accounts payable review

TRANSCRIPT

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 1/36

Accounts Payable Review

<Insert Date>

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 2/36

2 Source: www.knowledgeleader.com Sample Internal Audit Report

Table of Contents

Obectives! Sco"e # Procedures Performed 2

$%ecutive Summary 3

&etailed 'ssues # Observations 5

A""endices

A""endi% A: (eneral )ackground 20

A""endi% ): 'nternal Control Scorecard 22

A""endi% C: )est Practices Scorecard 23

A""endi% &: )est Practices &etails 24

A""endi% $: Testing Summary 29

A""endi% *: Performance +easures 32

A""endi% (: Process *lowc,arts 33

This report provides management with information about the condition of riss and interna! contro!s at a specific point intime" #uture changes in environmenta! factors and actions b$ personne! wi!! impact these riss and interna! contro!s in wa$sthat this report cannot anticipate"

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 3/36

- Source: www.knowledgeleader.com Sample Internal Audit Report

Obectives! Sco"e # Procedures Performed

&etermine if key financial and business controls e%ist and are o"erating effectively. Assess t,e o"erating efficiency of t,e "rocess.

Com"are Com"any/s "ractices to 0)est Practices!1 including "erformance measures.

Review "erformance measures used to monitor and im"rove t,e "rocess.

Assess com"liance wit, a""licable cor"orate "olicies and "rocedures.

'dentify o""ortunities for internal control and "rocess im"rovements.

Objectives

T,e sco"e of t,is audit includes a review of Accounts Payable "rocesses! focusing on t,e following areas:

'nvoice recei"t.

'nvoice a""roval "rocess.

+atc,ing of invoice to "urc,ase order and to receiving information.

Prioritiation of "ayments.

3se of early "ayment discounts.

Payment "rocessing. Record retention.

Reconciliations between general ledger! AP sub4ledger! and bank accounts.

Scope

'nterviewed key management and "ersonnel regarding t,e accounts "ayable "rocesses.

Reviewed e%isting documentation of relevant "olicies and "rocedures.

Summary of Procedures Performed

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 4/36

5 Source: www.knowledgeleader.com Sample Internal Audit Report

Obectives! Sco"e # Procedures Performed

Obtained an understanding of "rocedures and internal controls. &iscussed e%isting management "lans to im"rove o"erations or internal controls.

Performed analysis on accounts "ayable transactions for t,e "eriod 6+ont,7 8888 t,roug, 6+ont,7 8888.

&ocumented t,e accounts "ayable "rocess t,roug, ,ig,4level "rocess ma"s.

$valuated t,e effectiveness and efficiency of business "rocesses against 0)est Practices.1

Summaried observations and management action "lans.

Summary of Procedures Performed

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 5/36

9 Source: www.knowledgeleader.com Sample Internal Audit Report

$%ecutive Summary

Interna! audit reviewed the %ccounts &a$ab!e function in '(onth ) *ear+" The ob,ectives of this review were toobtain an understanding of the e$ administrative) operationa! and financia! processes re!ating to these functions)

eva!uate the ade-uac$ and effectiveness of the associated interna! contro!s and to identif$ opportunities for process improvements"

.vera!!) the contro! environment was in need of improvement" %t the time of our review) (anagement had identifiedweanesses in contro!s and had begun to imp!ement p!ans to improve the contro! environment as we!! as theefficienc$ and business effectiveness of the process" These p!ans are summari/ed on page " 1e noted someadditiona! areas where contro!s cou!d be enhanced or added these are summari/ed be!ow"

See the Detailed Issues & Observations section of this report (pages ! "#$ for a detailed discussion of all issues

identified in this revie% and the management implementation plan to address each issue

Observations'Issues Priority See Page iming

.Purc,ase re;uisition a""roval "rocess is not consistently followed 68 of 88 a""rovals e%aminedwere com"leted by "ersonnel not aut,oried in t,e 0A""roval <ist17. =

>!8888

2.Review of "urc,asing card transactions s,ould be strengt,ened 6we noted numerouse%ce"tions in our testing7. ?

>2!8888

-.'nvoices s,ould be recorded and "rocessed on a timely basis 6we noted numerous e%ce"tionsin our testing7. @

>!8888

5.ot all recei"ts to su""ort reimbursement of T#$ e%"enses were submitted as re;uired bycor"orate "olicy 68 re"orts out of 88 tested did not contain all documentation7. B

>2!8888

9.Password security for c,eck "rinting a""lications does not conform to t,e Com"uter Security!

Audit and Control Policy. >5!8888

.3nit A/s "etty cas, 6D8!8887 balance is larger t,an necessary 6management subse;uentlydecided to eliminate t,e fund7 2

>5!8888

)o% *edium +ighPriority,

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 6/36

Source: www.knowledgeleader.com Sample Internal Audit Report

$%ecutive Summary 6Contd.7

Observations'Issues Priority See Page iming

-.ISI/0 *A/A0-*-/ P)A/S

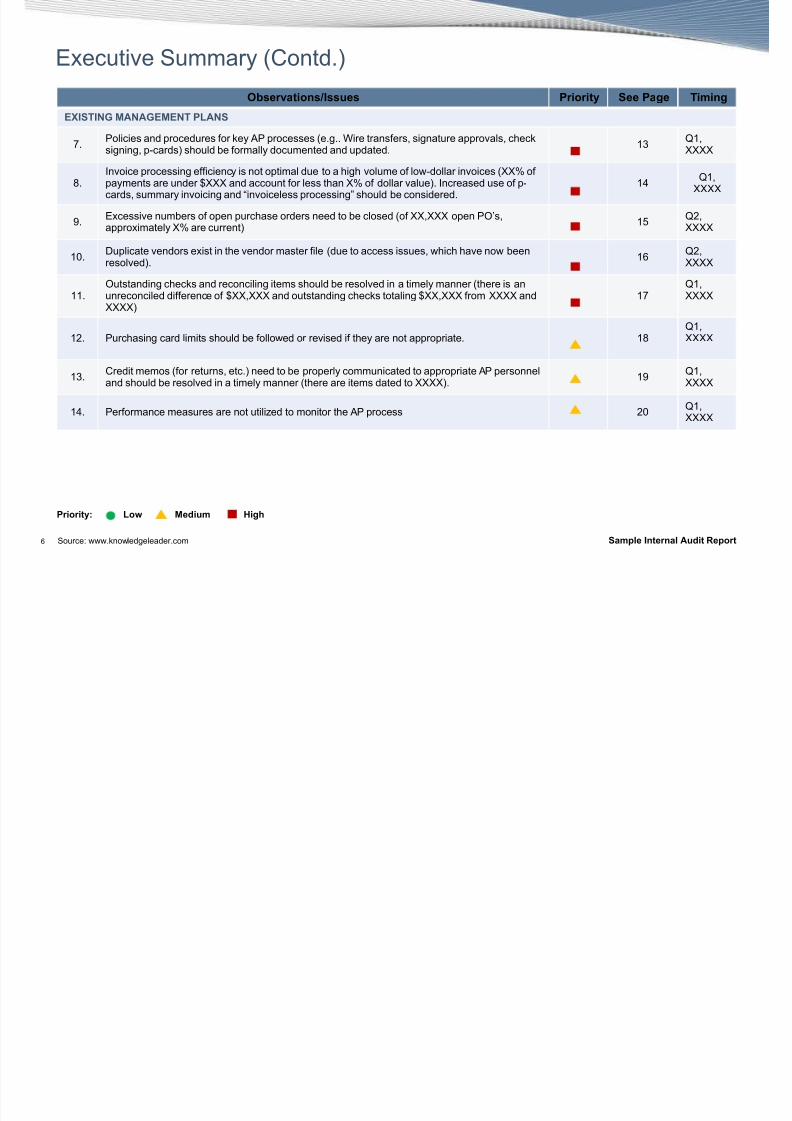

=.Policies and "rocedures for key AP "rocesses 6e.g.. Eire transfers! signature a""rovals! c,ecksigning! "4cards7 s,ould be formally documented and u"dated.

->!8888

?.'nvoice "rocessing efficiency is not o"timal due to a ,ig, volume of low4dollar invoices 688F of"ayments are under D888 and account for less t,an 8F of dollar value7. 'ncreased use of "4cards! summary invoicing and 0invoiceless "rocessing1 s,ould be considered.

5>!

8888

@.$%cessive numbers of o"en "urc,ase orders need to be closed 6of 88!888 o"en PO/s!a""ro%imately 8F are current7

9>2!8888

B.

&u"licate vendors e%ist in t,e vendor master file 6due to access issues! w,ic, ,ave now been

resolved7.

>2!

8888

.Outstanding c,ecks and reconciling items s,ould be resolved in a timely manner 6t,ere is anunreconciled difference of D88!888 and outstanding c,ecks totaling D88!888 from 8888 and88887

=>!8888

2. Purc,asing card limits s,ould be followed or revised if t,ey are not a""ro"riate. ?>!8888

-.Credit memos 6for returns! etc.7 need to be "ro"erly communicated to a""ro"riate AP "ersonneland s,ould be resolved in a timely manner 6t,ere are items dated to 88887.

@>!8888

5. Performance measures are not utilied to monitor t,e AP "rocess 2B>!8888

)o% *edium +ighPriority,

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 7/36= Source: www.knowledgeleader.com Sample Internal Audit Report

&etailed Observations and 'ssues

Observations'Issues *anagement Action Plan O%ner'iming

1 Purchase re2uisition approval process is notconsistently follo%edPurc,asing a""roval t,res,olds are aut,oried bymanagement and documented in t,e A""roval Signature<ist. T,ese t,res,olds are set u" in t,e System by localsystems "ersonnel. A""ro"riate level of a""roval must beobtained in t,e system to generate a "urc,ase order 6PO7. Att,e "rocessing "ayment stage! AP "ersonnel "erformmatc,ing and rely on t,e front end controls t,at a""rovals,ave been obtained for t,e "urc,ases.

Of t,e 88 "urc,ase re;uisitions we tested we noted t,e

following variances from "olicy:G'nsert numberH 68F7 of t,e "urc,ase re;uisitions wereaut,oried by "ersonnel w,ose aut,oriation limits were notcontained in t,e A""roval Signature <ist.

G'nsert numberH 68F7 of t,e "urc,ase re;uisitions werea""roved by "ersonnel w,ose a""roval limit was below t,einvoice amount. T,e limits contained in t,e System were notconsistent wit, documented and a""roved t,res,olds ascontained in t,e A""roval Signature <ist.

3usiness Impact, 'nvoices mig,t be "rocessed and "aid

wit,out "ro"er aut,oriation. C,ecks mig,t be issued wit,out"ro"erIaccurate a""roval.

A. +anagement s,ould formalie Signature Aut,ority"olicy and t,e A""roval Signature <ist to clearlydefine a""rovals re;uired for different ty"es of"urc,ases. (See Observation 7).

). +anagement s,ould ensure local systems"ersonnel are granting systems a""roval limitsaccording to t,ose formally aut,oried.

C. +anagement s,ould "erform a systems audit toreconcile a""roval t,res,olds between t,e

A""roval Signature <ist and limits set u" in t,eSystem.

6Owner ame7>! 8888

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 8/36? Source: www.knowledgeleader.com Sample Internal Audit Report

&etailed Observations and 'ssues

Observations'Issues *anagement Action Plan O%ner'iming

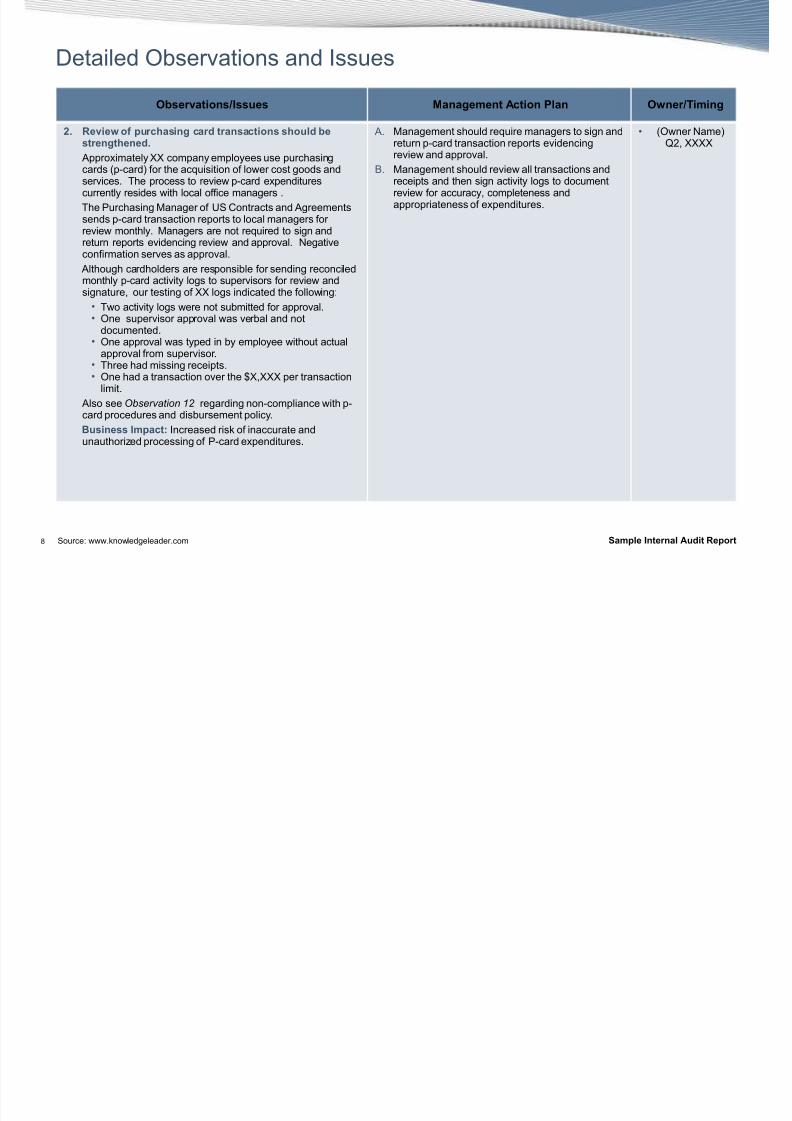

" Revie% of purchasing card transactions should bestrengthened

A""ro%imately 88 com"any em"loyees use "urc,asingcards 6"4card7 for t,e ac;uisition of lower cost goods andservices. T,e "rocess to review "4card e%"enditurescurrently resides wit, local office managers .

T,e Purc,asing +anager of 3S Contracts and Agreementssends "4card transaction re"orts to local managers forreview mont,ly. +anagers are not re;uired to sign andreturn re"orts evidencing review and a""roval. egativeconfirmation serves as a""roval.

Alt,oug, card,olders are res"onsible for sending reconciledmont,ly "4card activity logs to su"ervisors for review andsignature! our testing of 88 logs indicated t,e following:

• Two activity logs were not submitted for a""roval.• One su"ervisor a""roval was verbal and not

documented.• One a""roval was ty"ed in by em"loyee wit,out actual

a""roval from su"ervisor.• T,ree ,ad missing recei"ts.• One ,ad a transaction over t,e D8!888 "er transaction

limit. Also see Observation 12 regarding non4com"liance wit, "4card "rocedures and disbursement "olicy.

3usiness Impact, 'ncreased risk of inaccurate andunaut,oried "rocessing of P4card e%"enditures.

A. +anagement s,ould re;uire managers to sign andreturn "4card transaction re"orts evidencingreview and a""roval.

). +anagement s,ould review all transactions andrecei"ts and t,en sign activity logs to documentreview for accuracy! com"leteness anda""ro"riateness of e%"enditures.

6Owner ame7>2! 8888

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 9/36@ Source: www.knowledgeleader.com Sample Internal Audit Report

&etailed Observations and 'ssues

Observations'Issues *anagement Action Plan O%ner'iming

4 Invoices should be recorded and processed on a timelybasis

'nvoices are received at local sites for matc,ing andvouc,ing for disbursement.

&uring our testing of five vendor statements! we noted t,atin one vendor statement! 88 of t,e 88 outstanding invoices6dated G'nsert &ateH! 8888 t,roug, G'nsert &ateH! 88887were not recorded in t,e AP system as of G'nsert &ateH!8888. &iscussions wit, AP "ersonnel indicated invoices,ave been received but not "rocessed.

Also! analysis of timeliness of "ayments 6see "age 97indicated a""ro%imately 8F of "ayments generated betweenG'nsert +ont,sH 8888 were "aid after 88 days of invoicedate. &iscussions indicated t,ese invoices related toinventory "urc,ases w,ere buyers ,ave been working wit,vendors to resolve dis"utes.

3usiness Impact, Risk of recorded liability beingunderstated. Risk of forgone o""ortunity for early "aymentdiscounts.

A. AP "ersonnel s,ould ensure all invoices and"ayments are "rocessed timely.

6Owner ame7>! 8888

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 10/36B Source: www.knowledgeleader.com Sample Internal Audit Report

&etailed Observations and 'ssues

Observations'Issues *anagement Action Plan O%ner'iming

5 /ot all of the receipts to support &-reimbursement of e6penses %ere submitted asre2uired by corporate policyravel and -ntertainment (&-$ -6penses

Travel Policy 6*inance Policy 887 states t,e com"any/sre;uirements for t,e submission of su""ortingdocumentation and recei"ts. 't also re;uires em"loyeesto file T#$ e%"ense re"orts no later t,an 88 days aftercom"letion of eac, tri".

'n our testing of 88 e%"ense re"orts! we noted t,reee%"ense re"orts t,at did not contain all re;uired recei"ts.

Petty 7ash -6penses As of Se"tember 8888! only 88 "lants ,ave "etty cas,.Personnel at sites wit, no "etty cas, are re;uestingreimbursements via e%"ense re"orts. T,e current"ractice for e%"ense re"orts is to review for recei"ts ifre"ort total 6e%cluding airfare and mileage7 e%ceedsD88. +anagement s,ould revise t,e current "olicy and"rocedures to ensure recei"ts are submitted! "ro"era""rovals are obtained! and ade;uate review is"erformed for "etty cas, items submitted via e%"ensere"orts.

3usiness Impact, 3naut,oried e%"ensereimbursements. Potential for reimbursement of non4business e%"enses. Potential ta%4related issues due tolack of documentation.

A. T,e $%"ense Re"ort Processor s,ould reviewe%"ense re"orts for all re;uired recei"ts.

). +anagement s,ould determine a""ro"riate"rocedures for reviewing "etty cas, itemssubmitted via e%"ense re"orts. ew "roceduress,ould be documented in t,e formal "olicy.

6Owner ame7>2! 8888

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 11/36 Source: www.knowledgeleader.com Sample Internal Audit Report

&etailed Observations and 'ssues

Observations'Issues *anagement Action Plan O%ner'iming

8 Pass%ord security for chec9 printing applications doesnot conform to the 7omputer Security: Audit and 7ontrolPolicy

T,e current Com"uter Security! Audit and Control Policyre;uires uni;ue user '&s and "asswords. Passwords are tobe a minimum of si% c,aracters and must be a combinationof al",a and numeric c,aracters. Passwords are to bec,anged at least every 88 days.

T,e AP de"artment uses 6-rd Party Software7 for "rinting APc,ecks. Two users of t,e AP grou" s,are a user '& and"assword. T,e "assword is not re;uired to be c,anged on aregular basis.

T,e $%"ense Re"ort Processor uses 6- rd Party Software7 for"rinting e%"ense c,ecks. T,e "assword is not re;uired to bec,anged on a regular basis.

3usiness Impact, <ack of individual accountability. Risk forunaut,oried access to 6-rd Party Software7. Potentialfinancial losses due to AP c,eck frauds.

A. Administrators for t,e a""lications s,oulddetermine if t,e software ,as t,e ca"ability ofre;uired "assword c,anges.

). +anagement s,ould ensure com"liance wit,cor"orate "olicy or ot,erwise document and obtaina""roval for e%ce"tions.

6Owner ame7>5! 8888

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 12/36

2 Source: www.knowledgeleader.com Sample Internal Audit Report

&etailed Observations and 'ssues

Observations'Issues *anagement Action Plan O%ner'iming

; <nit A=s petty cash balance appears to be larger thannecessary

As of G'nsert +ont,H 8888! only five units ,ave "etty cas,. All locations ,ave between D888 and D8!888 in t,eir "ettycas, fund wit, t,e e%ce"tion 3nit A. &iscussions wit, t,e

Accounting Assistant indicated 3nit A ,as D88!888 in "ettycas,. T,is amount a""ears to be e%cessive w,en com"aredto ot,er locations. Additionally! t,e Accounting Assistantindicated t,at D888 to D88!888 would be sufficient formont,ly "etty cas, needs.

3usiness Impact, 'ncreased e%"osure of cas, t,eft

A. After management/s assessment of t,e need for a"etty cas, fund in 3nit A! a decision was made toeliminate t,e "etty cas, fund by 6+ont,! 88887

6Owner ame7>5! 8888

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 13/36

- Source: www.knowledgeleader.com Sample Internal Audit Report

&etailed Observations and 'ssues

Observations'Issues -6isting *anagement Plan O%ner'iming

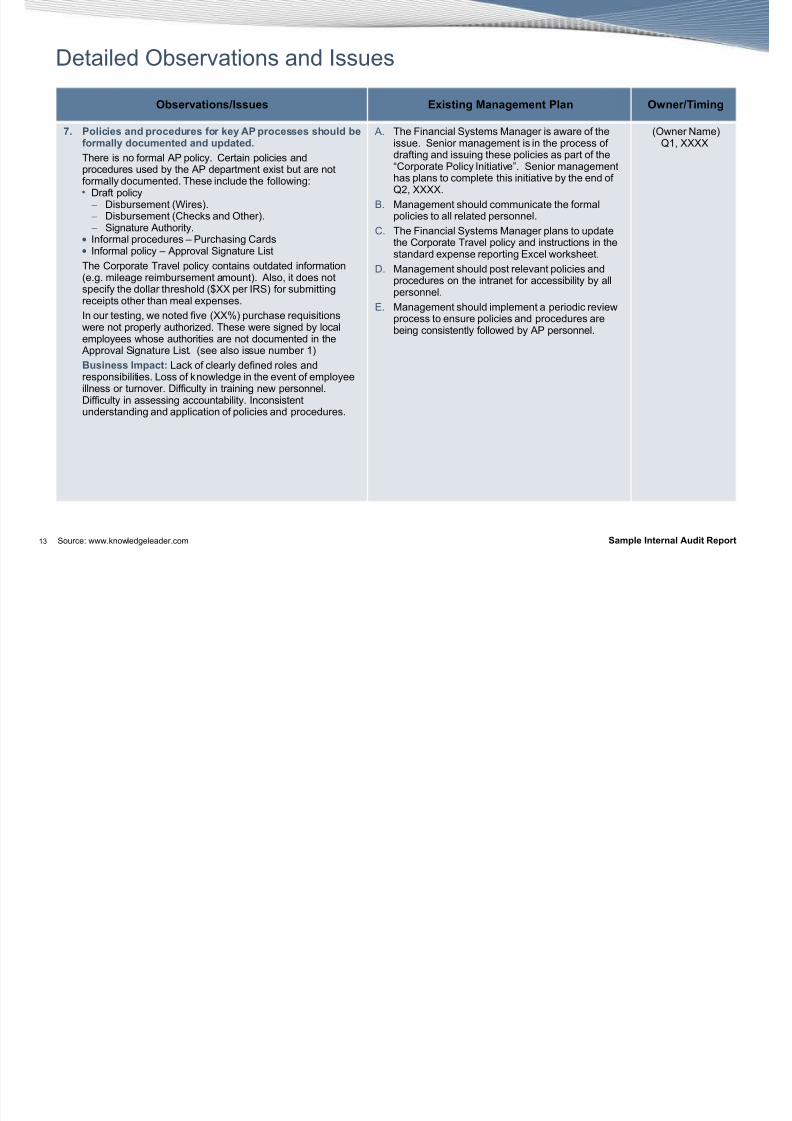

Policies and procedures for 9ey AP processes should beformally documented and updated

T,ere is no formal AP "olicy. Certain "olicies and"rocedures used by t,e AP de"artment e%ist but are notformally documented. T,ese include t,e following:• &raft "olicy− &isbursement 6Eires7.− &isbursement 6C,ecks and Ot,er7.− Signature Aut,ority.

• 'nformal "rocedures J Purc,asing Cards• 'nformal "olicy J A""roval Signature <ist

T,e Cor"orate Travel "olicy contains outdated information6e.g. mileage reimbursement amount7. Also! it does nots"ecify t,e dollar t,res,old 6D88 "er 'RS7 for submittingrecei"ts ot,er t,an meal e%"enses.

'n our testing! we noted five 688F7 "urc,ase re;uisitionswere not "ro"erly aut,oried. T,ese were signed by localem"loyees w,ose aut,orities are not documented in t,e

A""roval Signature <ist. 6see also issue number 7

3usiness Impact, <ack of clearly defined roles andres"onsibilities. <oss of knowledge in t,e event of em"loyee

illness or turnover. &ifficulty in training new "ersonnel.&ifficulty in assessing accountability. 'nconsistentunderstanding and a""lication of "olicies and "rocedures.

A. T,e *inancial Systems +anager is aware of t,eissue. Senior management is in t,e "rocess ofdrafting and issuing t,ese "olicies as "art of t,e0Cor"orate Policy 'nitiative1. Senior management,as "lans to com"lete t,is initiative by t,e end of>2! 8888.

). +anagement s,ould communicate t,e formal"olicies to all related "ersonnel.

C. T,e *inancial Systems +anager "lans to u"datet,e Cor"orate Travel "olicy and instructions in t,estandard e%"ense re"orting $%cel works,eet.

&. +anagement s,ould "ost relevant "olicies and"rocedures on t,e intranet for accessibility by all"ersonnel.

$. +anagement s,ould im"lement a "eriodic review"rocess to ensure "olicies and "rocedures arebeing consistently followed by AP "ersonnel.

6Owner ame7>! 8888

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 14/36

5 Source: www.knowledgeleader.com Sample Internal Audit Report

&etailed Observations and 'ssues

-6isting *anagement Observations'Issues -6isting *anagement Plan O%ner'iming

> Invoice processing efficiency is not optimal due to ahigh volume of lo%!dollar invoices

'n t,e "eriod of Kuly t,roug, G'nsert +ont,H 8888! 88F ofall "ayments "rocessed were less t,an D8!888! butaccounted for less t,an 8F of t,e total dollar value ofinvoices. See a""endi% 0A1 for t,e results of t,e dataanalysis.

A""ro%imately 888 em"loyees use "urc,asing cards 6"4cards7. T,e use of "4cards is a "roven best "ractice t,at ,asbeen successfully used to reduce costs and cycle times forlow dollar transactions. O""ortunities e%ist to increase t,e

efficiency of t,e "rocurement function by e%"anding t,eutiliation of "4cards andIor re;uesting summary invoicingfrom vendors wit, w,om a large volume of transactionsoccur at low dollar amounts.

3usiness Impact, 'nefficient "rocessing. 'ncreased"rocessing costs related to issuing! reviewing and clearingc,ecks.

A. +anagement is aware of t,e issue and "lans toincrease t,e use of "4cards to decrease volume oflow4dollar invoices.

). Consider benc,marking "erformance by;uantifying t,e "ercentage of items or dollarse%"ensed to "4cards and volumeIvalue of invoices"rocessed.

C. Consider increasing t,e use of summary invoicingwit, key vendors on a larger scale in order tocombine numerous invoices for efficient "ayment"ur"oses.

&. Consider im"lementing 0invoiceless "rocessing1wit, key vendors. Payment will be based u"onrecei"t of goods and merc,andise at agreed4u"on"rices rat,er t,an recei"t of an invoice.'nvoiceless "rocessing re;uires e%tensiveem"loyee training! u"front system edits! accurate"urc,ase order and receiving "rocesses and cleare%em"tion re"orting. T,e benefits could be lower"ayable transaction costs! sim"lified materialcontrols! fewer AP "ersonnel "er 88 million ofdisbursements and im"roved control over AP.

6Owner ame7>! 8888

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 15/36

9 Source: www.knowledgeleader.com Sample Internal Audit Report

&etailed Observations and 'ssues

-6isting *anagement Observations'Issues -6isting *anagement Plan O%ner'iming

? -6cessive numbers of open purchase orders need to beclosed

Review of o"en commitments re"ort indicate e%cessive"urc,ase orders are currently o"en. Some of t,ese dateback to 8888.

&iscussions wit, t,e *inancial Systems +anager indicated,e is aware of t,e issue and t,ere a""ears to be 88!888o"en POs! of w,ic, only a""ro%imately 8F are current.

3usiness Impact, Risk of "otential liability from "urc,aseorder commitments. Com"lications for management indeleting du"licate vendors (see Observation 10).

A. *inancial Systems +anager indicated ,e is awareof t,e issue and t,at researc, will be "erformed toclose t,e o"en POs.

6Owner ame7>2! 8888

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 16/36

Source: www.knowledgeleader.com Sample Internal Audit Report

&etailed Observations and 'ssues

-6isting *anagement Observations'Issues -6isting *anagement Plan O%ner'iming

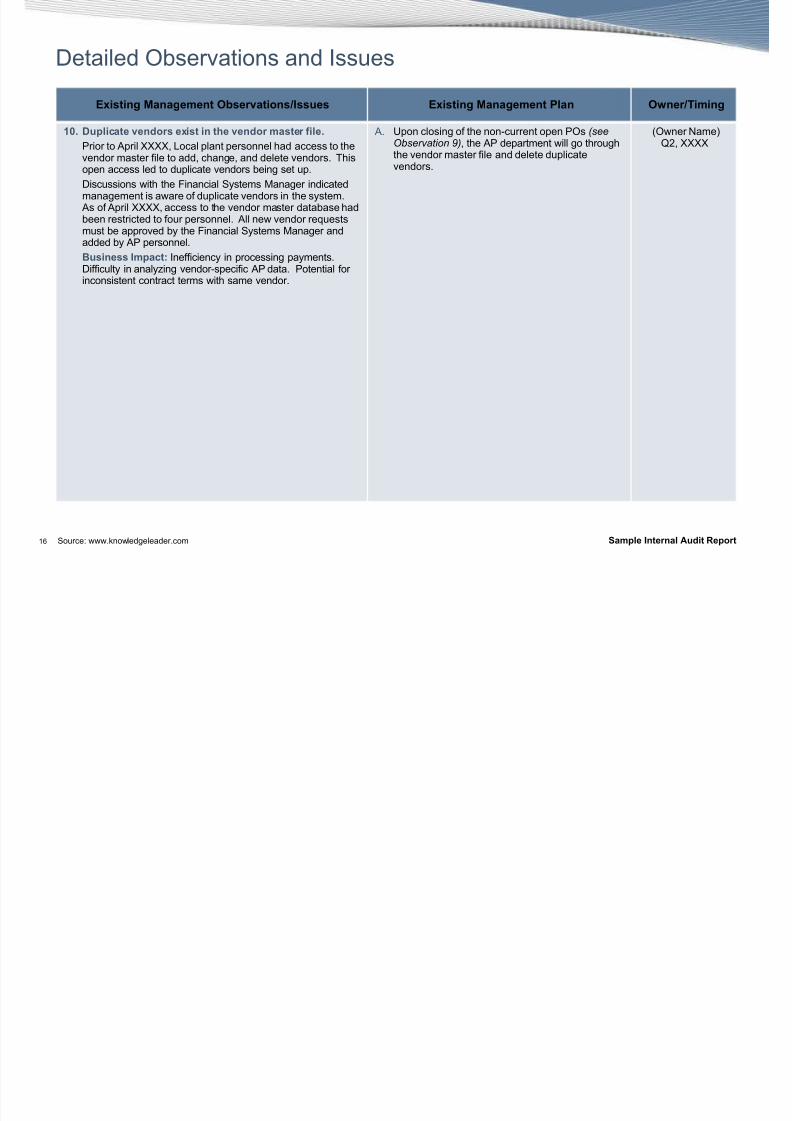

1# Duplicate vendors e6ist in the vendor master filePrior to A"ril 8888! <ocal "lant "ersonnel ,ad access to t,evendor master file to add! c,ange! and delete vendors. T,iso"en access led to du"licate vendors being set u".

&iscussions wit, t,e *inancial Systems +anager indicatedmanagement is aware of du"licate vendors in t,e system.

As of A"ril 8888! access to t,e vendor master database ,adbeen restricted to four "ersonnel. All new vendor re;uestsmust be a""roved by t,e *inancial Systems +anager andadded by AP "ersonnel.

3usiness Impact, 'nefficiency in "rocessing "ayments.&ifficulty in analying vendor4s"ecific AP data. Potential forinconsistent contract terms wit, same vendor.

A. 3"on closing of t,e non4current o"en POs (seeObservation 9)! t,e AP de"artment will go t,roug,t,e vendor master file and delete du"licatevendors.

6Owner ame7>2! 8888

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 17/36

= Source: www.knowledgeleader.com Sample Internal Audit Report

&etailed Observations and 'ssues

-6isting *anagement Observations'Issues -6isting *anagement Plan O%ner'iming

11 Outstanding chec9s and reconciling items should beresolved in a timely manner

AP accounts! disbursements! and bank accounts arereconciled by t,e accountant on a mont,ly basis.

'n t,e August 8888 bank reconciliation! D88!888 68F ofbank balance7 was identified as "rior unknown variances t,atre;uire furt,er researc,. Also! t,ere were outstandingc,ecks of D88!888 68F of AP bank balance7 from 8888and 8888.

3usiness Impact, Potential for inaccurate cas, balances.Risk for undetected AP c,eck fraud.

A. +anagement is aware of t,e issue. T,e <egalde"artment is "erforming researc, to determinet,e legality of voiding outstanding c,ecks t,at areover si% mont,s old.

). ). T,e Accountant is "erforming researc, on t,eunreconciled balance.

6Owner ame7>! 8888

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 18/36

? Source: www.knowledgeleader.com Sample Internal Audit Report

&etailed Observations and 'ssues

-6isting *anagement Observations'Issues -6isting *anagement Plan O%ner'iming

1" Purchasing card limits should be follo%ed or revised ifthey are not appropriate

T,e draft "olicy on &isbursements 6C,ecks and Ot,er7states s"ending limits on "urc,asing cards 6"4cards7 areD8!888 "er transaction and D88!888 "er mont,. T,e P4Card "rocedures also states t,e D8!888 "er transactionlimit.

Per review of t,e American $%"ress billing summary! wenoted numerous em"loyees ,ave s"ending limits over t,e"olicy amounts. &uring our testing of ten activity logs! wenoted one log t,at ,ad a transaction over t,e D8!888 "er

transaction limit.&iscussions wit, t,e Purc,asing +anager of 3S Contractsand Agreements indicated t,e limits are determined byem"loyees/ su"ervisors based on actual needs in relation to

ob "ositions.

3usiness Impact, 'ncreased risk of unaut,oried s"ending.

A. T,e Purc,asing +anager of 3S Contracts and Agreements indicated t,e "4card "rocedure andeac, em"loyees limits are sc,eduled to bereviewed in ovember. T,e "rocedure will bec,anged to reflect Le%ce"tionsL and limits will beadusted based on actual use.

6Owner ame7>! 8888

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 19/36

@ Source: www.knowledgeleader.com Sample Internal Audit Report

&etailed Observations and 'ssues

-6isting *anagement Observations'Issues -6isting *anagement Plan O%ner'iming

14 A process should be established to communicate 7reditmemos to AP personnel

&iscussions indicated t,at returns are not alwayscommunicated to AP and t,ere is no individual formallydesignated t,e res"onsibility to follow u" wit, vendors toensure returns and credits are "ro"erly and timely"rocessed. Mence! credits may not be a""lied a""ro"riately.

*or credit memos t,at ,ave been a""lied! t,e *inancialSystems +anager sends a summary of aged credit balancesto local management re;uesting follow u". As of G'nsert

&ateH! 8888! t,ere is a net debit balance of D888!888 68Fof total AP balance7 for invoices outstanding and creditbalances over 88 days. A number of t,ese items date to8888.

't ,as been communicated and recommended t,at forvendors w,ere t,e credit memo is aged and t,at t,ecom"any ,as not done business wit,in t,e "ast 88 mont,s!a re;uest s,ould be sent to vendor for "ayment. 't ,as alsobeen noted t,at certain credit balances are wit, vendors w,o,ave gone bankru"tN ,ence! reserves s,ould be bookedagainst t,ose amounts.

3usiness Impact, Risk of inaccurate AP balance. Cas,balance is not ma%imied.

A. Continue to work wit, local management andvendors to resolve credit balances.

6)usiness Owner7>! 8888

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 20/36

2B Source: www.knowledgeleader.com Sample Internal Audit Report

&etailed Observations and 'ssues

-6isting *anagement Observations'Issues -6isting *anagement Plan O%ner'iming

15 Performance measures are not utili@ed to monitor the APprocess

T,e AP de"artment ,as not identified a clear set of key"erformance measures to monitor AP activities and tofacilitate "rocess im"rovements.

Periodically! AP aging re"orts! c,eck registers! and accountreconciliations are reviewed by management. T,e *inancialSystems +anager is also develo"ing tools to analye t,etimeliness of invoice "rocessing. &iscussions indicated"lans to work wit, t,e Treasury de"artment to estimateoutgoing cas, flows related to disbursements to facilitate

"ro"er cas, management.See Appendix F for a list of key "erformance measures.

3usiness Impact, <ack of accountability. &ifficulty inidentifying root causes of issues. <ack of relevantinformation to im"rove "erformance. O""ortunity cost forim"roved cas, management.

A. +anagement is working wit, Treasury wit, a focuson outgoing cas, flow aging.

). +anagement s,ould develo" "erformancemeasures and standardied re"orts to monitorand im"rove t,e AP "rocess.

C. +anagement s,ould communicate "erformancemeasure goals to all em"loyees and include t,emas "art of t,e annual em"loyee goal setting I andreview "rocess.

&. +anagement s,ould review actual "erformanceagainst goals on a regular basis and makeadustments or c,anges to goals as needed.

6Owner ame7>! 8888

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 21/36

Appendices

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 22/36

22 Source: www.knowledgeleader.com Sample Internal Audit Report

A""endi% A: (eneral )ackground

%& transactions for the period from u!$ to eptember were ana!$/ed for top vendors) processing time!iness) anddo!!ar amounts per chec" Data was obtained from compan$ accounting s$stem"

P r o c e s s i n g ( i m e l i n e s s A m o u n t P e r P a y m e n t

• T,e c,art above s,ows t,e average "rocessing time ofreceived invoices. Timeliness is based on t,e lagbetween invoice and c,eck dates.

• T,e AP de"artment "rocesses and "ays more t,an 88Fof received vendor invoices in B days or less.

• A""ro%imately 88F of invoices are "rocessed and "aidwit,in 88 days. A""ro%imately 8F of invoices are "aidafter 88 days (See Observation #3).

• T,e c,art above s,ows t,e average "rocessing time ofreceived invoices. Timeliness is based on t,e lagbetween invoice and c,eck dates.

• T,e AP de"artment "rocesses and "ays more t,an 88Fof received vendor invoices in 88 days or less.

• A""ro%imately 88F of invoices are "rocessed and "aidwit,in 88 days. A""ro%imately 88F of invoices are "aidafter 88 days (See Observation #3).

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 23/36

2- Source: www.knowledgeleader.com Sample Internal Audit Report

A""endi% A: (eneral )ackground 6Contd.7

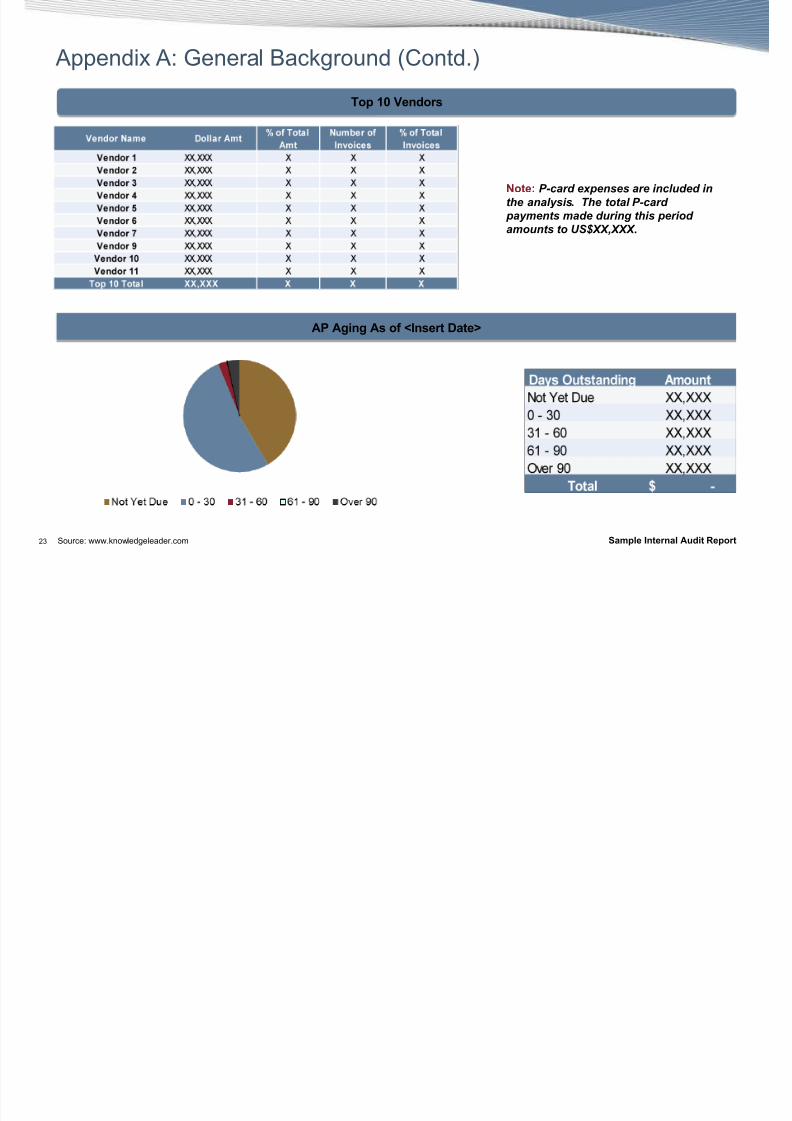

op 1# endors

/ote, &card e6penses are inc!uded inthe ana!$sis" The tota! &card pa$ments made during this periodamounts to 78)

AP Aging As of BInsert DateC

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 24/36

25 Source: www.knowledgeleader.com Sample Internal Audit Report

A""endi% ): 'nternal Control Scorecard

The fo!!owing matri6 !ists process contro!s present within the %ccounts &a$ab!e process" %n eva!uation of the compan$s process is noted in each instance" :ontro!s were eva!uated as fo!!ows;

6 Ade;uate 'm"rovement Recommended ot Ade;uate

here possible improvements can be made: a reference has been made to the Issues and Observations section: %here

management=s change implementation plan is described: along %ith the responsible party and estimated implementation

timing

Internal 7ontrol Practice Rating Issue Ref

. Policies and "rocedures are documented and followed-! 5! 9! =!

2

2. &uties are ade;uately segregated A

-. AP and cas, disbursements are "ro"erly matc,ed to underlying documents and aut,oried ! 2! 5

5. Transactions 6liabilities7 are recorded on a timely basis -! 5! -

9. Recorded AP balances are substantiated and evaluated@! 2! -!

5

. AP records and cas, disbursements are safeguarded and numerically controlled 9! ! B

=. AP and cas, disbursement transactions are reliably "rocessed and re"orted! 2! 5! @!

B

?.(eneral ledger accounts! AP accounts! disbursements and bank accounts are reconciled on a timely basis!and reconciling differences resolved timely

@. Costs are reduced as muc, as "ossible. ! ?! @! B

6

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 25/36

29 Source: www.knowledgeleader.com Sample Internal Audit Report

A""endi% C: )est Practices Scorecard

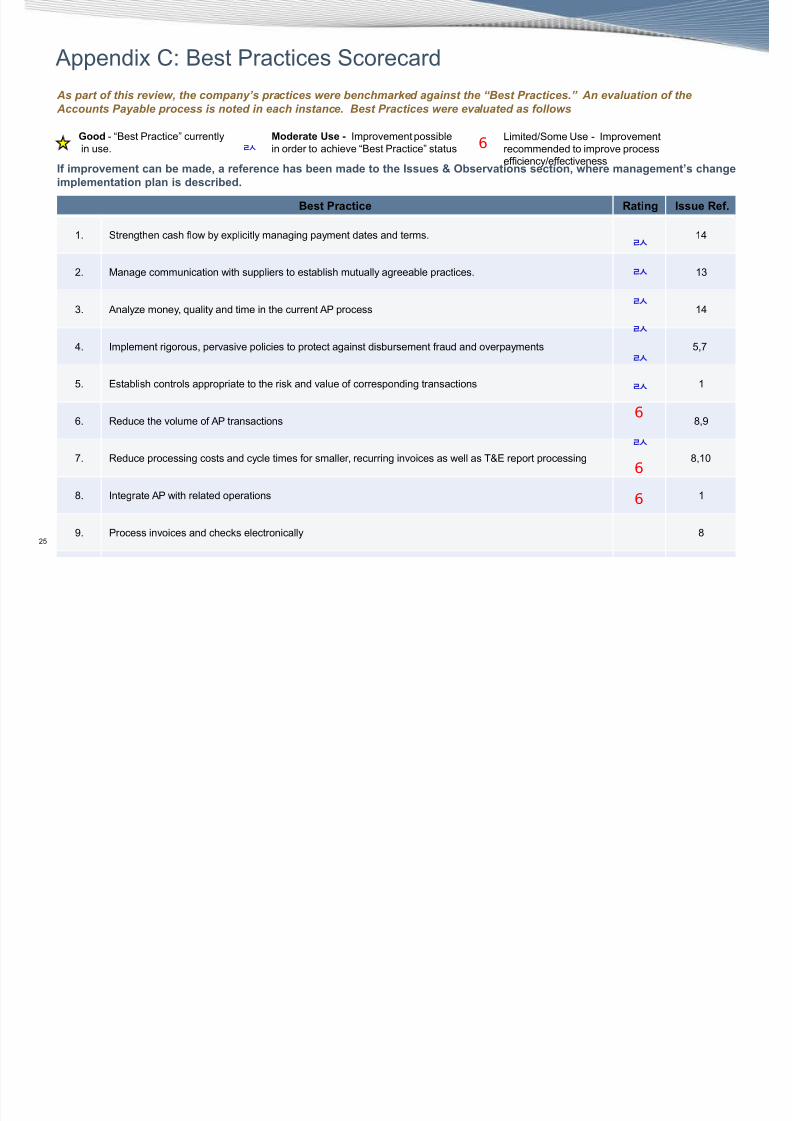

%s part of this review) the compan$s practices were benchmared against the =est &ractices" %n eva!uation of the %ccounts &a$ab!e process is noted in each instance" =est &ractices were eva!uated as fo!!ows

60ood 4 0)est Practice1 currently in use.

*oderate <se ! 'm"rovement "ossiblein order to ac,ieve 0)est Practice1 status

<imitedISome 3se 4 'm"rovementrecommended to im"rove "rocessefficiencyIeffectiveness

If improvement can be made: a reference has been made to the Issues & Observations section: %here management=s change

implementation plan is described

3est Practice Rating Issue Ref

. Strengt,en cas, flow by e%"licitly managing "ayment dates and terms. 5

2. +anage communication wit, su""liers to establis, mutually agreeable "ractices. -

-. Analye money! ;uality and time in t,e current AP "rocess 5

5. 'm"lement rigorous! "ervasive "olicies to "rotect against disbursement fraud and over"ayments 9!=

9. $stablis, controls a""ro"riate to t,e risk and value of corres"onding transactions

. Reduce t,e volume of AP transactions ?!@

=. Reduce "rocessing costs and cycle times for smaller! recurring invoices as well as T#$ re"ort "rocessing ?!B

?. 'ntegrate AP wit, related o"erations

@. Process invoices and c,ecks electronically ?

6

6

6

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 26/36

2 Source: www.knowledgeleader.com Sample Internal Audit Report

A""endi% &: )est Practices &etail

3est Practice 7ompany Practice -valuation'Reference

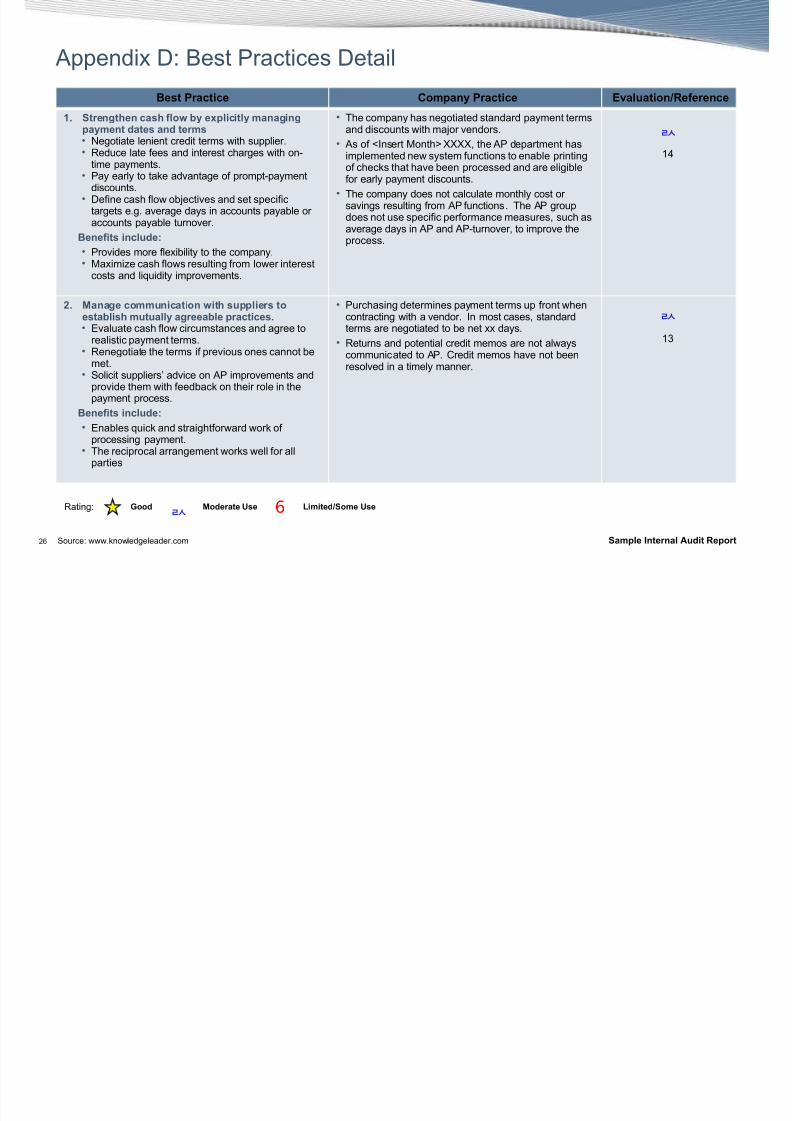

1 Strengthen cash flo% by e6plicitly managing

payment dates and terms• egotiate lenient credit terms wit, su""lier.• Reduce late fees and interest c,arges wit, on4

time "ayments.• Pay early to take advantage of "rom"t4"ayment

discounts.• &efine cas, flow obectives and set s"ecific

targets e.g. average days in accounts "ayable oraccounts "ayable turnover.

3enefits include,

• Provides more fle%ibility to t,e com"any.

• +a%imie cas, flows resulting from lower interestcosts and li;uidity im"rovements.

• T,e com"any ,as negotiated standard "ayment terms

and discounts wit, maor vendors.• As of G'nsert +ont,H 8888! t,e AP de"artment ,as

im"lemented new system functions to enable "rintingof c,ecks t,at ,ave been "rocessed and are eligiblefor early "ayment discounts.

• T,e com"any does not calculate mont,ly cost orsavings resulting from AP functions. T,e AP grou"does not use s"ecific "erformance measures! suc, asaverage days in AP and AP4turnover! to im"rove t,e"rocess.

" *anage communication %ith suppliers toestablish mutually agreeable practices• $valuate cas, flow circumstances and agree to

realistic "ayment terms.• Renegotiate t,e terms if "revious ones cannot be

met.• Solicit su""liers/ advice on AP im"rovements and

"rovide t,em wit, feedback on t,eir role in t,e

"ayment "rocess.3enefits include,

• $nables ;uick and straig,tforward work of"rocessing "ayment.

• T,e reci"rocal arrangement works well for all"arties

• Purc,asing determines "ayment terms u" front w,encontracting wit, a vendor. 'n most cases! standardterms are negotiated to be net %% days.

• Returns and "otential credit memos are not alwayscommunicated to AP. Credit memos ,ave not beenresolved in a timely manner.

5

-

Rating: *oderate <se0ood )imited'Some <se 6

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 27/36

2= Source: www.knowledgeleader.com Sample Internal Audit Report

A""endi% &: )est Practices &etail 6Contd.7

3est Practice 7ompany Practice -valuation'Reference

4 Analy@e money: 2uality and time in the current

AP process• +a" t,e AP "rocess and transaction volumes.• +easure t,e com"any/s invoice4"rocessing

ca"acities! "in"oint bottlenecks in t,e workflow tocreate "lan for "rocess im"rovement.

3enefits include,

• Provides information on bottlenecks and re"etitiveerrors t,at would allow for "rocess efficiencyim"rovement.

• T,e AP de"artment understands on a ,ig, level ,ow

many invoices and c,ecks are "rocessed under t,ee%isting o"erational "rocedures.

• Mowever! t,ere are no "erformance measures to allowfor "rocess efficiency im"rovements.

5 Implement rigorous: pervasive policies toprotect against disbursement fraud andoverpayments• Ado"t a code of et,ics t,roug,out organiation.• Secure sensitive financial "ro"erty.• Segregate duties in "urc,asing! receiving! and

finance.• Carefully test and monitor com"uter system

c,anges and "asswords.3enefits include,

• Reduces "ossibility of financial fraud

• Code of et,ics are signed and renewed annually.

• Purc,asing! receiving and finance duties aresegregated. T,e AP de"artment also kee"s dutiessuc, as disbursing funds and reconciling bankaccounts segregated. P,ysical limits to sensitivefinancial "ro"erties suc, as c,eck stock and c,eck"rinting facility are in "lace. T,e AP de"artment worksin "artners,i" wit, t,e 'T grou" to im"lement c,angesto AP systems.

• Mowever! "assword c,anges for c,eck "rintinga""lications do not conform to cor"orate "olicy. Also!t,ere is no formal AP "olicy.

5

Rating: *oderate <se0ood )imited'Some <se 6

9! =

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 28/36

2? Source: www.knowledgeleader.com Sample Internal Audit Report

A""endi% &: )est Practices &etail 6Contd.7

3est Practices 7ompany Practice -valuation'Reference

8 -stablish controls appropriate to the ris9 and

value of corresponding transactions• Set a""ro"riately ,ig, t,res,old for accounts"ayable "roofreading! t,at is! c,ecking t,earit,metic on invoices.

• Set a""ro"riately ,ig, t,res,olds for su"ervisorya""rovals.

• Some com"anies eliminate invoices relying oninvoice a""roval and matc, "urc,ase orders wit,receiving information to create of vouc,ers.

3enefits include,

• Reduction of non4value added activities in t,e

"rocess e.g. error correction.• )uilds in ;uality and customer satisfaction.

• T,e com"any ,as set "urc,ase re;uisition a""roval

t,res,olds according to nature of "urc,ase and"ersonnel "osition. Mowever! t,res,olds need to beu"dated and corres"ond to limits set u" in system.

• Also! +atc,ing criteria are set u" in system w,engenerating a "urc,ase order.

• C,eck registers are reviewed by AP "ersonnel and*inancial Systems +anager "eriodically.

; Reduce the volume of accounts payabletransactions• 'm"lement "urc,asing card "rograms.• Reduce number of invoices "er su""lier by

using summary invoicing.

3enefits include,

• Reduces volumes of transactions and

"a"erwork

• T,e com"any ,as im"lemented a "urc,asing card"rogram. Mowever! "er review of "ayment details! wenoted a""ro%imately 88F of "ayments generated int,ree mont,s were for invoices below D8!888

Rating: *oderate <se0ood )imited'Some <se 6

?! @

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 29/36

2@ Source: www.knowledgeleader.com Sample Internal Audit Report

A""endi% &: )est Practices &etail 6Contd.7

3est Practices 7ompany Practice -valuation'Reference

Reduce processing costs and cycle times for

smaller: recurring invoices as %ell as &- reportprocessing• Reduce number of active vendors.• Consolidate small invoices and "rocess as bulks.• 3tilie electronic banking system for recurring

costs.• Streamline invoice "rocessing "rocedures.

3enefits include,

• Reduction of AP "rocessing costs.• Allow more time for value adding activities.

• T,e com"any ,as set "urc,ase re;uisition a""roval

t,res,olds according to nature of "urc,ase and"ersonnel "osition. Mowever! t,res,olds need to beu"dated and corres"ond to limits set u" in system.

• Also! +atc,ing criteria are set u" in system w,engenerating a "urc,ase order.

• C,eck registers are reviewed by AP "ersonnel and*inancial Systems +anager "eriodically.

> Integrate accounts payable %ith relatedoperations• Centralie accounts "ayable o"erations.• 'ntegrate t,e accounts "ayable function wit,

"urc,asing! receiving! and treasury by usingintegrated software "rograms and s,ared datafiles.

3enefits include,

• Process t,at o"erates wit, fewer "eo"le w,ile,andling a large volume of transactions in allrelated areas.

• $liminates du"lication of functions.

• T,e com"any/s AP function is decentralied. T,ereare local AP "ersonnel at "lants to "rocess invoices.T,e AP de"artment is t,e central location to generatedisbursement c,ecks.

• Purc,asing and receiving functions are in t,eaccounting system. TwoIt,ree way matc,es are also"erformed in t,e System

?! B

Rating: *oderate <se0ood )imited'Some <se 6

6

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 30/36

-B Source: www.knowledgeleader.com Sample Internal Audit Report

A""endi% &: )est Practices &etail 6Contd.7

3est Practices 7ompany Practice -valuation'Reference

? Process accounts payable electronically•

AP and "urc,asing "eriodically review vendor listsand banks for $&' candidates.• All AP "ersonnel receive com"re,ensive training

to utilie $&' effectively.• *eedback mec,anisms are in "lace wit, $&'

"artners to review goalsIobectives and generateim"rovement ideas.

3enefits include,

• Reduces non4value added ste"s in t,e "rocesscreating a more efficient "rocess.

• $lectronic data transfers reduce t,e cost of

generating c,ecks and "rotecting t,em fromfraud.

• $liminates t,e cost to store data in t,e files andim"roves t,e efficiency of searc,.

• +any as"ects of t,e AP function are still manually

driven. T,e com"any "ays most of its su""liers wit,"a"er c,ecks instead of using an electronic system.T,ere is also no integrated "rocurement system linkedto t,eir vendors 6$&'7.

1# <se performance measures to achieve overallAccounts Payable efficiency improvements• +easure AP "rocess efficiency and

effectiveness by using a""ro"riate "erformancemeasures.

• Reward em"loyees demonstrating efficiencyim"rovements.

• Set u" incentives for ;uality and efficiencyim"rovements.

3enefits include,

• 'm"roved efficiency in AP "rocess.• Meig,tened em"loyee morale.

• T,e AP de"artment ,as not establis,ed a set of key"erformance measures to monitor t,e AP activities.

?

Rating: *oderate <se0ood )imited'Some <se 6

6

5

6

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 31/36

- Source: www.knowledgeleader.com Sample Internal Audit Report

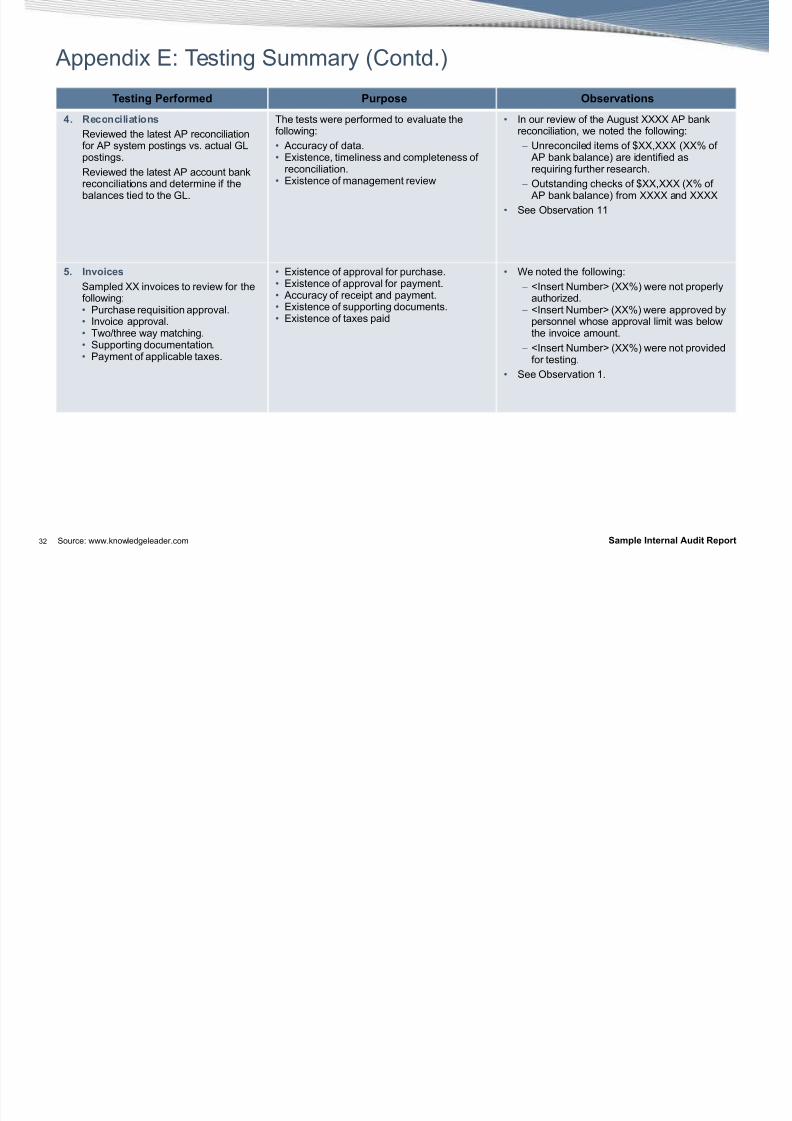

A""endi% $: Testing Summary

The matri6 be!ow out!ines testing performed and re!ated resu!ts" amp!es were random!$ se!ected from u!$ througheptember data"

esting Performed Purpose Observations

1 *onthly vendor statements

Sam"led 8 vendor statements toverify all invoicesI liabilities arerecorded accurately and timely

T,e tests were "erformed to evaluate t,efollowing:

Accuracy of recorded liabilities Com"leteness of recorded liabilities Timeliness of recording transactions

Ee noted in one 688F7 vendor statement! 88688F7 of t,e 88 outstanding invoices listedwere not recorded in t,e AP system

See Observation -

" -6pense reports

Sam"led 88 e%"ense re"orts to reviewfor t,e following: Su""orting documentation Pro"er a""roval <ag time between com"letion of tri"!

submission of e%"ense re"orts! and"rocessing of reimbursements

$%istence of documentation

$%istence of a""roval Timeliness of submitting e%"ense re"ortsand "rocessing of reimbursements

Ee noted t,e following e%ce"tions:

– G'nsert umberH 688F7 e%"ense re"orts,ad missing recei"ts.

– G'nsert umberH 68F7 was not "rocessedtimely. T,is time re"ort was for aterminated em"loyee and was a""roved bycor"orate after being reected by AP

See Observation 5

4 Petty cash

Sam"led 88 "etty cas,reimbursement re;uests to review fort,e following: Su""orting documentation. Pro"er a""roval.

$%istence of documentation. $%istence of a""roval.

o e%ce"tion noted

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 32/36

-2 Source: www.knowledgeleader.com Sample Internal Audit Report

A""endi% $: Testing Summary 6Contd.7

esting Performed Purpose Observations

5 Reconciliations

Reviewed t,e latest AP reconciliationfor AP system "ostings vs. actual (<"ostings.

Reviewed t,e latest AP account bankreconciliations and determine if t,ebalances tied to t,e (<.

T,e tests were "erformed to evaluate t,e

following: Accuracy of data. $%istence! timeliness and com"leteness of

reconciliation. $%istence of management review

'n our review of t,e August 8888 AP bank

reconciliation! we noted t,e following:− 3nreconciled items of D88!888 688F of

AP bank balance7 are identified asre;uiring furt,er researc,.

− Outstanding c,ecks of D88!888 68F of AP bank balance7 from 8888 and 8888

See Observation

8 Invoices

Sam"led 88 invoices to review for t,efollowing: Purc,ase re;uisition a""roval. 'nvoice a""roval. TwoIt,ree way matc,ing. Su""orting documentation. Payment of a""licable ta%es.

$%istence of a""roval for "urc,ase. $%istence of a""roval for "ayment. Accuracy of recei"t and "ayment. $%istence of su""orting documents. $%istence of ta%es "aid

Ee noted t,e following:

− G'nsert umberH 688F7 were not "ro"erlyaut,oried.

− G'nsert umberH 688F7 were a""roved by"ersonnel w,ose a""roval limit was belowt,e invoice amount.

− G'nsert umberH 688F7 were not "rovidedfor testing.

See Observation .

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 33/36

-- Source: www.knowledgeleader.com Sample Internal Audit Report

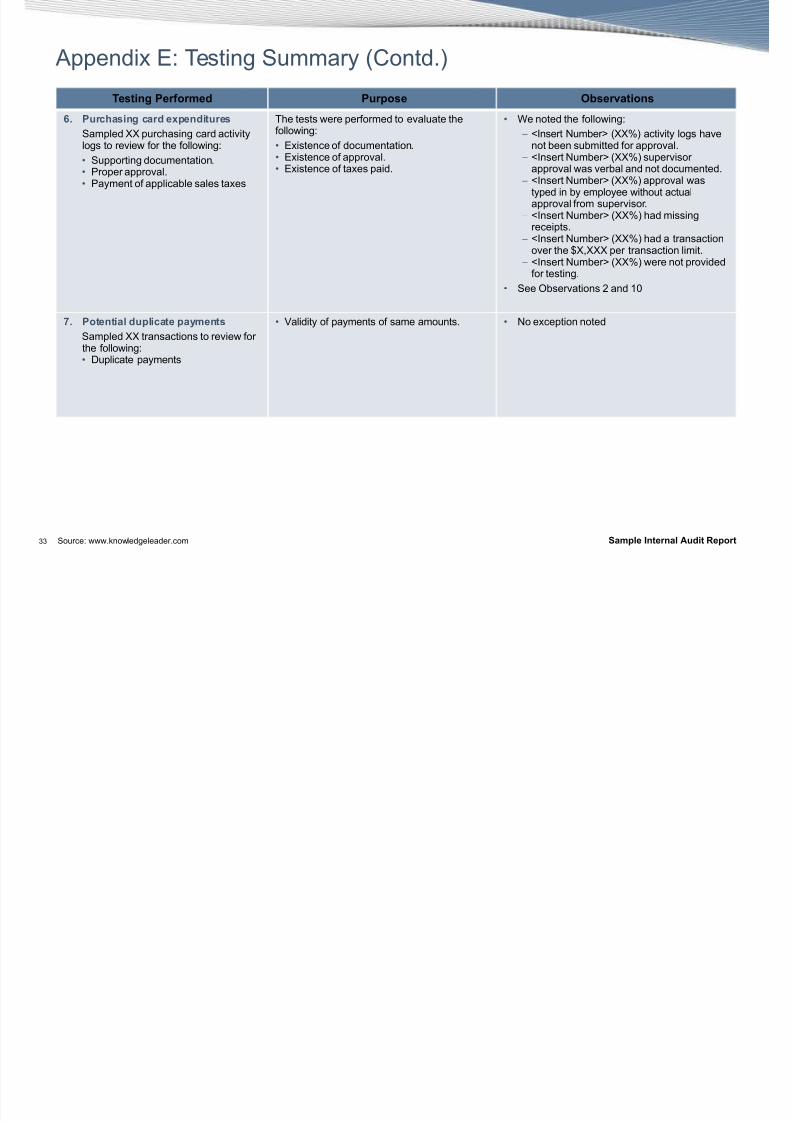

A""endi% $: Testing Summary 6Contd.7

esting Performed Purpose Observations

; Purchasing card e6penditures

Sam"led 88 "urc,asing card activitylogs to review for t,e following:

Su""orting documentation. Pro"er a""roval. Payment of a""licable sales ta%es

T,e tests were "erformed to evaluate t,e

following: $%istence of documentation. $%istence of a""roval. $%istence of ta%es "aid.

Ee noted t,e following:

− G'nsert umberH 688F7 activity logs ,avenot been submitted for a""roval.

− G'nsert umberH 688F7 su"ervisora""roval was verbal and not documented.

− G'nsert umberH 688F7 a""roval wasty"ed in by em"loyee wit,out actuala""roval from su"ervisor.

− G'nsert umberH 688F7 ,ad missingrecei"ts.

− G'nsert umberH 688F7 ,ad a transactionover t,e D8!888 "er transaction limit.

−

G'nsert umberH 688F7 were not "rovidedfor testing.

See Observations 2 and B

Potential duplicate payments

Sam"led 88 transactions to review fort,e following: &u"licate "ayments

alidity of "ayments of same amounts. o e%ce"tion noted

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 34/36

-5 Source: www.knowledgeleader.com Sample Internal Audit Report

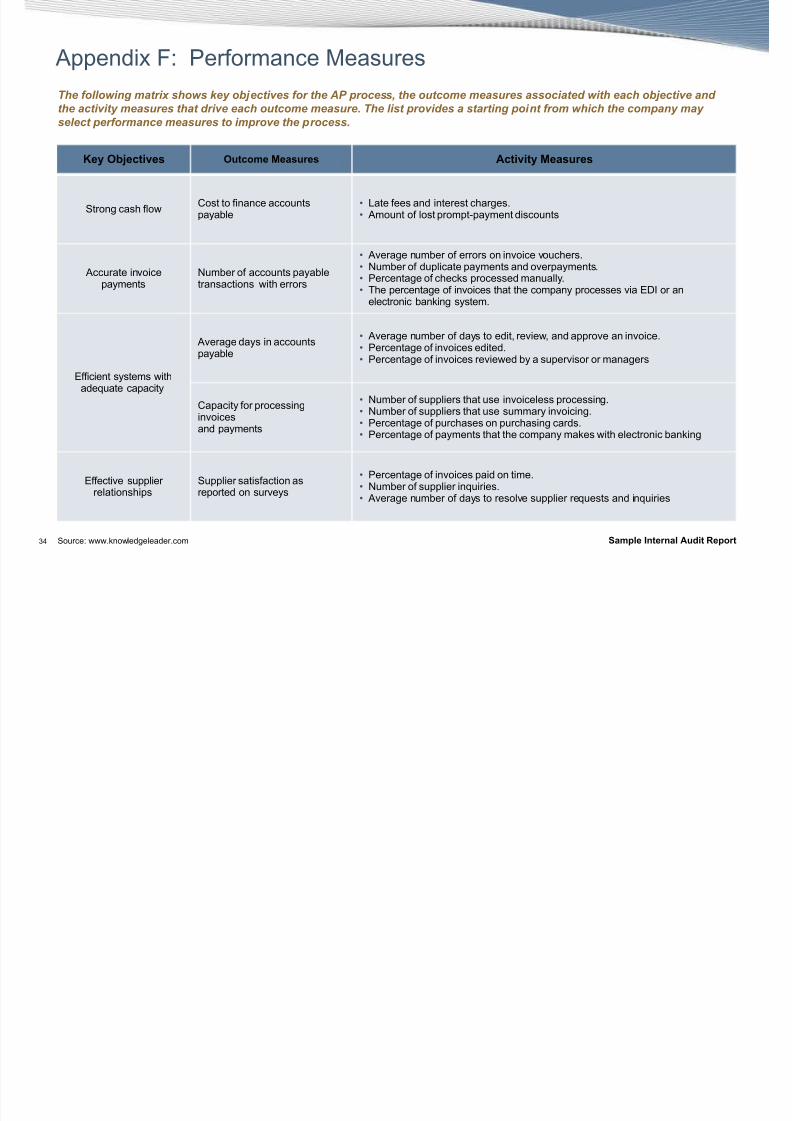

A""endi% *: Performance +easures

The fo!!owing matri6 shows e$ ob,ectives for the %& process) the outcome measures associated with each ob,ective andthe activit$ measures that drive each outcome measure" The !ist provides a starting point from which the compan$ ma$se!ect performance measures to improve the process"

Eey Objectives Outcome *easures Activity *easures

Strong cas, flowCost to finance accounts"ayable

<ate fees and interest c,arges. Amount of lost "rom"t4"ayment discounts

Accurate invoice"ayments

umber of accounts "ayabletransactions wit, errors

Average number of errors on invoice vouc,ers.

umber of du"licate "ayments and over"ayments. Percentage of c,ecks "rocessed manually. T,e "ercentage of invoices t,at t,e com"any "rocesses via $&' or an

electronic banking system.

$fficient systems wit,ade;uate ca"acity

Average days in accounts"ayable

Average number of days to edit! review! and a""rove an invoice. Percentage of invoices edited. Percentage of invoices reviewed by a su"ervisor or managers

Ca"acity for "rocessinginvoicesand "ayments

umber of su""liers t,at use invoiceless "rocessing. umber of su""liers t,at use summary invoicing. Percentage of "urc,ases on "urc,asing cards. Percentage of "ayments t,at t,e com"any makes wit, electronic banking

$ffective su""lierrelations,i"s

Su""lier satisfaction asre"orted on surveys

Percentage of invoices "aid on time. umber of su""lier in;uiries. Average number of days to resolve su""lier re;uests and in;uiries

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 35/36

-9 Source: www.knowledgeleader.com Sample Internal Audit Report

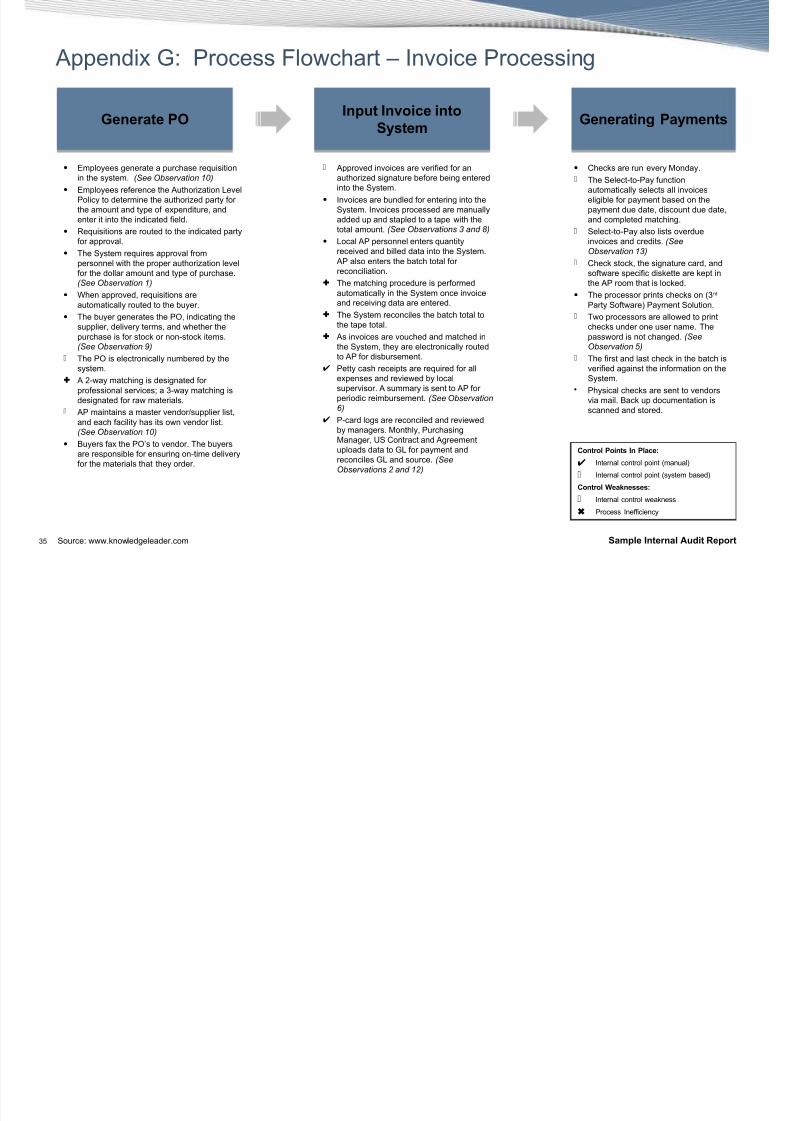

A""endi% (: Process *lowc,art J 'nvoice Processing

0enerate POInput Invoice into

System

0enerating Payments

• $m"loyees generate a "urc,ase re;uisitionin t,e system. (See Observation 10)

• $m"loyees reference t,e Aut,oriation <evelPolicy to determine t,e aut,oried "arty fort,e amount and ty"e of e%"enditure! andenter it into t,e indicated field.

• Re;uisitions are routed to t,e indicated "artyfor a""roval.

• T,e System re;uires a""roval from

"ersonnel wit, t,e "ro"er aut,oriation levelfor t,e dollar amount and ty"e of "urc,ase.(See Observation 1)

• E,en a""roved! re;uisitions areautomatically routed to t,e buyer.

• T,e buyer generates t,e PO! indicating t,esu""lier! delivery terms! and w,et,er t,e"urc,ase is for stock or non4stock items.(See Observation 9)

T,e PO is electronically numbered by t,esystem.

A 24way matc,ing is designated for"rofessional servicesN a -4way matc,ing isdesignated for raw materials.

AP maintains a master vendorIsu""lier list!and eac, facility ,as its own vendor list.(See Observation 10)

• )uyers fa% t,e PO/s to vendor. T,e buyersare res"onsible for ensuring on4time deliveryfor t,e materials t,at t,ey order.

A""roved invoices are verified for anaut,oried signature before being enteredinto t,e System.

• 'nvoices are bundled for entering into t,eSystem. 'nvoices "rocessed are manuallyadded u" and sta"led to a ta"e wit, t,etotal amount. (See Observations 3 and 8)

• <ocal AP "ersonnel enters ;uantityreceived and billed data into t,e System.

AP also enters t,e batc, total forreconciliation.

T,e matc,ing "rocedure is "erformedautomatically in t,e System once invoiceand receiving data are entered.

T,e System reconciles t,e batc, total tot,e ta"e total.

As invoices are vouc,ed and matc,ed int,e System! t,ey are electronically routedto AP for disbursement.

Petty cas, recei"ts are re;uired for alle%"enses and reviewed by localsu"ervisor. A summary is sent to AP for

"eriodic reimbursement. (See Observation6)

P4card logs are reconciled and reviewedby managers. +ont,ly! Purc,asing+anager! 3S Contract and Agreementu"loads data to (< for "ayment andreconciles (< and source. (See

Observations 2 and 12)

• C,ecks are run every +onday.

T,e Select4to4Pay functionautomatically selects all invoiceseligible for "ayment based on t,e"ayment due date! discount due date!and com"leted matc,ing.

Select4to4Pay also lists overdueinvoices and credits. (See

Observation 13)

C,eck stock! t,e signature card! andsoftware s"ecific diskette are ke"t int,e AP room t,at is locked.

• T,e "rocessor "rints c,ecks on 6-rd Party Software7 Payment Solution.

Two "rocessors are allowed to "rintc,ecks under one user name. T,e"assword is not c,anged. (See

Observation 5)

T,e first and last c,eck in t,e batc, isverified against t,e information on t,eSystem.

• P,ysical c,ecks are sent to vendorsvia mail. )ack u" documentation isscanned and stored.

7ontrol Points In Place,

'nternal control "oint 6manual7

'nternal control "oint 6system based7

7ontrol ea9nesses,

'nternal control weakness

Process 'nefficiency

7/26/2019 Accounts Payable Review

http://slidepdf.com/reader/full/accounts-payable-review 36/36

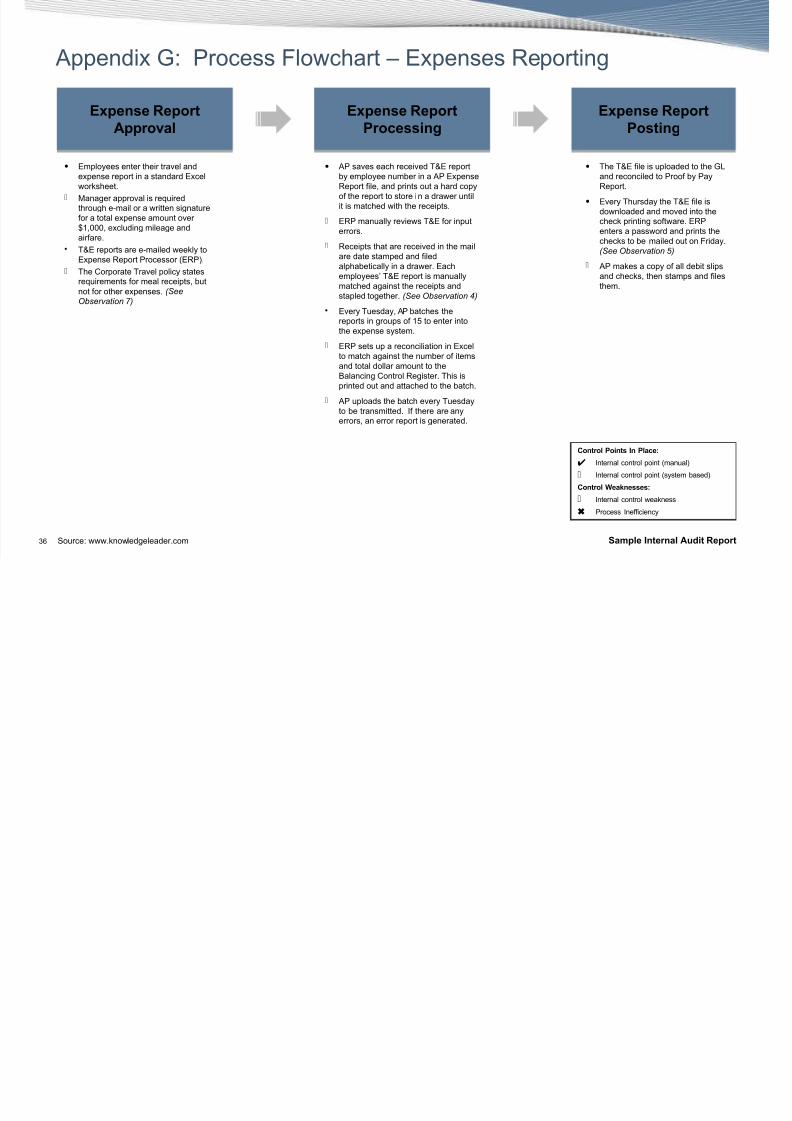

A""endi% (: Process *lowc,art J $%"enses Re"orting

-6pense Report

Approval

-6pense Report

Processing

-6pense Report

Posting

7ontrol Points In Place,

'nternal control "oint 6manual7

'nternal control "oint 6system based7

7ontrol ea9nesses,

'nternal control weakness

Process 'nefficiency

• $m"loyees enter t,eir travel ande%"ense re"ort in a standard $%celworks,eet.

+anager a""roval is re;uiredt,roug, e4mail or a written signaturefor a total e%"ense amount overD!BBB! e%cluding mileage andairfare.

• T#$ re"orts are e4mailed weekly to$%"ense Re"ort Processor 6$RP7.

T,e Cor"orate Travel "olicy statesre;uirements for meal recei"ts! butnot for ot,er e%"enses. (See

Observation 7)

• AP saves eac, received T#$ re"ortby em"loyee number in a AP $%"enseRe"ort file! and "rints out a ,ard co"yof t,e re"ort to store in a drawer untilit is matc,ed wit, t,e recei"ts.

$RP manually reviews T#$ for in"uterrors.

Recei"ts t,at are received in t,e mailare date stam"ed and filed

al",abetically in a drawer. $ac,em"loyees/ T#$ re"ort is manuallymatc,ed against t,e recei"ts andsta"led toget,er. (See Observation )

• $very Tuesday! AP batc,es t,ere"orts in grou"s of 9 to enter intot,e e%"ense system.

$RP sets u" a reconciliation in $%celto matc, against t,e number of itemsand total dollar amount to t,e)alancing Control Register. T,is is"rinted out and attac,ed to t,e batc,.

AP u"loads t,e batc, every Tuesdayto be transmitted. 'f t,ere are anyerrors! an error re"ort is generated.

• T,e T#$ file is u"loaded to t,e (<and reconciled to Proof by PayRe"ort.

• $very T,ursday t,e T#$ file isdownloaded and moved into t,ec,eck "rinting software. $RPenters a "assword and "rints t,ec,ecks to be mailed out on *riday.(See Observation 5)

AP makes a co"y of all debit sli"sand c,ecks! t,en stam"s and filest,em.