accounting for property according to ifrs different ...€¦ · different important valuation and...

TRANSCRIPT

Accounting for property according to IFRS

Different important valuation and accounting issues

Bo NordlundTechn dr Royal Inst of Technology,

StockholmAccounting and valuation specialist

Real Estate

EU – legislation: CompaniesListed on Stock Exchange within EU

Lisbon strategy dated 2000

At latest in 2005 listed companies within EU shall apply IAS/IFRS in

Consolidated Financial statements

Member states may require or admit application of IAS/IFRS by unlisted companies

IFRS standards interesting whenaccounting for property, for instance:

IAS 40 – Investment propertyIAS 16 – Property, Plant & EquipmentIAS 17 – LeasesIAS 18 – RevenueIAS 12 – Income TaxesIAS 1 – Presentation of Financial StatementsIAS 34 – Interim Financial ReportingIFRS 3 – Business CombinationsIFRS 5 – Non-current Assets Held for Sale and Discontinued OperationIFRS 8 – Operating SegmentsIAS 23 – Borrowing CostsIAS 39 – Financial InstrumentsEtc, etc

Property companies – very important to be aware of the importance of ”Net rental incom

Net rental income (NRI) is:Rental income less operating and maintenance costs

Often used when evaluating income return:NRI divided with carrying amount/fair value/market value

In many annual reports used to legitimate a fair value figure

The relevance of a historical acquisition cost dated 1968 of 1.000 SEK /sqmwhen the fair value of the same property was 20.000 SEK/sqm last year?

ACCOUNTING DEVELOPMENT

Anglo-saxon tradition: Principal-agencyStock market financing

Transparency

Anglo-saxon tradition: Principal-agencyStock market financing

Transparency Continental tradition:Strong connection accounting - taxationPrudence conceptBank- financingStakeholder model

For instanceGermanyFrance

For instanceUSAUK

Overview trends - developmentFinancial reporting – for instance:

Acquisition cost

Market value

Market value

Tax rulesinfluence

True and fair viewTrue and fair view

Accounting for external purposes–Different approaches

BALANCE SHEET APPROACH:Correct wealth

INCOME STATEMENT APPROACH:Correct income

In an IFRS context - Which meaning has:

PRUDENCE CONCEPT

REALISATION CONCEPT

MATCHING CONCEPT

ACCOUNTING-CULTURAL ORIENTATION"Long term or short term"

Other stakeholders:BanksPublic sectorEmployeesCustomersSuppliers

Other stakeholders:BanksPublic sectorEmployeesCustomersSuppliers

Provide users with information useful for decion-making in financial issues:Users primarily investors providing risk capital

Provide users with information useful for decion-making in financial issues:Users primarily investors providing risk capital

Anglo-saxonin many respects

Purpose of financial statements:Interpretation of IASB:s Framework

Connection to”investor theory”

Paragraph 37 in IASB:s Framework:

Qualitative characteristics – financial reporting:Reliabilily Relevance

Properties – different accounting models

Rörelsefastighet Förvaltningsfastighet

IAS 16 Property, Plant & Equipment IAS 40 Investment Property

"Revaluationmodel"

"Cost model" "Cost model" "Fair valuemodel"

Olika typer av fastigheter – olika regler

Rörelsefastigheter (oavsett modell) och förvaltningsfastigheterredovisade enligt ”cost model”– Strikt krav på komponentavskrivning !

Owner occupied property Investment property

Owner occupied properties (regardless chosen model)and investment property (cost model) – Depreciation shall

be based on a component approach

Investment propertyInvestment propertyDefinitionDefinition

Properties held with the purpose of generating rental income and/or value appreciation

Not properties held for purpose to be used in the production or supply of goods or services or administration purposes

Not properties held for the purpose of sale in the ordinary course of business

Investment property – what accounting model chosen

In Sweden all listed property companieshave chosen the ”fair value model”(there may be some exemption…)

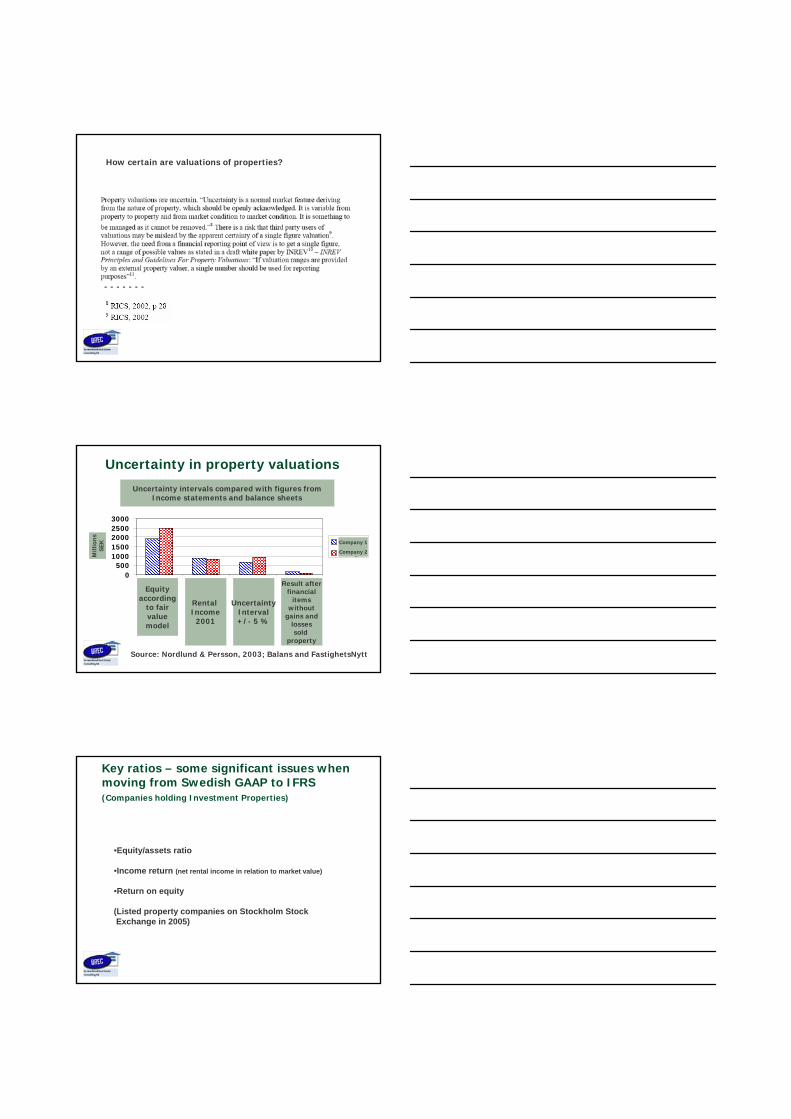

Investment property – what accounting model chosen

Source: Nordlund, B: Valuation and performance reporting inProperty Companies according to IFRS

- - - - - - -

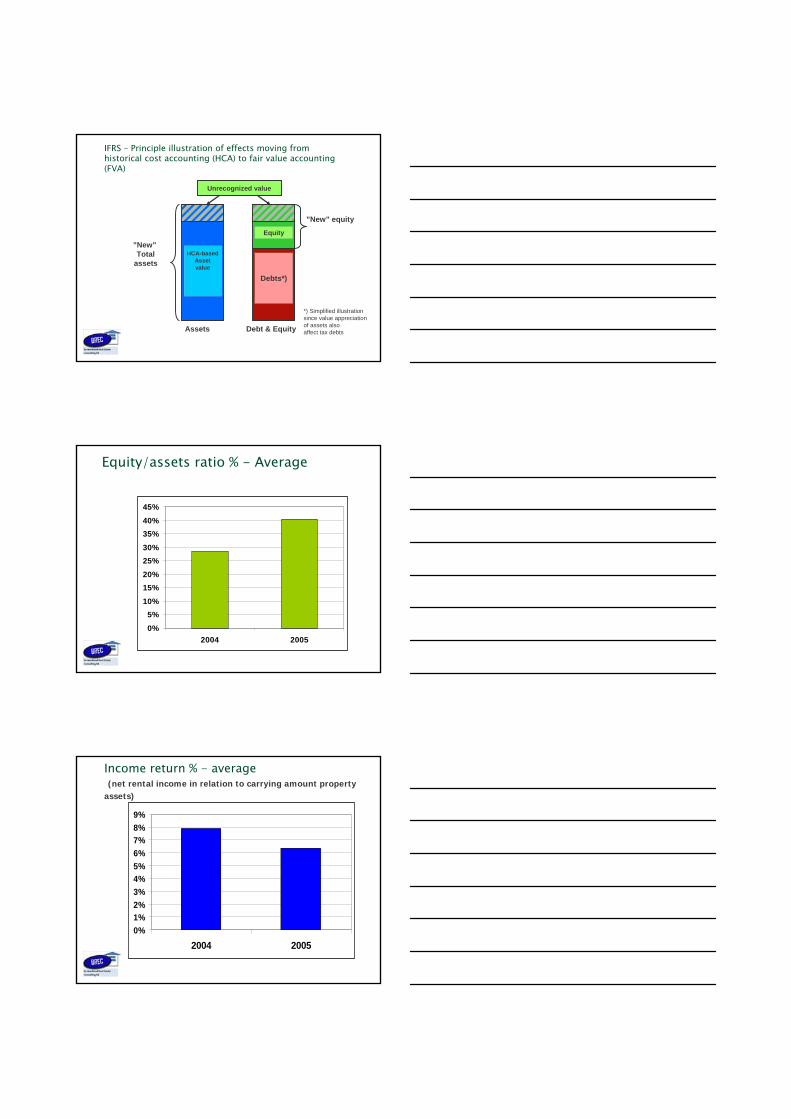

How certain are valuations of properties?

Uncertainty in property valuationsOsäkerhetsintervall i förhållande till resultat -

och balansmått

0500

10001500200025003000

Eget

kap

ital e

nlfa

ir va

lue

mod

el

Hyr

esin

täkt

er 2

001

Osä

kerh

etsi

nter

vall

MV

+/-5

%

Förv

altn

ings

resu

ltat

200

1

Mkr Bolag 1

Bolag 2

Source: Nordlund & Persson, 2003; Balans and FastighetsNytt

Uncertainty intervals compared with figures fromIncome statements and balance sheets

Equityaccording

to fairvaluemodel

Rental Income

2001

UncertaintyInterval+/- 5 %

Result afterfinancial

itemswithout

gains andlossessold

property

Company 1

Company 2Mill

ions

SEK

Key ratios – some significant issues when moving from Swedish GAAP to IFRS(Companies holding Investment Properties)

•Equity/assets ratio

•Income return (net rental income in relation to market value)

•Return on equity

(Listed property companies on Stockholm StockExchange in 2005)

IFRS – Principle illustration of effects moving from historical cost accounting (HCA) to fair value accounting (FVA)

Assets Debt & Equity

HCA-basedAssetvalue

Debts*)

Equity

Unrecognized value

”New”Total

assets

”New” equity

*) Simplified illustrationsince value appreciationof assets alsoaffect tax debts

Equity/assets ratio % - Average

0%

5%10%

15%20%

25%30%

35%40%

45%

2004 2005

Income return % - average (net rental income in relation to carrying amount property

assets)

0%1%2%3%4%5%6%7%8%9%

2004 2005

Return on equity % - Average(Net profit after tax divided with average equity)

0%

5%

10%

15%

20%

25%

30%

2004 2005Smaller equity butonly gains/loss on soldproperties affected thevisible return

Larger equity, butalso valuation gainsaffected the visiblereturn

IFRS – Accounting according to fair value model in IAS 40 some interesting issues (2005)

0%10%20%30%40%50%60%70%80%90%

1 2Fair value adjust-ments after tax, 28 %

divided with netprofit

Fair value adjust-ments divided

with rental income

Indication of total return 2005 Listed Swedish property companies(Net rental income + value appreciation divided with average fair value in the balance sheet)

Value appreciation7,4 %

Income return6,4 %

Total returnca 13,8 %

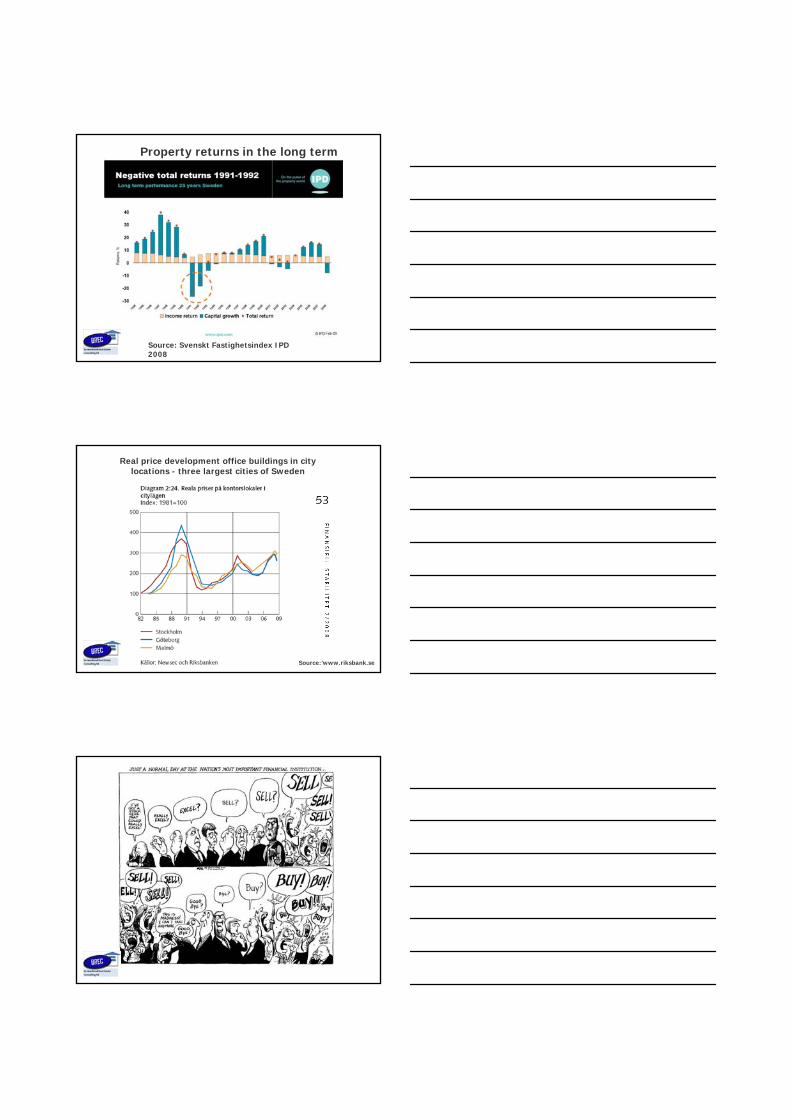

Property returns in the long term

Source: Svenskt Fastighetsindex IPD 2008

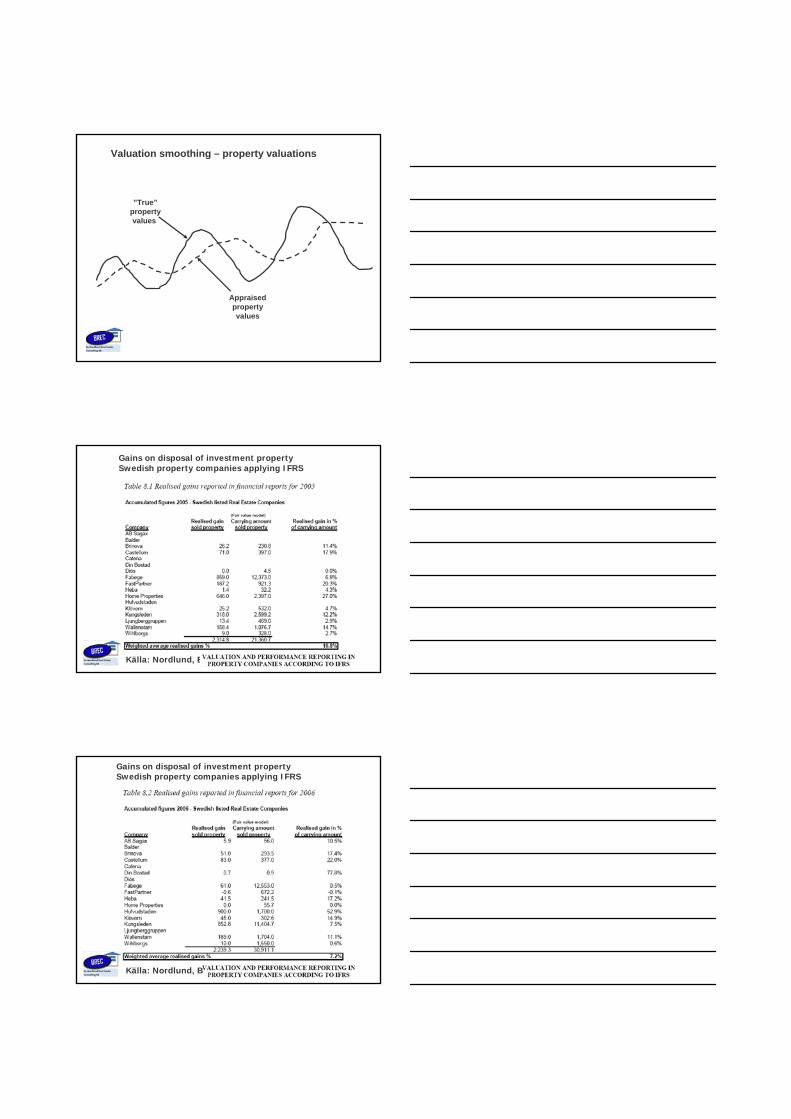

Source:’www.riksbank.se

Real price development office buildings in citylocations - three largest cities of Sweden

Valuation smoothing – property valuations

”True”propertyvalues

Appraisedpropertyvalues

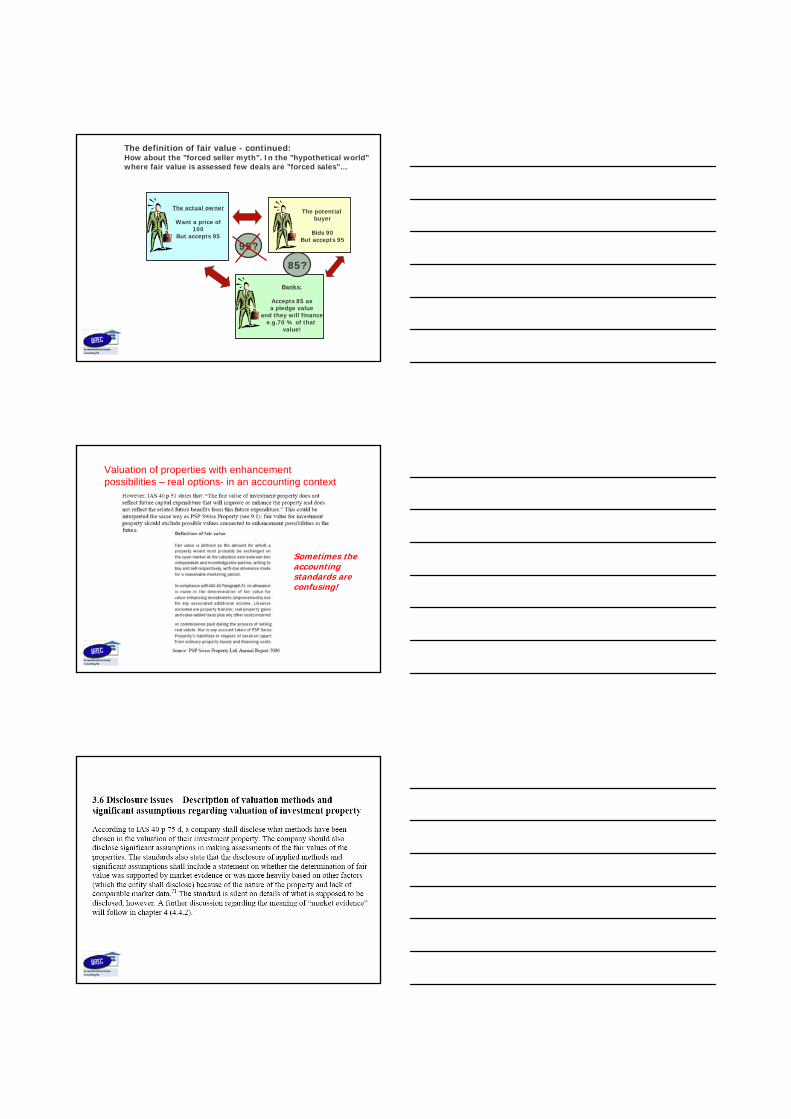

Gains on disposal of investment property Swedish property companies applying IFRS

Källa: Nordlund, B

Källa: Nordlund, B

Gains on disposal of investment property Swedish property companies applying IFRS

Valuation figure presented in theBalance sheet or in disclosures

-Relevant value concepts-Valuation methods-Disclosure connected to the valuation

Market value

Individual investment value

Fair value (E.g. IAS 40)Recoverable amount (IAS 36)Value in use (IAS 36)

Valuation of properties – Different value concept

-Production cost-Building cost

-Production cost-Building cost

”Long term sustainable

values”?????

”Long term sustainable

values”?????

IAS 40 Investment property

FAIR VALUEis the amount for which an asset could be exchanged between knowledgeable, willing parties in an arm’s length transaction (Source: IAS 40, paragraph 5)

FAIR VALUEis the amount for which an asset could be exchanged between knowledgeable, willing parties in an arm’s length transaction (Source: IAS 40, paragraph 5)

No deduction for sale-costs

Market value according to International Valuation Standards (IVS) – Used by property appraisers

Market value: ”The estimated amount for which a property should exchange on the date of valuation between a willing buyer and a willing seller in an arm’s-length transaction after proper marketing wherein the parties had each acted knowledgeably, prudently, and without compulsion.Property normally appraised from the view of ”highest and best use”: ”The most probable use of a property which is physically possible, appropriately justified, legally permissible, financially feasible, and which results in the highest value of the property being valued.”

IASB:s ED ”Fair Value Measurement”

What is meant by a fair value?Entry price or Exit price approach?

Entry price is the acquisition cost –founded on the buyers individual investment value (What info do we have of market prices? Risk of ending up in ”winners curse”?)

Exit price the amount that will be received when selling the asset…

On many occasions entry and exit price could be the same amount but we cannot be sure of that…

39

The definition of fair value:

The willing selleris a

hypotheticseller!

Willing to sell at

the best price obtainable in the light of

current market

conditions

Investors/creditors:”could be

exchanged” in the definitionmeans their

opinion must be weighted!

The willing buyer is prepared to

pay what’sdemanded in the market

Note! ”The factualcircumstances of the actual

investment property owner are not a part of this consideration.”

FAIR VALUEis the amount for which an asset could be exchanged between knowledgeable, willing parties in an arm’s length transaction (Source: IAS 40, paragraph 5)

40

The definition of fair value - continued:How about the ”forced seller myth”. In the ”hypothetical world”where fair value is assessed few deals are ”forced sales”…

The actual owner

Want a price of 100

But accepts 95

Banks:

Accepts 85 asa pledge value

and they will financee.g.70 % of that

value!

The potential buyer

Bids 90But accepts 95

95?

85?

Valuation of properties with enhancementpossibilities – real options- in an accounting context

Sometimes the accountingstandards areconfusing!

Valuation methods according to IAS 40

”Incomeapproach”

Comparablesales

(”marketapproach”)

Property valuation – different methods:

Comparable sales method: Area method Gross Income Multiplier methodMethod based on Net capitalization factor

Income approach:Direct capitalization method (same as Net capitalization above?)Discounted Cash flow method

Cost based methods:E.g. production costs, depreciated replacement cost

Problems finding Comparable sales:

-Indirect acquisitions-Special terms:

-Financing-Rental guarantees

-etc

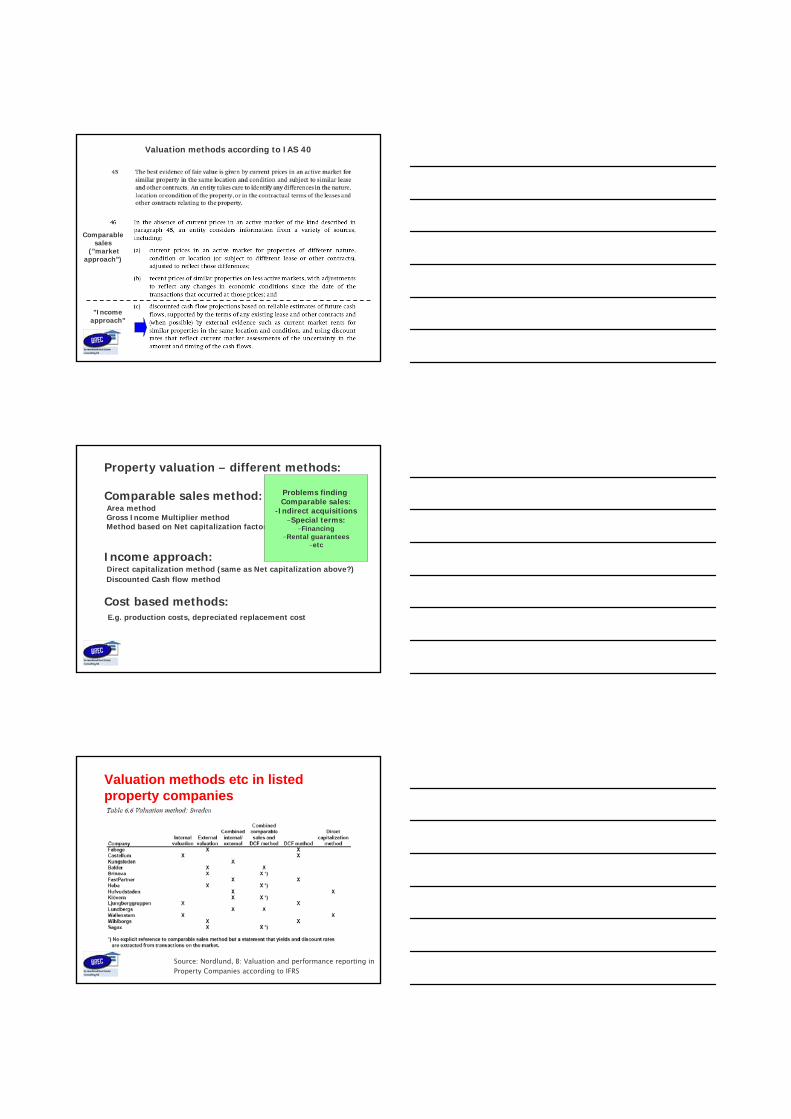

Valuation methods etc in listedproperty companies

Source: Nordlund, B: Valuation and performance reporting inProperty Companies according to IFRS

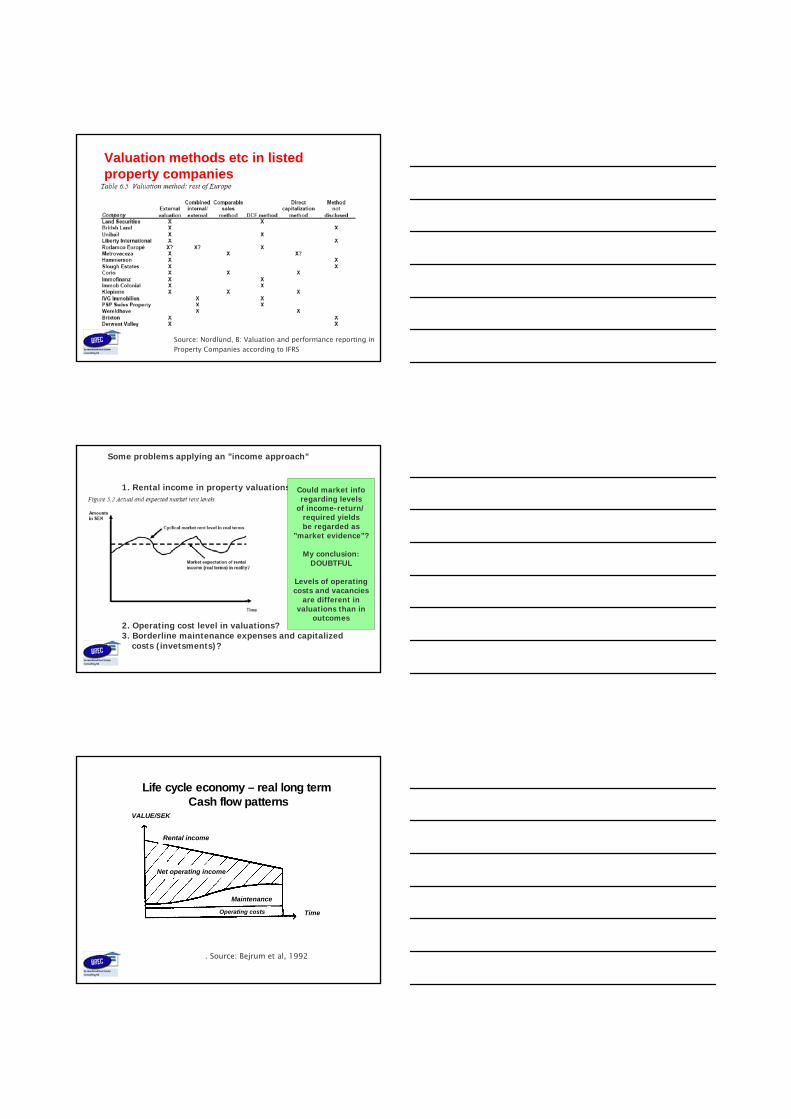

Valuation methods etc in listedproperty companies

Source: Nordlund, B: Valuation and performance reporting inProperty Companies according to IFRS

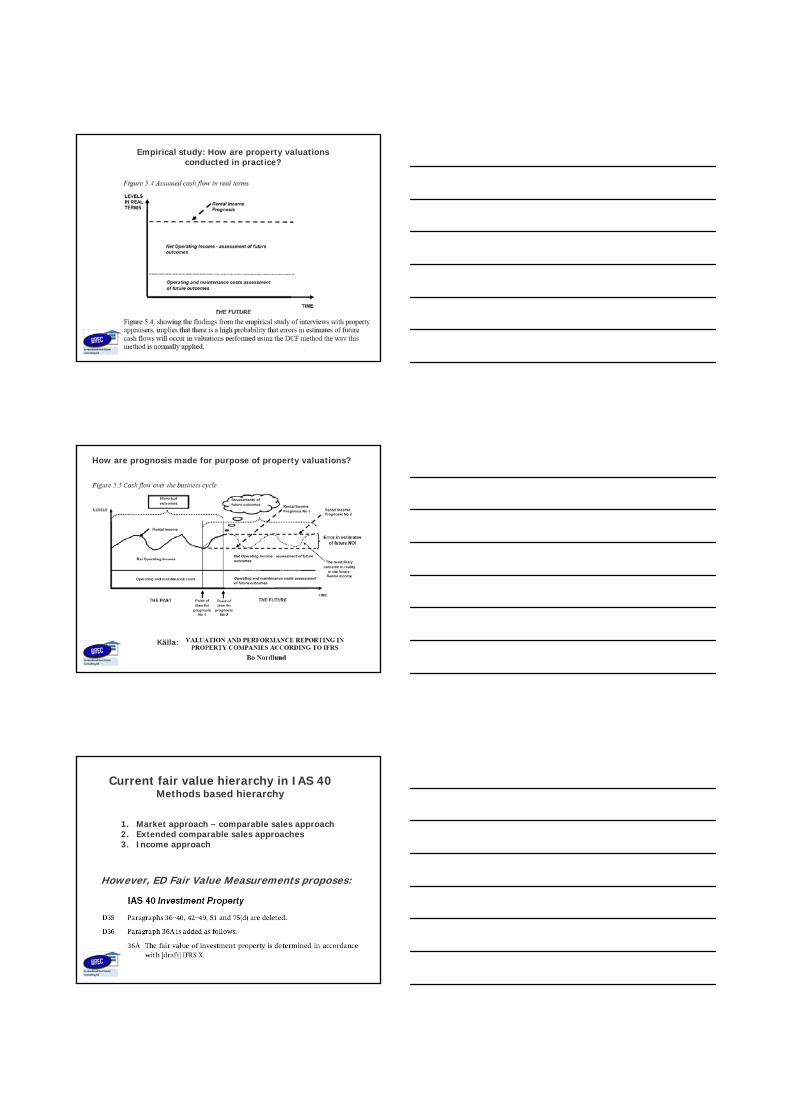

1. Rental income in property valuations:

2. Operating cost level in valuations?3. Borderline maintenance expenses and capitalized

costs (invetsments)?

Some problems applying an ”income approach”

Could market inforegarding levels

of income-return/required yieldsbe regarded as

”market evidence”?

My conclusion:DOUBTFUL

Levels of operatingcosts and vacancies

are different invaluations than in

outcomes

Life cycle economy – real long term Cash flowpatterns

VALUE/SEK

Rental income

Net operating income

Maintenance

Operating costs Time

. Source: Bejrum et al, 1992

Empirical study: How are property valuations conducted in practice?

Källa:

How are prognosis made for purpose of property valuations?

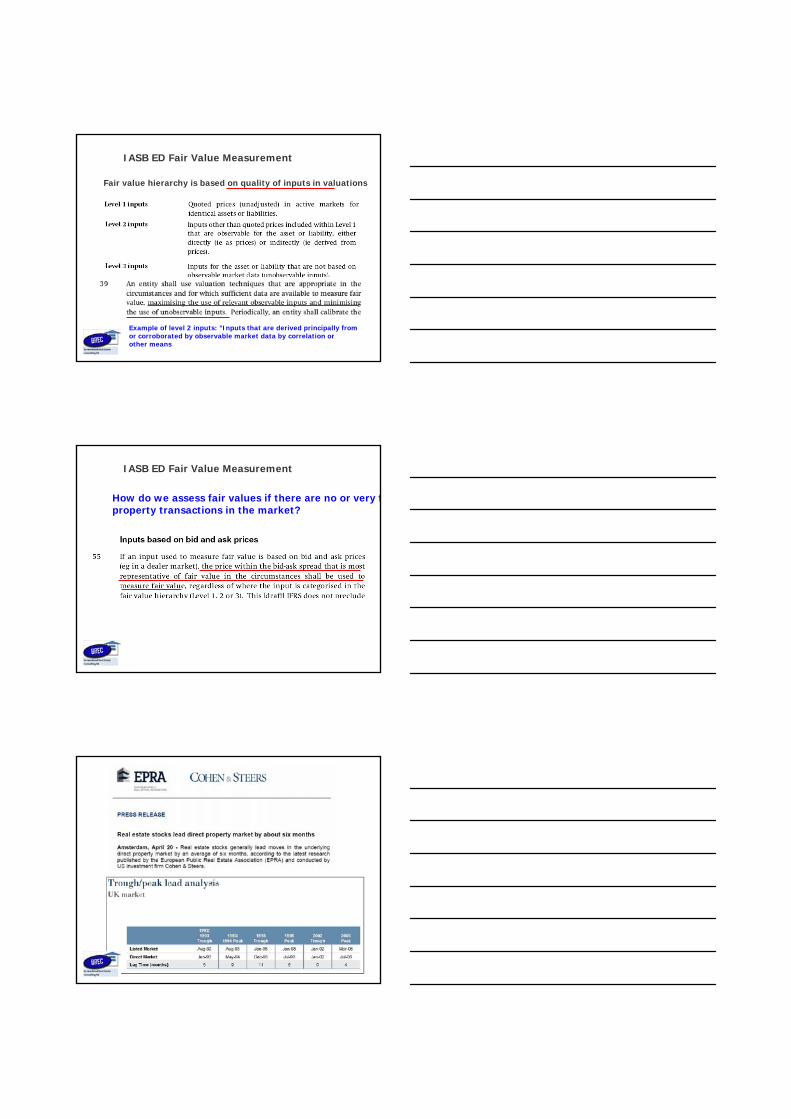

Current fair value hierarchy in IAS 40Methods based hierarchy

1. Market approach – comparable sales approach2. Extended comparable sales approaches3. Income approach

However, ED Fair Value Measurements proposes:

IASB ED Fair Value Measurement

…

Fair value hierarchy is based on quality of inputs in valuations

Example of level 2 inputs: ”Inputs that are derived principally fromor corroborated by observable market data by correlation orother means

IASB ED Fair Value Measurement

How do we assess fair values if there are no or very fproperty transactions in the market?

.

Source:

Information from stock market with reference to share Information from stock market with reference to share price/market capitalization: Case 1 price/market capitalization: Case 1 –– Discount to net asset Discount to net asset valuevalue

Börsvärde

Verkligt

värde

fastigheter Skulder

Discount

Fair valueof assets

Marketcapitalization

Fair valueof debts

Börsvärde

Verkligt

värde

fastigheter Skulder

Premium

Information from stock market with reference to share Information from stock market with reference to share price/market capitalization: Case 2 price/market capitalization: Case 2 –– Premium to net asset Premium to net asset valuevalue

Fair valueof assets

Marketcapitalization

Fair valueof debts

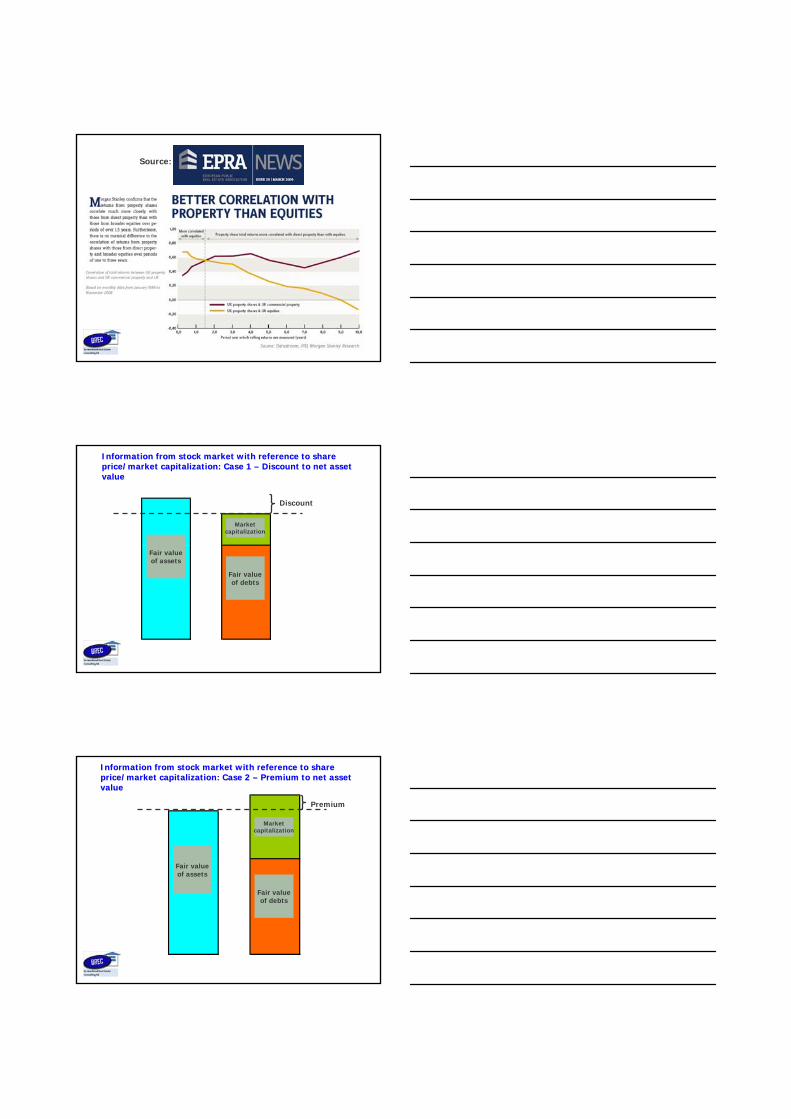

Implicit value of properties as extracted fromlisted property company shares

Balance sheetAssetsEquity &Liabilities

1.Market value of

equity

2.Market value

liabilities

3.Market value of other

assets

4.Implicit value of

properties

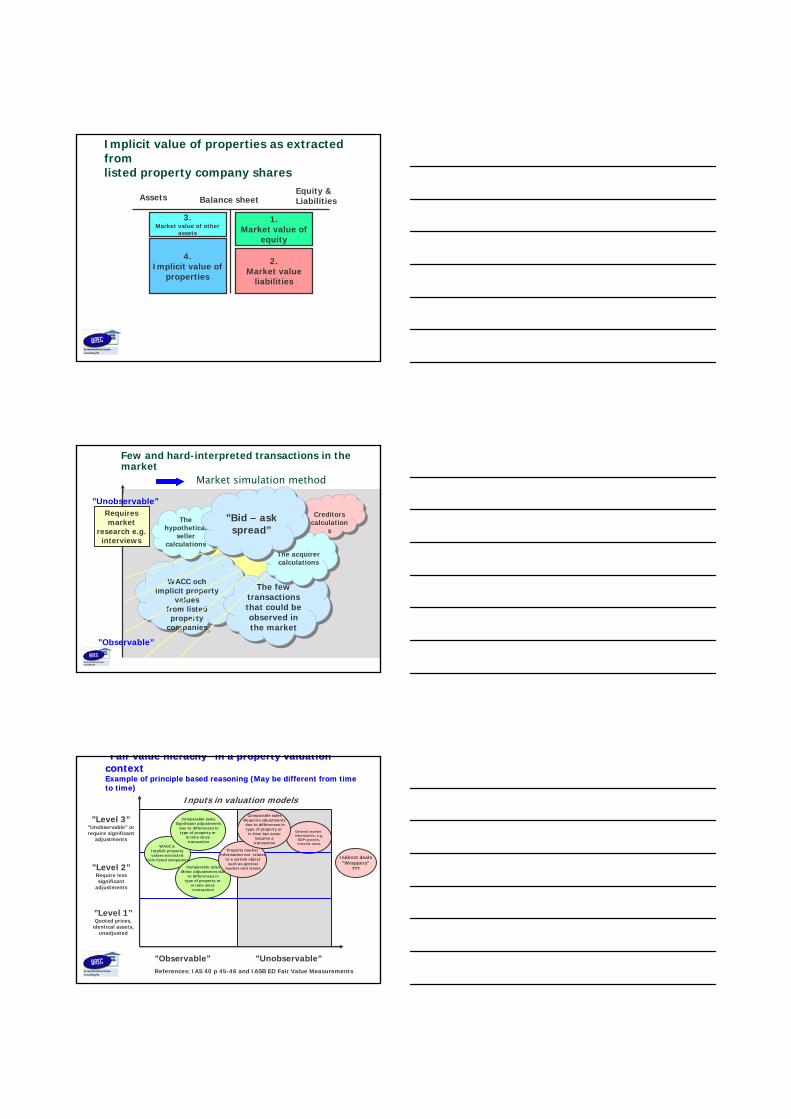

Few and hard-interpreted transactions in the market

Market simulation method

WACC och implicit property

valuesfrom listed property

companies

WACC och implicit property

valuesfrom listed property

companies

The few transactions that could be observed in the market

The few transactions that could be observed in the market

The hypothetical

seller calculations

The hypothetical

seller calculations

Creditors calculation

s

Creditors calculation

s

The acquirer calculations

The acquirer calculations

”Bid – ask spread”

”Bid – ask spread”

”Unobservable”

”Observable”

Requiresmarket

research e.g.interviews

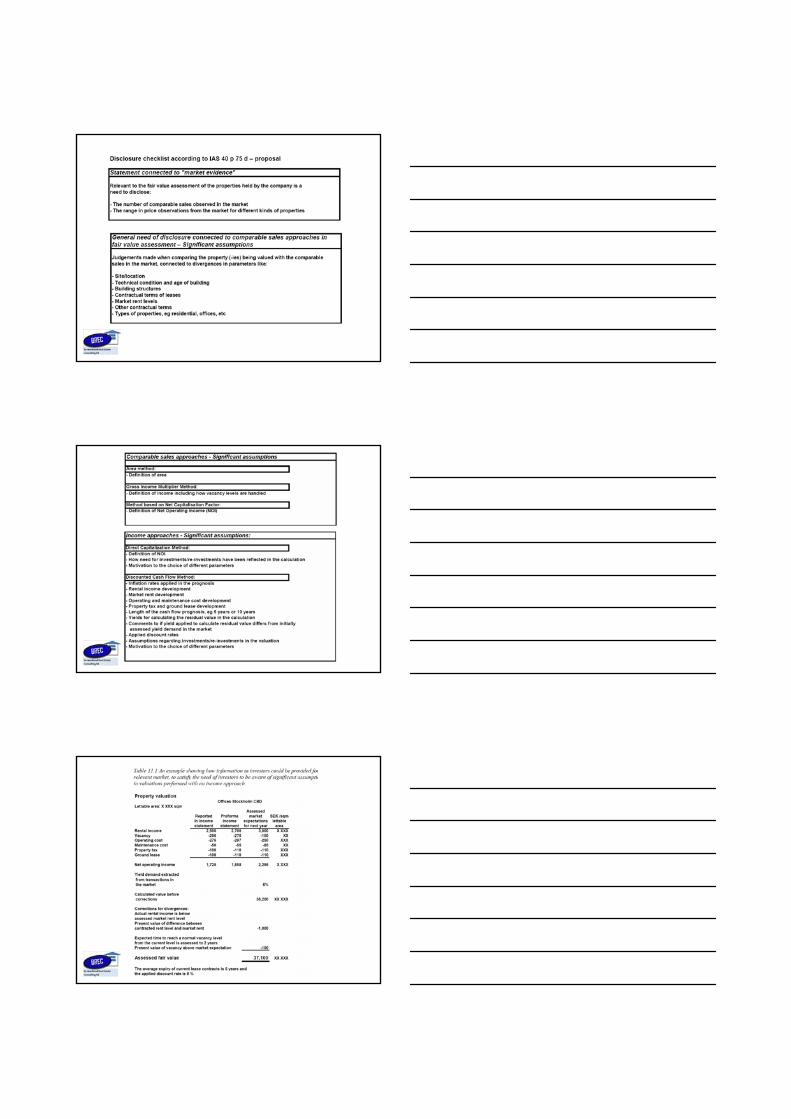

Fair value hierachyFair value hierachy in a property valuation in a property valuation contextcontextExample of principle based reasoning (May be different from timeExample of principle based reasoning (May be different from timeto time)to time)

”Level 1”Quoted prices,

identical assets,unadjusted

”Level 2”Require lesssignificant

adjustments

”Observable” ”Unobservable”

”Level 3””Unobservable” orrequire significant

adjustments

References: IAS 40 p 45-46 and IASB ED Fair Value Measurements

General market information, e.g.

GDP-growth,interest rates

WACC &Implicit propertyvalues extracted

from listed companies

Comparable salesMinor adjustments due

to differences intype of property or

in time since transaction

Property market Information not related

to a certain objectsuch as general

market rent levels

Comparable salesRequires adjustmentsdue to differences intype of property or in time but never

became atransaction

Comparable salesSignificant adjustments

due to differences intype of property or

in time since transaction

Inputs in valuation models

Indirect deals”Wrappers”

???

Items affecting Net Rental Income (Income statement)

-Rental income-Borderline between maintenance expenses andcapitalized costs (investments)

Rental income – accounting rules: Applying IAS 17 Leases

For example:Rent discountYear 1

Source:’www.riksbank.se

Real price development office rents in citylocations - Stockholm Sweden

Rents

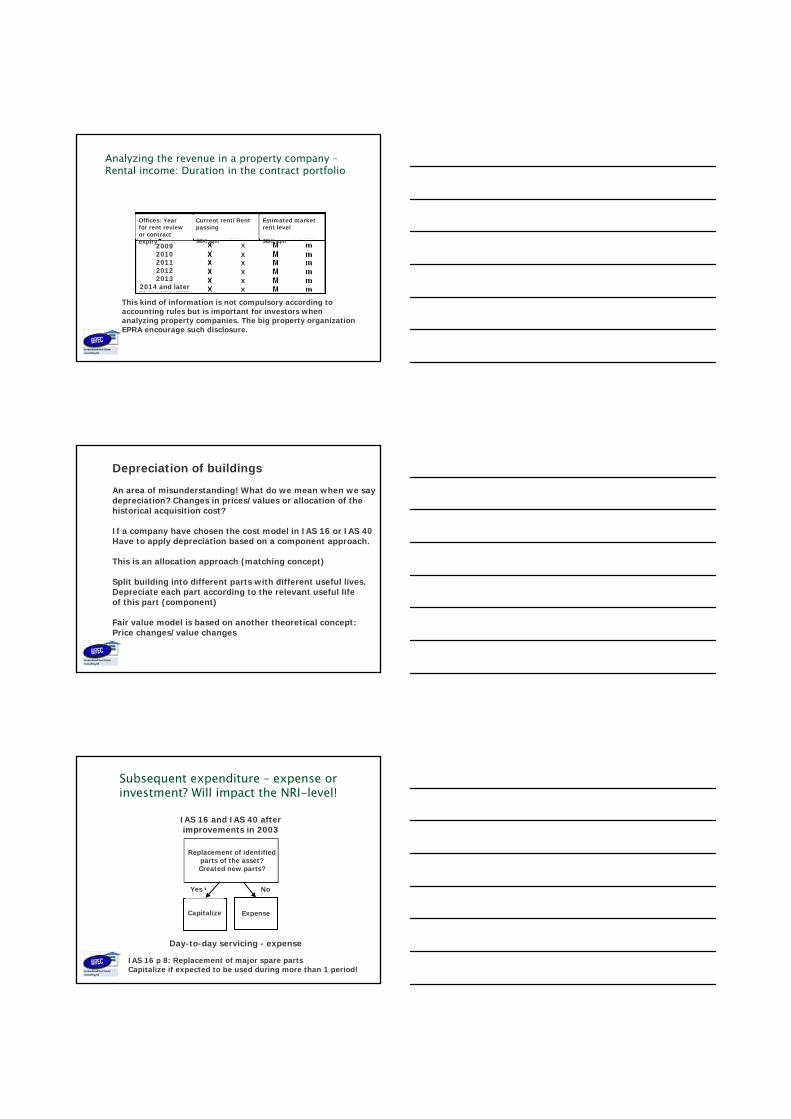

Analyzing the revenue in a property company –Rental income: Duration in the contract portfolio

20092010201120122013

2014 and later

Offices: Year for rent review or contract expiry

Current rent/Rent passing

SEK/sqm

Estimated market rent level

SEK/sqm

This kind of information is not compulsory according to accounting rules but is important for investors when analyzing property companies. The big property organizationEPRA encourage such disclosure.

Depreciation of buildings

An area of misunderstanding! What do we mean when we say depreciation? Changes in prices/values or allocation of the historical acquisition cost?

If a company have chosen the cost model in IAS 16 or IAS 40Have to apply depreciation based on a component approach.

This is an allocation approach (matching concept)

Split building into different parts with different useful lives.Depreciate each part according to the relevant useful lifeof this part (component)

Fair value model is based on another theoretical concept:Price changes/value changes

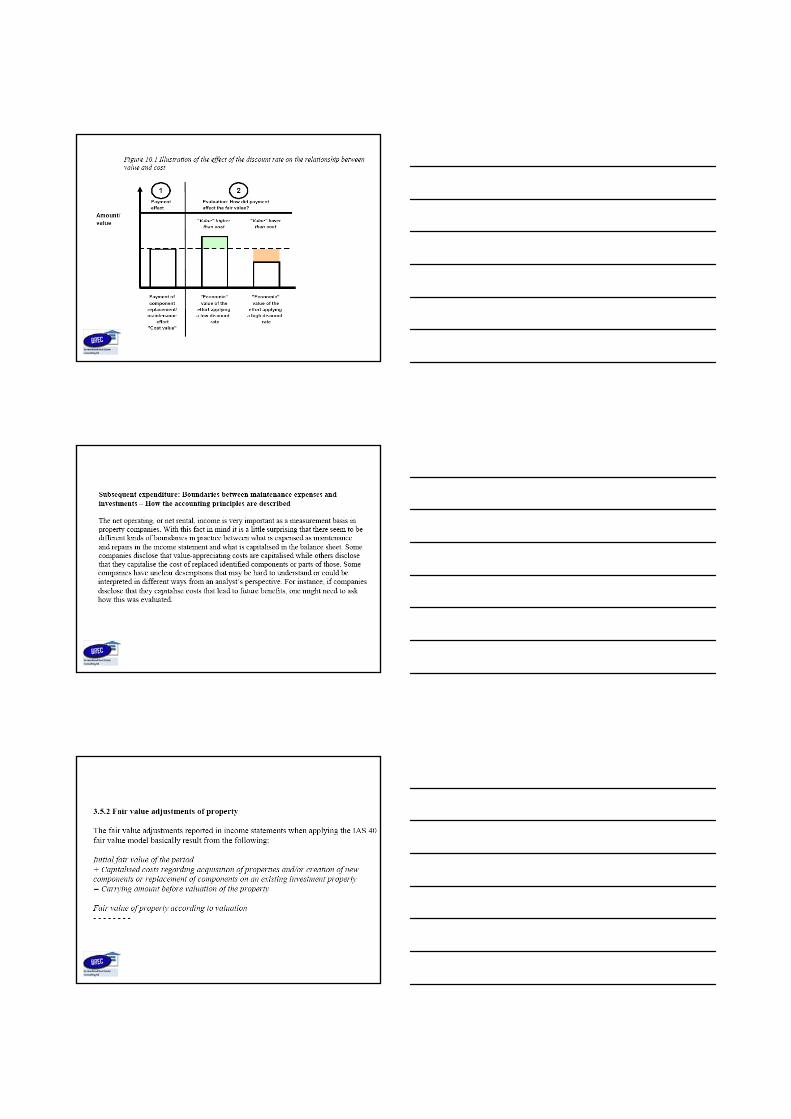

Subsequent expenditure – expense or investment? Will impact the NRI-level!

Avser åtgärden byte avhela eller delar av en

identifierad komponenteller avser åtgärden en

nytillskapad komponent?

Aktivera Kostnadsför

JA NEJ

”Day-to-day servicing” (reparationer) kostnadsföres!

”Nya” IAS 16 och IAS 40 efter”improvements”

IAS 16 p 8: Replacement of major spare parts Capitalize if expected to be used during more than 1 period!

IAS 16 and IAS 40 afterimprovements in 2003

Replacement of identifiedparts of the asset?Created new parts?

Yes No

Capitalize Expense

Day-to-day servicing - expense

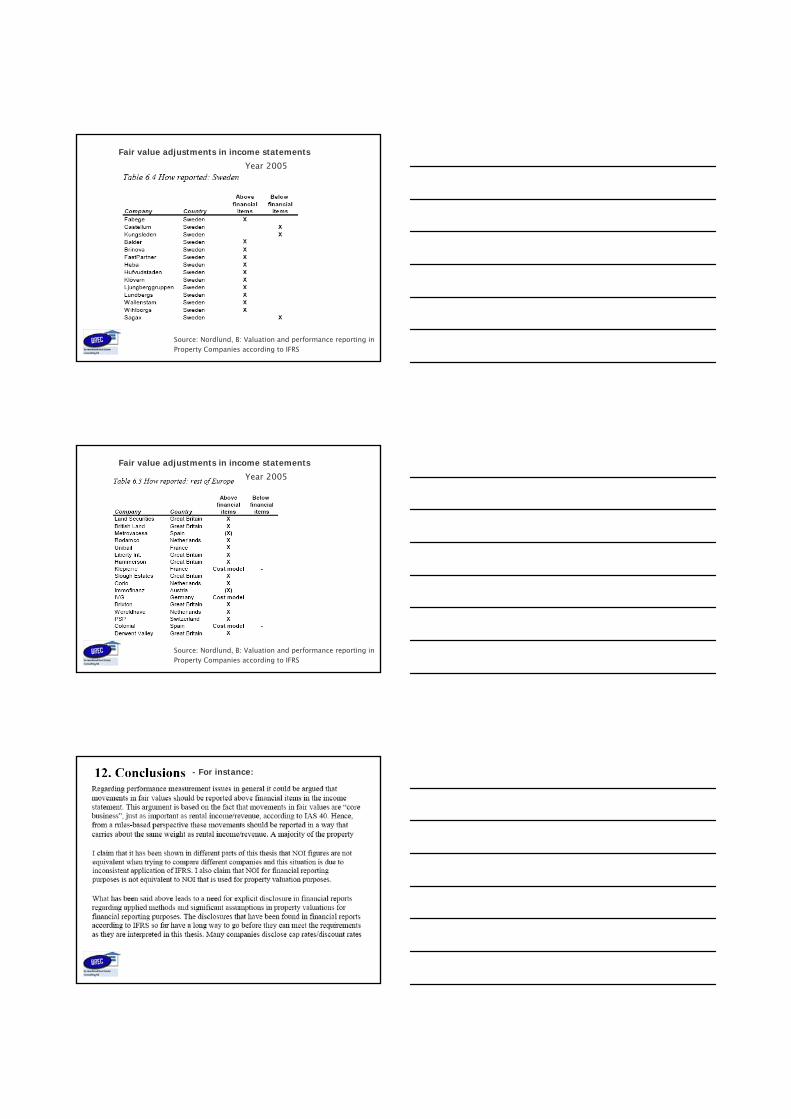

Fair value adjustments in income statements

Source: Nordlund, B: Valuation and performance reporting inProperty Companies according to IFRS

Year 2005

Fair value adjustments in income statements

Source: Nordlund, B: Valuation and performance reporting inProperty Companies according to IFRS

Year 2005

- For instance:

Principle illustration - Applying FVA-concept for different kinds of assets

Need for disclosure of- Applied methods in valuations- Significant assumptions in valuations- Connections between appraised figures and market evidence

High

Low

Subjectivity Objectivity

Need for disclosure regarding applied methods and significant assumptiIn valuations varies depending what kind of asset valued

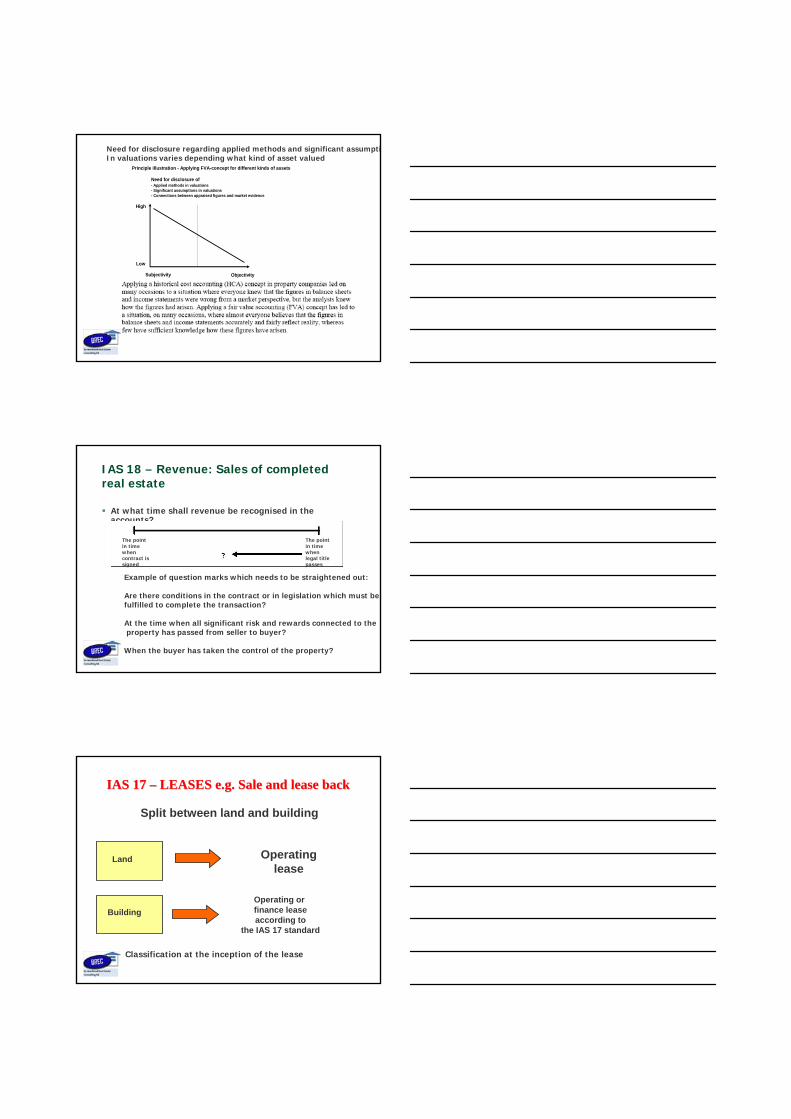

IAS 18 – Revenue: Sales of completed real estate

At what time shall revenue be recognised in the accounts?

Example of question marks which needs to be straightened out:

Are there conditions in the contract or in legislation which must be fulfilled to complete the transaction?

At the time when all significant risk and rewards connected to the property has passed from seller to buyer?

When the buyer has taken the control of the property?

The point in time when contract is signed

The point in time when legal titlepasses

IAS 17 IAS 17 –– LEASES e.g. Sale and lease backLEASES e.g. Sale and lease back

Split between land and building

Land

Building

Operatinglease

Operating or finance leaseaccording to

the IAS 17 standard

Classification at the inception of the lease