accounting_for_overheads_and_marginal_costing_1_.ppt

DESCRIPTION

Accounting_for_Overheads_and_Marginal_Costing_1_.pptTRANSCRIPT

Accounting for Overheads and

Marginal costing

By Gayithri KuruppuDept. of Management of Technology

University of Moratuwa

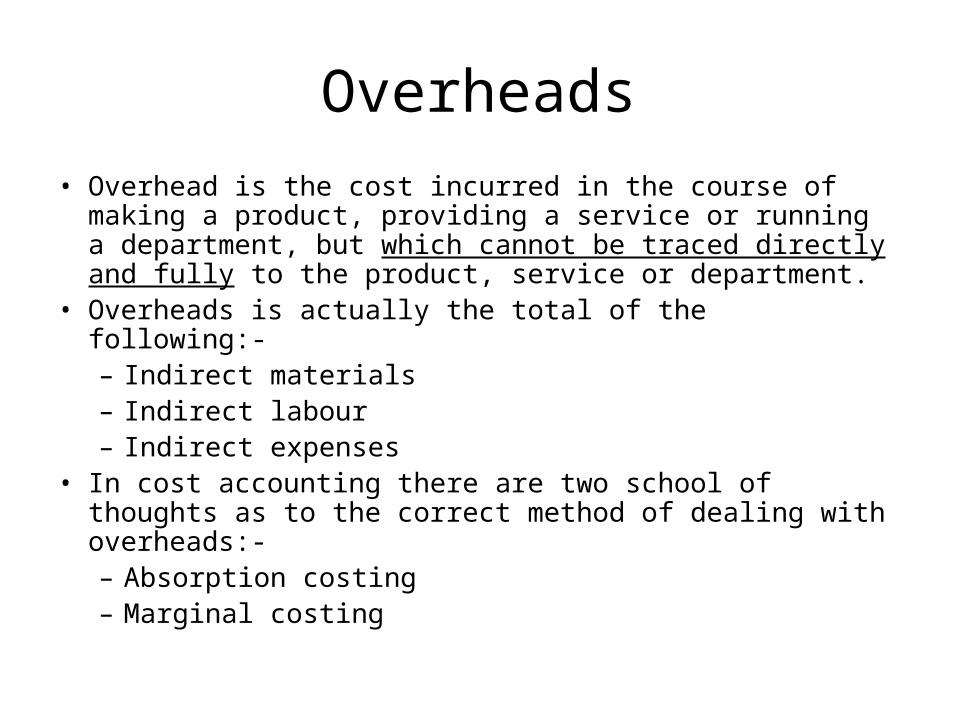

Overheads

• Overhead is the cost incurred in the course of making a product, providing a service or running a department, but which cannot be traced directly and fully to the product, service or department.

• Overheads is actually the total of the following:-– Indirect materials– Indirect labour– Indirect expenses

• In cost accounting there are two school of thoughts as to the correct method of dealing with overheads:-– Absorption costing– Marginal costing

Overheads

There are four categories of overheads.Production/ manufacturing overheadsMarketing/ selling and distribution overheadsResearch and development overheadsAdministration overheads

Allocating Overheads to Products

In general overheads are charged to products through two stages.

1. Overheads are assigned to cost centres

2. Accumulated costs at cost centres allocated to the products

Overhead Cost Allocation & Apportionment

1. Costs are specifically allocated, where they can be ascertained specifically and charged to a particular cost centre.

e.g. The depreciation of machines in production division.

In here, the depreciation of machines in production division, which is considered as a cost centre, can be charged (allocated) to that cost centre.

2. When overhead item is a common cost, the cost item is apportioned to the cost centres that benefit from the cost on an appropriate basis (e.g. machine hours, number of employees etc.).

3. The overheads are to be allocated to service department as well as to production departments.

4. Service department overheads are to be absorbed through jobs or products passing through production department.

So service department costs are re-apportioned to production departments.

Absorption costing stages

The three stages of absorption costing are:-– Allocation– Apportionment– Absorption

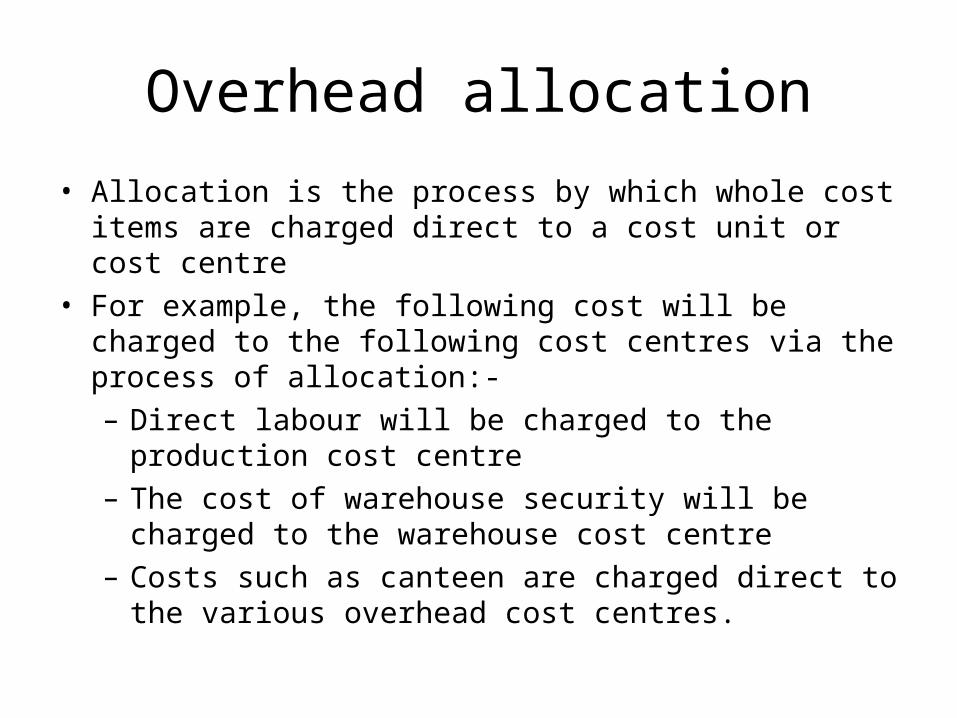

Overhead allocation

• Allocation is the process by which whole cost items are charged direct to a cost unit or cost centre

• For example, the following cost will be charged to the following cost centres via the process of allocation:-– Direct labour will be charged to the production cost

centre– The cost of warehouse security will be charged to the

warehouse cost centre– Costs such as canteen are charged direct to the

various overhead cost centres.

Apportionment of overhead

• Apportionment of overhead is distribution of overheads to more than one cost centre on some equitable basis.

• When the indirect costs are common to different cost centres, these are to be apportioned to the cost centres on an equitable basis. For example, the expenditure on general repair and maintenance pertaining to a department can be allocated to that department but has to be apportioned to various machines (Cost Centres) in the department. If the department is involved in the production of a single product, the whole repair & maintenance of the department may be allocated to the product.

Bases of apportionment

Overhead to which basis apply Basis of apportionment

Rent, rates, heating and light, repairs and depreciation of building

Floor area occupied by each cost centre

Deprecation and insurance of equipment Cost or book value of equipment

Personnel, office, canteen, welfare, wages and costs of offices, first aid

Number of employees, or labour hours worked in each cost centre

Overhead apportionment basis

Basis of apportionment of service cost centers

Service cost centre Possible basis of apportionment

Stores Number of cost value of material requisitions

Maintenance Hours of maintenance work done for each cost centre

Production planning Direct labour hours worked in each production cost centre

Overhead Cost Absorption

1. Determine an absorption rate at which the cost of each cost centre is charged to jobs / products passing through the cost centre.

Absorption Rate= Total cost at the centre Appropriate

basis

2. Overhead costs absorbed by individual products at an absorption rate based on the total expected output or volume of input.

Eg. total labour hours

Eg. Total Overhead of dept = Rs. 10,000, Tota labour hrs = 250

Absorption rate = 10,000/250 = Rs. 40 per labour hr

Example

The Assembly cost center has estimated overheads for period 1 of Rs. 225,000/=. Labour hours are considered the most appropriate basis and it is expected that 9,000 hours will be worked in total during the period.

What is the overhead absorption rate for Assembly?

= 225,000 = Rs 25 per lobour hour

9,000

Example

Job 232 is one of many jobs that pass through the assembly cost center during a period. The only work done on job 232 is assembly work and its direct costs are,•Direct materials 65•Direct labour ( 5 hours @ Rs 18) 90•Total direct cost 155

What is the total production cost of job 232 assuming that the Assembly OAR is Rs 25 per hour as previously calculated?

= DM+DL+OH= total production cost

=65+90+(25*5)=Rs 280

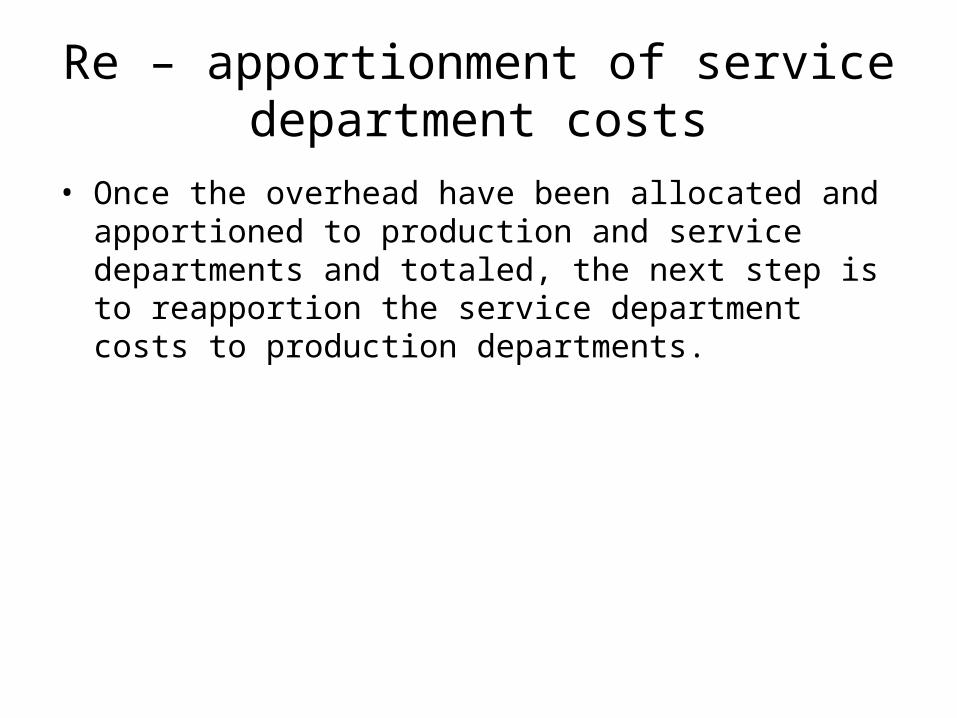

Re – apportionment of service department costs

• Once the overhead have been allocated and apportioned to production and service departments and totaled, the next step is to reapportion the service department costs to production departments.

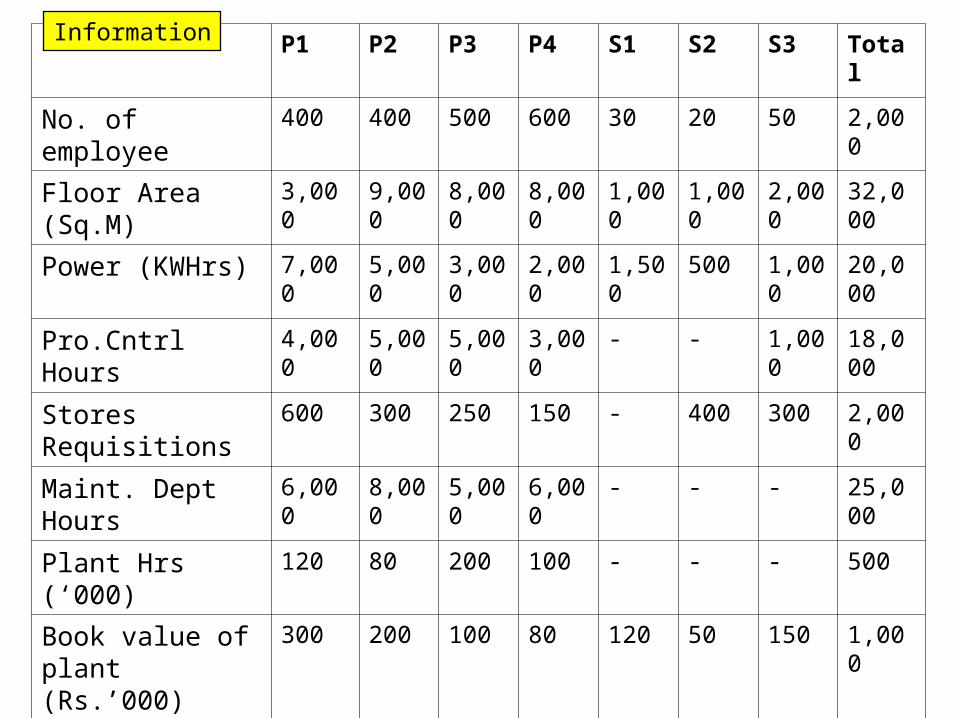

Example ABC Co. Ltd has four production departments P1, P2, P3 and P4 and three service departments S1, S2 and S3.

S1 –stores S2 –production control sectionS3 –maintenance department

Calculate for each production department an appropriate overhead absorption rate per machine hour.

Calculate the total cost of each department.

The annual overheads are as follows:

120Depreciation -Plant

240Depreciation -Building

100Insurance -Plant

160Insurance -Building

80Rent

600Power

200Supervision

2,000Indirect labour

Total (Rs.’000)Cost

Information

Indirect Labour Costs

Cost centres Actual costs

Rs.’000

P1 300

P2 200

P3 500

P4 100

S1 200

S2 300

S3 400

Information

P1 P2 P3 P4 S1 S2 S3 Total

No. of employee 400 400 500 600 30 20 50 2,000

Floor Area (Sq.M) 3,000 9,000 8,000 8,000 1,000 1,000 2,000 32,000

Power (KWHrs) 7,000 5,000 3,000 2,000 1,500 500 1,000 20,000

Pro.Cntrl Hours 4,000 5,000 5,000 3,000 - - 1,000 18,000

Stores Requisitions 600 300 250 150 - 400 300 2,000

Maint. Dept Hours 6,000 8,000 5,000 6,000 - - - 25,000

Plant Hrs (‘000) 120 80 200 100 - - - 500

Book value of plant (Rs.’000)

300 200 100 80 120 50 150 1,000

Information

498343289.4357.6

7825696613500Total

18614.49.6122436120Book valueDepreciation Plant

157.57.5606067.522.5240Floor areaDepreciation Building

152128102030100Book valueInsurance

Plant

105540404515160Floor areaInsurance Building

52.52.5202022.57.580Floor areaRent & Rates

3015456090150210600KWHrPower

52360504040200No. of employee

Supervision

4003002001005002003002000ActualInd. Labour

S3S2S1P4P3P2P1Total Basis Item

Allocation of costs to Production and Service Departments

Calculation Item Basis Total

P1

Ind. Labour Actual 2000 300.0

Supervision No. of Employee

200 (200/2,000)*400 = 40.0

Power KWHr 600 (600/20,000)*7000 = 210.0

Rent & rates Floor area 80 (80/32,000)*3000 = 7.5

Insurance -B Floor area 160 (160/32,000)*3000 = 15.0

Insurance-P Book value 100 (100/1,000)*300 = 30.0

Depreciation-B Floor area 240 (240/32,000)*3000 = 22.5

Depreciation-P Book value 120 (120/1,000)*300 = 36.0

Total 3500 661.0

Reallocation of Service Department Overheads to Production Departments

Item Basis Total

P1 P2 P3 P4 S1 S2 S3

Total costs

3500 661.0 569.0 782.0 357.6 289.4 343.0 498.0

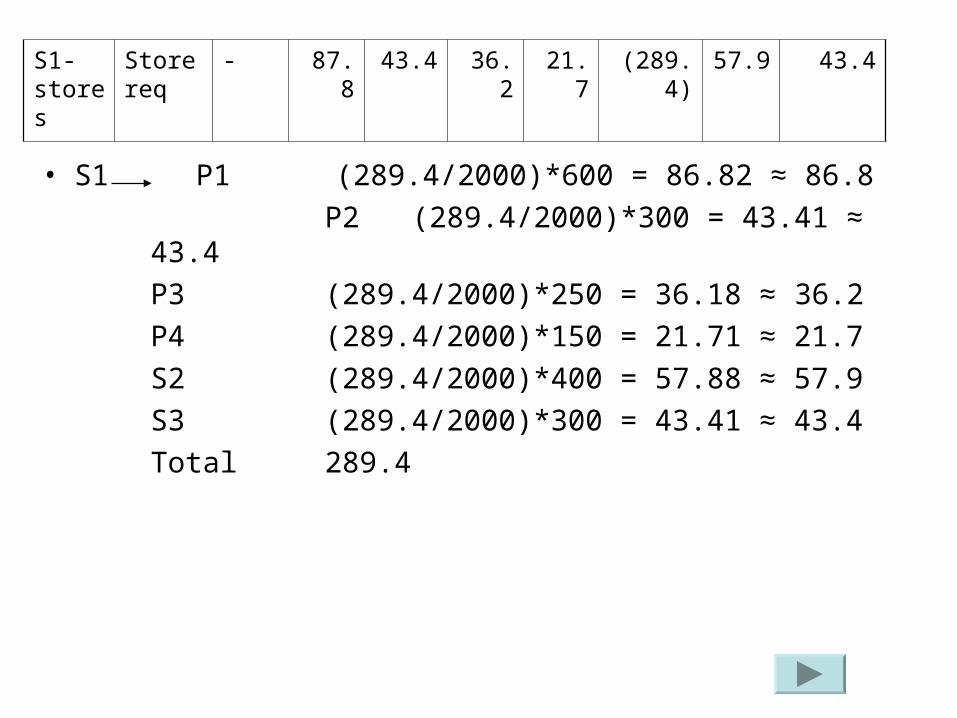

S1-stores

Store req

- 86.8 43.4 36.2 21.7 -289.4 57.9 43.4

S2-Pro Control

Prodn

control3500 748.8

89.1

612.4

111.35

818.2

111.35

379.3

66.8

-

-

400.9

-400.9

541.4

22.3

S3-Maint

Main Hrs

3500 837.9

135.3

723.75

180.4

929.55

112.7

446.1

135.3

-

-

-

-

563.7

-563.7

Total 3500 973.2 904.15 1042.25 581.4 - - -

S1-stores

Store req

- 87.8 43.4 36.2 21.7 (289.4) 57.9 43.4

• S1 P1 (289.4/2000)*600 = 86.82 ≈ 86.8

P2 (289.4/2000)*300 = 43.41 ≈ 43.4

P3 (289.4/2000)*250 = 36.18 ≈ 36.2

P4 (289.4/2000)*150 = 21.71 ≈ 21.7

S2 (289.4/2000)*400 = 57.88 ≈ 57.9

S3 (289.4/2000)*300 = 43.41 ≈ 43.4

Total 289.4

S2-Pro Control

Prodn

control3500 748.8

89.1

612.4

111.35

818.2

111.35

379.3

66.8

-

-

400.9

(400.9)

541.4

22.3

• S2 P1 (400.9/18,000)* 4000= 89.08 ≈ 89.1

P2 (400.9/18,000)* 5000=111.35

P3 (400.9/18,000)* 5000=111.35

P4 (400.9/18,000)* 3000=66.81 ≈ 66.8

S3 (400.9/18,000)* 1000=22.27 ≈ 22.3

S3-Maint

Plant Hrs

3500 837.9

135.3

723.75

180.4

929.55

112.7

446.1

135.3

-

-

-

-

563.7

(563.7)

S3 P1 (563.7/25,000)*6000 =135.288 ≈ 135.3

P2(563.7/25,000)*8000 =180.384 ≈ 180.4

P3(563.7/25,000)*5000 =112.74 ≈ 112.7

P4 (563.7/25,000)*6000 =135.288 ≈ 135.3

Total 563.7

Calculation of appropriate departmental overhead rates

• Based on machine hours

P1 = 973.3/120 = 8.11 per M/C hour

P2 = 904.15/80 = 11.30 per M/C hour

P3 =1042.25/200 = 5.21 per M/C hour

P4 = 581.4/100 = 5.81 per M/C hour

Charging Overhead Rates to Products

Overhead costs in each cost centre should be absorbed by the products, at an absorption rate of each product.

Pro.Dep. Job1(hours) Job2(hours) Job3(hours)

P1 3 12 1.5

P2 2.5 0 4

P3 0 5 10

P4 5 0 3

• Then, based on the production hours the overhead costs chargeable are as follows:

• Job 1 = 3*8.11+2.5*11.3+5*5.81 = 81.63

• Job 2 = 12*8.11+5*5.21 = 123.37

• Job 3 = 1.5*8.11+4*11.3+10*5.21+3*5.81 =

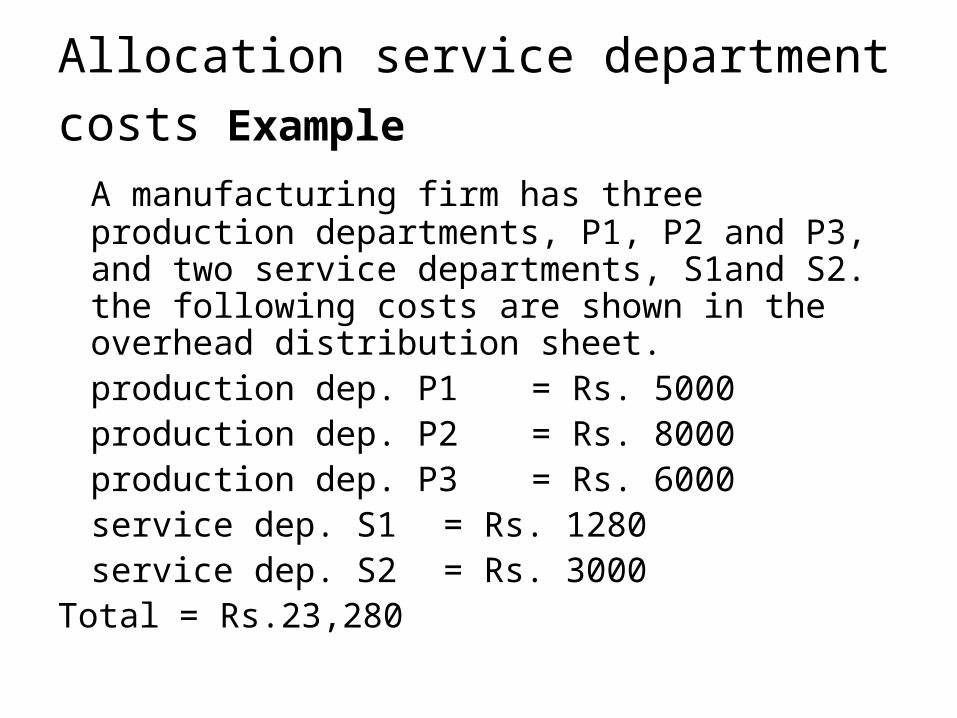

Allocation service department costs

Example A manufacturing firm has three production departments, P1, P2 and P3, and two service departments, S1and S2. the following costs are shown in the overhead distribution sheet.production dep. P1 = Rs. 5000production dep. P2 = Rs. 8000production dep. P3 = Rs. 6000service dep. S1 = Rs. 1280service dep. S2 = Rs. 3000

Total = Rs.23,280

• The costs of the two service departments S1 and S2 are to be re-apportioned to production departments using the following basis.

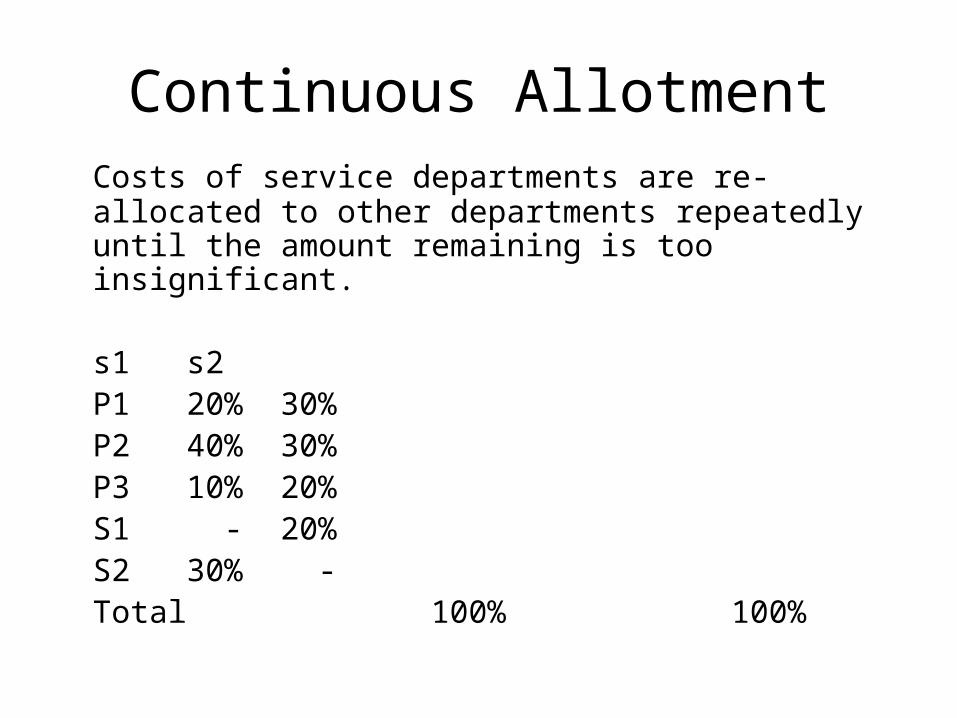

S1 S2P1 20% 30%P2 40% 30%P3 10% 20%S1 - 20%S2 30% -Total 100% 100%

• There are 3 basic methods of allocating service department costs.

1. Continuous Allotment

2. Simultaneous Equation method

3. Specified order of Re-Allocation

Continuous AllotmentCosts of service departments are re-allocated to other departments repeatedly until the amount remaining is too insignificant.

s1 s2P1 20% 30%P2 40% 30%P3 10% 20%S1 - 20%S2 30% -Total 100% 100%

Total P1 P2 P3 S1 S2

Cost before re-allocation

Dept S1

Dept. S2

Total

23280

2380

5000

256

1015

135

61

8

3.6

4

6479

8000

512

1015

271

62

16

3.6

4

9880

6000

128

677

68

40

4

2.4

3

6920

1280

(1280)

677

(677)

40

(40)

2.4

-

3000

384

(3384)

203

(203)

12

(12)

-

Simultaneous equation method

X=total cost of S1 after receiving 20% cost of S2

Y=total cost of S2 after receiving 30% cost of S1

X=1280+0.2Y

Y=3000+0.3X

By solving two equation above,

X=2000 and Y=3600

As above Total P1 P2 P3

Cost before re-allocation

19000 5000 8000 6000

Dept S1 2000 1400* 400* 800* 200*

Dept S2 3600 2880 1080 1080 720

Total 23280 6480 9880 6920

(2000/100)*70

=1400

(1400/70)*20

=400

(1400/70)*40

=800

(1400/70)*10

=200

Specified order of Re-allocation

• Assume that service dept. costs are first allocated to S1 and then to S2.

S1 S2

P1 20% 37.5%

P2 40% 37.5%

P3 10% 25.0%

S1 - -

S2 30% -

Total 100% 100%

30*(100/80)

30*(100/80)

20*(100/80)

Total P1 P2 P3 S1 S2

Cost before re-allocation

23280 5000 8000 6000 1280 3000

Dept S1 256 512 128 (1280) 384

Dept. S2 1269 1269 846 - (3384)

Total 2380 6525 9781 6974 - -

(1280/100)*20

=256

(1280/100)*40

=512

(1280/100)*10

=128

(1280) (1280/100)*30

=384

Choice of Overhead Rates

• The overhead rate is calculated based on several alternative bases. The basis chosen should be suitable for the cost centre activities.

Choice of Overhead Rates

• Direct labour hour rate

= (Total overhead)/(Direct labour hours)

• Machine hour rate

=(Total overhead)/(Machine hours)

• Direct material cost rate

=(Total over head/Direct material cost)

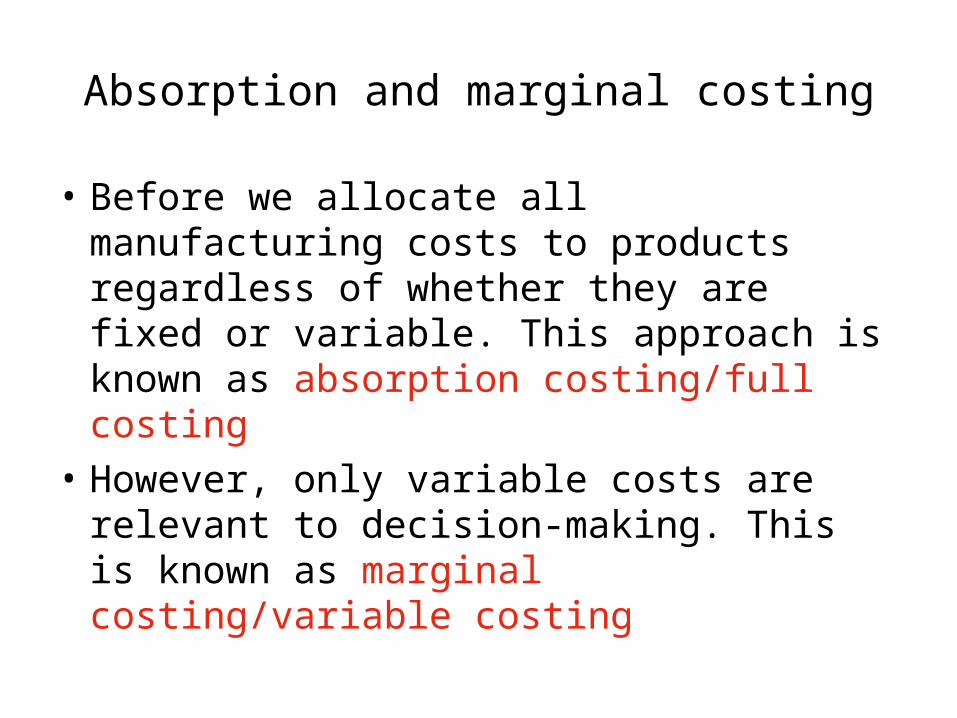

Absorption and marginal costing

• Before we allocate all manufacturing costs to products regardless of whether they are fixed or variable. This approach is known as absorption costing/full costing

• However, only variable costs are relevant to decision-making. This is known as marginal costing/variable costing

Practical reasons for using absorption costing

Inventory in hand must be valued for two reasons:-• For the closing inventory figure in the statement of financial position• For the cost of sales figure in the statement of comprehensive

income• In absorption costing, closing inventory is valued at fully absorbed

factory costs.

Many companies attempt to fix selling prices by calculating the full cost of production or sales of each product, and then adding a margin for profit. Without using absorption costing, a full cost is difficult to ascertain.

If a company sells more than one product, it will be difficult to judge how profitable each individual product is, unless overhead costs are shared on a fair basis and charged to the cost of sales of each product

Definition

• Absorption costingIt is costing system which treats all manufacturing costs

including both the fixed and variable costs as product costs

• Marginal costingIt is a costing system which treats only the variable

manufacturing costs as product costs. The fixed manufacturing overheads are regarded as period cost

Trading and profit and loss account

Absorption costing Marginal costing

$$

Sales X Sales X

Less: Cost of goods sold X Less: Variable cost of

Goods sold X

Gross profit X Product contribution margin X

Less: Expenses Less: variable non- manufacturing

• Selling expenses X expenses

• Admin. expenses X Variable selling expenses X

• Other expenses X X Variable admin. expenses X

Other variable expenses X

Total contribution expenses X

Less: Expenses

Fixed selling expenses X

Fixed admin. expenses X

Other fixed expenses X

Net Profit X Net Profit X

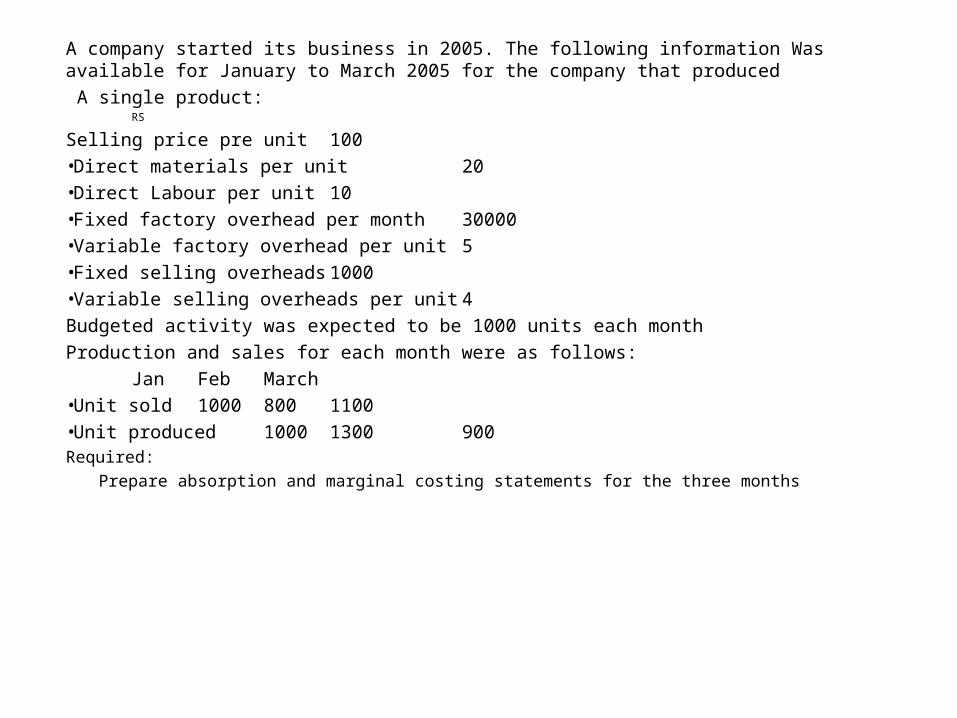

A company started its business in 2005. The following information Was available for January to March 2005 for the company that produced

A single product:RS

Selling price pre unit 100•Direct materials per unit 20•Direct Labour per unit 10•Fixed factory overhead per month 30000•Variable factory overhead per unit 5•Fixed selling overheads 1000•Variable selling overheads per unit 4

Budgeted activity was expected to be 1000 units each month

Production and sales for each month were as follows:

Jan Feb March•Unit sold 1000 800 1100•Unit produced 1000 1300 900Required:

Prepare absorption and marginal costing statements for the three months

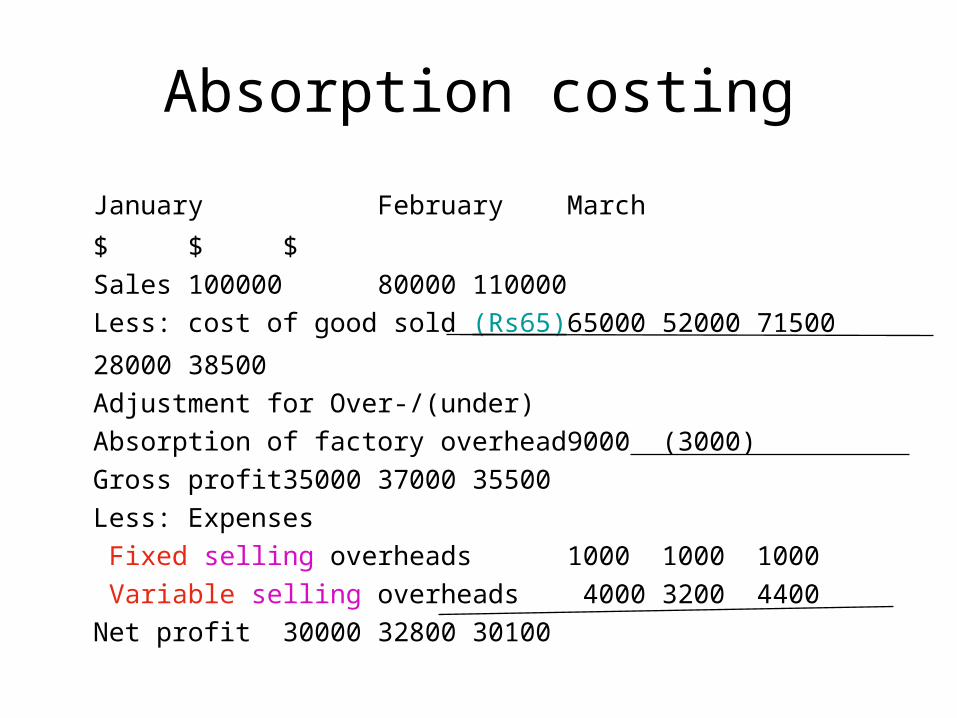

Absorption costing

January FebruaryMarch

$ $ $

Sales 100000 80000 110000

Less: cost of good sold (Rs65)65000 5200071500

2800038500

Adjustment for Over-/(under)

Absorption of factory overhead 9000 (3000)

Gross profit 35000 3700035500

Less: Expenses

Fixed selling overheads 1000 1000 1000

Variable selling overheads 4000 3200 4400

Net profit 30000 3280030100

Marginal costingJanuary February

March

$ $ $

Sales 100000 80000 110000

Less: Variable cost of good

sold ($35) 35000 28000 38500

Product contribution margin 65000 52000 71500

Less: Variable selling overhead4000 3200 4400

Total contribution margin 61000 48800 67100

Less: Fixed Expenses

Fixed factory overhead 30000 30000 30000

Fixed selling overheads 1000 1000 1000

Net profit 30000 32800 30100

Wk1:Standard fixed overhead rate

= Budgeted total fixed factory overheads Budgeted number of units produced

= $30000 1000 units

= $30 units

Wk 2:

Production cost per unit under absorption costing:

Direct materials20

Direct labour10

Fixed factory overhead absorbed 30

Variable factory overheads 5

65

Wk 3:(Under-)/Over-absorption of fixed factory overheads:

January February March$ $ $

Fixed overhead 30000 39000 27000Fixed overheads incurred 30000 30000 30000

0 9000 (3000)

Wk 4:Variable production cost per unit under marginal costing:

$Direct materials 20Direct labour 10Variable factory overhead 5

35

1000*$30 1300*$30 900*$30

No fixed factory overhead

Difference between absorption and marginal costingAbsorption costing Marginal costing

Treatment for fixed manufacturing overheads

Fixed manufacturing overheads are treated as product costing. It is believed that products cannot be produced without the resources provided by fixed manufacturing overheads

Fixed manufacturing overhead are treated as period costs. It is believed that only the variable costs are relevant to decision-making.

Fixed manufacturing overheads will be incurred regardless there is production or not.

Value of closing stock High value of closing stock will be obtained as some factory overheads are included as product costs and carried forward as closing stock

Lower value of closing stock that included the variable cost only

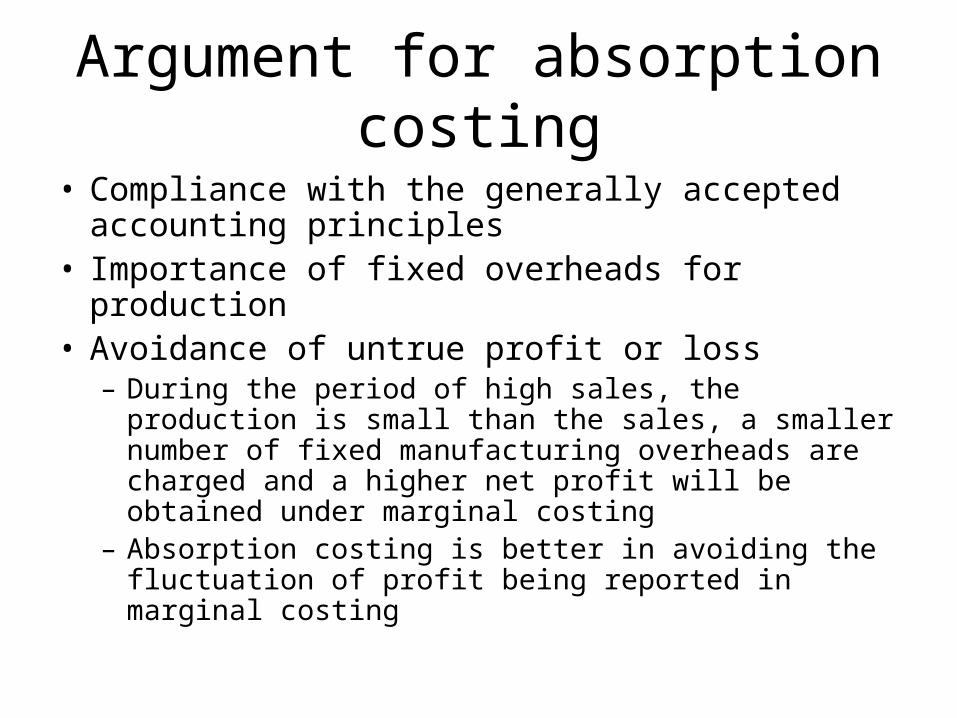

Argument for absorption costing

• Compliance with the generally accepted accounting principles

• Importance of fixed overheads for production• Avoidance of untrue profit or loss

– During the period of high sales, the production is small than the sales, a smaller number of fixed manufacturing overheads are charged and a higher net profit will be obtained under marginal costing

– Absorption costing is better in avoiding the fluctuation of profit being reported in marginal costing

Arguments for marginal costing

• More relevance to decision-making• Avoidance of profit manipulation

– Marginal costing can avoid profit manipulation by adjusting the stock level

• Consideration given to fixed cost– In fact, marginal costing does not ignore fixed costs in

setting the selling price. On the contrary, it provides useful information for break-even analysis that indicates whether fixed costs can be converted with the change in sales volume