accounting revenue from - deloitte us · 2017 deloitte renewable energy seminar innovating for...

TRANSCRIPT

2017 Deloitte Renewable Energy SeminarInnovating for tomorrowNovember 13-15, 2017

Accounting

for ASC 606,

revenue from

contracts with

customers

Teresa Thomas, Partner, Deloitte & Touche LLPJody Force, Managing Director, Deloitte & Touche LLP

Copyright © 2017 Deloitte Development LLC. All rights reserved. 3

Overview of ASC 606

Industry task force implementation update

Application for common arrangements

Disclosure requirements

Implementation challenges and best practices

Resources

Questions

Appendix: AICPA task force issue status

Agenda

Copyright © 2017 Deloitte Development LLC. All rights reserved. 4

Overview of ASC 606

Copyright © 2017 Deloitte Development LLC. All rights reserved. 5

• Applies to an entity’s contracts with customers

• Does not apply to:

‒ Lease contracts (ASC 840),

‒ Insurance contracts (ASC 944),

‒ Certain financial instruments and other contractual rights or obligations,

‒ Guarantees (other than product or service warranties), and

‒ Nonmonetary exchanges whose purpose is to facilitate a sale to another party

• Some key aspects apply to transfer (sale) of nonfinancial assets

Scope

Overview of ASC 606

Glossary terms

Contract: An agreement between two or more parties that creates enforceable rights and obligations.

Customer: A party that has contracted with an entity to obtain goods or services that are an output of the entity’s ordinary activities in exchange for consideration.

Copyright © 2017 Deloitte Development LLC. All rights reserved. 6

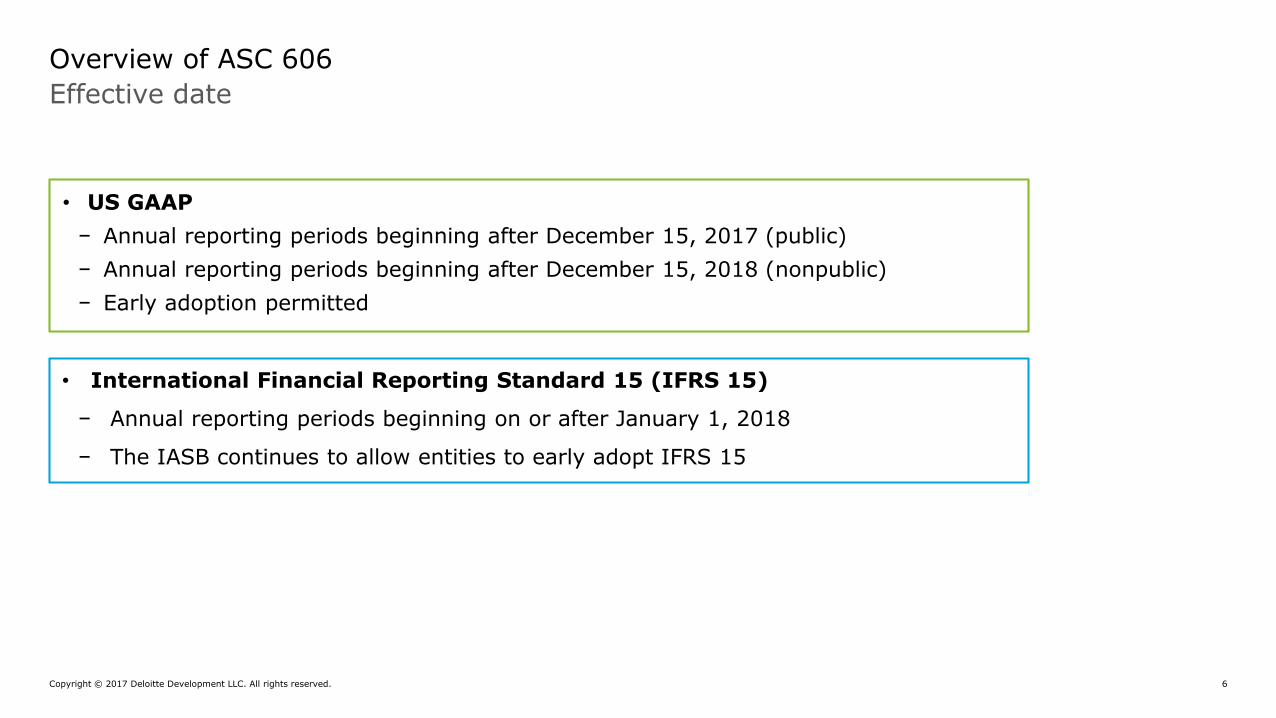

• US GAAP

− Annual reporting periods beginning after December 15, 2017 (public)

− Annual reporting periods beginning after December 15, 2018 (nonpublic)

− Early adoption permitted

Effective date

Overview of ASC 606

• International Financial Reporting Standard 15 (IFRS 15)

− Annual reporting periods beginning on or after January 1, 2018

− The IASB continues to allow entities to early adopt IFRS 15

Copyright © 2017 Deloitte Development LLC. All rights reserved. 7

• Full Retrospective Approach

− Restate prior periods in compliance with ASC 250

− Optional practical expedients

• Modified Retrospective Approach

− Apply revenue standard either to all contracts at the date of initial application or only to contracts that are not completed as of effective date and record cumulative catch up

− Required disclosures:

◦ Amount of each F/S line item affected in current period

◦ Explanation of significant changes

Example:

Transition options

Overview of ASC 606

January 1, 2018 Initial Application Year

2018Current Year

2017Prior Year 1

2016Prior Year 2

New contracts New ASU

Existing contracts New ASU + cumulative catch up

Legacy GAAP Legacy GAAP

Completed contracts Legacy GAAP Legacy GAAP

cumulative catch-up

Copyright © 2017 Deloitte Development LLC. All rights reserved. 8

Core principle: Recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration the entity expects to be entitled in exchange for those goods or services

This revenue recognition model is based on a transfer of control approach, which differs from the risks and rewards approach applied under current U.S. GAAP

The five-step model

Overview of ASC 606

Identify the contract with a

customer

(Step 1)

Identify the performance

obligations in the contract

(Step 2)

Determine the transaction price

(Step 3)

Allocate the transaction price to

performance obligations

(Step 4)

Recognize revenue when (or as) the entity satisfies a

performance obligation

(Step 5)

Copyright © 2017 Deloitte Development LLC. All rights reserved. 9

A legally enforceable contract (oral or implied) must meet all of the following requirements:

A contract will not be in the scope if:

Step 1: Identify the contract

Overview of ASC 606

The contract has commercial substance

The parties have approved the contract and are committed to

perform

The entity can identify each party’s rights regarding goods or services

The entity can identify the payment terms for the goods or services to be

transferred

It is probable the entity will collect the consideration to which it will be entitled in exchange for the goods or services that will be transferred to

the customer

The contract is wholly unperformedEach party can unilaterally terminate the contract without compensation

AND

Copyright © 2017 Deloitte Development LLC. All rights reserved. 10

The ASU defines a performance obligation as a promise to transfer to the customer a good or service (or a bundle of goods or services) that is distinct

Step 2: Identifying performance obligations

Overview of ASC 606

Identify all (explicit or implicit) promised goods and services in the contract

Are promised goods and services distinct from other goods and services in the contract?

Can the customer benefit from the good or service on its own or

together with other readily available resources?

Is the good or service separately identifiable from other promises in

the contract?

AND

Account for as a performance obligationCombine two or more promised goods or

services & reevaluate

YES

CAPABLE OF BEING DISTINCT DISTINCT WITHIN CONTEXT OF CONTRACT

NO

Copyright © 2017 Deloitte Development LLC. All rights reserved. 11

Transaction price shall include…

−Fixed consideration

−Variable consideration (estimated)

−Noncash consideration

◦ Measure at fair value at contract inception

◦ Constraint would not apply to variability due to the formof the consideration

−Adjustments for significant financing component

−Adjustments for consideration payable to customer

Transaction price does NOT include…

−Effects of customer credit risk

Step 3: Determining transaction price

Overview of ASC 606

Need to consider whether adjustments are for concessions or

credit risk

Principle: The transaction price is the amount of consideration to which an entity expects to be entitled in exchange for transferring promised goods or services to a customer (which excludes estimates of variable consideration that are constrained)

Copyright © 2017 Deloitte Development LLC. All rights reserved. 12

When accounting for variable consideration an entity shall…

• Estimate using expected value (probability weighted) or most likely amount methods

• Subject to the following “constraint”:

−Include in the transaction price some or all of an amount of variable consideration estimated only to the extent that it is “probable” that a significant reversal in the amount of cumulative revenue recognized will not occur when the uncertainty associated with the variable consideration is subsequently resolved.

−Consider the following factors in assessing whether the estimated transaction price is subject to significant revenue reversal:

◦ Highly susceptible to factors outside entity’s influence

◦ Uncertainty not expected to be resolved for a long time

◦ Entity’s experience is limited

◦ Entity typically offers broad range of price concessions/payment terms

◦ Large number of broad range possible outcomes

Step 3: Determining transaction price

Overview of ASC 606

Copyright © 2017 Deloitte Development LLC. All rights reserved. 13

Allocate transaction price on a relative standalone selling price basis (estimate standalone selling price if not observable)

• The expected cost-plus margin method, adjusted market assessment method, or residual method (only if price is highly variable or uncertain) are acceptable.

Allocate transaction price to all performance obligations, unless a portion of (or changes in) the transaction price relate entirely to one or more obligations and certain criteria are met

Do not reallocate for changes in standalone selling prices

If certain criteria are met, a discount or variable consideration may be allocated to one or more, but not all, of the performance obligations in a contract.

Step 4: Allocating the transaction price

Overview of ASC 606

Copyright © 2017 Deloitte Development LLC. All rights reserved. 14

Evaluate if control of a good or service transfers over time, if not then control transfers at a point in time. An entity satisfies a performance obligation over time if:

Measure progress toward completion using input/output methods

* An entity has a right to payment only if, at all times throughout the duration of the contract, the entity is entitled to an amount that at least compensates for performance completed to date. This compensation should approximate the selling price of the goods/services (i.e. costs incurred plus a reasonable profit margin)

Step 5: Recognizing revenue

Overview of ASC 606

Performance does not create an asset with an alternative use and the entity has an enforceable right to payment* for performance completed to date

Performance creates or enhances a customer controlled asset. (e.g., home addition)

The customer receives and consumes the benefit as the entity performs. (e.g., sale of electricity)

OR

OR

Copyright © 2017 Deloitte Development LLC. All rights reserved. 15

For performance obligations satisfied at a point in time, indicators that control transfers include, but are not limited to, the following:

Step 5: Recognizing revenue

Overview of ASC 606

The entity has a present right to payment

The customer has legal title

The entity has transferred physical possession

The customer has the significant risks and rewards of ownership

The customer has accepted the asset

Copyright © 2017 Deloitte Development LLC. All rights reserved. 16

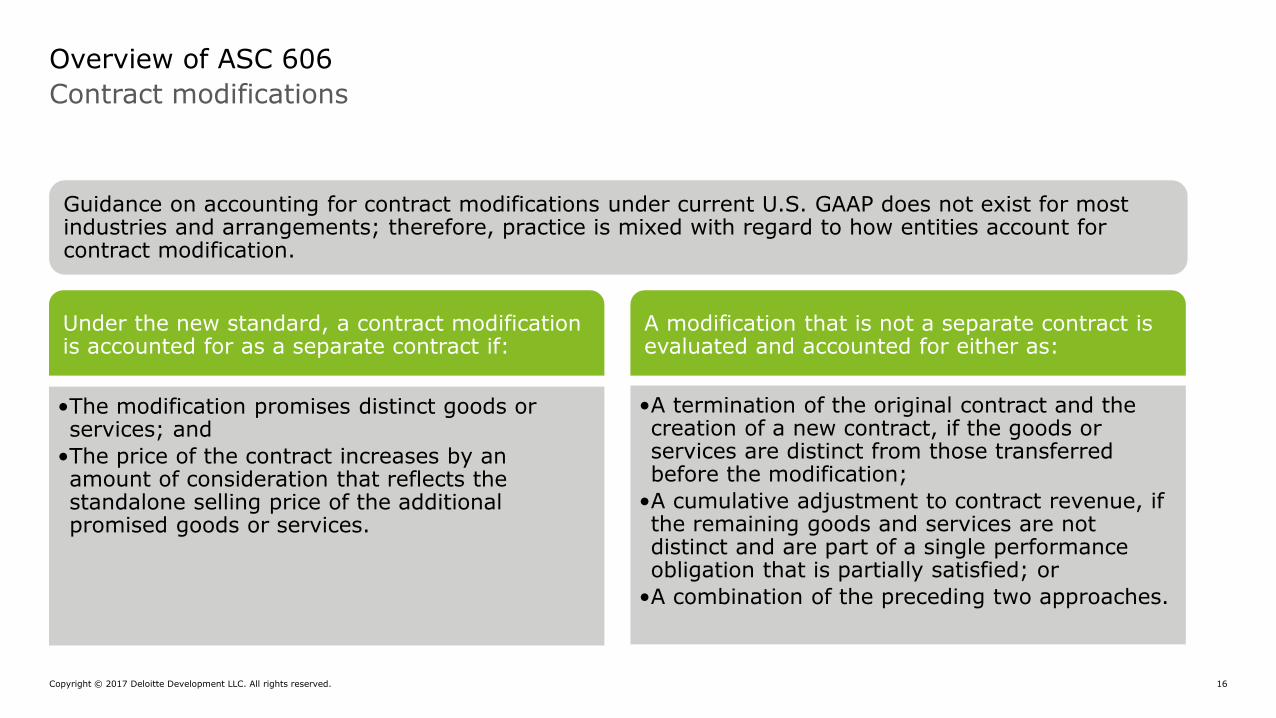

Contract modifications

Overview of ASC 606

Under the new standard, a contract modification is accounted for as a separate contract if:

A modification that is not a separate contract is evaluated and accounted for either as:

•A termination of the original contract and the creation of a new contract, if the goods or services are distinct from those transferred before the modification;

•A cumulative adjustment to contract revenue, if the remaining goods and services are not distinct and are part of a single performance obligation that is partially satisfied; or

•A combination of the preceding two approaches.

Guidance on accounting for contract modifications under current U.S. GAAP does not exist for most industries and arrangements; therefore, practice is mixed with regard to how entities account for contract modification.

•The modification promises distinct goods or services; and

•The price of the contract increases by an amount of consideration that reflects the standalone selling price of the additional promised goods or services.

Copyright © 2017 Deloitte Development LLC. All rights reserved. 17

In 2017, the FASB issued ASU 2017-05 which clarifies the following:

• Transactions that are within the scope of ASC 610-20

• Accounting for the partial sales of non-financial assets

Accounting for the full or partial sales of power-generating PP&E (e.g. sale of solar or wind farms)

• As part of the new revenue standard, ASC 610-20 was added to address the recognition and transfer of non-financial assets for contracts with non-customers

• Guidance supersedes the real estate guidance in ASC 360-20 which was typically used to account for sales of non-financial assets that were considered integral equipment.

In January 2017, the FASB issued ASU 2017-01

• clarifies and narrows the definition of a business.

• Under the revised definition, fewer real estate transactions may be businesses than current practice, and therefore more transactions could be accounted for in accordance with ASC 610-20.

Sales of non-financial assets

Overview of ASC 606

Copyright © 2017 Deloitte Development LLC. All rights reserved. 18

“Partial sales” are sales or transfers of a nonfinancial asset to another entity in exchange for a non-controlling ownership interest in that entity

• Accounted for in accordance with ASC 610-20

• If entity no longer retains a controlling interest in the non-financial assets:

• Derecognize when control is transferred consistent with the principles in ASC 606

• Retained non-controlling ownership interest is measured at fair value

Sales of non-financial assets

Overview of ASC 606

Copyright © 2017 Deloitte Development LLC. All rights reserved. 19

Sales of non-financial assets

ASC 610-20 Decision tree

Overview of ASC 606

Yes

No

Yes Yes

If the assets in an individual consolidated subsidiary are all nonfinancial assets and in substance nonfinancial assets, then apply Subtopic 610-20 to each distinct asset within that subsidiary. Otherwise, apply 810-40-3A(c) or 810-45-21A(b)(2) to the subsidiary. Apply other ASC topics or subtopics to the remaining parts of the contract, if any.

No

Yes Yes Yes

Apply

topic 606

Is the

transaction

the transfer

of a

business or

nonprofit

activity?

Apply

Subtopic

810-10

Is the

transaction

entirely

accounted

for in Topic

860?

Apply topic

860

Does

another

scope

exception

apply (610-

20-15-4)?

Apply other

topics or

subtopics

Are the

assets all

non-

financial and

in substance

non-financial

assets?

Apply Subtopic 610-20

to each distinct asset

promised in the

contract. Apply other

Topics or Subtopics to

the remaining parts of

the contract, if any.

Transfer of

an

ownership

interest in 1

or more

subsidiaries?

Start

Is the

counter

-party a

custom

er?

No

Apply Subtopic

610-20 to each

distinct

nonfinancial asset

promised in the

contract. Apply

other Topics or

Subtopics to the

remaining parts of

the contract, if

any.

No No No

Copyright © 2017 Deloitte Development LLC. All rights reserved. 20

Sales of non-financial assets

Interaction between ASC

610-20 and ASC 606

For de-recognition, unit of account is defined as a distinct nonfinancial asset

Applies many of the same principles as ASC 606 for determining the gain or loss to recognize when a nonfinancial asset is derecognized

If contract contains other elements that are not within the scope of ASC 610-20, apply guidance in ASC 606 for separation and measurement of goods and services

Overview of ASC 606

Copyright © 2017 Deloitte Development LLC. All rights reserved. 21

Industry task force

Implementation update

Copyright © 2017 Deloitte Development LLC. All rights reserved. 22

AICPA Task Forces

Implementation efforts

AICPA Task Forces

• 16 industry groups established

• Objective is to perform industry specific overview of the revenue standard and identify top issues that may warrant industry specific interpretive guidance

• Issues that, if not investigated on a group level, could lead to inconsistencies in implementation

Who is on the P&U Task Force?

• Participants from:

-Regulated and non-regulated companies

- Industry trade groups (EEI and AGA)

- Public accounting firms

Copyright © 2017 Deloitte Development LLC. All rights reserved. 23

AICPA Task Force (cont.)

Implementation efforts

How is the work of the industry Task Force reviewed or validated?

• Independent review bodies review the work of the Task Force, including:

−Revenue Recognition Working Group (RRWG)

◦ Accounting firms and members outside of the industries to review and evaluate for consistency across industries

−FinREC review

What will be the end product?

−AICPA publication similar to the AICPA accounting and audit guides

−Public comment period

−Not authoritative guidance, but expected to be widely accepted

Copyright © 2017 Deloitte Development LLC. All rights reserved. 24

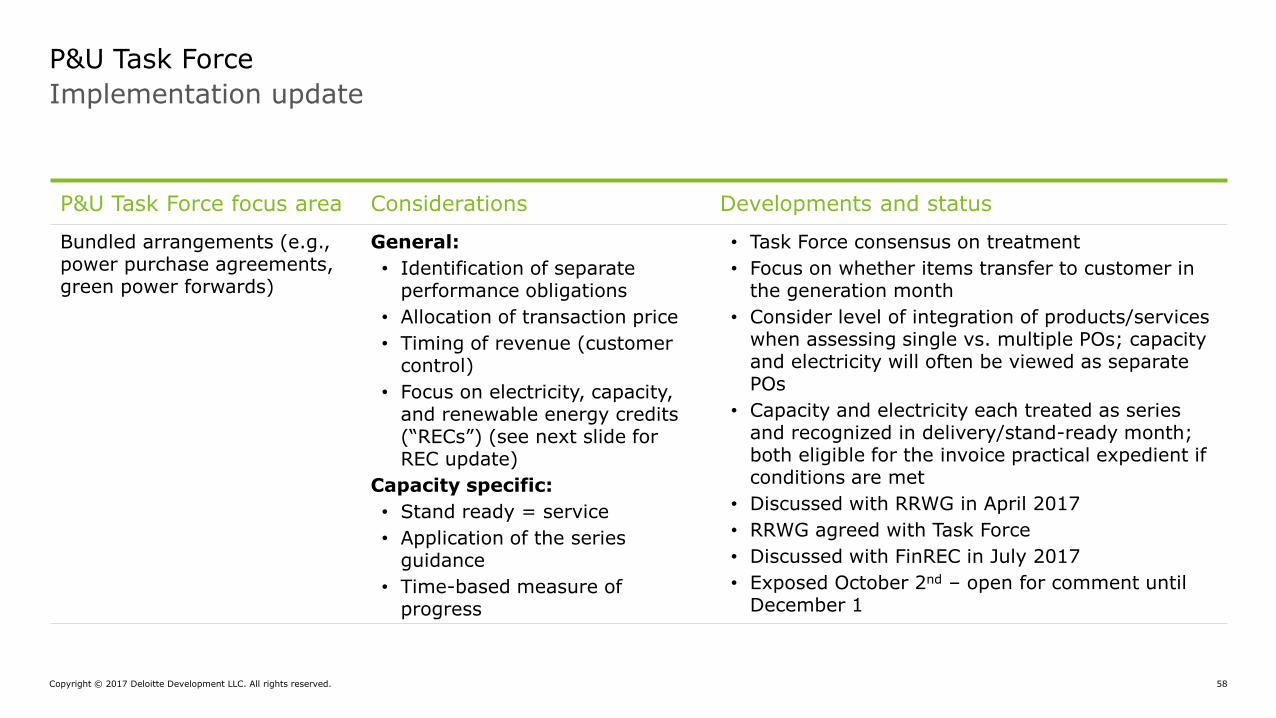

Implementation update

P&U Task Force

P&U Task Force focus area Considerations Developments and status

Bundled arrangements (e.g., power purchase agreements, green power forwards)

General:

• Identification of separate performance obligations

• Allocation of transaction price

• Timing of revenue (customer control)

• Focus on electricity, capacity, and renewable energy credits (“RECs”) (see next slide for REC update)

Capacity specific:

• Stand ready = service

• Application of the series guidance

• Time-based measure of progress

• Task Force consensus on treatment

• Focus on whether items transfer to customer in the generation month

• Consider level of integration of products/services when assessing single vs. multiple POs; capacity and electricity will often be viewed as separate POs

• Capacity and electricity each treated as series and recognized in delivery/stand-ready month; both eligible for the invoice practical expedient if conditions are met

• Discussed with RRWG in April 2017

• RRWG agreed with Task Force

• Discussed with FinREC in July 2017

• Exposed October 2nd – open for comment until December 1

Copyright © 2017 Deloitte Development LLC. All rights reserved. 25

Implementation update (cont.)

P&U Task Force

P&U Task Force focus area Considerations Developments and status

Sales of self-generated (yet-to-be-certified) RECs

• PO satisfied over time or point in time?

• Impact of certification lag?

• Transfer of control upon generation of electricity or certification?

• Task Force consensus that RECs represent a point in time PO and revenue should be recognized upon generation of associated electricity

• Emphasis on completion of all obligations by seller, present right to payment and analogy to customer acceptance guidance (objective evidence of acceptance)

• Discussed with RRWG in April 2017

• RRWG agreed with Task Force

• Discussed with FinREC in July 2017

• FinREC agreed with Task Force but also felt that recognition upon certification could likely be supported depending on facts and circumstances; issue paper has been modified to reflect this view

• Exposed October 2nd – open for comment until December 1

Copyright © 2017 Deloitte Development LLC. All rights reserved. 26

Implementation update (cont.)

P&U Task Force

P&U Task Force focus area Considerations Developments and status

Step vs. strip pricing • Both pricing conventions common in the industry

• Historical practice of recognizing revenue at the invoice price

• Can same performance result in different revenue profiles?

• Task Force consensus that different revenue profiles can be supported

• Straight-line pattern consistent with treatment as a single performance obligation (“PO”) satisfied over time and application of an output method based on units delivered

• Step (or shaped) pattern supportable if contract price is consistent with value to customer in the specified delivery period (based on application of the invoice practical expedient)

• RRWG agreed with Task Force

• Discussed with FinREC in July 2017

• Exposed September 1st – open for comment until November 1

Copyright © 2017 Deloitte Development LLC. All rights reserved. 27

Implementation update (cont.)

P&U Task Force

P&U Task Force focus area Considerations Developments and status

Partial terminations • Timing of recognition —immediate or over remainingterm?

• Can payment amount be objectively linked to the terminated deliveries?

• Was modification guidance in ASC 606 built to accommodate partial terminations?

• Task Force consensus that payments received for partial termination should be recognized immediately if objectively linked to terminated periods/deliveries

• RRWG disagreed with Task Force

• Issue was elevated to FASB staff for a TI

• TI conducted — FASB staff agreed with RRWG; seller must apply modification guidance to a partial termination, which will generally result in deferred recognition

• Answer applies to payments made or received in connection with a partial termination

• Issue discussed with RRWG (August) and FinREC (September) with no material changes

• Exposed October 2nd – open for comment until December 1

Copyright © 2017 Deloitte Development LLC. All rights reserved. 28

Application for common arrangements

Copyright © 2017 Deloitte Development LLC. All rights reserved. 29

Case Study: Accounting for a power purchase agreement (“PPA”) for the sale of energy and renewable energy credits (“RECs”)

• ABC Wind Farm (“ABC”) enters into a PPA to sell 100% of the electricity output and the associated RECs to a Regulated Utility at $32.71 MWh.

• ABC’s accounting policy is that RECs are not considered output of its wind facilityand revenue is recognized upon generation of the associated electricity

Discussion Topic: How should ABC account for its sale of electricity and REC’s under its PPA?

Bundled sale arrangements

Application for common arrangements

Copyright © 2017 Deloitte Development LLC. All rights reserved. 30

Contract Assessment Conclusions:

Bundled sale arrangements

Application for common arrangements

Step 1: Identify the Contract with Customer

Contract is within the scope of ASC 606 as both parties have an approved agreement, collectibility is assumed, payment terms are identified, each party has identified rights and obligations, and the contract affects risk, timing, and amount of ABC’s future cash flows.

Step 2: Identify the Performance Obligations (PO)

Buyer can benefit from the RECs and electricity on their own and the promise to transfer each product is separately identifiable within the PPA

1.Electricity

• Delivered overtime as the customer simultaneously receives and consumes the benefits of the energy as it is being delivered

• Represents a series of distinct services that are substantially the same and have the same pattern of transfer to the customer

2.RECs

Copyright © 2017 Deloitte Development LLC. All rights reserved. 31

Contract Assessment Conclusions (cont.):

Bundled sale arrangements

Application for common arrangements

Step 3: Determine the Transaction Price

Contract contains variable consideration as total consideration is dependent on the actual volumes produced by the facility.

Step 4: Allocate the Transaction Price to POs

Contract includes a single bundled price for the delivery of Energy and RECs. However, given that each obligation is performed and satisfied within the month (refer to step 5), it is not necessary to allocate contract consideration between the individual performance obligations. Further, variable consideration will be allocated to each distinct increment of service (monthly for practical purposes) because the amount corresponds to the value provided to the customer each month and is consistent with the allocation objectives in ASC 606-10-32-28

Copyright © 2017 Deloitte Development LLC. All rights reserved. 32

Contract Assessment Conclusions (cont.):

Bundled sale arrangements

Application for common arrangements

Step 5: Determine when to recognize revenue

1. Electricity

• Revenue recognized in the amount in which the entity has a right to invoice (ASC 606-10-55-18) as ABC has a right to consideration in an amount that corresponds directly with the value of its performance completed to date

2. RECs

• Recognized at a point in time as RECs are storable and do not meet any of the criteria in ASC 606-10-25-27

• Revenue recognized upon generation of the associated electricity

• The customer has the present right to payment at generation. Payment is made at the bundled rate when electricity is delivered

• The customer has the significant risks and rewards of the ownership at generation. There is virtually no certification risk related to a pre-certified generating facility

• ABC can objectively determine the time when the RECs are transferred to the customer (based on the meter read when electricity is generated)

• Upon generation, the seller has no significant obligations to fulfill and cannot direct the RECs to another buyer

Copyright © 2017 Deloitte Development LLC. All rights reserved. 33

Assessment impact if PPA pricing was not considered fixed and contract was considered a lease under ASC 840:

• The lease components (e.g. energy) of the contract would be scoped out of ASC 606

• Separate presentation or disclosure of revenue from non-lease components (e.g. RECs which are not considered output as a matter of policy) would be required

• Allocation of the transaction price based on the stand alone selling price would be required

Considerations for implementation of ASC 842:

• Be aware that agreement may need to be further assessed with the implementation of ASC 842 for the new leasing rules to determine if it no longer will meet the definition of a lease and will fall back into the scope of ASC 606. Key changes under ASC 842 include:

−Policy election regarding the treatment of RECs goes away as assessment is based on economic benefits rather than output

−Additional control requirements to meet the definition of a lease

Bundled sale arrangements

Application for common arrangements

Copyright © 2017 Deloitte Development LLC. All rights reserved. 34

Case Study: Accounting for a PPA with an availability guarantee

• XYZ Wind Farm (“XYZ”) enters into a PPA to sell 100% of the electricity output to a Regulated Utility at $32.71 MWh.

• Contract contains an availability guarantee which can result in a deficiency payment to the buyer if the annual availability requirement is not met.

• Guarantee assures that the facility is operating appropriately and available to produce electricity. It does not represent a material right under the contract.

Discussion Topic: What is the transaction price in the contract?

Variable consideration

Application for common arrangements

Copyright © 2017 Deloitte Development LLC. All rights reserved. 35

Contract Assessment Conclusions:

Discussion Topic: What if the provision was a minimum output guarantee as opposed to an availability guarantee?

Variable consideration

Application for common arrangements

Step 3: Determine the Transaction Price

Availability guarantee results in variable consideration the would be allocated to each annual service period (as opposed to each discrete increment of service)

• Provision needs to be monitored on an ongoing basis

• Payment may need to be estimated and included as reduction to the transaction price depending on the operation of the facility

• Estimation based on expected value (probability weighted)

Copyright © 2017 Deloitte Development LLC. All rights reserved. 36

Disclosure Requirements

Copyright © 2017 Deloitte Development LLC. All rights reserved. 37

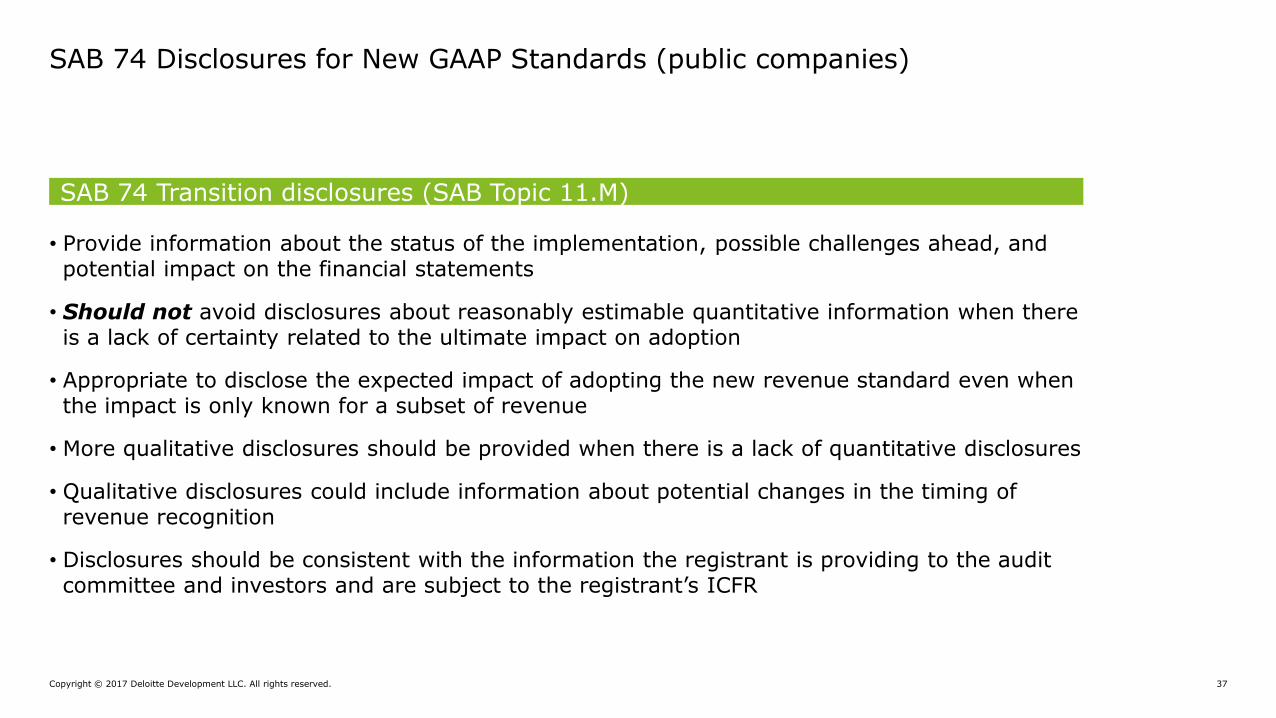

SAB 74 Disclosures for New GAAP Standards (public companies)

• Provide information about the status of the implementation, possible challenges ahead, and potential impact on the financial statements

• Should not avoid disclosures about reasonably estimable quantitative information when there is a lack of certainty related to the ultimate impact on adoption

• Appropriate to disclose the expected impact of adopting the new revenue standard even when the impact is only known for a subset of revenue

• More qualitative disclosures should be provided when there is a lack of quantitative disclosures

• Qualitative disclosures could include information about potential changes in the timing of revenue recognition

• Disclosures should be consistent with the information the registrant is providing to the audit committee and investors and are subject to the registrant’s ICFR

SAB 74 Transition disclosures (SAB Topic 11.M)

Copyright © 2017 Deloitte Development LLC. All rights reserved. 38

Disclosure requirements

Category Disclosure requirements

Practical expedient

available for nonpublic entities

Interim requirement (ASC 270)

Disaggregation

of revenue

Disaggregate revenue into categories that depict how revenue and cash flows are affected by economic factors

Yes* Yes

Sufficient information to understand the relationship between disaggregated revenue and each disclosed segment’s revenue information

Yes Yes

* An entity must at a minimum provide revenue disaggregated according to the timing of transfer of goods or services (e.g., goods transferred at a point in time and services transferred over time)

Copyright © 2017 Deloitte Development LLC. All rights reserved. 39

Disclosure requirements

Category Disclosure requirements

Practical expedient

available for nonpublic entities

Interim requirement (ASC 270)

Contract

balances

Opening and closing balances (receivable, contract assets and contract liabilities)

No Yes

Amount of revenue recognized from beginning contract liability balance

Yes Yes

Amount of revenue recognized from performance obligations (POs) satisfied in prior periods (e.g., changes in transaction price estimates)

Yes Yes

Explanation of significant changes in contract balances (using qualitative and quantitative information)

Yes No

Copyright © 2017 Deloitte Development LLC. All rights reserved. 40

Disclosure requirements

Category Disclosure requirements

Practical expedient

available for nonpublic entities

Interim requirement (ASC 270)

Performance

obligations

(POs) &

remaining

performance

obligations

(RPOs)

Qualitative information regarding when POs typicallysatisfied, significant payment terms, nature of goods/services promised, obligations for returns/refunds, warranties

No No

Transaction price allocated to the RPOs

•Disclose quantitative amounts

•Quantitative or qualitative explanation of when RPO amounts will be recognized as revenue

Yes

Yes

Yes

Yes

Copyright © 2017 Deloitte Development LLC. All rights reserved. 41

Disclosure requirements

Category Disclosure requirements

Practical expedient

available for nonpublic entities

Interim requirement (ASC 270)

Significant

judgments &

estimates

Qualitative information regarding determining the timing:

• Performance obligations satisfied over time

(e.g., methods of measuring progress, why methods are representative of transfer of goods or services, judgments in evaluating when customer obtains control of goods/services)

Yes No

• Performance obligations satisfied at a point in time, specifically the significant judgments used in evaluating when a customer obtains control

Yes No

Copyright © 2017 Deloitte Development LLC. All rights reserved. 42

Disclosure requirements

Category Disclosure requirements

Practical expedient

available for nonpublic entities

Interim requirement (ASC 270)

Significant

judgments &

estimates

(cont.)

Qualitative and quantitative information* regarding:

• Determining the transaction price (e.g., estimating variable consideration, adjusting for time value of money, noncash consideration)

Yes No

• Constraining estimates of variable consideration Yes No

• Allocating the transaction price, including estimating standalone selling prices and allocating discounts and variable consideration

Yes No

• Measuring obligations for returns, refunds, and other similar obligations

Yes No

Copyright © 2017 Deloitte Development LLC. All rights reserved. 43

Disclosure requirements

Category Disclosure requirements

Practical expedient

available for nonpublic entities

Interim requirement (ASC 270)

Contract costs Qualitative information concerning:

• Judgments made in determining the amount of the costs incurred to obtain or fulfill a contract

Yes No

• The method it uses to determine the amortization for each reporting period

Yes No

Quantitative information about:

• The closing balances of assets recognized from the costs incurred to obtain or fulfill a contract, by main category of asset

Yes No

Copyright © 2017 Deloitte Development LLC. All rights reserved. 44

Disclosure requirements

Category Disclosure requirements

Practical expedient

available for nonpublic entities

Interim requirement (ASC 270)

Contract costs • The amount of amortization and any impairment losses recognized in the reporting period

Yes No

Practical

expedients

Disclose use of practical expedients No No

Copyright © 2017 Deloitte Development LLC. All rights reserved. 45

Implementation

Challenges and best practices

Copyright © 2017 Deloitte Development LLC. All rights reserved. 46

Overview of potential key system challenges

Implementation

Issue Description

1. Disparatesystems/multiple source data systems

• Many entities perform revenue allocation in disparate systems with inconsistent data; as a result of the implementation of the standard, data stress levels will rise and companies may want to consider an automated tool or customization as part of the implementation solution

2. Significant use of spreadsheets in process

• Many entities, especially if acquisitive, rely on use of spreadsheets to manage revenue; the requirements of the standard may add complexities to those manual processes

• Entities may want to consider a bolt-on revenue recognition tool or customizing current system

3. Performance obligations

• Recording and tracking revenue for each performance obligation or contract in the sales or billing cycle may not be available in current systems

• System requirements may need to include the ability to reallocate revenue to completed performance obligations when changes in estimate of a variable transaction price occur

4. Disclosures • Most changes for disclosure will require changes to the structure and data elements needed for the month-end reports

Copyright © 2017 Deloitte Development LLC. All rights reserved. 47

Overview of potential key data and process impacts

Implementation

Issue Description

1. Recognition:distinct criteria

• Significant judgment may be needed when determining whether the goods or services are distinct within the context of the standard; as a result, policies and processes may need to be revised and/or developed

2. Recognition:performance obligations

• The guidance may increase the number of performance obligations within the contract or arrangements and may result in an increase to the number of data elements required to be captured

3. Initial measurement: time value of money

• Given that when determining the transaction price, an entity should adjust the amount of promised consideration for the effects of the time value of money (if the contract has a significant finance component), processes may need to be developed and data elements captured to satisfy the requirement

4. Allocation • An entity will likely be less constrained by the new allocation requirements for revenue recognition but may need to use more judgment around estimating the stand alone selling price for allocation; as a result, policies and process may need to be revised and/or developed to meet the new requirements

Copyright © 2017 Deloitte Development LLC. All rights reserved. 48

Common activities by phase

Implementation

Understand, educate, plan

Assess and design ImplementReassess and evaluate

sustainability

Understand, educate, plan

Understandthe standard and related impacts

• Read and understand the standard

• Review existing whitepapers, narratives, and process flows to understand current accounting policies and processes

Educate • Inform audit committee and other leaders within the organization regarding new standard

•Hold initial training session with key stakeholders and team leads

• Provide an overview of the standard and outline key impacts on business and functional groups

Plan • Identify appropriate leaders to monitor and oversee adoption efforts (e.g., establish a steering committee and appropriate governance) and coordinate among departments

• Identify key project personnel to own adoption process within functions

•Develop project plan and reporting protocols for project visibility and risk management

• Establish implementation milestones and timelines

Copyright © 2017 Deloitte Development LLC. All rights reserved. 49

Common activities by workstream

Implementation

Understand, educate, plan

Assess and design ImplementReassess and evaluate

sustainability

Assess and design

Accounting • Evaluate existing contracts using the new five-step model for revenue recognition

•Develop accounting calculation logic and determine necessary journal entries

•Document considerations describing the appropriate accounting and how conclusions were reached

• Assess tax implications

Controls • Assess risk throughout the process

• Evaluate impacts on internal controls, including controls over accounting, data quality, and reporting

Disclosures and reporting

•Draft disclosure information for reporting that contemplates 1) implementation impacts under SAB Topic 11.M and 2) requirements under the new standard and SEC reporting as necessary

Data and systems

• Identify data gaps and data needed to be tracked and retained

• Evaluate whether modifications to technology are needed

Copyright © 2017 Deloitte Development LLC. All rights reserved. 50

Common activities by workstream

Implementation

Understand, educate, plan

Assess and design ImplementReassess and evaluate

sustainability

Implement

Accounting • Review and approve the accounting calculation logic and journal entries

•Update accounting policies

Controls •Design controls to address risk of material misstatement arising from the adoption of the new standard

•Update process flow diagrams

• Inform and train personnel impacted by changes

• Review operation of key controls, processes, and reports

Data and systems

•Determine key user reports and journal entries

• Test modifications made to accounting systems and evaluate any error reports

• Implement data retention strategy

Disclosures and reporting

• Identify additional steps required in periodic close process and resource needs

• Perform a “test-close”

• Review and finalize draft disclosures

Copyright © 2017 Deloitte Development LLC. All rights reserved. 51

Common activities by workstream

Implementation

Understand, educate, plan

Assess and design ImplementReassess and evaluate

sustainability

Reassess and evaluate sustainability

Accounting • Evaluate sustainability of revised accounting processes and modify as appropriate

• Assess opportunities for further integration and efficiencies

Controls •Monitor and reassess control environment

Data and systems

• Perform post “go-live” assessments of system implementation or upgrades

Disclosures and reporting

• Review comparable company disclosures and assess opportunities for further refinement and enhancement of disclosures and reporting

Copyright © 2017 Deloitte Development LLC. All rights reserved. 52

The implementation of the ASC 606 specifically impacts, but is not limited to, COSO Principle 9 regarding the identification and assessment of changes that could significantly impact the system of controls.

COSO Principle 9: The organization identifies and assesses changes that could significantly impact the system of internal control.

• Application of the new accounting standard represents a change that should be appropriately factored into the risk-assessment process.

Internal Controls

Overview of ASC 606

Common COSO challenge Leading practice

Lack of consideration or evaluation of external events,

such as changes in accounting standards and their

impact on risk assessment and ICFR. For example:

• Impacts on roles are not considered

• Adequate training is not provided

• Roles and responsibilities related to changes not

monitored

In response to risks arising from changes,

management determines whether 1) new

controls are needed or 2) the risks are

adequately addressed by existing controls

Copyright © 2017 Deloitte Development LLC. All rights reserved. 53

Resources

Copyright © 2017 Deloitte Development LLC. All rights reserved. 54

• A roadmap to applying the new revenue recognition standard

• Heads Up — Implementing the new revenue standard — How do your disclosures stack up?

• Heads Up — Internal control considerations related to adoption of the new revenue recognition standard

• Heads Up — FASB amends guidance on derecognition and partial sales of nonfinancial assets

• Refer to the New Revenue Recognition Standard Resource Center for a comprehensive summary of internal resources and contacts:

−https://audit.deloitteresources.com/revrec/Pages/Home.aspx

• AICPA website: draft AICPA whitepapers being posted for public comment

Resources

Copyright © 2017 Deloitte Development LLC. All rights reserved. 55

Questions

Copyright © 2017 Deloitte Development LLC. All rights reserved. 56

Appendix

AICPA Task Force Status

Copyright © 2017 Deloitte Development LLC. All rights reserved. 57

Implementation update

P&U Task Force

P&U Task Force focus area Considerations Developments and status

Tariff-based sales • Scope clarification

• Carve-out of alternative revenue programs led some to question whether any tariff sales were in scope of ASC 606

• Task Force consensus that tariff-based sales are in scope

• For at-will customers, current contract limited to services rendered to date

• Some term contracts may exist (e.g., some commercial and industrial customers)

• RRWG and FinREC agreed with Task Force consensus and issue was released for exposure in Q1 2017

• Public exposure period ended May 1, 2017

• Final paper cleared at July 2017 FinREC meeting

Copyright © 2017 Deloitte Development LLC. All rights reserved. 58

Implementation update

P&U Task Force

P&U Task Force focus area Considerations Developments and status

Bundled arrangements (e.g., power purchase agreements, green power forwards)

General:

• Identification of separate performance obligations

• Allocation of transaction price

• Timing of revenue (customer control)

• Focus on electricity, capacity, and renewable energy credits (“RECs”) (see next slide for REC update)

Capacity specific:

• Stand ready = service

• Application of the series guidance

• Time-based measure of progress

• Task Force consensus on treatment

• Focus on whether items transfer to customer in the generation month

• Consider level of integration of products/services when assessing single vs. multiple POs; capacity and electricity will often be viewed as separate POs

• Capacity and electricity each treated as series and recognized in delivery/stand-ready month; both eligible for the invoice practical expedient if conditions are met

• Discussed with RRWG in April 2017

• RRWG agreed with Task Force

• Discussed with FinREC in July 2017

• Exposed October 2nd – open for comment until December 1

Copyright © 2017 Deloitte Development LLC. All rights reserved. 59

Implementation update (cont.)

P&U Task Force

P&U Task Force focus area Considerations Developments and status

Sales of self-generated (yet-to-be-certified) RECs

• PO satisfied over time or point in time?

• Impact of certification lag?

• Transfer of control upon generation of electricity or certification?

• Task Force consensus that RECs represent a point in time PO and revenue should be recognized upon generation of associated electricity

• Emphasis on completion of all obligations by seller, present right to payment and analogy to customer acceptance guidance (objective evidence of acceptance)

• Discussed with RRWG in April 2017

• RRWG agreed with Task Force

• Discussed with FinREC in July 2017

• FinREC agreed with Task Force but also felt that recognition upon certification could likely be supported depending on facts and circumstances; issue paper has been modified to reflect this view

• Exposed October 2nd – open for comment until December 1

Copyright © 2017 Deloitte Development LLC. All rights reserved. 60

Implementation update (cont.)

P&U Task Force

P&U Task Force focus area Considerations Developments and status

Step vs. strip pricing • Both pricing conventions common in the industry

• Historical practice of recognizing revenue at the invoice price

• Can same performance result in different revenue profiles?

• Task Force consensus that different revenue profiles can be supported

• Straight-line pattern consistent with treatment as a single performance obligation (“PO”) satisfied over time and application of an output method based on units delivered

• Step (or shaped) pattern supportable if contract price is consistent with value to customer in the specified delivery period (based on application of the invoice practical expedient)

• RRWG agreed with Task Force

• Discussed with FinREC in July 2017

• Exposed September 1st – open for comment until November 1

Copyright © 2017 Deloitte Development LLC. All rights reserved. 61

Implementation update (cont.)

P&U Task Force

P&U Task Force focus area Considerations Developments and status

Partial terminations • Timing of recognition —immediate or over remainingterm?

• Can payment amount be objectively linked to the terminated deliveries?

• Was modification guidance in ASC 606 built to accommodate partial terminations?

• Task Force consensus that payments received for partial termination should be recognized immediately if objectively linked to terminated periods/deliveries

• RRWG disagreed with Task Force

• Issue was elevated to FASB staff for a TI

• TI conducted — FASB staff agreed with RRWG; seller must apply modification guidance to a partial termination, which will generally result in deferred recognition

• Answer applies to payments made or received in connection with a partial termination

• Issue discussed with RRWG (August) and FinREC (September) with no material changes

• Exposed October 2nd – open for comment until December 1

Copyright © 2017 Deloitte Development LLC. All rights reserved. 62

Implementation update (cont.)

P&U Task Force

P&U Task Force focus area

Considerations Developments and status

Contributions in aid of construction (“CIAC”)

• Revenue vs. offset to property, plant, and equipment?

• Is CIAC akin to a reimbursement of set-up costs under ASC 606?

• Potential for significant change in practice if required to be reflected as revenue

• Potential for difference between regulatory accounting and GAAP

• Task Force reached consensus that CIAC is not required to be treated as revenue

• January 2017 — P&U industry reps invited to attend FASB roundtable on preproduction costs

• Issue was subsequently elevated to the FASB staff for a TI

• TI conducted — FASB agreed that CIAC in a regulated environment can continue to be treated as a reduction of utility plant (i.e., out of scope of ASC 606)

• Focus on nature of activity (nonrevenue) and inability to negotiate CIAC amount

• Issue discussed with RRWG (August) and FinREC (September) with no material changes

• SEC Staff input – Encourage consultation with Staff if a registrant plans to treat something as revenue under ASC 606 that was not deemed revenue under ASC 605 (not expected for P&U entities based on TI results)

• Exposed October 2nd – open for comment until December 1

Copyright © 2017 Deloitte Development LLC. All rights reserved. 63

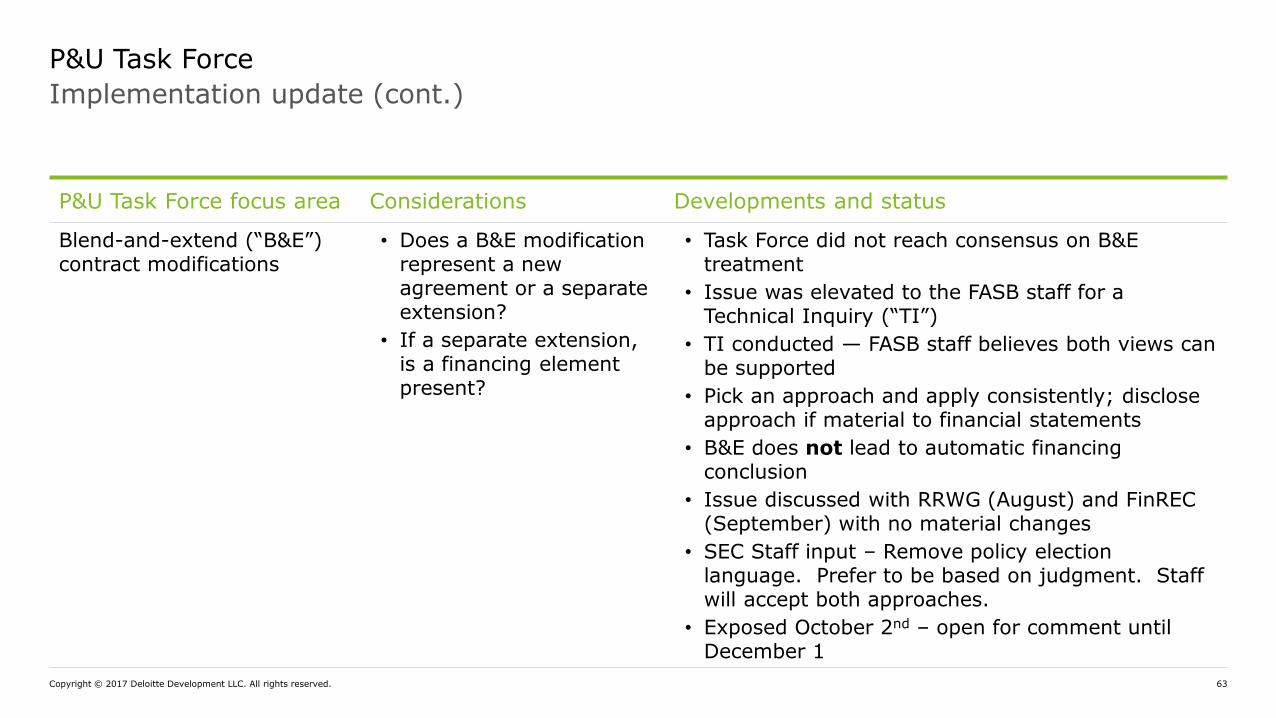

Implementation update (cont.)

P&U Task Force

P&U Task Force focus area Considerations Developments and status

Blend-and-extend (“B&E”) contract modifications

• Does a B&E modification represent a new agreement or a separate extension?

• If a separate extension, is a financing element present?

• Task Force did not reach consensus on B&E treatment

• Issue was elevated to the FASB staff for a Technical Inquiry (“TI”)

• TI conducted — FASB staff believes both views can be supported

• Pick an approach and apply consistently; disclose approach if material to financial statements

• B&E does not lead to automatic financing conclusion

• Issue discussed with RRWG (August) and FinREC (September) with no material changes

• SEC Staff input – Remove policy election language. Prefer to be based on judgment. Staff will accept both approaches.

• Exposed October 2nd – open for comment until December 1

Copyright © 2017 Deloitte Development LLC. All rights reserved. 64

Implementation update (cont.)

P&U Task Force

P&U Task Force focus area Considerations Developments and status

Variable consideration • Dealing with various forms of price and volume variability

• Application of the constraint guidance (ability to fully constrain?)

• Analysis in TRG Paper No. 48 on customer options for additional goods and services

• Volume sold dictated by “customer’s customer”

• General view that many forms of price variability can be linked to discrete delivery of power

• Task Force view that volume variability will often represent optional purchases (e.g., requirements contract) and that pricing often represents a marketing offer as opposed to granting a material right

• View applies whether volumes are dictated by customer or customer’s customer (e.g., utility buying from independent power producer to serve end-user demand)

• Discussed with RRWG in April 2017 - RRWG agreed with Task Force

• Discussed with FinREC in July 2017

• Issued for public comment from August -October

Copyright © 2017 Deloitte Development LLC. All rights reserved. 65

Implementation update (cont.)

P&U Task Force

P&U Task Force focus area Considerations Developments and status

Stand-alone selling price (“SASP”) for commodities

• Alternatives to the forward curve?

• Replaced “series forstorable commodities” issue

• Concern that forward curve would be de facto SASP for all commodity forwards satisfied at a point in time (i.e., those ineligible for the series guidance)

• Issue was elevated to the FASB staff for a TI

• TI conducted — FASB indicated that forward curve is not required to be used for SASP; invoice price may be best indicator of SASP depending on facts and circumstances

• Issue discussed with RRWG (August) and FinREC (September) with no material changes

• Exposed October 2nd – open for comment until December 1

Copyright © 2017 Deloitte Development LLC. All rights reserved. 66

Implementation update (cont.)

P&U Task Force

P&U Task Force focus area Considerations Developments and status

Alternative revenue programs (“ARP”)

• Separate presentation requirement for ARP revenue (new requirement)

• Proper presentation of revenue when billed through tariff (occurs after initial recognition of ARP revenue)?

• Recycle through ASC 606 revenue or treat as a balance sheet event (e.g., recovery of regulatory asset)?

• Task Force consensus that either approach should be acceptable

• RRWG did not conclude due to concerns about diversity

• Issue was elevated to the FASB staff for a TI

• TI conducted — FASB staff believes both approaches can be supported

• Pick an approach and apply consistently; disclose approach if material to financial statements

• Issue discussed with RRWG (August) and FinREC (September) with no material changes

• Exposed October 2nd – open for comment until December 1

Copyright © 2017 Deloitte Development LLC. All rights reserved. 67

Implementation update (cont.)

P&U Task Force

P&U Task Force focus area

Considerations Developments and status

Collectibility —Regulated utility sales to low-credit–quality customers

• Step 1 of ASC 606 —contract consideration must be probable of collection

• Ability to socialize credit losses through rates (i.e., a “regulatory backstop”)

• Price concession?

• Task Force view that regulatory backstop should be part of overall assessment

• RRWG expressed double-counting concern

• Group of Task Force and other industry representatives met with FASB in March 2017 to discuss collectibility broadly

• Focus on full arsenal of credit mitigation techniques available to regulated utilities and purpose for collectibility screen (ensure transactions are “valid and genuine”)

• FASB agreed with industry analysis and indicated that ASC 606 collectibility screen was generally consistent with current requirement that collectibility be reasonably assured (i.e., should not lead to change in practice)

• Task Force has lowered priority of this item; will consider addressing in the future if warranted based on constituent feedback

Copyright © 2017 Deloitte Development LLC. All rights reserved. 68

Implementation update (cont.)

P&U Task Force

P&U Task Force focus area Considerations Developments and status

Sales of nonfinancial assets

• Replacing real estate sale rules

• Partial sales — unit of account?

• FASB issued ASU 2017-05 in February 2017, which addresses partial sales of nonfinancial assets

• Task Force has dropped the issue and has no further plans to address

This publication contains general information only and is based on the experiences and research of Deloitte practitioners. Deloitte is not, by means of this publication, rendering

business, financial, investment, or other professional advice or services. This publication is not a substitute for such professional advice or services, nor should it be used as a basis for

any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional

advisor. Deloitte, its affiliates, and related entities shall not be responsible for any loss sustained by any person who relies on this publication.

About Deloitte

Deloitte refers to one or more of Deloitte Touche Tohmatsu Limited, a UK private company limited by guarantee (“DTTL”), its network of member firms, and their related entities. DTTL

and each of its member firms are legally separate and independent entities. DTTL (also referred to as “Deloitte Global”) does not provide services to clients. Please see

www.deloitte.com/about for a detailed description of DTTL and its member firms. Please see www.deloitte.com/us/about for a detailed description of the legal structure of Deloitte LLP

and its subsidiaries. Certain services may not be available to attest clients under the rules and regulations of public accounting.

Copyright © 2017 Deloitte Development LLC. All rights reserved.