analytical overview of russian perfumery & 2017 osmetics ... · analytical overview of russian...

TRANSCRIPT

2017Analytical overview of Russian perfumery &

cosme tics industry

2 Market Review: Russia is gaining momentum

4 Face Care: Beauty Reflexion | 7 Make-up: Bright palette

10 Hair Care: Right up There | 14 Body Care: Pile on Pounds

16 Bath Care: Bubbling and Sparkling | 18 Male Care: Booming Grooming

22 Sun care: Blaze in Glory | 24 Oral Care: Smart and Bright

26 Retail: Healthy Drogerie | 30 Perfumery: Blessed Blossom

34. Baby Care: Little pigeons

WWW.INTERCHARM.RU/EN

TIME FOR

2 MARKET REVIEW

MORE ON WWW.INTERCHARM.RU/EN

RUSSIA IS GAININGMOMENTUM

There are more than 50,000 new cosmetic pro ducts available on the Russian market. The Russian cos-metics market (2.2% of the world) occupies the fourth place in Europe after Germany, France and the Unit-ed Kingdom. The attractiveness of Russia for the perfumery sector is due to the size of its market with a population of 144 million inhabit-ants, mostly urban, its demography: a third of the population – women between 20 and 60 are the most ac-tive consumers of cosmetics.

Their average annual expenditure on cosmetics is around 170 euro for personal hygiene and beauty, which implies active spending up to 30% of their salary. This is higher than in the countries of Western Europe. The Russian cosmetics market is one of the most dynamic in the world and, has been able to grow at a rate of over 12% per year. The LVMH bet is a winning horse. The French group Moet Hennessy Louis Vuitton has completed the purchase of 100% of the perfume network Ile de Beaute which will certainly give Ile de Beaute the chance to win mar-ket share. Ile de Beaute is, by vol-ume of sales, the third specialized retailer of cosmetics and perfumes of Russia, after L’Etoilе and Rive Gauche. Ile de Beaute revenues in 2016 amounted to 300 million eu-ros, to achieve a net profit of around 6.5 million euros. L’Etoile turnover in 2015 amounted to 1.2 billion eu-ros, Rive Gauche invoiced 500 bil-lion euros, according to an estimate by RBK, news agency and market reports.

Mass-market brands like L’Oréal, Mary Kay, also tend to steadily show a good perfomance, as well as luxury brands like Chanel, Dior, Clinique or Givenchy. Apart from

the specialized perfumeries, domi-nated by three large chains, – Ile de Beaute, L’Etoile, Rive Gauche, – a large part of cosmetics (about 60%) are now sold in drugstores, among which stand out those of Magnit, the largest chain of Russian hypermar-kets. Its Magnit Kosmetik cosmet-ics store formats (€ 1 billion sales in 2015) have grown dramatically in recent years, being very close to the sales of L’Etoile, the current leading perfumery chain in the market.

As for countries, France has tradi-tionally been an undisputable leader in cosmetic export to Russia when goes to premium class cosmetics, skin care pro ducts and perfumes. Second largest exporter is Germany, especially in hair and body care and eco industries. Poland holds the seventh position exporting mainly make-up and wash substances. Within the last few years, cosmetic goods originating from the US and Italy have also gained great popu-larity in Russia, mainly due to ag-gressive marketing and promotional campaigns. South Korea came into top 10 chart in the past year.

Recently, the more and more cosmetic brands tend to increase energize their promotional push, noticeably increasing their market-ing budgets. The most prominent growth has been performed by GlaxoSmithKline (+93%), Beiersdorf (+68%) and Avon (+38%). According to recent statistics, the steak of e-commerce transfer in the cosmetic market in Russia has by now been developing at the level of 4-5% of overall value. Google and Yandex, the growth rate of search queries concerned with cosmetics performs an average figure of 25% annu-ally, which means over 7 million queries monthly. The most popular

keywords used are: Chanel, Yves Rocher, L’Oréal, Lancôme and Cli-nique. On-line store bestsellers are mostly cosmetics coming from Ger-many, France and Poland.

There are presently two main rea-sons to on-line selling rapid growth in Russia. The first one is a large number of fake brands operating on Russian market tampering or imitat-ing popular international brands, sold at lower prices. The second one is well-built logistics infrastruc-ture which enables for people from outlying districts an easier access to well-known brands often unavail-able in local stores. According to a common experts’ opinion, the Rus-sian on-line cosmetic market is about to achieve a value similar Eu-ropean within the next 5-6 years.

Other brands are also looking for new ways to enhance their impact on the market.

In September, L’Oréal Russia has inaugurated the extension of its plant in the Kaluga region, located 85 km south of Moscow. With this extension, L’Oréal opens new pro-duction lines for L’Oréal Paris and Garnier skincare pro ducts. The fo-cus of the plant’s extension was to respond to the growing demand of its pro ducts by the consumers, at the main time addressing new norms of quality, security and sus-tainable development.

Established in 2010 for the pro-duction of hair care pro ducts (sham-poos, hair conditioners) and hair-dyes for L’Oréal Paris and Garnier brands, the plant initially covered an area of 10000 m2 in the Vorsino in-dustrial park. In 2015, L’Oréal decid-ed to implement the second phase of the investment project, creating an extension of 13,700 m2. The extension allowed to double the ca-

MARKET REVIEW 3

MORE ON WWW.INTERCHARM.RU/EN

pacity of pro duction, to produce new pro ducts and to integrate highly ef-ficient modern technologies aimed at preserving the environment. The extension project started in March 2016, and the first tests of equip-ment and pro duction of Garnier sk-incare pro ducts were carried out in July 2017.

Foreign investors keep persis-tently launching at Russian market new brands or pro duct series. Asian cosmetics, especially those if Japa-nese, Korean, Chinese and Thai ori-gin, have recently become an over-taking cosmetic and beauty trends. The clue to their success roots in those brands’ favorable quality cou-pling with modest pricing. The most compelling part of those goods, as revealed, is presence of such in-gredients as green tea, bamboo, coco-nut and white truffle extracts and essences. Promptly caught by Russian manufacturers, this trend immediately got adopted by domes-tic brands adding such pro ducts to their offer.

According to Euromonitor Interna-tional, the Russian beauty and per-sonal care market recorded a posi-tive performance in 2016, thanks to a number of categories in which both economy and premium brands recorded sales increases through the launch of new formats and multifunctional pro ducts. Younger consumers, who are especially in-fluenced by social media, are also becoming more interested in beauty and personal care pro ducts due to growing social pressures. Beauty and personal care companies are increasingly attempting to attract consumers at an earlier age, target-ing advertising and marketing cam-paigns towards the younger genera-tion.

Mass beauty and personal care had higher sales than premium beauty and personal care in 2016, especially in categories in which pro-ducts are seen as daily essentials, such as bath and shower, hair care and oral care. The majority of con-sumers experienced low spending

power and wanted to economise, which continued to benefit the mass segment. However, in terms of facial skin care, consumers preferred to choose these pro ducts more care-fully, where possible purchasing masstige and premium brands.

The competitive environment in Russia in 2016 was very fragment-ed and diverse. With the presence of multiple brands, from luxury to low-cost, consumers have a wide range of options from which to choose. Due to declining disposable incomes, some Russians switched to private label pro ducts due to their more affordable prices. This was most evident in bath and shower, depilatories, men’s grooming, oral care and hair care.

Despite the unfavourable eco-nomic circumstances, innovation was employed by various players, often managing to drive up volume sales and, more importantly, value sales. In the majority of beauty and personal care categories, key man-ufacturers continued to introduce new ingredients, largely natural and organic, as well as playing with the format, scent and texture of pro-ducts and improving the ability of pro ducts to solve specific problems. New launches also fuelled sales in the innovation-driven skin care cat-egory, and especially facial care.

Domestic Russian cosmetic brands have also performed a great deal of competition against western manufacturers, attracting more and more customers by offering original pro ducts and creative packaging de-sign.

There are more than five hundred cosmetics manufacturers in Russia. Among these companies are differ-ent in scope and range of its activi-ties. Manufacturers of cosmetics in Russia provide pro ducts for daily skin care: its nutrition, cleansing, moisturizing and protection. They also develop pro duction of special tools: intensive anti-ageing skin cream, baby cosmetics, pro fes sio-nal salon cosmetics, as well as pro-ducts to treat acne and other skin

problems. Another trend in modern cosmetics is interest in natural and organic pro ducts.

The key to success of the Russian manufacturers of cosmetics are modern pro duction methods and beneficial properties of natural in-gredients. Local herbalists have al-ways been famous for their recipes based on natural pro ducts that have been adapted to current conditions and successfully used in manufac-tures of medical cosmetics for face and body.

Demand for innovative packag-ing for cosmetic pro ducts increases year by year. The annual average growth rate of the Russian cosmetic market is 15%. Russia takes a lead-ing position in the world in the im-plementation of cosmetic pro ducts. A prospective market is luxury cos-metics, including pro ducts for chil-dren and men. At the same time, many companies prefer to buy Eu-ropean packaging that looks expen-sive and stylish. Russian manufac-turers gladly buy the package from Europe, that can boast high quality and innovative solutions.

Positive momentum is anticipat-ed for beauty and personal care in Russia, which is predicted to see a value CAGR of 2% at constant 2016 prices over the forecast period, ac-cording to Euromonitor Interna-tional. Possible threats to growth could be ongoing tight household incomes, as well as the competition from retailers and their private label pro ducts, which would push the av-erage unit price down, forcing large companies to innovate and offer dif-ferentiated pro duct quality to justify the difference in price to consumers keen to save money.

There continues to be strong de-mand for the Western technologies and pro ducts for the Russian manu-facturers and customers. And there continues to be a requirement for substantial investment: processes and pro duct quality are in particu-lar need of further optimisation in the manufacturing of cosmetics and perfumery.

4 FACE CARE

MORE ON WWW.INTERCHARM.RU/EN

BEAUTY REFLEXION1. MARKET SIZE

Facial care is the key driver to growth in Europe and as all experts agree it’s the segment where new technologies and pro duct launches take place. Euromonitor positions Russian facial care as the fifth larg-est in Europe with 8% year-on-year growth and further average dynam-ics of 9% up to 2017. Russian con-sumers are very fastidious in their choice of facial skin care, they prefer a multi-functional pro ducts such as BB-creams, anti-aging treatments, moisturizing creams and serums.

Facial care registered the stron-gest current retail value growth in skin care, being the last pro ducts Russian consumers would econo-mise on, though unit price hikes were greatest in this category, especially in the premium segment. Micellar water was a trend in facial cleans-ers, with mass brands quickly adopt-ing the novelty from premium brands and earning consumers’ loyalty.

The skin care category in Russia is still developing, with more con-sumer groups joining, and consum-er concerns are increasing about the quality of skin care pro ducts, especially facial care.

According to Euromotitor, anti-ag-ers registered the strongest current retail value growth of 28% in 2015, due to developments and rises in the prices of premium brands, which are considered by consumers to be the most effective in anti-agers. 2015 was successful for all cat-egories. Forecast for 2016 results predicts slightly slow dynamics for facial care with the most impressive growth in masks and moisturisers.

Niche brands demonstrated good performance – a number of pro-fes sio nal facial care brands such as Elizabeth Arden PRO and Ioma entered the category in Russia.

These pro fes sio nal brands target middle-aged consumers and benefit from innovations and a scientific ap-proach to facial care pro ducts.

Skin whitening is not a feature demanded by Russian consumers. However, by the end of 2015 skin whitening premium pro ducts started to appear more often on the shelves of health and beauty retailers and this trend continued in 2016.

2. CONSUMER HABITSAlong with the growing matu-

rity of skin care, consumers con-tinued to change their purchasing preferences towards more rational choices, as they thought about the

necessity of each pro duct. Consum-ers wanted to buy higher-quality brands at reasonable prices, and therefore started to educate them-selves about ingredients and pro-ducts. Increasing interest in Korean brands was observed in facial care. Korean brands offered unique pro-ducts with exotic ingredients such as snail secretion filtrate, soya and white truffle extracts.

The consumers’ preferences are shifting towards domestic pro ducts. However, even in this case the Rus-sians are not inclined to save on fa-cial care. When selecting pro ducts, they pay attention not only to the price but also to the brand.

Market Sizes | Historical/Forecast | Retail Value RSP | RUB bn | Constant 2015 Prices

Geographies Categories 2013 2014 2015

Russia Acne Treatments 4,50 4,40 4,90 4,80

© Euromonitor International

Market Sizes | Historical/Forecast | Retail Volume | TonnesGeographies Categories 2013 2014 2015 2016 (forecast)

Russia Acne Treatments 823,60 794,90 762,80 739,00

© Euromonitor International

Market Sizes | Historical/Forecast | Retail Value RSP | RUB Per Capita | Constant 2015 Prices

Geographies Categories 2013 2014 2015 2016

Russia Acne Treatments 31,50 30,60 33,90 33,20

© Euromonitor International

Brand Shares Ranking (Global - Historical Owner) | Historical | Retail Value RSPGeographies Categories Brand Company name (GBO) 2015

Russia Acne Treatments Basiron Nestlé SA 1

Russia Acne Treatments Zinerit Daiichi Sankyo Co Ltd 2

Russia Acne Treatments ClearasilReckitt Benckiser Group

Plc (RB)3

Russia Acne Treatments Curiosin Richter Gedeon Nyrt 4

Russia Acne Treatments Garnier Chistaya Kozha Aktiv L'Oréal Groupe 5

© Euromonitor International

FACE CARE 5

MORE ON WWW.INTERCHARM.RU/EN

Consumers are increasingly look-ing for value for money pro ducts which are natural and healthy for the skin, provide a range of combined benefits of high priced premium pro-ducts at a lower cost. This pro duct class has been dubbed “masstige”.

According to Ipsos survey, over one half (55%) of Russian popula-tion use skin care pro ducts, mainly women – 86% of them use skin care pro ducts; among men – 19% (one in five). Women aged 25-44 make the backbone of target audience (most active users of facials). Day cream use 51%; night cream – 37%, hy-gienic lipstick – 31%; gel and facial wash – 31% and makeup remover (lotion, toner , etc.) – 27%.

Among TOP-5 skincare brands are: Avon with 23%, Nivea with 22%, Chistaya Linia with 21%, Cherny Zhemchug with 18% and Oriflame with 14%.

3. TRENDSRussian women still looking for

a premium skin care and it has led brands to introduce more sophisti-cated pro ducts contributing to the premiumization trend.

Another particular consumer trend for facial care in Russia is us-ing all range of pro ducts for a daily treatment. For an average West-ern woman, it is enough to just put some moisturizer, while a Russian woman would use an entire range of cosmetics, including regular facial masks, peeling creams and prim-ers. They also start to use anti-aging creams at an earlier age, which is an advantage for the brands. They are also more responsible about their diets.

Russian women love all natural, and almost everyone has a recipe for her grandma’s homemade cream. The market players agree that in contrast to mass-market cosmet-ics consumers, the fans of organic pro ducts managed to preserve their buying power and did not search for cheaper stuff. For example, the skin pro ducts of Weleda leading organic brand had the same sales dynamics

as before. The organic pro ducts are gradually loosing the privilege edge of the capital becoming a frequent preference of regional people.

In addition to combat the signs of aging today its main problem many women find it rough, earthy tone. Fatigue, stress, bad weather – are not the best way affects the colour of the face. Also, many women are concerned about the appearance of age spots.

Overall, cosmeceuticals are the most promising category in the segment. An aging population concerned with holding onto their youth is an important task. Experts note the trend toward higher priced formulae as a most effective solu-tion for the skin. Consumers pre-fer to buy more targeted pro ducts when looking for anti-aging ben-efits, and brands offer them wide range of pro ducts to satisfy their demands.

4. KEY PLAYERSL’Oréal keeps the key position

in the segment with 14% of mar-ket share and compete with oth-ers multinational corporations such as Unilever, Proc ter&Gam-ble, Beiersdorf and direct sales. L’Oréal is a leader in moisturisers and anti-acne segments while Uni-lever takes a first position in anti-age thanks to Cherny Zhemchug brand and follows Avon in masks segment with its Sto Retseptov Krasoty brand.

Over strong competition in the segment local companies make an effort to compete with the multina-tional giants. The majority of local manufacturers are increasing their value sales annually and can eas-ily compete with their multinational counterparts. In this way, Russian brands entered into more sophis-ticated pro ducts categories, which was not a core category for national companies.

6 FACE CARE

MORE ON WWW.INTERCHARM.RU/EN

5. DISTRIBUTIONAs far as the distribution chan-

nels for facial care pro ducts are concerned, the specialized shops re-main predominant, however the best sales dynamics are seen in pharma-cies, despite the fact that the aver-age rate of surcharge collected at pharmacies might be higher than in other distribution channels.

Pharmacies demonstrate a sus-tainable growth are seen as a most promising distribution channel for cosmetics with a 10% share of facial and hair care pro ducts in their port-folio.

6. FORECASTAccording to Euromonitor, Rus-

sian consumers are expected to continue to seek quality at reason-able prices. They study pro duct ingredients and make rational purchasing choices on this basis. Over the forecast period consum-ers are expected to choose pro-ducts with natural ingredients, which are offered by local compa-nies at attractive prices, with Rus-sian pro ducts gaining trust from consumers.

Further penetration of pro fes sio-nal and Korean brands is expected in the premium segment. Consum-ers using premium facial care pro-ducts are not expected to shift to mass pro ducts, due to facial care being the last pro ducts Russian women would economise on.

Consumers are expected to be-come more interested in socially-responsible brands. Beiersdorf, for example, ran a campaign to sup-port the reconstruction of children’s skating rinks in 2015.

The economic situation positively influenced the development of local mass brands, thanks to consumers’ price sensitivity, good quality pro-ducts and patriotic moods. Local manufacturers are expected to fol-low premium brands in terms of new pro duct launches and develop their own pro ducts at affordable prices.

Market Sizes | Historical/Forecast | Retail Value RSP | RUB bn | Constant 2015 Prices

Geographies Categories 2013 2014 2015 2016 (forecast)

Russia Anti-Agers 33,00 31,80 35,40 32,40

© Euromonitor International

Brand Shares Ranking (Global - Historical Owner) | Historical | Retail Value RSPGeographies Categories Brand Company name (GBO) 2015

Russia Face Masks Avon Planet Spa Avon Products Inc 1

Russia Face Masks Oriflame Pure Nature Oriflame Cosmetics SA 2

Russia Face Masks Sto Retseptov Krasoty Unilever Group 3

Russia Face Masks Garnier Skin Naturals L'Oréal Groupe 4

Russia Face Masks Domashnie Retsepty Pervoe Reshenie OOO 5

© Euromonitor International

Динамика продаж увлажняющих средств, в млрд рублейКатегория 2013 2014 2015 2016 (forecast)

Увлажнители 32,20 30,90 33,80 32,80

© Euromonitor International

MAKE-UP 7

MORE ON WWW.INTERCHARM.RU/EN

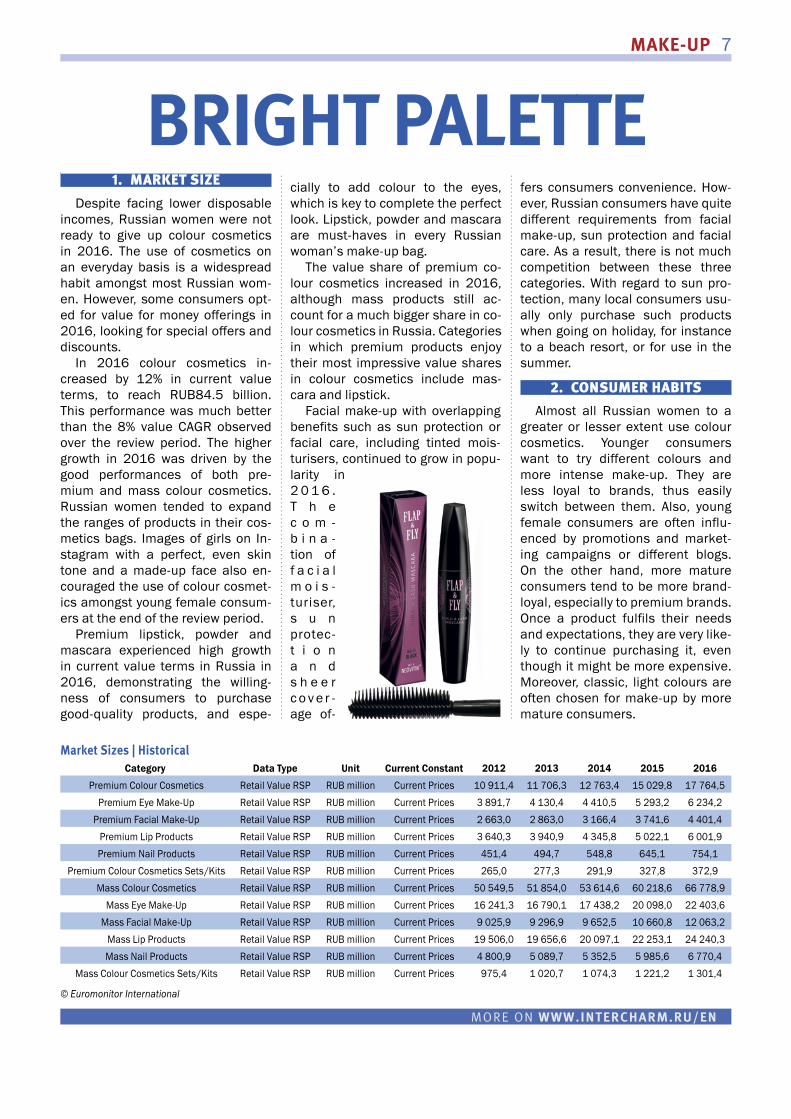

1. MARKET SIZEDespite facing lower disposable

incomes, Russian women were not ready to give up colour cosmetics in 2016. The use of cosmetics on an everyday basis is a widespread habit amongst most Russian wom-en. However, some consumers opt-ed for value for money offerings in 2016, looking for special offers and discounts.

In 2016 colour cosmetics in-creased by 12% in current value terms, to reach RUB84.5 billion. This performance was much better than the 8% value CAGR observed over the review period. The higher growth in 2016 was driven by the good performances of both pre-mium and mass colour cosmetics. Russian women tended to expand the ranges of pro ducts in their cos-metics bags. Images of girls on In-stagram with a perfect, even skin tone and a made-up face also en-couraged the use of colour cosmet-ics amongst young female consum-ers at the end of the review period.

Premium lipstick, powder and mascara experienced high growth in current value terms in Russia in 2016, demonstrating the willing-ness of consumers to purchase good-quality pro ducts, and espe-

cially to add colour to the eyes, which is key to complete the perfect look. Lipstick, powder and mascara are must-haves in every Russian woman’s make-up bag.

The value share of premium co-lour cosmetics increased in 2016, although mass pro ducts still ac-count for a much bigger share in co-lour cosmetics in Russia. Categories in which premium pro ducts enjoy their most impressive value shares in colour cosmetics include mas-cara and lipstick.

Facial make-up with overlapping benefits such as sun protection or facial care, including tinted mois-turisers, continued to grow in popu-larity in 2 0 1 6 . T h e c o m -b i n a -tion of f a c i a l m o i s -turiser, s u n protec-t i o n a n d s h e e r c o v e r -age of-

fers consumers convenience. How-ever, Russian consumers have quite different requirements from facial make-up, sun protection and facial care. As a result, there is not much competition between these three categories. With regard to sun pro-tection, many local consumers usu-ally only purchase such pro ducts when going on holiday, for instance to a beach resort, or for use in the summer.

2. CONSUMER HABITSAlmost all Russian women to a

greater or lesser extent use colour cosmetics. Younger consumers want to try different colours and more intense make-up. They are less loyal to brands, thus easily switch between them. Also, young female consumers are often influ-enced by promotions and market-ing campaigns or different blogs. On the other hand, more mature consumers tend to be more brand-loyal, especially to premium brands. Once a pro duct fulfils their needs and expectations, they are very like-ly to continue purchasing it, even though it might be more expensive. Moreover, classic, light colours are often chosen for make-up by more mature consumers.

BRIGHT PALETTE

Market Sizes | HistoricalCategory Data Type Unit Current Constant 2012 2013 2014 2015 2016

Premium Colour Cosmetics Retail Value RSP RUB million Current Prices 10 911,4 11 706,3 12 763,4 15 029,8 17 764,5

Premium Eye Make-Up Retail Value RSP RUB million Current Prices 3 891,7 4 130,4 4 410,5 5 293,2 6 234,2

Premium Facial Make-Up Retail Value RSP RUB million Current Prices 2 663,0 2 863,0 3 166,4 3 741,6 4 401,4

Premium Lip Pro ducts Retail Value RSP RUB million Current Prices 3 640,3 3 940,9 4 345,8 5 022,1 6 001,9

Premium Nail Pro ducts Retail Value RSP RUB million Current Prices 451,4 494,7 548,8 645,1 754,1

Premium Colour Cosmetics Sets/Kits Retail Value RSP RUB million Current Prices 265,0 277,3 291,9 327,8 372,9

Mass Colour Cosmetics Retail Value RSP RUB million Current Prices 50 549,5 51 854,0 53 614,6 60 218,6 66 778,9

Mass Eye Make-Up Retail Value RSP RUB million Current Prices 16 241,3 16 790,1 17 438,2 20 098,0 22 403,6

Mass Facial Make-Up Retail Value RSP RUB million Current Prices 9 025,9 9 296,9 9 652,5 10 660,8 12 063,2

Mass Lip Pro ducts Retail Value RSP RUB million Current Prices 19 506,0 19 656,6 20 097,1 22 253,1 24 240,3

Mass Nail Pro ducts Retail Value RSP RUB million Current Prices 4 800,9 5 089,7 5 352,5 5 985,6 6 770,4

Mass Colour Cosmetics Sets/Kits Retail Value RSP RUB million Current Prices 975,4 1 020,7 1 074,3 1 221,2 1 301,4

© Euromonitor International

8 MAKE-UP

MORE ON WWW.INTERCHARM.RU/EN

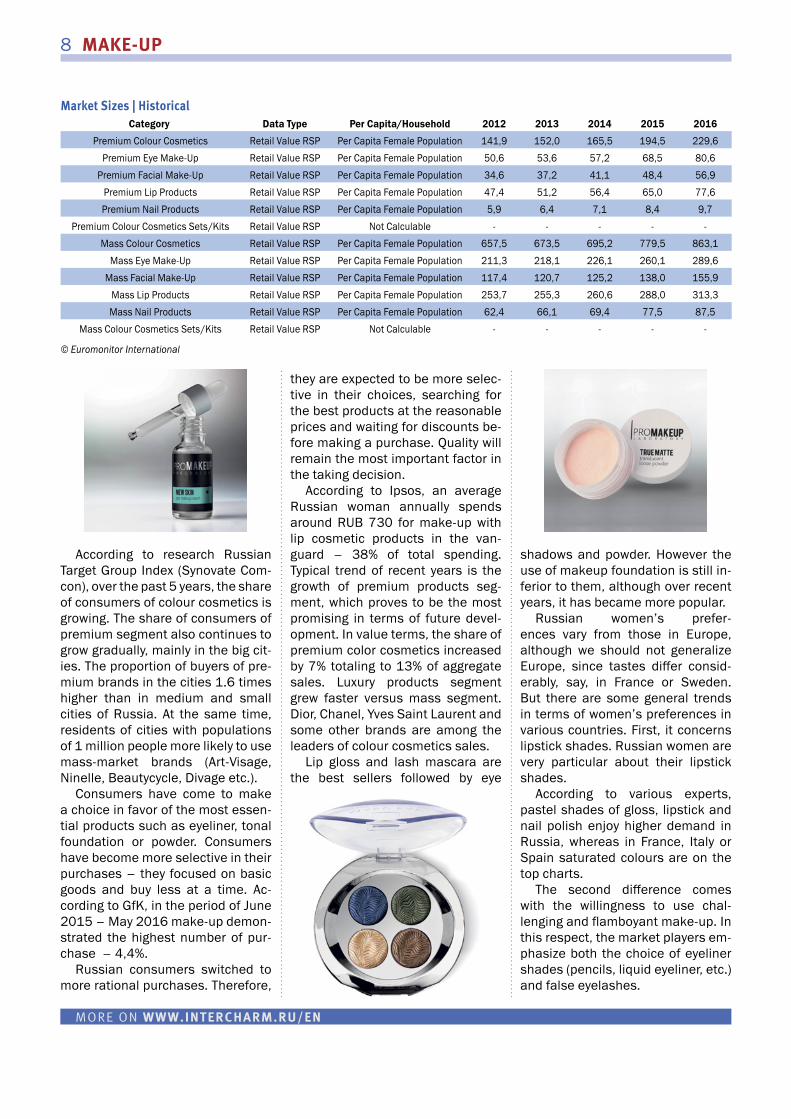

According to research Russian Target Group Index (Synovate Com-con), over the past 5 years, the share of consumers of colour cosmetics is growing. The share of consumers of premium segment also continues to grow gradually, mainly in the big cit-ies. The proportion of buyers of pre-mium brands in the cities 1.6 times higher than in medium and small cities of Russia. At the same time, residents of cities with populations of 1 million people more likely to use mass-market brands (Art-Visage, Ninelle, Beautycycle, Divage etc.).

Consumers have come to make a choice in favor of the most essen-tial pro ducts such as eyeliner, tonal foundation or powder. Consumers have become more selective in their purchases – they focused on basic goods and buy less at a time. Ac-cording to GfK, in the period of June 2015 – May 2016 make-up demon-strated the highest number of pur-chase – 4,4%.

Russian consumers switched to more rational purchases. Therefore,

they are expected to be more selec-tive in their choices, searching for the best pro ducts at the reasonable prices and waiting for discounts be-fore making a purchase. Quality will remain the most important factor in the taking decision.

According to Ipsos, an average Russian woman annually spends around RUB 730 for make-up with lip cosmetic pro ducts in the van-guard – 38% of total spending. Typical trend of recent years is the growth of premium pro ducts seg-ment, which proves to be the most promising in terms of future devel-opment. In value terms, the share of premium color cosmetics increased by 7% totaling to 13% of aggregate sales. Luxury pro ducts segment grew faster versus mass segment. Dior, Chanel, Yves Saint Laurent and some other brands are among the leaders of colour cosmetics sales.

Lip gloss and lash mascara are the best sellers followed by eye

shadows and powder. However the use of makeup foundation is still in-ferior to them, although over recent years, it has became more popular.

Russian women’s prefer-ences vary from those in Europe, although we should not generalize Europe, since tastes differ consid-erably, say, in France or Sweden. But there are some general trends in terms of women’s preferences in various countries. First, it concerns lipstick shades. Russian women are very particular about their lipstick shades.

According to various experts, pastel shades of gloss, lipstick and nail polish enjoy higher demand in Russia, whereas in France, Italy or Spain saturated colours are on the top charts.

The second difference comes with the willingness to use chal-lenging and flamboyant make-up. In this respect, the market players em-phasize both the choice of eyeliner shades (pencils, liquid eyeliner, etc.) and false eyelashes.

Market Sizes | HistoricalCategory Data Type Per Capita/Household 2012 2013 2014 2015 2016

Premium Colour Cosmetics Retail Value RSP Per Capita Female Population 141,9 152,0 165,5 194,5 229,6

Premium Eye Make-Up Retail Value RSP Per Capita Female Population 50,6 53,6 57,2 68,5 80,6

Premium Facial Make-Up Retail Value RSP Per Capita Female Population 34,6 37,2 41,1 48,4 56,9

Premium Lip Pro ducts Retail Value RSP Per Capita Female Population 47,4 51,2 56,4 65,0 77,6

Premium Nail Pro ducts Retail Value RSP Per Capita Female Population 5,9 6,4 7,1 8,4 9,7

Premium Colour Cosmetics Sets/Kits Retail Value RSP Not Calculable - - - - -

Mass Colour Cosmetics Retail Value RSP Per Capita Female Population 657,5 673,5 695,2 779,5 863,1

Mass Eye Make-Up Retail Value RSP Per Capita Female Population 211,3 218,1 226,1 260,1 289,6

Mass Facial Make-Up Retail Value RSP Per Capita Female Population 117,4 120,7 125,2 138,0 155,9

Mass Lip Pro ducts Retail Value RSP Per Capita Female Population 253,7 255,3 260,6 288,0 313,3

Mass Nail Pro ducts Retail Value RSP Per Capita Female Population 62,4 66,1 69,4 77,5 87,5

Mass Colour Cosmetics Sets/Kits Retail Value RSP Not Calculable - - - - -

© Euromonitor International

MAKE-UP 9

MORE ON WWW.INTERCHARM.RU/EN

3. KEY PLAYERSColour cosmetics in Russia con-

tinued to be led by the multinational company L’Oréal Russia in 2016. The company constantly increases both its value sales and its value share. Throughout its presence in Russia, L’Oréal Russia has built a strong image as well as the loyalty of its customers. It strengthened its leading position due to offering a wide portfolio of brands within the various price ranges, develop-ing its distribution and new pro duct launches supported by strong pro-motional activities.

National producers such as Art-Visage, Divage and some others are worthy competitors with the volume of Russian-made colour cosmetics.

4. DISTRIBUTIONDistribution of colour cosmet-

ics is developing on the back of ex-panding drogerie chains. Retailers seek to reach more customers by virtue of loyalty programs including discount cards, various promos and expanded online stores so as to fa-cilitate consumers’ choice and price comparison as well as to find the best deals.

Over half of consumers buy cos-metics in specialized perfumery and cosmetics chains, 31.3 % – in su-per/hypermarkets, 23.8% prefer di-rect sales and 11.2 % visit drogeries.

5. TRENDSThe freshest ideas in colour cos-

metics came from Asia, especially

Korea – the leading international colour cosmetics brands adopted these ideas and ingredients to meet their regular consumers’ needs. Thus, “cushion” pro ducts was a trend in foundation and powder pro-ducts in 2015.

Premiumization trend is seen as the most prominent in the market of colour cosmetics. Sometime ago, the “demonstrational consumption” was a kind of premiumization driv-er, but today people need high and guaranteed quality. Nevertheless, the evident rational consumption forces some women to buy pro ducts in more democratic price category provided they satisfy their quality needs.

Multifunctional pro ducts such as creams with moisturizing, sun-screen and anti-aging effects, deco-rative face care “3 in 1” (base, tint-ing cream and powder), lipstick or lip gloss to moisturize lips, etc. are winning popularity.

Dramatic eyes have long been a big beauty trend in Russia, and now 3D extreme eyelashes are all the rage. They’re a super soft, very light-weight synthetic fiber that doesn’t weigh the follicle down as much as mink or other natural hairs, so a ‘bouquet’ can be applied to each natural lash, fanning it out with up to a 6:1 volume ratio instead of the more typical 1:1.

Russian women traditionally pay much attention to their appearance and buy a lot of colour cosmetics pro ducts. However, they became more rational in their purchasing choices and focused on multifunc-tional pro ducts.

Not only mass brands offered multifunctional pro ducts – premi-um brands also offered hybrid pro-ducts, such as concealer plus foun-dation. For example, La Prairie SpA launched Skin Caviar Concealer-Foundation SPF 15.

Colour cosmetics with sun pro-tection gradually increased in pop-ularity, in foundation/concealer pro ducts mostly. Colour cosmet-ics with sun protection became a trend not only in the premium seg-ment, however, but spilled over to the mass segment, with producers increasingly introducing new pro-ducts. For example, Bourjois SA launched Bourjois City Radiance foundation with SPF 30 in January 2016.

6. FORECASTConsumers are expected to be

more rational in purchasing choic-es – make one pro duct purchase at a time and pay much attention to discounts and promotional of-fers. At the same time, premium colour cosmetics is expected to slight-ly outperform the mass segment, with consumers being at-tached to affordable luxuries.

BB/CC creams is expected to reg-ister the stron-gest retail value compound annual growth rate (CAGR) of 1% (constant 2015 prices) over the next 5 years, driven by con-sumers’ interest in multifunc-tional pro ducts and new formats, e.g. cushions.

Mass brands are expected to follow premium pro duct launches, with new launches an effective tool for development, as Russians like to try new pro ducts within colour cosmetics. Therefore, new pro ducts will be an essential part of the de-velopment of companies in the country.

10 HAIR CARE

MORE ON WWW.INTERCHARM.RU/EN

RIGHT UP THERE1. MARKET SIZE

According to Euromonitor Inter-national, the Russian market of hair care pro ducts in 2016 was 91 470 million rubles. Consumers pur-chased pro fes sio nal hair care pro-ducts because they believe that it will affect better. The Russians think of the hair health and realize the need to invest in a complex and ef-fective care.

Among the commodity groups of the category the largest share of the Russian market in 2016, was hair pro ducts (25.7% in value terms), ac-cording to Nielsen. Sales still show a negative trend, however, has slowed the fall: whereas in the 2015 com-pare to 2014 fell by 6.8%, in 2016 by only 3%.

To look for new avenues for growth, manufacturers continued to focus on pro duct segmentation, concentrating on various aspects of hair care, such as hair thickening and scalp health.

Regarding conditioners by type, rinse-out pro ducts continued to out-perform leave-in pro ducts in 2016.

Natural and organic ingredients are favoured by Russian consum-ers, due to their lack of side-effects. As such, silicone-, paraben- and SLS- (Sodium Laureth Sulphate) free hair care pro ducts have been well-received by consumers, and are likely to continue to be the focus of new pro duct development over the forecast period.

Hair loss treatments registered a static performance in current value terms in 2016.

Dry shampoo remained a niche pro duct in Russia at the end of re-view period.

Mass hair care led overall hair care in Russia in 2016, with a 90% value share. Mass hair care pro-ducts and brands are usually cheap-er than imported or international offerings, and therefore demand for

mass hair care pro ducts will contin-ue, as these pro ducts are often good quality and thus offer good value for money.

Salon hair care saw the best performance within hair in 2016, growing by 11% in current value terms. The rising number of people looking for at-home hair and beau-ty treatments benefited hair care in 2016. Hair care manufacturers continued to diversify their ranges, launching new pro ducts which al-lowed consumers to carry out po-tentially complicated hair care tech-niques which are popular in hair salons themselves at home.

2. CONSUMER HABITSHome-made hair masks and af-

ter-shampoo rinses were still very popular amongst Russian consum-

ers at the end of the review period, say Euromonitor International. There are various recipes that Rus-sians, mainly women, share on the internet. Amongst the most popu-lar pro ducts used as ingredients in home-made masks are honey, eggs, oils, mustard and pepper. They are used to nourish and accelerate hair growth. Home-made masks and rinses are considered to be more natural and healthy than pro ducts purchased in stores.

Usually, the majority of Russians use one or two pro ducts in their hair care routine. However, younger con-sumers, particularly women, include multiple steps in their hair care rou-tines, including shampoos, condi-tioners and more specific pro ducts such as combing creams, treatment masks and styling agents.

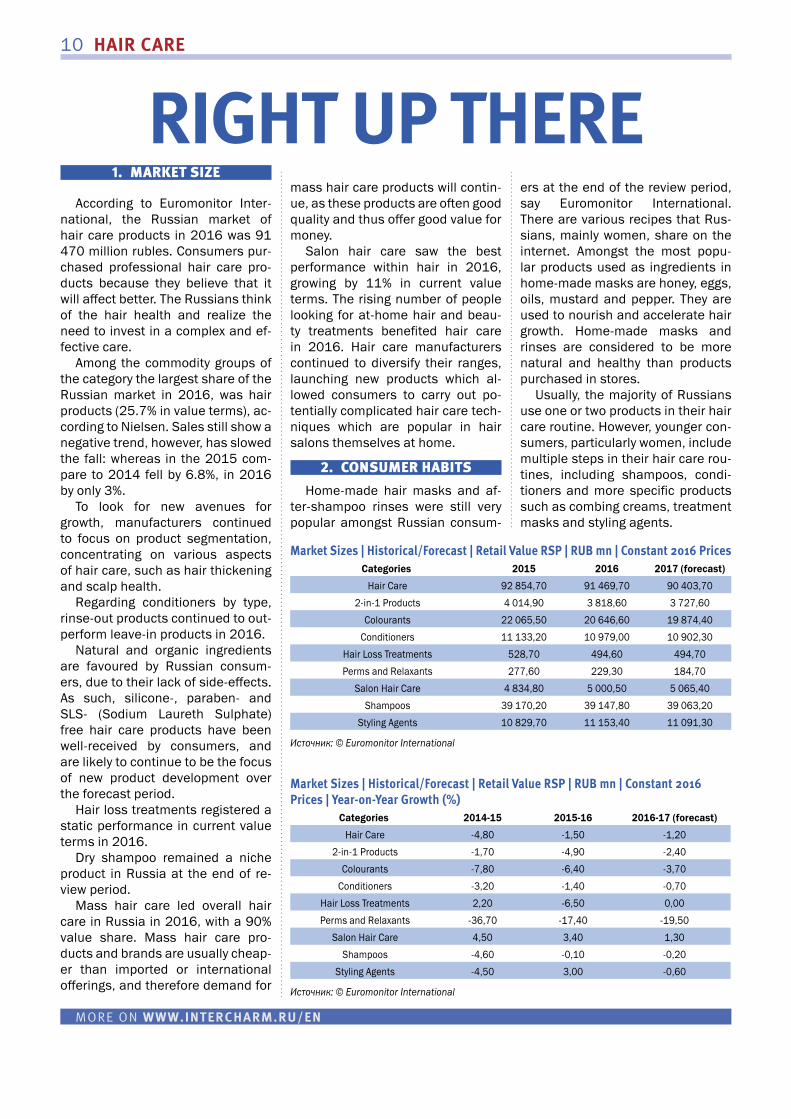

Market Sizes | Historical/Forecast | Retail Value RSP | RUB mn | Constant 2016 PricesCategories 2015 2016 2017 (forecast)

Hair Care 92 854,70 91 469,70 90 403,70

2-in-1 Pro ducts 4 014,90 3 818,60 3 727,60

Colourants 22 065,50 20 646,60 19 874,40

Conditioners 11 133,20 10 979,00 10 902,30

Hair Loss Treatments 528,70 494,60 494,70

Perms and Relaxants 277,60 229,30 184,70

Salon Hair Care 4 834,80 5 000,50 5 065,40

Shampoos 39 170,20 39 147,80 39 063,20

Styling Agents 10 829,70 11 153,40 11 091,30

Источник: © Euromonitor International

Market Sizes | Historical/Forecast | Retail Value RSP | RUB mn | Constant 2016 Prices | Year-on-Year Growth (%)

Categories 2014-15 2015-16 2016-17 (forecast)

Hair Care -4,80 -1,50 -1,20

2-in-1 Pro ducts -1,70 -4,90 -2,40

Colourants -7,80 -6,40 -3,70

Conditioners -3,20 -1,40 -0,70

Hair Loss Treatments 2,20 -6,50 0,00

Perms and Relaxants -36,70 -17,40 -19,50

Salon Hair Care 4,50 3,40 1,30

Shampoos -4,60 -0,10 -0,20

Styling Agents -4,50 3,00 -0,60

Источник: © Euromonitor International

HAIR CARE 11

MORE ON WWW.INTERCHARM.RU/EN

Regarding styling agents, hair-spray/lacquer remained the most popular format in Russia at the end of the review period. Consumers usually consider this type of pro duct to be easy and fast to use.

Perms are not very common amongst Russian consumers any longer. However, those who still have them usually prefer to have them done at a hair salon, rather than try-ing to do it themselves at home.

The main category in hair care is shampoo followed by hair condi-tioner or balm rinse. Every second woman in Russia uses hair dyes. Preference is given to well-known brands of multinational companies: Schwarzkopf, Garnier, Wella, L’Oréal.

Last year the experts noted the growing popularity of hair masks. This trend continued in 2017. Other pro ducts such as shampoos with oils and natural extracts strongly compete with the masks – every third Russian woman select green hair care.

The current economic situation affects the consumer who tends to choose a quality pro duct at an at-tractive price. Therefore the pro duct quality and price are the main crite-ria for a consumer.

The following consumer proper-ties contribute to the stable demand for hair care: attractive package and marking, colour, scent, texture, designation, treatment properties, comfort, as well as optimal value for money of these pro ducts. All above meantioned properties that create an additional stimulus for purchase stabilize the demand, increase the number of trial purchases and popu-larity rating.

Pro ducts for different types of hair colours and lengths such as

oils, shampoos with natural ingredi-ents become more popular. Ammo-nia free hair dye is one example of high-demand pro ducts.

Hair dyes for home use positioned as a pro fes sio nal strengthen its po-sition. Another trend is a strong de-mand for cream colorants with a re-sistant effect.

Sales of natural dyes and or-ganic brands demonstrate constant growth. Consumer concerned about some problems such as hair loss, dandruff, dull, etc., looking for less harmful pro ducts.

Strengthening and stimulation of hair growth is one of the “hot” topic. That is why the pro ducts are designed to solve these problems, show a dynamic growth in sales and will be in demand in the future.

According to Ipsos data, top-de-mand hair care pro ducts are sham-poos, balms and hair masks. The most popular brands of shampoos and conditioners are Head & Shoul-ders, Schauma, Chistaya Liniya, Nivea and Pantene. The most popu-lar brands of hair dyes are Palette, Garnier, Estel.

3. KEY PLAYERSAccording to Euromonitor,

Schwarzkopf & Henkel led hair care with a value share of 24% in 2016, to reach RUB21.9 billion. Its success was supported by solid brands such as Schauma, Syoss, Gliss/Gliss Kur and various brands of colourants. Schwarzkopf & Henkel was followed by L’Oréal Russia, with a value share of 16%.

The seg-ment of hair care pro ducts is one of the few where do-mestic manu-

Company Shares (National – Latest Owner) | Historical | Retail Value RSP | % breakdown

Categories Companies 2016

Hair Care Schwarzkopf & Henkel ZAO 23,90

Hair Care L'Oréal Russia 16,40

Hair Care Proc ter & Gam ble OOO 8,00

Hair Care Kalina Concern OAO 5,40

Hair Care Avon Pro ducts ZAO 3,00

Источник: © Euromonitor International

Brand Shares (Local – Latest Owner) | Historical | Retail Value RSP | % breakdownCategories Brand (GBO) Company name (NBO) 2016

Hair Care Schauma (Henkel AG & Co KGaA) Schwarzkopf & Henkel ZAO 4,50

Hair Care Chistaya Liniya (Unilever Group) Kalina Concern OAO 4,00

Hair Care Head & Shoulders (Proc ter & Gam ble Co, The) Proc ter & Gam ble OOO 3,80

Hair Care Schwarzkopf Palette (Henkel AG & Co KGaA) Schwarzkopf & Henkel ZAO 3,70

Hair Care Garnier Fructis (L'Oréal Groupe) L'Oréal Russia 3,70

Источник: © Euromonitor International

12 HAIR CARE

MORE ON WWW.INTERCHARM.RU/EN

facturers compete with up to multi-national companies. So, in the top of local manufacturers of hair care is a Russian company Vertex with its hair loss treatment pro duct Al-erana.

4. DISTRIBUTIONAs Discovery Research Group

states, the main retail channels for hair care in Russia are super and hypermarkets that followed by per-fumery and cosmetics chains. Spe-cialized stores are likely for premi-um pro ducts with its 5% of market share.

In recent years there has been an interesting trend – on the one hand, the clear positioning of pro-ducts in retail, based on their price, on the other – the desire to introduce brands to the maximum num-ber of channels. The exception is only premium and salon brands that can be found more often in specialized shops for hairdressers.

Specialized pro-ducts such as treat-ment shampoos and masks are pur-chased in pharma-cies, and for organic brands the key chan-nels are bio stores and the Internet.

5. TRENDSThere was a growing trend to-

wards pro fes sio nal hair care – the preservation of the quality of the hair during colouring and highlight-ing. This trend affected both salon hair care and colourants.

In addition to the overall promo-tion of healthy lifestyles the major trend in hair care is increasing in-terest in natural pro ducts. The con-sumer pays more attention to the ingredients and the quality.

The main trend: positioning and repositioning of brands as pro fes-sio nal, but affordable in terms of prices and salon level for home hair care. Consumers are interested in these pro ducts and are prepared to

pay more so as to get an effective care without visiting beauty salons. Large companies are aggressively developing portfolios of well-known consumer brands and invest in new pro ducts together with necessary marketing support.

6. FORECASTHair care is expected to recover

during the forecast period 2016-2021, with a negligible value CAGR at constant 2016 prices. Speciali-sation and innovation are expected to be the key trends over the fore-cast period. There are opportuni-ties for the further penetration of premium brands in hair care in Russia.

Significant chang-es in the competi-tive landscape in hair care are not expected in Russia over the forecast pe-riod. Nonetheless, the competition is expected to remain fierce.

The forecast pe-riod promises to be very encouraging in terms of the launch of new pro ducts with a higher than aver-age unit price, due to the very favour-able economic out-look in relation to the review period.

BODY CARE 13

MORE ON WWW.INTERCHARM.RU/EN

14 BODY CARE

MORE ON WWW.INTERCHARM.RU/EN

PILE ON POUNDS1. MARKET SIZE

Russian body care demonstrated positive results in 2016 – 7.5%, the value of the market reached 124246,7 mln Rub 10619 mn Rub (app. 1800 mm euro). According to Nielsen, the growth of the segment was 3.2% in volume compare to the previous year. Firming pro ducts were doing well showed a tiny de-crease for 0.10%.

General purpose pro duct such as light texture cosmetics for body care have been dominating the Rus-sian market for several years, in-cluding milks or lotions that are top demand. Body creams and scrubs occupy the second place in terms of popularity with gentle peelings and gel texture exfoliates in the van-guard. Body care is a smaller than a facial care and has a more seasonal character, specially when we mean anti-cellulite and firming pro ducts that are on a high demand are in spring and summer months.

2. CONSUMER HABITSIt is evident that consumers have

reduced spending on pro ducts that they consider unnecessary for ev-

eryday and regular use, notably body firming and anti-cellulite pro ducts.

Another factor affecting consum-er spending habits was price, which especially impact on the anti-ageing and skin-protective category. On the other hand, there is a group of pro-ducts that consumers do feel are necessary and are willing to spend money on, such as moisturizers. Ac-cording to experts, the budget real-location trend persists, whereby the shoppers prefer to spend moderate-ly on the pro ducts that are outside the essential range, for example, anti-cellulite or skin firming. Con-sumers wanted to buy higher-qual-ity brands at reasonable prices, and therefore started to educate them-selves about ingredients and pro-ducts. Increasing interest in Korean brands was observed in bady care as in facial care.

Interesting that inspite of Rus-sian women obsession about body shape they prefer to buy lotions and creams more than special aimed pro ducts and spend on pur-chase general purpose pro ducts three times more than anti-cellulite creams.

It is expected that many of the consumers who switched to lower-priced pro ducts at the end of this period may continue to use lower-priced pro ducts from domestic or Byelorussian manufacturers, as the quality of these pro ducts is high, and may satisfy consumers. The ex-pansion of lower-priced brands is expected to continue at the begin-ning of the forecast period, which will drag the development of the cat-egory.

Along with increasing concerns about appearance, more Russian women are looking for pro fes sio nal solutions for solving particular prob-lems. Consumers are more often choosing special services for their body care. Anti-ageing procedures

Market Sizes | HistoricalCategory Data Type Unit Current Constant 2012 2013 2014 2015 2016

Skin Care Retail Value RSP RUB million Current Prices 87 152,0 88 867,3 91 876,7 111 112,3 124 246,7

Body Care Retail Value RSP RUB million Current Prices 12 039,9 12 006,3 11 988,9 13 276,3 14 278,0

Facial Care Retail Value RSP RUB million Current Prices 65 459,1 66 879,0 69 429,6 86 001,1 97 086,8

Hand Care Retail Value RSP RUB million Current Prices 5 518,4 5 655,0 5 903,9 6 786,2 7 428,9

Skin Care Sets/Kits Retail Value RSP RUB million Current Prices 4 134,7 4 327,0 4 554,3 5 048,7 5 452,9

© Euromonitor International

Market Sizes | Historical | Year-on-year growth (%)Category Data Type Unit Current Constant 2012–13 2013–14 2014–15 2015–16

Skin Care Retail Value RSP RUB million Current Prices 2,0 3,4 20,9 11,8

Body Care Retail Value RSP RUB million Current Prices -0,3 -0,1 10,7 7,5

Facial Care Retail Value RSP RUB million Current Prices 2,2 3,8 23,9 12,9

Hand Care Retail Value RSP RUB million Current Prices 2,5 4,4 14,9 9,5

Skin Care Sets/Kits Retail Value RSP RUB million Current Prices 4,7 5,3 10,9 8,0

© Euromonitor International

BODY CARE 15

MORE ON WWW.INTERCHARM.RU/EN

remain one of the most p o p u l a r within the high range of services that were on offer. Sales of p ro fes s io -

nal cosmetics to beauty salons may become an increasingly important niche area.

3. KEY PLAYERSAccording to Euromonitor, multi-

national companies remain the ma-jor players in the body care market. L’Oréal, a permanent market leader, which was offering a wide range of pro ducts in the mass and premium segments, still led the segment in 2016. The majority of the company’s brands were present across most modern retailing channels, and the rapid development of beauty spe-cialist retailers, hypermarkets and other channels directly supported the sales of the company.

In the market of body care are actively developing Russian compa-nies – Pervoye Reshenie, Magrav, Fratti NV, Floresan. Russian compa-nies are constantly updating their pro duct offerings, introduce new technologies, develop new catego-

ries, in particular, the seg-ment of natural and organic cosmetics. Pervoye Resh-esnie is one of the most powerful players, and other companies try to follow their experience. The company pro duct range features sev-eral lines of care positioned as organic, and even certi-fied by relevant standards.

4. DISTRIBUTIONBody care presented in all retail

formats. For the premium pro ducts specialized stores and pharmacies are more preferable while for mass market the main channels are su-permarkets and drogeries.

The Russian consumers of body care are addicted to their favourite cosmetics channels. Most of them buy body care pro ducts at special-ized stores, followed by direct sales companies, supermarkets or phar-macies. Super- and hypermarkets welcome many domectics brand that developed thier ranges and offer quite sophisticated lined at a reasonable prices.

5. TRENDSOne of the key trends in body care

is an increasing demand for natural pro ducts. Organic brands are ex-panding the range and produce dif-ferent oils and cosmetics with a light texture.

Another trend is an increasing interest in the Korean brands that offer unique pro ducts with rare and exotic ingredients, such as the snail secretion filtrate, soy extracts, and white truffles.

The niche Russian brands are gaining the moment and launch new pro ducts with natural ingredi-ents and in simple and remarkable packaging.

Another trend is advanced skin hydration technologies. Modern cosmetics have active ingredients that are capable of regulating the natural process of hydration, thus keeping the skin moisturized for a long time (from 24 hours to 7 days).

Cosmetic market is literally go-ing through ‘oil boom’: especially popular dry oil having both caring nourishing properties and is quickly absorbed texture.

Consumers started to read differ-ent webpages, social networks such as Instagram, Facebook and VKon-takte, and watched educational vid-eos from popular Russian bloggers, who accounted for half a million subscribers and were very powerful in terms of not only their reviews of pro ducts, but also in terms of mar-keting.

6. FORECASTFurther expansion of lower-priced

pro ducts is expected to be seen in the mass segment over the forecast period. The leading manufacturers are expected to focus more on value for money pro ducts offering the mar-ket cheaper yet attractive packaging and pro duct lines. Further segmen-tation of consumers according to type is expected if manufacturers manage to find significant differ-ences between variety of skin ages and types of skin, and manage to communicate to the market the ne-cessity of treating them accordingly. consumers are expected to choose pro ducts with natural ingredi-ents, which are offered by local companies at attractive pric-es, with Rus-sian pro ducts gaining trust from consu-mers.

16 BATH CARE

MORE ON WWW.INTERCHARM.RU/EN

1. MARKET SIZE

According to Nielsen, in 2016 the share of Russian bath care was 22% in terms of value. By pro duct category the segment is divided into six categories: bar soaps, bath addi-tives, shower gels, intimate hygiene, liquid soap and talcum powder. The sales of bath care grew up 3.2% in volume and 10.7% in value.

All key players note the positive results. The volume of sales in Lush company grew 13% in 2016. Fresh Spa by Natura Siberica jumped up to 30% this year.

The highest rate of market growth of bath and shower is observed in the category of intimate hygiene. Shower gels occupy a leading posi-tion in bath care in terms of sales thanks to direct sales companies.

Dynamics of liquid soap market is still positive, it is one of the fast-est growing segments of the market. The category is still far from satura-tion. The long-term trend indicates no decline in pro duction, as experts say that the current growth of liquid soap is associated with the effect of import substitution.

Dynamics of pro duction of liquid soap in value reflects the dynamics of pro duction in volume terms, while

having a more pronounced growth. Thus, in the first quarter of 2016 the volume of pro duction in terms of value was at 107% above the same period last year.

The largest volume of pro duction accounted for the Central Federal District: in the first quarter of 2016 there were produced 2932 tons of liquid soap that is 36% of the to-tal volume. In second place with a share of 25% was the Volga Federal District. In third place –Siberian Federal District with 21%. Together, the federal district data accounted for 82% of the Russian pro duction volume in the 1st quarter of 2016.

Bath and shower premium pro-ducts, as well as premium segment on the whole, are gaining demand especially in large cities, where premium cosmetics and perfumery chains are relatively well developed and residents have enough money to spend on premium brands.

2. CONSUMER HABITSShower gels are the most popular

format used by Russian consum-ers. Fragrance of shower pro ducts is important for over half of consum-ers. Russians are also more likely to seek out cleansing benefits.

In France, just 6% of consumers use bath pro ducts, compared to a high of 18% in the UK and Russia. Frequency of use is also very low at less than twice a week in most countries, except the UK and Rus-sia, where consumers take a bath on average 2.4 and 2.2 times a week, respectively. Liquids are the most common bath additive format, although 1 in 10 Russian consum-ers prefer bath salts or cubes.

Russian consumers are expected to continue to seek quality at rea-sonable prices. They study ingredi-ents and make rational purchasing choices on this basis. Over the fore-cast period consumers are expected to choose pro ducts with natural in-gredients, which are offered by local companies at attractive prices. Con-sumers have a low level of loyalty to brands in bath and shower, and as a result are ready to switch to brands with better promotion and higher discounts.

3. KEY PLAYERSAvon Pro ducts led bath and show-

er with a value share of 9% in 2016. This is because of its wide pro duct range in both body wash/shower gel and bath foam/gel, offering good value for money.

Direct sales players have evident strong footholds in this segment, e.g. Avon, Oriflame, as well as Rus-sian company Faberlic.

Unlike other categories, bath and shower in Russia is quite fragment-ed due to many international and domestic companies having a pres-ence.

Domestic manufacturers are producing more and more new pro-ducts in this category.

Manufacturers in mass market segment have adopted the popu-lar concepts of aromatherapy, spa and wellness reflected in pro duct names, dressing and advertising.

BUBBLING AND SPARKLING

BATH CARE 17

MORE ON WWW.INTERCHARM.RU/EN

Obsession of exclusivity, natural-ness and uniqueness of ingredi-ents give a push to the segments of solid soaps, shower gels and bath pro ducts. Among local manufactur-ers are Pervoye Reshenie, Magrav, Nevskaya Kosmetika, Floresan, My-lovarov and Lauren Cosmetic.

4. DISTRIBUTIONThe main retail channels for bath

care in Russia are super and hyper-markets that followed by perfumery and cosmetics chains. As bath care is quite fragmented segment it gives the distributors bug fortune to place the brands in a wide range of retail for-mat – from supermarkets and droger-ies to specialized perfumery and cos-metics chains and organic shops.

Due to the growing competition manufacturers of bath care began to look for new ways to develop their pro ducts. Chains of shops selling natural and organic pro ducts be-come key channels.

Basic pro ducts, shower gels and soap, are the main categories for supermarkets and drogeries, the market share accounts for 40 to 60% according to experts research companies.

5. TRENDSFunctionality and the addition of

beauty benefits are key trends in Europe’s bath and shower market, where the preferred method of per-

sonal cleansing is taking a shower.

Many Russian consum-ers have started to dem-onstrate a shift towards increasingly sophisti-cated domestic brands particularly Faberlic and Natura Siberica.

Fragrance have be-come very influential fac-tor in the personal care industry. The most popu-lar flavours in Russia in-clude lavender, rose and vanilla, fruit flavors, cara-mel and tea.

Over the past year has been experienced sig-nificant growth of sen-sory pro ducts. More and more brands are using fragrances in combination with abstract con-cepts, trying to satisfy the consum-ers demands, using the ingredients and flavors, described as ‘heating’, refreshing and detox.

In view of the outlined trend for organic pro ducts hand made bath care is growing in popularity.

6. FORECASTEuromonitor International, bath

and shower is set to register a val-ue CAGR of 2% at constant 2016 prices, to reach RUB54.3 million in 2021. Despite the generally high level of maturity and competition

within bath and shower in Russia, which will limit future volume growth, manufacturers are still expected to continue cre-ating added-value, thus driving impulse purchas-es, which should support value growth. New pro-duct launches specifical-ly addressing individual needs and a more emo-tional side are expected to contribute to value and volume growth over the forecast period.

The largest contribu-tion to the growth of the segment will make the category shower gels, its average annual growth

rate will be 1% due to increasing hy-giene culture and retail development. Shower gel and soap will demon-strate the largest growth up to 2019.

Experts stress that the growing demand for basic pro ducts will re-main a long-term trend. Consumers are becoming more discerning, sen-sitive to price and promotions. How-ever, small towns in the regions will show better results in sales as the market there is not saturated and interest in the pro ducts of various formats, including non-essential is very high. Therefore, there is expect-ed to increase in sales of foam, salt, bombs and oils.

18 MALE GROOMING

MORE ON WWW.INTERCHARM.RU/EN

1. MARKET SIZE It is clear that the last few years

have seen the male grooming mar-ket drastically increase. The men’s haircare market alone is set to grow by 11% by 2020, with up to 25% of men actively seeking out brands specifically designed for males. This is reflected throughout the personal care industry.

22% of men think it is fashionable to have a beard, and the facial hair trend has picked up serious speed in the last two years. This has impact-ed hugely on the shaving and depila-tory market, with nostalgic and retro shaving pro duct commonly found in stores. It is estimated that over a third of consumers have bought shaving cream, and 41% purchase prestige shaving pro ducts due to the quality of ingredients used.

Russian men have been actively interested in cosmetics and toilet-ries, so this segment is growing sig-nificantly and male grooming is a driver of the Russian market.

Growing interest in premium pro-ducts encourages men to buy luxury cosmetics supposed to be more ef-ficient and able to confirm the social status that men value most.

The experts note the current rise in the cost of men’s deodorant,

which also showed a movement towards premiumization. Premium bath care also show steady growth, and will increase by an average of 1 % over the next five years. More and more Russian men begin to regu-larly use toiletries and cosmetics. At the same time, experts believe that the male cosmetics sales may decline in the near future due to the economic situation.

There was a trend towards beards, which came from Europe. More men started to have beards, which reduced the potential num-ber of consumers; however, this trend influenced launches of new pro ducts designed especially for beards, including balm, oil and spe-cial pro ducts to stimulate growth of beards.

2. CONSUMER HABITSFor the male audience effective-

ness of the pro duct is still more im-portant than fragrance. Russian men annually increase spending on the cosmetics purchase for more than 40 % – about $115 per month – it is twice more than in the US.

Men spend more money on cos-metics. In Russia, 70% of men buy shaving pro ducts, almost the same number use the perfume, 57% –

deodorants, 10% – hand cream. It should also be understood that any male cosmetics on average 20% more expensive than women pro ducts, men are more brand ad-dicted. However, an important consumer of male grooming is still woman. Only 50% of men in Russia are buying cosmetics on their own. The Russian men’s spending on cosmetics of the average wage is approximately 1% per year.

TOP-5 skincare brands are Nivea, Chistaya Liniya, Avon, Oriflame and Clearasil. TOP- 5 perfumery brands: Adidas, Avon, Hugo Boss, Gillette and Oriflame. TOP-5 aftershave brands: Gillette, Nivea, Arko, Old Spice and Arko Men.

According to GfK, as young men actively researching and choosing between different personal care pro ducts, it is essential for manu-facturers to understand how to en-gage with them. Although a large number of men are visiting stores to view pro ducts, in general they are less likely to browse in a store than women. The exceptions to this trend are young men in Russia where 46% browse in a store, compared to 42% of young women.

For manufacturers and retailers targeting those markets, promotion and clear packaging are essential to help young male shoppers choose

BOOMING GROOMING

MALE GROOMING 19

MORE ON WWW.INTERCHARM.RU/EN

between pro ducts when they are in a shop, as well as to encourage im-pulse to buy and to try new pro duct.

When we compare what informa-tion sources young men and women are persuaded by when considering a purchase in the personal care cat-egory, there is a strong bias amongst men towards traditional media, most notably advertising. Men’s opinions are significantly more likely to be shaped by advertising than women in all markets as our results show four in ten (41%) young men versus 29% of young women in Russia.

Google and other Internet search engines play a major part in the re-search phase for young men. In the majority of markets, men aged 16-21 are significantly more likely than women to use search engines: 41% of young men use search engines compared to 29% of young women.

3. KEY PLAYERSThe Russian male grooming seg-

ment is dominated by the key inter-national players like P&G, Gillette, Beiersdorf. Gillette Group led men’s grooming with a value share of 30% in 2016, to reach RUB26.3 billion. The company has a strong hold in men’s grooming due to its out-standing leading position in men’s shaving, the largest category within men’s grooming. The company at-tributes its success to its brand Gillette, the leading brand in men’s

shaving. The company maintained the strong position of its brand by continuously being in line with new trends and launching new pro ducts accompanied by extensive market-ing campaigns. It was followed by Beiersdorf, with a value share of 5%.

Local manufacturers extend their male collections and launch new pro ducts.

St. Petersburg cosmetic company Firma Vita made a rebranding of male grooming line Maitre. The main purpose of the redesign was elimi-nate a brand in a very competitive environment, make it more modern and understandable to the consum-er. The packaging color – black – re-mained unchanged. The new design became discreet and laconic. The numbers on the packaging are not only a decorative element but also the steps of the grooming proce-

dure: a shower, shaving and etc.Black soap for body and hair from

the big local manufacturer Svoboda has innovative formula with a coal can be used as shampoo, shower gel and shaving. Soap forms a thick foam with a pleasant refreshing aroma. It protects the skin, per-fectly softens beard hair, provides easy shaving and absolute comfort throughout the grooming proce-dure.

4. DISTRIBUTIONMen prefer to buy cosmetics and

perfumery in specialized stores (52%), in super- and hypermarkets (38%); the share of consumers from individual distributors is small – just 6%.

According to the research of Rus-sian Business Consulting “Russian market of male cosmetics in 2016”,

20 MALE GROOMING

MORE ON WWW.INTERCHARM.RU/EN

as a whole both in Russia and in some regions the greatest popularity among men who buy cosmetics and perfumes in the past six months, are the five retail leaders: L’Etoile, Rive Gauche, Magnet Cosmetic, Yves Ro-cher and Ile de Beaute.

The level of their popularity in Russia on average more than 2.5 times higher than their closest pur-suers. Thus, the share of recognition of these chains in Russia exceeds 40%, and the proportion of the drogerie Ruble Boom, (6th place in the ranking) is only 16.3%. High vis-ibility and traffic the leaders due to the large number of points and the broad coverage of Russia. Thus, the Magnet Cosmetic was a leader of 2016, with more than 2500 stores.

Besides Magnet Cosmetic the other 4 chains operate for more than 15 years in the Russian market.

However, despite the high popu-larity of these chains the highest loyalty among Russians belongs to such large specialized chains as the Fortune (the share of loyal cus-tomers 62.1%) and Perfume Leader (60.7%). In L’Etoile, Rive Gauche, Yves Rocher and Ile de Beaute val-ue of the same indicator is slightly more than half of their customers. This ratio can be determined by chain format, range and price seg-ment. Magnet Cosmetic and Fortu-na are drogeries, which have a wide range of goods economy segment.

5. TRENDSRussian men pay more attention

both to customary and specialized pro ducts for skin and hair care. To date, virtually all cosmetic brands offer lines for men. Moreover, manu-facturers of mass pro-ducts pay particular attention to anti-aging

a s -p e c t s i n c l u d i n g cosmetics to re-cover freshness in the morning, re-lieve baggy lower eyelids, anti-age creams, etc. Men wishing to say goodbye to gray hair have a range of brands offering both dyers and ton-ers. Experts believe that these pro-duct categories are very promising.

As before, Russian men opt for sim-ple and universal hair care pro ducts. Shampoos for hair and body ‘two-in-one’ have become widespread late-

ly. A man w o u l d need just one bottle to refresh his body and hair. As before, the stron-ger sex is n e g l e c t -ing condi-tioners or extra care pro ducts – they simply do not see them necessary. Russian men are rational and conservative in their choice: having tried a pro duct once, they would become an addict.

6. FORECASTMore men, especially the young-

er generation, are expected to take greater care over their personal hygiene over the forecast period,

and this should create steadily increasing demand for men’s grooming pro ducts. The increasing num-ber of office jobs which require a well-

tended and c l e a n a p -p e a r -a n c e , a l o n g

with the i n f l u e n c e

of social media, is expected to help support the growth of men’s grooming.

The target audience for male care is expected to grow be-

cause more and more Russian men will buy and regularly use cosmetics and personal hygiene pro ducts.

Experts underline the increase knowledge of consumers, careful attention to the ingredients, popu-larity of the pro ducts positioned like natural. As forecast predicts mass market and private label, especially shampoos, shower gels and shav-ings will be on the rise.

SUN CARE 21

MORE ON WWW.INTERCHARM.RU/EN

22 SUN CARE

MORE ON WWW.INTERCHARM.RU/EN

BLAZE IN GLORY1. MARKET SIZE

In 2016 sun care increased by 7% in current value terms, to reach RUB5.6 billion (Euromontor data). The performance registered in 2016 was slightly faster than the 6% cur-rent value CAGR seen over the re-view period. This can be attributed to the significant increase in the av-erage unit price, which grew by 9% in 2016.

Mass sun protection saw the best current value performance in 2016, growing by 9%. Sun protec-tion remained the largest sun care category in 2016. Due to the fact that the majority of Russians were financially constrained at the end of the review period, they chose the most affordable options regarding sun protection.

Russian consumers tend to per-ceive that mass sun care pro ducts are often as good as premium pro-ducts. Therefore, premium sun care pro ducts need to have very specific features that are desired by con-sumers in order to be attractive. Pre-mium facial sun care pro ducts often have added benefits, for example anti-ageing properties, which helps to justify their higher price.

Sun protection sprays continued to gain popularity in 2016, as they are considered easier to apply than regular sun creams. However, cream remained the most popular format in sun care in Russia.

Meanwhile, this segment offers broad opportunities to sellers and manufacturers, since it does not

require such large investments, as are essential for skin care segment. A peculiar feature of the sunscreen cosmetics is that actually it can be marketed without advertising. This feature is acknowledged both by the market players and the data of surveys carried out by various agen-cies. The point is that when choos-ing a pro duct for sun protection, the consumer would be guided by the advice of friends or his/her own previous experience, rather that by advertising slogans.

2. CONSUMER HABITSRussian consumers remain very

price-sensitive and prefer to buy good quality stuff at more afford-able price. The local manufacturers have responded to the demand and launched some pro duct lines whose quality is not inferior as compared to well promoted foreign brands.

People are becoming more edu-cated on the issue of protecting the skin from harmful sun rays. Con-sumers have realized that tan – not a harmless phenomenon, and the threat to health. They under-stand that a reliable sunscreen is a necessary attribute and cosmetic companies launch pro ducts with sunscreens designed for everyday use. Especially popular are the day cream with SPF. Russian consumers are looking for pro ducts that con-tains natural ingredients that are beneficial to the skin.

Consumer behavior is chang-ing. Consumers have become more

aware of sun care that is the most suitable for their type of skin. For ex-ample, many already know that not all sun cosmetics is suitable for chil-dren and people with sensitive skin.

A healthy trend of recent years – to use sunscreen in summer and in the cold season. This applies not only to the people who are leaving for a vacation to a warmer climate. Winter sun is dangerous as well and people use skin care and makeup with a light SPF.

3. KEY PLAYERSThe leaders of the market are

international companies: L’Oréal, Beiersdorf, Russian manufacturer Floresan, Sarantis SA Group (Kolas-tyna) and Avon. Perhaps the most saturated segment of the market ‘solar’ cosmetics is a mass segment. It is available for most consumers, sold in pharmacy chains and other retail outlets (supermarkets and hypermarkets, specialized stores, etc.). In this segment, successfully competing with each other brands such as Nivea Sun (Beiersdorf), Gar-nier Ambre Solaire (L’Oréal), Yves Rocher, as well as the pro ducts of Russian companies – Floresan, pro fes sio nal cosmetics manufac-turer Salon Cosmetica, direct sales Faberlic and others.

4. DISTRIBUTIONThe development of

retail formats, in partic-ular the emergence of new drogeries and their expansion, enabled the domestic produc-ers of sun-protection cosmetics to present a wider range of their pro ducts to the mass consumers and to fun-nel the raised moneys into the pro duct range diversification.

Market Sizes | Historical/Forecast | Retail Value RSP | RUB mn | Constant 2016 PricesCategories 2014 2015 2016 2017 (forecast) Sun Care 5 740,80 5 636,70 5 647,30 5 673,60

Adult Sun Care 5 084,00 4 938,30 4 947,30 4 970,10

Aftersun 816,50 779,20 747,40 735,30

Self-Tanning 427,40 349,70 325,30 315,00

Sun Protection 3 840,10 3 809,30 3 874,50 3 919,90

Baby and Child-specific Sun Care 656,80 698,40 700,00 703,50

© Euromonitor International

SUN CARE 23

MORE ON WWW.INTERCHARM.RU/EN

All retail operators require to take out the goods should they fail to sell them before the autumn. Another challenge is the need for long cred-its for this pro duct. In times of eco-nomic instability the approach to these challenges must be extremely careful.

In terms of sales channels pref-erences, the situation is as follows: 31% of Russians buy sun-protection cosmetics in pro fes sio nal stores, 20% in super/hypermarkets, 14% – from individual consultants/distrib-utors and 13% in pharmacies.

One of the key distribution channel for sun care is pharma-cies – 55 brands and about 430 SKU are sold there. Analytical com-pany DSM Group estimates this segment in the last year 9.4 mln euro in value (+16,9% compare to 2014). The leaders are La Roche-Posay (30.13%), Vichy (19.71%) and Avene (10.3%). The TOP-3 brands in therms of volume are La Roche-Po-say (15.02%), Russian brands Flore-san (14.23%) and Moye Solnyshko (13.88%).

5. TRENDSOne of the trends, which is high-

lighted by most market players, is the high demand for pro ducts ensur-ing maximum sun protection and, on the other hand, suntan oils with low SPF level. This contradiction confirms the evident diversification of the consumer audience: senior generation willing to preserve youth-fulness prefers high protection aids,

whereby the teenagers for whom the g skin means success and prosperity stake on nice pink and fast tan.

As regards to such actual trend as the de-mand for natu-ral and organic cosmetics, such pro ducts for sun

care are less popular yet. In par-ticular, this phenomenon can be explained by insufficient represen-tation on the market and the high price contributes as well.

Meanwhile, there are players, which are quite satisfied with the last year sales outcomes in the medium or even high price range. In other words, many Russians are still willing to pay more for the pre-mium brands. That say, the success of relevant sales directly depends on the brand distributor’s market-ing strategy.

Sunscreen facial pro ducts are the most popular category, since it enjoys more attention. Certainly, the consumer’s drive towards particular brands primarily depends on his/her financial capacities. A reason-able value for money factor is impor-tant for people with average income. Luxury brands are attracting and will attract the Russians with high in-come.

6. FORECASTRussia is expected to keep posi-

tion in the BRIC nations with a value of $109.6 million in 2020. The mar-ket has a strong growth potential. Its development will be stimulated by several factors including promising

macroeconomic environment with higher consumer incomes, deeper penetration of retail business in the regions, higher awareness of local residents of sun harm and acceler-ated evolution of tourism in warm and sunny regions, both abroad and in Russia.

According to Euromonitor, Sun care is set to record a value CAGR of 2% at constant 2016 prices in the upcoming five years period, rising to RUB6.1 billion in 2021. This will be a better performance than the nega-tive value CAGR of 2% recorded over the review period. The expected sta-bilisation of the national currency and higher incomes will contribute to more Russians having beach holi-days abroad. As a result, increased demand for sun protection is antici-pated over the forecast period.

Experts predict that self-tanners will attain the most dynamic growth of 4% CAGR in monetary terms for the forecast period and may account for 18% of sales of sunscreen cos-metics by the end of 2017. This cat-egory will definitely benefit from the consumers’ desire to have tanned skin even in cold or cloudy weather because self-tanners enable to tan their skin quickly and comfortably without tedious visits to solariums.

24 ORAL CARE

MORE ON WWW.INTERCHARM.RU/EN

SMART AND BRIGHT1. MARKET SIZE

Currently, the range oral care is extremely broad covering tooth-pastes, rinses, balms, toothbrushes, flosses, fresheners and many other items, but toothpastes undoubtedly make the bulk of the market. Today, consumers seek pro fes sio nal pro-ducts, and this is the main trend in oral care market. Now people can afford to pay more for high quality pro ducts to get excellent results.

Moreover, plain toothpaste is not enough for consumers, since they need high quality and effective pro-duct; so, in recent years, premium and super premium segments re-sponded with strong sales.