annexes - trade sustainability impact assessment of...

TRANSCRIPT

ANNEXES - Trade Sustainability Impact Assessment of the Association Agreement to be negotiated between the EU and Central America TRADE08/C1/C14 & C15 - Lot 2

Annexes – Final Report Client: European Commission, DG-Trade Submitted by:

In cooperation with:

Rotterdam, 18 September 2009

ECORYS Nederland BV

P.O. Box 4175

3006 AD Rotterdam

Watermanweg 44

3067 GG Rotterdam

The Netherlands

T +31 (0)10 453 88 00

F +31 (0)10 453 07 68

W www.ecorys.com

Registration no. 24316726

ECORYS Macro & Sector Policies

T +31 (0)10 453 87 53

F +31 (0)10 452 36 60

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America

Table of contents

List of Acronyms and Abbreviations 9

Annex I References 11

Annex II Overview Trends and Issues EU and Central America 21 II.1 European Union – Central America Current Trade & Investment 21

II.1.1 Trade in Goods 21 II.1.2 Trade in Services 25 II.1.3 Investment 27

II.2 European Union – Central American Relations and Relevant Agreements 27 II.3 Sustainability issues in the European Union 30

II.3.1 Main economic issues European Union 30 II.3.2 Main social issues European Union 31 II.3.3 Main environmental issues European Union 32

II.4 Sustainability issues in Central America 33 II.4.1 Main economic issues Central America 33 II.4.2 Main social issues Central America 34 II.4.3 Main environmental issues Central America 36

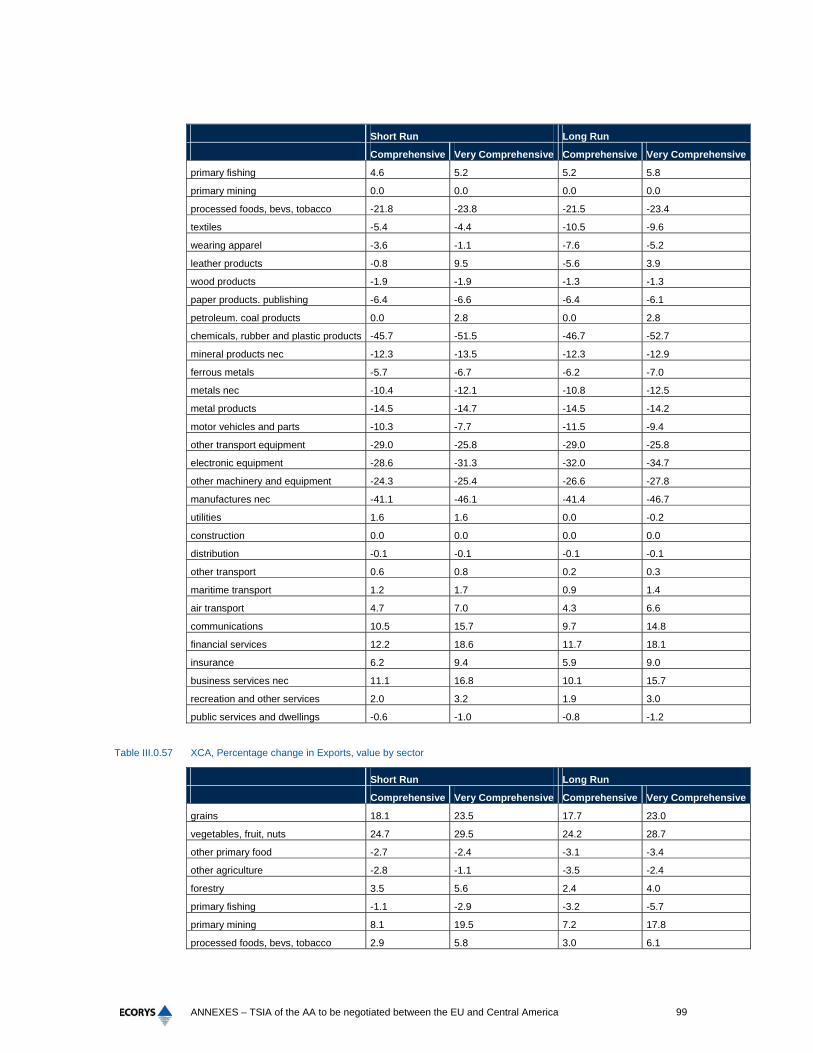

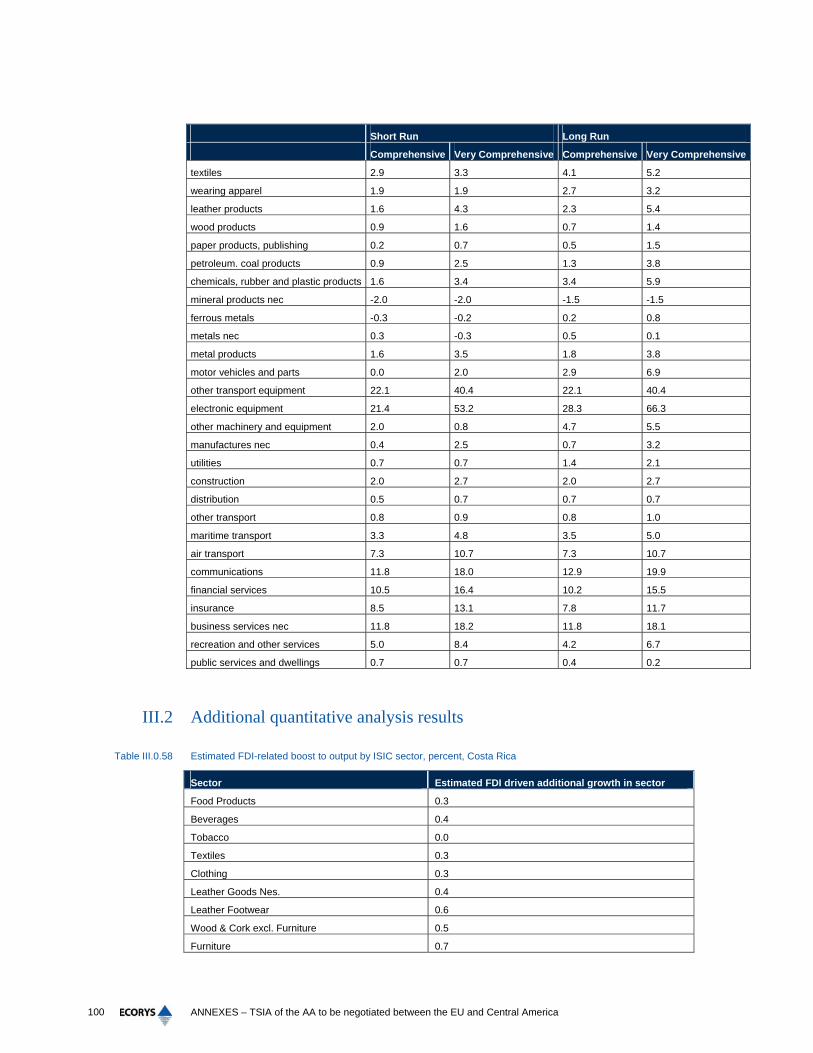

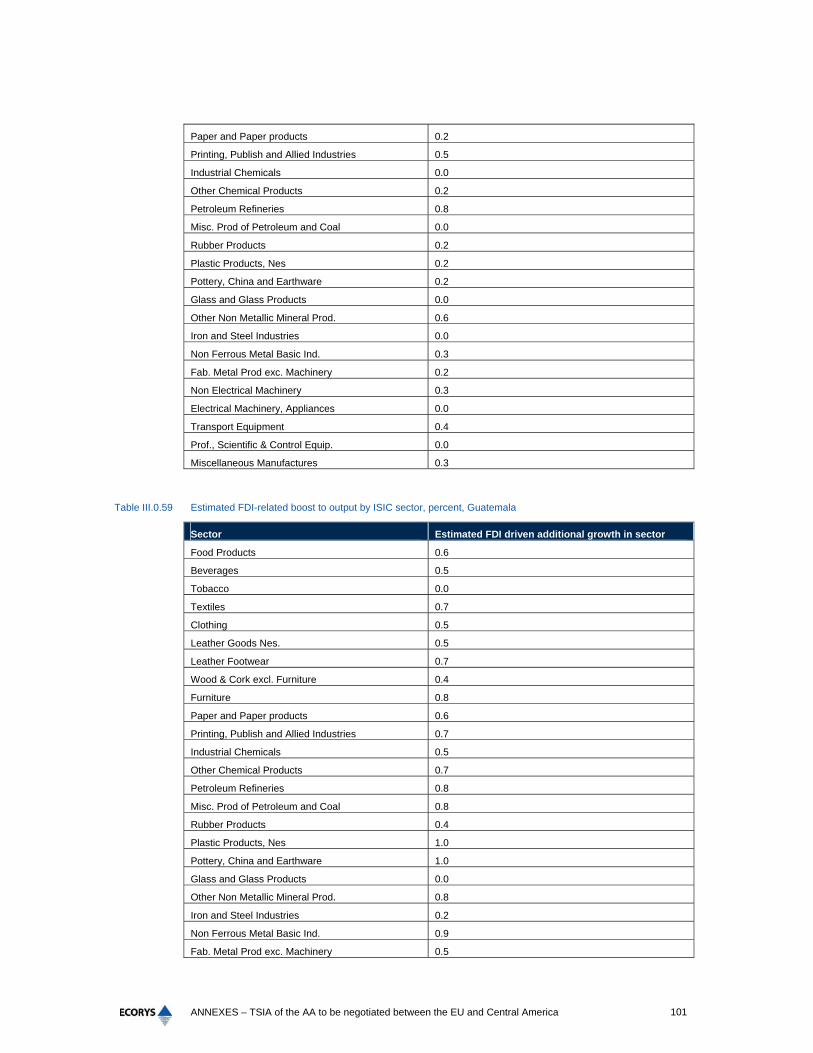

Annex III Modelling results 39 III.1 CGE related modelling 39 III.2 Additional quantitative analysis results 100 III.3 Poverty methodology 103

Annex IV Civil Society Consultations 105

Annex V In-depth Analyses 137

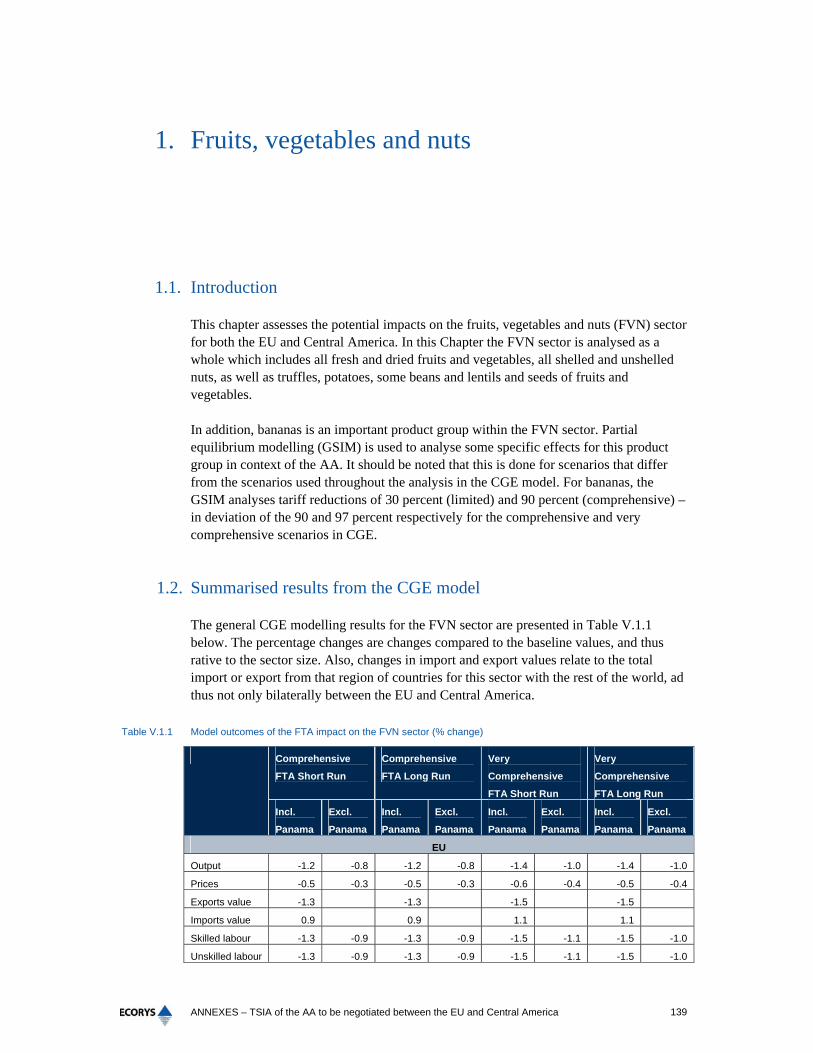

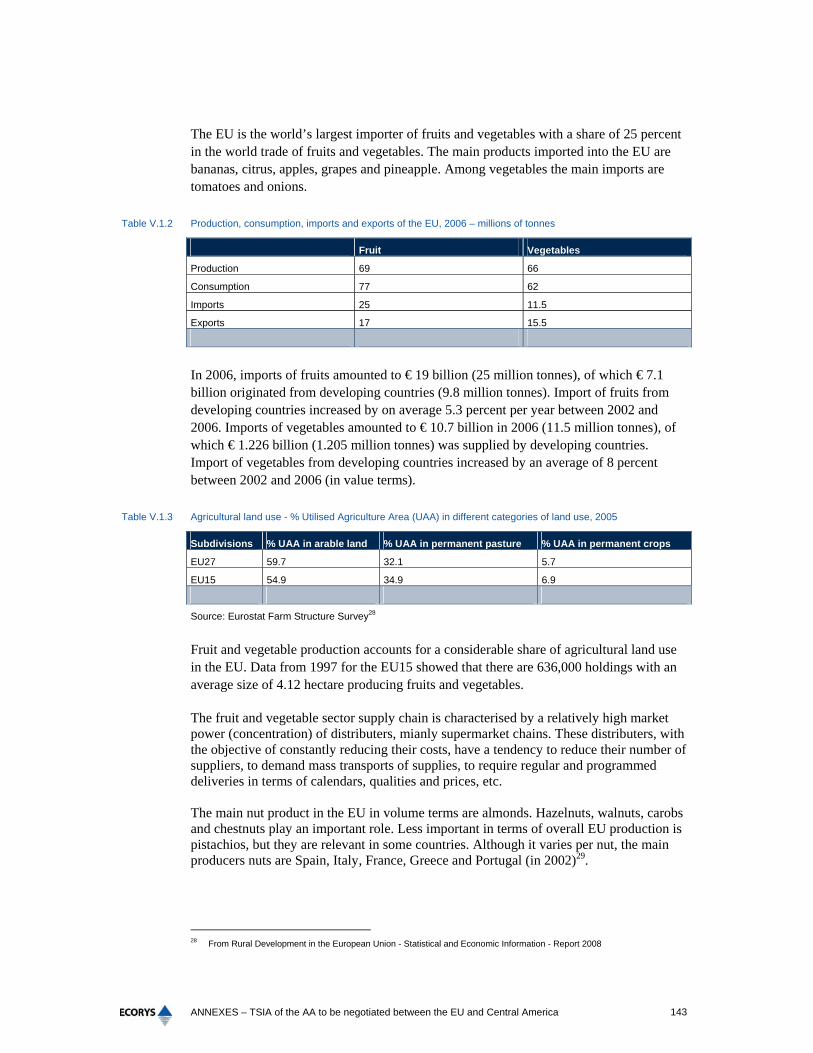

1. Fruits, vegetables and nuts 139 1.1. Introduction 139 1.2. Summarised results from the CGE model 139 1.3. Vertical dimension: main issues in the sector 142

1.3.1. European Union 142 1.3.2. Central America 146

1.4. Partial equilibrium modelling on bananas 150 1.5. Sustainability impact assessment 152

1.5.1. European impacts 152 1.5.2. Impacts Central America 154

1.6. Conclusions 158

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America

1.6.1. European Union 158 1.6.2. Central America 158

1.7. Policy recommendations 158 1.7.1. European Union 159 1.7.2 Central America 159

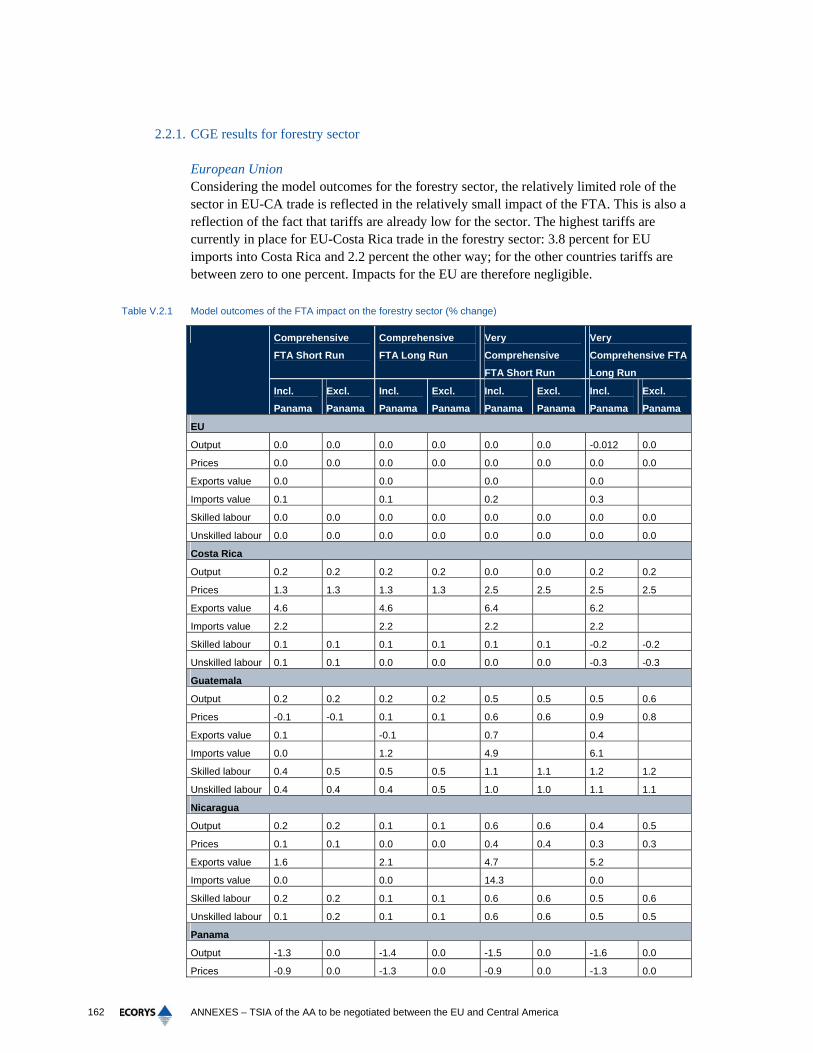

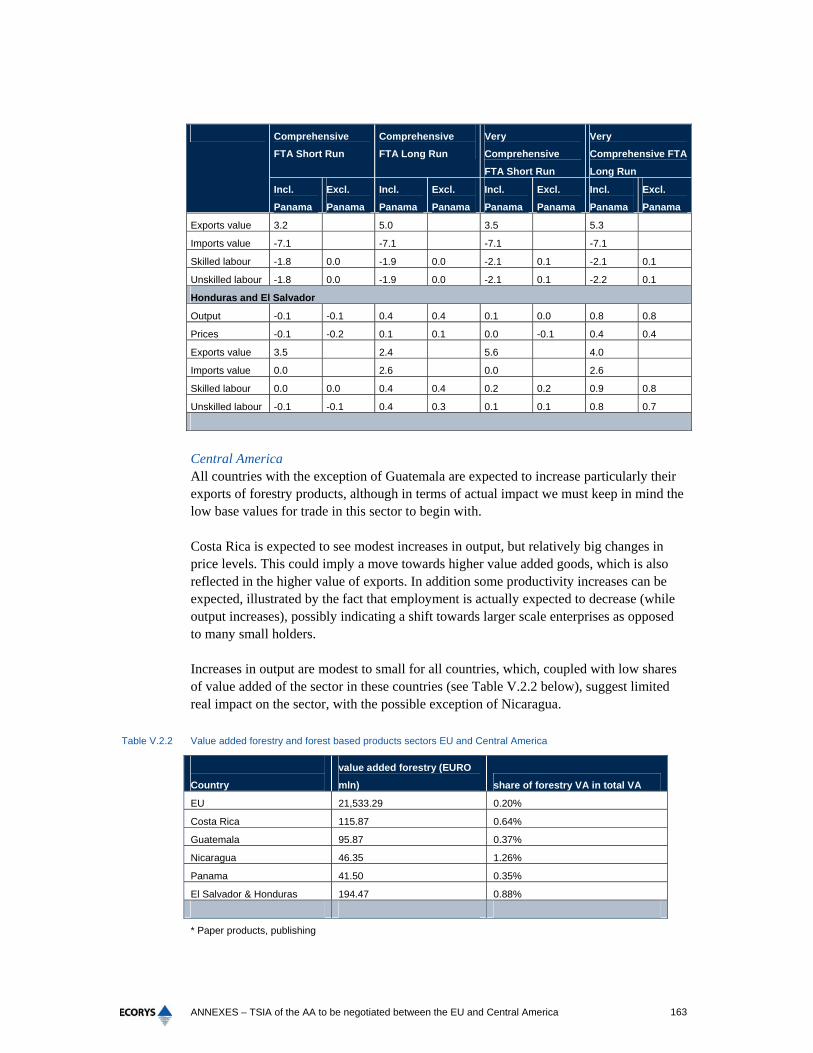

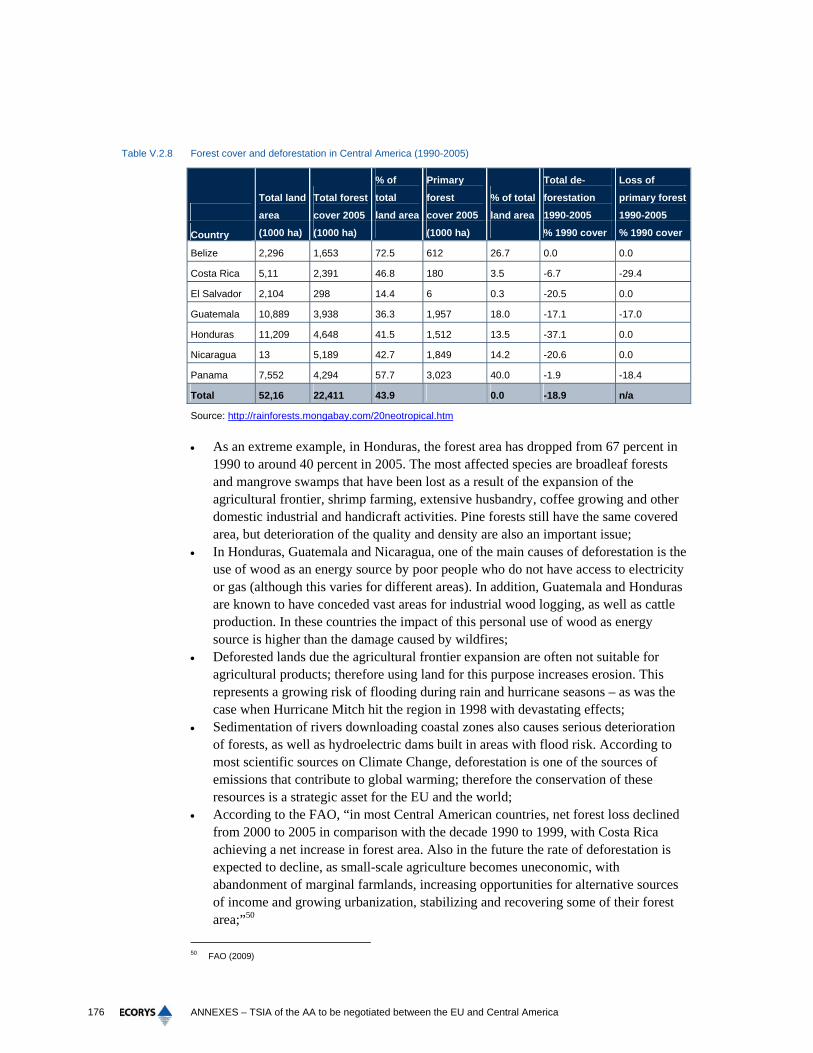

2. Forestry 161 2.1. Introduction 161 2.2. Summarised results from the CGE model 161

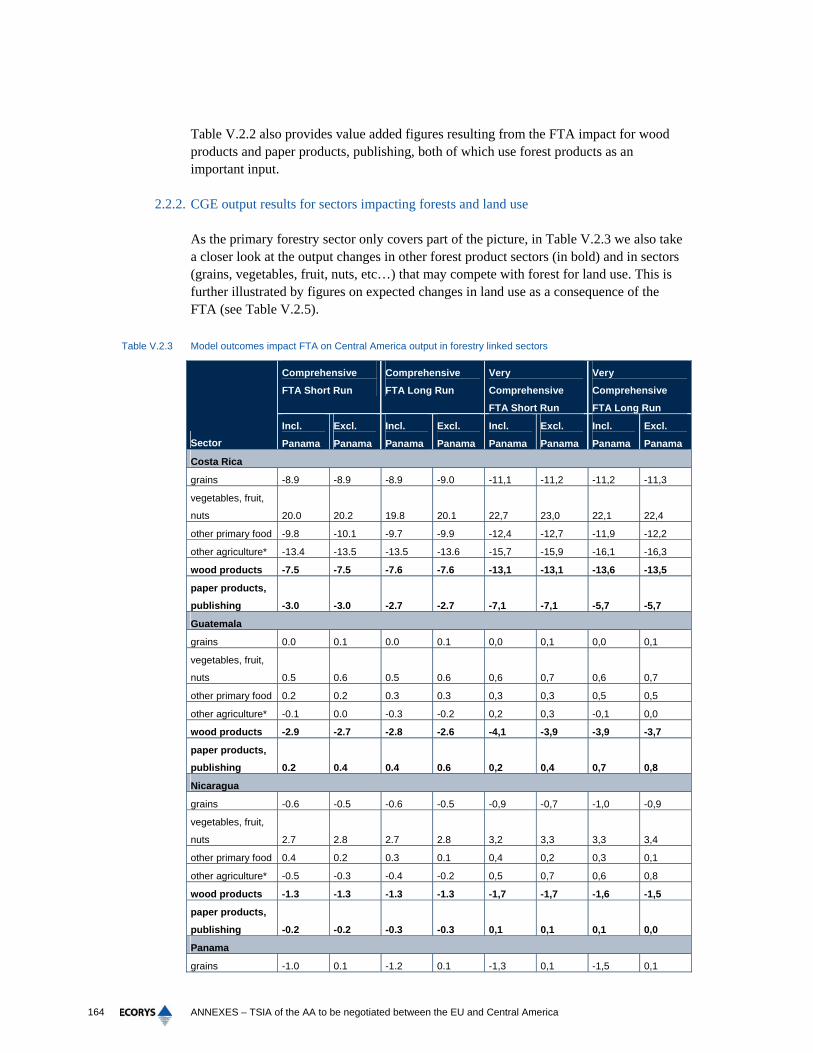

2.2.1. CGE results for forestry sector 162 2.2.2. CGE output results for sectors impacting forests and land use 164

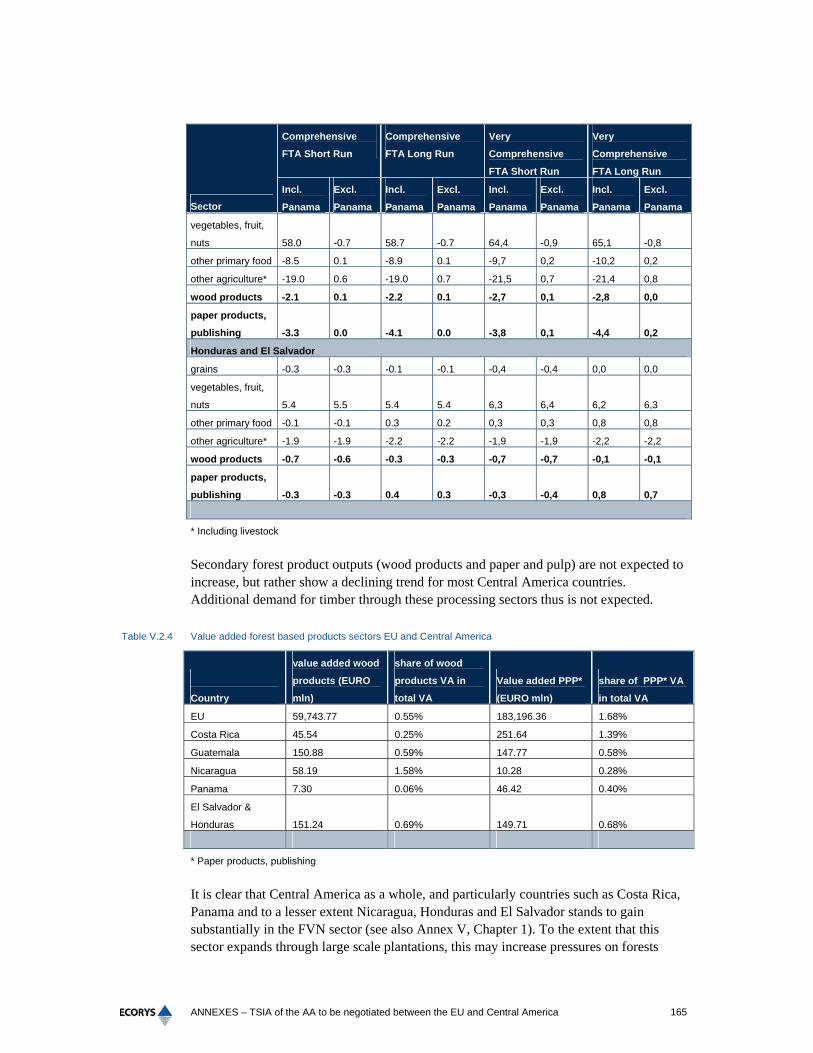

2.3. Vertical dimension: main issues in the sector 166 2.3.1. European Union 167 2.3.2. Central America 172

2.4. Sustainability impact assessment 178 2.4.1. European Union sustainability impacts 178 2.4.2. Central America sustainability impacts 179

2.5. Conclusions 183 2.5.1. European Union 183 2.5.2. Central America 183

2.6. Policy recommendations 184 2.6.1. Eurpean Union 184 2.6.2. Central America 185

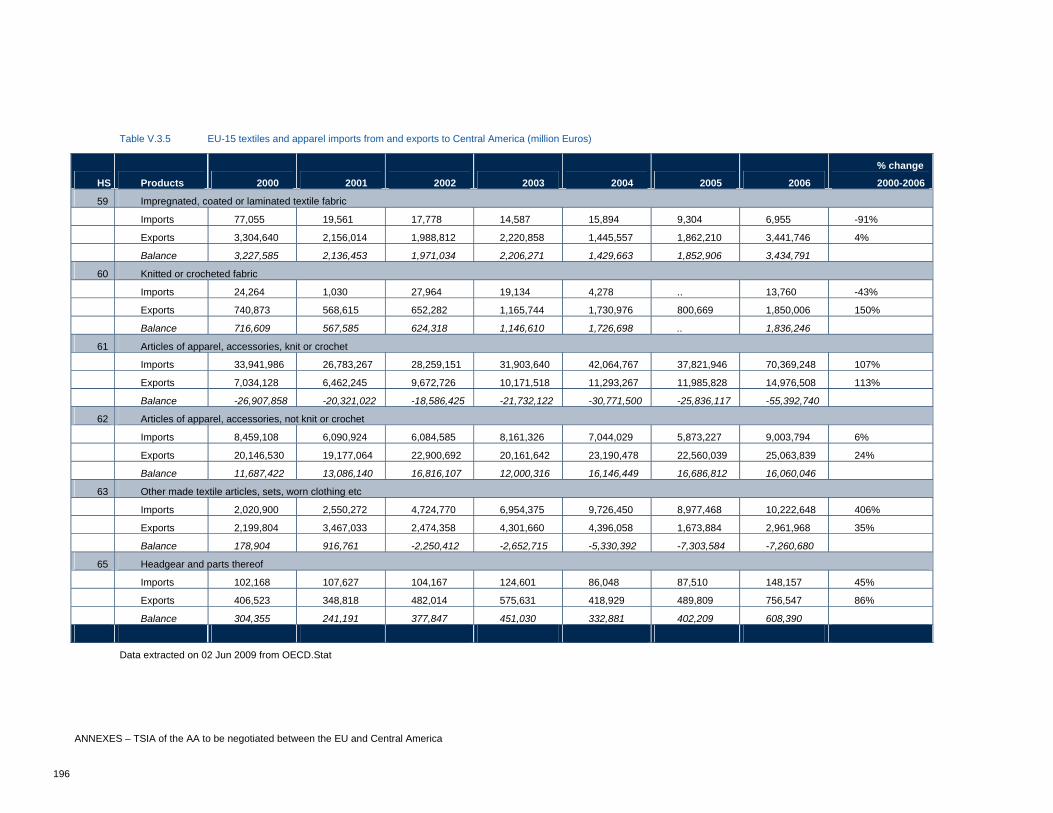

3. Textiles and clothing 187 3.1. Introduction 187 3.2. Summarised results from the CGE model 188 3.3. Vertical dimension: main issues in the sector 192

3.3.1. European Union 192 3.3.2. Central America 197

3.4. Sustainability impact assessment 202 3.4.1. European Union sustainability impacts 203 3.4.2. Central America sustainability impacts 203

3.5. Conclusions 206 3.5.1. European Union 206 3.5.2. Central America 207

3.6. Policy recommendations 207 3.6.1. European Union 207 3.6.2. Central America 208

4. Electronics 209 4.1. Introduction 209 4.2. Summarised results from the CGE model 209 4.3. Vertical dimension: main issues in the sector 211

4.3.1. European Union 211 4.3.2. Central America 213

4.4. Sustainability Impact assessment 215 4.4.1. European Union impacts 215

4.4.2. Impacts Central America 217 4.5. Conclusions 220

4.5.1. European Union 220 4.5.2. Central America 220

4.6. Policy recommendations 221 4.6.1. European Union 221 4.6.2. Central America 221

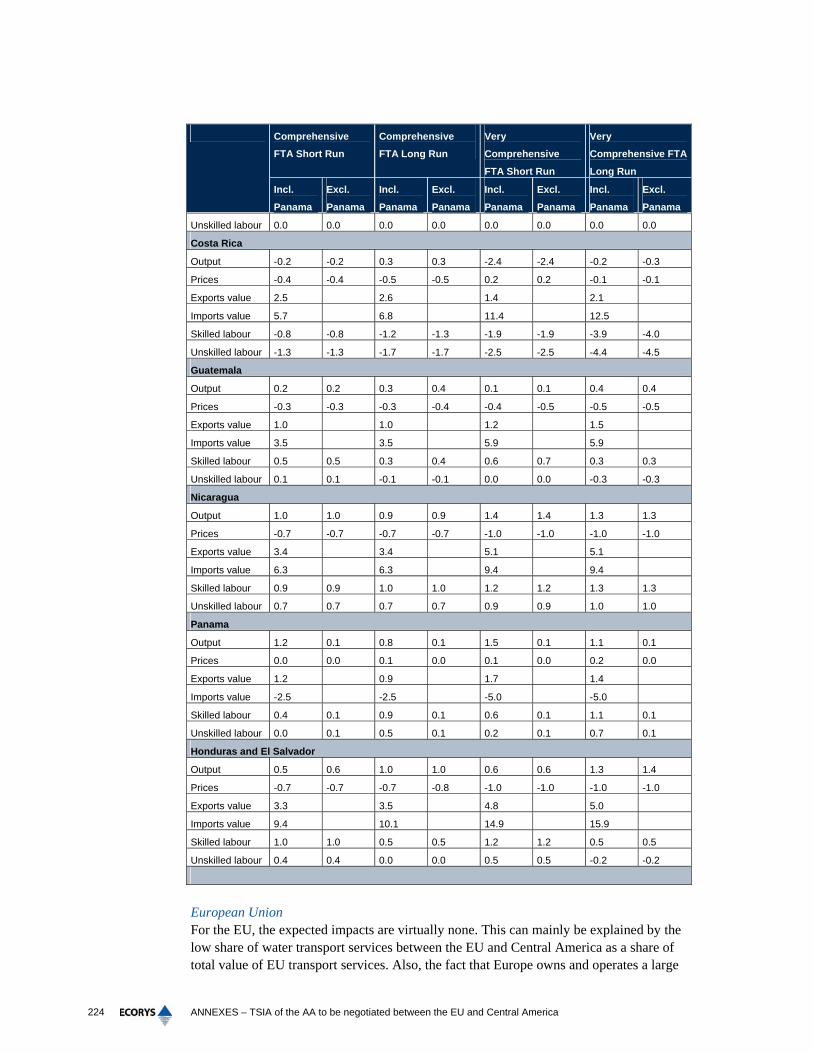

5. Maritime transportation services 223 5.1. Introduction 223 5.2. Summarised results from the CGE model 223 5.3. Vertical dimension: main issues in the sector 226

5.3.1. European Union 226 5.3.2. Central America 227

5.4. Sustainability impact assessment 230 5.4.1. European Union impacts 230 5.4.2. Impacts Central America 232

5.5. Conclusions 236 5.5.1. European Union 236 5.5.2. Central America 236

5.6. Policy recommendations 237 5.6.1. European Union 237 5.6.2. Central America 238

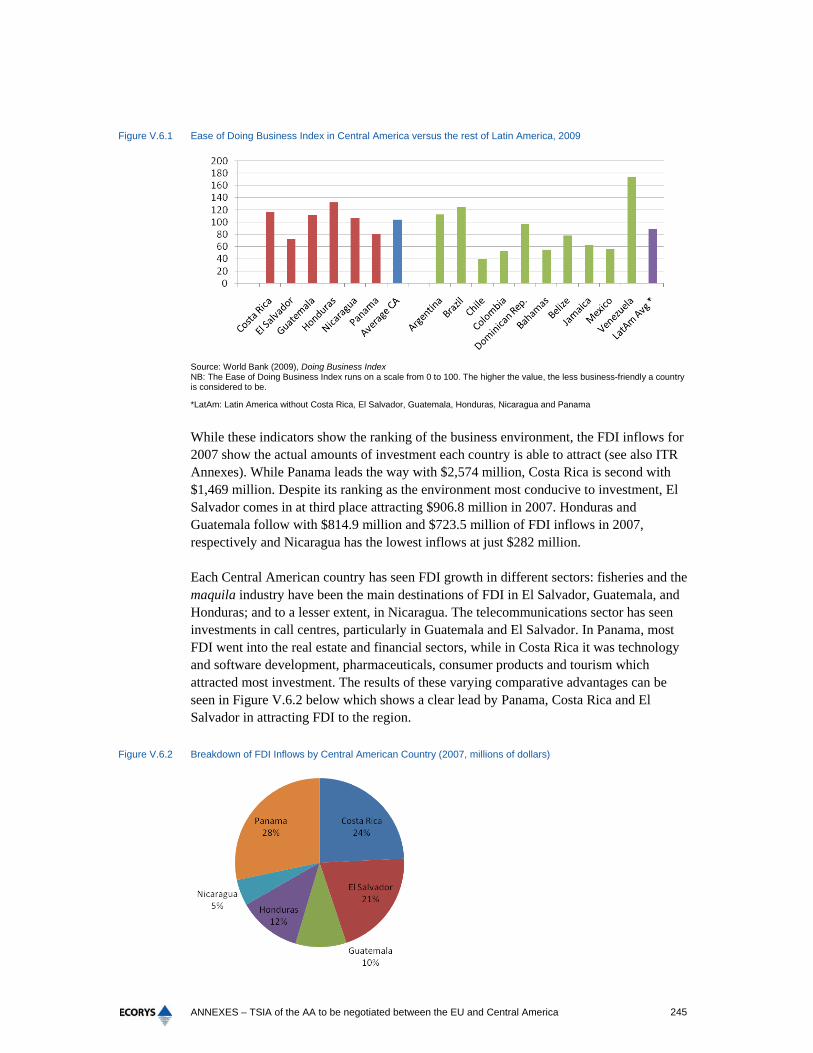

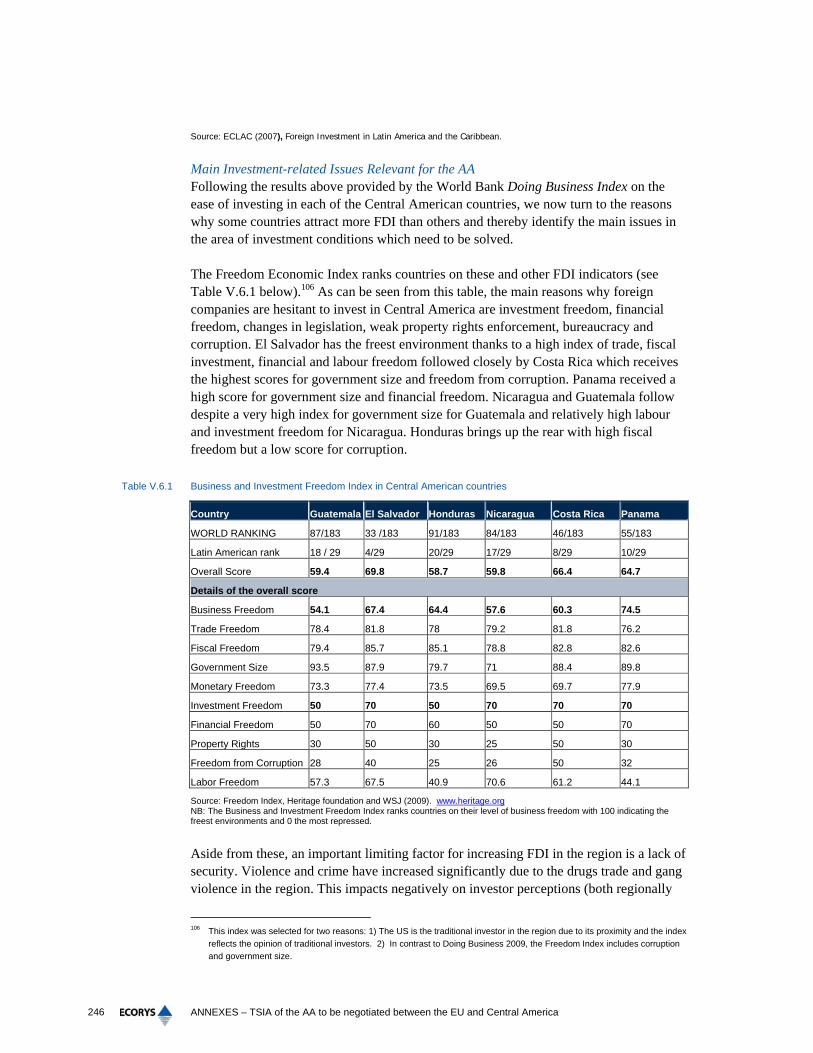

6. Investment conditions 241 6.1. Introduction 241 6.2. Investment Climates and FDI Flows in the EU and Central America 241

6.2.1. European Union Investments and Investment Conditions 241 6.2.2. Central America 243

6.3. Impact Assessment 247 6.3.1. CGE modelling results 247 6.3.2. Gravity analysis 248 6.3.3. European Union Impacts 249 6.3.4. Central American Impacts 250

6.4. Conclusions 254 6.4.1. European Union 254 6.4.2. Central America 254

6.5. Policy recommendations 255 6.5.1. European Union 255 6.5.2. Central America 255

7. In focus: Labour Issues 257 7.1 Introduction 257 7.2 Main Labour Issues – European Union 258 7.3 Main Labour Issues – Central America 258 7.4 Labour and the AA 260 7.4 Conclusions 261

7.4.1 European Union 261

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America

7.4.2 Central America 261 7.5 Policy Recommendations 262

7.5.1 AA-related 262 7.5.2 Flanking measures 263

8. In Focus: Environmental Issues 265 8.1. Multilateral Environmental Agreements (MEAs) 265

8.1.1 European Union 265 8.1.2 Central America 265

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 9

List of Acronyms and Abbreviations

Abbreviation Description

AA Association Agreement

AHM Maquila Association of Honduras

ALOP Asociación Latinoamericana de Organizaciones de Promoción

ATC Agreement on Textile and Clothing

CACM Central American Common Market

CAWN Central American Women’s Network

CCA Causal Chain Analysis

CDR Centro de Estudios para el Desarrollo Rural

CCAD Central American Commission

CGE Computational General Equilibrium

CMT Cut-make and trim

CSR Core Social Responsibility

DDA Doha Development Agenda

DR-CAFTA Dominican Republic-Central American Free Trade Agreement

DWA Decent Work Agenda

DWCP Decent Work Country Programme

EC European Commission

ECLAC Economic Commission for Latin America

EDF Economic Development Foundation

EEA European Environment Agency

EMSA European Maritime Safety Agency

ESF European Services Forum

ETS Emission Trading System

EU European Union

EURATEX European Apparel and Textile Organisation

FAO Food and Agriculture Organisation

FAP Forest Action Plan

FDI Foreign Direct Investment

FLEGT Forestry Law Enforcement, Governance and Trade

FMT Francois, Van Meijl, and Van Tongeren

FoEE Friends of the Earth Europe

FTA Free Trade Agreement

FTZs Free Trade Zones

FUDI Fundación de Desarrollo Integral

FVN Fruits, Vegetables and Nuts

GDP Gross Domestic Product

GHG Greenhouse Gas

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 10

Abbreviation Description

GSP Generalized System of Preferences

IEA International Energy Agency

IEAs International Environmental Agreements

ILO International Labour Organisation

IMO International Maritime Organisation

IPR Intellectual Property Rights

ITR Interim Technical Report

LULUFC Land Use, Land use Change and Forestry

MEAs Multilateral Environmental Agreements

MFA Multi Fibre Agreement

MT Make and trim

NTM Non Tariff Measure

NWFP Non-wood forest product

NWGS Non-wood goods and services

ODI Overseas Development Institute

OEM Original equipment manufacturers

PPP Purchasing Power Parity

R&D Research and Development

RMLIC Rest of Middle and Low Income Countries

RoHS Restriction on the Use of Hazardous Substances

ROW Rest of World

SFM Sustainable forest management

SICA Central American Integration System

SIECA Secretariat for Central American Economic Integration

SL Skilled labour

SMEs Small and Medium Enterprises

SPS Ssanitary and phytosanitary measures

SSS Short sea shipping

T&C Textiles and clothing

TEUs Twenty feet Equivalent Units

ToR Terms of Reference

TSIA Trade Sustainability Impact Assessment

UL Unskilled labour

UMIP Panama International Maritime University

UN United Nations

US United States

VA Value added

VPA Voluntary Partnership Agreements

WEEE Waste Electrical and Electronics Equipment Directive

WEI Water Exploitation Index

WTO World Trade Organisation

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 11

Annex I References

Abrahamson, Peter (2007). ‘Free Trade and Social Citizenship Prospects and Possibilities of the Central American Free Trade Agreement (CAFTA-DR)’ in Global Social Policy, Vol. 7, No. 3, 339-357;

Abrahamson, Peter (2008). ‘European Union influence on Central American Integration: The case of the coming Association Agreement’. Paper presented in the ISA RC 19th Annual Conference: The Future of Social Citizenship: Politics, Institutions and Outcomes, Stockholm, 4-6 September;

Asociación Coordinadora Indígena y Campesina de Agroforestería Comunitaria Centroamericana, (2008), “Carta de los pueblos indígenas y campesinos a los gobiernos de Centroamérica”, Managua: Hellen Ruíz; BCIE (CABEI), (2009), “Implicaciones de la crisis económica internacional para el sistema financiero Centroamericano”, Tegucigalpa; Blinova, Natalia, Nicolas Dorgeret and Razvan-Florian Maximiuc (2006),‘The EU in the Complex WTO’, Paper presented at WTO Seminar, Geneva, 11-13 May; Brockmeier, M. and J. Pekikan (2008), "Agricultural marketaccess: A moving target in the WTO negotiations?" Food Policy 33: 250–259. Cáceres Sinforiano, (2009), Hasta ahora, el AdA no nos sirve para nada; Carlos García, José (2007). Las relaciones comerciales entre Centroamérica y la Unión Europea. Secretaria de Integración Económica Centroamericana: Caracas;

CBI, (2008), “The fresh fruit and vegetable market in the EU”, on http://www.cbi.eu/marketinfo/cbi/docs/the_fresh_fruit_and_vegetables_market_in_the_eu;

CC-SICA (2007). Perspectivas hacia un Acuerdo de Asociación Propuestas para la negociación del Acuerdo de Asociación Europa Centroamérica, desde la Sociedad Civil Centroamericana. Resultados del II Foro Sociedad Civil Centroamérica Europa. Comité Consultivo – Sistema de la Integración Centroamericana: Tegucigalpa, Marzo;

CC-SICA (2009). Propuesta estrategica de la sociedad civil de Nicaragua ante el Acuerdo de Asociación entre Centroamérica y la Unión Europea.

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 12

CC-SICA Nicaragua (2009), “Balance de las negociaciones del Acuerdo de Asociación entre la Unión Europea y Centroamérica”; Central American Women´s Network, (2009), “El Acuerdo de Asociación entre la Unión Europea y Centroamérica: su posible impacto en la vida de las mujeres centroamericanas. Informe final de investgación”, DFID – DSID Departamento para el Desarrollo, Internacional del Gobierno Britanico; Centro Humboldt (2009), Programas de cooperación en materia ambiental para compensar las asimetrías de Nicaragua en el marco de las negociaciones del Acuerdo de Asociación entre CA-UE, Managua.; CEPA/CIFCA, (2007), “Posibles sectores perdedores en la Región Centroamericana y Panamá, de las negociaciones de un Acuerdo de Asociación con la Unión Europea (AdA)”, Oxfam Internacional y la Coalición Flamenca para la Cooperación Norte Sur; CEPAL, (2007), “Anuario estadístico de América Latina y el Caribe”, Santiago de Chile; Céspedes, Oswald and Juan José Flores (eds) (2007). ‘El Acuerdo de Asociación entre Centroamérica y la Unión Europea: sus tres pilares’ in Jornada anual de la Academia de Centroamérica. Friedrich Naumann Stiftung: San José; CEPA, 2007. The Central American Agricultural Sector in the run-up to negotiations for the EAA with the European Union: Potential Conflicts and Scenarios

Clark, Ximena & Dollar, David & Micco, Alejandro, 2004, "Port efficiency, maritime transport costs, and bilateral trade," Journal of Development Economics, Elsevier, vol. 75(2), pages 417-450; Coronado Marroquín, Jorge, El Acuerdo de Asociación Union Europea/Centroamérica: Mas que un espejismo una propuesta neoliberal expoliadora, Costa Rica: Alianza Social Continental; Council of the European Union, (2006), ‘II, UE – Central American Summit’ in Joint Communiqué, May, Vienna;

DG Environment, (2008), “Forest Law Enforcement, Governance and Trade (FLEGT)”, found on the DG Environment website: http://ec.europa.eu/environment/forests/flegt.htm;

DG Trade, (2008), “DG Trade Statistics, Top Trading Partners”, Eurostat; EC – External Trade, (2006), Handbook for Trade Sustainability Impact Assessment, available at http://trade.ec.europa.eu/doclib/docs/2006/march/tradoc_127974.pdf EC, (2003), ‘Central American Integration: What’s Next?’ available at http://www.sice.oas.org/TPD/CACM_EU/Studies/integen1203_e.pdf EC, (2007), ‘EU-Central America Regional Strategy Paper 2007-2013’ available at http://ec.europa.eu/external_relations/ca/rsp/07_13_en.pdf

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 13

EC, (2008), ‘EU Trade with the World / EU Trade with Central America’ available at http://trade.ec.europa.eu/doclib/docs/2006/september/tradoc_113478.pdf EC, (2008), Europe in Figures: Eurostat Yearbook 2008, Luxembourg: Office for Official Publications of the European Communities, available at http://epp.eurostat.ec.europa.eu/cache/ity_offpub/ks-cd-07-001-intro/en/ks-cd-07-001-intro-en.pdf EC Political Dialogue and Cooperation Agreement with Central America, (2003) (Multilateral agreement, 15/12/2003) available at http://ec.europa.eu/external_relations/ca/pol/pdca_12_03_en.pdf EC, (2007), “Guatemala, Country Strategy Paper – 2007-2013”, E/2007/480;

EC, (2008), “EU Bilateral Trade and Trade with the World : Central America”, available at http://trade.ec.europa.eu/doclib/docs/2006/september/tradoc_113478.pdf accessed May 2009;

ECLAC, (2009), Foreign Direct Investment in Latin America and the Caribbean in 2008; ECLAC, (2007), “Foreign Investment in Latin America and the Caribbean”, available at http://www.eclac.org/publicaciones/xml/1/32931/lcg2360i.pdf accessed May 2009;

EIA, (various), ‘Boletín del Proyecto Evaluación de Impacto Ambiental en Centroamérica’ available at www.iucn.org;

Electra, (2008), “Twenty Solutions for growth and investment to 2020 and beyond”

Estrella Pineda, (2008), “Maquilas. Labor slavery of XXIst Century”, www.ccoo.cat/maquila accessed 14 April, 2009;

ETUC/ITUC, (2007), ETUC/ITUC Statement of Trade Union Demands Relating to Key Social Elements of ‘Sustainable Development’ Chapters in European Negotiations on Free Trade Agreements (FTAs); Eurochambres, (2008) Economic Obstacles for EU-Latin American cooperation: The view of the private sector;

European Commission, (1990), “Directive 90/219/EC on the contained use of genetically modified micro-organisms”, Official Journal of the European Union, No. C 96, 17. 4;

European Commission, (1991), “Directive 91/493/EEC laying down the health conditions for the production and the placing on the market of fishery products; Official Journal of the European Union, L 268, pp. 15-34;

European Commission, (2001), “Directive 2001/18/EC on the deliberate release into the environment of genetically modified organisms, Official Journal of the European Communities, L 106/1;

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 14

European Commission, (2003), “Directive 2003/30/EC of the European Parliament and of the Council on the promotion of the use of biofuels or other renewable fuels for transport”, Official Journal of the European Union, L 123/42;

European Commission, (2003), “Regulation (EC) 1829/2003 on genetically modified food and feed”, Official Journal of the European Union, L 268/1;

European Commission, (2003), “Regulation (EC) 1946/2003 on transboundary movements of genetically modified organisms”, Official Journal of the European Union, L 287/1;

European Commission, (2005), “Council Regulation (EC) No 2173/2005 of 20 December 2005 on the establishment of a FLEGT licensing scheme for imports of timber into the European Community”, Official Journal of the European Union, L 347/1;

European Commission, (2006), “COM (2006) 71 final, Report on equality between women and men – 2006”, Brussels;

European Commission, (2007), “Communication from the Commission on the Mid-term review of the Sixth Community Environment Action Programme, COM (2007) 225 final”, Brussels;

European Commission, (2009), “Com (2009) 8 final, Strategic Goals and Recommendations for the EU’s Maritime Transport Policy until 2018”, Brussels;

European Commission, (2009), “EU and Central America pursue negotiations for an AA; €15 million EC assistance package for regional integration announced”, EU press release accessed February 2009 at http://europa.eu/rapid/pressReleasesAction.do?reference=IP/09/119&format=HTML&aged=0&language=EN&guiLanguage=en;

European Commission, DG Enterprise, Maritime, at http://ec.europa.eu/enterprise/sectors/maritime/shipbuilding/index_en.htm;

European Environment Agency, (2007), “Europe’s Environment: The Fourth Assessment”, Copenhagen;

European Environment Agency, (2008), “Core Sustainability Indicators”;

European Monitoring Centre on Change, (2008), “Trends and drivers of change in the European textiles and clothing sector: Mapping report.”;

European Sustainable Energy Review, Issue 4, 2008 page 5;

Eurostat, (2009), “Press release: EU27 Foreign Direct Investment”;

Eurostat, 2008, “Comext, Statistical Regime 4”, DG Trade;

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 15

Expertise Centrum voor Duurzame Ontwikkeling (ECDO), (2006), “Size does matter - The possibilities of cultivating Jatropha curcas for biofuel production in Cambodia”, Universiteit van Amsterdam

FAO, (2009), “State of the World’s Forests – 2009”;

FAOSTAT (2007), “Production of Fruits and Vegetables Shares in the World”;

FAOSTAT, website: http://faostat.fao.org/default.aspx;

Figini and Görg, (2006), “Does FDI Affect Wage Inequality? An Empirical Investigation”, Bonn: IZA Discussion Paper;

Framework Cooperation Agreement between the European Economic Community and the Republics of Costa Rica, El Salvador, Guatemala, Honduras, Nicaragua and Panama, 22 February 1993;

Francois and Hall, (2003), “Global Simulation Analysis of Industry-level Trade Policy”, http://www.intereconomics.com/handbook/Models/Spreadsheet%20Models/GSIMpaper.pdf;

Francois, J.F, B. Hoekman, and J. Woerz (2007), ‘Does Gravity Apply to Nontangibles: Trade and FDI Openness in Services,’ plenary paper at the 2007 ETSG meetings, and an unpublished 2008 updated version; Francois, J.F. (1998), ‘Scale economies and imperfect competition in the GTAP model,’ GTAP consortium technical paper; Francois, J.F. (2001) The Next WTO Round: North-South stakes in new market access negotiations, CIES Adelaide and the Tinbergen Institute, Adelaide: CIES; Francois, J.F. and D.W. Roland-Holst (1997), ‘Scale economies and imperfect competition’, in J.F. Francois and K.A. Reinert, eds. (1997), Applied methods for trade policy analysis: a handbook, New York: Cambridge University Press; Francois, J.F., B. McDonald and H. Nordstrom (1996), ‘Trade liberalization and the capital stock in the GTAP model’, GTAP consortium technical paper; Francois, J.F., B.J. McDonald, and H. Nordstrom (1997), ‘Capital Accumulation in Applied Trade Models,’ in J.F. Francois, and K.A. Reinert, eds. (1997), Applied methods for trade policy analysis: a handbook, New York: Cambridge University Press; Francois. J.F., H. van Meijl and F. van Tongeren (2005), ‘Trade Liberalization in the Doha Development Round,’ in Economic Policy April: 349-391; Freedom Index, Heritage foundation and WSJ (2009) at www.heritage.org;

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 16

Gereffi, G.; Humphrey, J.; Kaplinsky, R. & Sturgeon, T.J., (2001), “Introduction: Globalisation, Value Chains and Development”, Special Issue IDS Bulletin, 32(2), pp.1-8;

GTAP V7.5 (pre-release, April 2008); Guisán Seijas, Mª Carmen, Karen Cis Rosales, and Sandra Neira Gómez (2003). ‘Relaciones internacionales de Centroamérica y procesos de integración económica’ in Observatorio de la Economía Latinoamericana, Grupo Eumed.net (Universidad de Málaga), Issue 7, May; Hall, R.E. (1988), ‘The relation between price and marginal cost in U.S. industry’, in Journal of Political Economy, Vol. 96, No. 5, pp. 921-947. Heldt, Sven (1977). ‘Las Relaciones entre America Latina y la Comunidad Económica Europea’ in Nueva Sociedad, Vol 31-32, July-October, 49-60;

Henson, S., Saqib, M. and D. Rajasenan, (2004), “Impact of Sanitary Measures on Exports of Fishery Products from India: The case of Kerala”, World Bank / IBRD, Agricultural and Rural Development Discussion Paper 17; Hernández González, Greivin (2007), “La Agricultura de Americal Central en Juego”, Utrecht: ICCO; Hertel, T. and M. Tsigas (1996), ‘The Structure of GTAP,’ in Hertel, T., ed., (1996), in Global Trade Analysis, Cambridge MA: Cambridge University Press; Hidalgo Celaré, Nidia (2008), “La privatización de los servicios de agua potable en Centroamérica: avances y perspectivas frente a los acuerdos de libre comercio”, San Salvador: Centro para la defensa del Consumidor;

http://rainforests.mongabay.com/20neotropical.htm

http://trade.ec.europa.eu/doclib/docs/2006/september/tradoc_113478.pdf http://www.centristpolicynetwork.org/pages_2005/06/white_paper_summary.pdf;

http://www.ilo.org/global/About_the_ILO/Media_and_public_information/Feature_stories/lang--en/WCMS_093879/index.htm;

ICAES and CCT (2006). Desafíos laborales para América Central de cara a la firma del Tratado de Libre Comercio con la Unión Europea. Instituto Centroamericano de Estudios Sociales and Confederación Centroamericana de Trabajadores; Instituto de Investigaciones Sociales (2008). Centroamérica InformADA. Proyecto: Seguimento de las relaciones comerciales entre Centroamérica y la Unión Europea. San José: University of Costa Rica;

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 17

ILO, (2004), “Analysis of Child Labour in Central America and Dominican Republic”;

ILO, (2008), “Decent Work Country Programme: Honduras”, at www.ilo.org;

ILO, (2009), “The cost of coercion”, International Labour Conference, 98th session;

ILO, (2008), Newsletter 6;

IMF, (2002), “Manual on Statistics for International Trade Services”, jointly published by UN, EC, IMF, OECD, UNCTAD and WTO;

Instituto Nacional de Estadisticas y Censos, website: http://www.inec.gov.ec/;

Leon A, Andres; Ramirez, Alonso y Dinatte Roberto, (2007), “El Sector Agricola Centroamericano de Cara al Acuerdo de Asociacion con la Union Europea: Posibles Escenarios”, CEPA;

Maquila Solidarity Network, (2009), “Was the Jerzees factory closed to get rid of the union?”, Maquila Solidarity Update, Volume, 14, No. 1.

Morazan, Pedro and Maria Negre (2008), ‘Analisis del Impacto del CAFTA en Honduras y Recomednaciones par alas Negociaciones de un Acuerdo de Asociación con la Unión Europea: Informe de la Consultoria para el Comisionado Nacional de los Derechos Humanos de Honduras.

OECD, (2008), “Foreign Direct Investment Statistics in OECD Countries”, available at http://www.oecd.org/dataoecd/24/35/2956455.pdf accessed May 2009;

Overseas Development Institute, (2004), “The Doha Development Agenda Impacts on Trade and Poverty”, accessed February 2009 at http://www.odi.org.uk/resources/specialist/doha-briefings/collection.pdf;

Political Dialogue and Cooperation Agreement between the European Community and its Member States for the one part, and the Republics of Costa Rica, El Salvador, Guatemala, Honduras, Nicaragua and Panama for the other part, Rome, Italy, 15 December 2003;

PROCOMER, (2008), “Análisis de las Estadísticas de Exportación Costa Rica, 2007”, Promotara del comercio esterior de Costa Rica, Dirección de Estudios Económicos;

Red Regional De Monitoreo De Los Impactos Del TLC Entre Centroamérica República Dominicana y Estados Unidos (2007). Impactos del TLC: Informe Preliminar de Monitoreo del TLC un año de entrada en vigencia, Varias organizaciones de Centroamérica con el apoyo de Oxfam Internacional.

Red Regional De Monitoreo De Los Impactos Del TLC Entre Centroamérica República Dominicana y Estados Unidos (2008). II Informe Regional Sobre los Impactos del DR-CAFTA en Centroamérica y Republica Dominicana. Varias organizaciones de Centroamérica con el apoyo de Oxfam Internacional.

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 18

Red Regional de Monitoreo del DR-CAFTA, (2008), “Editorial: Dos años y la misma tendencia del DR-CAFTA en Centroamérica y República Dominicana”, Guatemala; Rivoli, P., (2006), “The Travels of a T-Shirt in the Global Economy: An Economist Examines the Markets, Power, and Politics of World Trade”;

Sanchez-Ancochea, Diego, (2006), “Development Trajectories and New Comparative Advantages: Costa Rica and the Dominican Republic under Globalization”, World Development 34, No. 6. Elsevier: pp. 996-1015;

SICA, (2008), ‘Cooperación Regional Unión Europea-Centroamérica’ Suplemento Especial, available at http://www.sica.int/busqueda/Centro%20de%20Documentaci%C3%B3n.aspx?IDItem=29227&IdCat=50&IdEnt=55&Idm=1&IdmStyle=1 SICA. San José Dialogues, available at http://www.sice.oas.org/TPD/CACM_EU/Negotiations/2005SanJose_e.pdf SIECA, (2008), ‘Trade Relations between Central America and the European Union’, available at http://www.sieca.org.gt/site/VisorDocs.aspx?IDDOC=CacheING/17990000002662/17990000002662.swf SIECA, (2008), “Declaración de San José”;

Smakman, F., (2004), “Local Industry in Global Networks. Competitive Adjustment, Corporate Strategies and Pathways of Development in Singapore and Malaysia’s Garment Industry.”, PhD Thesis, Utrecht University, The Netherlands, Rozenberg: Amsterdam, (http://igitur-archive.library.uu.nl/dissertations/2004-0616-130904/inhoud.htm);

Smith, H (1995) European Union Foreign Policy and Central America, New York: St. Martin's Press. T&E (2002), European Federation for Transport and Environment, Safe and Sustainable Freight Transport – Our common challenge, available at http://www.transportenvironment.org/Publications/view/cid:515-start:10;

The Labor Dimension in Central America and the Dominican Republic available at http://www.centristpolicynetwork.org/pages_2005/06/white_paper_summary.pdf;

Trocaire (2008), El Aassociación de Acuerdo entre Centroamérica y la Unión Europea:¿Que es el cual será su posible impacto en la reducción de la pobreza y el desarrollo sostenibe de Centroamérica?, Maynooth: Trocaire.

UICN-ORMA (2009), Acuerdo de Asociación entre Centoamérica y la Comunidad Europea: Pago de Servicios Ambientales.

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 19

UNCTAD, (2008), “Review of Maritime Transport 2008”, available at http://www.unctad.org/en/docs/rmt2008_en.pdf;

UNCTAD, (2008), “World Investment Report”;

UNECE, (2005), “European Forest Sector Outlook Study, 1960-2000-2020, Main Report”, ECE/TIM/SP/20;

Van den Eynde-Coppin (2005) The Manufacture of electrical and electronic equipment in the EU, Statistics in Focus 6/2005, Eurostat;

WIDE (2002), ‘Gender and Trade Indicators’ in Wide Infosheet, February;

World Bank (2009), Doing Business Index;

World Bank, (2006), “The Impact of Intel in Costa Rica. Nine years after the Decision to Invest”, Washington, DC; World Development Report, (2009), “Reshaping Economic Development, Annex 1”; WTO, (2007), “Trade Policy Review Panama”, see http://www.wto.org/english/tratop_e/tpr_e/tp287_e.htm;

Zamora-Cordero, Maria (2006). Contexto internacional del comercio internacional “Centroamérica ante los retos de la globalización” in Acta Académica, May, available at http://www.uaca.ac.cr/actas/2006/Acta38/latinoamericano/Contexto.pdf

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 21

Annex II Overview Trends and Issues European Union and Central America

II.1 European Union – Central America Current Trade & Investment

II.1.1 Trade in Goods

The EU is the second biggest importer in the world, after the United States (US). In 2007, EU merchandise imports constituted 18.2 percent of world imports. In terms of exports, the EU is the world’s largest exporter, accounting for 16.5 percent of merchandise exports, followed by China and the US. In terms of total trade (imports + exports), the EU is the largest player, accounting for 17.4 percent of global total trade1. Figure II.1 presents developments during the last couple of years in EU trade with the rest of the world.

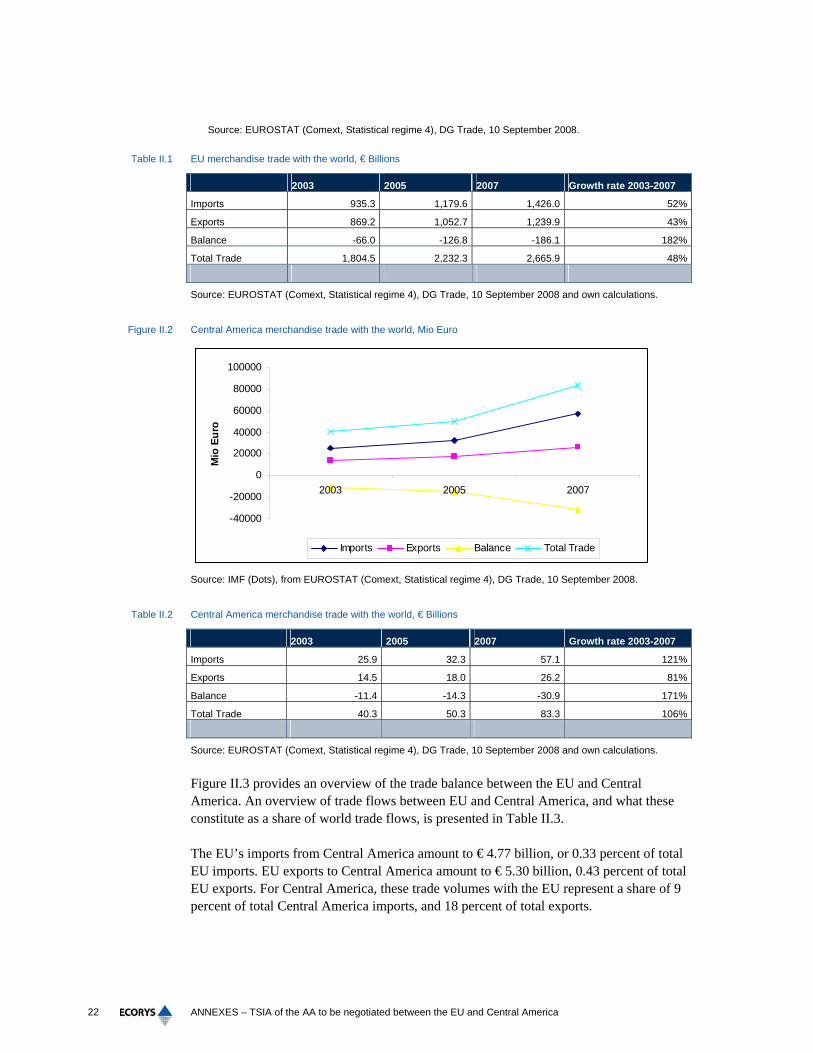

Imports, exports and total trade grew with almost 50 percent from 2003 - 2007. The EU trade balance is slightly negative and increased somewhat over past years (see Table II.1).

Table II.2 and Figure II.2 show the development of Central America (including Panama) merchandise trade with the world. Trade has more than doubled during recent years. In 2003, total merchandise trade was worth €40.3 billion and in 2007, this had reached €83.3 billion. Exports from Central America almost doubled during this time, but this increase was still lower than the increase in imports, implying that the negative trade balance increased considerably between 2003 and 2007.

Figure II.1 EU’s merchandise trade with the world, Mio Euro

-500000

0

500000

1000000

1500000

2000000

2500000

3000000

2003 2005 2007

Mio

Eur

o

Imports Exports Balance Total Trade

1 Source of the data: DG Trade Statistics.

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 22

Source: EUROSTAT (Comext, Statistical regime 4), DG Trade, 10 September 2008.

Table II.1 EU merchandise trade with the world, € Billions

2003 2005 2007 Growth rate 2003-2007

Imports 935.3 1,179.6 1,426.0 52%

Exports 869.2 1,052.7 1,239.9 43%

Balance -66.0 -126.8 -186.1 182%

Total Trade 1,804.5 2,232.3 2,665.9 48%

Source: EUROSTAT (Comext, Statistical regime 4), DG Trade, 10 September 2008 and own calculations.

Figure II.2 Central America merchandise trade with the world, Mio Euro

-40000

-20000

0

20000

40000

60000

80000

100000

2003 2005 2007

Mio

Eur

o

Imports Exports Balance Total Trade

Source: IMF (Dots), from EUROSTAT (Comext, Statistical regime 4), DG Trade, 10 September 2008.

Table II.2 Central America merchandise trade with the world, € Billions

2003 2005 2007 Growth rate 2003-2007

Imports 25.9 32.3 57.1 121%

Exports 14.5 18.0 26.2 81%

Balance -11.4 -14.3 -30.9 171%

Total Trade 40.3 50.3 83.3 106%

Source: EUROSTAT (Comext, Statistical regime 4), DG Trade, 10 September 2008 and own calculations.

Figure II.3 provides an overview of the trade balance between the EU and Central America. An overview of trade flows between EU and Central America, and what these constitute as a share of world trade flows, is presented in Table II.3.

The EU’s imports from Central America amount to € 4.77 billion, or 0.33 percent of total EU imports. EU exports to Central America amount to € 5.30 billion, 0.43 percent of total EU exports. For Central America, these trade volumes with the EU represent a share of 9 percent of total Central America imports, and 18 percent of total exports.

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 23

Figure II.3 EU trade balance with Central America, Mio euro, 2007

47655297

532

10062

0

2000

4000

6000

8000

10000

12000

2007

Mio

eur

o

Imports Exports Balance Total Trade

Source: EUROSTAT (Comext, Statistical regime 4), DG Trade, 10 September 2008.

Table II.3 EU- Central America trade as share of total EU/ Central America trade

Share of total trade

Flow EU from/to Central America Central America from/to EU

Imports 0.33% 9.28%

Exports 0.43% 18.20%

Total trade 0.38% 12.08%

Source: EUROSTAT (Comext, Statistical regime 4), DG Trade, 10 September 2008 and own calculations.

Whereas the EU’s and Central America’s total trade with the world increased by 48 and 107 percent respectively from 2003 – 2007 (Table II.1 and Table II.2), total trade between the EU and Central America increased by just 28 percent over the same period. For Central America, the EU is the fourth major import partner, the second major export partner and the second major total trade partner, after the US. For the EU, Central America does not belong to its top 20 major import, export or total trade partners.

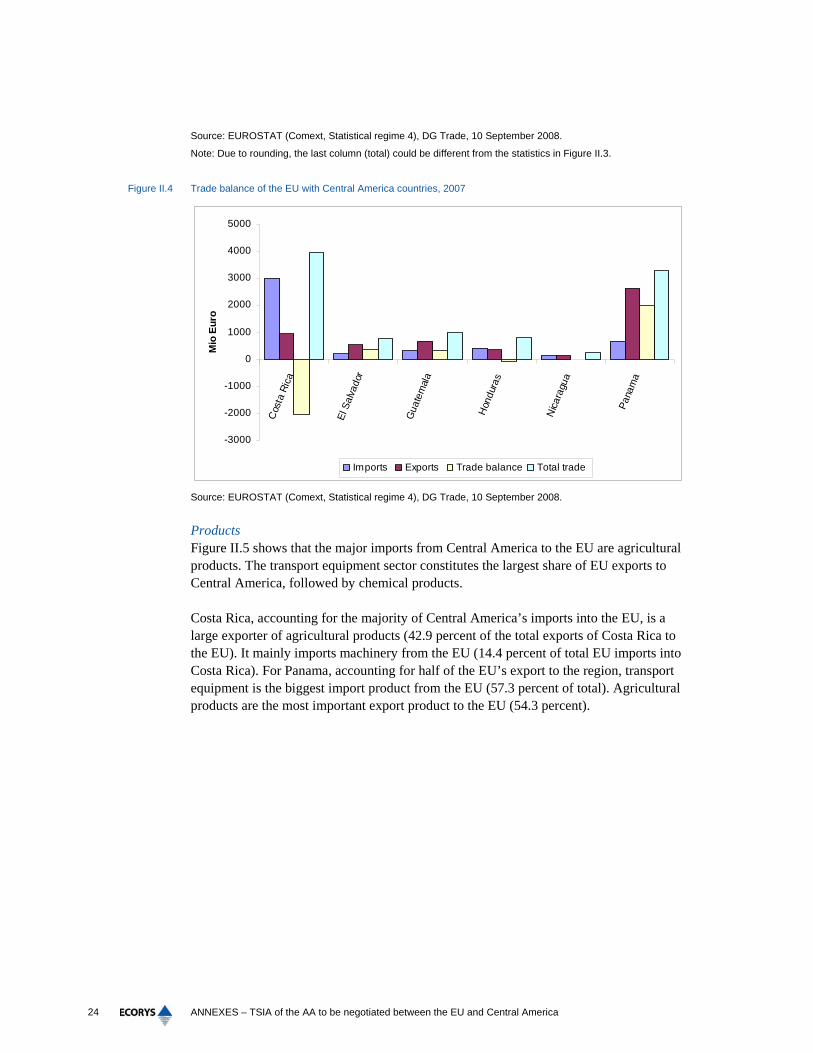

Costa Rica and Panama At country-level, Costa Rica and Panama are the EU’s main trading partners (see Table II.4 and Figure II.4). In 2007, Costa Rica was the main import partner for the EU, accounting for 63 percent of Central America’s imports into the EU. Panama was the largest export partner, accounting for 49 percent of total.

Table II.4 EU merchandise trade with Central America countries in Mio euro, 2007

Costa Rica El Salvador Guatemala Honduras Nicaragua Panama Total

Imports 2,998 196 333 434 144 660 4,765

Exports 966 557 667 349 130 2,629 5,298

Trade balance -2,032 360 334 -85 -14 1,969 532

Total trade 3,963 753 1,000 783 273 3,289 10,061

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 24

Source: EUROSTAT (Comext, Statistical regime 4), DG Trade, 10 September 2008.

Note: Due to rounding, the last column (total) could be different from the statistics in Figure II.3.

Figure II.4 Trade balance of the EU with Central America countries, 2007

-3000

-2000

-1000

0

1000

2000

3000

4000

5000

Cos

ta R

ica

El S

alva

dor

Gua

tem

ala

Hon

dura

s

Nica

ragu

a

Pana

ma

Mio

Eur

o

Imports Exports Trade balance Total trade

Source: EUROSTAT (Comext, Statistical regime 4), DG Trade, 10 September 2008.

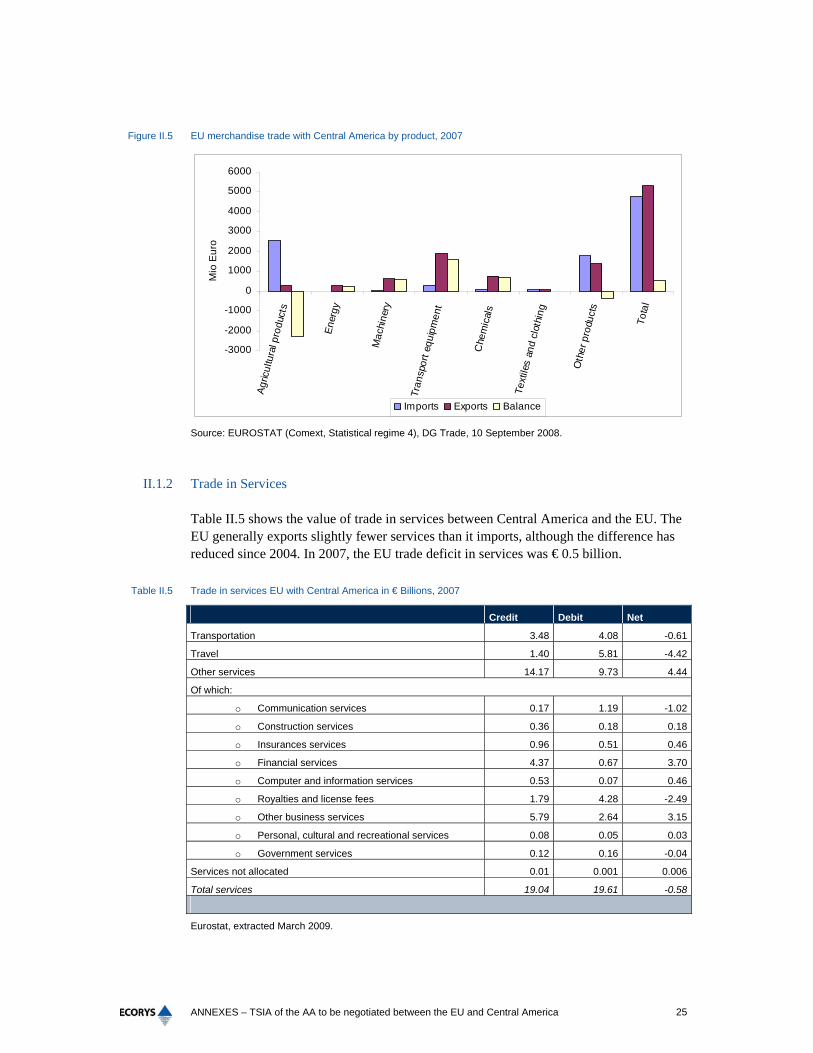

Products Figure II.5 shows that the major imports from Central America to the EU are agricultural products. The transport equipment sector constitutes the largest share of EU exports to Central America, followed by chemical products. Costa Rica, accounting for the majority of Central America’s imports into the EU, is a large exporter of agricultural products (42.9 percent of the total exports of Costa Rica to the EU). It mainly imports machinery from the EU (14.4 percent of total EU imports into Costa Rica). For Panama, accounting for half of the EU’s export to the region, transport equipment is the biggest import product from the EU (57.3 percent of total). Agricultural products are the most important export product to the EU (54.3 percent).

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 25

Figure II.5 EU merchandise trade with Central America by product, 2007

-3000

-2000

-1000

0

1000

2000

3000

4000

5000

6000

Agric

ultu

ral p

rodu

cts

Ener

gy

Mac

hine

ry

Tran

spor

t equ

ipm

ent

Che

mic

als

Text

iles

and

clot

hing

Oth

er p

rodu

cts

Tota

l

Mio

Eur

o

Imports Exports Balance

Source: EUROSTAT (Comext, Statistical regime 4), DG Trade, 10 September 2008.

II.1.2 Trade in Services

Table II.5 shows the value of trade in services between Central America and the EU. The EU generally exports slightly fewer services than it imports, although the difference has reduced since 2004. In 2007, the EU trade deficit in services was € 0.5 billion.

Table II.5 Trade in services EU with Central America in € Billions, 2007

Credit Debit Net

Transportation 3.48 4.08 -0.61

Travel 1.40 5.81 -4.42

Other services 14.17 9.73 4.44

Of which:

o Communication services 0.17 1.19 -1.02

o Construction services 0.36 0.18 0.18

o Insurances services 0.96 0.51 0.46

o Financial services 4.37 0.67 3.70

o Computer and information services 0.53 0.07 0.46

o Royalties and license fees 1.79 4.28 -2.49

o Other business services 5.79 2.64 3.15

o Personal, cultural and recreational services 0.08 0.05 0.03

o Government services 0.12 0.16 -0.04

Services not allocated 0.01 0.001 0.006

Total services 19.04 19.61 -0.58

Eurostat, extracted March 2009.

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 26

In 2007, Central America accounted for 1.8 percent of EU trade (imports + exports) in services; see Figure II.6 and Table II.6. Intra-EU trade (accounting for by far the largest part of EU services trade) is included in Others.

Figure II.6 Central America share of EU 27 total (imports + exports) trade in services, 2007

US Sw itzerland Latin America Central America Japan Others

Source: Eurostat, extracted March 2009-03-31

Table II.6 EU’s trade in services with partners, € Billions, 2007

Credit Debet Net

Total (credit +

debet)

Percentage

(total trade)

US 139.1 127.7 11.4 266.9 12.1%

Switzerland 61.5 44.0 17.5 105.5 4.8%

Latin America 23.3 17.4 5.9 40.6 1.8%

Central America 19.0 19.6 -0.6 38.7 1.8%

Japan 19.4 13.8 5.6 33.2 1.5%

Others 915.8 814.5 101.3 1,730.3 78.1%

World 1,178.1 1,037.0 141.1 2,215.1 100.0%

Source: Eurostat, extracted March 2009-03-31

It is also important to mention the current account deficits which the Central American countries currently have. In the case of Nicaragua in particular, the deficit is considered to be unsustainable (see Table II.7).

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 27

Table II.7 Central American current account deficits as percentage of GDP

Current account deficits 2007 2008

Belize -4,0% -7,6%

Costa Rica -6,2% -8,1%

El Salvador -0,9% -4,6%

Guatemala -5,1% -4,6%

Honduras -9,9% -11,8%

Nicaragua -18,3% -25,8%

Panama -7,3% -9,1%

Source: ECLAC.

II.1.3 Investment

Table II.8 below shows the levels of foreign direct investment (FDI) between the EU and Central America. EU outflows are much higher than inflows and fluctuate vastly from year to year. In recent years, inflows into the EU have risen substantially.

Table II.8 EU FDI with Central America, Bn. Euros

Year Inflows Outflows Balance

2004 -0.6 36.1 36.7

2005 2.4 8.5 6.2

2006 17.8 30.2 12.4

Source: EUROSTAT.

II.2 European Union – Central American Relations and Relevant Agreements

The EU and Latin America have had enhanced links since the 1960s and today, their relationship is important for both regions, politically as well as economically. Below, a short overview is given of the EU- Central America AA under consideration here and its aims, as well as some other agreements relevant in this context.

Box II.1 AA EU – Central America republics

Plans for an EU-Central America AA were formed at the 2006 EU-Latin America Summit in Vienna, Austria.2 It

was decided that the agreement would encompass the three pillars of political dialogue, cooperation

programmes and a FTA, and negotiations on these pillars began in mid-2007 with Guatemala, El Salvador,

Nicaragua, Honduras and Costa Rica. Panama is not included in these negotiations due to the fact that the

country is not yet a member of the SIECA (Secretariat for Central American Economic Integration).

2 Declaration of Vienna from the IV EU-LAC Summit, Vienna, Austria, 12 May 2006.

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 28

Political Dialogue pillar

The San José Dialogues between the EU and Central America started in 1984 with the aim of reaching a

peaceful end to the civil conflicts in the region, by way of dialogue and negotiations mediated by Europe. The

last San José Dialogue meeting took place in 2007.3 Now, the EU holds a summit with the Latin American and

Caribbean countries every two years, and in the other year, the EU meets with the Rio Group. There is a new

EU-Central America Political Dialogue and Cooperation Agreement4 which must be ratified by the EU Member

States. This aim of the agreement is to deepen relations between the regions and set the stage for an effective

AA.

Cooperation Programmes pillar

Aside from the San José Dialogues’ political dialogue component, a cooperation programme was also created

at that time to help with the economic effects of the conflicts. The 1993 Framework Cooperation Agreement5

focused on human rights and democracy, rural development, disaster reconstruction, social development and

regional integration. €145 million was granted by the EU for this purpose between 1995 and 2005. Other EU

cooperation initiatives have included a reconstruction programme after Hurricane Mitch, support for Small and

Medium Enterprise (SME) development, and support for food security, environmental conversation and human

rights. In 2001, a five-year regional programme of cooperation was signed by the EU and Central America for a

total of €655 million with a strong focus on regional integration. In 2008, the EU launched a second ‘Programme

of Support to Central American Regional Integration’ with the aim of strengthening the Central American

Integration System (SICA) institutional system by making it more transparent and open, and increasing civil

society participation and information dissemination to the public. A Joint Committee and Sub-Committee for

Cooperation also meet regularly to discuss these various issues.6

Trade Agreement pillar

A FTA is currently being negotiated between the EU and the Central American countries with the aim of going

beyond World Trade Organisation (WTO) rules. The two sides have been meeting to discuss several issues in

twelve sub-groups. It is hoped that the negotiations will be completed within 2009. An important part of the AA in

general and the FTA in particular is Sustainable Development. A Trade and Sustainable Development Chapter

is envisaged within the FTA, which will reflect International Labour Organisation (ILO) core labour standards;

facilitate and promote trade in environmentally-friendly goods and services, integrate environmental, labour and

social considerations into the FTA and encourage a transparent and cooperative agreement.7

Box II.2 Other agreements relevant for EU – Central America relations

The model incorporates all trade agreements which have been implemented by both regions to date. What

follows is a selection of these.

3 San José Dialogue Ministerial Meeting between the European Union Troika and the Ministers of the Countries of Central

America, Santo Domingo, Dominican Republic, 19 April 2007. 4 Political Dialogue and Cooperation Agreement between the European Community and its Member States for the one part,

and the Republics of Costa Rica, El Salvador, Guatemala, Honduras, Nicaragua and Panama for the other part, Rome, Italy, 15 December 2003.

5 Framework Cooperation Agreement between the European Economic Community and the Republics of Costa Rica, El Salvador, Guatemala, Honduras, Nicaragua and Panama, 22 February 1993.

6 EU and Central America pursue negotiations for an AA; €15 million EC assistance package for regional integration announced, EU press release accessed February 2009 at http://europa.eu/rapid/pressReleasesAction.do?reference=IP/09/119&format=HTML&aged=0&language=EN&guiLanguage=en

7 Discussion Paper on Sustainable Development for the Association Agreement between the EU and Central America.

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 29

Doha Development Agenda (DDA)

The Doha Development Agenda is the current WTO negotiation round which started in November 2001. The

round has met several obstacles as the developed and developing world clash over issues such as agriculture,

pharmaceuticals patenting, special and differential treatment for developing countries and the difficulties

developing countries have had in implementing trade agreements. Recent negotiations in July 2008 also broke

down but talks are expected to resume in 2009. The Central American countries would stand to gain

substantially, if subsidies on agricultural products such as sugar were to be reduced by the developed world.8

For its part, the EU has included the abolition of farming export subsidies completely and has campaigned for

the inclusion of a package of development measures in the final round agreement.

EU – LAC Summit

A summit between the European Union and the Latin American and Caribbean countries has taken place every

two years since 1999. The main issues to be tackled at these summits include social cohesion, drugs, migration

and relations with civil society. Results of the talks include for example the 2005 Communication on a Stronger

Partnership between the European Union and Latin America and the Regional Strategy Paper 2007-2013 which

defines regional development cooperation programmes.

GSP (Plus)

Commercial relations between the EU and the Central America are dominated by the Generalised System of

Preferences (GSP) which was introduced by the EU in 1971. This arrangement provides duty-free access to EU

markets for all industrial products from Central America as well as some agricultural products. It also has a

provision for combating drug production and trafficking. A new GSP Plus regime came into effect in 2005 aimed

at poorly diversified economies. It also demanded the ratification and effective implementation of several

international (social, labour, environmental, good governance) conventions in order to qualify.

CAFTA

The Dominican Republic-Central American Free Trade Agreement (DR-CAFTA) is between the US and

Guatemala, El Salvador, Honduras, Nicaragua, Costa Rica and the Dominican Republic. Negotiations took

place from January 2003 – March 2004 and the agreement was ratified and implemented by most countries in

2006 (2008-9 in Costa Rica). Although it is early days, the first indications by a World Bank Report9 are that

there are some positive effects of this agreement for the Central American countries given their increased

market access to the US (particularly for the food processing industry10), and the US has also benefited through

expanded export markets for food, petroleum products and machinery.11 As a result of DR-CAFTA negotiations,

a White Paper was published in 2005 by the Ministers responsible for trade and labour in DR-CAFTA countries

in which they identified key areas for improving workers rights, enhancing capacity and promoting compliance

with labour standards.12 Similar commitments will be part of the EU- Central America AA Sustainable

Development Chapter.

8 The Doha Development Agenda Impacts on Trade and Poverty accessed February 2009 at

http://www.odi.org.uk/resources/specialist/doha-briefings/collection.pdf 9 Jaramillo, Carlos Felipe and Daniel Lederman (2006) Challenges of CAFTA, Washington DC: World Bank. 10 Red Regional de Monitoreo DR-CAFTA (2007), Impactos del TLC: Informe Preliminar. 11 Source: United States of America Department of Commerce available at www.buyusa.gov 12 The Labor Dimension in Central America and the Dominican Republic available at

http://www.centristpolicynetwork.org/pages_2005/06/white_paper_summary.pdf.

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 30

II.3 Sustainability issues in the European Union

This section highlights the main economic, social and environmental issues for the EU that are most relevant in the context of this EU – Central America AA, taking the sustainability indicators into account.

II.3.1 Main economic issues European Union

• Real income o With a GDP of €12,353 billion (at market prices), the EU is the largest economy in the

world. GDP per capita in the EU27 is €24,900 (2007, at market prices). There are some differences between Members States: while Luxembourg’s GDP per capita is three times higher than EU average, Bulgaria has a value of €3,800. In 2007, the growth rate of GDP per capita in the EU27 was 2.7 percent;

o The inflation rate in the EU is low and rather stable; it fluctuated around 2 percent since 2000. In 2007, the inflation rate was 2.3 percent;

o The tertiary sector accounts for the largest part of value added generated by the EU economy; all EU Member States have a services value added of more than 50 percent of GDP in 2006, ranging from 52 percent (Romania) to 85 percent (Luxembourg). This share has been growing substantially over the past years. Agriculture value added (as a percentage of GDP) in 2006, ranged from 0 percent in Luxembourg to 11 percent in Romania. For Industry value added (as a percentage of GDP) again Luxembourg had the lowest value of 15 percent (2006) and in Czech Republic the highest value added was observed, 39 percent (2006).13

• Investment o Total investment in the EU27 amounted to 21.3 percent of GDP in 2007, the largest share

coming from business investment (18.7 percent), while public investment accounted for the rest;

o While the lion share of EU investment is done inside the EU, the average value of inward and outward FDI flows stood at 3.4 percent of GDP in 2007, which makes the EU the largest foreign investor worldwide, followed by the US.

• Trade o Trade is of significant importance for an open economy like the EU. Merchandise imports

amounted to €1,426 billion in 2007 and merchandise export to €1,234 billion, implying that the EU is running a trade deficit for merchandise;

o Trade in services accounted for a large share of total trade and this share has been growing in importance in the trade decomposition for the EU. In 2007, the EU27 had a positive (and increasing) trade balance in services of €147 billion, with imports of services amounting to €1,073 billion and exports to €1,221 billion.

13 Source: World Development Indicators

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 31

II.3.2 Main social issues European Union

• Employment and labour issues o The unemployment rate in the EU-27 decreased from 9 percent in 2003 to 7 percent in

2008. The long term unemployment rate in the EU-27 was 3 percent in 2007. Participation in the labour force has risen since the mid-1980s from just under 66 percent to 70.1 percent in 2006. Self-employment in the EU27 decreased from 18.2 percent in 1995 to 14.1 percent in 2007;

o The labour productivity growth rate in the EU15 is modest (i.e. compared to the US). Yet the labour cost and wages and salaries in the EU25 have been increasing since 2000 (both by around 28 percent);

o In only 8 Member States more than 50 percent of the employed population is member of a trade union. The objectives of the ILOs Decent Work Agenda are prevalent in Europe at the moment. The EU has recently had discussions with the ILO on creating a regional minimum wage in these times of crisis, as well as extending social security.14

• Poverty and (gender) equality o 16 percent of the households in the EU lives with 60 percent of the EU median income

(defined as households at-risk-of poverty). This share varies between the Member States. In 2007, the income inequality (Gini-index) was 0.30 for the EU, ranging between 0.23 and 0.37 for individual Member States;

o With respect to gender equality, the employment rate gap between men and women declined to 14.2 points in 2007. Women are involved more in traditional “female” activities, work more in part-time and there is still a significant pay gap between men and women. Generally, women are at greater risk of social exclusion and poverty than men. Yet, enrolment in primary and secondary education is 90 percent or higher within the EU both for boys and girls and enrolment in tertiary education is higher for females.

• Health o Life expectancy at birth equals 78.4 years for the EU27 (2005). In general, life

expectancy is lower in the Eastern European countries. Both infant and maternal mortality rates in the EU have declined steadily over the past decades;

o The coverage and access to health care services are broadly guaranteed to all inhabitants in most Member States. However, the situation for disadvantaged groups is a point of interest in the EU. Most of the EU population also has access to good quality water and sanitation. The main focus of the EU nutritional policy is ‘overweight’ and ‘obesities’.

• Education o The enrolment in primary and secondary education is over ninety percent. In general in

Northern and Western Europe enrolment is close to hundred percent. In 2004, a little more than 15 percent of all those enrolled in education were in tertiary education in the EU27;

o Between 10-20 percent of the population in the EU is functional illiterate; in the New Member States functional illiteracy is a bit higher (up to 30 percent). 14 ILO Brussels Newsletter, November 2008.

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 32

II.3.3 Main environmental issues European Union15

• Atmosphere o Regarding climate change mitigation, the EU in 2007 made a firm independent

commitment to achieve at least 20 percent reduction of greenhouse gas (GHG) emissions by 2020 compared to 1990. In addition to substantial emissions reductions at home, the countries can also use Kyoto Mechanisms like CDM for off-setting;

o With respect to adaptation to climate change, some extremes of heat and drought, rain and flooding are affecting parts of Europe. Draughts and consecutive water shortages especially in Spain, Italy and Greece are growing;

o Issues of air pollution and accumulation of hazardous substances in the atmosphere directly link to health concerns; this also holds for drinking water quality, contamination of soil and food security.

• Biodiversity, Land & Fresh and waste water o Concerns with respect to maintaining Europe’s biodiversity and carrying capacity of

ecosystems are growing. Increased attention is present for the issue of sustainability of production, consumption and trade in the globalized economy;

o Similarly, with respect to the use of natural resources, an increased urgency regarding the need to reduce the ecological footprint in order to regain long term sustainable development is perceived;

o Although 80 percent of Europeans live in big cities, towns or urban settlements, the rural landscape has a large significance in terms of providing food, raw materials, fuel and recreational opportunities. Farmers manage half of the EU's land area and agriculture uses half of the water available in southern Europe. In magnitude, farming causes almost half of the nitrogen pollution in rivers, 94 percent of ammonia emissions and 9 percent of total GHG emissions;

o With respect to the marine environment, overuse of marine resources, considerable pollution and extinction of species has become a continuous point of concern in many coastal waters of Europe.

• Environmental quality o Energy is an important strategic issue at present for the EU. Key drivers are security of

supply, efficient use of energy, promotion of energy saving and increasing the share of renewable energy production. In 2008 the EU set targets to increase the share of renewable energy by 20 percent and improve energy efficiency by 20 percent by 2020. However, the switch from fossil fuels to bio-energy bears considerable environmental risks, mainly in terms of land-use change and overall balance of GHG emissions;

o An eco-efficient economy can not be reached without reducing the amount of raw materials used and waste generated during the life cycle of products. Responsible consuming requires recycling of materials; however, global transfers of waste streams are a concern.

15 The environmental issues and trends for the EU27 reflect the current state of the environment in the EU and are prioritized

in line with the relevance to the current environmental policy debate in Europe. See: EEA Signals 2009/3 Key Environmental Issues Facing Europe, EEA Copenhagen 2009.

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 33

II.4 Sustainability issues in Central America

This section highlights the main economic, social and environmental issues for the Central American republics that are most relevant in context of this EU – Central America AA.

II.4.1 Main economic issues Central America

• Real income o Costa Rica and Panama are considered upper-middle income countries; El Salvador,

Guatemala, Honduras and Nicaragua are lower middle income countries.16; GNI per capita is highest in Costa Rica and Panama ($5,560 and $5,510; Nicaragua has the lowest GNI per capita ($980). In PPP terms, GDP per capita is also highest in Costa Rica, followed by Panama. Nicaragua and Honduras have the lowest GDP per capita in PPP ($3,674 and $3,430).

o For Costa Rica, Panama, El Salvador and Guatemala, the secondary and tertiary sectors represent the major part of the value added in the economy17, while for Honduras and Panama, the agricultural sector still has a relatively more important economic weight. For example in Costa Rica, the structural transformations from the agro-export model to a new economic model since the 1980s has diminished dependence of on agriculture significantly, while in contrast, in Nicaragua and Honduras e.g. lack of technology dissemination, human capital and labour opportunities has inhibited a similar process;

o Reduction of inflation, roughly around 10 percent in the Central American republics, is considered one of the main issues for the governments, especially in Honduras, Nicaragua and Guatemala, considering their high levels of poverty (and inflation affecting consumer purchasing power). The Panama and El Salvador monetary system are dollarized which kept inflation relatively low, until food and other import goods started rising from 2007 onwards. Monetary policy in most republics is closely linked with internal debt issues and fiscal management.

• Investment o Though few reliable data are available, fixed capital formation (from National Accounts)

is roughly around 25 percent in the region; o CAFTA has stimulated productive investment in the export sectors. Yet, issues like

security concerns, lack of skilled workers and poor infrastructure hamper FDI in reaching the expected or desired levels;

o Especially Panama and Costa Rica received significant amounts of FDI in recent years ($2.57 billion and $1.47 billion in 2006, respectively), mainly directed to services and linked to a skilled labour force. Nicaragua’s low levels of FDI ($0.28 billion) suggest that the country’s lower levels of human capital and less attractive business environment make the country less attractive for FDI.

16 According to the World Bank classification. 17 For example, in Costa Rica the service sector represents 60 percent of the economy (mainly driven by tourism), in Panama

77 percent (mainly financial and transport services).

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 34

• Trade o The EU is the second most important external trade partner for the Central American

region, after the US. From the six countries, Costa Rica and Panama are most internationally oriented trade partners, both towards the EU and the US. These countries generally have a relatively more diversified (yet still poorly) export package, and have better terms of trade18 than the other countries;

o Regional economic integration remains a crucial factor in stimulating trade potential for the region, but does not go without difficulties. For example, as of yet Panama has not signed the Protocol for Central American Economic Integration (SIECA), which was considered by the EC as a sine qua non for Panama as a cosignatory in an AA between the two blocks. In addition, even without this country in SIECA, not all Central American countries apply uniform external import tariffs in trading with the world;

o In addition to trade in goods and services, family remittances are fairly important in the balance of payments of the Central American economies. For most countries, they represent more than half the value of total exports (in El Salvador even 83 percent). Remittances only play a minor role in the external sector of Costa Rica (5 percent of exports). The main source of remittances in Nicaragua is unskilled migrants working in Costa Rica’s agriculture, construction or service sectors. Due to the general economic crisis, especially in the United States and Spain, which receive most of the Latin-American immigrants, these remittances are decreasing , which will have a direct impact during the next years on families that depend on remittances for satisfying their basic needs.

II.4.2 Main social issues Central America

• Employment and labour issues o Official unemployment rates in the region vary, roughly between 3 percent and 10

percent. Real unemployment is however substantially higher, but remains mainly hidden, as unskilled or laid off workers have to make a living in the informal sector, mostly in the countryside. Self-employment rates for Central America6 vary between 20 percent (Costa Rica) to 38 percent (Honduras). Unemployment is a chronically unresolved problem in Central America, in particular for the poorest countries in the region with abundant low skilled workers and with a productive sector poorly diversified. Both factors have directly contributed to significant underemployment, and indirectly to labour migration, mostly to the US;

o At country-level, Costa Rica’s and Panama’s (formal) labour markets are more capable of absorbing labour supply than the other Central American countries. Informality rates are therefore much higher in e.g. Nicaragua and Guatemala (82 and 69 percent) than in Costa Rica (26 percent). Productivity is higher and unemployment rates lower in Costa Rica, as compared to Panama;

o Migration has become a major social issue, especially for countries where the lack of prospects lacking for a lasting improvement in employment opportunities is perceived high. For example in Nicaragua, a net outflow was recorded of 210,000 people over

18 The terms of trade effects show how many imports a country’s export can buy (in value terms); see Table III.0.11.

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 35

2000-2005. In contrast, Costa Rica and Panama received net inflows over the same period (84,000 and 8,000 people, respectively).

• Poverty and income inequality o Poverty is a problem throughout the Central American region, though some countries

clearly perform better than others. The percentage shares of the population living on less than $2 a day range between almost 20 percent and 70 percent. Costa Rica and Panama perform relatively well in terms of poverty levels when compared to the other countries in the region (e.g. Nicaragua and Honduras);

o Generally, the levels of poverty (and ranking of the Central American countries) are also reflected in other social indicators, such as the level of unemployment, or access to sanitary facilities, especially in rural areas;

o Income inequality has been on the rise on the Central American region over the last decades (in line with the often observed phenomenon of economic growth going accompanied by rising income inequality in some stages of growth). The Gini coefficient is high in all six Central American countries, ranging between 0.48 (Costa Rica) and 0.61 (Honduras).19

• Equality o With respect to gender equality in the Central American region, women tend to have less

access to the labour market and earn less when in the labour force than men. They either remain more often in the informal sector than men (e.g. in Nicaragua), or encounter horizontal and vertical segregation (as represented by the low rates of female directors and managers). They tend to have less access to social services than men (save primary and secondary education). While this is the region-wide picture, some country-level differences exist, roughly correlating to poverty (vulnerability) levels. For example, Costa Rica women have better access to pensions and health care than in other Central American countries;

o A recent report published by the Central American Women’s Network (CAWN), analyses the potential impacts of the AA on Central American women. There is a risk that women’s employment opportunities may be limited and the report therefore recommends promoting the inclusion of women in policy decisions and thereby creating more employment and reducing their vulnerability as a Group;20

o According to the EC’s new regional strategy, there is ample scope for improving the record in the region with regard to the strength of social and human resource development, democratic institutions and labour rights, including health, safety standards and the activities of trade unions. Some civil society actors consider the EC technical cooperation as a mechanism to protect the interests of weaker segments, especially SMEs, ethnic minorities and rural property owners in coastal areas, in the context of exposure to increased openness and transatlantic trade and investments.

• Health

19 ECLAC (2006). 20 El Acuerdo de Asociación entre la UE y Centro América: Su Posible Impacto en la Vida de las Mujeres Centroamericanas,

CAWN, January 2009.

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 36

o One important health-related issue in the region is the increase in drug trafficking and related crimes. Common and violent crimes have as a result been on the rise in the region, aggravated by a feeling of corruption with police authorities and impunity. For example, El Salvador and Guatemala have homicide rates of 55.3 and 45.2 homicides /100,000 inhabitants respectively, 21 which is extremely high in comparison to the world average (7.6 homicides /100,000 inhabitants)22 and especially the Latin American average (25.6 homicides /100,000 inhabitants);23

o Differences in social investments between the countries are reflected in various social indicators, including health. Costa Rica has a relatively long history of high social investment by the State compared to the other countries (public social investment represents 17.5 percent of PIB, or a $772 per capita, compared to e.g. Nicaragua where these numbers are 10.8 percent, or $90 per capita). Differences in access to healthcare (in comparison e.g. relatively high in Costa Rica) in turn reflect in differences in maternal and child mortality rates and life expectancy at birth (76 years for men and 81 for women in Costa Rica, compared to e.g. 70 and 76 years in Nicaragua).

• Education o The primary enrolment rate of the region lies close to 95 percent (ranging at country level

between 87 and 98 percent). In contrast, secondary enrolment rates are much lower and vary more between the six countries (between 30 and 64 percent). For example in Honduras, the primary enrolment rate is 96 percent, whereas secondary enrolment in only 30 percent. This directly affects the qualification of young people, negatively affecting their employment opportunities and increasing crime rates (the increased presence of gangs - “maras”- pose a real problem, for the general population, the economy and investment climate;

o Generally, the differences in educational enrolment rates between the countries are roughly in line with the differences in literacy rates.

II.4.3 Main environmental issues Central America

• Atmosphere o CO2 emissions per capita in the region varied (at country level) between 0.8 (Nicaragua)

to 1.9 (Panama) metric tons per capita in 2004; the differences can partly be attributed to the transport sector and use of personal vehicles. Compared to EU per capita emission levels (around 10 tons), this is relatively low, but emission levels have increased considerably since 1990 (e.g. Honduras has a 2004 index of almost 194 against 1990);

o With respect to other GHG emission, Guatemala stands out for a high level of S02 emissions (8.4 kg/person in 2004 versus e.g. only 0.4 in Honduras);

o It should be noted that air quality monitoring networks are not well developed in any of the countries in the region.

• Land and biodiversity 21 Observatorio Centroamericano de la Violencia (2007), Tasas de Homicidios Dolosos en Centroamérica y República

Dominicana por 100,000 habitantes (1999 -2007). 22 Geneva Declaration on Armed Violence and Development (2008), Global Burden of Armed Violence Report. 23 II Foro Iberoamericano sobre Seguridad Ciudadana, Violencia y Políticas Públicas (2008).

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 37

o Deforestation is one of the main environmental concerns throughout the Isthmus. A combination of population pressure, secularly high timber prices in the construction sector, low agricultural productivity, land demanded for cattle raising, together with highway construction projects to the Atlantic Coast had serious impacts;

o At present, land covered by forest varies between 14 percent in El Salvador, up to 46 percent in Costa Rica and 57 percent in Panama. The two most prosperous countries share most of the forest resources remaining on the Isthmus, whereas the poorest countries Honduras, Nicaragua and Guatemala face the highest rates of deforestation. Primary forest resources have virtually vanished in El Salvador, and dramatically dwindled in Guatemala (Petén), Honduras (Olancho), Nicaragua (RAAN and RAAS) and Panama (Darién);

o In Costa Rica, approximately 20,000 acres of land are still being deforested annually. Next to the lasting efforts of the ‘Fundación de Parques Nacionales’, the Ministry of Environment, Energy and Telecommunications (MINAET) now promotes conservation to the agriculture industry by offering financial incentives to farmers for their efforts in protecting primary and secondary forests on their land. Costa Rica’s pioneering public policies in forest resources date back to the 1970s, with now 9.3 percent of its total land area under public management, with additional and valuable community initiatives Panama and Nicaragua follow with 6.5 and 6 percent, respectively, under public management. Contrasting, Costa Rica has about 56 percent of its land area in use for agriculture, Nicaragua 44 percent and Panama 30 percent, and the latter two countries have a much larger area of forests (51.9 percent and 42.9 percent, respectively) than Costa Rica (23.9 percent);

o Biodiversity is closely related to the issue of deforestation. The region is extremely rich in biodiversity, which presents a strong asset for the tourism industry. For example in Costa Rica and Panama, there are over a 1,000 animal species, of which each over 400 bird species, and around 10,000 plant species;

o Urbanisation rates in the region are quite high, generally close to 60 percent of the population lives in urban areas (Panama being most urbanised with a rate of 66 percent, Guatemala lowest with 40 percent). The urbanisation rates are expected to increase further, with subsequent effects of e.g. decrease in use of agricultural land and increase in urban pollution.

• Environmental quality o Total energy production in thousands of metric tons petroleum equivalent is around 1,500

in Costa Rica and Panama, and about half of that in Nicaragua. However, with high oil prices in 2007, it became clear that these countries are highly dependent on fossil energy and that renewable sources of energy have yet to be fully exploited. In a related context, trade in carbon emission rights has received government attention, especially in Costa Rica. El Salvador is the country with the highest geothermal energy production in Central America.

• Fresh and waste water o In the Central American region, lack of waste water treatment, relatively low levels of

access to safe drinking water (overall ranging from 63 percent in rural areas in Nicaragua to 99 percent of population in urban areas in Costa Rica) and sewage systems in some

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 38

parts as well as water pollution are an issue, especially in rural areas and for the poorer parts of population. Considerable regional disparities exist;

o The increasing urbanisation rates pose challenges to municipalities being strained in their present systems of sewage and drinking water supply;

o Guatemala today has the second largest water reserves of the American continent after Brazil. Soil and surface water pollution is particularly a problem in Costa Rica. For Panama, the impact of Canal expansion is relevant.

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 39

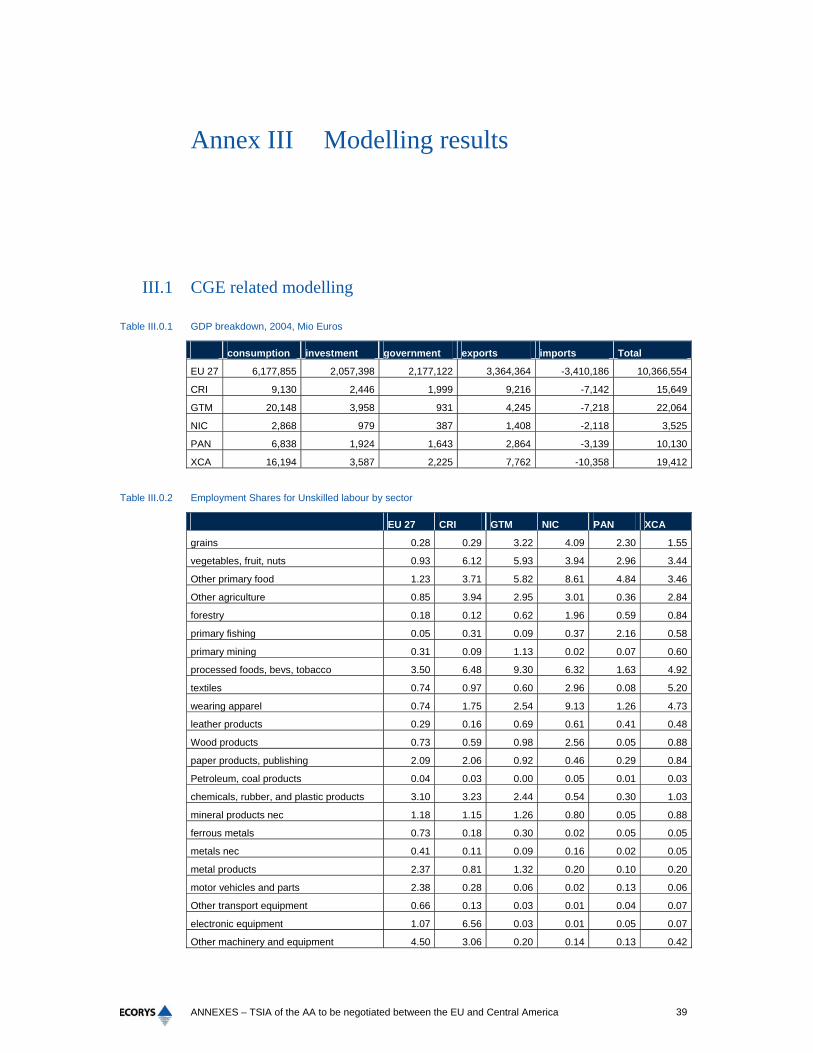

Annex III Modelling results

III.1 CGE related modelling

Table III.0.1 GDP breakdown, 2004, Mio Euros

consumption investment government exports imports Total

EU 27 6,177,855 2,057,398 2,177,122 3,364,364 -3,410,186 10,366,554

CRI 9,130 2,446 1,999 9,216 -7,142 15,649

GTM 20,148 3,958 931 4,245 -7,218 22,064

NIC 2,868 979 387 1,408 -2,118 3,525

PAN 6,838 1,924 1,643 2,864 -3,139 10,130

XCA 16,194 3,587 2,225 7,762 -10,358 19,412

Table III.0.2 Employment Shares for Unskilled labour by sector

EU 27 CRI GTM NIC PAN XCA

grains 0.28 0.29 3.22 4.09 2.30 1.55

vegetables, fruit, nuts 0.93 6.12 5.93 3.94 2.96 3.44

Other primary food 1.23 3.71 5.82 8.61 4.84 3.46

Other agriculture 0.85 3.94 2.95 3.01 0.36 2.84

forestry 0.18 0.12 0.62 1.96 0.59 0.84

primary fishing 0.05 0.31 0.09 0.37 2.16 0.58

primary mining 0.31 0.09 1.13 0.02 0.07 0.60

processed foods, bevs, tobacco 3.50 6.48 9.30 6.32 1.63 4.92

textiles 0.74 0.97 0.60 2.96 0.08 5.20

wearing apparel 0.74 1.75 2.54 9.13 1.26 4.73

leather products 0.29 0.16 0.69 0.61 0.41 0.48

Wood products 0.73 0.59 0.98 2.56 0.05 0.88

paper products, publishing 2.09 2.06 0.92 0.46 0.29 0.84

Petroleum, coal products 0.04 0.03 0.00 0.05 0.01 0.03

chemicals, rubber, and plastic products 3.10 3.23 2.44 0.54 0.30 1.03

mineral products nec 1.18 1.15 1.26 0.80 0.05 0.88

ferrous metals 0.73 0.18 0.30 0.02 0.05 0.05

metals nec 0.41 0.11 0.09 0.16 0.02 0.05

metal products 2.37 0.81 1.32 0.20 0.10 0.20

motor vehicles and parts 2.38 0.28 0.06 0.02 0.13 0.06

Other transport equipment 0.66 0.13 0.03 0.01 0.04 0.07

electronic equipment 1.07 6.56 0.03 0.01 0.05 0.07

Other machinery and equipment 4.50 3.06 0.20 0.14 0.13 0.42

ANNEXES – TSIA of the AA to be negotiated between the EU and Central America 40

EU 27 CRI GTM NIC PAN XCA

manufactures nec 1.03 3.32 1.96 0.00 0.07 0.74

utilities 1.09 2.38 1.41 1.03 2.32 0.64

construction 7.52 9.61 7.04 8.52 21.50 7.23

distribution 16.50 9.05 19.70 22.20 11.80 20.40

Other transport 4.94 2.75 0.56 5.83 2.32 13.60

maritime 0.55 0.17 0.03 0.31 11.20 0.78

air transport 0.54 0.43 0.05 0.67 1.61 2.18

communications 1.68 0.38 0.73 1.03 0.90 0.58

financial services 2.52 2.32 1.78 1.74 3.77 2.43

insurance 0.86 0.47 0.36 0.33 1.42 0.89

business services nec 9.58 6.13 8.20 0.95 4.20 3.76

recreation and other services 2.65 3.47 4.47 2.29 3.26 1.02

public services and dwellings 22.20 17.40 13.20 9.11 17.70 12.50

CGDS 0.00 0.00 0.00 0.00 0.00 0.00

Total 100.00 100.00 100.00 100.00 100.00 100.00

Table III.0.3 Employment Shares for Skilled labour by sector

EU 27 CRI GTM NIC PAN XCA

grains 0.03 0.02 0.29 0.17 0.37 0.15

vegetables, fruit, nuts 0.09 0.17 0.22 0.17 0.08 0.12

Other primary food 0.12 0.10 0.22 0.37 0.13 0.12

Other agriculture 0.08 0.11 0.11 0.13 0.01 0.10

forestry 0.01 0.00 0.02 0.08 0.02 0.03

primary fishing 0.00 0.01 0.00 0.02 0.06 0.02

primary mining 0.20 0.03 0.49 0.01 0.02 0.24

processed foods, bevs, tobacco 1.54 2.59 5.34 3.78 0.57 2.49

textiles 0.26 0.31 0.26 1.49 0.03 2.19

wearing apparel 0.22 0.53 1.06 4.32 0.38 1.87

leather products 0.09 0.05 0.30 0.30 0.13 0.20

Wood products 0.23 0.16 0.36 1.06 0.01 0.30

paper products, publishing 1.23 0.84 0.51 0.29 0.11 0.44

petroleum, coal products 0.06 0.01 0.00 0.03 0.00 0.02

chemicals, rubber, and plastic products 2.47 1.55 1.60 0.41 0.14 0.64

mineral products nec 0.53 0.41 0.61 0.44 0.02 0.40

ferrous metals 0.36 0.06 0.14 0.01 0.02 0.02

metals nec 0.18 0.04 0.05 0.10 0.01 0.03

metal products 1.07 0.30 0.68 0.12 0.04 0.10

motor vehicles and parts 1.29 0.12 0.04 0.01 0.05 0.03

Other transport equipment 0.35 0.05 0.02 0.01 0.02 0.04

electronic equipment 0.89 3.29 0.02 0.01 0.02 0.05

Other machinery and equipment 3.74 1.53 0.14 0.11 0.06 0.27

manufactures nec 0.44 0.89 0.72 0.00 0.02 0.26

utilities 1.82 2.36 1.92 1.60 2.28 0.83