alberta’s montney growth story - blackbird energy inc · who is blackbird energy? blackbird...

TRANSCRIPT

Alberta’s Montney Growth Story TSX-V: BBI

Advisory

Summary of Forward‐Looking Statements and Advisories

Certain information included in this presentation constitutes forward‐looking information under applicable securities legislation. This information relates to future events or future performance of Blackbird Energy Inc. ("Blackbird"). Investors are cautioned that reliance on such information may not be appropriate for making investment decisions. Many factors could cause Blackbird's actual results, performance or achievements to vary from those described herein. The forward‐looking information contained in this presentation is expressly qualified by this and other cautionary statements set forth in the continuous disclosure record of Blackbird.

For a complete description of the forward‐looking statements or information and certain other advisories, see slide 30 "Forward‐Looking Statements or Information and Additional Advisories."

2

Who is Blackbird Energy?

Blackbird Energy Inc. is an emerging oil and gas exploration company

focused on the liquids-rich Montney fairway at Elmworth, near Grande

Prairie, Alberta:

75 sections (48,000 acres) of 100% working interest Montney rights

at Elmworth / Gold Creek

Highly productive Upper and Middle Montney reservoirs

Recent Middle Montney production test: 1,768 boe/d (>30% liquids)

Strategic growth strategy – acquire > delineate > de-risk > cash flow

Team in place with the skills and experience to develop the resource

Strong balance sheet

3Note: * $23 million in working capital pre commencement of the 2-20 drilling operations

The Asset

4

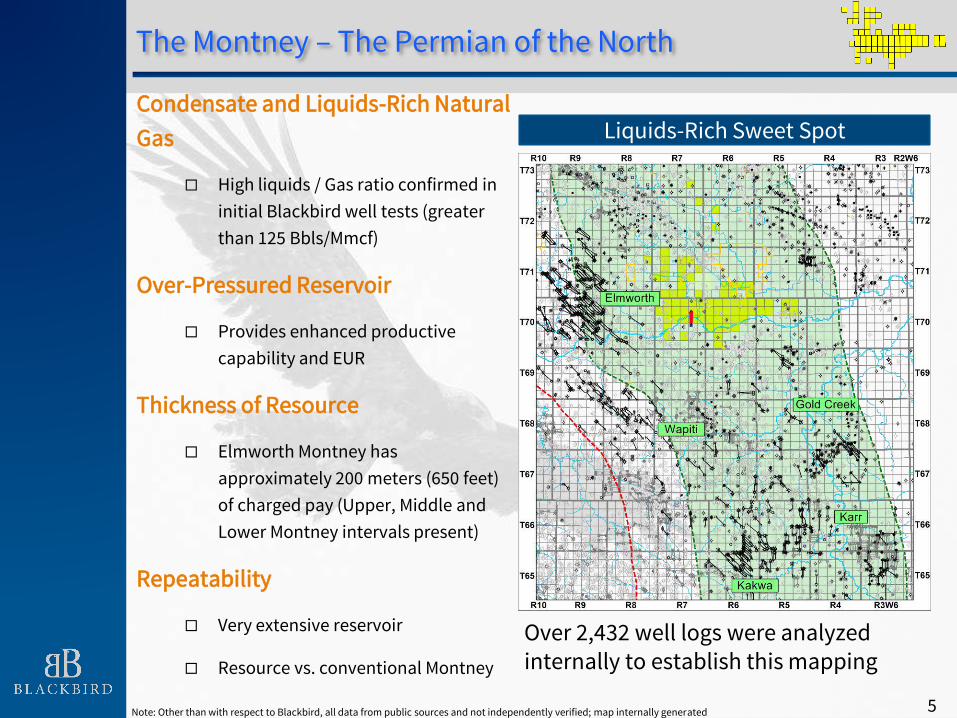

The Montney – The Permian of the North

Condensate and Liquids-Rich Natural

Gas

High liquids / Gas ratio confirmed in

initial Blackbird well tests (greater

than 125 Bbls/Mmcf)

Over-Pressured Reservoir

Provides enhanced productive

capability and EUR

Thickness of Resource

Elmworth Montney has

approximately 200 meters (650 feet)

of charged pay (Upper, Middle and

Lower Montney intervals present)

Repeatability

Very extensive reservoir

Resource vs. conventional Montney

Over 2,432 well logs were analyzed internally to establish this mapping

Note: Other than with respect to Blackbird, all data from public sources and not independently verified; map internally generated

Liquids-Rich Sweet Spot

5

Low Cost Land Assembly

Early mover advantage

Assembled 75 sections for ~$6.9

million or $92,500 per section

~900 potential drilling locations

(Upper and Middle Montney)

Elmworth Montney land sale

valuations have steadily

increased:

Near proximity land sales have

seen multi-section packages go

for approximately $2.9 million

per section

All in an area that is economic

today with robust torque as

commodity prices increase

Blackbird Land Assembly

6

De-Risked Elmworth

Other people’s money is de-risking the play

Industry results: Encana 2-15, Encana 13-22 and BBI 5-26 demonstrating

strong liquids yields in Upper Montney; 2-20 and 6-26 demonstrating

Middle Montney productivity

Over 150 Producing Montney Wells in Our CorridorNote: Other than with respect to Blackbird, all data from public sources and not independently verified; map internally generated 7

Legend

Blackbird

Encana

CNRL

Nuvista

Chinook

Apache

Sinopec

Birchcliff

Paramount / Inception

MontneyWell

Well Licence

Multi-Zone Elmworth Montney

8

650

Feet

Upper Montney/Doig

Belloy

Upper Montney

Middle Montney

Lower Montney

BBI 2-20 HzDensity Porosity Gas Detector

Up to 6% Porosity

Gas response confirms presence of hydrocarbons throughout Montney

Gamma Ray Resistivity Lithology

Blackbird 10-8-70-7 W6Pilot Hole for 2-20-70-7 W6 Hz

ECA 13-22 Hz

EnCana 15-14-70-8 W6Pilot Hole for 13-22-70-8 W6 Hz

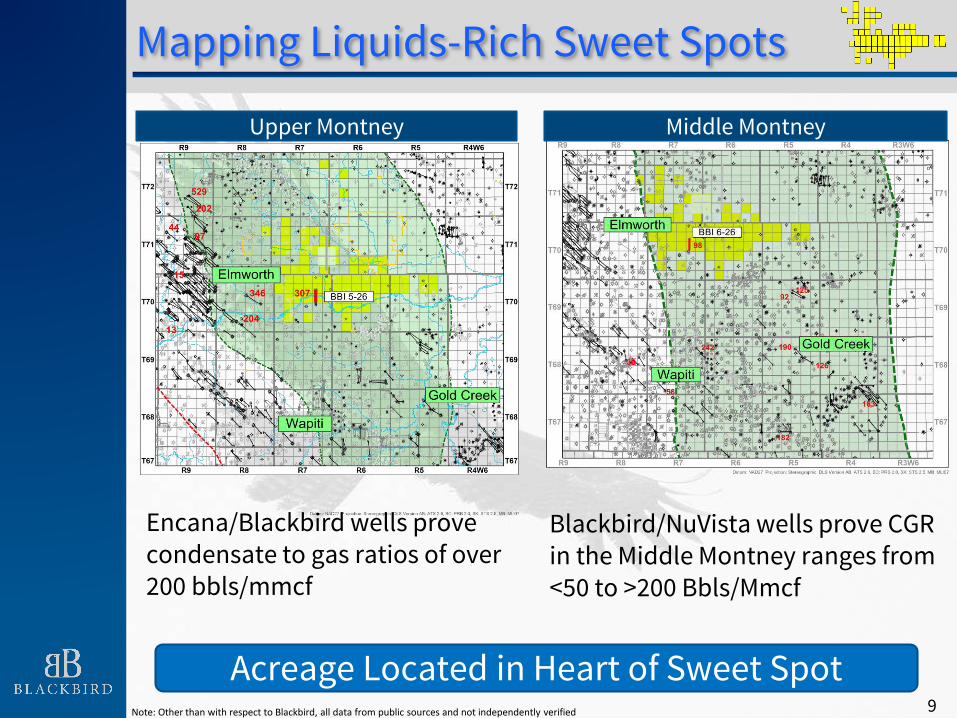

Mapping Liquids-Rich Sweet Spots

Blackbird/NuVista wells prove CGR in the Middle Montney ranges from <50 to >200 Bbls/Mmcf

Upper Montney Middle Montney

Acreage Located in Heart of Sweet SpotNote: Other than with respect to Blackbird, all data from public sources and not independently verified 9

Encana/Blackbird wells prove condensate to gas ratios of over 200 bbls/mmcf

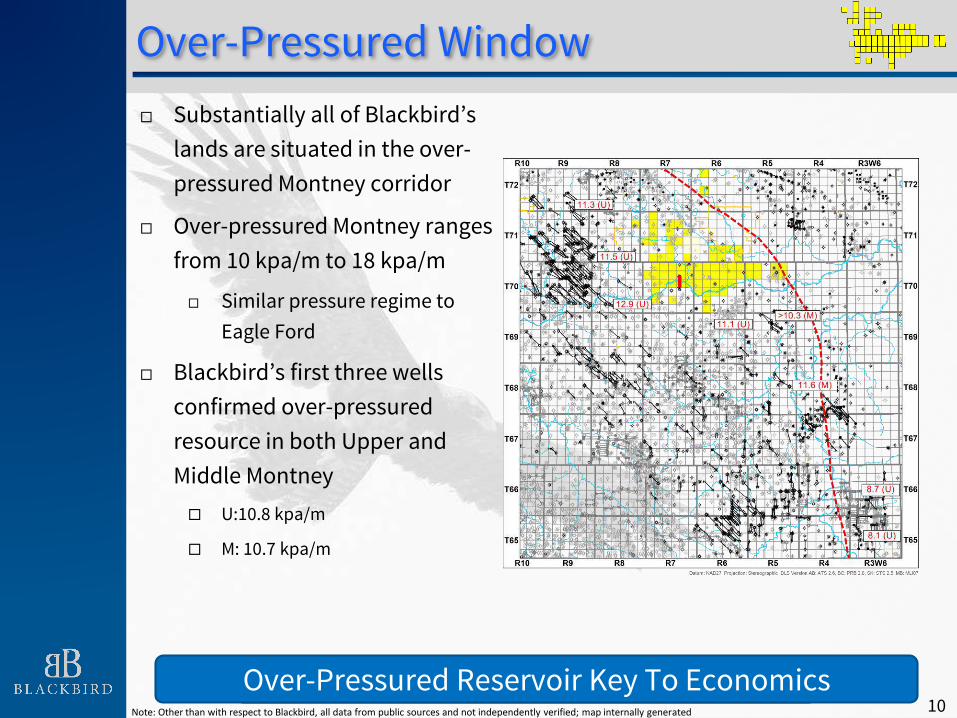

Over-Pressured Window

Over-pressured reservoir key to EUR and Productivity

Substantially all of Blackbird’s

lands are situated in the over-

pressured Montney corridor

Over-pressured Montney ranges

from 10 kpa/m to 18 kpa/m

Similar pressure regime to

Eagle Ford

Blackbird’s first three wells

confirmed over-pressured

resource in both Upper and

Middle Montney

U:10.8 kpa/m

M: 10.7 kpa/m

Over-Pressured Reservoir Key To EconomicsNote: Other than with respect to Blackbird, all data from public sources and not independently verified; map internally generated 10

Infrastructure

11

Access to Infrastructure

Key for any E&P is access to pipelines & processing

Juniors have to solve this without significant dilution /

destruction of balance sheet

Near-term solution for takeaway:

Solution to handle our sour gas

Scalability starting from 5 Mmcf/d + associated liquids

Multiple options available

Infrastructure Optionality Provides Strength 12

Blackbird’s Infrastructure Solution

Note: Other than with respect to Blackbird, all data from public sources and not independently verified 13

Infrastructure is being focused on a resource play that works in

this current commodity price environment.

Up to 1.35 Bcf/d

of new processing

planned for this

area

LNG Opportunity

Currently there are 18 BC LNG projects being contemplated that

would represent almost 350 Tcf of gas resources

Some key facilities that look to be moving ahead are:

Kitimat (Chevron, Woodside) – 1.3 Bcf/d

Pacific Northwest (Petronas) – 2.7 Bcf/d

Aurora (CNOOC, INPEX, JGC Corp.) – 3.1 Bcf/d

WCC LNG (Imperial / Exxon) – 4.0 Bcf/d

Douglas Channel – 0.2 Bcf/d

LNG Canada (Shell et al) – 3.2 Bcf/d

Triton (Altagas, Idemitsu) – 0.3 Bcf/d

Above facilities equate to 14.9 Bcf/d

3.1 Bcf/d expansion of TCPL infrastructure in Grande Prairie area will

assist LNG projects

LNG provides future upside to North American gas production and

prices14Note: Data from page as per Cormark Secutiries

D&C Optimization

15

Drilling Optimization

First Upper Montney well – 39 days

First Middle Montney well – 49 days

Latest Middle Montney well (2-20) – 24 days

First Monobore in Elmworth / Gold Creek Montney

Modification of drilling fluids (Brine vs. Invert)

Rig selection (Ensign, hot Montney crew)

Selection of bit and motor combinations

Movement to multi-well pads (significant efficiency

gains)

16Innovation Driving Economic Recovery

Completion Optimization

Movement to sliding sleeve from plug and perf

Movement to single entry port vs. clustered intervals

Higher rates and tonnage (greater liquids rates,

shallower liquid declines, higher EUR)

Movement to energized foam from slick water for

testing purposes

Movement back to slickwater for long term cost

reduction and efficiency of operations

Objective: Higher EUR / Shallower Decline in Liquids

Innovation Driving Economic Recovery17

What Does This All Mean?

18

Blackbird 2-20 Well Results

Blackbird has recently released the results from its latest well, the 2-20.

The results are seen in the table below:

The 2-20 is one of the top-tier wells in the region for the Middle Montney

Successfully de-risks 25 sections of the Middle Montney

Significant Behind Pipe ProductionNote: management estimate based on test rates and independent third party analysis 19

WellAverage Flowing Casing Pressure

(kPa) (1)

Raw Gas (MMcf/d) (2)

Liquid Hydrocarbons (Bbls/d) (2) (3)

Total Combined Production (Boe/d) (2)

Liquids to Gas Ratio

(Bbls/MMcf)2-20

7,973 6.8 641 1,768 94

Type Curve (5) 3.25 439 981 135

(1) The 2-20 well produced through a 19.05 millimeter choke at the beginning of the final 24 hour test period and a 21.30 millimeter

choke at the end of the final 24 hour test period.

(2) The 2-20 well average rates over the final 24 hours of the test.

(3) The 2-20 well total liquid hydrocarbons are comprised of 316 Bbls of free condensate and 325 Bbls of natural gas liquids based on

the composition from the 6-26 gas analysis.

(4) Blackbird’s Elmworth Middle Montney type curve based on internal best estimates and publicly available data.

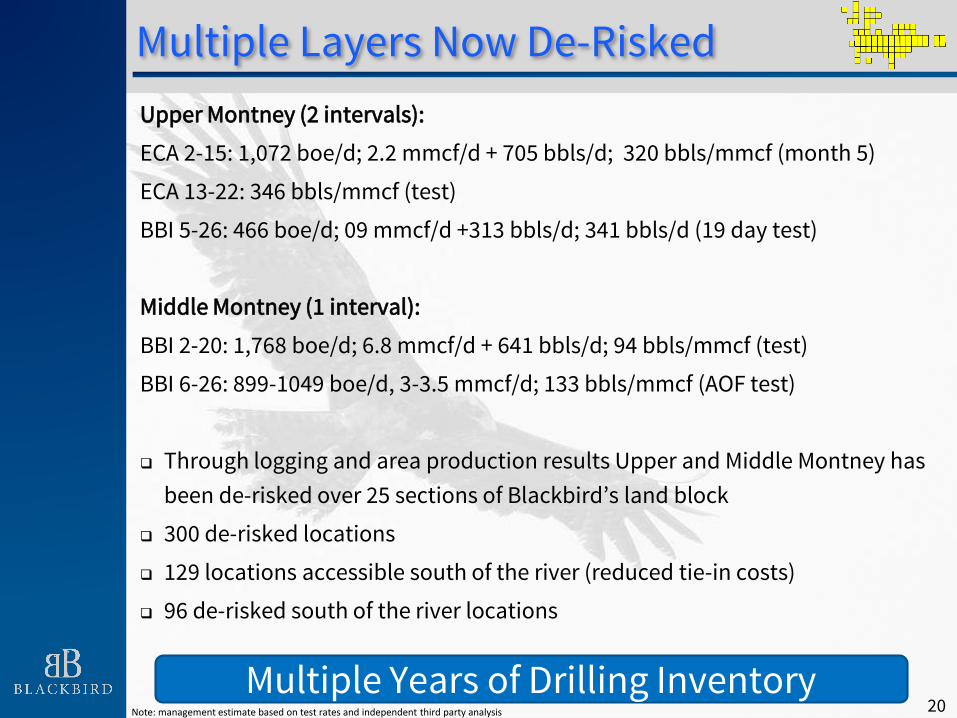

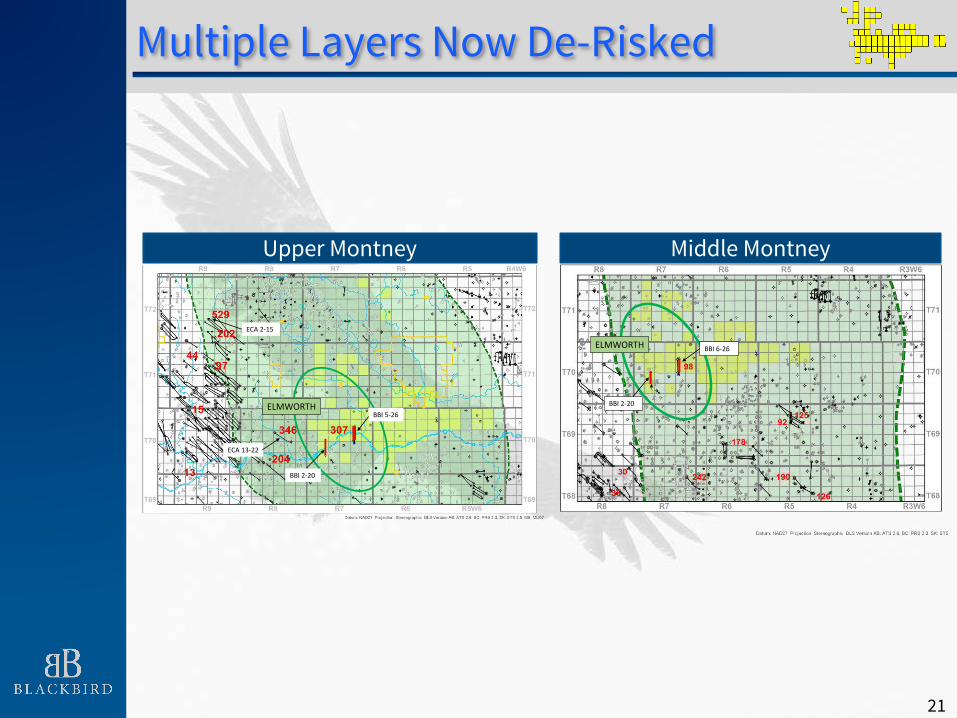

Multiple Layers Now De-Risked

Upper Montney (2 intervals):

ECA 2-15: 1,072 boe/d; 2.2 mmcf/d + 705 bbls/d; 320 bbls/mmcf (month 5)

ECA 13-22: 346 bbls/mmcf (test)

BBI 5-26: 466 boe/d; 09 mmcf/d +313 bbls/d; 341 bbls/d (19 day test)

Middle Montney (1 interval):

BBI 2-20: 1,768 boe/d; 6.8 mmcf/d + 641 bbls/d; 94 bbls/mmcf (test)

BBI 6-26: 899-1049 boe/d, 3-3.5 mmcf/d; 133 bbls/mmcf (AOF test)

Through logging and area production results Upper and Middle Montney has

been de-risked over 25 sections of Blackbird’s land block

300 de-risked locations

129 locations accessible south of the river (reduced tie-in costs)

96 de-risked south of the river locations

Multiple Years of Drilling InventoryNote: management estimate based on test rates and independent third party analysis 20

Multiple Layers Now De-Risked

21

BBI 6-26

BBI 2-20

ELMWORTH

ECA 2-15

ECA 13-22

BBI 5-26

BBI 2-20

ELMWORTH

Upper Montney Middle Montney

What is Next?

22

Infrastructure Development

Blackbird has established a near-term

solution for takeaway which can handle

sour gas:

Processing arrangement starting from 5

mmcf/d + associated liquids (~1,500

boe/d);

Ability to scale processing capacity

upwards from 10 mmcf/d to 30 mmcf/d;

Multiple options available for long term

capacity both north and south of the

Wapiti, which will allow production to

exceed 30 mmcf/d.

Blackbird sees four potential solutions

for future expansion above and beyond

30 mmcf/d.

Near Term Movement To Cash FlowNote: management estimate based on test rates and independent third party analysis 23

Resource Development

Next Steps:

Proceed with development on Western Acreage (70% Upper, 30% Middle)

Staged, Low Risk Development Plan24

129 locations south of Wapiti River

8 years of drilling inventory (base case)

North of the Wapiti to be accessed by ~Q2 2018

Blackbird 2-20-70-7W6 Blackbird 5-26-70-7W6

Blackbird 6-26-70-7W6

Initial development split between (70% Upper and 30% Middle)

Strong land position in one of the most economic

plays in Canada – correct revenue / boe cocktail

(high CGR)

Management team that is aligned with

shareholders and that has shown an ability to

solve the impediments of success

Strong balance sheet that allows for organic

growth through drill bit

Blackbird has a plan to create value

Low cost entry point with catalysts to come

Why You Should Buy and Hold

25

Blackbird has committed to offset its environmental impact

through planting trees in NW Alberta with the Carbon Farmer

Asking stakeholders and friends to support initiative as well

Goal of 100,000 trees

Blackbird has committed 5,000 trees

National Bank Financial has committed 7,000 trees

Raymond James has committed to 750 trees

Each tree costs $1.99

Go to our website to learn more:

www.blackbirdenergyinc.com

Tree Planting Pledge

26

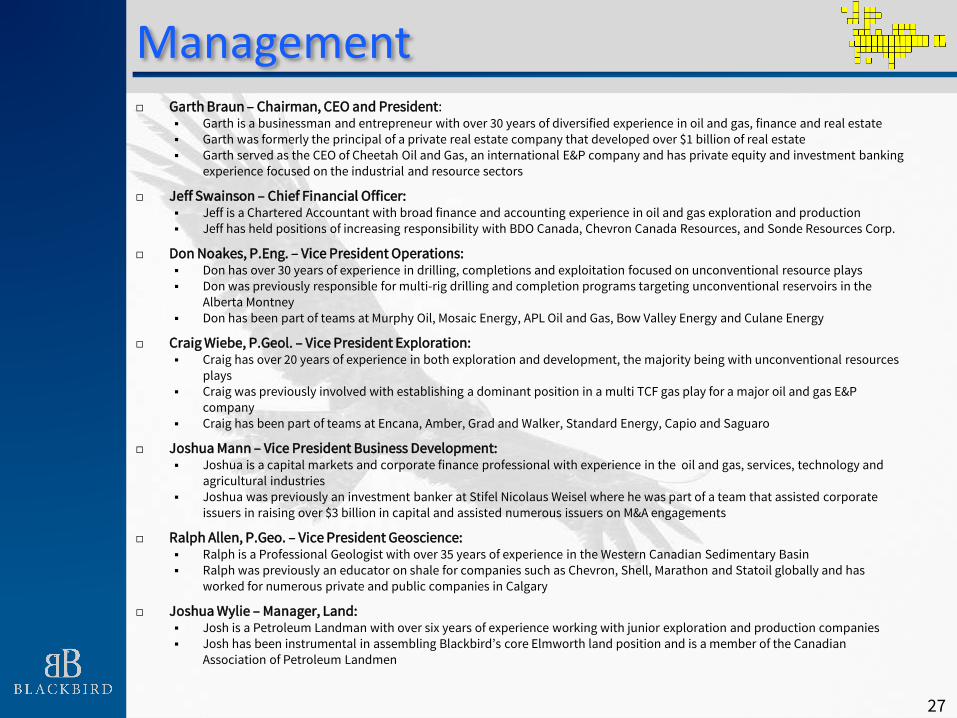

Management Garth Braun – Chairman, CEO and President:

Garth is a businessman and entrepreneur with over 30 years of diversified experience in oil and gas, finance and real estate Garth was formerly the principal of a private real estate company that developed over $1 billion of real estate Garth served as the CEO of Cheetah Oil and Gas, an international E&P company and has private equity and investment banking

experience focused on the industrial and resource sectors

Jeff Swainson – Chief Financial Officer: Jeff is a Chartered Accountant with broad finance and accounting experience in oil and gas exploration and production Jeff has held positions of increasing responsibility with BDO Canada, Chevron Canada Resources, and Sonde Resources Corp.

Don Noakes, P.Eng. – Vice President Operations: Don has over 30 years of experience in drilling, completions and exploitation focused on unconventional resource plays Don was previously responsible for multi-rig drilling and completion programs targeting unconventional reservoirs in the

Alberta Montney Don has been part of teams at Murphy Oil, Mosaic Energy, APL Oil and Gas, Bow Valley Energy and Culane Energy

Craig Wiebe, P.Geol. – Vice President Exploration: Craig has over 20 years of experience in both exploration and development, the majority being with unconventional resources

plays Craig was previously involved with establishing a dominant position in a multi TCF gas play for a major oil and gas E&P

company Craig has been part of teams at Encana, Amber, Grad and Walker, Standard Energy, Capio and Saguaro

Joshua Mann – Vice President Business Development: Joshua is a capital markets and corporate finance professional with experience in the oil and gas, services, technology and

agricultural industries Joshua was previously an investment banker at Stifel Nicolaus Weisel where he was part of a team that assisted corporate

issuers in raising over $3 billion in capital and assisted numerous issuers on M&A engagements

Ralph Allen, P.Geo. – Vice President Geoscience: Ralph is a Professional Geologist with over 35 years of experience in the Western Canadian Sedimentary Basin Ralph was previously an educator on shale for companies such as Chevron, Shell, Marathon and Statoil globally and has

worked for numerous private and public companies in Calgary

Joshua Wylie – Manager, Land: Josh is a Petroleum Landman with over six years of experience working with junior exploration and production companies Josh has been instrumental in assembling Blackbird’s core Elmworth land position and is a member of the Canadian

Association of Petroleum Landmen

27

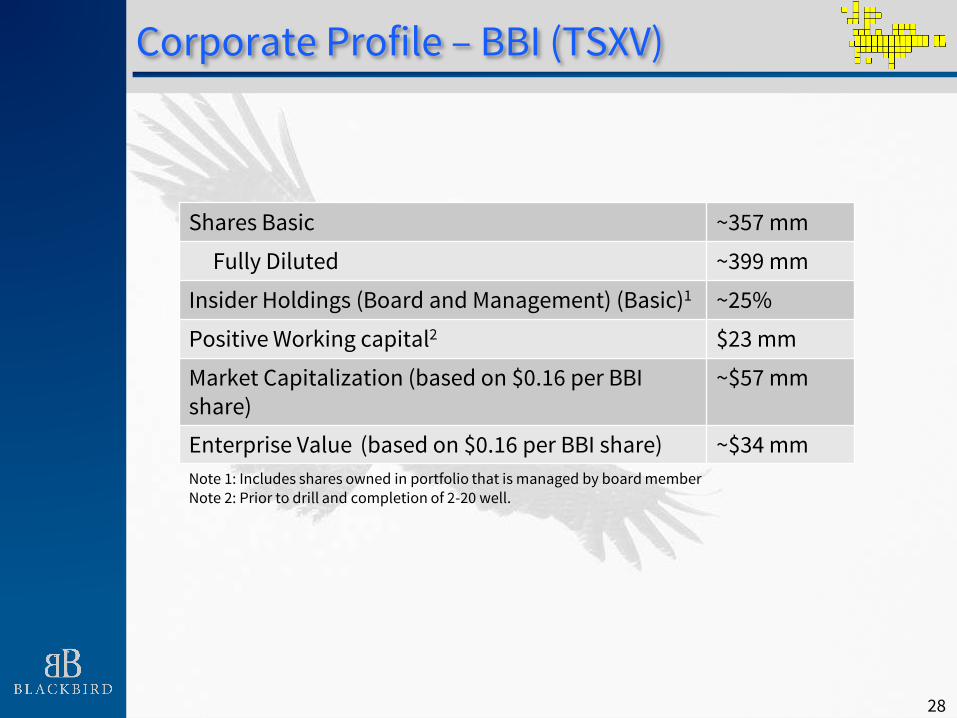

Corporate Profile – BBI (TSXV)

Note 1: Includes shares owned in portfolio that is managed by board memberNote 2: Prior to drill and completion of 2-20 well.

Shares Basic ~357 mm

Fully Diluted ~399 mm

Insider Holdings (Board and Management) (Basic)1 ~25%

Positive Working capital2 $23 mm

Market Capitalization (based on $0.16 per BBI share)

~$57 mm

Enterprise Value (based on $0.16 per BBI share) ~$34 mm

28

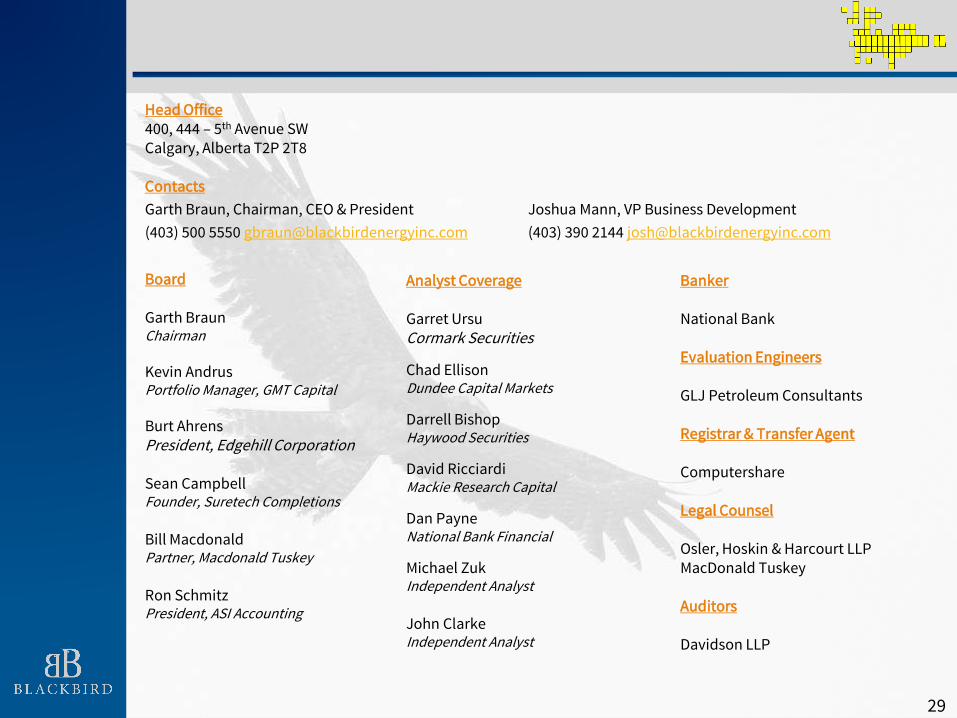

Board

Garth BraunChairman

Kevin AndrusPortfolio Manager, GMT Capital

Burt AhrensPresident, Edgehill Corporation

Sean CampbellFounder, Suretech Completions

Bill MacdonaldPartner, Macdonald Tuskey

Ron SchmitzPresident, ASI Accounting

Analyst Coverage

Garret UrsuCormark Securities

Chad EllisonDundee Capital Markets

Darrell BishopHaywood Securities

David RicciardiMackie Research Capital

Dan PayneNational Bank Financial

Michael ZukIndependent Analyst

John ClarkeIndependent Analyst

Banker

National Bank

Evaluation Engineers

GLJ Petroleum Consultants

Registrar & Transfer Agent

Computershare

Legal Counsel

Osler, Hoskin & Harcourt LLPMacDonald Tuskey

Auditors

Davidson LLP

Head Office400, 444 – 5th Avenue SWCalgary, Alberta T2P 2T8

Contacts

Garth Braun, Chairman, CEO & President Joshua Mann, VP Business Development

(403) 500 5550 [email protected] (403) 390 2144 [email protected]

29

Advisory

Forward‐Looking Statements or Information and Additional Advisories

Certain statements included in this presentation constitute forward‐looking statements or forward‐looking information under applicable securities legislation. Such forward‐looking statements or information are provided for the purpose of providing information about management's current expectations and plans relating to the future. Readers are cautioned that reliance on such information may not be appropriate for other purposes, such as making investment decisions. Forward‐looking statements or information typically contain statements with words such as "anticipate", "believe", "expect", "plan", "intend", "estimate", "propose", "project" or similar words suggesting future outcomes or statements regarding an outlook. Forward‐looking statements or information concerning Blackbird in this presentation may include, but are not limited to, statements or information with respect to: guidance, forecasts and related assumptions; capital spending and availability of cash; expected resource potential of the Elmworth project; business strategy and objectives; type curves; drilling, development and exploration activities and plans and the timing, associated costs and results thereof; commodity pricing; costs associated with operating in the oil and natural gas business; and future production levels, including the composition thereof. Forward‐looking statements or information are based on a number of factors and assumptions which have been used to develop such statements and information but which may prove to be incorrect. Blackbird believes that the expectations reflected in such forward‐looking statements or information are reasonable; however, undue reliance should not be placed on forward‐looking statements because Blackbird can give no assurance that such expectations will prove to be correct. In addition to other factors and assumptions which may be identified in this presentation, assumptions have been made regarding, among other things: the impact of increasing competition; the timely receipt of any required regulatory approvals; the ability of Blackbird to retain and obtain qualified staff, equipment and services in a timely and cost efficient manner; the ability of Blackbird to operate in a safe, efficient and effective manner; the ability of Blackbird to obtain financing on acceptable terms; the timing and costs of operating Blackbird's business; the ability of Blackbird to secure adequate product transportation; future oil and natural gas prices; currency, exchange and interest rates; the regulatory framework regarding royalties, taxes and environmental matters; and the ability of Blackbird to successfully market its oil and natural gas products. Readers are cautioned that the foregoing list is not exhaustive of all factors and assumptions which have been used.

Forward‐looking statements or information are based on current expectations, estimates and projections that involve a number of risks and uncertainties which could cause actual results to differ materially from those anticipated by Blackbird and described in the forward‐looking statements or information. These risks and uncertainties may cause actual results to differ materially from the forward‐looking statements or information. The material risk factors affecting Blackbird and its business are contained in Blackbird's Annual Information Form which is available at SEDAR at www.sedar.com. The forward‐looking statements or information contained in this presentation are made as of the date hereof and Blackbird undertakes no obligation to update publicly or revise any forward‐looking statements or information, whether as a result of new information, future events or otherwise unless required by applicable securities laws. The forward‐looking statements or information contained in this presentation are expressly qualified by this cautionary statement.

Additional Advisories

Disclosure provided herein in respect of Bbls, Bbls/d, boe, boes or boes/d may be misleading, particularly if used in isolation. A boe (barrel of oil equivalent) conversion ratio of 6 mcf per one (1) boe is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead.

The foregoing outlook and guidance has been provided to assist investors in analyzing Blackbird's anticipated development strategies and prospects and it may not be appropriate for other purposes and actual results could differ from the guidance provided above.

The TSX Venture Exchange does not accept responsibility for the adequacy or accuracy of the information contained in this presentation.

30