alternative delivery & public-private partnerships

TRANSCRIPT

© PFM 1© PFM 1© PFM 1

Alternative Delivery & Public-Private PartnershipsPFM Client Seminar

May 2021

PFM Financial Advisors LLC

.

368 Ninth Avenue

6th Floor

New York, NY 10001

212.809.4212

pfm.com

© PFM 2© PFM 2© PFM 2

Agenda

T o p i c s

O b j e c t i v e s

Introduction to Alternative Delivery (AD) and Public-Private

Partnerships (P3)

Best Practice: Evaluating AD and P3 Feasibility and Cost/Benefit

AD & P3 Financing Strategies

Understanding AD and P3s

How to determine when AD/P3s are appropriate and feasible

AD & P3s financing mechanics

1

2

3

© PFM 3© PFM 3© PFM 3

What is a “P3”?

• A “P3” is defined by the World Bank as “a long term contract between a private party and a government agency, for providing a public asset or service, in which the private party bears significant risk and management responsibility”

• The term P3 is used broadly to describe a variety of contractual arrangements, ranging from an outsourcing of an aspect of a municipal operation to the sale of a municipal asset to a private entity.

• P3s vary widely in their financial and governance structures, investor base, technical complexity and impact to the host institutions

© PFM 4© PFM 4© PFM 4

U.S. AD/P3 market and background

• P3s are not new in the U.S. – federal, state, local governments and non-profits often

rely on private sector skills, organizations, and finance to enhance or deliver public

services and projects

– Outsourced administrative services

– Building management and maintenance

– Solid waste disposal

– Social services

– Design-Build construction

– Design-Build-Finance – Turnkey project delivery

• P3s in the U.S. have become an effective tool to provide essential public services and

infrastructure projects that otherwise may have been delayed or abandoned due to

issues such as cost, complexity, and desire to avoid using balance sheet and credit

• More and more states are enacting P3 authorizing legislation and initiatives

• Private sector interest in U.S. infrastructure investment continues to grow

– Steady, predictable returns and moderate risk

© PFM 5© PFM 5© PFM 5

When is AD/P3 a value add alternative?

• New or “greenfield” projects

– Large capital initiatives

– Complex projects with higher risk due to design and construction

elements and accelerated delivery timeline

– Opportunity for “whole-life costing”

– Redevelopment and economic development

• Existing capital assets or “brownfield” projects

– Underfunded lifecycle costs and maintenance

– Improvements or expansion to existing facilities or projects

– Changing demographics and market demand allow for redevelopment

and potential repricing

• Financial considerations

– Debt constraints and “off balance sheet” or “off credit” objectives

– Monetization

– Value capture (unlocking pricing power, expense reductions or other

benefits)

• Service delivery

– Contractual arrangements for service enhancements and cost savings

© PFM 6© PFM 6© PFM 6

Strategies to Leverage the Private Sector

– Manage project delivery risk for on-time, on-budget project completion

o Private sector expertise / efficiency for technically complicated development projects

o Bundling of assets

– Alignment of interests with private partner for asset life cycle responsibility and risk

o Private partners with equity at risk

Design / Delivery

Operations

Finance

– Transfer operating risks for noncore and/or technically complex assets

– Private sector efficiency

– Manage balance sheet / credit impact of the development of non-core assets

o Debt covenants, internal debt policies

– Monetize non-core assets with commercial value

‒ Transfer demand risk

– Demand Risk P3

o Design / Build / Finance / Operate / Maintain P3

o Shared governance and risk allocations

– Private Development

o Ground lease arrangements

o Private partner at risk for financial performance of asset

– Availability payment arrangements

– Design-build contracts

– Availability payment arrangements

– Service concession agreements

– Management contracts

Goals and Objectives Alternative Delivery Structure

Governance– Statutory limitations

– Ability to manage procurement or existing labor requirements

– Disposition on non-core assets

© PFM 8© PFM 8© PFM 8

P3s are Applicable Across All Sectors of Municipal Services

Transportation

• Roads, bridges, tunnels

• Transit

• Airports

• Ports

Utilities

• Municipally owned water

treatment, distribution and

wastewater systems

• Generation, distribution,

district energy, streetlights,

CNG, and solar

Education

• Student housing

• Parking

• Energy

• Athletics

• Academic facilities

Municipal Operations

• Judicial buildings

• Corrections facilities

• Government office buildings

Economic Development

• Convention centers and

hotels

• Recreation and

entertainment facilities

• Commercial developments

Health Care

• Medical office buildings,

specialized facilities, parking

and energy assets

• Service delivery contracts

© PFM 9© PFM 9© PFM 9

Misconceptions about AD/P3s

• Despite increasing visibility in the U.S., many misconceptions remain about P3s

Misconception Realities

• P3s can provide “free money” to close funding gaps for projects

• Private financing partners require some mechanism for repayment and return on investment

• Cost of borrowing is always most significant value driver

• Cost of capital is one consideration in project’s total value, along with lifecycle costs, risk-sharing, value engineering opportunities, etc.

• P3s give away government oversight and allow private sector free reign to raise rates

• Detailed project agreements preserve government oversight or define limitations on rate increases

• P3s are hostile to public-sector unions • Successful P3s have been structured both with and without continuing union labor contracts

• Profit motives for the private sector make P3 delivery more expensive

• Private sector already profits through construction contracts. AD/P3s provide for design innovation to lower overall costs

© PFM 10© PFM 10© PFM 10

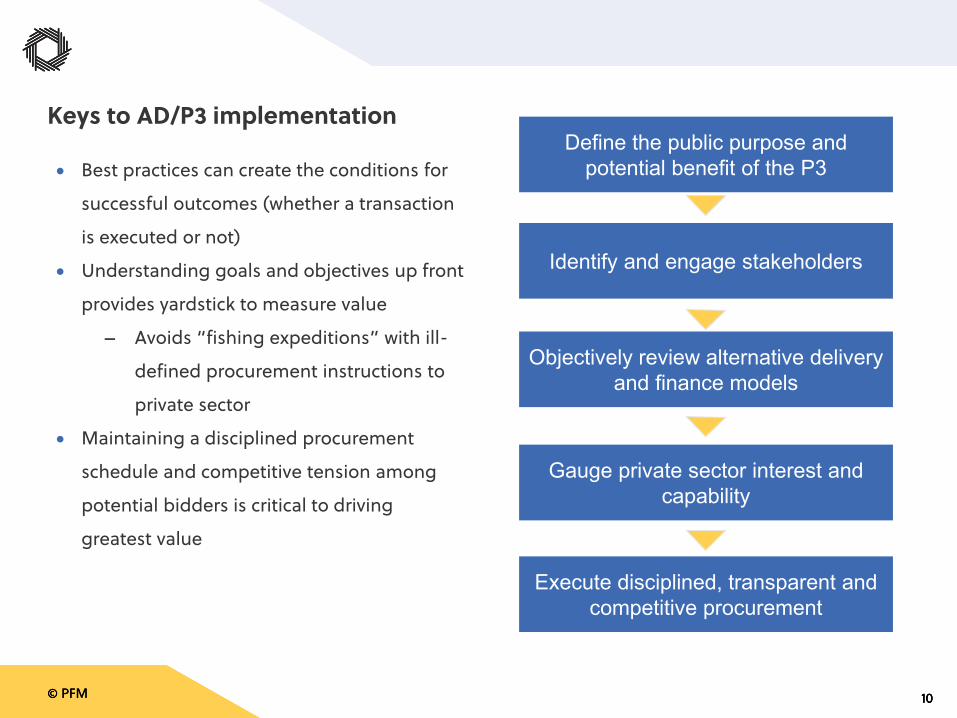

Keys to AD/P3 implementation

• Best practices can create the conditions for

successful outcomes (whether a transaction

is executed or not)

• Understanding goals and objectives up front

provides yardstick to measure value

– Avoids “fishing expeditions” with ill-

defined procurement instructions to

private sector

• Maintaining a disciplined procurement

schedule and competitive tension among

potential bidders is critical to driving

greatest value

Define the public purpose and potential benefit of the P3

Identify and engage stakeholders

Objectively review alternative delivery and finance models

Gauge private sector interest and capability

Execute disciplined, transparent and competitive procurement

© PFM 11© PFM 11© PFM 11

Attractive to Investors

Acceptable to Lenders/ RAs

Meet Govt Objectives

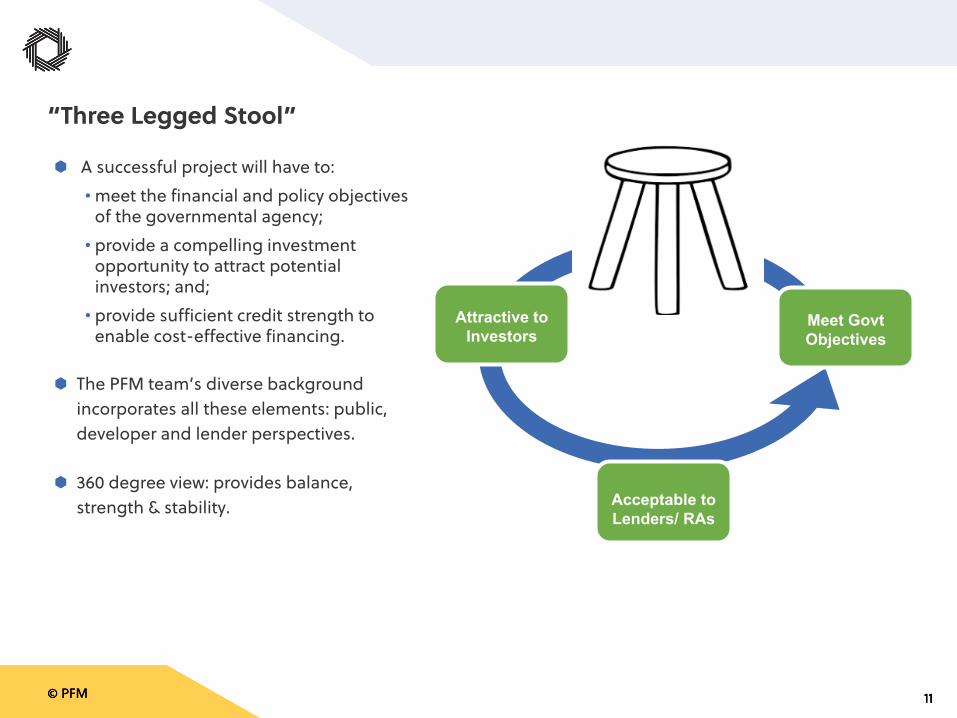

A successful project will have to:• meet the financial and policy objectives

of the governmental agency; • provide a compelling investment

opportunity to attract potential investors; and;

• provide sufficient credit strength to enable cost-effective financing.

The PFM team’s diverse background incorporates all these elements: public, developer and lender perspectives.

360 degree view: provides balance, strength & stability.

“Three Legged Stool”

© PFM 12© PFM 12© PFM 12

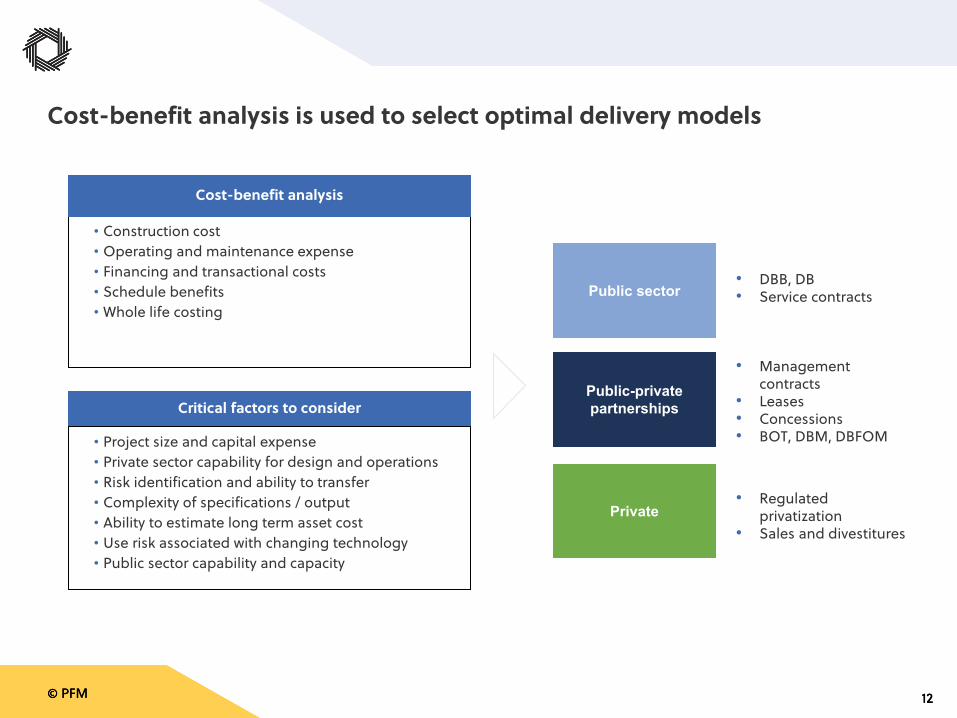

• Construction cost • Operating and maintenance expense• Financing and transactional costs• Schedule benefits• Whole life costing

Cost-benefit analysis is used to select optimal delivery models

Cost-benefit analysis

Critical factors to consider

• Project size and capital expense• Private sector capability for design and operations• Risk identification and ability to transfer• Complexity of specifications / output• Ability to estimate long term asset cost• Use risk associated with changing technology• Public sector capability and capacity

Public sector

Public-private partnerships

Private

• Management contracts

• Leases• Concessions• BOT, DBM, DBFOM

• Regulated privatization

• Sales and divestitures

• DBB, DB• Service contracts

© PFM 13© PFM 13© PFM 13

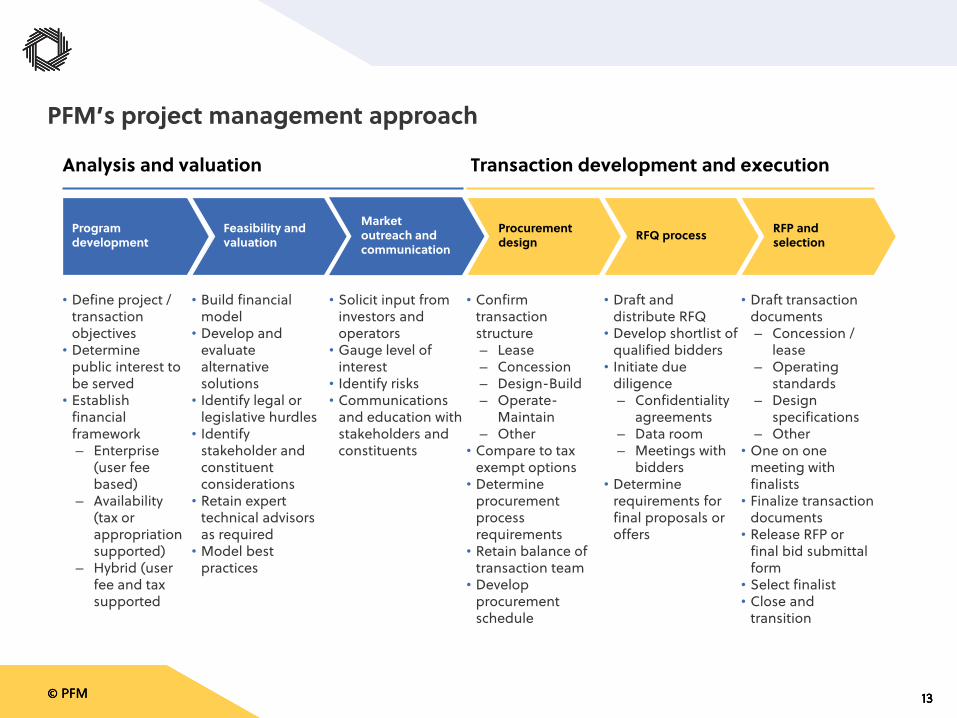

PFM’s project management approach

• Define project / transaction objectives

• Determine public interest to be served

• Establish financial framework– Enterprise

(user fee based)

– Availability (tax or appropriation supported)

– Hybrid (user fee and tax supported

• Build financial model

• Develop and evaluate alternative solutions

• Identify legal or legislative hurdles

• Identify stakeholder and constituent considerations

• Retain expert technical advisors as required

• Model best practices

• Confirm transaction structure – Lease– Concession– Design-Build– Operate-

Maintain– Other

• Compare to tax exempt options

• Determine procurement process requirements

• Retain balance of transaction team

• Develop procurement schedule

• Draft and distribute RFQ

• Develop shortlist of qualified bidders

• Initiate due diligence– Confidentiality

agreements– Data room– Meetings with

bidders• Determine

requirements for final proposals or offers

• Draft transaction documents– Concession /

lease– Operating

standards– Design

specifications– Other

• One on one meeting with finalists

• Finalize transaction documents

• Release RFP or final bid submittal form

• Select finalist• Close and

transition

• Solicit input from investors and operators

• Gauge level of interest

• Identify risks• Communications

and education with stakeholders and constituents

Program development

Feasibility and valuation

Procurement design RFQ process RFP and

selection

Market outreach andcommunication

Analysis and valuation Transaction development and execution

© PFM 14© PFM 14© PFM 14

Scheduling for a Major Investment AD/P3

2019 2020 2021 2022Schedule QI QII QIII QIV QI QII QIII QIV QI QII QIII QIV QI QII QIIITraffic & Revenue StudyPFM Model Construction and ManagementAnalysis and RecommendationsBoard Approval for ProcurementDB/DBOMRequest for QualificationsShort List SelectedDraft Request for ProposalsTIFIA Application ProcessNEPA FEIS/RODFinal RFPPreferred BidderContract Negotiation and ExecutionFinancial CloseDBFOMRequest for QualificationsShort List SelectedDraft Request for ProposalsTIFIA and PAB Application ProcessNEPA FEIS/RODFinal RFPPreferred BidderCommercial CloseFinancial Close

© PFM 15© PFM 15© PFM 15

Project Company

Project Contract(DBFO, DBFM,Concession etc.)

Users

Tolls or user chargesif applicable

Availability or Shadow TollPayments if applicable

Lenders

Investors

Senior Debt,Security and Hedging

Equity and/orJunior Debt

ConstructionContractor

Operator

ConstructionContract

Operation Contract

DirectAgreement

Granting Authority Services

P3 parties and contractual structure• Each project will involve some variation of this contractual structure depending on its particular elements

© PFM 16© PFM 16© PFM 16

Project revenue: availability payments vs. user fees

• Private investors recoup their initial investment in a P3 project via rights to the income produced over a defined period of time

• There are two high-level ways for a project to generate income:

– User fees: Money paid directly by the consumers of a service, such as highway tolls, utility bills, transit fares or student

housing rent

– Availability payments: Periodic money that the government commits to pay to support an asset that does not generate

fee revenue, such as a courthouse, academic building or non-tolled highway; payment is based on a specified

performance level

• Hybrid models with a mix of both approaches also exist

Government Entity

Project

Availability Payments

Investors

User Fees

Consumers

Investors

Project

© PFM 17© PFM 17© PFM 17

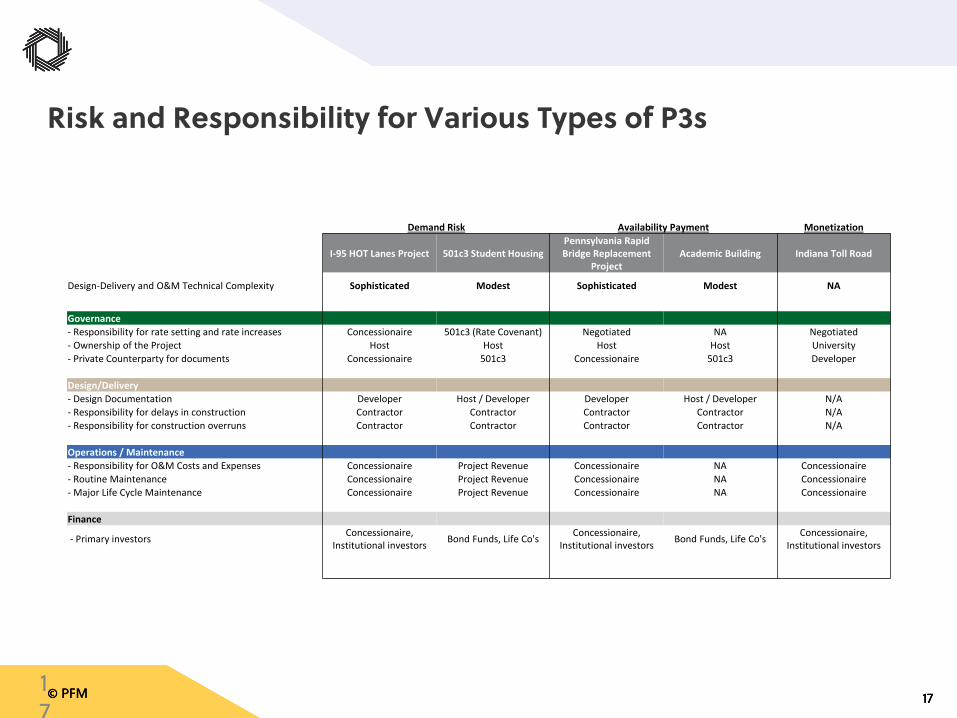

Risk and Responsibility for Various Types of P3s

17

Demand Risk Availability Payment Monetization

I-95 HOT Lanes Project 501c3 Student HousingPennsylvania Rapid Bridge Replacement

ProjectAcademic Building Indiana Toll Road

Design-Delivery and O&M Technical Complexity Sophisticated Modest Sophisticated Modest NA

Governance- Responsibility for rate setting and rate increases Concessionaire 501c3 (Rate Covenant) Negotiated NA Negotiated- Ownership of the Project Host Host Host Host University- Private Counterparty for documents Concessionaire 501c3 Concessionaire 501c3 Developer

Design/Delivery- Design Documentation Developer Host / Developer Developer Host / Developer N/A- Responsibility for delays in construction Contractor Contractor Contractor Contractor N/A- Responsibility for construction overruns Contractor Contractor Contractor Contractor N/A

Operations / Maintenance- Responsibility for O&M Costs and Expenses Concessionaire Project Revenue Concessionaire NA Concessionaire- Routine Maintenance Concessionaire Project Revenue Concessionaire NA Concessionaire- Major Life Cycle Maintenance Concessionaire Project Revenue Concessionaire NA Concessionaire

Finance

- Primary investors Concessionaire, Institutional investors Bond Funds, Life Co's Concessionaire,

Institutional investors Bond Funds, Life Co's Concessionaire, Institutional investors

© PFM 19© PFM 19© PFM 19

Infrastructure funds have significant capital to deploy

• Started with global pension funds looking to invest in stable, long life assets

• Infrastructure funds raised nearly $200 billion from 2016-2020

© PFM 20© PFM 20© PFM 20

Equity plays distinctive role in financing stack by providing both debt coverage and upfront proceeds

02468

1012141618

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 2324 25 26 27 282930

$Mill

ions

Year

80% debt / 20% equity (leveraged equity)

Debt Service Equity Return Net CF

Sources of Proceeds ($M)Debt $80Equity $20Project Cost $100

Interest Rate 6.0%Equity IRR 10.2%WACC (pretax) 7.3%

Equity return

Debt service

$80 Mproceeds

$20 Mproceeds 1.5x

coverage

• Equity leverages “at risk” cashflows to reduce required borrowing (project cost and reserves)

– Excess cash flow after debt service goes to the developer as a return on equity

• Equity provides additional flexibility for developers to reduce contingencies and other project

costs

© PFM 21© PFM 21© PFM 21

Investor Commentary

INFRASTRUCTURE INVESTMENT CRITERIA

• Monopolistic structures that offer protection from competition due to high barriers to entry

• Consistent and relatively inelastic demand for the assets’ services

• Stable and predictable inflation-linked cash flows

• Low-risk and long economic lives

• Stable and transparent regulatory frameworks

Source: Northleaf Capital

© PFM 22© PFM 22© PFM 22

GASB Statement 94 Impact on P3s and Availability Payment Arrangements

– Contract where an operator provides public services through the use and operation of an underlying asset

– Private party is compensated by third party fees

– Recognition as either capital asset or receivable, and offsetting deferred inflow of resources

– Financing secured by project revenue through ground lease or concession

– New capital projects or monetization of non-core assets

– Financing secured by fixed lease obligations made by institution

– On balance sheet and credit

– Manage public procurement, statutory authorization or internal debt policies

– Payments made to private party based on the underlying asset’s availability for use

– Multiple components to payment

– Component that is recognized as a financed purchase will be reflected as a long-term liability

– Potential ability to monetize real estate assets and promote economic development

– Potential ability to partner with third parties that have synergies with program offerings

Leas

eD

eman

d Ri

sk P

3sAv

aila

bilit

y Pa

ymen

tsPr

ivat

e D

evel

opm

ent

Example Assets

• GASB’s Statement No. 94 provides an organized approach to P3 projects that will increase transparency on the value add of these projects

GASB 94

– Administration buildings

– Academic buildings

– Multi-purpose facilities (rodeo)

– Student housing

– Parking

– Toll roads

– Utility concessions

– Mass transit

– Bridges

– K-12 Schools

– Courthouses

– Water systems

– Economic development

– Collaborative research

– Medical office building sale leaseback

© PFM 23© PFM 23© PFM 23

Examples of Alternative Delivery Projects in Higher Education

– Most common

– Financing typically secured by project revenue through lease or concession

Student Housing

Parking

Academic Buildings

Energy

Innovation/ Real Estate

– Potential efficiencies in project delivery and operations

– Balance sheet considerations

– Financing secured project revenue through lease or concession

– Monetization of future projected cash flows for existing assets

– Disposition of non-core asset

– Financing secured by fixed lease obligations made by institution

– On balance sheet and credit

– Manage public procurement, statutory authorization or internal debt policies

– Financing often secured by fixed lease obligations made by institution

– Potential for upfront payment

– Projects vary – energy savings contracts, utility system concessions, micro-grid projects

– Potential ability to monetize real estate assets and promote economic development

– Potential ability partner with corporate partners that have synergies with program offerings

Example PFM Client

Higher education institutions have leveraged the private sector to deliver projects for a wide variety of asset classes

Dem

and

Risk

Avai

labi

lity

Paym

ent

© PFM 24© PFM 24© PFM 24

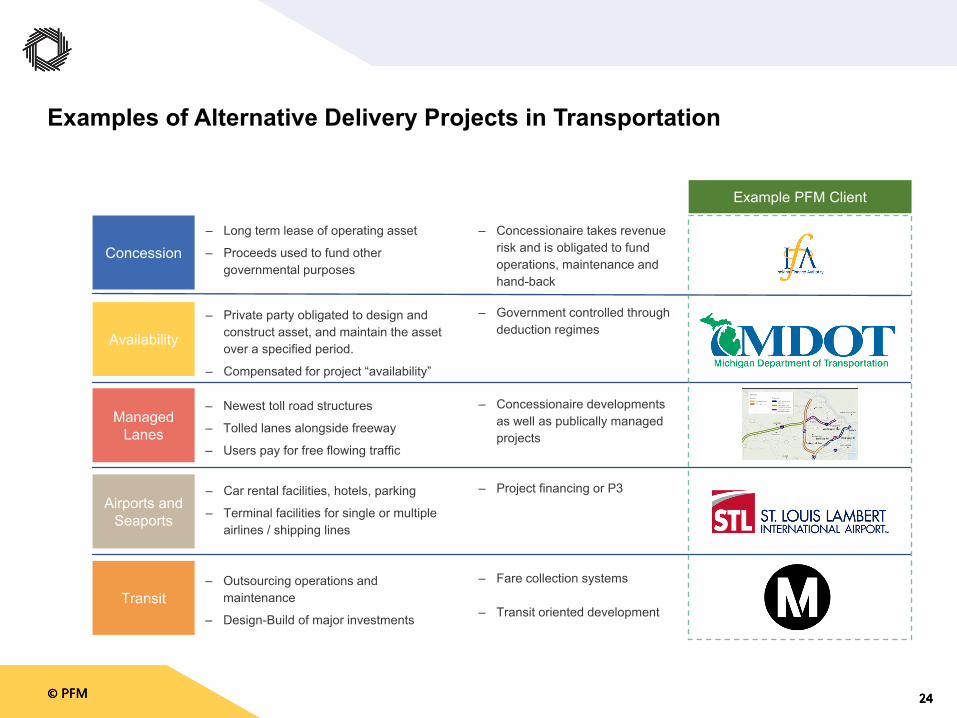

Examples of Alternative Delivery Projects in Transportation

– Long term lease of operating asset

– Proceeds used to fund other governmental purposes

Concession

Availability

Managed Lanes

Airports and Seaports

Transit

– Concessionaire takes revenue risk and is obligated to fund operations, maintenance and hand-back

– Private party obligated to design and construct asset, and maintain the asset over a specified period.

– Compensated for project “availability”

– Government controlled through deduction regimes

– Newest toll road structures

– Tolled lanes alongside freeway

– Users pay for free flowing traffic

– Concessionaire developments as well as publically managed projects

– Car rental facilities, hotels, parking

– Terminal facilities for single or multiple airlines / shipping lines

– Project financing or P3

– Outsourcing operations and maintenance

– Design-Build of major investments

– Fare collection systems

– Transit oriented development

Example PFM Client

© PFM 25© PFM 25© PFM 25

Examples of Alternative Delivery Projects in Other Sectors

– Government development and/or ownership of stadia and arenas

– Sports team primary tenant

Sports Facilities

Convention Centers and

Hotels

Utilities

K-12

Real Estate

– Projects may need subsidies to be viable

– Project revenues from sponsorship

– Generators of tourism to import tax dollars

– Support through hotel and other transient taxes

– Project financings

– Security may include partial government guaranty

– Development of new facilities

– Long-term O&M contracts for existing facilities

– Address deferred maintenance

– Achieve economies of scale with consolidation

– Contracts for maintenance of buildings, including utility plants

– Construction of new school and administrative facilities

– Development of sports and other ancillary facilities

– Availability based payments

– Redevelopment of government owned land

– Master development agreements

– Tax increment financing

– Government provisions of infrastructure for greenfields

Example PFM Client

© PFM 27© PFM 27© PFM 27

Contact information:

Mary FrancoeurManaging Director, New York

• [email protected]• Office: 212-809-4212

Ryan ConwayDirector, Charlotte

• [email protected] • Office: 704-541-8339

Scott ShearerManaging Director, Harrisburg

• [email protected] • Office: 717-232-2723

Robert GambleManaging Director, San Francisco

• [email protected]• Office: 415-982-5544

Whitney WarrenSenior Managing Consultant, NY

• [email protected] • Office: 212-809-4212

Mike NadolManaging Director, Philadelphia

• [email protected] • Office: 215-567-6100

© PFM 28© PFM 28© PFM 28

Questions?