americas trading overview - platts · · 2014-09-18source: ed&f man research. cuba’s...

TRANSCRIPT

Americas trading overview

1

0

5

10

15

20

25

30

35

0

5

10

15

20

25

30

35

40

80/81 85/86 90/91 95/96 00/01 05/06 10/11 13/14

Brazil Cuba NY#11 (RHS)

Production (mln MT) Average (c/lb)Production (mln MT) Average (c/lb)

0

5

10

15

20

25

30

35

0

1

2

3

4

5

6

80/81 85/86 90/91 95/96 00/01 05/06 10/11 13/14

Mexico Centrals Colombia ArgentinaPeru Venezuela NY#11 (RHS)

Production (mln MT) Average (c/lb)Production (mln MT) Average (c/lb)

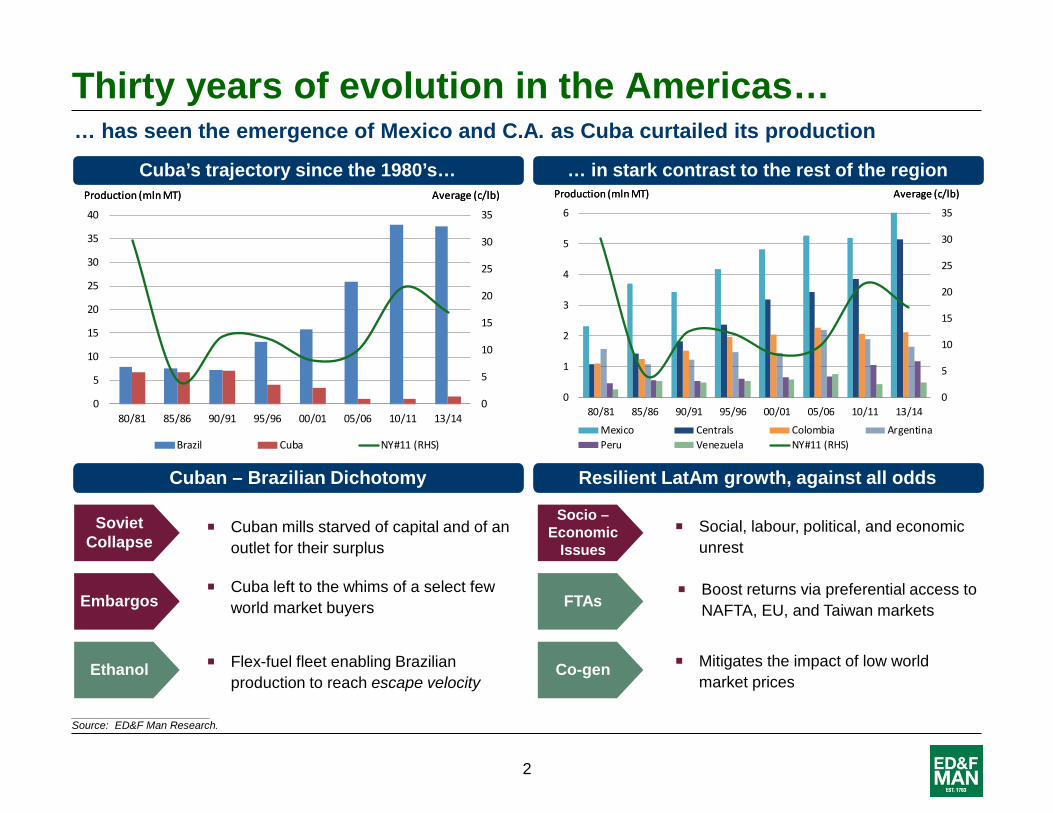

… has seen the emergence of Mexico and C.A. as Cuba curtailed its production

Thirty years of evolution in the Americas…

___________________________ Source: ED&F Man Research.

Cuba’s trajectory since the 1980’s… … in stark contrast to the rest of the region

Soviet Collapse

Embargos

Socio – Economic

Issues

Co-gen Ethanol Flex-fuel fleet enabling Brazilian production to reach escape velocity

Cuban mills starved of capital and of an outlet for their surplus

Cuba left to the whims of a select few world market buyers

Mitigates the impact of low world market prices

Social, labour, political, and economic unrest

FTAs Boost returns via preferential access to

NAFTA, EU, and Taiwan markets

Cuban – Brazilian Dichotomy Resilient LatAm growth, against all odds

2

… while capturing an increasing share of the global volume traded, from 11% to 15% in seven years

Americas’ (ex-BR) production growth has kept pace

___________________________ Source: ED&F Man Research.

Global exporters focus on Raws… … while Americas (ex-BR) shifts to Whites

27.0

40.2

17.020.661%

66%

58%

59%

60%

61%

62%

63%

64%

65%

66%

67%

0

5

10

15

20

25

30

35

40

45

2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14

Raws shareExports (mln MT)

Exp. (raws) Exp. (whites) Raws share (RHS)

3.8

5.6

1.4

3.1

73%

65%

0%

10%

20%

30%

40%

50%

60%

70%

80%

0

1

2

3

4

5

6

2006/07 2007/08 2008/09 2009/10 2010/11 2011/12 2012/13 2013/14

Raws shareExports (mln MT)

Exp. (raws) Exp. (whites) Raws share

Freight Advantage

VHP Edge

Logistics

Value-add

Logistics Focus on bulk loading facilities

Brazil, Thailand, Australia benefit from cheaper freight to the Gulf, India, APAC refiners

Brazil benefits from a first-mover advantage in meeting VHP requirements solicited by modern refineries

Keen to establish recognizable international brands, mills are willing to customize packaging for clients

C. A. mills located within 100 km of ports Dedicated sugar terminals reduced

competition with other export crops for bagged loading

Co-gen Additional energy costs from refining paid for with energy sales to transnational grids

“Big 3” catering to stand-alone refineries Americas (ex-BR) filling the void

3

Top three – 60% of production

NAFTA, Venezuela, and Chile dictate the regional flows

Overview of the region

___________________________ Source: ED&F Man Research.

Top two – 50% of exports Top four – 80% of imports

US26%

Mexico21%

Guatemala10%

Colombia7%

Argentina6%

Cuba6%

Others24%

2013/14 - Production (28.4m MT)

US40%

Mexico17%

Argentina7%

Colombia7%

Canada5%

Others24%

2013/14 - Consup. (25.8m MT)

Mexico26%

Guatemala22%

Cuba10%Colombia

8%

Nicaragua6%

El Salvador5%

Others23%

2013/14 - Exports (8.8m MT)

US43%

Canada19%

Venezuela12%

Chile6%

Colombia3%

Others17%

2013/14 - Imports (7.1m MT)

NAFTA leads consumption

4

Northern demand is met by Southern supply…

___________________________ Source: ED&F Man Research.

USA

Colombia

Canada

Mexico

Venezuela

Chile

Argentina

Peru

Caribbean

Canada and USA

Central America

South America - tight

… Venezuela, and Chile being the exceptions

5

Deficit markets

Surplus markets

Main drivers in the region

___________________________ Source: ED&F Man Research.

Sugar production (2000/01 – 2013/14)

Net surplus (2000/01 – 2013/14)

0.0

1.5

3.0

4.5

6.0

7.5

9.0

Peru

Nica

ragu

a

Guat

emal

a

Hond

uras

El S

alva

dor

Cost

a Ri

ca

Mex

ico

Arge

ntin

a

Colo

mbi

a US

Vene

zuel

a

Chile

Cuba

Strong increase Increase Unchanged Decrease

Production (mln MT)

79% 72% 62% 60% 46% 24% 22% 14% 4% -3% -17% -44% -49% Total Growth

5% 4% 4% 4% 3% 2% 2% 1% 0% 0% -1% -4% -5% CAGR

-3.0

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

Guat

emala

Mex

ico

Cuba

El Sa

lvado

r

Colom

bia

Nica

ragu

a

Costa

Rica

Hond

uras

Arge

ntina Peru

Chile

Vene

zuela US

Surplus/deficit (mln MT)

6

Raws to value-added whites

7

230

157

225

289

188

248200 189

6543

96 95

13 2

80 93

2010/11 2011/12 2012/13 2013/14*

Imports (k MT)

Centrals Colombia Argentina Brazil

792 783

579

873

77 63

210

382

2010/11 2011/12 2012/13 2013/14*

Imports (k MT)

Brazil Centrals

1,411

953

1,8901,734

463

793

331511

300475

167 16055 42 43 1587 76 60 8

2010/11 2011/12 2012/13 2013/14*

Imports (k MT)

Mexico Centrals Brazil Colombia Argentina

139

190

117

178

83

7 834

80

137

198

137

2010/11 2011/12 2012/13 2013/14*

Imports (k MT)

Colombia Brazil Centrals

Main importers in the region

___________________________ Source: ED&F Man Research. * Last available date. All numbers in 1,000 MT.

Chile Venezuela

USA Caribbean

8

Trade flows shifting out of the region

___________________________ Source: ED&F Man Research.

Central America – sugar exports by destination

0

250

500

750

1,000

1,250

1,500

1,750

2,000

Africa Asia Americas Others2009/10 2010/11 2011/12 2012/13 2013/14*

0% 16%

21% 35%

82% 66%

9

Export mix shifting from raws to value-added whites

___________________________ Source: ED&F Man Research.

Guatemala / Colombia exports (2009/10 – 2012/13) Brazilian Exports

0

200

400

600

800

1,000

1,200

Raw White Raw White

Guatemala Colombia

Exports (k MT)

0

5,000

10,000

15,000

20,000

25,000

2009/10 2010/11 2011/12 2012/13 2013/14

Exports (k MT)

Raw Whites

Brazil is focusing its sales to the raw markets, while Guatemala and Colombia are filling the void left in whites sugar exports

Value-added Central American sugars head to preferential markets

10

Protection from the World Market

11

Three key components to the Americas

World and

regional markets

Preferential markets

(USA, EU, Taiwan, Andean)

Domestic Market

12

Domestic markets play an important role in the region

World market exposure

___________________________ Source: ED&F Man Research.

Global vs. Regional prices Consumption / Production ratio (2013/14)

300

400

500

600

700

800

900

1,000

Price (USD/MT)

*weighted prices - (Guatemala, El Salvador, Colombia, Mexico and Peru)

Domestic market* LDN5 NY16 NY11

104%

80%

64%57%

42% 39%28% 27% 27% 31%

Domestic prices shield regional producers from NY #11 and LDN #407 volatility

Price stability is achieved via trade barriers, production seasonality, and market size

Regional producers are less exposed to the world market than the Big 3

13

100%

28%

8%

62%

Production Domestic Market TRQ and FTA Regional and Worldmarkets

100%80%

3%

27%

Production Domestic Market TRQ and FTA Regional and Worldmarkets

100%

36%

24%

37%

Production Domestic Market TRQ and FTA Regional and Worldmarkets

100%

42%

7%

34%

Production Domestic Market TRQ and FTA Regional and Worldmarkets

Market mix varies among the producers

___________________________ Source: ED&F Man Research.

Guatemala (2012/13)

Colombia (2012/13)

El Salvador (2012/13)

Nicaragua (2012/13)

14

0%10%20%30%40%50%60%70%80%90%

100%

2008 2009 2010 2011 2012 2013

Hydro Thermal Cogen Geo Wind Solar Biogás0

100

200

300

400

500

600

700

Guatemala Colombia Nicaragua El Salvador Honduras Costa Rica

MW

Further protects producers from the vagaries of the world market

co-generation

___________________________ Source: ED&F Man Research.

Centrals – Installed capacity by energy type Installed capacity (2008 – 2013)

co-generation represents nearly 7% of total electricity produced in Central America

In Guatemala co-generation provides ~25% of the country’s electricity

Central American installed capacity increased ~45% over the past 5 years(984 MW in 2013)

Colombian installed capacity increased ~60% (187 MW in 2013) over the same period

Electricity is therefore an important source of revenue for the mills, enabling sugar production growth in a period of low world market prices

15

Ethanol

___________________________ Source: ED&F Man Research.

Colombia – Sugar and ethanol exports

Ethanol is another important by-product for the region

The biofuel market allows countries to not only depend less on oil imports, but also export ethanol to the international market.

Colombia has increased ethanol production by ~50% in the past 5 years

Countries with low area available for cane expansion will tend to reduce sugar production in order to meet mandatory blend levels

0

100

200

300

400

500

600

700

800

900

1,000

2006 2007 2008 2009 2010 2011 2012 2013Sugar exports Ethanol production

Quantity (k MT and m3)

Current Mandates

E10

E5

E25

E7.8

E8

E10

Ethanol mandates in the region

16

Long term competitive advantage

17

Potential global growth by 2030

___________________________ Source: ED&F Man Research, IMF.

Global per capita consumption (2013) Population growth (2013 – 2030)

+ 1.2 billion more people on the planet than today

+ 25 million MT of additional consumption via population growth alone, centered on Africa and Asia-Pacific

+ 55 million MT of additional consumption via GDP growth alone, Africa and Asia-Pacific having the highest

GDP growth prospects

N/C America,

81South

America, 58

Europe/CIS, 22Africa, 486

Asia-Pacific, 471

Middle East, 75

23

35

49

34 33

16 17

29

38

World N/CAmerica

SouthAmerica

WesternEurope

EastenEurope

Africa Asia MiddleEast

Oceania

Asia-Pacific and Africa are poised to be the main drivers of future consumption growth

18

24

Potential global growth by region 2030/31 consumption is projected to far exceed current production levels

___________________________ Source: ED&F Man Research. All figures in millions of MT tel quel. 2030/31 figures equal to 2013/14 production less 2030/31 projected consumption.

3

7

4

3

26

1

5

NAFTA Europe

CIS

W. Africa

E. Africa

Southern Africa

Asia Pacific

MENA

Indian Subcontinent

Central America

South America

Brazil

19

1 0

3

5

10 18

4 10

2

7

1

21

0

26

3

4

26

2030/31 (P13/14 – C30/31)

32 2013/14

103 27

Regional Surplus’

Regional Deficits

5.5

75

Global Balance

Competitiveness in the region Sugar efficiency vs. potential acreage

>400

Low

Production Costs

___________________________ Source: ED&F Man Research.

Sugar (MT/ha)

20

High

Outlook

21

The Americas are well-positioned to continue weathering out the storm and benefit from an eventual transition to a deficit market

Regional outlook

Supply Demand

The region will continue to increase production, although area expansion opportunities are shrinking

22

Ethanol Ethanol mandates could eat into sugar

production, particularly in Colombia

Domestic markets will continue to play an important role as a result of strong domestic GDP and population growth

Emerging Markets

The Peruvian privatizations are bearing their fruits, Peru is set to become a net exporter in the medium term

LatAm producers stand to benefit from the NAFTA dispute, at Mexico’s expense

Increased exports of whites from the region, as Brazil focuses its exports on bulk raws

Peru NAFTA

Product Mix

The region will be a strong beneficiary of the consumption per capita increases in Asia and Africa

Yield + Acreage

Co-gen Co-generation growth will be the main

driver behind incremental cane acreage, and as a consequence, sugar tonnage

23

Developed by ED&F MAN Commodity Research

Thank you

Disclaimer: Any comments or opinions in this presentation are not intended to be an offer to buy or sell commodities or futures and options thereon as they merely state our views and carry no guarantee as to their accuracy. © 2014 ED&F Man Holdings