africa’s project pipeline for -...

TRANSCRIPT

Africa’s Project Pipeline for

Infrastructure in the Context of the

Global Financial Crisis

INFRA Platform Partners Forum

Brussels, July 2009

Impact of global crisis

on Africa

Contrary to initial beliefs Africa has not been

‘insulated’ from the global crisis

African financial system spared at first but there are nowcauses for concern.

In South Africa, 40% of loans are mortgages and house prices are falling.

Crisis hit Africa when, for first time in 20 years, the continent was enjoying growth as fast as other developing countries, excluding India and China.

Crisis is affecting Africa in three major ways:

Significant decline in capital flows

Rapid decline in commodity prices

Indirect impacts on long term growth

A. Biggest impact from decline in capital flows

Private flows mainly for infrastructure and commodity-based investments

reached $53 billion in 2007, but have started to fall.

Ghana and Kenya have postponed sovereign bond offerings worth over

$800M, delaying the constructuion of toll roads and gas pipelines

Remittances are falling, after a peak of $20 billion a year in 2007.

Kenya has reduced expected growth rate of remittance for 2008 from

11.1 to 5.4 %, and to zero for 2009.

ODA could fall substantially, since in past crises it has shown to be pro-

cyclical rather than counter-cyclical.

– Despite pledges to maintain aid flows, actual commitments are $20

billion short of commitments made in Gleneagles in 2005.

B. Commodity prices falling with varying impact

Exporters of commodities are the hardest hit.

Substantial reduction in export revenues and often in fiscal

revenues (Zambia, DRC, South Africa)

Africa’s large oil exporters will be affected, but not as badly as could be

expected.

Large exporters’ price reference was about $57 when actual price

was $140 (Nigeria, Angola, Gabon)

Revenues from other exports such as tourism are likely to decline

(Mauritius, Kenya, Tanzania).

Oil importers are likely to benefit.

C. Growth projections fall from 5.1% to 3.5%

Pre-existing macro imbalances will make it harder to weather the

shocks for some and output contractions may be greater.

With a current account deficit of 8% of GDP, South Africa has now

revised growth estimates to 1.9% for 2009

Asymmetrical impact of growth volatility on human development in

Africa.

Child mortality rises during decelerations ( by 40 deaths per 1,000

people), but barely falls during booms (by 15 deaths per 1000 people).

Primary school completion rates are substantially lower in countries

experiencing growth decelerations, as is life expectancy.

Political support for economic reforms may start to wane.

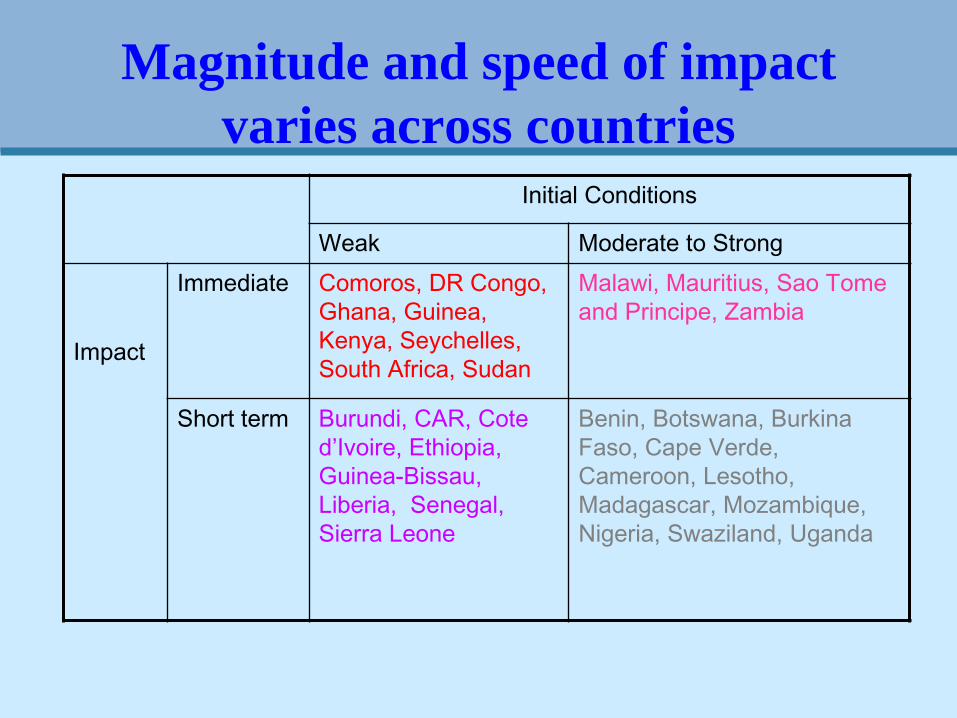

Magnitude and speed of impact

varies across countries

Initial Conditions

Weak Moderate to Strong

Impact

Immediate Comoros, DR Congo,

Ghana, Guinea,

Kenya, Seychelles,

South Africa, Sudan

Malawi, Mauritius, Sao Tome

and Principe, Zambia

Short term Burundi, CAR, Cote

d’Ivoire, Ethiopia,

Guinea-Bissau,

Liberia, Senegal,

Sierra Leone

Benin, Botswana, Burkina

Faso, Cape Verde,

Cameroon, Lesotho,

Madagascar, Mozambique,

Nigeria, Swaziland, Uganda

Total absence of stimulus

packages in SSA

Countries shaded in yellow are those that have approved stimulus packages

Implications for African

infrastructure

Overall price tag of US$100 billion, split

evenly between investment and maintenance

US$ bn. pa

over 10 years

ICT 7.0 2.0 9.0

Irrigation2.9 0.6 3.4

Power26.7 14.1 40.8

Transport13.6 11.5 25.2

WSS 14.2 6.8 21.0

Total 64.5 35.0 99.4

Capital

expenditure

Operating

expenditureTotal

Source: AICD 2009

Overall financing gap of US$54 billion per

year concentrated largely in power

US$bn pa

Energy ICT Irrigation Transport WSS Total

MIC10.7 0.0 0.1 0.4 1.6 12.8

Resource-Rich7.8 0.5 1.9 2.1 5.4 17.7

LIC-NoFragile6.5 0.0 0.8 4.1 5.1 16.4

LIC-Fragile4.3 0.7 0.0 3.2 3.0 11.2

Africa29.2 0.0 2.6 8.9 13.4 54.1

Foreseeable negative impacts of the crisis

Public expenditures cuts

Could be particularly harmful – public expenditure represent 2/3 of financing.

Every dollar cut from road maintenance leads to four dollar liability for rehabilitation.

Drying up external finances

Reduced availability of debt finance already in ITC, constraining new deals and restricting debt roll-over on existing investments

Ghana and Kenya postponed sovereign bond offering over 800 million, delaying construction of toll roads and gas pipelines.

Donors Funds could slow down as fiscal pressures are mounting at home, despite the claims to the contrary.

Weaker sector revenues

For utilities that already operate in the red.

For Road Funds due to lower traffic declining exchange rates.

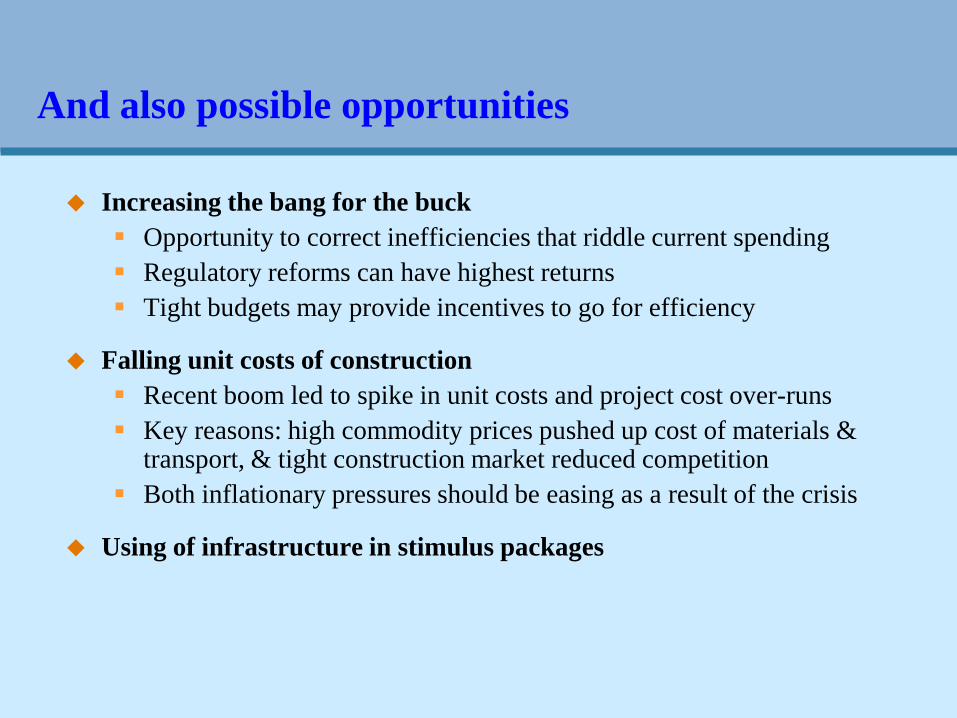

And also possible opportunities

Increasing the bang for the buck

Opportunity to correct inefficiencies that riddle current spending

Regulatory reforms can have highest returns

Tight budgets may provide incentives to go for efficiency

Falling unit costs of construction

Recent boom led to spike in unit costs and project cost over-runs

Key reasons: high commodity prices pushed up cost of materials & transport, & tight construction market reduced competition

Both inflationary pressures should be easing as a result of the crisis

Using of infrastructure in stimulus packages

Infrastructure investments create employment

generating growth

0%

20%

40%

60%

80%

100%

Arg

entin

a

Bra

zil

Chin

a

India

*

Indon

esia

Mex

ico

Russ

ia

Other Stimulus Measures

Infrastructure Spending

$4.8$10.5

$93.2$4.6 $2.8$11.4

$29.6

$3.6 $8.7 $1.1 $4.6 $0$82.0$0

Percentage of

Stimulus

Spending

Fiscal Stimulus Packages for 2009 (US$ b)

Potential operational responses

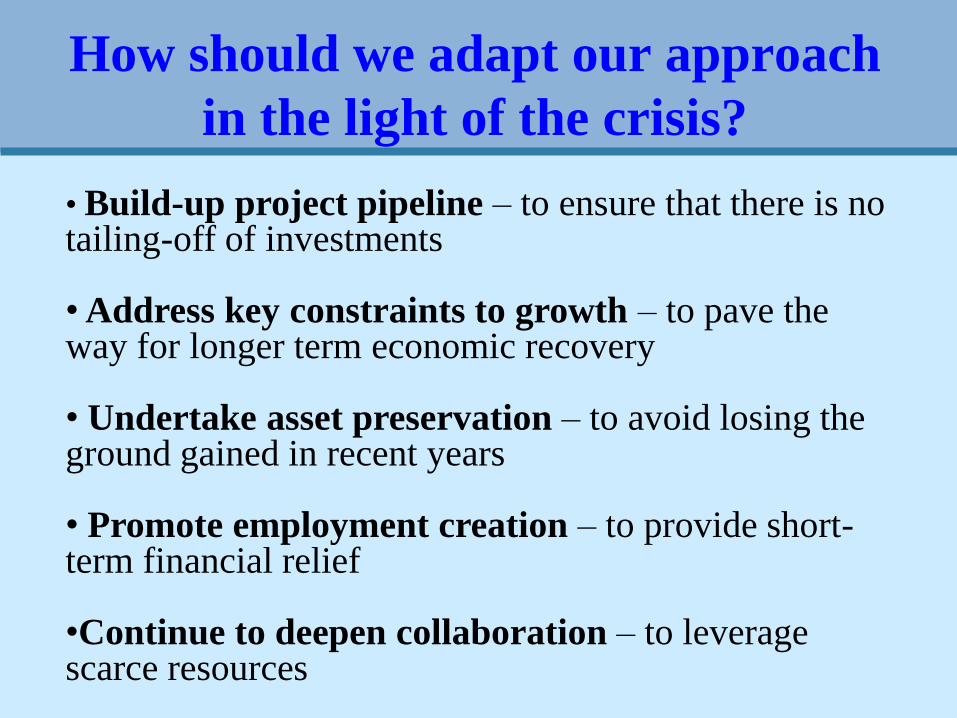

How should we adapt our approach

in the light of the crisis?

• Build-up project pipeline – to ensure that there is no tailing-off of investments

• Address key constraints to growth – to pave the way for longer term economic recovery

• Undertake asset preservation – to avoid losing the ground gained in recent years

• Promote employment creation – to provide short-term financial relief

•Continue to deepen collaboration – to leverage scarce resources

What can be done to strengthen

the project pipeline?

• Strong growth in project pipeline from

US$0.6bn in FY01 to US$3.5bn in FY10

• This has been achieved by cleaning out

project pipeline

• Concern that medium-term pipeline is

dwindling and requires additional effort

– Pipeline for FY10/12 average US$1.9bn pa

– Deliveries for FY07/09 average US$2.5bn

Can we move faster on addressing key

growth bottlenecks?

• Stimulus packages of around US$2 trillion have been approved globally

– Between 40-80% of these linked to infrastructure

• ODI estimates Africa needs stimulus of US$50bn, and focusing this on infrastructure gives largest growth boost

– Short-run impact - 2010 growth of 4% versus 1.7%

– Long-run impact - permanent GDP increase 2.5%

• Regional integration projects good to address growth bottlenecks and currently under-funded

Regional integration pipeline

exceeds available resources

Regional IDA for

FY09-FY11 is over

programmed by

$3billion

Can we use projects to support

preservation of critical assets?

• Maintenance expenditure particularly high

return and yet particularly vulnerable

– Every US$1 spent on road maintenance saves

US$4 on rehabilitation

• May be case for increasing focus on

maintenance through new instruments

– Policy Operations, Budget Support, SWAp,

Output-Based Aid

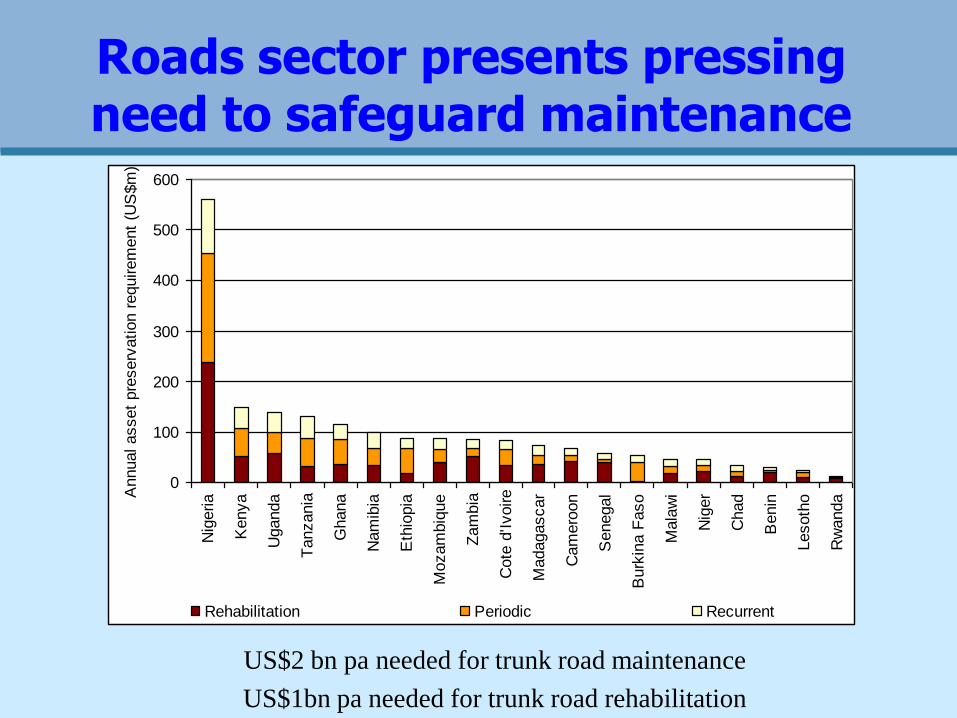

Roads sector presents pressing need to safeguard maintenance

US$2 bn pa needed for trunk road maintenance

US$1bn pa needed for trunk road rehabilitation

0

100

200

300

400

500

600

Nig

eria

Kenya

Uganda

Tanzania

Ghana

Nam

ibia

Eth

iopia

Mozam

biq

ue

Zam

bia

Cote

d'Ivoire

Madagascar

Cam

ero

on

Senegal

Burk

ina F

aso

Mala

wi

Nig

er

Chad

Benin

Lesoth

o

Rw

andaA

nnual asset

pre

serv

ation r

equirem

ent

(US

$m

)

Rehabilitation Periodic Recurrent

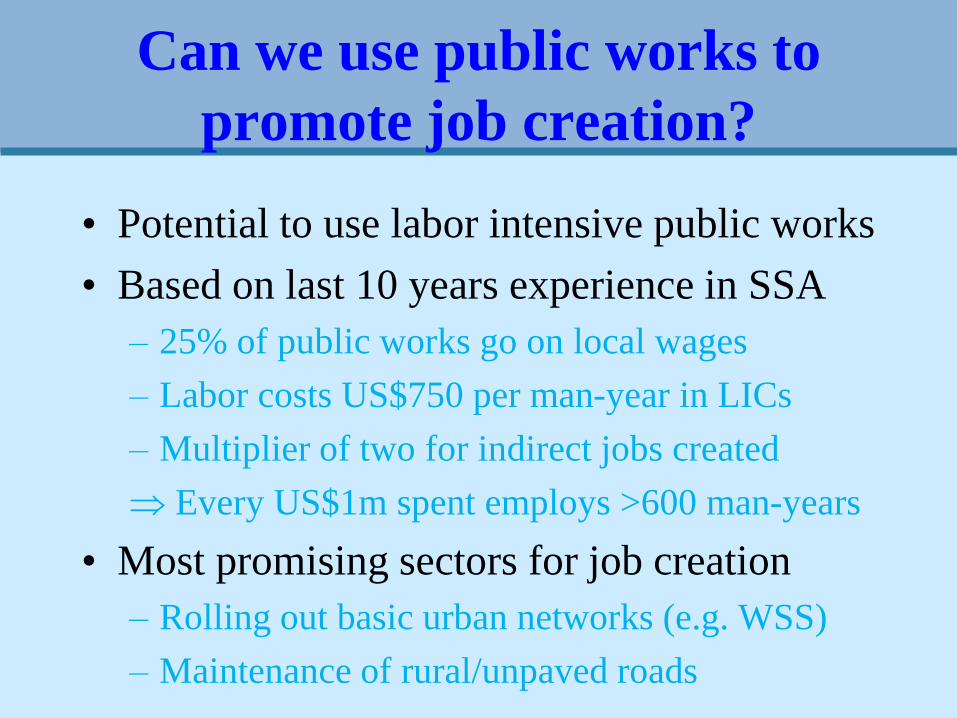

Can we use public works to

promote job creation?

• Potential to use labor intensive public works

• Based on last 10 years experience in SSA

– 25% of public works go on local wages

– Labor costs US$750 per man-year in LICs

– Multiplier of two for indirect jobs created

Every US$1m spent employs >600 man-years

• Most promising sectors for job creation

– Rolling out basic urban networks (e.g. WSS)

– Maintenance of rural/unpaved roads

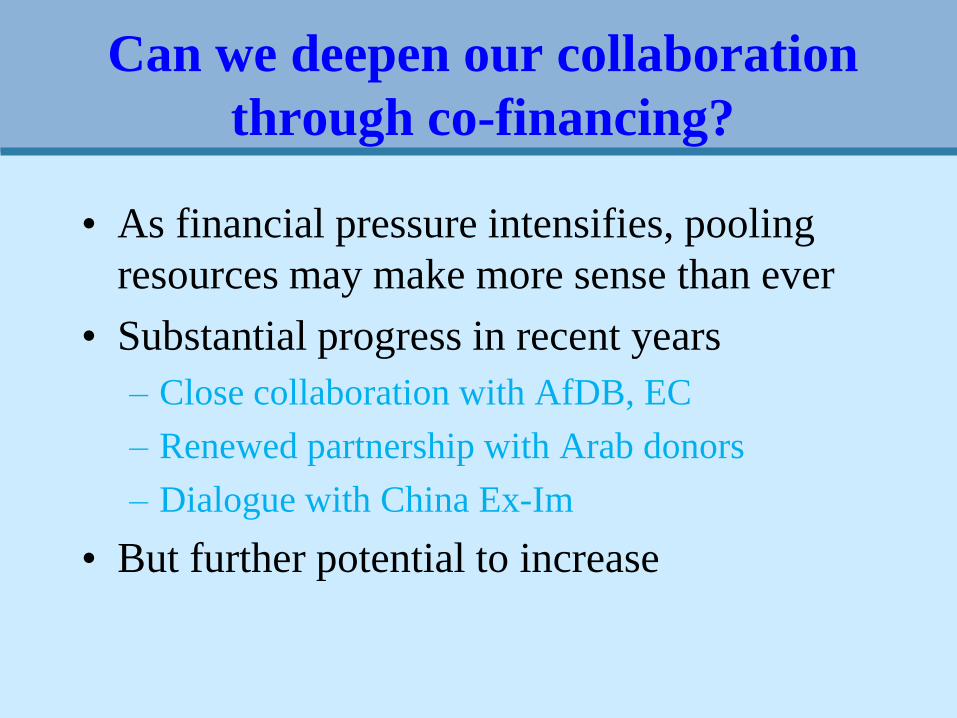

Can we deepen our collaboration

through co-financing?

• As financial pressure intensifies, pooling

resources may make more sense than ever

• Substantial progress in recent years

– Close collaboration with AfDB, EC

– Renewed partnership with Arab donors

– Dialogue with China Ex-Im

• But further potential to increase

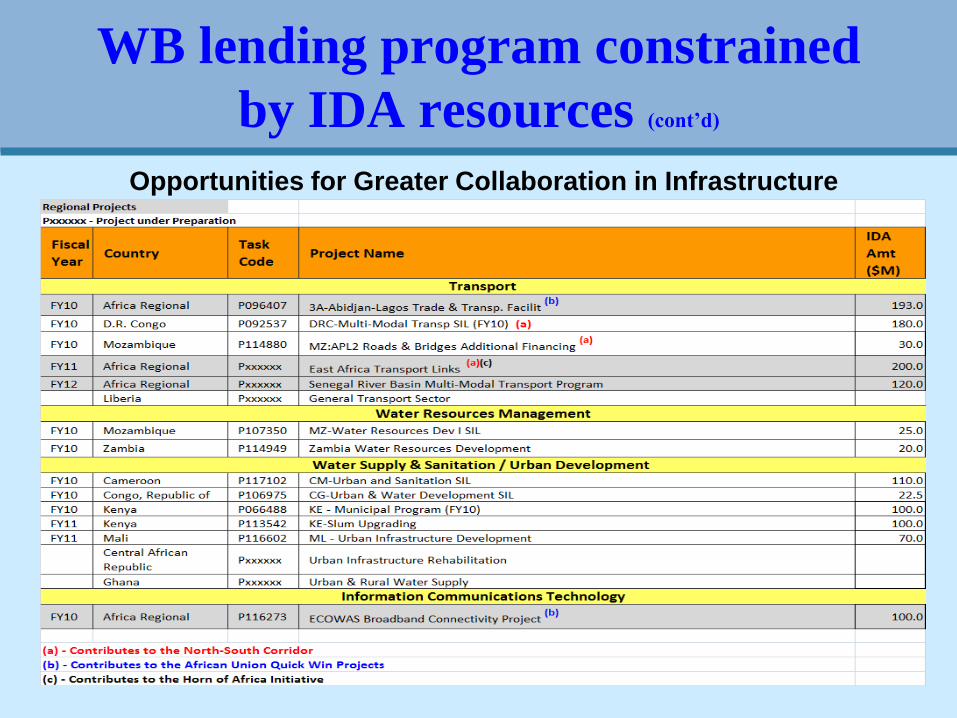

WB lending program constrained

by IDA resourcesOpportunities for Greater Collaboration in Infrastructure

WB lending program constrained

by IDA resources (cont’d)

Opportunities for Greater Collaboration in Infrastructure

Thank you!