analytics of the philippine economy continuity++ …iro.ph/article_doc/cd807f75_bsp presentation -...

TRANSCRIPT

Analytics of the Philippine Economy

Continuity++ Building & Sustaining Strength

Briefing on the Philippine Economy

9 March 2018

Davao

2

Prospects for the Philippine economy remain bright

� PHL economy is expected to sustain growth momentum over the medium term

6.7%6.9% 7.0 –8.0%

7.0 –8.0%

7.0 –8.0%

2016 2017 2018 2019 2020

6.6%(IMF)

6.7%(WB)

6.7%(ADB)

6.7%(WB)

6.8%(ADB)

6.7%(IMF)

3

PH leads the ASEAN pack

“ The Philippines will continue to be the fastest-growing eco nomy inASEAN, despite some stabilization of investment growth.”

World Bank Global Economic Prospects (Jan 2018)

4

Prevailing narrative is favorable � Supportive macroeconomic environment:

� broad-based growth low inflation comfortable external payments

� Healthy banking system

� Disciplined policy frameworks

Key Indicators 2005 – 2009 2010 – 2015 2016 2017

Strong growth Real GDP growth (%) 4.4 6.2 6.9 6.7

Low inflation Headline inflation (%) 5.5 3.4 1.8 3.2Sustained fiscal

disciplineFiscal balance (% of GDP) -1.7 -1.8 -2.4 -2.2

Ample liquidity &

credit

Domestic Liquidity (% of GDP)

(% y-o-y change)

47.215.1

55.613.2

65.612.8

67.311.9

Outstanding loans -U/KBs

(% y-o-y change)8.9 15.7 17.3 19.4

Sound & stable

banking system

Non-performing loans

(% of total loans) - U/KBs*5.0 2.2 1.4 1.2

Capital Adequacy Ratio

(consolidated basis) - U/KBs**16.7 17.2 15.1 15.7 (end-Sep)

Robust external

payments position

Current Account Balance ($ Bn)

(% of GDP)

5.13.6

8.23.2

-1.0-0.3

0.03 (Jan-Sep)0.01 (Jan-Sep)

Gross International Reserves

(months of imports of g/s/inc)6.4 10.8 8.8 8.3

External debt (% of GDP) 46.1 30.9 24.5 23.4 (end-Sep)

External DSR (% of exports of

goods, services & income)12.3 7.9 7.0 6.2 (Jan-Nov)

5

PHL economic growth has been sustained…

Real GDP Growth(year-on-year growth, in %)

Average: 5.2% (1999-2017)

Positive economic growth for 76 consecutive quarters

Average: 6.6% (2013-2017)

6

…and is robust as well as broad-based

Source: Philippine Statistics Authority (PSA)

Services sector has remained the

key driver of growth…

…but share of industry (e.g., mfg.,

construction) has been expanding

GDP breakdown by expenditure (%)

Rising contribution of capital formation

7

Strong public infrastructure program

Aggressive investment agenda is the springboard to stronger growth

*Obligation basis 2017 ProgrammedProjections consistent with the medium-term fiscal targets and growth assumptions approved during the 170th Development Budget Coordination Committee (DBCC) Meeting on June 9, 2017

1.8 1.82.0

2.7 2.7

4.14.5

5.4

0.0

100.0

200.0

300.0

400.0

500.0

600.0

700.0

800.0

900.0

1,000.0

0

0.5

1

1.5

2

2.5

3

3.5

4

4.5

5

5.5

6

2010 2011 2012 2013 2014 2015 2016 2017

Infrastructure budget (PHP bn) % of GDP*

8

Rising investments boost growth & create jobs

Source: PSA, NEDA, BSP, * Investment approved by the Philippines’ Investment Promotion Agencies – Board of Investments (BOI), Clark Development Corporation (CDC), Philippine Economic Zone Authority (PEZA),

Subic Bay Metropolitan Authority (SBMA), Authority of the Freeport Area of Bataan (AFAB), BOI-Autonomous Region of Muslim Mindanao (BOI-ARMM), and Cagayan Economic Zone Authority (CEZA)

Real growth (%)

Growing investment pledges favorablefor growth prospects

Considerable foreign interest inmanufacturing sector

Economy increasingly supported by a vibrant manufac turing sector

9

Stable inflation supports greater economic activity

Low and stable inflation Well-anchored inflation expectations

Source: PSA Source: BSP

Sources: AP Consensus (February 2018), Bloomberg Co ntributor Forecasts (as of 8 February 2018), Oxford Economics Forecasts as of 8 February 2018

Inflation Forecasts for the

Philippines2018 2019

Bloomberg Consensus Forecasts

3.6 3.4

Oxford Economics 3.6 3.9

Asia Pacific Consensus 3.9 3.6

Source: BSP, IBPAP

Manageable balance of payments position shields economy from external headwinds

Structural flows from remittances & BPOs

Overseas Filipinos' cash remittances and BPO revenues, ($ bn)

Ample reserves

FX reserves ($bn) and months of import cover

Sustained decline in external debt-to-GDP

External debt ($bn) and external debt/GDP, (%)

2017 BPO revenues based on IBPAP

Resilient foreign direct investments

Non-Residents’ direct investments, by instrument ($ bn, net)

11

Current account components (in US$ bn)

Strong imports growth has led to narrowing of curre nt account surplus

-3

-2

-1

0

1

2

3

4

5

-30

-20

-10

0

10

20

30

40

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Goods Exports (lhs) Goods Imports (lhs) BPO receipts (lhs)

OF remittances (lhs) Travel receipts (lhs) Current Account Balance (rhs)

-30.0

-20.0

-10.0

0.0

10.0

20.0

30.0

40.0

-

20,000

40,000

60,000

80,000

100,000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

in p

erce

nt

in m

illio

n U

S$

Goods Imports, by major commodity

Capital Goods Mineral Fuels and Lubricant Mat/Acc. for Manufacture of Elec. Eqpt.

Other Raw Materials/Intermediate Goods Consumer Goods Other Imports

Total Imports Growth (in %, RHS)

12Source: BSP

Peso is flexible and competitive

Philippine Peso (PHP) per USD Rate

01 Jan 2016:47.06

8 March 2018:52.03

13

end-December 2017:NPL ratio: 1.2 %NPA ratio: 1.3 %

Sep 2017:CAR (solo): 15.0 %

CAR (consolidated): 15.7 %

Source: BSP

Quality of assets & loan portfolios sustain improvement

PHL banks are adequately capitalized, providing buffers to mitigate shocks

Banking system remains sound & stable

14

13.8 14.415.6 16.5 15.6

14.0 13.4 14.0 14.5 14.9 15.1 15.8 15.2 15.7

17.5 17.0 16.7 16.7 16.517.7 16.9 16.0 16.8 16.3 15.7 16.8 17.6 17.9

-3.7 -2.6-1.0 -0.2 -0.9

-3.7 -3.5-2.0 -2.3 -1.4 -0.6 -0.9

-2.4 -2.2 -3.0 -3.0 -3.0 -3.0 -3.0-5

0

5

10

15

20

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018P 2019P 2020P 2021P 2022PNG Revenues/GDP NG Expenditures/GDP NG Deficit/GDP

Tax reform => headroom for targeted social spending& infrastructure upgrading

Infrastructure Program, Obligation Basis 2018-2022

Fiscal Expenditure, Revenue and Deficit (% of GDP)

15

Source: Latest BSP staff estimates

Source: PSA

Employment Share by Class of Workers Employment Share by Educational Attainment

Improved potential capacity helps sustain growth tr ajectory

Incremental Capital-Output Ratio Total Factor Productivity

9.5

6.44.2 3.7

0.0

2.0

4.0

6.0

8.0

10.0

1989 - 1992 1993 - 2001 2002 - 2009 2010 - 2017

0.0 0.5

2.0 2.1

0.0

0.5

1.0

1.5

2.0

2.5

1989 - 1992 1993 - 2001 2002 - 2009 2010 - 2017

33.426.6

38.141.4

4.7

26.5 25.8

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

College Post Secondary High School

Elementary (w/ SPED) No Grade Completed

51.162.5

12.36.0

32.3 27.8

4.4 3.7

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Employer in Own Family Self-Employed

Unpaid Worker Wage and Salary Workers

16

Philippine Credit Rating

BBB+Affirmed BBB+ rating

stable outlook 2 August 2016

BBBUpgraded rating to BBB

stable outlook10 December 2017

BBBRe-affirmed BBB rating

stable outlook28 April 2017

Baa2Re-affirmed Baa2 rating

stable outlook27 June 2017

Credit rating upgrades: show of faith

17

Year Selected Structural & Policy Reforms

1994 Foreign bank entry liberalized

1995 Telecommunications industry liberalized

1997 Water services privatized

1998 Oil industry deregulated; consolidated bank supervision adopted

2000 Philippine E-Commerce Act passed

2002 Inflation targeting framework adopted by BSP

2003 Government Procurement Reform Act passed

2005 Value-added tax (E-VAT) expanded

2006 VAT rate increased

2007 Risk-based bank supervision fully implemented

2009 TransCo and NPC privatized

2013

2016

Excise tax rates on alcohol and tobacco (“sin taxes”) revised

Further liberalization of FX regulations

A house built of bricks...purposeful structural ref orms

18

Dependency ratios: Philippines2005-2050 (in %)

� Large number of young, skilled & educated working population supports strong growth outlook

…and favorable demographic dynamics

*Source: United Nations, Department of Economic and Social Affairs, Population Division (2017). World Population Prospects: The 2017 Revision,

Volume II: Demographic Profiles (ST/ESA/SER.A/380).

Median Age of the Population (2015):

24.1 years old

Total dependency ratio to decline from

68.2% in 2005 to 50.8% by 2050

19

Looking ahead…

� confident about prospects for expansion in coming years

� storyline of robust home demand alongside improving

external demand remains intact

…but with challenges

What are the challenges to the positive narrative?

� Will growth be crimped by:

� External factors?

� Domestic constraints?

20

On external front: some reasons for caution

� Timing & magnitude of Fed interest rate policy hikes

� Geopolitical concerns

How is BSP preparing for tighter global financial conditions?

� Best defense is good offense: disciplined macroeconomic policies & prudent financial sector oversight help keep “house in order”

� Use full menu of instruments to respond to ebb/flow of capital, including:� exchange rate flexibility� interest rate action � careful/clear communication to manage sentiment

21

� Overheating

� Infrastructure gaps

� Leverage

� Economic inclusion: Jobs challenge

� Natural disasters

On domestic front: some potential stress points

Speed bumps

22

Overheating concerns?� Growth momentum accompanied by substantial rise in credit,

raising concerns

� Fundamentally-driven growth: broadening growth drivers, rising

incomes, growing middle class, favorable labor market dynamics

� Efforts underway to address infrastructure gaps and improve

business environment

Growth momentum accompanied by a substantial rise i n credit, raising concerns

242.2216.5

186.6 183.2158.0 154.4 154.3

138.6123.3

66.241.0

HONG KONG CHINA JAPAN SOUTH

KOREA

SINGAPORE NEW

ZEALAND

AUSTRALIA MALAYSIA THAILAND PHILIPPINES INDONESIA

Domestic Credit as % of GDP

Q4 2017

23

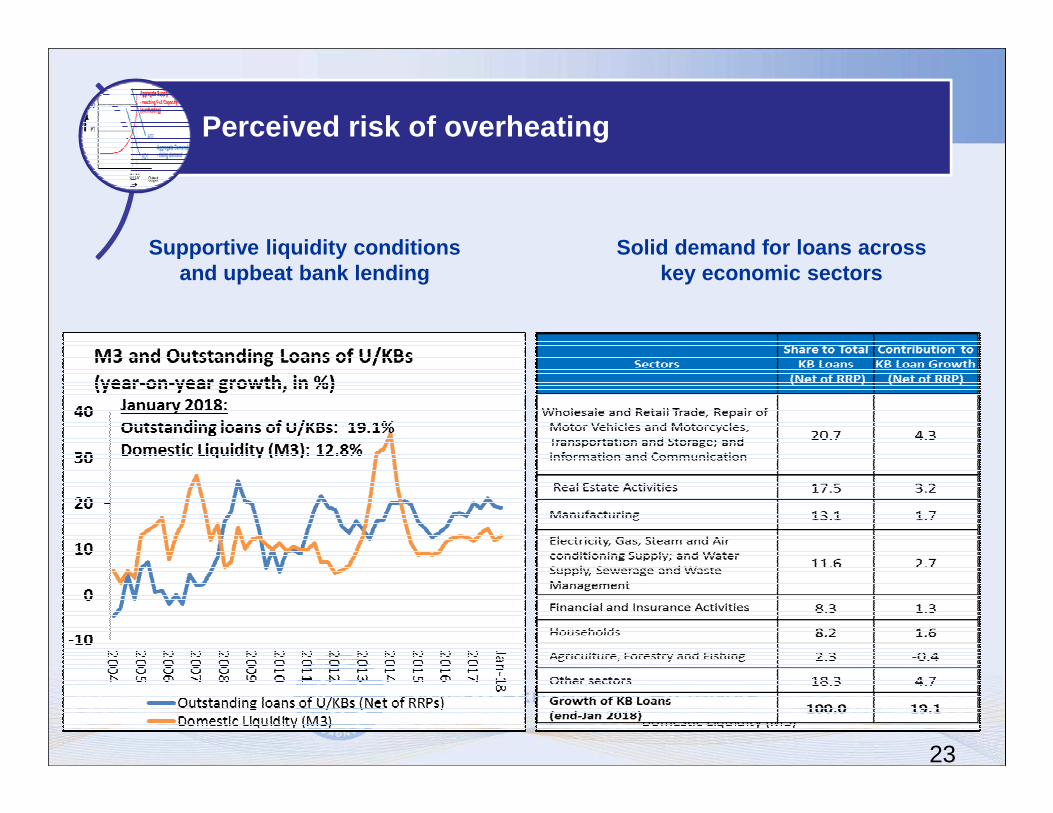

Perceived risk of overheating

Solid demand for loans across key economic sectors

Supportive liquidity conditions and upbeat bank lending

24

Perceived risk of overheating

� Current property prices broadly aligned with fundamentals

Source: BSP Source: BSP

25

38.7%

36.4%

30.0%

32.0%

34.0%

36.0%

38.0%

40.0%

42.0%

44.0%

Ma

r

Jun

Se

p

De

c

Ma

r

Jun

Se

p

De

c

Ma

r

Jun

Se

p

De

c

Ma

r

Jun

Se

p

De

c

Ma

r

Jun

2013 2014 2015 2016 2017

Outstanding General Government Debt

(as percent of GDP)

National Government less BSF

General Government

Source: Department of Finance

Asia: Nonfinancial Corporate Sector Debt(as percent of GDP)

Leverage in a rising interest-rate environment

4%

5%

6%

7%

8%

9%

10%

20

11

:01

Q

20

11

:02

Q

20

11

:03

Q

20

11

:04

Q

20

12

:01

Q

20

12

:02

Q

20

12

:03

Q

20

12

:04

Q

20

13

:01

Q

20

13

:02

Q

20

13

:03

Q

20

13

:04

Q

20

14

:01

Q

20

14

:02

Q

20

14

:03

Q

20

14

:04

Q

20

15

:01

Q

20

15

:02

Q

20

15

:03

Q

20

15

:04

Q

20

16

:01

Q

20

16

:02

Q

20

16

:03

Q

20

16

:04

Q

20

17

:01

Q

20

17

:02

Q

20

17

:03

Q

Consumer Loans

(as percent of GDP)

26

� Structural rather than cyclical story of economic growth

� Disciplined policies and purposeful structural reforms have yielded

dividends.

� Economy is in position of strength to weather volatilities.

What can bring PHL economy to the next level?

� Continued macroeconomic discipline (the ABC’s: ammunition,

buffers, communication)

� It’s all about the I’s (infrastructure, institutions, inclusiveness)

Key Messages

Analytics of the Philippine Economy

Continuity++ Building & Sustaining Strength

Briefing on the Philippine Economy

9 March 2018

Davao