algoma district school board - · pdf filein our opinion, the consolidated financial...

TRANSCRIPT

Consolidated Financial Statements of

ALGOMA DISTRICT SCHOOL BOARD

Year ended August 31, 2013

KPMG LLP Telephone (705) 949-5811 Chartered Accountants Fax (705) 949-0911 111 Elgin Street, PO Box 578 Internet www.kpmg.ca Sault Ste. Marie ON P6A 5M6

KPMG LLP, is a Canadian limited liability partnership and a member firm of the KPMG network of independent member firms affiliated with KPMG International Cooperative (“KPMG International”), a Swiss entity. KPMG Canada provides services to KPMG LLP.

INDEPENDENT AUDITORS' REPORT

To the Trustees of the Algoma District School Board

We have audited the accompanying consolidated financial statements Algoma District School Board, which comprise the consolidated statement of financial position as at August 31, 2013, the consolidated statements of operations and accumulated surplus, change in net debt and cash flows for the year then ended, and notes, comprising a summary of significant accounting policies and other explanatory information.

Management's Responsibility for the Consolidated Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with the basis of accounting described in note 1 to the consolidated financial statements, and for such internal control as management determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ Responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audit. We conducted our audit in accordance with Canadian generally accepted auditing standards. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on our judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. In making those risk assessments, we consider internal control relevant to the entity's preparation and fair presentation of the consolidated financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity's internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the consolidated financial statements of the Algoma District School Board as at August 31, 2013, are prepared, in all material respects, in accordance with the basis of accounting described in note 1 to the consolidated financial statements.

Emphasis of Matter

Without modifying our opinion, we draw attention to note 1 to the consolidated financial statements which describes the basis of accounting used in the preparation of these consolidated financial statements and the significant differences between such basis of accounting and Canadian public sector accounting standards.

Comparative Information

The financial statements of the Algoma District School Board as at and for the year ended August 31, 2012 were audited by another auditor who expressed an unmodified opinion on the statements on December 5, 2012.

Chartered Accountants, Licensed Public Accountants

December 3, 2013

Sault Ste. Marie, Canada

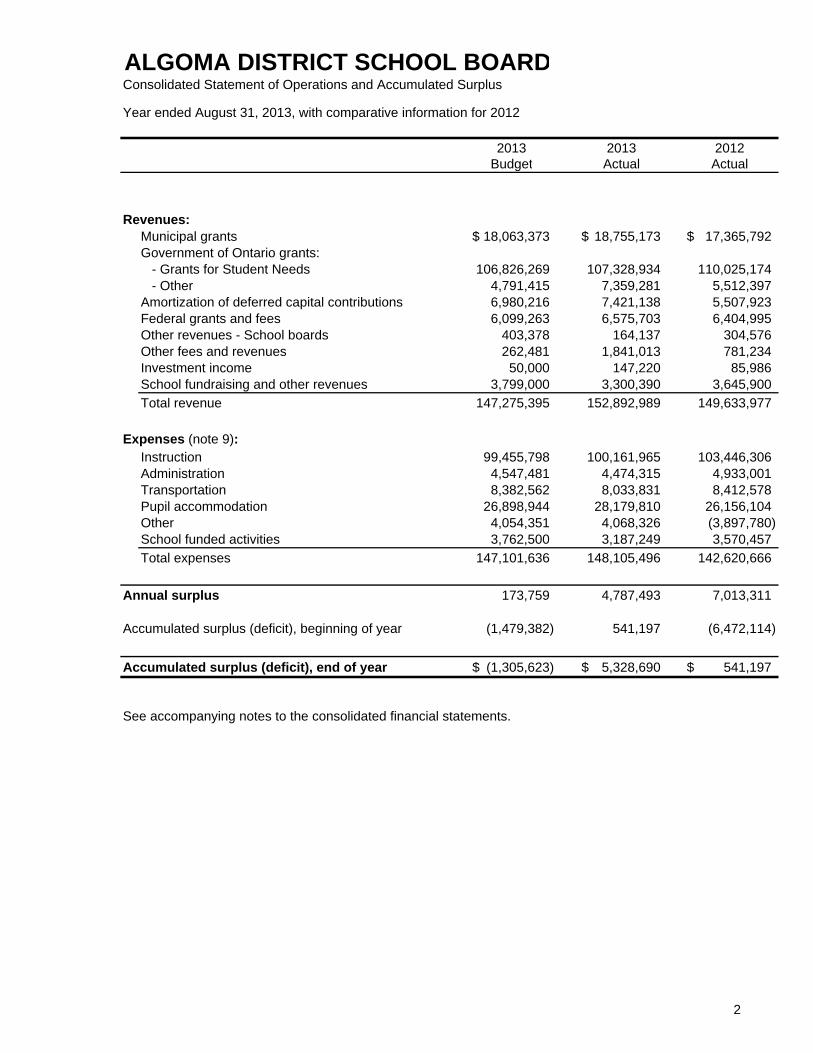

ALGOMA DISTRICT SCHOOL BOARDConsolidated Statement of Operations and Accumulated Surplus

Year ended August 31, 2013, with comparative information for 2012

2013 2013 2012Budget Actual Actual

Revenues:Municipal grants 18,063,373$ 18,755,173$ 17,365,792$ Government of Ontario grants: - Grants for Student Needs 106,826,269 107,328,934 110,025,174 - Other 4,791,415 7,359,281 5,512,397 Amortization of deferred capital contributions 6,980,216 7,421,138 5,507,923 Federal grants and fees 6,099,263 6,575,703 6,404,995 Other revenues - School boards 403,378 164,137 304,576 Other fees and revenues 262,481 1,841,013 781,234 Investment income 50,000 147,220 85,986 School fundraising and other revenues 3,799,000 3,300,390 3,645,900

Total revenue 147,275,395 152,892,989 149,633,977

Expenses (note 9):Instruction 99,455,798 100,161,965 103,446,306 Administration 4,547,481 4,474,315 4,933,001 Transportation 8,382,562 8,033,831 8,412,578 Pupil accommodation 26,898,944 28,179,810 26,156,104 Other 4,054,351 4,068,326 (3,897,780) School funded activities 3,762,500 3,187,249 3,570,457

Total expenses 147,101,636 148,105,496 142,620,666

Annual surplus 173,759 4,787,493 7,013,311

Accumulated surplus (deficit), beginning of year (1,479,382) 541,197 (6,472,114)

Accumulated surplus (deficit), end of year (1,305,623)$ 5,328,690$ 541,197$

See accompanying notes to the consolidated financial statements.

2

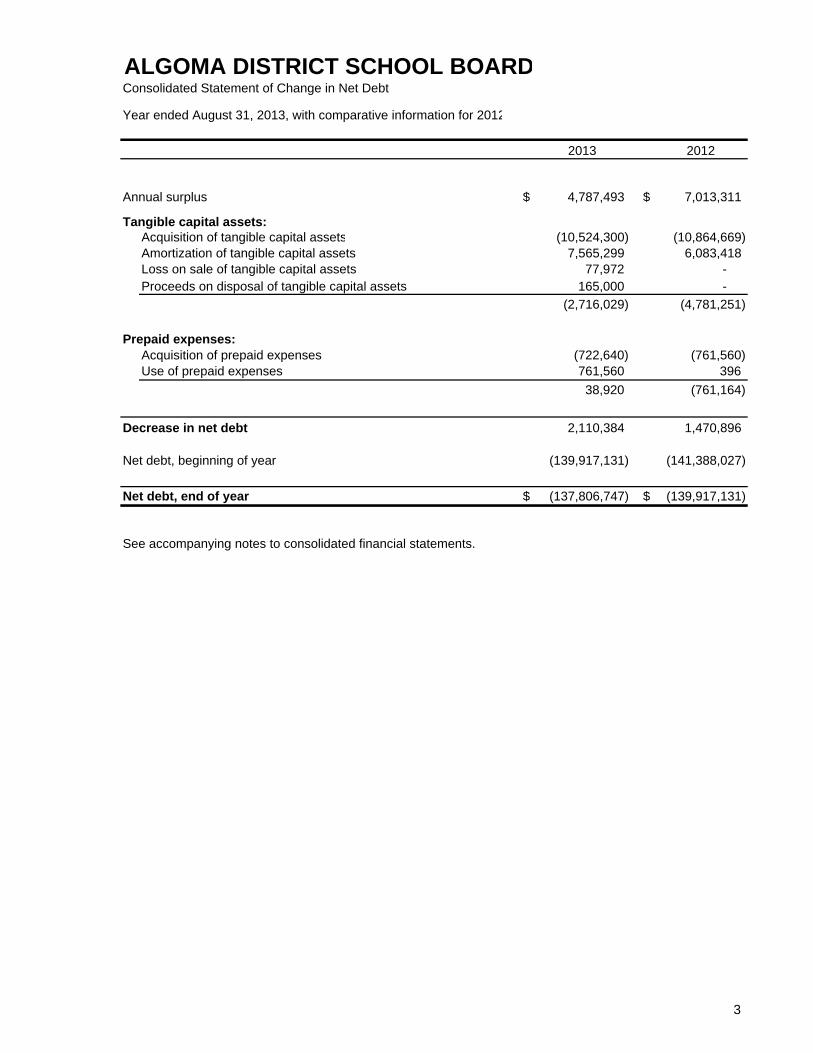

ALGOMA DISTRICT SCHOOL BOARDConsolidated Statement of Change in Net Debt

Year ended August 31, 2013, with comparative information for 2012

2013 2012

Annual surplus $ 4,787,493 $ 7,013,311

Tangible capital assets:Acquisition of tangible capital assets (10,524,300) (10,864,669) Amortization of tangible capital assets 7,565,299 6,083,418 Loss on sale of tangible capital assets 77,972 - Proceeds on disposal of tangible capital assets 165,000 -

(2,716,029) (4,781,251)

Prepaid expenses:Acquisition of prepaid expenses (722,640) (761,560) Use of prepaid expenses 761,560 396

38,920 (761,164)

Decrease in net debt 2,110,384 1,470,896

Net debt, beginning of year (139,917,131) (141,388,027)

Net debt, end of year $ (137,806,747) $ (139,917,131)

See accompanying notes to consolidated financial statements.

3

ALGOMA DISTRICT SCHOOL BOARDConsolidated Statement of Cash Flows

Year ended August 31, 2013, with comparative information for 2012

2013 2012

Operating transactions:Annual surplus $ 4,787,493 $ 7,013,311

Items not involving cash:Amortization of tangible capital assets 7,565,299 6,083,418 Amortization of deferred capital contributions (7,421,138) (5,507,923) Loss on sale of tangible capital assets 77,972 -

5,009,626 7,588,806 Change in non-cash assets and liabilities:

Decrease (increase) in accounts receivable 1,003,952 (1,500,740) Increase (decrease) in accounts payable and accrued liabilities 1,949,644 (10,198,303) Increase (decrease) in deferred revenue (1,031,892) 2,750,689 Decrease in employee future benefits (1,006,686) (8,608,918) Decrease (increase) in prepaid expenses 38,920 (761,163)

Cash provided by operating transactions 5,963,564 (10,729,629)

Capital transactions:Cash used to acquire tangible capital assets (10,524,300) (10,864,669) Proceeds on disposal of tangible capital assets 165,000 -

Cash applied to capital transactions (10,359,300) (10,864,669)

Financing transactions:Long-term liabilities issued 5,257,714 72,428,764 Decrease in temporary borrowings - (57,854,792) Debt principal repayments (2,399,249) (632,883) Increase in accounts receivable - Approved Capital Funding 2,134,435 - Additions to deferred capital contributions 9,769,151 10,864,669

Cash provided by financing transactions 14,762,051 24,805,758

Increase in cash 10,366,315 3,211,460

Cash, beginning of year 10,203,500 6,992,040

Cash, end of year $ 20,569,815 $ 10,203,500

See accompanying notes to consolidated financial statements.

4

5

ALGOMA DISTRICT SCHOOL BOARD Notes to Consolidated Financial Statements Year ended August 31, 2013

The principal activity of the Algoma District School Board (the “Board’) is to administer the operations of the English elementary and secondary schools in the District of Algoma.

1. Significant accounting policies:

The consolidated financial statements of the Board have been prepared by management in accordance with the basis of accounting described below. The consolidated financial statements contain the following significant accounting policies:

(a) Basis of accounting:

The consolidated financial statements have been prepared in accordance with the Financial Administration Act supplemented by Ontario Ministry of Education memorandum 2004:B2 and Ontario Regulation 395/11 of the Financial Administration Act.

The Financial Administration Act requires that the consolidated financial statements be prepared in accordance with the accounting principles determined by the relevant ministry of the Government of Ontario. A directive was provided by the Ontario Ministry of Education within memorandum 2004:B2 requiring school boards to adopt Canadian public sector accounting standards commencing with their year ended August 31, 2004 and that changes may be required to the application of these standards as a result of regulation.

In 2011, the government passed Ontario Regulation 395/11 of the Financial Administration Act. The regulation requires that contributions received or receivable for the acquisition or development of depreciable tangible capital assets and contributions of depreciable tangible capital assets for use in providing services, be recorded as deferred capital contributions and be recognized as revenue in the statement of operations and accumulated surplus over the periods during which the asset is used to provide service at the same rate that amortization is recognized in respect of the related asset. The regulation further requires that if the net book value of the depreciable tangible capital asset is reduced for any reason other than amortization, a proportionate reduction of the deferred capital contribution along with a proportionate increase in the revenue be recognized. For Ontario school boards, these contributions include government transfers, externally restricted contributions and, historically, property tax revenue.

The accounting policy requirements under Ontario Regulation 395/11 are significantly different from the requirements of Canadian public sector accounting standards which require that:

government transfers, which do not contain a stipulation that creates a liability, be recognized as revenue by the recipient when approved by the transferor and the eligibility criteria have been met in accordance with public sector accounting standard PS3410;

externally restricted contributions be recognized as revenue in the period in which the resources are used for the purpose or purposes specified in accordance with public sector accounting standard PS3100; and

property taxation revenue be reported as revenue when received or receivable in accordance with public sector accounting standard PS3510.

6

ALGOMA DISTRICT SCHOOL BOARD Notes to Consolidated Financial Statements Year ended August 31, 2013

1. Significant accounting policies:

(a) Basis of accounting (continued):

As a result, revenue recognized in the statement of operations and accumulated surplus and certain related deferred revenues and deferred capital contributions would be recorded differently under Canadian public sector accounting standards.

(b) Reporting entity:

The consolidated financial statements reflect the assets, liabilities, revenues and expenses of the reporting entity. The reporting entity is comprised of all organizations accountable for the administration of their financial affairs and resources to the Board and which are controlled by the Board.

The consolidated financial statements include the following organizations:

(i) School generated funds: the assets, liabilities, revenues, expenses that exist at the school level and which are deemed to be controlled by the Board, have been reflected in the consolidated financial statements.

Interdepartmental and inter-organizational transactions are eliminated in these financial statements.

(c) Trust funds:

Trust funds and their operations administered by the Board are not included in the consolidated financial statements as they are not controlled by the Board.

(d) Government transfers:

Government transfers, which include legislative grants, are recognized in the consolidated financial statements in the period in which events giving rise to the transfer occur, providing the transfers are authorized, any eligibility criteria have been met and reasonable estimates of the amount can be made.

Government transfers for the purchase or development of tangible capital assets are recorded as deferred capital contributions as described in note 1(j).

(e) Cash and cash equivalents:

Cash and cash equivalents comprise of cash on hand, demand deposits and short-term investments. Short-term investments are highly liquid, subject to insignificant risk of changes in value and have a short maturity term of less than 90 days.

(f) Non-financial assets:

Non-financial assets are not available to discharge existing liabilities and are held for use in the provision of services. They have useful lives extending beyond the current year and are not intended for sale in the ordinary course of operations.

7

ALGOMA DISTRICT SCHOOL BOARD Notes to Consolidated Financial Statements Year ended August 31, 2013

1. Significant accounting policies (continued):

(g) Tangible capital assets:

Tangible capital assets are recorded at historical cost less accumulated amortization. Historical cost includes amounts that are directly attributable to acquisition, construction, development or betterment of the asset. The Board does not capitalize interest paid on debt used to finance the construction of tangible capital assets. When historical records were not available, other methods were used to estimate the cost and accumulated amortization.

Tangible capital assets, excluding land, are amortized on a straight-line basis over their estimated useful lives as follows:

Land improvements 15 years Buildings 40 years Portable structures 20 years First-time equipping 10 years Furniture 10 years Equipment 5 - 10 years Computer hardware 5 years Computer software 5 years Vehicles 5 - 10 years Capital leases – computer hardware Term of lease

Amortization is taken at 50% of the above rates in the year of acquisition, except for capital leases.

Assets under construction are not amortized until the assets are available for productive use.

Buildings permanently removed from service and held for resale cease to be amortized and are recorded at the lower of carrying value and estimated net realizable value.

(h) Deferred revenue:

The Board receives amounts pursuant to legislation, regulation or agreement that may only be used for certain programs or in the delivery of specific services and transactions. These amounts are recognized as revenue in the fiscal year the related expenditures are incurred or services performed.

(i) Investment income:

Investment income earned is reported as revenue in the period earned.

Investment income earned on externally appropriated funds such as pupil accommodation, special education, energy efficient schools capital and proceeds of disposition, when required by the funding government or related Act, is added to the fund balance and forms part of the respective deferred revenue balances.

8

ALGOMA DISTRICT SCHOOL BOARD Notes to Consolidated Financial Statements Year ended August 31, 2013

1. Significant accounting policies (continued):

(j) Deferred capital contributions:

Contributions received or receivable for the purpose of acquiring or developing a depreciable tangible capital asset for use in providing services, or any contributions of depreciable tangible capital assets received or receivable for use in providing services, are recorded as deferred capital contributions when the asset is acquired as required under Ontario Regulation 395/11 of the Financial Administration Act. Amounts are recognized into revenue at the same rate as the related tangible capital asset is amortized.

(k) Retirement and other employee future benefits:

The Board provides defined retirement and other future benefits to specified employee groups. These benefits include pension, life insurance and health care benefits, retirement gratuity, service awards, worker’s compensation and long-term disability benefits. The Board accrues its obligation for these employee benefits. In 2013, changes were made to the Board’s short-term leave and disability plan. The Board has adopted the following policies with respect to accounting for these employee benefits:

(i) The costs of self insured retirement and other employee future benefit plans are actuarially determined using management’s best estimate of salary escalation, accumulated sick days, insurance and health care costs trends, disability recovery rates, long-term inflation rates and discount rates. In prior years, the cost of retirement gratuities that vested or accumulated over the periods of service provided by the employee were actuarially determined using management’s best estimate of salary escalation, accumulated sick days at retirement and discount rates. As a result of the plan change, the cost of retirement gratuities are actuarially determined using the employee’s salary, banked sick days and years of service as at August 31, 2012 and management’s best estimate of discount rates. The changes resulted in a plan curtailment and any unamortized actuarial gains and losses were recognized as at August 31, 2012. Any actuarial gains and losses arising from changes to the discount rate are amortized over the expected average remaining services life of the employee group.

For self-insured retirement and other employee future benefits that vest or accumulate over the periods of service provided by employees, such as life insurance and health care benefits for retirees, the cost is actuarially determined using the projected benefits method prorated on service. Under this method, the benefit costs are recognized over the expected average service life of the employee group.

For those self-insured benefit obligations that arise from specific events that occur from time to time, such as obligations for worker’s compensation, long-term disability and life insurance and health care benefits for those on disability leave, the cost is recognized immediately in the period the events occur. Any actuarial gains and losses that are related to these benefits are recognized immediately in the period they arise.

9

ALGOMA DISTRICT SCHOOL BOARD Notes to Consolidated Financial Statements Year ended August 31, 2013

1. Significant accounting policies (continued):

(k) Retirement and other employee future benefits (continued):

(ii) The costs of multi-employer defined pension plan benefits, such as the Ontario Municipal Employees Retirement System (“OMERS”) pensions, are the employer’s contributions due to the plan in the period.

(iii) The costs of insured benefits are the employer’s portion of insurance premiums owed for coverage of employees during the period.

(l) Budget figures:

Budget figures have been provided for comparison purposes and have been derived from the budget provided by the Board.

The budget approved by the Board is developed in accordance with the provincially mandated funding model for school boards and is used to manage program spending within the guidelines of the funding model.

The Board approves the budget annually. The approved budget for 2012-2013 is reflected on the Consolidated Statement of Operations and Accumulated Surplus.

(m) Use of estimates:

The preparation of consolidated financial statements in conformity with the basis of accounting described in note 1(a) requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements, and the reported amounts of revenues and expenses during the year. Actual results could differ from those estimates. These estimates are reviewed periodically, and, as adjustments become necessary, they are reported in earnings in the year in which they become known. Significant estimates include assumptions used in:

(i) estimating provisions for accrued liabilities, and

(ii) performing actuarial valuations of employee future benefits liabilities

10

ALGOMA DISTRICT SCHOOL BOARD Notes to Consolidated Financial Statements

Year ended August 31, 2013

2. Adoption of new accounting standard:

On September 1, 2012, the Board adopted Public Sector Accounting Standard PS 3510 – Tax Revenue. The standard was adopted retrospectively. The new standard provides guidance on the entities who are able to record tax revenue on their financial statements.

Under PS 3510, only the entity that levies the tax will record tax revenue in their financial statements. All other entities who receive revenue from taxes as transfers from the original taxing authority (the Province of Ontario) will record these amounts as grants in their financial statements.

As a result of adopting PS 3510, the Board now records the tax revenue received from Municipalities as Municipal grants.

3. Accounts receivable - other:

2013 2012

Government of Ontario $ – $ 1,143,484 Government of Canada 347,716 – First Nations 1,521,424 746,676 Local governments 2,323,446 2,229,081 Other school boards 146,322 289,576 Other 1,170,936 2,104,979

$ 5,509,844 $ 6,513,796

4. Accounts receivable – Approved Capital Funding:

The Government of Ontario replaced variable capital funding with a one-time debt support grant in 2009-10. The Board received a one-time grant that recognizes capital debt as of August 31, 2010 that is supported by the existing capital programs. The Board receives this grant in cash over the remaining term of the existing capital debt instruments. The Board may also receive yearly capital grants to support capital programs which would be reflected in this account receivable.

11

ALGOMA DISTRICT SCHOOL BOARD Notes to Consolidated Financial Statements

Year ended August 31, 2013

5. Net long-term liabilities:

Net long-term liabilities reported on the Consolidated Statement of Financial Position consist of

the following:

2013 2012

Long-term debt:

Loans payable to the Ontario Financing Authority with interest rates ranging from 3.56% to 5.232%, due in semi-annual installments including interest, with maturity dates ranging from November 2031 to May 2038 $ 94,763,184 $ 91,904,531

Capital Leases:

Macquarie Equipment Finance Ltd. capital lease due $109,470 annually including interest at 6.75% per annum, matured September 2012 – 102,468

Concentra capital lease due $22,478 annually including interest at 6.75% per annum, matured September 2012 – 21,046

IBM capital lease due $46,155 annually including interest at 4% per annum, matured September 2012 – 44,345

IBM capital lease due $36,932 annually including interest at 4% per annum, matured September 2012 – 35,484

Dell capital lease due $53,663 annually including interest at 4% per annum, maturing September 2013 51,367 101,133

CSI Leasing Canada capital lease due $39,586 annually including interest at 11.99% per annum, maturing September 2013 35,348 66,911

Pacific and Western Bank of Canada capital lease due $142,128 annually including interest at 5.93% per annum, maturing September 2014 260,833 380,403

Lenovo Financial Services capital lease due $25,075 annually including interest at 6% per annum, maturing September 2014 45,972 67,025

Pacific and Western Bank of Canada capital lease due $59,318 annually including interest at 6% per annum, maturing September 2015 158,558 205,543

Compugen Finance Inc. capital lease due $58,694 annually including interest at 6% per annum, maturing September 2015 156,889 203,380

Carried forward 95,472,151 93,132,269

12

ALGOMA DISTRICT SCHOOL BOARD Notes to Consolidated Financial Statements

Year ended August 31, 2013

5. Net long-term liabilities (continued):

2013 2012

Brought forward $ 95,472,151 $ 93,132,269 De Lage Lander Financial Services capital lease due

$18,995 annually including interest at 6% per annum, maturing September 2015 34,825 –

Pacific and Western Bank of Canada capital lease due $90,482 annually including interest at 6% per annum, maturing September 2016 241,857 –

Pacific and Western Bank of Canada capital lease due $69,811 annually including interest at 6% per annum, maturing September 2017 241,901 –

$ 95,990,734 $ 93,132,269

Included in the consolidated statements of operations and accumulated surplus is interest on long-term debt and capital leases paid of $ 3,622,390 (2012 - $2,272,032).

Principal and interest payments relating to long-term debt and capital leases outstanding are due as follows:

Principal Interest Total

2013-2014 $ 3,103,881 $ 3,908,838 $ 7,012,719 2014-2015 3,142,980 3,654,702 6,797,682 2015-2016 3,088,071 3,655,949 6,744,020 2016-2017 3,005,521 3,542,714 6,548,235 2017-2018 3,054,476 3,522,266 6,576,742 Thereafter 80,595,805 31,579,959 112,175,764

$ 95,990,734 $ 49,864,428 $ 145,855,162

13

ALGOMA DISTRICT SCHOOL BOARD Notes to Consolidated Financial Statements

Year ended August 31, 2013

6. Deferred revenue:

Deferred revenue consists of amounts received by the Board that are restricted for specific purposes by the funder and amounts that are required to be set aside by the Board for specific purposes, legislation, regulation or agreement.

Deferred revenue is comprised of:

2013 2012

Amounts restricted by legislation, regulation or agreement: Pupil accommodation $ 3,667,904 $ 3,477,190 Proceeds of disposition 166,109 318 Provincial grants 1,532,802 1,886,079 Green school pilot initiative – 54,704 School condition improvement 594,642 1,804,453 School funds capital – 52,903 Child care retrofit 282,298 –

$ 6,243,755 $ 7,275,647

7. Employee future benefits:

The Board provides defined retirement and other future benefits to specified employee groups. These benefits include pension, life insurance and health care benefits, retirement gratuity, worker’s compensation and long-term disability benefits.

a) Plan changes:

During the year, further changes were made to the short term leave and disability plan. Under the new short term leave and disability plan, 11 unused sick leave days may be carried forward into the following year only, to be used to top-up benefits received under the short term leave and disability plan in that year. A new provision was established as of August 31, 2013 representing the expected usage of sick days that have been carried forward for benefit top-up in the following year.

Retirement life insurance, health and dental benefits have been grandfathered to existing retirees and employees who retired between September 1, 2012 and August 31, 2013. Effective September 1, 2013, any new retiree accessing retirement life, health or dental benefits will pay the full premiums for such benefits and will be included in a separate experience pool for participating retirees that is self-funded which has been the past procedure for the Algoma District School Board.

14

ALGOMA DISTRICT SCHOOL BOARD Notes to Consolidated Financial Statements

Year ended August 31, 2013

7. Employee future benefits (continued):

b) Retirement benefits:

(i) Ontario Teacher’s Pension Plan:

Teachers and related employee groups are eligible to be members of Ontario Teacher’s Pension Plan. Employer contributions for these employees are provided directly by the Province of Ontario. The pension costs and obligations related to this plan are a direct responsibility of the Province. Accordingly, no costs or liabilities related to this plan are included in the Board’s consolidated financial statements.

(ii) Ontario Municipal Employees Retirement System:

All non-teaching employees of the Board are eligible to be members of the Ontario Municipal Employees Retirement System (OMERS), a multi-employer pension plan. The plan provides defined pension benefits to employees based on their length of service and rates of pay. The Board contributions equal the employee contributions to the plan. During the year ended August 31, 2013, the Board contributed $1,624,381 (2012 - $1,552,858) to the plan. As this is a multi-employer pension plan, these contributions are the Board’s pension benefit expenses. No pension liability for this type of plan is included in the Board’s consolidated financial statements.

(iii) Retirement gratuities:

The Board provides retirement gratuities to certain groups of employees hired prior to specified dates. The Board provides these benefits through an unfunded defined benefit plan. The benefit costs and liabilities related to this plan are included in the Board’s consolidated financial statements. In the prior year, the amount of gratuities payable to eligible employees at retirement was based on their salary, accumulated sick days, and years of service at retirement. As a result of the plan change, the amount of the gratuities payable to eligible employees at retirement is now based on their salary, accumulated sick days, and years of service at August 31, 2013. The changes to the Board’s retirement gratuity plan resulted in a one-time increase to the Board’s obligation of $424,000 and a corresponding curtailment loss was reported in the consolidated statement of operations and accumulated surplus as at August 31, 2013.

15

ALGOMA DISTRICT SCHOOL BOARD Notes to Consolidated Financial Statements Year ended August 31, 2013

7. Employee future benefits (continued):

c) Other employee future benefits:

(i) Workplace Safety and Insurance Board Obligations:

The Board is a Schedule 2 employer under the Workplace Safety and Insurance Act and, as such, assumes responsibility for the payment of all claims to its injured workers under the Act. The Board does not fund these obligations in advance of payments made under the Act. The benefit costs and liabilities related to this plan are included in the Board’s consolidated financial statements. Plan changes made in 2012 require the Board to provide a salary top-up to a maximum of 4 ½ years for employees receiving payments from the Workplace Safety and Insurance Board, where previously negotiated collective agreements included such provision.

(ii) Long-term disability life insurance:

The Board provides life insurance benefits to employees on long-term disability leave. The Board is responsible for the payment of life insurance premiums under this plan. The Board provides these benefits through an unfunded defined benefit plan. The costs of salary compensation paid to employees on long-term disability leave are fully insured and not included in this plan.

(iii) Service awards:

The Board provides a one-time service award to teachers, principals and vice-principals upon achievement of the service requirements. Effective September 1, 2012, only teachers, principals and vice-principals that have met the required three consecutive years of service as of August 31, 2013 are eligible for the one-time service award benefit. The changes to the Board’s service awards resulted in a one-time reduction to the Board’s obligation of $247,500 and a corresponding curtailment gain was reported in the consolidated statement of operations and accumulated surplus as at August 31, 2013.

(iv) Accumulated sick leave:

As a result of the plan changes, the Board’s liability related to compensated absences from sick leave accumulations was eliminated, resulting in a one-time reduction to the obligation of $8,259,355 and a corresponding curtailment gain was reported in the consolidated statement of operations and accumulated surplus as at August 31, 2012.

As a result of plan changes made during 2013 to the short term leave and disability plan, a maximum of 11 unused sick leave days from the current year may be carried forward into the following year only, to be used to top-up salary for illnesses paid through the short term leave and disability plan in that year. The benefit costs expensed in the consolidated financial statements are $120,496 (2012 - $Nil).

The accrued benefit obligation for the sick leave top-up is based on an actuarial valuation for accounting purposes as at August 31, 2013. This actuarial valuation is based on assumptions about future events.

16

ALGOMA DISTRICT SCHOOL BOARD Notes to Consolidated Financial Statements Year ended August 31, 2013

7. Employee future benefits (in thousands) (continued):

The accrued benefit obligations for employee future benefit plans as at August 31, 2013 are based on the most recent actuarial valuation completed for accounting purposes as at August 31, 2013. These actuarial valuations were based on assumptions about future events. The economic assumptions used in these valuations are the Board’s best estimates of expected rates of:

2013 2012

Wage and salary escalation 0.0% 0.0% Discount on accrued benefit obligation 3.4% 3.0%

Assumed health care cost trend rates at August 31, 2013 and 2012:

2013 2012

Wage and salary escalation 8.3% 8.3% Discount on accrued benefit obligation 4.5% 4.5% Year that the rate will be ultimately reached 2030 2030

The Board has internally appropriated an amount for retirement gratuities totaling $3,418,157 (2012 - $3,385,990).

Information with respect to the Board’s retirement and other employee future benefit obligations is

as follows:

2013 2012 Other Total Total employee employee employee Retirement future future future benefits benefits benefits benefits

Accrued employee futures benefits obligations $ 5,889,267 $ 1,696,024 $ 7,585,291 $ 8,461,419 Unamortized actuarial gains (losses) (130,558) – (130,558) –

Employee future benefit liability $ 5,758,709 $ 1,696,024 $ 7,454,733 $ 8,461,419

17

ALGOMA DISTRICT SCHOOL BOARD Notes to Consolidated Financial Statements Year ended August 31, 2013

7. Employee future benefits (continued):

Accrued benefit obligation 2013 2012

Other Total Total employee employee employee Retirement future future future benefits benefits benefits benefits

Balance, beginning of year $ 6,197,509 $ 2,016,408 $ 8,213,917 $ 17,070,337

Current period benefit costs – 39,115 39,115 944,935

Interest cost 176,693 49,706 226,399 566,257

Recognized actuarial losses – – – 415,228

Benefits paid (1,039,493) (337,388) (1,376,881) (2,729,411)

Recognition of unamortized actuarial losses on plan amendments/curtailments 130,558 – 130,558 –

Curtailment loss (gain) 424,000 (71,817) 352,183 (7,805,927)

Balance, end of year 5,889,267 1,696,024 7,585,291 8,461,419

Unamortized actuarial gains (losses) (130,558) – (130,558) –

Accrued benefit liability $ 5,758,709 $ 1,696,024 $ 7,454,733 $ 8,461,419

Employee future benefit expense1 2013 2012

Other Total Total employee employee employee Retirement future future future benefits benefits benefits benefits

Current year benefit cost $ – $ 39,115 $ 39,115 $ 944,935 Interest on accrued benefit obligation 176,693 49,706 226,399 566,257 Amortization of actuarial losses (gains) – – – 415,228 Curtailment loss (gain) 424,000 (71,817) 352,183 (7,805,927)

$ 600,693 $ 17,004 $ 617,697 $ (5,879,507)

1 Excluding pension contributions to multi-employer pension plans, described in note 7(b).

18

ALGOMA DISTRICT SCHOOL BOARD Notes to Consolidated Financial Statements Year ended August 31, 2013

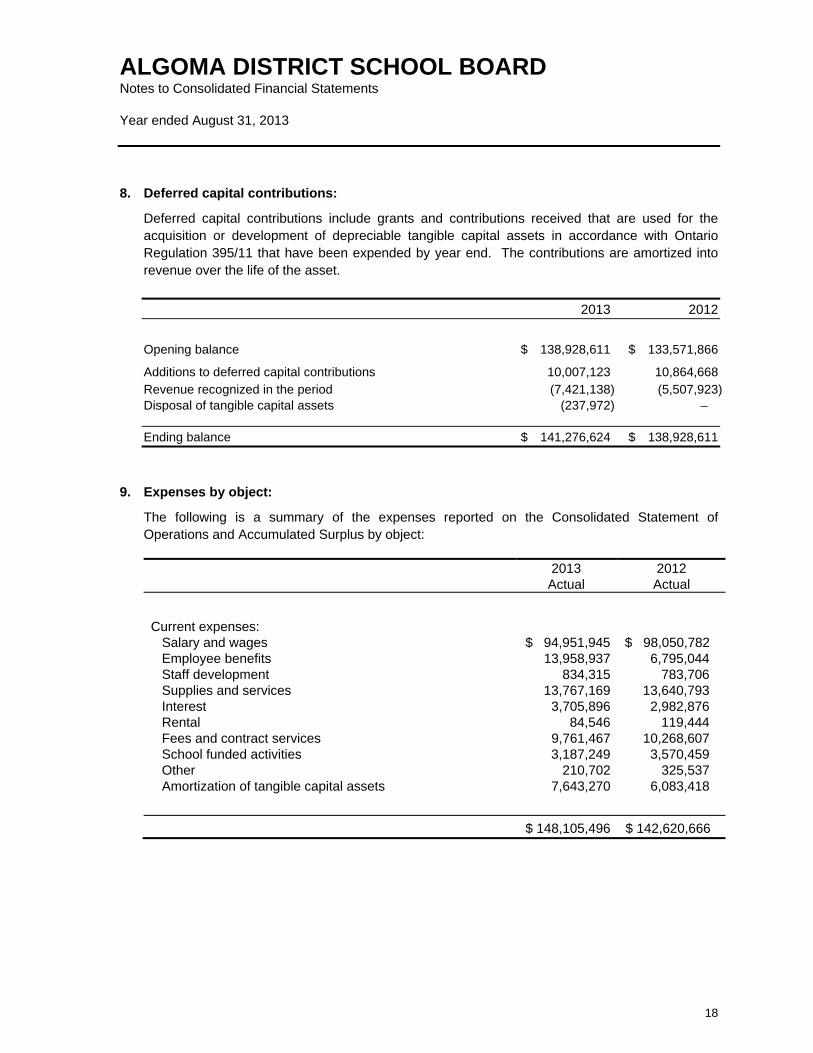

8. Deferred capital contributions:

Deferred capital contributions include grants and contributions received that are used for the acquisition or development of depreciable tangible capital assets in accordance with Ontario Regulation 395/11 that have been expended by year end. The contributions are amortized into revenue over the life of the asset.

2013 2012

Opening balance $ 138,928,611 $ 133,571,866

Additions to deferred capital contributions 10,007,123 10,864,668 Revenue recognized in the period (7,421,138) (5,507,923) Disposal of tangible capital assets (237,972) –

Ending balance $ 141,276,624 $ 138,928,611

9. Expenses by object:

The following is a summary of the expenses reported on the Consolidated Statement of Operations and Accumulated Surplus by object: 2013 2012 Actual Actual

Current expenses: Salary and wages $ 94,951,945 $ 98,050,782 Employee benefits 13,958,937 6,795,044 Staff development 834,315 783,706 Supplies and services 13,767,169 13,640,793 Interest 3,705,896 2,982,876 Rental 84,546 119,444 Fees and contract services 9,761,467 10,268,607 School funded activities 3,187,249 3,570,459 Other Amortization of tangible capital assets

210,702 7,643,270

325,537 6,083,418

$ 148,105,496 $ 142,620,666

19

ALGOMA DISTRICT SCHOOL BOARD Notes to Consolidated Financial Statements

Year ended August 31, 2013

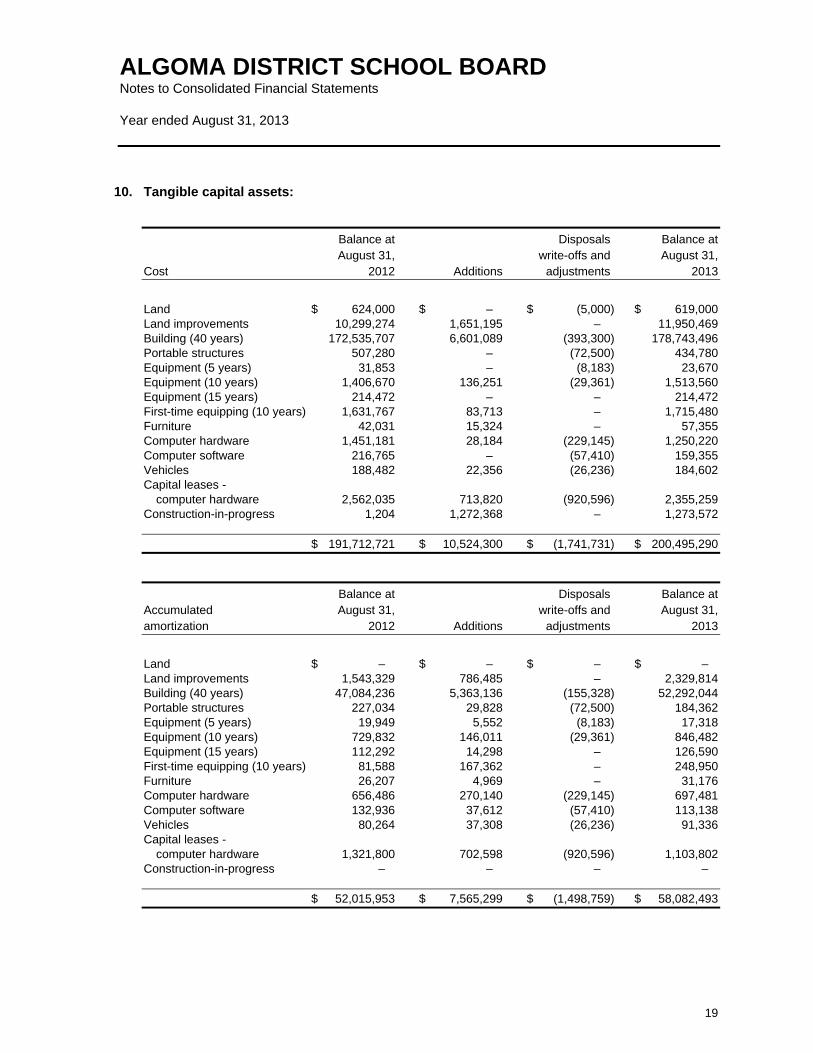

10. Tangible capital assets:

Balance at Disposals Balance at August 31, write-offs and August 31, Cost 2012 Additions adjustments 2013

Land $ 624,000 $ – $ (5,000) $ 619,000 Land improvements 10,299,274 1,651,195 – 11,950,469 Building (40 years) 172,535,707 6,601,089 (393,300) 178,743,496 Portable structures 507,280 – (72,500) 434,780 Equipment (5 years) 31,853 – (8,183) 23,670 Equipment (10 years) 1,406,670 136,251 (29,361) 1,513,560 Equipment (15 years) 214,472 – – 214,472 First-time equipping (10 years) 1,631,767 83,713 – 1,715,480 Furniture 42,031 15,324 – 57,355 Computer hardware 1,451,181 28,184 (229,145) 1,250,220 Computer software 216,765 – (57,410) 159,355 Vehicles 188,482 22,356 (26,236) 184,602 Capital leases -

computer hardware 2,562,035 713,820 (920,596) 2,355,259 Construction-in-progress 1,204 1,272,368 – 1,273,572

$ 191,712,721 $ 10,524,300 $ (1,741,731) $ 200,495,290

Balance at Disposals Balance at Accumulated August 31, write-offs and August 31, amortization 2012 Additions adjustments 2013

Land $ – $ – $ – $ – Land improvements 1,543,329 786,485 – 2,329,814 Building (40 years) 47,084,236 5,363,136 (155,328) 52,292,044 Portable structures 227,034 29,828 (72,500) 184,362 Equipment (5 years) 19,949 5,552 (8,183) 17,318 Equipment (10 years) 729,832 146,011 (29,361) 846,482 Equipment (15 years) 112,292 14,298 – 126,590 First-time equipping (10 years) 81,588 167,362 – 248,950 Furniture 26,207 4,969 – 31,176 Computer hardware 656,486 270,140 (229,145) 697,481 Computer software 132,936 37,612 (57,410) 113,138 Vehicles 80,264 37,308 (26,236) 91,336 Capital leases -

computer hardware 1,321,800 702,598 (920,596) 1,103,802 Construction-in-progress – – – –

$ 52,015,953 $ 7,565,299 $ (1,498,759) $ 58,082,493

20

ALGOMA DISTRICT SCHOOL BOARD Notes to Consolidated Financial Statements Year ended August 31, 2013

10. Tangible capital assets (continued):

Net book value Net book value August 31, 2013 August 31, 2012

Land $ 619,000 $ 624,000 Land improvements 9,620,655 8,755,945 Building (40 years) 126,451,452 125,451,471 Portable structures 250,418 280,246 Equipment (5 years) 6,352 11,904 Equipment (10 years) 667,078 676,838 Equipment (15 years) 87,882 102,180 First-time equipping (10 years) 1,466,530 1,550,179 Furniture 26,179 15,824 Computer hardware 552,739 794,695 Computer software 46,217 83,829 Vehicles 93,266 108,218 Capital leases - computer hardware 1,251,457 1,240,235 Construction-in-progress 1,273,572 1,204

$ 142,412,797 $ 139,696,768

11. Ontario School Board Insurance Exchange (OSBIE):

The school board is a member of the Ontario School Board Insurance Exchange (OSBIE), a reciprocal insurance company licensed under the Insurance Act. OSBIE insures general public liability, property damage and certain other risks. The ultimate premiums over a five-year period are based on the reciprocal’s and the Board’s actual claims experience. Periodically, the Board may receive a refund or be asked to pay an additional premium based on its pro rata share of claims experience. The current five-year term expires December 31, 2016.

12. Accumulated surplus:

Accumulated surplus consists of the following:

2013 2012

Revenues recognized for land $ 619,000 $ 624,000 Surplus available for compliance 11,400,686 7,476,494 School generated funds 2,049,265 1,936,124 Employee future benefits (7,675,261) (8,461,419) Other surplus appropriated, unavailable for compliance (1,065,000) (1,034,002)

Total accumulated surplus $ 5,328,690 $ 541,197

21

ALGOMA DISTRICT SCHOOL BOARD Notes to Consolidated Financial Statements Year ended August 31, 2013

13. Areas of jurisdictions without municipal organization:

The Board performs the duties of levying taxes, conducting elections of members, etc. in territory without organization. The outlay by the Board in 2012-2013 in respect of performing duties of municipal council is reported by area to the Ministry in a separate statement. Certain costs are recoverable through an offset to the local taxation revenue.

14. First Nation fees:

Tuition and transportation fee revenue for education services provided to First Nations’ students

for the year are as follows:

2013 2012

Chapleau Cree First Nation $ 209,886 $ 209,894 Chapleau Ojibwe 45,567 57,643 Serpent River First Nation 502,905 520,347 Thessalon First Nation 345,034 352,940 Mississauga First Nation 646,822 750,059 Brunswick House First Nation 368,953 295,593 Michipicoten First Nation 138,538 131,641 Garden River First Nation 2,607,043 2,625,395 Batchewana First Nation 1,710,955 1,461,483

$ 6,575,703 $ 6,404,995

15. Contingent liabilities:

The Board is involved in certain legal matters and litigation, the outcomes of which are not presently determinable. The loss if any, from these contingencies will be accounted for in the year in which the matters are resolved. Management is of the opinion that these matters are mitigated by adequate insurance coverage.