analysis of used oil policy management options for the waste

TRANSCRIPT

Analysis of Used Oil

Policy Management

Options

for

The Waste Authority, Western Australia

February 2009

This report has been prepared by: David Fitzsimons with Dan Eatherley and Jenni Rasanen Checked as a final draft by: Katie Deegan Reviewed by: ………………………………………. Date: 23rd February 2009 (including comments from consultees) Contact: [email protected] File reference number: WEST01 165 issue2.doc Client Project Reference KE-50 2008

For more information visit www.oakdenehollins.co.uk

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 1

Contents

Glossary 3

Acknowledgements 4

1 Summary 5

2 Introduction 8 2.1 Background 8 2.2 Scope of Study 8

3 International Case Studies 9 3.1 Alberta Province, Canada 9 3.2 Denmark, Europe 17 3.3 Finland, Europe 29 3.4 Spain, Europe 37 3.5 Summary Case Study Metrics 39

4 Base-Line Scenario 41 4.1 Supply of Used Oil 41 4.2 Demand for Burner Fuels 44 4.3 Drivers for Competitive Change 48 4.4 Summary Costs and Benefits of Base-Line Case 52

5 Local Lube-to-Lube Re-Refining Scenario 54 5.1 Background 54 5.2 Optional Additional Policy Measures 55 5.3 Summary Costs and Benefits from Local Re-refining 60

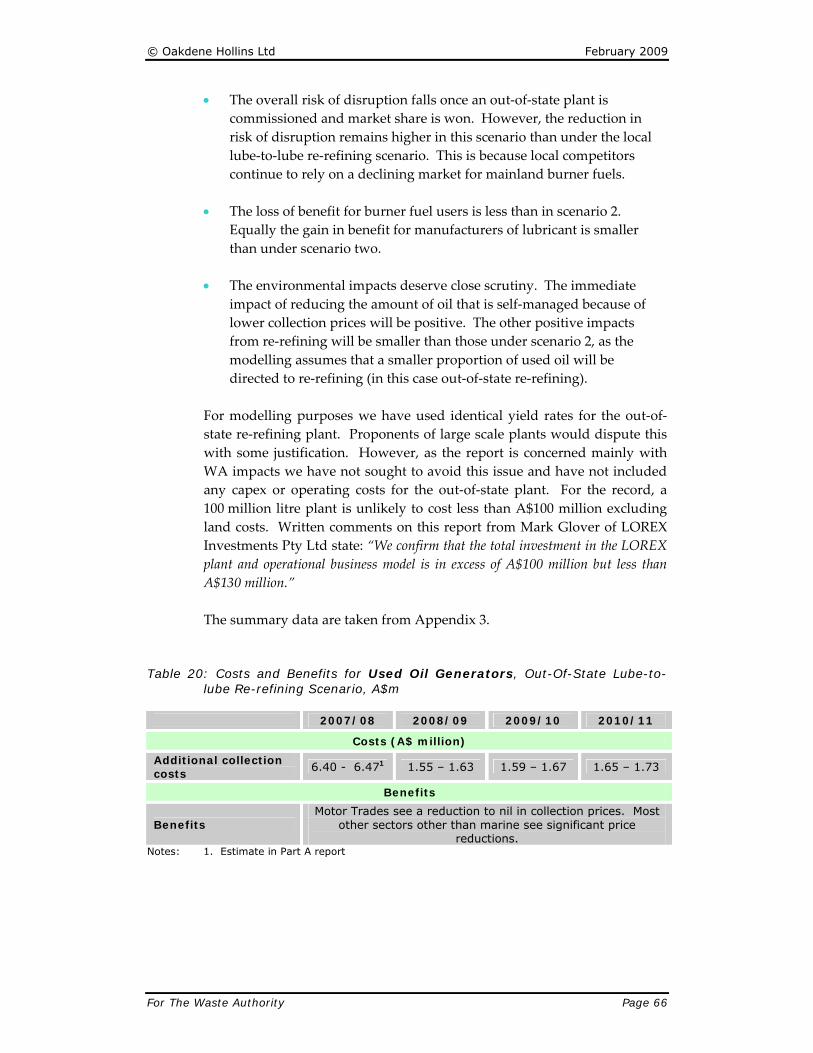

6 Out-of-State Lube-to-Lube Re-Refining Scenario 64 6.1 Background 64 6.2 Optional Additional Policy Measures 65 6.3 Summary Costs and Benefits From Out-of-State Re-refining 65

7 Policy Options 69 7.1 Option 1 69 7.2 Option 2 70 7.3 Option 3 70 7.4 Option 4 71 7.5 Option 5 71 7.6 Option 6 72 7.7 Summary of Options 72

8 Sensitivity Analysis 73 8.1 Market Share Assumptions, Scenario 3 (Out-of-State) 74 8.2 Blending Ratio for Bottoms, Scenario 2 (Local Re-refining) 75

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 2

8.3 Used Oil Supply – All Scenarios 75 8.4 Mainland Demand for Burner Fuels 76

9 Conclusions 77

References 78 Case Studies - Alberta 78 Case studies - Denmark 80 Case studies - Finland 82

Appendices 85

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 3

Glossary

AORA Australian Oil Recyclers Association

Bottoms The thick residue following the refining of used oils, also referred to as VTB (vacuum tower bottoms)

C/L Cents per litre

LCA Life cycle assessment

PSO Product Stewardship (Oil) Act 2000

Regeneration Synonym in this report for “re‐refining”

Re‐refining The processing of used mineral oils to manufacture base oil

Tonnes Used as an approximate equivalent of 1,000 litres

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 4

Acknowledgements

Robert Atkins Director DEC Environmental Regulation

Lyle Barrett Institute of Automotive Mechanical Engineers

Steve Beilby Business Co‐ordinator DEC Environmental Regulation

Peter Fitzpatrick Motor Traders Association

Mark Glover LOREX

Rod Lucatelich Environment Manager, BP

Rob Jarrett Boral Midland Brick

Jose Fernando Suarez Mejido Sener Grupo de Ingenieria S A

Sean McSevich Industry Regulation, DEC South West Region

Ged Styles ToxFree Solutions

Ken Tushingham Verve Energy

Gary Watson Transpacific Industries Group Ltd

Fred Wren Managing Director, Wren Oil

Thanks to Sam Wilkinson at DEC for providing suggestions and local contacts and to

Leanne Reid at DEC for co‐ordinating the stakeholder meetings in WA for David

Fitzsimons of Oakdene Hollins during 31st October to 9th November 2008.

Thanks also for the written comments received in January 2009 from Gary Watson of

Transpacific Industries Ltd, Fred Wren of Wren Oil and Mark Glover Of LOREX

Investments Pty Ltd.

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 5

1 Summary

What actions, if any, might be taken to ensure greater stability in the collection and processing of used oil in Western Australia (WA)? This study sets out a range of policy options centred on three scenarios. To inform the policy options we have provided three detailed up‐to‐date case studies from Alberta, Denmark and Finland and a shorter case study on recent regulatory changes in Spain. All four States operate a levy and subsidy system similar in some respects to the Federal Product Stewardship for Oil (PSO) in Australia. In Denmark and Finland new re‐refinery plants have just been, or are about to be, completed. This study sets out how costs and benefits are distributed between four categories of stakeholder; used oil generators, used oil collectors and processors, burner fuel and lubricant buyers, and the WA Environment. The base‐line scenario describes what is most likely to occur in WA if no further policy interventions are taken during the period to 2011/12. It describes a situation in which the joint venture between Wren Oil and Nationwide continues to enjoy the benefits of higher prices and reduced collection costs but there is no investment in a local re‐refining plant. The higher collection prices increase the amount of oil that is self‐managed by generators thereby increasing the risk of environmental damage due to uncollected oil being inappropriately discarded. Our modelling shows that up to 350,000 litres of used oil will be self‐managed and we estimate an initial risk of 15% (and growing thereafter) of disruption to the burner fuel market leading to a repeat of the problems experienced in 2006/07. A second scenario investigates the building of a local re‐refinery by the joint venture at a claimed cost of A$20 million. From 2010 it receives 30 million litres of feedstock. The collection price for most of these oils falls from 15 to 8 cents per litre, especially for generators of oil in the automotive sector. Our modelling shows that up to 200,000 litres will be self‐managed, but with a lower risk of disruption than in the base‐line scenario. However, the disposal of bottoms from the re‐refinery (5.5 million litres) continues to carry a risk of disruption because at least 50% of it will need to be blended at a ratio of 1:1 and exported to non‐mainland markets. A third scenario investigates the implications if a new competitor (LOREX) enters the market in order to collect oils for storage and onward transfer by sea freight to out‐of‐state re‐refining. In this scenario prices for collection fall extensively to 5 cents per litre for industry and the mining sector and nil in the automotive sector. This price reduction reduces the quantity of self‐managed oil to less than 50,000 litres. The risk of disruption falls but this is sensitive to the extent of market share won by the new competitor (we have assumed a maximum of 25%). As the out‐of‐state re‐refinery is treated differently in our model because its own vacuum tower bottoms (VTBs) are not sent included in shipments to non‐mainland markets from WA, we modelled a range of options for a fairer comparison. The shaded area in the figure

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 6

below can be interpreted as meaning that local and out‐of‐state lube‐to‐lube re‐refining offer potentially similar risk profiles within a range of 25% and 50% market share for the out‐of‐state re‐refinery. Comparative Risk of Disruption to Collection (measured by the proxy figure of used oil sent to non-mainland markets) under Each Scenario

0.0

5.0

10.0

15.0

20.0

25.0

30.0

35.0

Jul-0

8

Jan-0

9Ju

l-09

Jan-1

0Ju

l-10

Jan-1

1Ju

l-11

Jan-1

2Ju

l-12

Jan-1

3Ju

l-13

Jan-1

4Ju

l-14

Jan-1

5Ju

l-15

Year

Non

Mai

nlan

d B

urne

r Fue

l, M

illio

n Li

tres

No Intervention Local Re-refining Out of State Re-refining

LR with Bottoms OSR 50% Market Share

Amount of Self-Managed Oil under Each Scenario

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

Jul-0

8Ju

l-09

Jul-1

0Ju

l-11

Jul-1

2Ju

l-13

Jul-1

4Ju

l-15

Year

Self

Man

aged

Oil,

L

$0.00

$0.01

$0.02

$0.03

$0.04

$0.05

$0.06

$0.07

$0.08

$0.09

$0.10

$0.11

$0.12

$0.13

$0.14

$0.15

$0.16

$0.17

$0.18

Col

lect

ion

Cos

t, A

$No Intervention Local Re-refining Out of State Re-refiningNI Collection Cost LR Collection Cost OSR Collection Cost

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 7

All three scenarios are possible without any further policy interventions. This study does not provide recommendations but we have set out a number of possible policy options for consideration (Section 7). These are: Option 1 Establish a timetable for the introduction of new atmospheric

pollution abatement controls for plants that accept waste derived fuels.

Option 2 Monitor the progress of the JV toward delivering a new lube-to-lube plant. Option 3 Offer a grant toward the cost of a re-refining plant/tank storage capacity

conditional on commissioning before 2011. Option 4 Investigate the introduction of more onerous license conditions for used oil

operators. Option 5 Request that the relevant state Government Departments including

Transport Department give priority to investigating the viability of using bottoms in asphalt products.

Option 6 Write formally to the JV partners recommending that that they seek authorisation from the ACCC for the public interest issues arising from the achievement of the JV objective, offering to provide information.

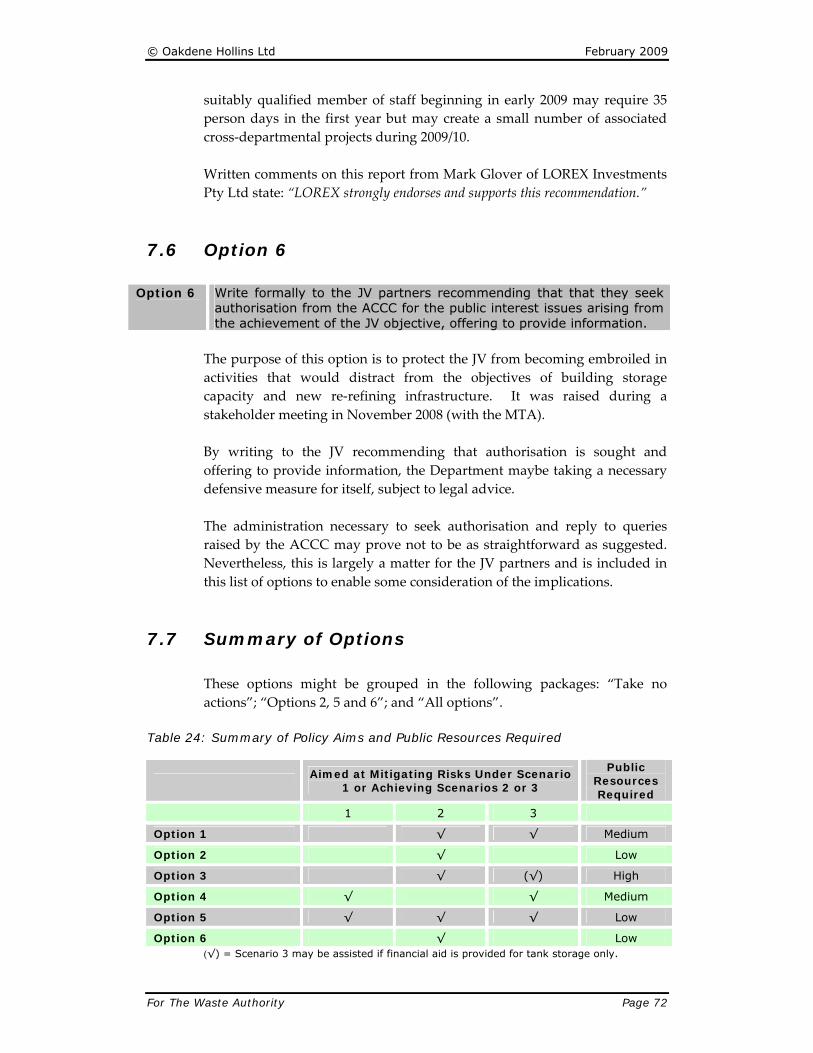

These policy options are targeted at improving the prospects of achieving one or more of the scenarios. This is shown in the table below along with an indication of the public sector resources required to deliver them. Summary of Policy Options and Public Resources Required

Aimed at Mitigating Risks under Scenario 1 or

Achieving Scenarios 2 or 3

1 2 3

Public Resources Required

Option 1 √ √ Medium

Option 2 √ Low

Option 3 √ (√) High

Option 4 √ √ Medium

Option 5 √ √ √ Low

Option 6 √ Low (√) = Scenario 3 may be assisted if financial aid is provided for tank storage only.

Each scenario offers a different distribution of the main costs and benefits between the principal stakeholders. These are detailed in Sections 4, 5 and 6. Amongst generators of used oil, the automotive sector stands to gain most from the construction of a re‐refining plant, whether in state or out‐of‐state as prices for collection are forecast for these generators to fall significantly from current levels. The modelling results, although sensitive to four key assumptions, can be interpreted to mean that the greatest level of stability in the collection and processing of used oil will be achieved by: 1. Accelerating the construction of new oil storage facilities and a local lube‐to‐lube

re‐refinery, followed by 2. Increased competition at collection, possibly led by an out‐of‐state re‐refinery

operator.

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 8

2 Introduction

2.1 Background

In the light of the disruption caused to the used oil collection and processing infrastructure during 2006/07, the Department, on behalf of the Waste Authority, wishes to investigate options that will improve the certainty of service provision for used oil collection and processing across the State. It is this wish that forms the principal objective of this study.

2.2 Scope of Study

In August 2008, Oakdene Hollins was commissioned by the Waste Authority to prepare Part B of a study of used oil management in the State of Western Australia. At the same time, Perth‐based consultant ACIL Tasman was appointed to prepare Part A of the study. The specification for the study was set out in schedule 2 of the “Request, KE 50 2008” and published on the State Government web site. For Part B, the scope of work is: • prepare selected case studies of other jurisdictions (Section 3) • establish the base‐line case and “likely changes” case (Sections 4, 5 & 6) • identify expected outcomes of alternative management options

(Section 7) • prepare a sensitivity analysis (Section 8) • consult with key stakeholders. At the same time, the Federal Government engaged PwC (PriceWaterhouseCoopers) to conduct an independent review of the Product Stewardship (Oil) Act 20001.

1 PSO Review, PwC Economics (Level9) GPO Box 2650 Sydney NSW 1171. email

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 9

3 International Case Studies

The system of waste oil collection and treatment in the State of Western Australia (WA) exhibits features that are significantly different from those seen in other advanced economies concerned with the issue: in particular, WA’s remoteness from similar markets for the feedstock and outputs of used oil treatment. Nevertheless, we have drawn on three case studies where elements of their experience in managing used oils help to inform the options to be considered by policy makers in WA.2 The three case studies are: • Alberta Province, Canada • Denmark, Northern Europe • Finland, Northern Europe. We have selected Alberta on the basis of its relatively remote location, being equidistant between the only re‐refining plants in Canada. Denmark has been selected for its policy management choices during a recent transition from sending used oil to fuel outlets toward fulfilling a 75% target of re‐refining. Finland has been selected for its remoteness issues and the almost finished new investment in a single re‐refining plant. All three are comparable in terms of population, tonnages of used oil collected, management systems designed to fund the collection or reprocessing of oils and aspects of long distance transport economics.

3.1 Alberta Province, Canada

The western Canadian Province of Alberta operates an Advanced Disposal Fee system similar to that implemented by Australia’s Federal Government, except that in Alberta the payments (return incentives) are disbursed to collectors rather than to reprocessors. In addition, return incentives are not only available for used oil but also for the collection of oil filters and containers. Alberta’s system has been stable for more than a decade, principally because it permits trade in used oil with other Canadian Provinces and exports to the United States. Stability has, arguably, been reinforced by the Province’s indifference as to whether used oil is directed toward reprocessing for legitimate fuel uses or lubricant products.

2 All costs, prices and values quoted in the case studies are in local currency, with Australian dollar

equivalents in parentheses. Conversions from local currency values to Australian dollar equivalents were performed using the conversion website xe.com and should be treated with caution as they were made in October 2008 while global financial markets were experiencing significant instability.

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 10

3.1.1 Notable Differences with Western Australia

• There is no Federal Government programme of used oil management. The Provincial Government alone is responsible for policy in this arena, with a private sector body responsible for day‐to‐day running of the used oil collection programme.

• Trade opportunities are more extensive as road and rail distances are

not prohibitively expensive.

• Almost 87 million litres of used oil were collected in 2007 from Alberta’s population of 3.3 million. WA collects approximately 42.3 million litres.

• Lubricant sales are far larger due to the quantity of oils sold for pumps

and compressors from which only a small proportion is recoverable.

• Competition is more intense. Although the collection market is dominated by two companies, Enviro‐West Inc and Newalta Inc, competition is so great in urban areas that some generators of used oil in September 2008 were paid as much as 18 Canadian cents per litre.

• Public policy interest in used oil is centred on extending the existing

C$15.7 million (A$18.7 million) levy on lubricants programme.

1000 km

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 11

Canada has a population of 33 million of which 3.3 million live in Alberta. Population density in the Province is as low as 0.34 per km2 (Northern Lights) but in the main urban area of Calgary is 28.6 people per km2.

3.1.2 The AUOMA Model

For the last ten years, the industry‐led Alberta Used Oil Management Association (AUOMA) has managed an extended producer responsibility (EPR) scheme for collecting and recycling post‐consumer oil, filters and containers. Funds raised from a levy of 5 cents per litre of lubricant at the point of first sale incentivise the recovery of used oil materials by a network of collectors across the Province. In 2007, the levy raised an aggregate sum of C$15.7 million (A$18.7 million). The AUOMA model has led to its adoption in four other Provinces under the auspices of Canada’s Used Oil Management Association (UOMA). The system is deemed to be necessary to ensure the collection of oil from rural areas and from those who change engine oil at home. Ontario, Canada’s largest Province, has to date resisted adopting a similar scheme on the grounds that given the current high price of fuels the need for any ADF (Advanced Disposal Fee) system on lubricants is unnecessary. Instead, it is argued, a market framed by clear legal constraints should be sufficient to ensure that oil is collected and treated effectively. The AUOMA programme has its roots in an approach made by the Canadian Council of Ministers of the Environment (CCME) to the Canadian Petroleum Products Institute (CPPI) in 1988. CCME was concerned that the existing scheme (whereby retailers were responsible for taking back used oil from customers) was ineffective, and due to the high cost of disposal was in effect penalising those retailers diligent enough to accept the returned oil. Free‐riders were evidently disadvantaging conscientious garage owners. CCPI, the national association of oil refiners and marketers which counts Chevron, Shell, Esso and Petro‐Canada among its members, was asked to quantify the environmental impact of used oil. This prompted the government of Alberta to initiate a stakeholder consultation exercise with improved used oil management as its goal. In April 1993 AUOMA was established and charged with trialling a user‐pay incentive‐based programme in six locations in Alberta. The outcome of this two year pilot resulted in the 1997 Lubricating Oil Material Recycling and Management Regulation. The Alberta Used Oil Management Programme was launched, and continues to this day. AUOMA is a multi‐stakeholder not‐for‐profit organisation now consisting of 184 oil and filter wholesalers, oil collectors, transporters and processors. Its key function is to maximise used oil collection but it does not stipulate end‐uses for the recovered material. There are a number of things AUOMA

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 12

itself does not do: it does not transport, or at any stage take ownership of used oil materials; it does not control collection or recycling facilities; it is not government‐funded; and it does not regulate. AUOMA is instead a ‘delegated administrative organisation’ directed to carry out business on behalf of the Provincial government. The Federal government of Canada has no responsibility for regulating used oil management. The AUOMA programme, described as ‘government initiated and industry‐driven’, is broadly revenue‐neutral and works as follows. All first sellers operating in the Province are required to register with AUOMA, paying it the fixed five cents environmental handling charge (EHC) for every litre of lubricating oil sold to a non‐registered buyer. No EHC is payable for two‐cycle oil, chain oils, drilling, machining and cutting fluids. ‘First sellers’ include manufacturers, marketers, wholesalers, retail distributors or importers. The EHC, also levied on filters and containers, can either be absorbed by the seller or passed on to the customer. The levy is not paid on supply sales transactions between registered members. AUOMA collected $15.7 million (A$18.7 million) through the EHC in 2007. While a portion of the funds (4%) pays for administration and public awareness‐raising activities, around 92% is redistributed as a return incentive (RI) to private sector collectors of used oil. The used oil is collected from some 4,000 generators throughout Alberta, of which about 400 serve as registered ‘drop‐off locations’ accepting used oil materials from ‘do‐it‐yourself oil changers’, farmers and small businesses. Most of these depots are managed by the Alberta Bottle Depot Association, although a few are run by municipalities.

3.1.3 Collection Zoning

To qualify for an RI, collectors must demonstrate that the oil will be recycled ‘appropriately’ by submitting documentation signed by reprocessors registered with AUOMA and whose operations have government approval. Registered collectors are also audited annually and must be in possession of a Letter of Regulatory Compliance. The RI is disbursed based on actual volumes of oil collected determined by tank gauging and discounted by the percentage of contamination by water and by solids. To decide on a sufficient level of incentive, given that the cost of transportation can be an important consideration in oil collection, the Province is divided into six geographic zones (Figure 1). A Freight Equalized Zone Pricing system then dictates the appropriate RI to be paid based on primary and secondary road networks, the volume of oil to be collected and Provincial demographics. The RI thus ranges from 6 cents (A$0.07) per litre in Calgary (Zone 1) to 16 cents (A$0.19) per litre in the far north of the Province (Zone 6). In the Province of British Columbia return incentives are as much as 27 cents (A$0.34) per litre for the remote Queen Charlotte Islands.

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 13

Fig. 1: Used Oil Collection Zones in Alberta

Source: Corporate Link Management Consultants. 2002. Economic and environmental

performance of Alberta’s used oil program

3.1.4 Metrics

In an area of wastes management where data are often lacking or of poor quality, a clear success of the AUOMA programme has been the significant quantity of auditable annual collection and processing figures made publicly available. Used oil recovery rates have grown markedly: in 2007, 86.9 million litres were collected, a rise of 32.8 million litres over 1998; the market for lubricants in Alberta is unusual compared to most advanced economies. AUOMA claims that last year’s collection figure represents 82% of recoverable used oil3. Given the extent of cross‐border trade in used oil, it is feasible that some of the increase in collection volume is derived from material recovered in the USA and thereby not subject to the Advanced Disposal Fee (ADF): however, such fraud would be comparatively complex to arrange. The number of collection facilities has almost doubled in the same period. The programme also picks up 6.5 million filters and 1,800 tonnes of containers, the majority of which were previously disposed of to landfill, although AUOMA concedes that improvements in container collection rates (currently standing at 45%) are needed. The Association claims a heightened public support for its scheme and notes that the biggest

3 This is difficult to verify as we are not privy to the assumptions which need to be made regarding

what constitutes a ‘recoverable’ fraction. However, AUOMA’s 2007 Annual Report states that the Association raised C$15.681 million (A$18.7 million) through the 5 cents/litre EHC suggesting that some 313.6 million litres of lubricant were sold in the Province last year. Data from the scheme show that 165,319,155 litres were levied in 2007.

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 14

recovery rate gains have occurred in rural areas previously disadvantaged by their remoteness. The success of the so‐called ‘Prairie model’ has led to its adoption in British Columbia, Saskatchewan, Manitoba and Quebec. However the programme has not been universally welcomed. Ontario is home to one of only two re‐refineries in Canada (SafetyKleen in Breslau, Ontario; the other is Newalta’s plant on Vancouver Island, British Columbia). This Province has so far resisted harmonization with UOMA and has recently implemented a program of its own for collecting filters and containers. Similarly, the maritime Provinces of Nova Scotia, Prince Edward Island and Newfoundland still choose to operate a retail service model. For many critics, the chief bone of contention is that the more environmentally favourable option of re‐refining used oil into new lubricants is not incentivised with the result that collected oil is more likely to be directed towards the residual fuel market. This argument seems justifiable given the high price of fuel. But although most of Alberta’s used oil certainly is directed towards combustion, a surprisingly high proportion is actually re‐refined. This, despite a lack of facilities in the Province and in the face of stiff competition from fuel uses ‐ used oil collectors are said to be paying some urban generators 10 to 18 cents (A$0.12 to A$0.21) per litre.

Fig. 2: End Uses for Collected Used Oil in Alberta in 2007

Recycled As Oil Base Stock

16%

Reprocessed Other Lub. Products

22%

Fuel for Lg. Industrial Burners

12%

Fuel for Asphalt Plants 45%

Fuel for Small Space Heaters

5%

Source: AUOMA 2007 Annual Report. NB: “Other Lub Products” are not actually new lubricants but lower grade products such as oil

fracturing fluids.

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 15

According to AUOMA’s 2007 Annual Report, although most of the 91 million litres4 passed on for recycling last year was burnt as a fuel (mostly in the Province’s asphalt plants), as much as 38% of the collected oil was apparently directed towards lubricant products (see Figure 2). This would seem too high a figure given that the Province lacks a re‐refinery, the closest plant being Newalta’s facility on Vancouver Island some 1,400 miles distant. However, AUOMA’s new chief executive informs us that the 22% of “Other Lub. Products” does not refer to re‐refining but rather a “lesser process [wherein] the used oil is used as additive for new products, like oilfield fracturing fluid.” Thus, the 16% figure reflects the truer ‐ albeit still surprisingly high ‐ figure for re‐refining of Alberta’s used oil.

3.1.5 Trade in Used Oil and Transport Economics

A striking feature of the management of used oil in Alberta is the extent to which collected oil is transported to end uses outside the Province (Table 1).

Table 1: Collected Oil End Uses& Destinations in 2007, litres

USED OIL End uses

Within Alberta

Outwith Alberta

% sent out of Province

Recycled as base oil 128,298 14,592,173 99.1%

Other lubricant products* 14,392,485 5,985,413 29.4%

Fuel for industrial burners 1,439,603 9,436,731 86.8%

Fuel for asphalt plants 26,930,501 13,490,622 33.4%

Fuel for small space heaters 2,014,692 2,666,592 57%

Total 44,905,579 46,171,531 50.69% Source: AUOMA 2007 Annual Report. Notes: *Refers to “lesser processes” where low quality lubricant is used as an additive, for

example, in oilfield fracturing fluids

The majority of the used oil that is sent out of the Province is directed to the west and south west for use as a fuel supplement in large‐scale industrial processes such as paper mills. Some oil filters are reported to travel as far south as Texas but the general rule of thumb used by collectors is not to exceed one day of travel or a maximum budget of 6 or 7 cents (A$0.07 or A$0.08) per litre.

4 86.9 million litres of used oil are reported to have been collected through the AUOMA scheme in

2007. We assume the 91 million litre figure for used oil processed includes additional volumes of used oil stockpiled from previous years. Also, according to AUOMA’s Annual Report figures on end-use volumes were not audited and may vary from the schedule of used oil materials collected because of production losses and changes in inventory.

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 16

3.1.6 Policy Priorities

AUOMA views accidental spillage into water bodies as the greatest environmental risk posed by used lubricating oil. The focus is squarely on maximising collection of oil provided that the material is not disposed of to landfill or spread on roads ‐ both legal practices in some Canadian Provinces. The focus on collection is such that oil filters and the containers in which lubricants are packaged and sold have become an increasingly important priority. The fact that used containers and filters can sometimes hold significant quantities of oil residues which risk spillage into water bodies if disposed of inappropriately provides the impetus. The method of disbursing funds through the RI via six zones in which different rates are paid is cumbersome and requires careful audit if it is not to be abused. The system sets financial payments as a proxy for market prices. Consequently, during periods when prices in general and oil prices in particular are changing frequently, the accuracy of the financial payments needs to be reviewed more often. Inefficiency is an inherent risk in any such detailed market intervention. Some contend that the potential for anti‐competitive practice is behind Ontario’s reluctance to adopt the UOMA model since oil companies, which manufacture lubricant products, have a vested interest in preventing competitors from manufacturing base oil derived from used oils. Equally there are concerns of market manipulation in the other direction. Should the Provincial government place tight limits on the market for burner fuels derived from used oil and arrange for a re‐refining plant to be constructed, the operators would then enjoy regional market power since there would be no prospect of a competing plant being opened.

3.1.7 Learning Points from the Alberta Case Study

Alberta’s AUOMA model has provided: • 10 years of stability in the system for collecting used oil • significantly increased collection tonnages during a period of static or

declining lubricant sales • rich data records on volumes and sources of used oil in a developed

economy • improved collection from isolated rural areas • data to demonstrate that oil filters and the containers in which lubricant

is sold present a potentially significant environmental hazard.

In the context of the options under consideration in Western Australia, the case study provides the following learning points:

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 17

• Stability was achieved through a mix of risk reduction policies, not through a single policy intervention.

• Once re‐refineries are built and their capital is regarded as a sunk cost,

the operators can compete for used oil over a very large geographic area. This might encourage high levels of short term financial support for re‐refineries to get them established in Australia.

• Major industrial plant closures and switches in industrial fuel demand

in Alberta during the 10 year period had no impact on the collection infrastructure.

• Risk to the collection system was reduced by enabling diversification of

outlets through out‐of‐Province trade.

• Risk of collection failure was further reduced with strict ‘fitness’ criteria for collection companies seeking registration to receive return incentive payments.

• Oil filters and lubricant packaging were shown to present associated

environmental risks to the quality of water resources. The significant differences between WA and Alberta overwhelm the superficial similarities such as the issue of isolation and also the presence of a large mining industry. A key issue, given the higher costs of transport from WA to reach other markets for used oil, is the experience of other developed economies that chose to encourage local re‐refining for the majority of the collected oil. For this reason our next case study investigates the experiences of Denmark.

3.2 Denmark, Europe

Two mechanisms for used oil collection operate side‐by‐side in the northern European country of Denmark. The Mineral Oil Branch (MB), a private sector body, incentivises the free collection of waste oils suitable for re‐refining through a levy on new gear, engine and hydraulic oils. The subsidy is paid based on the recovered oil ultimately re‐refined. Used oils contaminated with metals or with high volumes of water, such as marine lubricants and spent cutting and drilling fluids, are excluded from the MB programme. Generators of such non re‐refinable materials are instead required to pay market rates for their disposal. Denmark has recently prioritized regeneration over fuel uses for waste lubricant, effected via fiscal and regulatory changes. Before 2002, most

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 18

recovered oil was burnt in local district heating plants. The Danish government has accomplished this transition with minimal disruption to the collection infrastructure. This has been achieved by effectively restricting competition for used oil collection to two companies ‐ one operating the country’s sole re‐refinery. The same two firms dominate collection across both the MB and market systems. Denmark’s easy access to markets beyond its borders has further smoothed the transition from fuel uses to regeneration. In 2007, a total of 68.2 million litres of all lubricant types was consumed by Denmark’s population of 5.5 million. Although the MB system recovered just 18.3 million litres of waste oil in the same year, a 90% recovery rate is claimed since non‐re‐refinable materials are ignored in the calculation, which also assumes that half the remaining re‐refinable lubricant is lost in use. The volumes collected by the market outside the MB system are less clear, although one company reports that it collected 17 million litres of non‐re‐refinable used oils. Given Denmark’s small size (43,098 km2), high population density (127 per km2) and the fact that a significant proportion of the oil is excluded, it is reasonable to question the value for money achieved by the MB scheme. The running costs are some 30 million Danish Krone (A$7 million) per annum. Per litre of oil collected, we calculate the Danish system costs twice as much as Alberta’s.

3.2.1 Notable Differences with Western Australia

• A twin approach to used oil collection: a levy and subsidy programme for maximising recovery of re‐refinable used oils and a market‐based scheme for the remaining lower quality used oils.

• Although there are numerous populated islands, the country is small

(with around one‐sixtieth the land area of WA) with a far higher average population density.

• Transport economics allow used oil to be transferred by road tanker to

neighbouring countries, especially Germany, for approximately 2 to 3 Euro cents (A$0.04 to A$0.05) per litre. Similarly, Denmark’s proximity to Scandinavia permits ‘topping up’ of feedstock for its seaport‐connected Kalundborg plant in the event of reduced local supply.

• Denmark operates a highly regulated market in which two companies,

Dansk Olie Genbrug (DOG) and Gunnar Lund Olieservice, enjoy protection from market entrants in the collection of used oil. Notably, DOG also owns the one re‐refining plant operated in Denmark.

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 19

3.2.2 Background

In common with most of Europe, the Danish tax system historically favoured combustion outlets for used oil by setting the excise duty on fuel oil derived from treated used oil at zero. Denmark’s fiscal arrangements were the subject of an EU infringement case and in 1992 the difference in duty on fuel oils produced from waste oil versus virgin oil was removed. The change in the rules presented a problem for the Danish government as the economic incentive for waste companies to collect oil was thereby removed. With generators such as garages now required to pay collectors for the removal of used oil, the authorities were concerned that illegal disposal would result. To tackle the issue, the government started to subsidise used oil collection in 1993, financing the scheme by imposing an ADF (advanced disposal fee) of 2 Danish Krone (DKK) (A$0.48) per litre on sales of new lubricants. The government‐run system recovered between 35 and 40 million litres of waste oil per annum by the late 1990s. This has been estimated to represent perhaps 75% of the total used oil recoverable in Denmark, but such figures

400 km

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 20

are hard to verify given assumptions made concerning oil volume losses during use. The system was, however, considered expensive and by the late 1990s oil collection was increasingly viewed as something the State should not be managing directly. In 1998, the annual subsidy had reached 42 million DKK (A$10 million). Succumbing to political pressure, the government started cutting back the subsidy and eventually withdrew it, passing control of oil collection to the Mineralolie Branchenforening (MB), an industry association representing lubricant importers and sellers. On 1 July 2000 a new privately‐run scheme focusing solely on re‐refinable oils, and funded by a continuing ADF, was introduced and continues to the present day. The state tax on lubricant sales was withdrawn in 2002. Waste oils not suitable for regeneration were excluded from the MB scheme and are instead collected at market cost to generators.

3.2.3 Re-refinable Oils: The MB Collection System

The not‐for‐profit MB voluntarily runs a programme wherein a charge is levied on lubricant sold by its members. The levy now stands at 50 Danish øre (A$0.12)5 per litre and is payable only on lubricant grades which, at the end of their life, are suitable for re‐refining. This material tends to be used gear, engine and hydraulic oil. Oils designed for cutting, drilling and various marine purposes do not attract the levy and are excluded from the MB programme. The funds collected through the levy are passed to the Miljøpuljen ApS – an Environmental Pool fund used to subsidise the free collection of re‐refinable waste oils. The subsidy is disbursed on the basis of the volume of re‐refinable oil collected, after solids and water are removed. The current subsidy stands at around 1.5 DKK (A$0.36) per litre re‐refined. The subsidy is payable only for the output of base oil that is sold for lubricant uses6. We understand the MB plans to reduce it as base oil prices rise. The subsidy is paid for the total volume of both the regenerated base oils and fuel oils produced. Danish law does not preclude any firm from recovering used oil and claiming Miljøpuljen funds, but in practice the collection market is dominated by just two companies: Dansk Olie Genbrug (DOG), owned by Avista Oil (itself part of Mustad International Group) and its only significant competitor Gunnar Lund Olieservice. DOG claims to recover around two thirds of Denmark’s collectable oil with Gunnar Lund accounting for the rest. Both businesses are protected from new entrants to the MB scheme by a requirement that any oil collection company seeking to claim a subsidy must offer free, national collection for any quantity of used oil above 200 litres that is suitable for re‐refining. Although Denmark is

5 On 1 October 2008 this levy was lowered from 60 øre (14 Australian cents), reflecting the increasing

value in used oil since 2006 and thereby the reduced costs involved in its collection. Similarly, we have been informed that the subsidy passed onto the collectors has also been reduced.

6 The subsidy can be paid for oil that is refined using TFE (Thin Film Evaporators) similar to that used by Wren Oil at Picton - but only if the feedstock has been carefully selected.

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 21

small ‐ taking just four hours to drive its length ‐ the country is composed of numerous, populated islands. This disadvantages new collectors whose business plan is to start recovering local oil with the intention of eventually offering nationwide coverage. Discussions with DOG reveal that in 2007 it collected 13 million litres of oil of the type suitable for re‐refining. Following dewatering and the removal of solid contaminants at a plant in the city of Horsens, the remaining 10.4 million litres were then re‐refined into 7.8 million litres of base oil and 2.6 million litres of fuel oils. The 10.4 million litres regenerated by DOG would therefore have attracted a total subsidy of around 15.6 million DKK (A$3.7 million)7. Oil generators are also able to deposit waste lubricants at one of around 40 collection points distributed around Denmark. Unlike in Alberta, the scheme does not reward the collection of oil filters and lubricant packaging; instead the emphasis is on re‐refining at least 75% of the collected oil. Filters and containers are, however, collected through the market system.

3.2.4 Non-Refinable Oils: The Market System

Both DOG and Gunnar Lund dominate the collection market for lower grades of oils outside the MB programme. These include slops from shipping and oils containing metal impurities from cutting and drilling industries are not suitable for re‐refining. Unlike with the re‐refinable used oils, generators of such material are expected to pay for its collection and disposal. DOG reports that it collected around 17 million litres of such material in 2007, ensuring that re‐refinable and non‐re‐refinable grades of oil are collected separately, and asking generators producing both grades to keep them apart. A small quantity of oil is also collected outside the MB programme by several intermediary companies including the hazardous waste firm KommuneKemi and Stena Miljø a large general waste collector who then sell on re‐refinable oil to DOG. Stena Miljø also collects used oil containers and filters, something neither DOG nor Gunnar Lund are able to do since they lack the vacuum trucks for removing sand from the filters.

3.2.5 Re-refining Priority

Denmark had long delayed transposing into national law Article 3(1) of the 1975 EU waste oil directive (75/439/EEC) requiring Member States to prioritize re‐refining of used oil over fuel uses8. Instead, Denmark’s

7 Note that until September 2008, Denmark did not have a functioning re-refinery so the used oil regeneration described here would have occurred at the Dollbergen plant in Germany. 8 Article 3 (1) of Directive 75/439/EEC on the disposal of waste oils, amended by Council Directive 87/101/EEC of 22 December 1986, states: “Where technical, economic and organizational constraints so allow, Member States shall take the measures necessary to give priority to the processing of waste oils by regeneration.”

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 22

existing statute BEK 619 (Bekendtgørelse om affald 619 or ‘Statutory Order no. 619’) governing waste oil allowed it to be directed to heating uses as a means of recovering heat value. This is not surprising given that the country has had no domestic re‐refining capacity until very recently. Although a re‐refinery plant was established at the Danish seaport of Kalundborg in the 1990s, the 35 million litres per annum input capacity facility failed to perform for much of the decade. During this period most lubricating oil recovered was instead incinerated in district heating plants. In 2002, however, Denmark passed BEK 616 which amended BEK 619 by giving priority to re‐refining, thereby satisfying the EU. A voluntary target of re‐refining 75% of the collected used oil was subsequently inserted in the latest of Denmark’s National Waste Strategies. In the context of Denmark, re‐refining is taken to include re‐refining recovered lubricant into both new base oils and also new fuel oils. The subsidy is paid for the total dewatered lubricant regenerated. In order to support this target the State Government: • Taxed all fuel oils, which since 1992 included those derived from waste

oils; last year the excise duty rate on heavy fuel oil used for heating by businesses stood at the equivalent of 325 Euros (578 AUD) per thousand litres ‐ the third highest in the EU‐27 (Figure 3).

• Raised the emissions standards to such an extent that upgrading small

and medium‐sized power plants to meet the new regulations while continuing to burn waste oil was no longer cost effective. The main outcome has been that small district heating plants no longer are able to burn waste lubricating oil.

In 2003, the Mustad International Group from Houston USA, acquired DOG and subsequently also purchased the largest European re‐refining plant, the 150 million litre per annum capacity Mineralöl‐Raffinerie Dollbergen GmbH in Germany. This investment provided the opportunity to upgrade and enlarge the Dollbergen plant using the company’s solvent extraction based Vaxon process. But with both the Dollbergen and Kalundborg facilities running at around 70% capacity, Mustad decided to close Kalundborg in February 2005. For three years, used oil collected in Denmark was stockpiled at Kalundborg and exported by road tanker (and sea ferry) almost 600 kilometres south to Dollbergen.

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 23

Fig. 3: Excise Duty on Heavy Fuel Oil (Heating “Business Use”) in EU Member States

0

50

100

150

200

250

300

350

400

450

BEB G CZ DK DE EE EL ES FR I.E. IT IT CY

LVLT LU HU HU HU MT NL AT PL PT RO SI SK FI SE UK

Member State

Exci

se D

uty

Rat

e (v

alue

s in

EU

RO

per

th

ousa

nd li

tres

at 1

Oct

200

7)

Source: European Environment Agency 2007 NB: Minimum excise duty: 15 Euros per 1000kg

DK = Denmark

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 24

Recent higher oil prices and guarantees of continuing regulatory control over alternative fuel uses in Denmark made possible an investment decision by Mustad International Group to upgrade the Kalundborg plant in 2008. Previously, technical problems had meant that Kalundborg’s outputs were suitable only for industrial and bunker fuel markets. Moreover, the plant’s equipment was said to be relatively energy‐intensive. Industry contacts now inform us that the revamped Kalundborg, which re‐opened in August 2008, is significantly more efficient and now produces more widely accepted base oil products. From interviews conducted for this case study we are told that the outputs of the Kalundborg plant are:

Table 2: Kalundborg Plant Data

PRODUCTS Re-refined from Used Oil

Input Feedstock - Used Oil incl. water and solids

(million litres/yr)

Outputs (million litres/yr)

40.0 Base Oil Production 24.0

Fuel Oils 5.5 Heavy Fuel 2.5

Asphalt extender 5.0 Source: Estimates from trade interviews by Oakdene Hollins Ltd

Used oil is no longer being shipped south to Dollbergen. Additional used oil feedstock for Kalundborg has also been negotiated from nearby Sweden, and Norway, and DOG is now planning to source additional oil from Finland. These plans may prove to be frustrated by new re‐refining plants that were announced in 2008 for Norway (Puralube Nordic AS and Ineos Bamble AS) and Finland (see the following case study, Section 3.3). The only Danish outlet for lower quality oils collected by DOG and Gunnar Lund, and the bottoms from the distillation process at Kalundborg, is now as auxiliary fuel burnt by a hazardous waste incinerator run by KommuneKemi. The latter company does collect small quantities of oil itself and has in the past exchanged any re‐refinable material it recovers for poorer quality oil collected by Gunnar Lund. We understand that less than 1 million litres is now sold to KommuneKemi each year – and the figure is falling rapidly as the Danish government continues restricting waste oil combustion. DOG also exports these materials for fuel distillation at the Dutch ‘North Refinery’ and for a reduction process at the Salzgitter Flachstahl steel mill in Germany. For a period oily sludges and ‘bottoms’ from the re‐refining processes were also incinerated at the Ålborg Portland cement works but Ålborg chose not to renew its permit to process following the introduction of the 2005 EU Waste Incineration Directive. Two large Danish industrial groups, Danfoss and Grundfos, were until recently also

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 25

permitted to burn small but significant quantities of waste lubricating oil which they generate, but the practice has now been outlawed.

Fig. 4: Key Outlets for Danish Used Oil, 1990 – 2008

3.2.6 Metrics

Overall lubricant oil consumption in Denmark has been steadily falling, reflecting the general trend in developed economies as cars become more efficient in their use of lubricating oil. In 1986, just over 96 million litres of all grades were sold; last year sales stood at around 68 million litres (Figure 5).

300 km

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 26

Fig. 5: Consumption of Lubricants in Denmark

0

20

40

60

80

100

120

1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006

New

Lub

rican

t Con

sum

ptio

n (m

illion

litre

s)

Total Automotive Industrial Marine SundryLubricants

Source: Mineralolie Branchenforening

The MB estimates that of the total lubricants sold in any one year, roughly 60% are of the type that ultimately can be re‐refined. On that basis, around 41 million litres of re‐refinable lubricants were estimated to be sold in 2007. Assuming around 50% is lost in use, 20 million litres per annum would be expected to be recoverable. Thus, the MB system seems fairly effective as last year 18.3 million litres were actually collected (Figure 6). Unaccounted‐for oil is thought to be burnt illegally by farmers, and in small space heaters, although widespread dumping of oil is considered unlikely.

Fig. 6: Fates of Used Lubricants Collected through the MB System

0

5

10

15

20

25

2001 2002 2003 2004 2005 2006 2007

Mill

ion

Litre

s

Used Oil Collected Re-refined as Heating Oil Re-refined as Base Oils

Source: Mineralolie Branchenforening

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 27

In line with the new Danish policy favouring regeneration, over the last six years the volume of used oil re‐refined to base oil has steadily increased, while fuel oil production has plummeted. In 2001, just 1.7 million litres of base oil were produced from recovered oil. Last year, the figure stood at around 13.5 million litres. Figure 7 shows the fate of the used oil collected through the MB system in 2007. About 15% of the 18.3 million litres collected in 2007 was comprised of water and solid contaminants. The removal of the latter gave 15.5 million litres of used oil for which a total subsidy of 23.3 million DKK (A$5.7 million) was payable. Just over 2 million litres of heating oil and, as mentioned, 13.5 million litres of base oil were then produced.

Fig. 7: Management of Used Oil Collected in Denmark in 2007

Re-refined as Base Oils

74%

Re-refined as Heating Oil

11%

Water, Solids, Contaminants

Removed15%

Source: Mineralolie Branchenforening Although the Danish system is apparently achieving its target of maximising the volumes of oil being re‐refined, the system is not cheap. In fact, we estimate it costs almost twice as much as the Alberta programme. According to the Danish Topic Centre on Waste & Resources, in 2006 the MB scheme cost consumers approximately 30 million DKK (A$7 million). Although this suggests a 30% saving on the previous government‐run scheme which cost 42 million DKK (A$10 million), this is equivalent to 1.68 DKK (A$0.41) per litre of oil recovered. In 2007, based on the total income achieved through levies, we calculate that the Alberta scheme cost consumers just 18 Canadian cents (A$0.22) per litre recovered9.

9 According to the AUOMA Annual Report for 2007, 86,891,745 litres of used oil were collected at a

cost of C$15,681,140 in Environmental Handling Charges. This excludes C$567,921 raised by AUOMA from Investment income and C$3,076 in Registration fees.

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 28

3.2.7 Prices

With an increasing demand for oil products manufactured from re‐refined oil, the Dollbergen plant in Germany has been able to pay feedstock suppliers between 80 and 100 Euros (A$142 and A$178) per tonne for their used oil at the refinery gate. Despite the costs of transporting oil to Germany by road tanker (approximately 25 to 30 Euros (A$44 to A$53) per tonne including ferry costs), oil collectors in Denmark could remain profitable and the Danish used oil management system remain stable. In the event that gate prices fell, the DOG and Gunnar Lund could in any case ask for higher return incentive payments from the Miljøpuljen. The two oil collectors also receive payment from the lower quality oils they handle. As mentioned above, these non‐re‐refinable oils are excluded from the MB system and generators are expected to pay DOG and Gunnar Lund for their disposal. For example, we are informed that shipping companies will pay the collectors between 560 and 710 DKK (A$134 and A$169) per tonne. The price paid depends on the quality and volume of oil being recovered and the prevailing fuel price. The collection companies also raise revenue from selling the material to KommuneKemi at approximately 220 DKK (A$52) per tonne; they achieve even higher prices from the German and Dutch plants described above.

3.2.8 Learning Points from the Danish Case Study

• Denmark has focused on the collection of waste oils which are re‐refinable but has left the market to deal with the more problematic oil bottoms, marine slops, and oils contaminated with metals. Proximity to other markets, particularly in Holland and Germany, has provided outlets for such materials.

• In order to encourage private sector investment in a small‐scale re‐

refining plant, the State government took fiscal and regulatory actions designed to limit the threat presented by the competing market of industrial fuels.

• The increased risks to the stability of the collection system in relying on

a single local re‐refining plant were reduced by the plant’s owner (Mustad International) operating a second larger‐scale plant within economic transport distance.

• These risks were further reduced by requiring additional tank storage

capacity on‐site at Kalundborg.

• The regulatory controls placed over new market entrants further reduced the investment risk to Mustad International.

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 29

• The local collection company (Gunnar Lund Olieservice), equivalent to Wren Oil in WA, survived the acquisition of its only major competitor (DOG) and that competitor’s integration with the new re‐refining plant.

• Contracts with the collection companies include enforceable

performance terms. Failure to collect from remote locations on grounds that it is too expensive would lead to action under the contract. To date this has never been necessary. Performance bonds are not required since subsidy payments are made during each year.

However, as with Alberta, modest transport costs to neighbouring markets have permitted stability in Denmark’s collection system during upheavals in the market – this marks the single most important difference with conditions experienced in Western Australia.

3.3 Finland, Europe

Finland has a population of 5.3 million and operates a similar ADF system to that used in Denmark and elsewhere. A levy is charged on most lubricants and the accumulated fund is distributed to a single collection business targeting mostly the best quality used oil; suitable for re‐refining. The case study expands on the evidence from Denmark since a new 60,000 tonne re‐refining plant is being built and will be opened in 2009. Notably, the investment risks associated with the new privately‐funded re‐refining plant were reduced by controlling the burner fuel market and establishing a five year used oil supply contract with the monopoly collection business. We estimate that more than 40% of the collectable oil is left outside the subsidised collection system.

3.3.1 Notable Differences with Western Australia

• The State Government manages the fund raised from a levy on lubricant sales.

• Subsidies are paid to a single monopoly collector on the basis of an

open book ‘cost plus’ system. A five year contract is negotiated with the single collector to ensure that public service requirements are explicit.

3.3.2 Background

Historically, the management of waste lubricants in Finland was poor. Most recovered oil tended to be combusted in industrial burners with poor emissions standards. Increasing environmental awareness in the 1980s led

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 30

to the passing of new regulations governing waste oil in Finland10. The Ekokem hazardous waste incinerator (discussed below) was opened at Riihimäki in 1984 with greatly improved emissions levels. In December 1986 Laki öljyjätemaksusta, ‘the law of waste oil fees’, introduced the current system of a levy on most lubricants and a subsidy paid for its collection. In line with other EU Member States, the Finnish regulations now state that where technically feasible it is necessary to prioritize regeneration (re‐refining) of used lubricant over energy recovery.

3.3.3 Collection System

As in many other jurisdictions a levy and subsidy system operates in Finland, although here it is the State government which is responsible for its management. Since 2006, the levy (oljyjätemaksu) has been set at 5.75 Euro cents (A$0.11) per litre of new lubricant sold. The levy is payable on any lubricant which is destined to become waste oil in Finland, so new oils which are to be exported are exempt, as are those which are wholly consumed during use.

10 1986 Law for Waste Oil Fees (Laki Oljyjatemaksusta 5.12.1986/894) and 1987 Decision of the

Council of State to limit waste oil burning. This decision (447/1987) banned the burning of used oil derived fuels in plants of less than 5 MW output.

600 km

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 31

The levy is passed on to the Ministry of the Environment which then uses the money in two ways. A proportion is used to subsidise the collection, transportation and storage of waste oil, while the rest is directed toward an Oil Conservation Fund (Öljysuojelurahasto) for cleaning up soil and water contaminated with spilled lubricant oil. In Finland, the waste oil collection market is monopolised by Ekovoima Oy (literally ‘Eco Power Ltd’), a subsidiary of Ekokem Group, and this is the only company which directly receives the subsidy. In the past some competition was provided by the Finnish environmental management and services giant L&T (Lassila & Tikanoja), but as discussed below L&T has now changed its focus to oil reprocessing. The exact amount of subsidy paid to Ekokem varies according to the cost of the collection operation and, according to the rules of the Finnish Council of State (Valtioneuvosto), is set at a level such that the collecting companies can make ‘reasonable profit’. Rather than being paid per litre collected, Ekokem is instead given a fixed annual subsidy depending on the yearly cost of oil collection. This is essentially a ‘cost plus’ contract based on an open book arrangement in which the collector provides accounting information as required. Ekokem’s 2007 Annual Report states that it received €2.052 million (A$4.1 million) of waste oil subsidy in 2007. This is slightly down on the 2006 figure of €2.558 million (A$5.2 million) because increasing efficiencies and crude oil price rises last year led to greater profits for Ekokem. We estimate that this subsidy is equivalent to 9 Euro cents per litre in 2007 (A$0.18). For the year 2008, the Finnish Ministry of the Environment informs us that no subsidy at all may be paid since Ekovoima is now so profitable. However, our contact at Ekovoima thinks a small subsidy of €0.5‐1 million (A$1 to A$2 million) might still be disbursed (equivalent to between 2 and 4 cents, or A$0.04 to A$0.08, per litre). Ekokem’s 2007 report also reveals that the Ministry of the Environment and Ekokem signed a new five year agreement for managing waste oil collection in Finland. Ekovoima has nationwide responsibility for overseeing the collection and handling of Finnish waste oil, and delivery to the ‘appropriate’ processor. While in some municipalities the company will collect directly, in most parts of the country it sub‐contracts recovery to a number of other smaller firms which are also subject to new five year contracts with Ekovoima. The latter are required to use standard vehicles, uniform and other visible branding symbols to reassure generators that they are part of the official collection scheme. Part of the subsidy agreement is that any quantity of good quality oil exceeding 400 litres is collected at no charge to the generator. Generators of smaller quantities of good quality used lubricants are required to pay for

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 32

collection. We understand the amount charged varies between 15 and 48 Euro cents (A$0.30 to A$0.96) per litre depending on the transportation distance and whether or not other wastes can be recovered at the same time. Collectors are also permitted to charge generators a disposal fee for lower quality oils contaminated with more than 10% water and other foreign particles, regardless of the volume collected. The charge includes an additional 20 Euro cents (A$0.40) per litre processing fee and varies between 35 and 68 Euro cents (A$0.70 to A$1.36) per litre depending on transportation distance. Generators are requested to keep the different grades of used oil separately. Small volumes of waste oil can also be deposited free of charge by the public at collection points provided by ‘municipal waste corporations’ and are handed over to Ekovoima. The municipalities pay Ekovoima approximately 20 cents per litre (A$0.40) for this service as the oil is typically of a poor quality.

3.3.4 Reprocessing

All waste lubricant collected in Finland is reprocessed or disposed of in‐state. This looks likely to continue given the imminent commissioning of a major new regeneration facility described below. The fate of collected oil will depend on its quality but, where feasible, regeneration is now Finland’s priority. Until autumn 2007, the vast majority of waste oil was burnt, either in large industrial plants or at Ekokem’s hazardous waste incinerator at Riihimäki. The plant at Riihimäki has been in operation since 1984 and meets tight emissions controls11. A small amount (2,000 tonnes annually) of recovered material categorized as ‘white’ used oil was ‐ and still is ‐ sent for de‐watering and cleaning at another Ekokem facility in Jämsänkoski. The output from this plant tends to be lower quality base oils and is used mainly in the forestry sector for cutting tools. Waste oil of the type formerly sent for burning is now being stockpiled by a separate company called L&T Recoil Oy, a joint venture company managed by L&T. This is in readiness for a new 60 million litres per annum capacity oil re‐refinery located at the Finnish port of Hamina (Figure 8). Originally scheduled for the end of 2008, the Hamina plant’s opening has been delayed until spring 2009.

11 The plant is compliant with WID (Waste Incineration Directive) requirements on emissions

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 33

Fig. 8: Waste Oil Reprocessing Facilities in Finland

250 km

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 34

The Managing Director of L&T Recoil informs us that the new plant uses similar technology to that employed by Puralube at its plant in Tröglitz near Leipzig in Germany. It will be able to reprocess waste oils into new base oils SN150 and SN500 for overseas markets. The plant would thereby easily qualify for the highest level of PSO benefit in Australia. We understand that all the Finnish sourced waste oil to be reprocessed by L&T Recoil will be delivered by Ekovoima as part of a new five year contract. However, 50% of its feedstock will need to be imported from other countries. Hamina was probably chosen as a location in order to give the plant convenient access to feedstock from nearby countries such as Poland and Sweden. This plant will likely compete for regional feedstock with the newly re‐opened Danish facility at Kalundborg described in the previous case study (Section 3.2). In addition, Puralube, in association with Ineos Bamble AS is opening a new 85 million litre per annum re‐refining plant at Ronningen, Norway in 201012. Approximately 10,500 tonnes of used oil, not best suited for regeneration, is likely to continue to be directed towards combustion in industrial plants, although their output must exceed 5 megawatts and meet the strict emissions standards.

3.3.5 Metrics

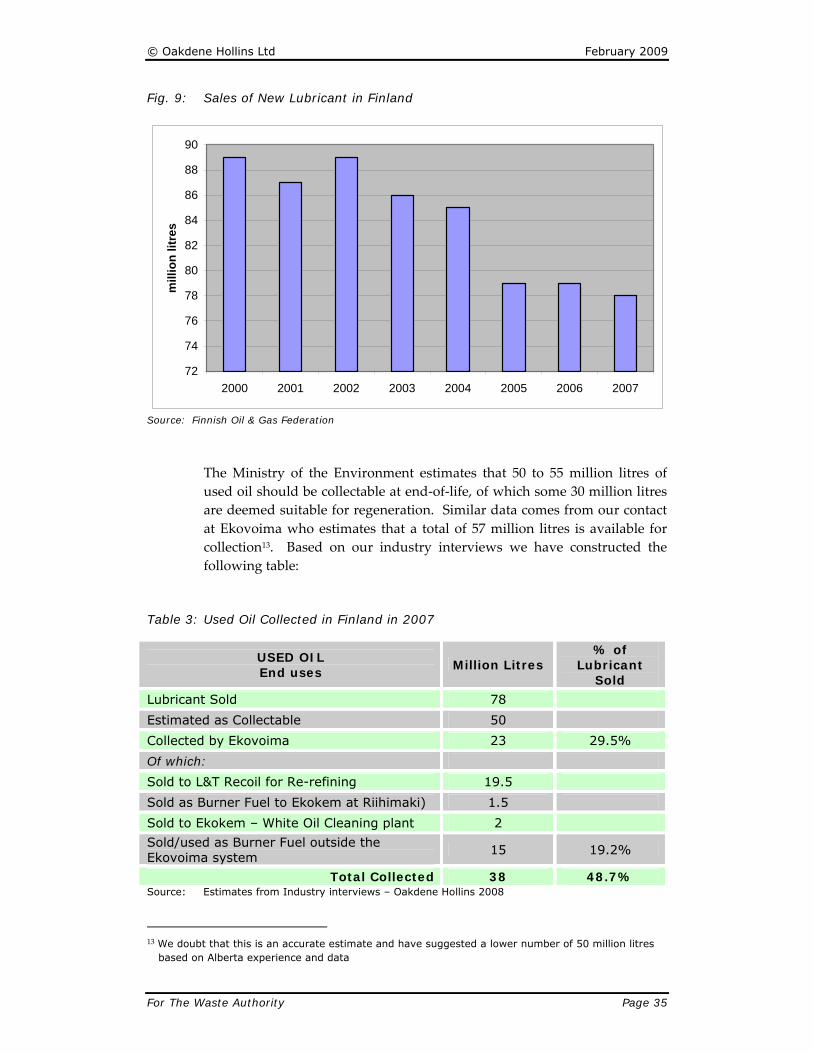

Neste, Shell and Teboil dominate the market for lubricating oil sales in Finland. According to the Finnish Oil & Gas Federation, a total of 77.86 million litres of new lubricant were sold in 2007, 31.93 million litres of which being motor oil. As in other developed economies, this represents a significant decline in sales as lubricant longevity increases (Figure 9). In 1990, almost 118 million litres (of all grades) were sold. Given the 5.75 Euro cents (A$0.11) per litre levy on sales of new lubricant, we calculate that in 2007 the Finnish government should have collected some €4.5 million (A$9 million). This broadly concurs with the €4 million figure for total levies collected in 2007 published by the Finnish Oil & Gas Federation.

12 The reported investment cost is US$70.6 million

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 35

Fig. 9: Sales of New Lubricant in Finland

72

74

76

78

80

82

84

86

88

90

2000 2001 2002 2003 2004 2005 2006 2007

mill

ion

litre

s

Source: Finnish Oil & Gas Federation

The Ministry of the Environment estimates that 50 to 55 million litres of used oil should be collectable at end‐of‐life, of which some 30 million litres are deemed suitable for regeneration. Similar data comes from our contact at Ekovoima who estimates that a total of 57 million litres is available for collection13. Based on our industry interviews we have constructed the following table:

Table 3: Used Oil Collected in Finland in 2007

USED OIL End uses

Million Litres % of

Lubricant Sold

Lubricant Sold 78

Estimated as Collectable 50

Collected by Ekovoima 23 29.5%

Of which:

Sold to L&T Recoil for Re-refining 19.5

Sold as Burner Fuel to Ekokem at Riihimaki) 1.5

Sold to Ekokem – White Oil Cleaning plant 2

Sold/used as Burner Fuel outside the Ekovoima system

15 19.2%

Total Collected 38 48.7% Source: Estimates from Industry interviews – Oakdene Hollins 2008

13 We doubt that this is an accurate estimate and have suggested a lower number of 50 million litres

based on Alberta experience and data

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 36

Around half of the used oil collected in Finland comes from garages, with the rest arising from industrial uses.

3.3.6 Prices

The price data gathered from industry sources is summarised as:

Table 4: Used Oil Collection Prices in Finland in 2007/8, Euro cents

USED OIL Types

Collection Price Cents

per litre

Subsidy (2007) Cents

Subsidy (2008) Cents

Clean oil in quantities > 400 litres Free 9 2 – 4

Clean oil in quantities < 400 litres 15 - 48 9 2 – 4

Oil contaminated with >10% water etc 35 - 68 9 2 – 4

Oil from Municipality Collection Points 20 9 2 – 4

Oil sold to re-refinery (mid 2008 Gate Price)

16 - 18

Source: Estimates from Industry interviews – Oakdene Hollins 2008

3.3.7 Learning Points from the Finnish Case Study

• In common with Denmark the collection system is designed to target the oil most suited to re‐refining and to prevent it from being used as a burner fuel.

• The quantity of oil outside the levy and subsidy system represents, we

estimate, slightly less than 40% of the collected oil in Finland. The regulatory authorities are confident that this is managed correctly as there is a culture in which inappropriate management would be unacceptable.

• The construction of the new re‐refining plant was supported by the

State government by preventing competition from burner fuel markets and providing an assured five year supply of suitable oils.

In order to provide a broader evidence base we have included a short case study of Spain (Section 3.4) which has very recently reformed its system in order to encourage the collection of all used oils whilst giving priority to re‐refining to base oil.

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 37

3.4 Spain, Europe

Until 3 June 2006, Spain operated a national system of subsidies for the collection and processing of used oils. The maximum level of these subsidies was:

Table 5: Maximum Subsidies for Used Oil in Spain until 2006

USED OIL

Euro Cents per litre

A$ cents Equivalent

Transport & collection 2.405 4.8

Re-refining 6.612 13.2

Treatment to produce a burner fuel or bituminous product

1.804 3.6

In practice, the budget for these subsidies was uncertain from one year to the next. In 2002, for example, the budget shortfall was 11% and in 2003 the budget shortfall was declared as being 50% until intense lobbying led to a more generous budget provision. The uncertainty created by the budget changes led to a wholesale review of the system and, in common with Denmark, the system was delegated to a new private sector organisation funded by a levy of 5 cents per litre (A$0.10) on most new lubricant sales. In 2007 lubricant sales in Spain were approximately 520,000 tonnes. Legislation was agreed in June 200614 that created SIGAUS (Sistema Integrado de Gestion de Aceites Usados). In October 2008 the collection subsidy was reduced slightly (from 2.88 to 2.68 cents per litre (A$0.5.5) in recognition of the higher values attached to used oils during 2008 in particular. The new rates of subsidies are:

Table 6: Maximum Subsidies for Used Oil in Spain in2008

USED OIL

Euro Cents per litre

A$ cents Equivalent

Transport & collection 2.68 5.5

Re-refining 9.00 18.0

Treatment to produce a burner fuel or bituminous product

2.40 4.8

The SIGAUS management board is expected to achieve targets for diverting a proportion of the collected used oil to re‐refining. These annual targets

14 RealDecreto 679/2006 “por el que se regula la gestion de los aceites industrials usados”

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 38

are 55% in 2007 and 65% in 2008, with a review in 2009 with the aim of identifying the opportunity to increase the target further. In practice many collectors pass on their right to claim a subsidy to the reprocessor of oil, whether for burner fuel or re‐refining as base oil. Although the system encourages competition between collectors, the market power of the re‐refining plant operators is leading to an increasing market share for integrated collection and re‐refining companies. 214,000 tonnes of used oil are reported as being collected, of which 120,000 tonnes are re‐refined. We are not confident that this information is accurate as we are aware that Portugal exports approximately 30,000 tonnes of used oil into Spain, of which 10,000 tonnes are directed to re‐refining. The current re‐refining capacity in Spain is not more than 95,000 tonnes although new capacity is being planned in the Rioja region.

Table 7: Re-Refining Throughput by Plant, 2008

Plant Tonnes

CATOR 32,000

ECO LUBE 27,000

AURECAN 18,000

AUREMUA 18,000

TOTAL 95,000 Notable differences between this system and those managed in Denmark and Finland are: • Subsidy payments are made for all used oil feedstock, thereby

encouraging collection of oil regardless of its origin. The higher subsidy for re‐refining seeks to make it competitive with burner fuel markets thereby encouraging collectors to keep separate those oils suitable for re‐refining. In 2008, collectors were being paid up to 16 Euro cents per litre (A$0.32) on the gate by re‐refineries in Spain.

• During 2008, most oils are reported as being collected free of charge in

Spain except for Marpol (marine) wastes and heavily contaminated industrial oils.

• The subsidy for re‐refining has encouraged proposed new investment

in the sector albeit during a period of exceptionally high oil prices.

• The levy on lubricants raises approximately €26 million (A$52 million). We estimate that SIGAUS performs at broadly the same level as

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 39

Finland in paying 12 Euro cents (A$0.24) for every litre of collected used oil, with a similar proportion directed to re‐refining.

3.5 Summary Case Study Metrics

Comparing the outcome measures from the three detailed case study jurisdictions (Table 8) raises questions over the definitions of terms, and the data associated with those definitions. In Alberta, re‐refining includes use of the collected oil as a drilling lubricant, which requires very little treatment to meet the necessary specification. In all three, different methods are used to estimate the proportion of sold lubricants that are collectable. In Alberta this is especially important given the significantly higher level of lubricant sales. Denmark and Finland have introduced complex ADF (Advanced Disposal Fee) systems to target only those oils suitable for re‐refining. Other used oils are subject to high collection prices with the risk that this provides an incentive for inappropriate disposal. When challenged, the authorities in both countries did not consider this risk of environmental damage to be a real one ‐ for cultural reasons. At a broad level of comparison, Western Australia appears to be performing well, with comparatively high levels of per capita lubricant sales and a percentage collection level similar to that achieved in Finland and Denmark. By 2009 the main difference will be that WA will direct no oil to re‐refining.

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 40

Table 8: Summary Metrics from Case Studies 2006/7

Western Australia

Alberta Denmark Finland

System Operator Fed Gov Private-sector

(UOMA)

Private-sector

(Mineral Oil Branch)

Private sector

(Ekovoima)

System Funded by ADF ADF ADF ADF

ADF per litre 5.449 cents 5.0 cents 50 øre 5.75 cents

ADF Total Annual Fund (Million)

27.7 C$15.7 DKK30 Euros 4.5

ADF (A$m equivalent)

A$3.8 WA Only A$18.7 A$7.0 A$9.0

Incentive Paid to Reprocessor Collector Collector Collector

End-use Prioritization Yes,

Re-refining No Yes,

Re-refining Yes,

Re-Refining

Population (millions) 2.1 3.3 5.47 5.5

Lubricating Oil Sold (tonnes) 70,000 165,319 70,000 78,000

Used Oil Collected within ADF System (tonnes)

42,300 87,000 18,300 23,000

Total Used Oil Collected (tonnes)

42,300 87,000 40,000 38,000

Of which: Long Distance Transport (%) > 15% 50%

> 15% Nil from

2009

> 20% Nil from

2009 % to Base Oil for Lubricant1 (estimate for 2009)

0% 16% 60% 60%

Notes: 1. Re-refining to base oil for use as a lubricant

© Oakdene Hollins Ltd February 2009

For The Waste Authority Page 41

4 Base-Line Scenario

This section describes likely outcomes over the period 2008 to 2011 should the State Government make no additional interventions in the market for collection and processing of used oil. In order to frame this base‐line scenario, the following “business as usual” assumptions have been made: • The 2008 PSO review will lead to no significant changes in the current

system of benefit payments to processors of used oil. • The substitution of solid fuels by gas in the grid and off‐grid power

sectors, as well as in energy‐intensive industrial processes, will continue15.

• Demand for lubricants in 2006/7 of 72.6 million litres will grow by

approximately 3.5% in each year to 201116.

• Volatile prices (upwards and downwards) for mineral oil products will continue.

• Research carried out by Wren Oil on the incorporation of ‘bottoms’ into

asphalt uses will result in no new commercial applications by 2011.

• The substitution of long cycle carbon fuels by short cycle carbon fuels to reduce the CO2 emissions from energy‐intensive processes will either begin or, in some cases such as cement production, continue.