annual general meeting june 7, 2016 -...

TRANSCRIPT

ANNUAL GENERAL MEETING

JUNE 7, 2016

TSX:TGZ / ASX:TGZ

2

ALAN R. HILLCHAIRMAN

3

Receive 2015 Financial Statements

Re-appointment of Auditors

BUSINESS OF THE MEETING

Election of Directors

4

RICHARD YOUNGPRESIDENT & CEO

5

This presentation contains certain statements that constitute forward-looking information within the meaning of applicable securities laws (“forward-looking statements”),

which reflects management’s expectations regarding Teranga Gold Corporation’s (“Teranga” or the “Company”) future growth, results of operations (including, without

limitation, future production and capital expenditures), performance (both operational and financial) and business prospects (including the timing and development of new

deposits and the success of exploration activities) and opportunities. Wherever possible, words such as “plans”, “expects”, “does not expect”, “budget”, “scheduled”,

“estimates”, “forecasts”, “anticipate” or “does not anticipate”, “believe”, “intend”, “ability to” and similar expressions or statements that certain actions, events or results “may”,

“could”, “would”, “might” or “will” be taken, occur or be achieved, have been used to identify such forward looking information. Although the forward-looking information

contained in this presentation reflect management’s current beliefs based upon information currently available to management and based upon what management believes to

be reasonable assumptions, Teranga cannot be certain that actual results will be consistent with such forward looking information. Such forward-looking statements are

based upon assumptions, opinions and analysis made by management in light of its experience, current conditions and its expectations of future developments that

management believe to be reasonable and relevant. These assumptions include, among other things, the ability to obtain any requisite Senegalese governmental approvals,

the accuracy of mineral reserve and mineral resource estimates, gold price, exchange rates, fuel and energy costs, future economic conditions, anticipated future estimates of

free cash flow, and courses of action. Teranga cautions you not to place undue reliance upon any such forward-looking statements

The risks and uncertainties that may affect forward-looking statements include, among others: the inherent risks involved in exploration and development of mineral

properties, including government approvals and permitting, changes in economic conditions, changes in the worldwide price of gold and other key inputs, changes in mine

plans and other factors, such as project execution delays, many of which are beyond the control of Teranga, as well as other risks and uncertainties which are more fully

described in the Company’s Revised Annual Information Form dated September 1, 2015, and in other company filings with securities and regulatory authorities which are

available at www.sedar.com. Teranga does not undertake any obligation to update forward-looking statements should assumptions related to these plans, estimates,

projections, beliefs and opinions change. Nothing in this report should be construed as either an offer to sell or a solicitation to buy or sell Teranga securities.

This presentation is dated as of the date on the front cover. All references to the Company include its subsidiaries unless the context requires otherwise.

This presentation contains references to Teranga using the words “we”, “us”, “our” and similar words and the reader is referred to using the words “you”, “your” and similar

words.

All dollar amounts stated are denominated in U.S. dollars unless specified otherwise.

FORWARD-LOOKING STATEMENTS

6

Replaced reserves

& improved mine life

Advanced organic

growth initiatives

Reduced costs by

$20 million

Strengthened balance sheet

& improved liquidity

Brought on strategic

cornerstone investor

Missed 2015

guidance of

200K-230Koz

MAJOR ACHIEVEMENTS IN 2015 . . . BUT MISSED PRODUCTION GUIDANCE

7

MAJOR ACHIEVEMENTS IN 2015

Replaced reserves

& improved mine life

Advanced organic

growth initiatives

Reduced costs by

$20 million

Strengthened balance sheet

& improved liquidity

Brought on strategic

cornerstone investor

8

CORNERSTONE INVESTOR SUPPORTS EXECUTION OF GROWTH STRATEGY

Unique strategic cornerstone investor owns ~13% of Teranga

Increase

Production

Grow

Reserve

Base

New Strategic Cornerstone Investor

David Mimran (Tablo Corporation) completed strategic

private placement for 39.2M shares in Q4 2015 and has

since purchased more than 11M additional shares in the

open market

David Mimran is Considered a “Local” in Senegal

With homes in Geneva, Senegal and Ivory Coast, David

spends nearly 20 days out of every month in Africa

Strong Partner with In-Depth Local Knowledge

Mimran Group has a long history of operating successfully

and responsibly in Africa and is the largest private sector

employer in Senegal

Expand

Margins

9

Mitigating Our Impacts Sharing the Benefits

of MiningGood Governance

Our People and

Culture

Working with our partners to have a positive long-term impact on local and regional communities

MINING RESPONSIBLY

Our CSR Approach

Integrating responsible mining into all aspects of the mine life

10

UPDATED LIFE OF MINE PLAN

11

(8)

90

180

330

390

350

730

2.6M Proven & Probable Reserves(1) at $1,100 gold.

Average mined grade of 1.59 grams per tonne*(As at December 31, 2015)

Proven & Probable Reserves(1)

(in Moz)

Refer to endnote (1) on the last slide

LARGE RESERVE BASE WITH 13.5-YEAR MINE LIFE

310

220

30

Since 2010, increased reserve base by 80% and this is after producing 1 million ounces

80% increase in reserves since IPO

*Not including stockpile of 0.39Moz

12

SOLID BASE CASE PRODUCTION PROFILE(2)

00

0’s

oz A

u

Opportunity to grow

production by increasing

material movement

Opportunity to increase

production through resource

conversion and new discoveries(3)

+200Koz average annual production from 2012- 2024(2)

Significant potential upside to life of mine base case production profile(3)

2016 Outlook

200K-215Koz

Refer to endnote (2) and (3) on the last slide

13

ORGANIC GROWTH: SIGNIFICANT INCREASE IN THROUGHPUT DUE TO MILL OPTIMIZATION

2016 LOM Mill Rate vs 2014 LOM Mill Rate

Leveraging existing mill and related infrastructure to increase organic growth

Up to 15% increase in throughput

5% reduction in costs

+50% IRR

14

FUTURE ORGANIC GROWTH: HEAP LEACHING

Heap Leach Flow Sheet

Heap leaching has potential to increase Teranga’s annual production by 10% - 20%

GRIZZLY

FEEDER

SCALPING

SCREEN

JAW

CRUSHER

SECONDARY

CRUSHER

GOLD

ROOM

AGGLOMERATOR

CIS

TANKS

HEAP LEACH

PREGNANT LIQUOR

STACKER

Technically Viable For Processing Low-grade Ore

Confirmed by pre-feasibility study,

which was completed in Q4 2015

High Ore Recovery Range

Oxide 78% - 83%

Transition 61% - 66%

Current Economic Estimates

Capital cost: $50M

Processing costs: ~$7 per tonne

Valuable Stockpile

~150,000 ounces of low-grade inventory

available for heap leaching

15

DECLINING COSTS & ATTRACTIVE CASH FLOW PROFILE

Life of Mine

Cash Flow(5)

$240/ozat $1,200 gold

23% decrease in mining costs since 2014

40% decrease in milling costs since 2014

Benefitting from lower fuel prices, favourable FX rates

and mill optimization

40-50% of costs are Euro-denominated

Cost saving initiatives are ongoing

LOM 2016 - 2020

Gold Price $ 1,200 $ 1,200

All-in Sustaining Cost(4) $ 887 $ 914

$ 313 $ 286

Franco-Nevada Stream* $ 73 $ 92

Cash flow/oz(5) $ 240 $ 194

*Fixed portion of Franco-Nevada gold stream ends in 2019 and will be replaced by

variable stream, estimated to be $58/oz LOMRefer to endnotes (4) and (5) on the last slide

16

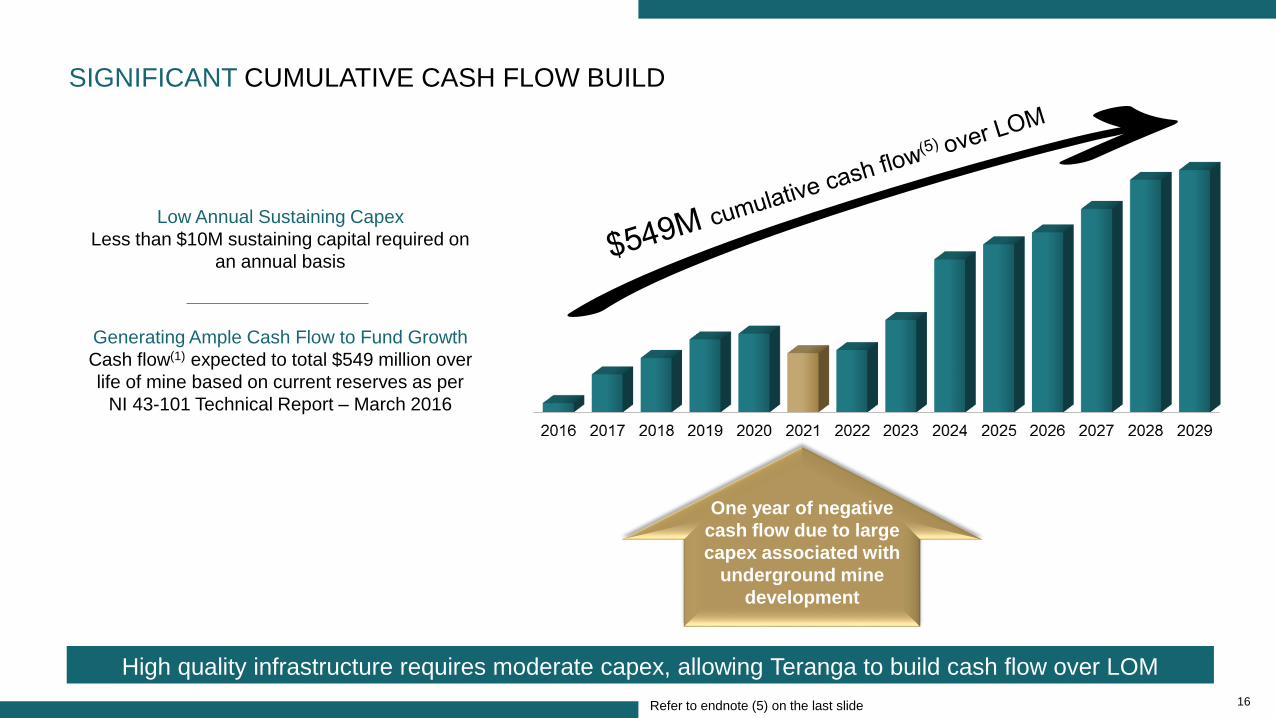

SIGNIFICANT CUMULATIVE CASH FLOW BUILD

High quality infrastructure requires moderate capex, allowing Teranga to build cash flow over LOM

Refer to endnote (5) on the last slide

One year of negative

cash flow due to large

capex associated with

underground mine

development

Low Annual Sustaining Capex

Less than $10M sustaining capital required on

an annual basis

Generating Ample Cash Flow to Fund Growth

Cash flow(1) expected to total $549 million over

life of mine based on current reserves as per

NI 43-101 Technical Report – March 2016

17

Senegal

12M+ ounces Au

discovered over

last 10 years

Mali

40M+ ounces Au

discovered over

last 25 years

Africa

Emerging

Gold Belt

Potential for Major Discoveries

Emerging gold belt straddles border between

Senegal and Mali where +50 million ounces have

been discovered(6)

Only Commercial Gold Mill in Senegal

Ability to process regional discoveries and enter

into strategic combinations to process

neighbouring deposits

Safe, Stable, Mining-Friendly Jurisdiction

Democratic government strongly supports mining

and views it as a key pillar for Senegal’s

economic growth

EARLY DAYS ON EMERGING WORLD-CLASS GOLD BELT

Mine License

Regional Land PackageRefer to endnote (6) on the last slide

18

GROWING RESERVES ON MINE LICENSE

Mine License of 291km2

Focus on increasing reserves on mine license, which

are within close proximity to mill

Reserves of 2.6Moz at $1,100 Gold(1)

Average mined grade of 1.59 grams per tonne (not

including stockpile of 0.39Moz)

Multi-year Development ProgramFocused on adding higher grade mill material and

lower grade material for potential heap leach

Refer to endnote (1) on the last slide

Masato

Au 730 (Koz)

Niakafiri Main

Au 260 (Koz)

Niakafiri SW

Au 10 (Koz)

Maki Medina

Au 30 (Koz)

Niakafiri SE

Au 40 (Koz)

Kerekounda

Au 90 (Koz)

Golouma West

Au 200 (Koz)

Golouma South

Au 130 (Koz)

Golouma South

Au 60 (Koz) Golouma West

1 - Au 120 (Koz)

2- Au 60 (Koz)

Sabodala

Au 180 (Koz)

Kerekounda

Au 100 (Koz)

Reserves – Open Pit

Reserves – U/G

Increasing Exploration Spend & Bench StrengthFocused on large discoveries – Increased focus in the

last six months has advanced a number of prospects

that are currently in drilling phase

19

FOCUSED ON BIG TARGETS ON LARGE REGIONAL LAND PACKAGE

Soreto-Soreto North

DDH Drilling

Program &

Trenching

Cinnamon North

Prospect

Trenching & DDH

Drilling Program

Leoba-Lerinde Granite

DDH Program &

Trenching

Leocounda Prospect

DDH Drilling Program

& Trenching

Marougou

Prospect

DDH Drilling

Program

Nienienko Main

RC Drilling Program

Marougou West

Prospect

Trenching & DDH

Drilling Program

Bransan

Trenching &

Drilling Program

KA Prospect

DDH Drilling

Program

~1,000km² Regional Land PackageExploration permits encompassing large of land

surrounding Teranga’s mine license

First Discovery: High-Grade Gora~5 grams per tonne deposit developed in 2015

20

-30%

-10%

10%

30%

50%

70%

90%

110%

130%

150%

Teranga Gold (TSX:TGZ) Market Vectors Global Junior Gold Miners Index (MVGDXJ) Gold Price (XAU)

Data Source: Thomson Reuters as at June 6, 2016

February 25:

Released full life of mine opexand capex detail

March 23:Filed new life of mine plan

(43-101 Technical Report)

January 29: Issued Q4 operating resultsReleased life of mine

production schedule

April 11:Pre-released Q1

production results

April 28: Released Q1 financial

and operating results

TGZ:

+118%

GDXJ:

+99%

Gold:

+17%

TGZ Share Price Performance vs Index and Gold Price

(52-Week Range: C$0.38 - $1.18)

OUTPERFORMING BOTH GOLD AND THE GDXJ INDEX

21

Data Source: BMO GoldPages published June 6, 2016

RELATIVE UNDERVALUATION PROVIDES ATTRACTIVE INVESTMENT OPPORTUNITY

Enterprise Value

($M)

EV/Production

(BMO based on gold sold, $/oz)

EV/2P Reserves

($/oz)EV/2016E EBITDA

($/oz)

*Project Developers

22

$1.02 $1.02 $1.02 $1.02$1.18

$1.30

$1.54

$1.89

SIGNIFICANT POTENTIAL UPSIDE REMAINS DESPITE SHARE PRICE APPRECIATION

Based on Teranga’s updated NI 43-101 and the 1.6x average NPV multiple for its peer group, Teranga’s share price should be C$1.89(7)

27% 51%

Revalued

Share Price

NPV Multiple 0.9x 1.1x 1.3x 1.6x

Teranga’s Share Price vs.

Teranga Net Present Value (NPV)(7)

per Share

Share

Price

85%

Revalued

Share Price

Share

PriceBMO NPV

per Share

Share

Price

Refer to endnote (7) the last slide

Average

Multiple

for Medium

Producers

1.6x NPV(7)

Revalued

Share PriceShare

Price

TGZ

Currently

Trading at

0.9x NPV(7)

Data Source: BMO GoldPages published June 6, 2016 – all figures are in Canadian dollars

23

23

Q & A

24

EMERGING

World-Class Gold Belt

in a Safe & Stable

Jurisdiction

SOLID

Balance Sheet &

Significant Insider

Ownership

LARGE LONG-LIFE

Reserve & Resource

Base(1)

LOW

All-in Sustaining

Costs per Ounce(4)

SIGNIFICANT

Organic Growth

Potential

STRONG

Life of Mine

Cash Flow(5)

Refer to endnotes (1) (4) and (5) on the last slide

STRONG VALUE PROPOSITION

Strong value proposition and undervalued relative to peer group = compelling investment opportunity

25

ENDNOTES

1. Mineral Reserves and Mineral Resources estimates as at December 31, 2015 as per Company disclosure. For more information regarding Teranga Gold’s Mineral Reserves and

Resources, please refer to Teranga Gold’s December Quarter and Year-end 2015 Report accessible on the Company's website at www.terangagold.com.

2. This production profile is based on existing proven and probable reserves only from the Sabodala mining license as disclosed in Teranga Gold’s December Quarter and Year-end

2015 Report accessible on the Company's website at www.terangagold.com.

3. Over the past several years more than twelve million ounces of measured and indicated resources have been identified within the south eastern Senegal region, including the

Massawa, Golouma, Makabingui and Mako projects, along with the Company’s own Sabodala gold mine. With exploration work completed to date and the prior exploration success

seen in the area Management believes there is a reasonable basis to anticipate future resource to reserve conversion.

4. Total cash costs per ounce and all-in sustaining costs per ounce are non-IFRS financial measures and do not have standard meanings under IFRS. All-in sustaining costs per ounce

sold include total cash costs per ounce, administration expenses (excluding Corporate depreciation expense), Regional Administration Costs, capitalized deferred stripping,

capitalized reserve development and mine site & development capital expenditures as defined by the World Gold Council. For more information regarding these measures, please

refer to Non-IFRS Performance Measures in the Company’s Management’s Discussion and Analysis for the three months ended March 31, 2016 accessible on the Company’s

website at www.terangagold.com.

5. Cash flow is the Life of Mine net cash flow based on the Company’s most recent NI 43-101 Technical Report (“43-101 plan”) filed in March 2016, before income taxes, interest, debt

repayments, closure costs, dividends and working capital.

6. Identified ounces on Birimian greenstone belt, which straddles the border of Senegal and Mali, West Africa, refers to gold ounces historically mined in addition to gold ounces

currently reported as Measured and Indicated Resources, as available on GFMS Thomson Reuters and latest company reserve and resource statements as of March 23, 2016.

7. Net Present Value (“NPV”) per share is a Non-IFRS financial measure. NPV per share, average NPV multiple of medium producers, and Teranga’s share price is as per BMO

GoldPages published June 6, 2016. According to BMO GoldPages, NPV per share is calculated using the net present value of the life of mine cash flows based on the NI 43-101

plan, less cash flow of corporate costs, less net debt per share, using the model at SPOT commodity prices and exchange rates. The “Revalued Share Price” is calculated using the

NPV per share at SPOT times the NPV multiples as listed. The BMO NPV calculation assumes a US$1,241 SPOT gold price per ounce, 5% discount, 0.77 USD/CAD exchange rate.

For more information regarding Non-IFRS financial measures, please refer to Non-IFRS Performance Measures in the Company’s Management’s Discussion and Analysis for the

three months ended March 31, 2016 accessible on the Company’s website at www.terangagold.com.