africa’s post-bali cotton work programme: what next? samuel k. gayi, phd head, special unit on...

TRANSCRIPT

Africa’s post-Bali Cotton work programme: what next?

Samuel K. Gayi, PhDHead, Special Unit on Commodities

and

Milasoa Chérel-Robson, PhD Economic Affairs Officer, Special Unit on

CommoditiesUNCTAD

LDC Group Ambassadors and Experts Retreat, 17-19 February, Montreux

Outline

I. Key developments in the cotton sector

II. Post Bali Work programme: What strategy on cotton?

Outline of Part I

I. Key developments in the cotton sector

1.Summary of US Farm Bill, 2014: Marketing Loan Programme; Stacked Income Protection Plan (Stax)

2.Highlights of Bali Ministerial Decision on cotton: trade-related & development-related aspects; reporting and monitoring

3.The state of the sector as of early 2015

4.Selected implications for trade related aspects

I.1 US Farm Bill, 2014 (1)

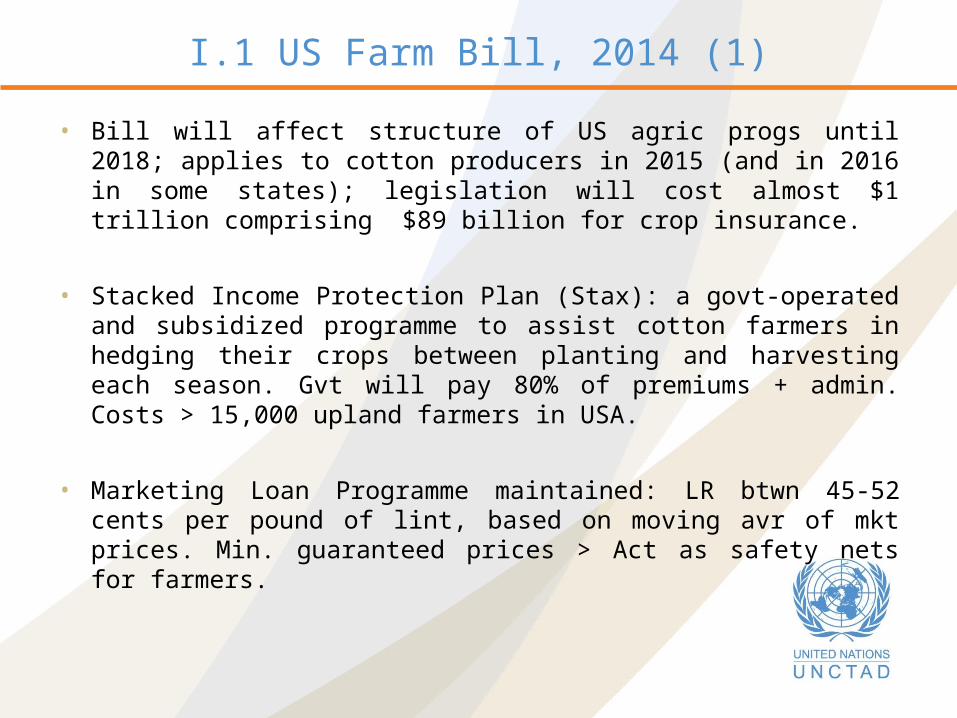

• Bill will affect structure of US agric progs until 2018; applies to cotton producers in 2015 (and in 2016 in some states); legislation will cost almost $1 trillion comprising $89 billion for crop insurance.

• Stacked Income Protection Plan (Stax): a govt-operated and subsidized programme to assist cotton farmers in hedging their crops between planting and harvesting each season. Gvt will pay 80% of premiums + admin. Costs > 15,000 upland farmers in USA.

• Marketing Loan Programme maintained: LR btwn 45-52 cents per pound of lint, based on moving avr of mkt prices. Min. guaranteed prices > Act as safety nets for farmers.

I.1 US Farm Bill, 2014 (2): Good News…

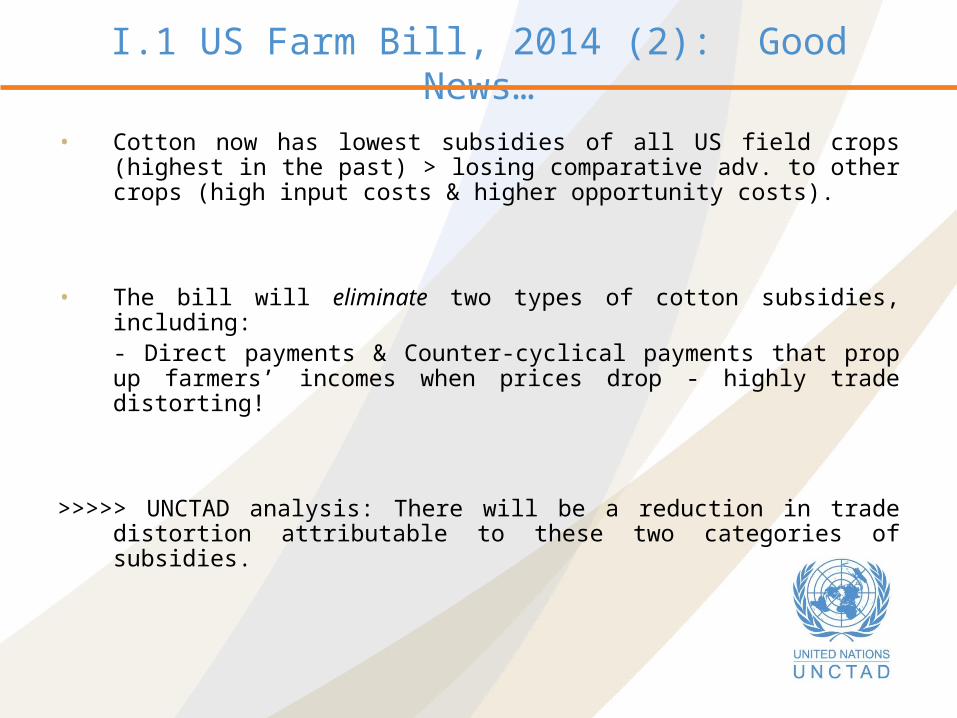

• Cotton now has lowest subsidies of all US field crops (highest in the past) > losing comparative adv. to other crops (high input costs & higher opportunity costs).

• The bill will eliminate two types of cotton subsidies, including: - Direct payments & Counter-cyclical payments that prop up farmers’ incomes when prices drop - highly trade distorting!

>>>>> UNCTAD analysis: There will be a reduction in trade distortion attributable to these two categories of subsidies.

I.1 US Farm Bill, 2014 (3): But, not-so-good news…..

• Subsidies based on planted acres, & not acres harvested which will increase total subsidies, ceteris paribus.

• Can be combined with federal insurance prog, criticized as being over subsidized

• Main issue: Will prices ever fall to very low levels, below current range?

I.2 Bali Ministerial Decision on Cotton (1): Trade related aspects

• Reaffirmed 2005 Hong Kong Ministerial Declaration and commitment to address cotton "ambitiously, expeditiously and specifically" within the agriculture negotiations.

• To hold dedicated bi-annual Special Sessions to examine trade-related developments on cotton across three pillars: market access, domestic support and export competition.

• In particular, the discussion shall consider all forms of export subsidies for cotton and all export measures with equivalent effect, domestic support for cotton, tariff and non-tariff measures applied to cotton exports from LDCs in markets of interest to them.

I.2 Bali Ministerial Decision on Cotton (2): Development related aspects

• Reaffirmed importance of development assistance aspects of cotton and committing to continued engagement in the D-G's Consultative Framework Mechanism on Cotton to strengthen cotton sector in LDCs.

• Underlined the importance of effective assistance provided to LDCs by Members and multilateral agencies.

– Inviting the LDCs to continue identifying their needs linked to cotton or related sectors, including on regional basis.

– Urging the development partners to accord special focus to such needs within the existing aid-for-trade mechanism/channels.

I.2 Bali Ministerial Decision on Cotton (3): Reporting and Monitoring

• Enhance transparency and monitoring in trade related aspects.

• WTO DG invited to continue to provide:

– Periodic reports on the development assistance aspects of cotton; and

– Progress made in the implementation of the trade-related components of the 2005 Hong Kong Ministerial Declaration, at each WTO Ministerial Conference.

I.3. The state of the sector as of early 2015 (1): World trade

• World Cotton trade experienced a sharp decline in 2013/14 and 2014/15 due to reduced imports from China (USDA, Jan. 2015).

• In 2014, cotton prices dropped to their lowest points in more than five years and likely to remain low in the medium term.

• Much of cotton production surplus >> China's domestic policies.

• India is now the top cotton producing country for the second consecutive year (ICAC Feb. 2015)

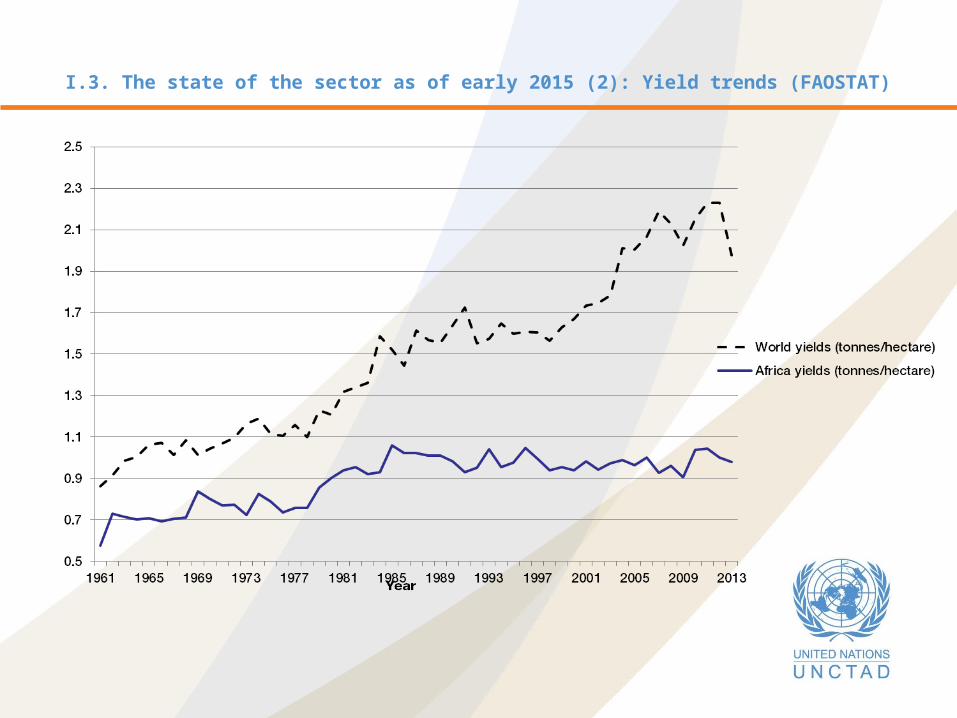

I.3. The state of the sector as of early 2015 (2): Yield trends (FAOSTAT)

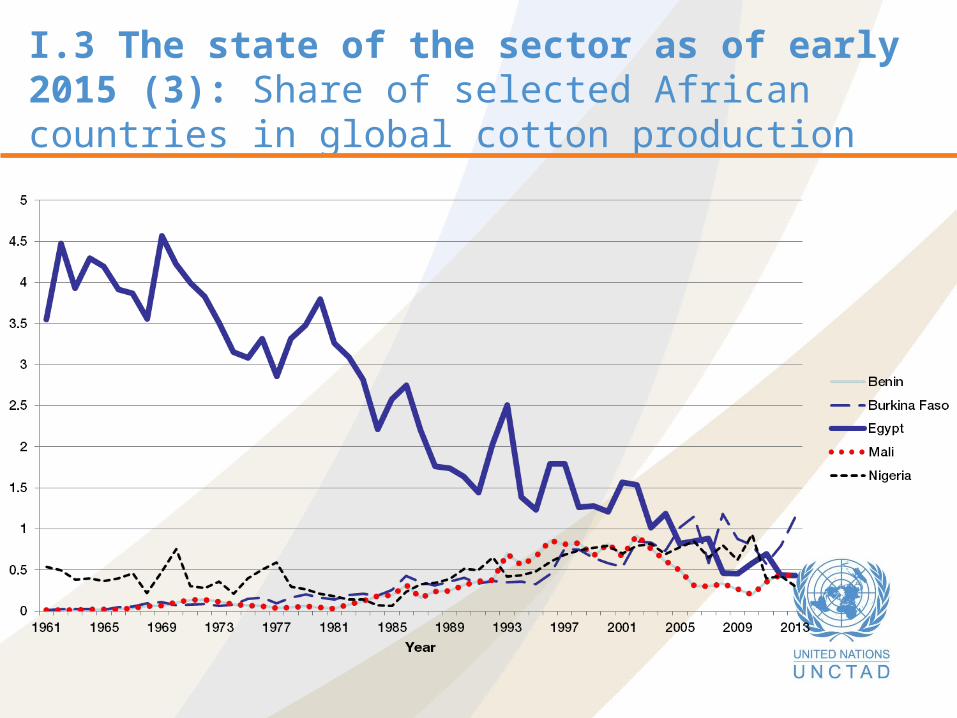

I.3 The state of the sector as of early 2015 (3): Share of selected African countries in global cotton production

I.3 The state of the sector as of early 2015 (4): Forecasts

• World cotton consumption expected to increase by 2% >> 2015/16 the first time in five seasons where consumption is greater than production (ICAC, Feb. 2015).

• But stocks held outside of China are also predicted to rise by 20% to nearly 9 million tons >> World exports will fall 15%.

• Biofuel mandates in US and Europe continue to keep prices of grain and oilseeds relatively high compared >> shrinkage in U.S. cotton acreage and production in next couple of years.

• Forecasts of reversal of contraction of world trade in cotton as USDA estimates that China's cotton imports will grow by an average of 11.2 percent a year between the 2015/16 crop year and 2014/25.

I.3 The state of the sector as of early 2015 (5): Trade-related aspects - subsidies

•Subsidies to the cotton industry inc. direct support to production, border protection, crop insurance subsidies and minimum support mechanisms est. > $6.5 billion in 2013/14 (10 countries) down from a record of $7.4 billion in 2012/13 (ICAC, Nov. 2014).

•ICAC has observed, since 1997/98, a negative correlation between subsidies and cotton prices (e.g., prices are low during periods of high subsidies). > also applied for 2013/14.

•Share of world production receiving direct assistance in 2013/14 = 44% down from 84% in 2008/09 and was on average 55% between 1997/98 and 2007/08.

I.3 The state of the sector as of early 2015 (6): Trade-related aspects - subsidies (cont'd)

• Both developed and developing countries subsidize their cotton sector to varying degrees including China, the EU, Turkey, Brazil and Columbia. But there are not generally trade distorting in LDCs.

• End of subsidies for Egyptian cotton > negative impact on Egypitian farmers; Use of "Egyptian cotton" by other countries allowed because no property right.

I.3 The state of the sector as of early 2015 (7): Brazil-US MoU

• End of Brazil-US cotton dispute - MoU signed in October 2014 and valid until 30, Sept. 2018: $300 million for a technical fund for Brazilian cotton farmers and for international cooperation in SSA countries and in MERCOSUR and associated countries that the two countries will agree upon; Brazil will not challenge the Farm Bill.

• > Question: Modalities for accessing the funds for SSA countries

• The US export credit guarantees under the GSM-102 was not terminated but changed: no guarantees for loans of more than 18 months, no extension and no renewal of guarantees once issued; fees for loans for between 12-18 months long + a series of conditions; USA will provide Brazil with semi-annual information on GSM-102 prog.

Selected implications on Trade-related aspects

• Make de minimis levels operative in terms providing domestic support: e.g. 2014 Farm Bill though Ceteris paribus, incentives to produce cotton will be weaker than in previous decades; Stax evaluations suggest implicit subsidy in premiums charged to farmers will cost govt about half as much as “old” cotton prog

• US Farm bill just one of several factors that impact on global cotton price; net impact of bill depends on devts in this price: if prices slide below historic levels, most probable impact of bill would be negative for African cotton producers.

• Clarify and tighten definition of amber box policies to forestall a reclassification (of previously green box) expenditures as amber box ones.

Outline of Part II

II. Post Bali Work programme: What strategy on cotton?

1.Selected C4 proposals

2.Leveraging on existing cotton strategies

3.The Pan African Cotton Road Map (PACRM): highlights and outlook

4.What next?

II.1. Post Bali Work programme (1): Selected C4 Proposals on Trade-related aspects

• Developed countries and developing countries declaring themselves in a position to do so, shall grant DFQF market access to cotton from LDCs from 1 Jan. 2015; other developing countries shall seek possibilities to increase cotton imports from LDCs.

• To reach an agreement on the substantial reductions of domestic support for cotton by the end of 2014.

• Developed countries that have not eliminated all forms of export subsidies for cotton should do so immediately (following the adoption of the present Decision).

II.1. Post Bali Work programme (2): Selected C4 Proposals on Development-

related aspects

• Establishing necessary link between the development aspect of cotton and the Aid for Trade initiative.

• Developing countries, in particular LDCs, shall prepare regional scale integrative projects linked to cotton or related sectors, for submission to development partners.

II.1. Post Bali Work programme (3): Selected C4 Proposals on Implementation

and Follow-up

• Improving reporting and monitoring, such as members' report on measures taken in fulfillment of WTO Ministerial Decisions and Declarations on cotton.

• Periodic reviews of the implementation of the Decision; periodic reports by D-G on the implementation of the Decision (including both trade and development aspects of cotton).

II.2. Post-Bali Work Programme (4): leveraging on existing strategies

• The “determination and general objective” of WTO members remain unchanged, with new dedication to address the 3 pillars of trade-related aspects of cotton & define pragmatic work programme.

• Build on existing strategies defined through multi-stakeholder processes and that address challenges of Africa’s cotton sector: low yields, lack of value addition, & marketing problems.

• The Pan-African Cotton Road Map (PACRM) formulated through a multi-stakeholder process overseen by UNCTAD builds on existing policies: WAEMU, ECCAS and COMESA cotton strategies.

II.3. Post-Bali Work Programme (1): PACRM

COMESA strategy

ECCAS strategy

WAEMU strategy

Recommendations from Cotonou, Bamako and Brussels meetings

Strategies,synergies and specificities in CAADP and NEPAD of AU

Strategies,synergies and specificities in CAADP and NEPAD of AU

II.3. Post-Bali Work Programme (2):Development-related aspects - PACRM

• Overall objective: to develop an African cotton value chain that is competitive and sustainable.

• Create the conditions necessary for implementing a Pan-African cotton strategy that enhances value addition, and thereby contribute to reducing poverty and enhancing food security.

• Addresses three major challenges facing the cotton sector: productivity, marketing and value addition.

II.3. Post-Bali Work Programme (3):PACRM > Outlook

• UNCTAD officially handed over PACRM to COS Coton, the Orientation and Monitoring Committee of the Action Framework of the EU-Africa Partnership on Cotton. NEPAD/AU through CAADP has been involved all along the process.

• PACRM will be officially validated at COS Coton meetings in Cotonou in March 2015.

• Expected to enhance the coordination, synergies and complementarities of the various actions on the ground.

II.3. Post-Bali Work Programme (4):PACRM > Outlook (continued)

• The EU-Africa Partnership on Cotton was established in 2004 and has since supported 200 actions in around 20 countries for a total of nearly 570 million euros most of which grants.

• Potential for synergies between COS Coton work programme, the Aid for Trade initiative and WTO Post-Bali Work Programme on Cotton.

• African producers may have to compete on price in global markets sooner rather than later.

• Holistic approach to dealing with trade- and development-related aspects of cotton in the WTO context critical.

Next Steps

• UNCTAD is now an observer at the COS Coton Steering Committee and will continue assisting the African cotton sector.

• Cotton will be discussed at UNCTAD Global Commodities Forum on 17-19 April.

• UNCTAD's Special Unit on Commodities (SUC) is available to answer any enquiry on PACRM and address any follow-up on building greater synergies >>> Post Bali Work Programme on Cotton.

THANK YOU

For more information, please contact:

Mr. Samuel Gayi, Head of Special Unit on Commodities, UNCTAD

E-mail: [email protected]

Tel (assistant): 0041- 22 917 16 48

Ms. Milasoa Chérel-Robson, Economic Affairs Officer, Special Unit on Commodities, UNCTAD

Email: [email protected]

Tel (direct line): 0041- 22 917 56 50