic” fresh look at the institution from an audit perspective

to the benefit of investors and regulators.

The arguments against rotation include;

c) Choice of auditors should be on performance rather than on the need to satisfy a

legal requirement.

d) Loss of trust and confidence which rotation engenders.

e) Might result in increased cost of audit since adequate knowledge of a client’s

business will be sacrificed on the altar of rotation.

f) Paradoxically it might whittle down competition as the four big firms will have a

field day at the expense of smaller audit firms.

g) It will even have a negative impact on provision of non-audit services which are

often assigned as a result of the brand name of firms involved in the audit.

h) Frequent turnover of auditors may also have a negative impact on the long-term

corporate strategy of client companies because of its disruptive implications

i) Elsewhere in the European Union, many countries do not have mandatory

provision for the rotation of auditors.

j) There is no guarantee that weak auditors will still not make foolish decisions

k) It is not in accord with global best practice.

It is instructive that the famous Sarbanes-Oxley Act of 2002 in the US did not go

as far as providing for statutory rotation of auditors. It merely required that a study be

conducted in that regard. The Cadbury committee on corporate governance in the UK

was of the opinion that no compelling case was made for mandatory rotation of auditors.

In fact only 11 member countries in the EU have independent public oversight up and

running. Many countries that had such provision including Spain have since had a

xxxv

rethink. Italy maintains a requirement for mandatory rotation of audit firms. Italy is

however not regarded as a model for good corporate governance. In Japan recent reforms

now require auditors to rotate client teams every seven years, with a two-year interval

before they return. In Nigeria the battle line have been drawn between ICAN and CBN on

the issue (Okwe, 2006:17). CBN now requires mandatory rotation of financial institutions

auditors’ every five years. ICAN’S official position, as articulated by the then president

of the Institute, Mrs. G.O Okparaeke, is that mandatory rotation of auditors does not

accord with global best practice. Following the Cadbury scandal, SEC appears to be also

sold on the idea of mandatory rotation. In a move that signals a divided accounting

profession in Nigeria, ANAN president has fully endorsed the idea of mandatory rotation

of auditors arguing that it will prevent cover-up in the reporting of the financial position

of an organization under audit.

2.10 ESTABLISHMENT OF FINANCIAL REPORTING COUNCIL

A financial reporting council is being proposed for Nigeria .If given legislative

approval the proposed council will superintend over the affairs of government

companies/entities registered with the corporate affairs commission, and their external

auditors and audit firms. The activities of the council will affect the accountancy

profession and chartered accountants actively working as auditors or working for

registered company or a government .It will be the duty of the council to promote

auditing and accounting standards among other duties. Stringent penalties are provided

for in the bill proposing the establishment of the council targeted at professional

accountants who in the exercise of their audit functions run foul of the independence and

ethical code of the profession or manifest negligence. It is worthy of note that the World

Bank is behind the establishment of this council. Nigerian auditors may also not be able

to practice abroad if the establishment of the council fails to materialize in Nigeria.

xxxvi

2.11 COMPOSITION OF AN ACTIVE AUDIT COMMITTEE MADE UP OF

NON–EXECUTIVE DIRECTORS AND KNOWLEDGEABLE IN

FINANCIAL MATTERS

The history of Audit committees in Nigeria dates back to the Companies and

allied matters Act of 1990. The act provided for the establishment of an equal number of

directors and shareholders representing up to a maximum of six. An audit committee is

one of the major shareholders´ watchdogs in the area of corporate finances. Strong audit

committees acting as surrogate for investor interests provide a key check and balance in

the governance system. The following advantages have been claimed to accrue to a

public company that has an effective audit committee;

i. Further strengthening of the independence of the external auditor .

ii. Added credibility of audited financial statements

iii. Supplementary assurance that corporate policies are in the best interest of

shareholders and society at large.

iv. Improved performance of senior management

The effectiveness of the audit committees in Nigeria’s corporate governance

history is an empirical one. Egbiki (2006:56)believes that audit committees in Nigeria

still need a lot of mileage to move close to the global trend that have seen audit

committees in recent times becoming more and more accountable and responsible.

“These audit committees who are supposed to work with companies auditors to ensure

good corporate governance look the order way when abnormalities are discovered in

order to ensure that their god fathers are funded.

Perhaps, the most damning of all the indictments to date of corporate audit

committee effectiveness in Nigeria is that provided by SEC coming in the hills of the

xxxvii

recent financial impropriety in Cadbury. The committee acquiesced in the issue of a right

circular which contained untrue statements.

The committee failed and neglected to discharge their statutory responsibilities as

specified under section 359(4) and (6) of CAMA. The presence of non-executive

directors with relevant industry experience, who are able to scrutinize the accounts,

internal controls and auditors’ report with real understanding coupled with at least some

members with a sound grasp of current developments in financial matters have been

fingered as part of the qualities that make for an elite audit committee. It remains to be

seen whether the implementation of the above recommendation will yield the desired

result in the case of Nigeria.

2.12 SEPARATION OF AUDIT SERVICE FROM OTHER SERVICES

One proposal that has continued to recur in the debate on auditor’s independence is

that provision of audit service should be kept separate from provision of other consulting

services. The argument is that increasing dependence of auditors on consulting can result

in conflicts of interest and can thus colour the disinterestedness of the auditor in carrying

out his attest function. The auditor is not independent if he is auditing his own work. It is

also argued that concentration on audit practice by a firm will force it to create an

emphasis on quality and toughness. Another argument is that the rising importance of

consulting has contributed to a decline in auditor skepticism.

However, proponents of retention of the present arrangement whereby auditors can

freely provide advisory services in addition to the audit argue that;

i. It is cost advantageous for audit firms to provide other non-audit services.

ii. There is no hard evidence in support of the allegation that provision of non-audit

services impairs independence.

iii. Costly litigation is enough safeguard for audit failures.

xxxviii

iv. Current attitudes are in danger of banning appropriate work that the auditor is best

placed to perform and that can benefit the client enormously.

v. Audit is a loss leader and auditors only do it to get the lucrative non-audit work.

An independent report commissioned by ICAEW concluded that the profession

did indeed have a perception problem as regards whether provision of non-audit services

to audit clients did compromise the independence of the auditors. Clients were not

convinced that the provision of consultancy services does not provide a potential conflict

for audit firms. Suggestions aimed at ameliorating the problem of conflict of interest

which provision of non-audit services could engender include;

i. Outright ban on accounting firms offering consulting and other services to their

audit clients.

ii. Division of non-audit services into those which the auditor can combine without

compromising his independence and those to be avoided because of possible

compromise of his independence. The former category includes tax work,

designing of systems (including computer system). The later category includes

keeping the books and performing internal audit, tax advocacy, head hunting and

involvement with decisions about the future direction of the client’s business.

Thus it is argued that size of the fees involved should not be the basis of banning

non-audit work. The appropriate yardstick should be the nature of work.

iii. Active involvement of appropriately empowered audit committees as they are in

the best position to judge the real impact of non-audit services on auditor

independence in the particular circumstances of their businesses.

iv. Further disclosure of audit fees and fees from non-audit services.

The Sarbanes-Oxley Act specifies nine areas of non-audit advisory work that

audit practices governed by US law cannot now supply. In Europe, following on the hills

xxxix

of the Enron saga, an EU recommendation required more care in decisions about whether

to provide non-audit services to an audit client. The UK profession has since reacted

appropriately to the recommendation (Johnson, 2002:65). Audit firms across the globe

are also beginning to drive the change by incorporating their consulting arms as separate

independent limited liability companies.

2.13 PUNISH COMPANY MANAGEMENT WHO MISLEAD THEIR

AUDITORS.

The relationship of directors to the company is of a fiduciary nature and he is

bound to observe utmost good faith both in the transaction with the company or on the

company’s behalf. The fiduciary duty of the director is generally strict in order to prevent

the danger arising from the difficulty of disproving in particular cases that the duty has

been breached. The fact that the director’s action should not in anyway conflict with his

duties and interest in respect of the company is provided for statutorily in section 280 of

CAMA. However, conflict of interest appears to be the bane of many corporate boards in

Nigeria and elsewhere. It is reported that conflict of interest is rife in Nigeria’s corporate

governance firmament. In the wake of the bank distress saga of the 1990’s in Nigeria, it

became common knowledge that insider non-performing credits extended to directors

were largely responsible for the demise of many of the banks. Owoyemi (1998:46) has

accordingly bemoaned the lack of financial integrity rampant among the helmsmen in

Nigeria’s public and private sectors The Enron debacle in corporate America and the

financial impropriety that befell Cadbury in Nigeria were all largely attributed to criminal

breach of trust as a result of conflicts of interest involving their directors. Where such

conflicts arise auditors are the first to be hoodwinked by boards’ intent on cover-up.

According to Lerner (2002:22), a climate where directors act with responsibility and with

a spirit of openness and highest integrity when dealing with auditors may be one sure

xl

way of reducing the conflicts of interests between auditors and directors. The point has

well been made that in this increasingly complex world it is impossible for the auditors to

unearth problems if the management and board are intent on hiding them. Prescription of

stiff penalties for boards that mislead their auditors may well serve as a deterrent for

recalcitrant directors.

2.14 ESTABLISHMENT OF A GOVERNMENT OVERSIGHT BODY TO

REGULATE AUDIT PRACTICE

One fall out of the Enron debacle in the US was the enactment of the Sarbanes-

Oxley act of 2002 which effectively ended the self regulatory status of the accounting

profession in America. However, not many countries across the globe have emulated the

American example. In the EU, for example, only 11 countries have independent public

oversight body up and running. Traditionally, auditors and indeed all professionals have

prided themselves in their ability to rein in their erring members through the instruments

of self regulation. Arguments in favour of self regulation include;

i. Professionals know their stuff: educating outsiders to a level sufficient to second

guess the experts would take lot of time and money.

ii. There is also a kind of consensus that comes from self-interest. If a group of like

minded people develop and enforce their own rules, they are likely to believe in

them, which mean they will keep them in mind even when the door is closed.

Proponents of external interference in the affairs of the profession argue that;

i. The professions are invariably monopolies thus circumscribing the ability of

individual members to opt out and chose another regulator instead.

ii. Since there is little competition there is little or no incentive to drive up standards

other than the desire to escape further interference from government.

iii. Code of conduct is always liable to morph into trade union rule books.

xli

iv. Strengthens the power of auditors to reject questionable accounting treatments,

lest they draw the attention of the authorities.

One other argument against government regulation of the profession is that it

could result in regulatory “overkill”. The International Federation of Accountants is

indifferent as to whether the regulatory framework used is administered by the profession

or by government. It cautions, however, that regulators must have a clear, overarching

purpose and the ability to resist any move towards regulation that is self-interested or

motivated by special interest groups. To IFAC serving the public interest means having

regulations that achieve their aim of being effective and efficient without imposing

unnecessary costs. It advocates a cost-benefit approach to effective regulation that

protects the public interest.

The international organization of Securities Commissions (IOSCO) has developed

a series of principles for regulators. These principles hold that:

i. The responsibilities of the regulator should be clear and objectively stated;

ii. The regulator should be operationally independent and accountable in the exercise

of its functions and powers;

iii. The regulator should have adequate powers, proper resources and the capacity to

perform its functions and exercise its powers;

iv. The regulator should establish clear and consistent regulatory processes; and

v. The staff of the regulator should observe the highest professional standards,

including appropriate standards of confidentiality.

Preliminary findings of the public company accounting oversight board

(PCAOB), an authority established by the Sarbanes-Oxley act, revealed that of the 174

auditors inspected, almost half have been deemed to have some trouble doing their job

satisfactorily. However, on the downside many companies are already delisting from US

xlii

rather than conform to some of the complex provisions of the act. In Nigeria the recent

requirement by CBN for mandatory rotation of auditors of financial institutions

represents an attempt to keep the profession in tow from outside.

2.15 INTRODUCE FORENSIC AND VALUE FOR MONEY AUDITS.

Omoniyi (2004:43) believes that forensic accounting/auditing is a good hedge

against fraud. In a recent review of 40 failures that led to government enforcement

actions in the US, it was discovered that in a number of cases that the auditors did not

take the extra step that would have uncovered the problem. So the call is for introduction

of some forensic auditing techniques into the average audit. It has been suggested that

revenue recognition issues and the establishment of reserves should be zeroed in as they

are the most common reasons for earnings misstatements. Forensic auditing is already

gaining currency especially in developed countries. Percy (2007:28) identifies the

following skills as ones that will place the forensic auditor/accountant in good stead:

i. Ability to understand business practices very quickly;

ii. Good attention to details;

iii. Intuition;

iv. Confidence to convey complex transactions and analysis to the court as an expert

witness; and

v. Healthy dose of skepticism

The downside is, however, that forensic audits have a negative impact on audit

fees.

Allied to forensic audit is value for money audit which ensures economy and

efficiency in business management.

xliii

2.16 ENCOURAGE SHAREHOLDERS TO ATTEND ANNUAL GENERAL

MEETINGS AND ASK DIFFICULT QUESTIONS.

Shareholder activism is certainly a veritable tool of good corporate governance.

Unfortunately this culture is yet to take firm root in Nigeria’s corporate governance

firmament. The reasons are not far to seek:

i. Fragmented shareholding structures;

ii. Presence of self-seeking shareholders’ associations;

iii. Inactive Institutional investors;

iv. Illiterate individual investors; and

v. A macro environment that abhors rocking the boat.

Elsewhere, especially in the developed world, shareholder activism is lead by

institutional investors as they appear to be in the best position to safeguard small

investors’ interest and to enforce corporate discipline. Critics argue that shareholder

activism may not augur well for company management since shareholders usually have

no direct experience of running a company. The democratic mandate of Institutional

investors to hold brief for other investors has also come under attack.

2.17 BRIDGING THE AUDIT EXPECTATION GAP-THE PERCEPTION OF

ICAN MEMBERS-EXPERIENCE OF OTHER COUNTRIES

Surveys conducted worldwide revealed that users were firm in the belief that the

auditor should have a greater role in reducing the uncertainty associated with financial

statements .In Canada, Ireland, Scotland and England various researches were

commissioned on how to tackle the problem. The main conclusion emerging from the

researches was that users’ perceptions of the audit were flawed. A research report

sponsored by The Association of Chartered Certified Accountants (ACCA) of London

stated that the expectation gap problem can only be bridged as it cannot be eliminated.

From the viewpoint of this research an audit is a product of a continuous process of

xliv

renegotiation and is therefore changeable. Deriving from this work, the auditors preferred

meaning of what an audit is involves two factors as follows:

i. The experience of the auditor in undertaking audits over a period of time; and

ii. His interest

According to this research effort, the original purpose of an audit included

detection of fraud although along the line case law removed this responsibility from the

auditors. The following conclusion emanate from this study:

(1) No party or stakeholder group is in a position to fix the meaning of an audit and

so the expectation gap problem cannot be completely eliminated;

(2) The meaning of audit has to be constantly renegotiated as different groups want

different things from an audit;

(3) The auditor’s duty should be clearly defined by legislation;

(4) Accountancy profession has neither the democratic mandate nor the independence

to adjudicate among competing claims on audit policy;

(5) Auditors’ should have the duty to detect/report material fraud;

(6) To reduce or manage the expectation gap problem, it is vital that the various

parties affected by audits are brought together;

(7) Auditing standards should be set by a body independent of the profession.

In a related development, another ACCA sponsored research recommended the

following among others:

(1) A body independent of the accounting profession to regulate all aspects of

accounting and auditing;

(2) Firms should be prohibited from providing non-audit services to PLC audit

clients;

(3) Rotation of auditors should be made mandatory

(4) Auditors should have a statutory duty to detect and report fraud;

(5) There should be no capping of auditor’s liability;

xlv

(6) Government should take civil action against firms who are ultimately accused in

DTI inspectors report.

One fall out of this study was that the authors accused the profession of being

self-serving.

Following in the steps of ACCA, The Institute of Chartered Accountants in

England and Wales published its own sponsored research on Audit and Expectation Gap.

The report suggested a three point plan for the profession as follows:

i. The creation of an independent regulatory agency which would allocate auditors

to companies, determine their fees and oversee their work;

ii. The responsibilities of auditors should be widened (from equity shareholders) to

include potential shareholders and existing and potential creditors;

iii. Auditors should detect and report on material fraud.

Although similar, the reports have attracted mixed reactions. The ACCA has

dissociated itself from the more controversial aspects of the report. On its part, The

English Institute is not won by the argument for an independent regulator. It is even more

uneasy with proposals to off-load responsibility for detecting fraud unto auditors.

2.18 REVIEW OF RELATED LITERATURE AND THEORETICAL

FRAMEWORK- A SUMMARY.

Audit expectation gap has been defined as the gap between the role of an auditor

as perceived by the auditor and the expectations of users of financial statements. It is two

dimensional- communication gap and performance gap. Communication gap arises from

the inability of investors to accept the legal definition of an audit. Performance gap on the

other hand arises as a result of many factors including lack of independence, sheer greed

and hostile corporate and macro environment that constrain the work of the auditor.

Traditionally, accountants had experimented with many methods in a bid to bridge the

gap. Mandatory continuing professional education ensures that auditors keep abreast of

xlvi

developments and remain professionally competent. Corporate advertisements are

sponsored to educate investors on the limitations of the modern audit process and the

respective responsibilities of the auditor and the directors in respect of financial

statements. Others include rotation of audit partners’, strict enforcement of professional

ethics and arraigning of erring members before the ICAN disciplinary tribunal.

However, like a sore thumb the audit expectation gap have persisted. The matter

has been exacerbated by growing incidence of audit failure across the globe. This has led

to fresh suggestions aimed at bridging the gap. The suggestions on offer include

mandatory rotation of auditors, separation of audit relationships from provision of other

services and institution of self-regulation with teeth. There is also the suggestion that

convocation of all stake holders has become necessary to negotiate the audit process. In

the US the Enron saga resulted in the loss of independent status of the profession as an

external regulator now regulates the audit function. Many research efforts, especially in

the UK came to similar conclusions on the nature of the audit expectation gap problem

and the ways to ameliorate its effect. The profession in the UK has, however, distanced

itself from the more controversial aspects of the reports laying itself bare to allegations of

serving self interest.

In Nigeria, signals from the Institute of Chartered Accountants of Nigeria suggest

that it will prefer a self-regulatory regime to deal with the audit expectation gap problem.

The recent introduction of mandatory rotation of bank auditors had drawn the ire of the

Institute. Fragmented shareholding structure remains the norm in Nigeria with only few

institutional shareholders as players in the market. It will be interesting to find out what

the rank and file of The Institute of Chartered Accountants of Nigeria thinks about the

suggestions that have been made in recent times to bridge the audit expectation gap. This

is the thrust of this research work.

xlvii

REFERENCES

Asein, A. (2007), “Mandatory Rotation of External Auditors”, Nigerian

Accountant, 40(2):20-23

Egbiki, H. (2006), “Whistle Blowing Culture Imperative for Anti-corruption

crusade”, The Guardian, 17 July, pp. 56-57

Herbinet, D. (2007),” Two's Company”, Accountancy, 139(1363):80-81

Johnson, M. (2002), “No Room for Complacency”,

Accountancy, 130(1308):65

Mitchell, A. (2002), “Reform or Nemesis”, Accountancy, 129(1305):1

Okwe, M. (2006), “CBN, ICAN Disagree on New Audit Rules for Banks”,

The Guardian, 1 November, p.17

Omoniyi, S. (2004), “The Emerging Role of Forensic Accounting”,

Nigerian Accountant, 37(2):43-46

Onosode, G. O. (2001), “Conflict of Interest in Corporate Governance”,

Business Times, 3 December, p. 7

Osisioma, B. C. (2004), “Corporate Strategic Change in Nigeria: A search

for an Accounting Perspective”, paper presented at an inaugural lecture

at Nnamdi Azikiwe University, Awka, 19 May, p. 40

Owoyemi, L. (2003), “Bridging the Audit Expectation Gap”, The Guardian,

18 July, p. 46

Percy, S. (2007), “On Her Majesty's Secret Service”,

Accountancy, 139(1362):28-29

Randle, J. K. (1998), “Corporate Governance, the Practitioners'

Perspective”, The Guardian, 17 November, pp. 19-20

Swinson, C. (2002), “What does it Profit a Man----?” Accountancy,

130(1308): p.66

xlviii

CHAPTER THREE

3.0 RESEARCH METHODOLOGY

3.1 RESEARCH DESIGN

Research design is a blue print or scheme that is used by the researcher for

specific structure and strategy in investigating the relationships that exist among variables

of the study. Research design is the plan for a research project. It provides guidelines

which direct the researcher towards solving the research problem and it may vary

depending on the nature of the problem being studied. Also consideration regarding

limitations posed by time, money and availability of data is an important factor in

determining research design for a particular study.

Research design is a term used to describe a number of decisions which need to

be taken regarding the collection of data before ever the data are collected. In sum

designing a research means preparing a mental plan or scheme of attack for solving a

research problem in a systematic manner within the circumstances of the researcher.

The survey design approach is adopted in this work as opinion of sample ICAN

MEMBERS were elicited .This allowed for the collection of data in a more economical

way .The standardized data in the questionnaire allowed for easy comparison. The

approach was also basically cross- sectional as the opinions of ICAN MEMBERS in

Nigeria were elicited at one point in time. Nigeria has a burgeoning population of about

150 million people. The country comprises 36 states and a capital territory. Oil is the

largest revenue earner for the country while agriculture remains the major occupation of

the people.

xlix

3.2 NATURE AND SOURCES OF DATA.

This study drew its data from primary and secondary sources. The primary source

of data used was the questionnaire. Section A of the questionnaire elicited personal

information from the respondents. Section B listed 29 methods/suggestions aimed at

bridging the audit expectation gap. ICAN MEMBERS were asked to indicate their

preferences for the methods on a five point likert scale- strongly agree, agree, strongly

disagree, disagree and undecided.

Five further suggestions were articulated in the lower part of Section B of the

questionnaire and ICAN MEMBERS were once again asked to indicate their choice of

the suggestions using this time a three point likert scale of –Agree, disagree and

undecided. The last part of section B of the questionnaire was unstructured and asked

ICAN MEMBERS to make general comment on their individual perceptions of the

expectation gap problem. The face to face distribution method was used to get across the

questionnaire to the respondents. The study drew copiously from such secondary sources

as text books, journals, magazines and internet.

3.3 POPULATION AND SAMPLE SIZE

A population is made up of specific conceivable traits, events, elements, people,

subjects or observation, which relate to the situation of interest in the study to be

conducted. The full set of cases from which the sample is taken is called the population.

The population of this study is all ICAN MEMBERS in Nigeria as revealed by the

Institute of Chartered Accountants membership list as at 30 May, 2008, that is, 23,324.

ICAN MEMBERS are a homogenous group in terms of standards of skill as evidenced by

success in uniform qualifying examinations set and supervised by the Institute of

Chartered Accountants of Nigeria. ICAN MEMBERS work in diverse areas as

l

consulting, auditing, lecturing, financial reporting and tax services. The research was

carried out between March 2007 and September 2008.

Using Taro Yamani ’s formula to determine a sample from a population:

n = N/1+ (Ne2

)

Where n = sample size

N = Population size

e = error limit.

In this study an error limit of 10% was applied to have a manageable sample size.

The number of ICAN MEMBERS respondents was therefore gotten as follows:

N = 23324

n = ?

e = 0.10

23324/ 1+ (23324х 0.01)

= 23324/ 1+233.24= 23324/234.24 = 99.57 OR 100

However, the researcher distributed about 230 questionnaires, in an attempt to

ensure greater validity of the study and was able to collect back 162. This gave a

response rate of about 70.4%. This was considered high enough for this study. However,

3 of the questionnaires were rejected because they were not properly completed. Annual

conferences, zonal conferences and MCPE conferences are usually veritable

opportunities to target ICAN MEMBERS from all parts of the country irrespective of sex

and religious affiliation. For the purpose of this work, therefore, the researcher sampled

ICAN MEMBERS at the Abuja 2007 annual conference, Owerri 2nd Eastern Zonal

conference and Enugu MCPE 2008 seminar. In each case simple random sampling

technique was used to select the ICAN MEMBERS. The face to face method of

distribution of questionnaire was adopted .The researcher and six other ICAN

li