advantage sales manufacturer & retailer 2021 plans …

TRANSCRIPT

Advantage SalesMANUFACTURER & RETAILER 2021 PLANS AND OUTLOOK

March 2021

Source: Manufacturer Concerns During COVID-19 Study Feb 2021 (Base 72-78) & Retailer Concerns During COVID-19 Study Feb 2021 (Base 19-22)

Manufacturers plan to increase prices and retailers plan to decrease assortment • 47% of Manufacturers plan to increase prices in 2021.

• Of these, 74% report they will increase prices by 5-10%.• 47% of Retailers plan to decrease SKUs in 2021.

• Of these, 67% report they will decrease SKUs by 5-10%.

Manufacturers and Retailers have differing outlooks on dollar sales for 2021• Retailers expect declines to continue through Q4, while Manufacturers expect sales to level out.• Retailers and Manufacturers also have differing views on the best way to drive sales,

Manufacturers’ innovations plans and where to focus e-commerce efforts.

Manufacturers plan to increase digital spending, but are unsure about its ROI• 68% believe a shift to digital is the most efficient way to use trade funds in 2021.• 88% anticipate spending more of their marketing funds on digital this year. • Yet 16% of Manufacturers believe digital is the best promotional vehicle to drive sales.

Supply chain and out of stocks key challenges for both Manufacturers and Retailers• 59% of Manufacturers and 74% of Retailers believe “out-of-stocks” are a top challenge for 2021.• About 70% of Manufacturers and Retailers believe “supply chain” issues are a top challenge.• Both Manufacturers and Retailers are concerned with production limitations and labor.

Summary of Findings

THE UNPREDICTABLE ROLLER COASTER OF SALES

58%

79%

90%

32%

32%

11%

11%

10%11%11%

59%

Q4 2021Q3 2021Q2 2021Q1 2021

Increase About the same Decline

25%34%

52%

32%

25%

17%

14%

8%

50%50%

34%

60%

Q4 2021Q3 2021Q2 2021Q1 2021

Increase About the same Decline

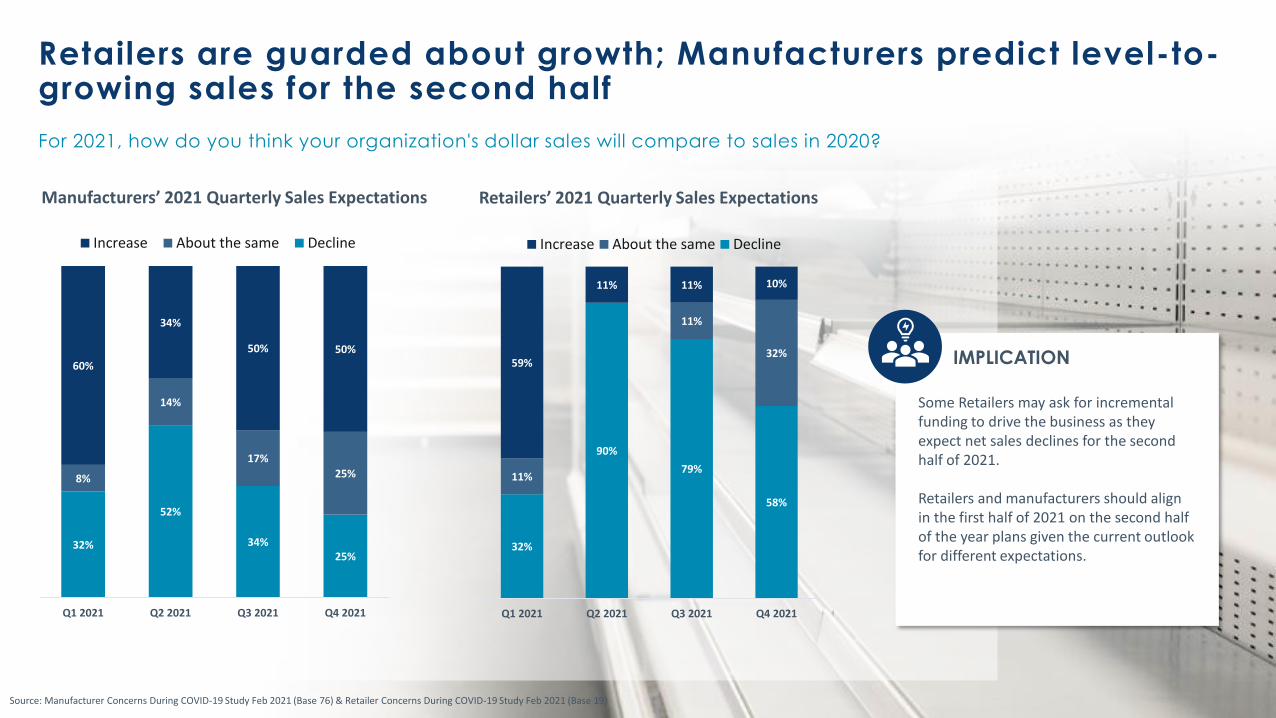

Retailers are guarded about growth; Manufacturers predict level-to-growing sales for the second half

For 2021, how do you think your organization's dollar sales will compare to sales in 2020?

Source: Manufacturer Concerns During COVID-19 Study Feb 2021 (Base 76) & Retailer Concerns During COVID-19 Study Feb 2021 (Base 19)

Manufacturers’ 2021 Quarterly Sales Expectations Retailers’ 2021 Quarterly Sales Expectations

Some Retailers may ask for incremental funding to drive the business as they expect net sales declines for the second half of 2021.

Retailers and manufacturers should align in the first half of 2021 on the second half of the year plans given the current outlook for different expectations.

IMPLICATION

DIGITAL COMMERCE

Manufacturers’ Likelihood to Increase Funds

22%

52%

20%

22%

58%

25%

Trade Funds Marketing Funds

Likely Neither Unlikely

Manufacturers anticipate more focus on digital platforms, shifting trade funds and increasing marketing fundsHow likely are you to increase trade and/or marketing funds in 2021?Where do you anticipate your trade funds being most efficiently spent in 2021? What changes do you foresee in marketing funds in 2021?

Source: Manufacturer Concerns During COVID-19 Study Feb 2021 (Base 76)

68%

55%

36%

12%7% 8%

Shift to digital Retailerpromotional

events

Displays Slotting Categorymanagement

Other

Manufacturer’s View of Most Efficient Trade Fund Spending

Manufacturers’ Spending More Marketing Funds on Digital

As manufacturers shift dollars to digital, they need information to understand the ROI on this spend. Focus on the basics first: fresh content, optimized SEO, first-page placement, retail media options, etc.

CASE STUDY

An innovative way for manufacturers to use digital is connected packaging and sampling. Connected packaging is the integration of digital experiences into product packaging via QR Codes, near field communications (NFC) and other methods to provide value to shoppers beyond the product itself.

Ice°Bottle used NFC to bring to life its goal of eliminating single-use plastics by giving shoppers an easy way to learn more and get involved in saving the planet. Consumers tap their smartphones on the NFC tag embedded in the bottom of the Ice°Bottle to launch the experience.

IMPLICATION

0%

88%

0%

11%

Spend more than 2020 Spend about the same as 2020 Spend less than 2020

Digital

42%

21%

16%

11%

Manufacturers’ View of Best Way to Drive Sales

Retailers’ View of Best Way to Drive Sales

Retailers are bullish on digital commerce to drive sales; Manufacturers believe displays are the best promotion vehicleWhat do you think is the best promotional vehicle to drive sales in 2021?

32%

27%

16%

16%

Source: Manufacturer Concerns During COVID-19 Study Feb 2021 (Base 75) & Retailer Concerns During COVID-19 Study Feb 2021 (Base 19)

Displays

More efficient promotional planning

Improved shelf location

Digital

Digital

Retailer Promotion Event

In-Store/Experiential

Displays

Shoppers have blurred the line between brick-and-mortar and online shopping. Spending will continue to shift toward digital and e-commerce, but in-store displays are still relevant. Manufacturers must strategically place themselves both in-store (displays) and online.

Retailers could help manufacturers understand the ROI of their digital spend by sharing information.

Manufacturers should position in-store displays for the second half of 2021 to accommodate potential soft sales.

IMPLICATIONS

Retailers are focused on improving e-commerce fulfillment, while Manufacturers look to marketing and better contentWhere will you focus your e-commerce efforts in 2021?

Source: Manufacturer Concerns During COVID-19 Study Feb 2021 (Base 72) & Retailer Concerns During COVID-19 Study Feb 20201 (Base 19)

79%

68%

63%

53%

5%

Fulfillment – improving fulfillment or delivery options

Retailers’ 2021 E-Commerce Efforts

90%

86%

56%

28%

3%

Content – improving online content

Marketing – focusing more on search, banner ads, etc.

Assortment – getting more products online

Other

Fulfillment – improving fulfillment or delivery options

Content – improving online content

Marketing – focusing more on search, banner ads, etc.

Assortment – getting more products online

Other

Manufacturers’ 2021 E-Commerce Efforts

Manufacturers may want to use the Advantage Digital Policy Playbook portal to understand content requirements per retailer and ensure they are adhering to the minimum requirements before focus on optimization efforts.

Retailers’ concerns about fulfillment will lead to evaluation of cost vs. benefits of the last-mile delivery.

IMPLICATIONS

Manufacturers will use trade funds to pay for increases ine-commerce expenses and “On-Time, In-Full”(OTIF) feesHow do you plan to fund your increases in digital/e-commerce expenditures? Select all that apply.How do your fund On Time In Full fees? Select all that apply.

Source: Manufacturer Concerns During COVID-19 Study Feb 2021 (Base 72)

54%

3%

49%

Those who said other:• 17% - Logistics/Supply Chain• 11% - Pricing/Fees

Manufacturers’ Funding Methods to Cover Increases in Digital Expenditures

Manufacturers’ Funding Methods for OTIF Fees

42%

33%

21%

4%

Traditional trade market funds

Shopper marketing funds

New funding

Other

Trade promotions

Shopper marketing

Other

With decreases in allocations expected, Manufacturers will need a sharper focus on what's driving sales versus using previous years’ totals as a guideline.

4 in 10 Manufacturers anticipate changes to their sales structure, with online/channel shifting driving changeDo you anticipate changes to your sales structure in 2021?What is the driver behind changing your sales structure?

Source: Manufacturer Concerns During COVID-19 Study Feb 2021 (Base 72)

39%

Anticipate changes to their sales structure in 2021

• 26% Channel shifting• 26% Prevalence of online

engagement with Retailers

Both [channel shifting and prevalence of online engagement with Retailers with an intention of becoming more efficient and effective

Streamlining structure

Market shifts

Investment for growth

Changing needs of the business

“

”

Among those that anticipate changes to their sales structure:

Changes in Sales Structure: Manufacturers

SKU ASSORTMENT

Nearly half of Retailers will trim SKU assortment; 2 in 3 will reduce SKUs by 5-10%What are your assortments plans in 2021 compared to pre-COVID-19?You indicated your will be reducing the number of SKUs you offer. How much?Please select the departments that will have the largest reduction in SKUs.

Source: Retailer Concerns During COVID-19 Study Feb 2021 (Base 19)

5%

37%

47%

Reduce

No Change

Increase

Retailers’ Plans for SKU Assortment

• 67% will decrease SKU assortment by 5-10%

Among those who plan to decrease assortment

75%

38%

38%

38%

25%

25%

25%

13%

13%

13%

13%

General food

Frozen

Beverages

Refrigerated

Home care

Tobacco

Beauty

Health

Meat

Produce

Departments With Largest SKU Reduction

Among those who plan to decrease assortmentManufacturers need to answer Retailers’ SKU rationalization with more efficient SKU assortment. They should emphasize core SKUs and incrementality of innovation and provide Retailers with consistent core-item performance. This will drive greater productivity for Retailers and, if done strategically, will benefit Manufacturers, too.

To ensure their spot on the shelf, Manufacturers’ strategy shouldn’t solely focus on their own brands, but drives category performance at the retailer. Brands must ensure assortment recommendations are based on shopper insights.

Declining SKU assortment can be a win for shoppers, if new assortments are based on local shopper profiles and needs. To create these wins, Retailers need to make shopper insights the core of their strategy.

IMPLICATIONS

General Merchandise

Retailers predict Manufacturers will pull back on innovation, while Manufacturers plan to expand or maintain their effortsWhat are your 2021 plans relative to innovation?What do you see Manufacturers doing in 2021 relative to innovation?

Source: Manufacturer Concerns During COVID-19 Study Feb 2021 (Base 75) & Retailer Concerns During COVID-19 Study Feb 2021 (Base 19)

15%

53%

32%

Manufacturers’ Innovation Plans

58%

32%

11%

Retailers’ Predictions for Manufacturers’ Innovation Plans

Expanding

Maintaining

Pulling back

Expanding

Maintaining

Pulling back

Retailers will adopt new, innovative products that appeal to shoppers. Key for brands is their ability to quickly pivot and develop products that meet shoppers’ changing needs. Brands who have done so during the pandemic have won with shoppers and Retailers.

IMPLICATION

Among those who plan to increase prices:

1%

36%

47%

Increase

No change

Decrease

Nearly half of Manufacturers plan to increase prices, with most planned for the first half of the yearWhat are your plans for pricing? How much will you increase prices?When do you plan to increase prices? What’s the reasoning behind increasing your prices?

Source: Manufacturer Concerns During COVID-19 Study Feb 2021 (Base 76)

Manufacturers’ Plans for Pricing

• 74% will increase prices 5-10%

97%

69%63%

49%

9% 6%

Cost rawmaterials

Increaseddistribution costs

Increasedproduction costs

COVID-19 relatedcosts

Innovation Other

43%49%

26%17%

First quarter Second quarter Third quarter Fourth quarter

Timeframe for Pricing Increase

Reason Behind Price Increase

Among those who plan to increase prices:

Among those who plan to increase prices:

Among those who plan to increase prices:

If Manufacturers plan to increase prices, they should do this in the first half of 2021. It may be challenging to take price increases after COVID growth slows, shares stabilize and there is a return to normal.

IMPLICATIONS

SUPPLY CHAIN

Two-thirds of Manufacturers anticipate fulfillment rates of about 80% or less for first half of 2021, with recovery in the second halfWhat level of order fulfillment do you anticipate during these time periods?

Source: Manufacturer Concerns During COVID-19 Study Feb 20201 (Base 56, 54)

Anticipated Level of Order Fulfillment

27%

2%

38%

9%

25%

52%

11%

37%

About 100%

About 90%

About 80%

Below 75%

First Half of 2021 Second Half of 2021

Source: Manufacturer Concerns During COVID-19 Study Feb 2021 (Base 78) & Retailer Concerns During COVID-19 Study Feb 2021 (Base 23)

Top 3 Manufacturer Challenges/Opportunities

Top 3 Retailer Challenges/Opportunities

Supply chain issues and out-of-stocks remain the top challenges for Manufacturers and RetailersWhat do you think your three biggest challenges/opportunities will be in 2021?

69%

56%

46%

Supply chain

Out-of-stocks

Digital

74%

74%

39%

Supply chain

Out-of-stocks

Digital

Manufacturers should address and communicate with Retailers on their supply chain efforts and improvements to not only deliver core SKUs in a timely manner, but to scale in the case of surging demand.

IMPLICATION

Product limitations and labor top Manufacturers’supply chain concerns

Thinking about the supply chain of your company, how concerned are you about the following?

Source: Manufacturer Concerns During COVID-19 Study Feb 2021 (Base 72) & Retailer Concerns During COVID-19 Study Feb 20201 (Base 18)

8%

11%

25%

28%

29%

33%

42%

47%

40%

51%

51%

60%

54%

39%

44%

49%

24%

21%

11%

13%

19%

Packaging

Warehouse

Raw materials

Manufacturing/Processing

Transportation

Labor

Productionlimitations

Very concerned Somewhat concerned Not concerned

Manufacturers’ Supply Chain Concerns

Manufacturers are concerned production limitations will continue to impact supply chain and cause out-of-stocks for shoppers. Product unavailability will push shoppers to switch brands, curbing brand loyalty.

In response, brands must stay connected to shoppers and work to stay top of mind, ensuring that when their products are back in supply, shoppers will know how and where to find them.

IMPLICATIONS

Most Retailers are very concerned with production limitations and laborThinking about the supply chain of your company, how concerned are you about the following?

Source: Manufacturer Concerns During COVID-19 Study Feb 2021 (Base 72) & Retailer Concerns During COVID-19 Study Feb 20201 (Base 18)

Retailers’ Supply Chain Concerns

28%

17%

28%

44%

39%

56%

67%

61%

33%

67%

56%

50%

28%

33%

11%

50%

6%

11%

17%

Packaging

Warehouse

Raw materials

Manufacturing/Processing

Transportaion

Labor

Productionlimitations

Very concerned Somewhat concerned Not concerned

Retailers anticipate changes in the supply chain

Thinking about your biggest supply chain concern, what changes do you anticipate in the future?

Source: Retailer Concerns During COVID-19 Study Feb 2021 (Base 14)

Manufacturers will operate a nimbler supply chain supported by increased safety stock.

SKU rationalization

Increased demand and not able to keep up.

Getting our fair share with limited supply.

Less LTL options

I would hope that vendors would become more proactive and have contingency plans.

Further diversify supply chain

Changes in assortment due to product shortages

”

“

IMPLICATIONS

Manufacturers and Retailers expect virtual meetings to continue after the pandemicPost COVID-19, what are your meeting expectations with Retailers/Manufacturers?What is your expected timeline for working in the office (not including manufacturing)?

Source: Manufacturer Concerns During COVID-19 Study Feb 2021 (Base 71) & Retailer Concerns During COVID-19 Study Feb 2021 (Base 19)

17%

65%

11%

75%

22%

15%

8%

13%

73%

Total meetings

Virtual meetings

In-person meetings

More meetings About the same Fewer meetings

11%

74%

11%

72%

21%

6%

17%

5%

83%

Total meetings

Virtual meetings

In-person meetings

More meetings About the same Fewer meetings

Manufacturers’ Post-COVID Meeting Expectations

Retailers’ Post -COVID Meeting Expectations

Manufacturers’ Timeline to Return to the Office• 37% - Once everyone is vaccinated• 18% - Second quarter• 6% - Never left• 39% - Other:

• 14% - Undetermined • 8% - Third quarter

Retailers’ Timeline to Return to the Office• 32% - Once everyone is vaccinated• 16% - Second quarter • 11% - Never left • 42% - Other:

• 32% - Undetermined

Virtual meetings are the new normal. Consider sending samples straight to secure home addresses, assuring product samples are delivered pre/post-meeting.

Also consider using virtual samples with incorporated marketing material.

RECOMMENDATION

IMPLICATIONS FOR MANUFACTURERS AND RETAILERS

SUMMARY

Manufacturers expect production limitations to impact supply chain and cause out-of-stocks for shoppers. Product unavailability will push shoppers to switch brands, curbing brand loyalty.

Brands must work to stay top of mind, ensuring that when their products are back in supply, shoppers will know how and where to find them.

Manufacturers need to address and communicate with Retailers about their supply chain efforts and improvements to not only deliver core SKUs, but to be able to scale in the case of surging demand.

Retailers will adopt new, innovative products. Brands need to pivot and quickly develop products that meet shoppers’ changing needs. Brands who have done so during the pandemic have won with shoppers and Retailers.

Manufacturers need to answer Retailers’ changing SKU rationalization with more efficient SKU assortment. They should emphasize core SKUs and incrementality of innovation, and provide Retailers with consistent core item performance. This will drive greater productivity for Retailers and, if done strategically, will benefit Manufacturers too.

Manufacturers should also create a strategy that doesn’t solely focus on their own brands, instead driving category performance at the retailer. Brands must ensure assortment recommendations are based on shopper insights.

Declining SKU assortment can be a win for shoppers, too, if new assortments are based on local shopper profiles and needs. To create these wins, Retailers need to make shopper insights the core of their strategy.

Manufacturers may want to use the Advantage Digital Policy Playbook portal to understand content requirements per retailer, and ensure they are adhering to the minimum requirements before focus on optimization efforts

In-store displays are still relevant. Manufacturers must strategically place themselves both in-store (displays) and online.

Manufacturers should position in-store displays for the second half of 2021 to accommodate potential soft sales.

As manufacturers shift dollars to digital platforms, they should focus on getting the best value for dollars spent. Make sure you have fresh content, understand SEO and first page placement, retail media options, etc.

Retailers’ concerns about fulfillment will lead to evaluation of cost vs. benefits of the last-mile delivery.

Some Retailers may ask for incremental funding to drive the business, as they expect net sales declines for the second half of 2021.

If Manufacturers plan to increase prices, consider doing this in the first half of 2021. It may be challenging to take price increases after COVID-fueled growth slows, shares stabilize and there is a return to normal.

Supply Chain SKU Assortment Digital/E-Commerce

Innovation

Price & Funding

Marketing & Displays

Other Manufacturer Recommendations for 2021

To win in 2021, Manufacturers must:

• Include digital fluency, co-creation, sustainability and the ability to pivot to meet new needs in brand strategy to succeed with the new wave of omnichannel-minded consumers.

• Continue to emphasize COVID-related health messaging.

• Be innovative with digital strategies and leverage shopper card information to identify cross-merchandising opportunities.

• In digital strategy, identify who will use product:

• Visuals should feature strong consumer profiles with high penetration.

• Call out products’ most influential attributes.

• Be creative in showcasing products. Show the whole product line when featuring a product.

• Engage with Retailers who practice test-and-learn tactics to support new merchandising recommendations.

APPENDIX

METHODOLOGY

Between February 1 and February 16, 2021,SMARTeam, a CPG market research agency and division of Ai2 in Advantage Sales, conducted two online surveys, one for Advantage Solution’s Manufacturer clients and the other for Retailers. Our team of professionals monitored the fielding of the research and data cleaning to ensure high-quality responses.

72 Manufacturer respondents completed the Manufacturer survey, and 6 partially completed the survey.

• 14% were Executive Leaders

• 60% were Sales Executive Managers

• 6% were Sales Regional Managers

• 21% were Directors

19 Retailers respondents completed the Retailers survey, and 3 partially completed the survey.

• 21% were Executive Leaders

• 32% were Sales Executive Managers

• 42% were Directors

• 5% Other