annual report 2015–2016 - pilbara regional council · during 2016, one of these regional advocacy...

TRANSCRIPT

1

AnnuAl RepoRt2015–2016

2

AdvAncingthe pilbARAAnnuAl RepoRt2015–2016

Message from the Chairperson

The Pilbara Regional Council Governance Model

Appointed Representatives

PRC Organisational Values

Message from the Chief Executive Officer

Year in Review

Independent Audit Report

Statutory Reports

Financial Report

3

4

5

6

8

9

17

19

21

3

messAgefRom thechAiRpeRson

2016 … what a year it has been. The media appears focused on the demise of our region but it’s hard tosee the reality in this. Certainly life as we knew it has changed but the Pilbara continues to move forwardalbeit at a slower but some could argue more sensible pace.

Despite the Pilbara having been a primary driver of contributions to national revenue and having beenunderprepared for the previous boom, at all levels of government, it seems barely believable that both theFederal and the State governments appear unwilling to invest further in the development of criticalinfrastructure in the north-west. This is despite the Commonwealth noting the strategic importance ofdeveloping northern Australia, and the Pilbara Development Commission identifying a significant portfolio of projects that would yield measurable economic benefit to the country. I refer of course to the development of a common-use facility at Lumsden Point to take advantage of the proximity to large multi-nationalcorporations and to service the rapidly growing level of agricultural investment in the region.

The City of Karratha has been a clear illustration of the yield from these infrastructure investments, with a large and stable population that has seen school enrollments actually growing despite the economic slowdown. We hear the ‘Pilbara has had its fair share’ rhetoric at every turn, however this is easily refuted by noting that sensible countries, companies and individuals invest in areas where there is the highest potential for return.

This is no more evident than in the tourism space, where we continue to be held to an artificial geographicalstructure that has tourism marketing for the Pilbara, one third of the State, managed by an organization based outside of this area. The Pilbara needs to take control of our own destiny and market our assets, known best by us, to the greater West Australia, Australia and indeed the world. Let us treat others to the wonders of the beautiful Karajini and naturally occurring beauty found throughout the magnificent Pilbara.

My Chairperson’s message for the 2016 annual report is clear – we all need to focus on developmentinitiatives that will build and support sustainable communities of the north west. The region already enjoysaccess to resources, proximity to markets, presence of huge multinational corporations, and interest from overseas investors. Our challenge is to come together to unlock as much of this potential as possible.

Cr Lynne CraigieChairperson

4

goveRnAnce model

The Councillors, Chief Executive Officer and staff, through a combined effort, are responsible for successfully leading and managing the PRC.

The organisation is accountable to its member local governments, and regularly publishes detailed financial statements and project performance reports for the review of its members.

Councillors

The four local governments arerepresented by the eight-member Pilbara Regional Council. Two Councillors are nominated from each member local government, governing for the interests of their town or shire and for the broader Pilbara region.

Council

The Chairperson and seven Councillors establish the strategic context ofthe PRC and govern to ensure that key objectives are met. The Council monitors the activities of the CEO and management team and ensures that the PRC remains true to its Constitution, vision and mission.

Council Meetings

Ordinary meetings of the Council are held primarily at the State Library in Perth, as well as in the Pilbara. Members of the public are welcome to attend Council meetings and are able to pose questions on specific issues of concern.

Chief Executive Officer

A Chief Executive Officer is employed by the Council to deliver the functions of the local government, and to service the requirements of members. The CEO employs a staff to deliver services and carry out directions of the Council. The CEO is responsible for all operationalaspects of the PRC, and is accountable to the Council for the performance of the organisation.

External Advisors

The PRC engages a number of specialist external advisors to assist in the management of its affairs. These advisors include auditors, legal counsel, project managers, financial advisors, information technology support, et al.

Contractors

As a project-driven member services organisation, the PRC occasionally engage with contractors to deliver components of some projects. All contractors work within the Council’s project governance framework, and under the specific direction of a nominated project manager.

Shire of Ashburton Shire of East Pilbara City of Karratha Town of Port Hedland

5

Appointed RepResentAtives

Cr Kerry WhiteShire President

Cr Glen DellarCouncilor

Cr Anita GraceCouncilor

Cr Lynne CraigieShire President

Cr Peter LongMayor

Cr John LallyCouncilor

Cr Kelly HowlettMayor

Cr Camilo BlancoCouncilor

6

7

8

messAge fRom the ceoIt is with pleasure that I present the 2016 Annual Report for the Pilbara Regional Council (PRC). It has been an eventful for the PRC; with a significant shift in the economy, a Federal Election announced, a State budget that offers some challenges for the Pilbara region, and a number of new Councillors joining the PRC.

Working in this dynamic environment, the PRC has sought to maintain relationships at all tiers of Government and across all major parties; maintaining open lines of communication to advocate for and on behalf of the region. Regular briefings have been held with parliamentarians and key staffers to ensure that they are familiar with key regional issues, and that the PRC’s position in these issues is clearly articulated. The value of this activity has been clearly illustrated through engagement during matters such as the proposed closure of remote aboriginal communities and other contentious issues, along with regular repeat access to key decision makers and influencers in both State and Federal Government.

These messages have been bolstered with closer alignment to both the Federal Government’s intent for developing northern Australia, and with the blueprint issued by the Pilbara Development Commission. This alignment has facilitated more targeted messaging that resonates with the recipients in both the Federal and State political environments. An enduring challenge for the Pilbara Regional Council is to select key advocacy initiatives for which the organisation is able to form a strong position– and to then exert some influence towards change. In a region that contributes such a significant portion of the Commonwealth and State revenues, and that is populated by industry giants, this is no easy task.

During 2016, one of these regional advocacy activities involved hosting the EASTxWEST Forum in Shenzhen, China. The main forum was attended by nearly 150 delegates; drawn from all tiers of Government as well as the private sector. A broad speaker lineup covered a diverse range of topics throughout the Forum, and the event was showcased at the Gala Dinner sponsored by Pardoo Beef. The event was delivered on time, scope and budget; with very positive press and sponsor reviews. The event highlighted that significant investment in agriculture and tourism offer opportunities for future regional diversification.

Our member local governments and our core partnership group continue to stimulate new opportunities to provide regional services to the governments of the Pilbara. During 2016, these activities encompassed historic building conservation, regional training, destination marketing, payroll processing, green waste processing, land deconstraint, and a number of studies. I’d like to take this opportunity to thank the Pilbara Development Commission, the Department of Local Government & Communities, the Department of Regional Development, Tourism WA, and our other partners who have contributed strongly to our successes in FY16.

FY17 offers a similar wealth of opportunities for service delivery to our member local governments, and I look forward to reporting the outcomes of these activates throughout the year to come.

Tony FridayChief Executive Officer

9

fY16 YeAR in RevieW

sAving moneY

Less CompLianCe Burden

Land De-ConstraintReduced the administrative functions associated with obtaining land tenure over all sites secured and managing all de-constraining activities. Regional Rating StrategyLeveraged economies of scale to regionally procure the reviewed and assessment of current rating strategies. Strategies were benchmarked against peers and evaluated. Rating efforts and individual rating model were produced to assist and inform future rating decisions.

Tourism Capacity BuildingRemoved separate authorisation and costs by centrally coordinating the delivery of a business case for a potential Camping with Custodian site on behalf of Tourism WA.

ATTRACTING FUNDS

Old Onslow ConservationThe project secured a total of $1,150,000 of State Agreement funds towards the outcomes of the project

pRoJect benefits And tAngible outcomes

with no matching contribution from either the PRC, or its members.

East x West ForumThe project secured a total of $72,500 in sponsorships and $160,082 in ticket sales. Conducted a successful economic forum that (overtime) will yield positive investment outcomes for the region. 134 Australian delegated and 137 Chinese attendees.

Tourism Capacity BuildingRemoved separate authorization and costs by centrally coordinating the delivery of a business case for a potential Camping with Custodian site on behalf of Tourism WA.

BeTTer supporTinG our memBers

Payroll ProcessingReduced the administrative functions to free up 0.5 FTE per participating members to perform other duties.

Training for Staff and CouncillorsThe project saved $27,090 this year by leveraging economies of scale for all procurement activities.

BeTTer supporTinG our CommuniTies

Volunteering Capacity BuildingLeveraged existing Welcome Wi-Fi infrastructure to encourage travellers to register their interest in volunteering.

Regional EventsCelebrated the rich and diverse heritage of the Pilbara by engaging with the Pilbara community to collect historical images that were used to create a visual display of the Pilbara’s history.

10

sAving time

mAKing life eAsieR

reduCed dupLiCaTion

Payroll ProcessingThe project saved an estimated 0.5 FTE a year to participating members.

Tourism Capacity BuildingReduced the administrative functions associated with applying for a diversifi cation permit. Centrally managing all activites to TWA’s satisfaction on behalf of their Camping with Custodians program.

Training for Staff and CouncillorsSaved an estimated 107.5 hours of works by centralising the procurement activities, travel arrangements and general administrative functions associated with the delivery of training sessions.

Visitor Centres Website ManagementProviding a single point of contact for all development activities.

Regional Tendering and ContractsReduced administrative functions associated with the procurement of 3 regional activities (green waste, solar audit, rating strategy) to free up an estimated 0.2 FTE.

Solar Feasibility StudyEvaluated the feasibility and viability of turning 25 nominated public buildings to renewable solar energy. The study outlined a number of discussion point that could lead a cost savings and return on investment.

GIS System and DataSystem implementation and delivery of user training for a fi t-for-purpose and fl exible GIS system at the Shire of Ashburton, Town of Port Hedland and Shire of East Pilbara. Users can now overlay of combine separate “thematic layers” of information to identify patters that may otherwise not be obvious. The implementation also integrates with existing infrastructure including IT Vision’s SynergySoft and receives automatic updates from SLP.

GoinG diGiTaL

Online Development ServicesOnline access for lodgement, payment and tracking the status of building applications, a more continent DIY service that is saving residents as well as staff time.

Pilbara Research OnlineComprehensive database of regularly updated new data about the Pilbara, referencing hundreds of articles, journals, and academic papers.

Regional EventsLeverage the Welcome Wi-Fi to create temporary pop-up advertisement for members and nominated community events throughout the region. (The Karajini experience ads were viewed 2,821 times across the whole network during March/April).

Welcome Wi-Fi (Rest Stops and Public Centres) 30,000+ unique visitors, and 70,000+ total users of the infrastructure in FY16.

Visitor Centres Websites ManagementDelivered the Marble Bar website for a total cost $1,020 – www.marblebar.org.au

Volunteering Capacity BuildingInnovative use of technology to offer access to targeted volunteering opportunities using the Welcome Wi-Fi.

easier inTeraCTions

Old Onslow ConservationWorked collaboratively with multiple stakeholders to re-invigorate stalled project and deliver outcomes against Chevron’s State Agreement, regional tourism objectives, and Shire of Ashburton Heritage obligations.

ADVOCACY

ANWT Board PositionMade direct and specifi c representation to ANWT and Tourism WA seeking to deepen and broaden Pilbara-focused destination marketing activities. Conducted a media campaign seeking to highlight inequities in fl ight pricing between the eastern and western seaboards.

Visitor Centres Websites ManagementProvisioned an estimated $25,000 cost savings in website changes and development compared to market rate. Works included making the Karratha VIC website mobile friendly and establishing Marble Bar VIC web presence.

11

Regional Reforms (Remote Aboriginal Communities)Made direct and specifi c representation to all tiers of government regarding proposed closure of Remote Aboriginal Communities.

Differential RatingCoordinated communication between members and the Department of Local Government and Communities (DLGC)regarding issues surrounding the approval of differential rating schemes, and brokered senior level meetings to advocate a regional position.

Transient WorkforcesDeveloped a regional position and made specifi c representation to all tiers of government and many segments of industry.

Regional EventsIn conjuction with the Australia China Business Council (ACBC) and Chamber of Commerce WA (CCIWA), coordinated a visit by the Chinese Consulate General to the City of Karratha.

11

East x West ForumPromoted the North West of Australia as an attractive investment destination by hosting a public forum in Shenzhen, China.

inCrease reGionaL CoLLaBoraTion and ConsisTenCY

Karratha & Hedland TAG: Active, meaningful and informed participation through knowledge sharing and collaboratioin with regional tourism groups.

reGionaL serViCe deLiVerY

Contribution to the PTPDP (Signage)Appraised signage infrastructure required to support the drive tourism market in the Pilbara. Regional strategy document published with clear, prioritised and costed initiatives for individual member LGAs and PRC to consider.

Contribution to the PTPDP (Trails)Appraised 72 Pilbara trails for length, diffi culty, targeted user groups, risks, maintenance, current/desired condition, heritage value and linkage to the 3 thematic experiences.

12

documents pRoduced goveRnAnce / mAnAgement

Regional Rating StrategyIndividual rating model per membersDesktop Solar PV Feasibility Report (for nominated public buildings)Newman CCTV Business case for live monitoring solutionsDigital Engagement StrategyRegional Trails BlueprintRegional Signage StrategyAshburton River Mouth Boat ramp feasibility study and technical designs Pilbara Enterprise Zone financial and economic model, proposal for policy and regulatory changes and supporting marketing materials.Designated Area Migration Agreement submission including an Operational PlanRegional VIC Online Booking Portal business caseQuarterly VIC Website analytics report PRC web and social media performance reportWelcome Wi-Fi usage report (monthly report for members, tourism groups and VICs)Agreed regional position statements for:

1.2.3.

4.

5.6.7.8.

9.

10.

11.

12.

13.

14.

Digital and Mobile Engagement PlanPeedamulla Camping with Custodians Business CasePardoo Tourism Feasibility StudyOld Onslow Conservation Management StrategyOld Onslow Interpretation PlanOnslow Tourism Plan

15.16.

17.18.19.20.

Closure of Remote Aboriginal CommunitiesDifferential RatingsTransient workforcesDAMA PEZ

Good GoVernanCe

Detailed compliance calendar maintained and reviewed fortnightly 6 Council meetings 2 Audit and Risk Committee meetings 1 missed compliance date (Auditor failed to file with the Department of Local Government and Communities (DLGC)

Internal Audits and Reviews Portfolio Governance Project Governance Records Management Risk Management Admin Procedures Workplace Safety

External Audits and Reviews Annual DLGC Audit Land Deconstraint Project Audit

peopLe

All staff completed performance reviews.

Employee turnover 2 redundancies 0 resignations 0 HR complaints received

13

Team Building Activity Chineses Language Workshop Applied Corporate Law RAC Defensive Driving

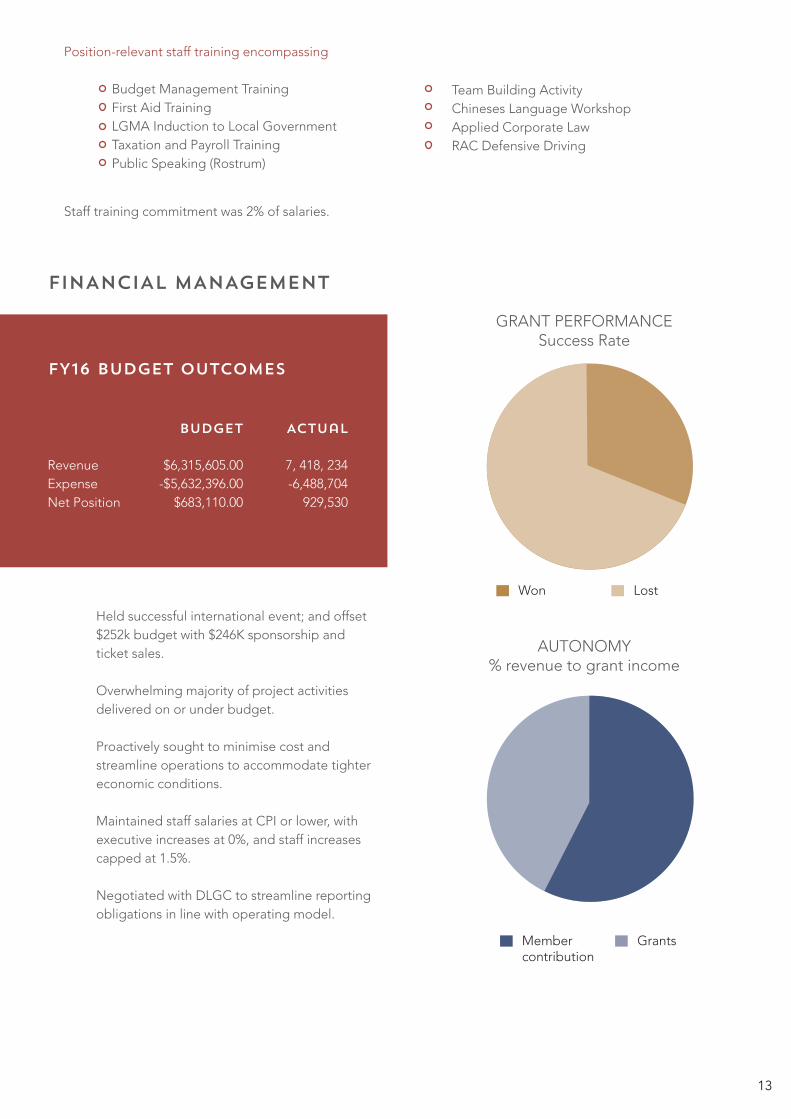

Held successful international event; and offset $252k budget with $246K sponsorship and ticket sales.

Overwhelming majority of project activities delivered on or under budget.

Proactively sought to minimise cost and streamline operations to accommodate tighter economic conditions.

Maintained staff salaries at CPI or lower, with executive increases at 0%, and staff increases capped at 1.5%.

Negotiated with DLGC to streamline reporting obligations in line with operating model.

finAnciAl mAnAgement

fY16 budget outcomes

Membercontribution

Grants

Won Lost

GRANT PERFORMANCESuccess Rate

AUTONOMY% revenue to grant income

Position-relevant staff training encompassing Budget Management Training First Aid Training LGMA Induction to Local Government Taxation and Payroll Training Public Speaking (Rostrum)

7, 418, 234-6,488,704

929,530

$6,315,605.00-$5,632,396.00

$683,110.00

RevenueExpenseNet Position

Actualbudget

Staff training commitment was 2% of salaries.

14

Old Onslow Augmented Reality

During FY16, the PRC has worked with leading edge technology providers to identify and investigate an augmented reality solution to assist with the interpretation of the Old Onslow conservation site. If implemented, this tool will allow visitors to ‘see’ Old Onlsow as it once was through the lens of their mobile devices. It will provide cultural and historical context, and bring meaning to the visual experience.

Welcome Wi-Fi Advertising

Durying FY16, the PRC utilized the Welcome Wi-Fi network of travellers that were passing through the region to raise awareness of the even and to promote regional attractions.

Volunteer Capacity Building

During FY16, the PRC partnered with the Department of Local Government and Communities and Volunteering WA to develop a volunteering portal that presents visitors to the region with volunteering positions in their immediate vicinity. Hailed as a very successful technology solution, both the DLGC and Volunteering WA have ought to extend this concept into other jurisdictions.

Online Time Sheets and Leave Applications

Building on its successful Payroll Processing project, durying FY16 the PRC worked with technology vendor IT Vision to offer additioinal functionality to participating Pilbara local governments. Implementation has now commenced to extend the payroll processing environment encompass online time sheets and online leave applications, both previously unavailable to Pilbara local government employees.

innovAtion

Camping with Custodians

The PRC, in partnership with Tourism WA, identified and validated a potential Camping with Custodians tourism site at Peedamulla Station in the Shire of Ashburton. Over the FY16 period, the PRC has worked with Tourism WA and the traditional owners to complete the project planning phase and secure funding for the implementation of the campground. Currently, we are working to secure the necessary permits in order to begin the construction phase of the project.

FB new page likes

190

TotalImpressions

213,173

Total postreach

128,031

Tweets

419

Number offollowers

674

Profile visits

9,864

sociAl mediA summARY

16.17.

18.19.20.21.

stAKeholdeR engAgement

Each project within portfolio has endorsed project reference group.

Delivered successful partnering activities with Tourism WA, Pilbara Development Commission, Volunteering WA, Pardoo Beef, and AustCham Beijing.

Interest in attending the PRC council meetings has become such that we are no longer able to accommodate all attendees at the PRC premises. Speakers and other external attendees now regularly contact the PRC in advance seeking meeting dates and other information.

15

background

Staff at the Pilbara Regional Council joined Kiva in August 2015. Kiva is a not-for-profit micro-financing organisation based in San Francisco. Founded in 2005, Kiva’s mission is to connect people through lending that alleviates poverty. For as little as $25USD, lenders can improve people’s lives by investing in their future.

How Kiva works

A borrower applies for a loan through Kiva, which goes through an underwriting and approval process. The loan is posted to the Kiva website to seek support from lenders. Lenders contribute in increments of $25 or more to ‘crowd fund’ the loan, which has a specified ‘loan goal’. Once the goal is reached, the borrower receives the funds. Borrowers repay the loans and lenders use repayments to fund new loans, donate or withdraw the money.

Lending activity

As at 30 June 2016, the PRC has raised a total of $1,820 AUD and have lent funds to over 73 borrowers from thirty-five (35) countries in thirteen (13) different sectors. 71% of staff contribute financially to the program, and 29% of staff contribute ‘in-kind’ through administration and research duties.

coRpoRAtegiving pRogRAm

16

Countries we have lent to

Colombia Education

Costa Rica Food

Ecuador Health

El Salvador Housing

Georgia Manufacturing

Ghana Personal Use

Guatemala Retail

Honduras Services

India Transportation

Indonesia

Jordan

Kenya

Lao People’s Democratic Republic

Lebanon

Madagascar

Mexico

Mozambique

Nicaragua

Pakistan

Palestine

Paraguay

Peru

Philippines

Rwanda

Sierra Leone

Tajikistan

Tanzania

Togo

Uganda

Ukraine

Vietnam

countries 35 / 77 sectors 13 / 15

Sectors we have lent to

Education

Food

Health

Housing

Manufacturing

Personal Use

Retail

Services

Transportation

29%

71%

Non-financial

Financial

STAFF ENGAGEMENT RATIO

17

independent AuditoR’s RepoRt

Level 1 10 Kings Park Road West Perth WA 6005 Correspondence to: PO Box 570 West Perth WA 6872 T +61 8 9480 2000 F +61 8 9322 7787 E [email protected] W www.grantthornton.com.au

Grant Thornton Audit Pty Ltd ACN 130 913 594 a subsidiary or related entity of Grant Thornton Australia Ltd ABN 41 127 556 389 ‘Grant Thornton’ refers to the brand under which the Grant Thornton member firms provide assurance, tax and advisory services to their clients and/or refers to one or more member firms, as the context requires. Grant Thornton Australia Ltd is a member firm of Grant Thornton International Ltd (GTIL). GTIL and the member firms are not a worldwide partnership. GTIL and each member firm is a separate legal entity. Services are delivered by the member firms. GTIL does not provide services to clients. GTIL and its member firms are not agents of, and do not obligate one another and are not liable for one another’s acts or omissions. In the Australian context only, the use of the term ‘Grant Thornton’ may refer to Grant Thornton Australia Limited ABN 41 127 556 389 and its Australian subsidiaries and related entities. GTIL is not an Australian related entity to Grant Thornton Australia Limited. Liability limited by a scheme approved under Professional Standards Legislation. Liability is limited in those States where a current scheme applies.

Independent Auditor’s Report To the Members of the Pilbara Regional Council We have audited the accompanying financial report of the Pilbara Regional Council (the “Council”), which comprises the statement of financial position as at 30 June 2016, the statement of comprehensive income by nature or type, statement of comprehensive income by program, statement of changes in equity and statement of cash flows for the year then ended, notes comprising a summary of significant accounting policies and other explanatory information to the financial report and the statement by the Chief Executive Officer.

Responsibility of the Council for the financial report The Council of the Pilbara Regional Council is responsible for the preparation and fair presentation of the financial report in accordance with Australian Accounting Standards (including the Australian Accounting Interpretations) and the Local Government Act 1995 Part 6. This responsibility includes establishing and maintaining internal control relevant to the preparation and fair presentation of the financial report that is free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Auditor’s responsibility Our responsibility is to express an opinion on the financial report based on our audit. We conducted our audit in accordance with Australian Auditing Standards. These Auditing Standards require that we comply with relevant ethical requirements relating to audit engagements and plan and perform the audit to obtain reasonable assurance whether the financial report is free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial report. The procedures selected depend on the auditor’s judgement, including the assessment of the risks of material misstatement of the financial report, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial report in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by the Council, as well as evaluating the overall presentation of the financial report.

Level 1 10 Kings Park Road West Perth WA 6005 Correspondence to: PO Box 570 West Perth WA 6872 T +61 8 9480 2000 F +61 8 9322 7787 E [email protected] W www.grantthornton.com.au

Grant Thornton Audit Pty Ltd ACN 130 913 594 a subsidiary or related entity of Grant Thornton Australia Ltd ABN 41 127 556 389 ‘Grant Thornton’ refers to the brand under which the Grant Thornton member firms provide assurance, tax and advisory services to their clients and/or refers to one or more member firms, as the context requires. Grant Thornton Australia Ltd is a member firm of Grant Thornton International Ltd (GTIL). GTIL and the member firms are not a worldwide partnership. GTIL and each member firm is a separate legal entity. Services are delivered by the member firms. GTIL does not provide services to clients. GTIL and its member firms are not agents of, and do not obligate one another and are not liable for one another’s acts or omissions. In the Australian context only, the use of the term ‘Grant Thornton’ may refer to Grant Thornton Australia Limited ABN 41 127 556 389 and its Australian subsidiaries and related entities. GTIL is not an Australian related entity to Grant Thornton Australia Limited. Liability limited by a scheme approved under Professional Standards Legislation. Liability is limited in those States where a current scheme applies.

Independent Auditor’s Report To the Members of the Pilbara Regional Council We have audited the accompanying financial report of the Pilbara Regional Council (the “Council”), which comprises the statement of financial position as at 30 June 2016, the statement of comprehensive income by nature or type, statement of comprehensive income by program, statement of changes in equity and statement of cash flows for the year then ended, notes comprising a summary of significant accounting policies and other explanatory information to the financial report and the statement by the Chief Executive Officer.

Responsibility of the Council for the financial report The Council of the Pilbara Regional Council is responsible for the preparation and fair presentation of the financial report in accordance with Australian Accounting Standards (including the Australian Accounting Interpretations) and the Local Government Act 1995 Part 6. This responsibility includes establishing and maintaining internal control relevant to the preparation and fair presentation of the financial report that is free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Auditor’s responsibility Our responsibility is to express an opinion on the financial report based on our audit. We conducted our audit in accordance with Australian Auditing Standards. These Auditing Standards require that we comply with relevant ethical requirements relating to audit engagements and plan and perform the audit to obtain reasonable assurance whether the financial report is free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial report. The procedures selected depend on the auditor’s judgement, including the assessment of the risks of material misstatement of the financial report, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial report in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by the Council, as well as evaluating the overall presentation of the financial report.

18

We performed the procedures to assess whether in all material respects the financial report presents fairly, in accordance with the Local Government Act 1995 Part 6 and Australian Accounting Standards (including the Australian Accounting Interpretations), a view which is consistent with our understanding of the Council’s financial position and of its performance.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

Independence

In conducting our audit, we have complied with the applicable independence requirements of the Accounting Professional and Ethical Standards Board.

Auditor’s opinion In our opinion, the financial report of the Pilbara Regional Council: (i) presents fairly, in all material respects, the Council’s financial position as at 30 June

2016 and of its performance and cashflows for the year then ended; (ii) complies with Australian Accounting Standards (including the Australian

Accounting Interpretations); and (iii) is prepared in accordance with the requirements of the Local Government Act 1995

Part 6 (as amended) and Regulations under that Act. Statutory Comp liance

I did not, during the course of my audit, become aware of any instance where the Council did not comply with the requirements of the Local Government Act 1995 and Local Government (Financial Management) Regulations 1996 as they relate to financial statements.

GRANT THORNTON AUDIT PTY LTD Chartered Accountants

M A Petricevic Partner - Audit & Assurance Perth, 26 October 2016

Level 1 10 Kings Park Road West Perth WA 6005 Correspondence to: PO Box 570 West Perth WA 6872 T +61 8 9480 2000 F +61 8 9322 7787 E [email protected] W www.grantthornton.com.au

Grant Thornton Audit Pty Ltd ACN 130 913 594 a subsidiary or related entity of Grant Thornton Australia Ltd ABN 41 127 556 389 ‘Grant Thornton’ refers to the brand under which the Grant Thornton member firms provide assurance, tax and advisory services to their clients and/or refers to one or more member firms, as the context requires. Grant Thornton Australia Ltd is a member firm of Grant Thornton International Ltd (GTIL). GTIL and the member firms are not a worldwide partnership. GTIL and each member firm is a separate legal entity. Services are delivered by the member firms. GTIL does not provide services to clients. GTIL and its member firms are not agents of, and do not obligate one another and are not liable for one another’s acts or omissions. In the Australian context only, the use of the term ‘Grant Thornton’ may refer to Grant Thornton Australia Limited ABN 41 127 556 389 and its Australian subsidiaries and related entities. GTIL is not an Australian related entity to Grant Thornton Australia Limited. Liability limited by a scheme approved under Professional Standards Legislation. Liability is limited in those States where a current scheme applies.

Independent Auditor’s Report To the Members of the Pilbara Regional Council We have audited the accompanying financial report of the Pilbara Regional Council (the “Council”), which comprises the statement of financial position as at 30 June 2016, the statement of comprehensive income by nature or type, statement of comprehensive income by program, statement of changes in equity and statement of cash flows for the year then ended, notes comprising a summary of significant accounting policies and other explanatory information to the financial report and the statement by the Chief Executive Officer.

Responsibility of the Council for the financial report The Council of the Pilbara Regional Council is responsible for the preparation and fair presentation of the financial report in accordance with Australian Accounting Standards (including the Australian Accounting Interpretations) and the Local Government Act 1995 Part 6. This responsibility includes establishing and maintaining internal control relevant to the preparation and fair presentation of the financial report that is free from material misstatement, whether due to fraud or error; selecting and applying appropriate accounting policies; and making accounting estimates that are reasonable in the circumstances.

Auditor’s responsibility Our responsibility is to express an opinion on the financial report based on our audit. We conducted our audit in accordance with Australian Auditing Standards. These Auditing Standards require that we comply with relevant ethical requirements relating to audit engagements and plan and perform the audit to obtain reasonable assurance whether the financial report is free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial report. The procedures selected depend on the auditor’s judgement, including the assessment of the risks of material misstatement of the financial report, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial report in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by the Council, as well as evaluating the overall presentation of the financial report.

19

Freedom of Information

In accordance with Section 96 and 97 of the Freedom of Information Act 1992, Council is required to publish an Information Statement which details the process of applying for information under the Act, as well as information that the Council provides outside the Act. During 2015/16 the PRC received no applications under the Freedom of Information Act 1992.

Disability Access and Inclusion Plan

The Pilbara Regional Council has developed a Disability Access and Inclusion Plan to ensure that people with disabilities are included and can access and use facilities, services and functions provided by the PRC.

The plan is reviewed biennially, at which time it may be amended and extended as new strategies are identified and priorities change. For the purposes of this Plan, the World Health Organisation’s definition of disability is utilised: “Disability is a loss or reduction of functional ability which results from an impairment. An impairment is defined as an anatomical or functional

stAtutoRY RepoRts

abnormality or loss which may or may not result in a disability.”

The PRC DAIP includes: Principles applicable to people with disabilities; A disability anti-discrimination statement; Functions, facilities and services provided by the PRC; A statement of Outcomes relevant to this Plan; and Strategies to improve access and inclusion in the PRC

The PRC DAIP can be accessed via Council¹s website at www.prc.wa.gov.au

National Competition Policy

Under the terms of the Competition Principles Agreement between the Commonwealth and the States, Local Governments, including Regional Councils, are required to report on their operations in relation to competition principles, in order to determine whether any inequities occur. In the event that there are any areas found where competition principles are not equitable, the Local Government is required to provide a plan for achieving competitive neutrality or determine why it is in the best interests of the community for the inequity to continue.

1.

2.3.

4.

5.

20

The Pilbara Regional Council did not, during the 2015/2016 financial year, engage in any activities which affected competitive neutrality.

Legislation Review

The Pilbara Regional Council has no legislation in place that is subject to review.

Public Interest Disclosure Act

The Pilbara Regional Council did not have any reportable matters relating to the Public Interest Disclosure Act.

Payments to Employees

In accordance with the requirements of s19B of the Local Government (Administration) Regulations 1996 (as amended), there is one employee of the Pilbara Regional Council entitled to a salary of $100,000 or more.

Purchasing Policy

The Regional Council maintained compliance with the Local Government Act, for all purchases of goods and/or

services ensuring consistency and value for money for all purchasing activities.

State Records Act

Being a very small authority, records are maintained in a paper format with some electronic records. The State Records Act 2000 states that an organisation must review its Plan within five years of the approval date. The PRC reviewed its Record Keeping Plan in 2011/2012 and received approval of its Record Keeping Plan from the State Records Commission in March 2012.

Conduct of Certain Officials – Local Government Act 1995

Section 5.53 of the Local Government Act states that the annual report is to contain details of entries made under section 5.121 during the financial year in the register of complaints. For the 2015-2016 financial year, there were no entries made in the Register of Complaints.

21

finAnciAl RepoRt foR thefinAnciAl YeAR ended30th June 2016

Statement by Chief Executive Officer

Statement of Comprehensive Income by Nature or Type

Statement of Financial Position

Statements of Changes in Equity

Statement of Cash Flows

Rate Setting Statement

Notes to and Forming Part of the Financial Report

22

23

24

25

26

27

28

22

stAtement bY the ceo

The attached financial report of the Regional Council being the annual financial report and other information for the

financial year ended 30 June 2016 are in my opinion properly drawn up to present fairly the financial position of the

Regional Council at 30th June 2016 and the results of the operations for the financial year then ended in accordance

with the Australian Accounting Standards and comply with the provisions of the Local Government Act 1995 and the

regulations under that Act.

Signed as authorisation of issue on the 26 October 2016

Anthony Friday

Chief Executive Officer

23

Operating Grants, Subsidies and ContributionsFees and ChargesInterest Earnings

Employee CostsMaterials and ContractsUtility ChargesDepreciation on Non-Current AssetsInsurance ExpensesOther Expenditure

2,026,588-

122,2662,148,854

27262(a)

1,888,95141,247

103,6032,033,801

Revenue

Expenses

note 2016$

2015$

1,492,50033,00067,396

1,592,896

2016budget

$

2(a)

Changes on revaluation of non-current assetsTotal Other Comprehensive Income

Loss on Asset Disposal

Net Result

-

(3,553,220)

-

(4,052,500)

-

(1,674,065)

(3,553,220) (4,052,500) (1,674,065)

--

--

--

Other Comprehensive Income

Total Comprehensive Income

19

10

stAtement of compRehensive income bY nAtuRe oR tYpe

FOR THE YEAR ENDED 30th June 2016

This statement is to be read in conjunction with the accompanying notes.

(733,650)(4,640,097)

(21,600)(4,500)

(25,000)(220,549)

(5,645,396)(4,052,500)

(690,244)(4,782,109)

(15,333)(3,118)

(21,188)(190,082)

(5,702,074)(3,553,220)

(602,809)(2,870,772)

(9,641)(5,156)

(23,431)(196,057)

(3,707,866)(1,674,065)

24

Cash and Cash EquivalentsTrade and Other Receivables

Provisions

Property, Plant and Equipment

Current LiabilitiesTrade and Other PayablesProvisions

45

9

6

79

1,748,789357,724

4,992,46289,939

13,925 14,766

--

3,118

618,10521,978

32,93232,096

Current Assets

Non-Current Assets

Non-Current Liabilities

EquityRetained Surplus

Total Equity

1,452,505

1,452,505

5,005,725

5,005,725

note 2016$

2015$

STATEMENT OF FINANCIAL POSITION

AS AT 30th June 2016

This statement is to be read in conjunction with the accompanying notes.

Total Current Liabilities

Total Current Assets 2,106,513

2,106,513

640,083 65,028

13,925654,008

1,452,505 5,005,725

14,76679,794

5,082,401

5,085,5193,118Total Non-Current Assets

Total Assets

Total Liabilities

Net Assets

Total Non-Current Liabilities

25

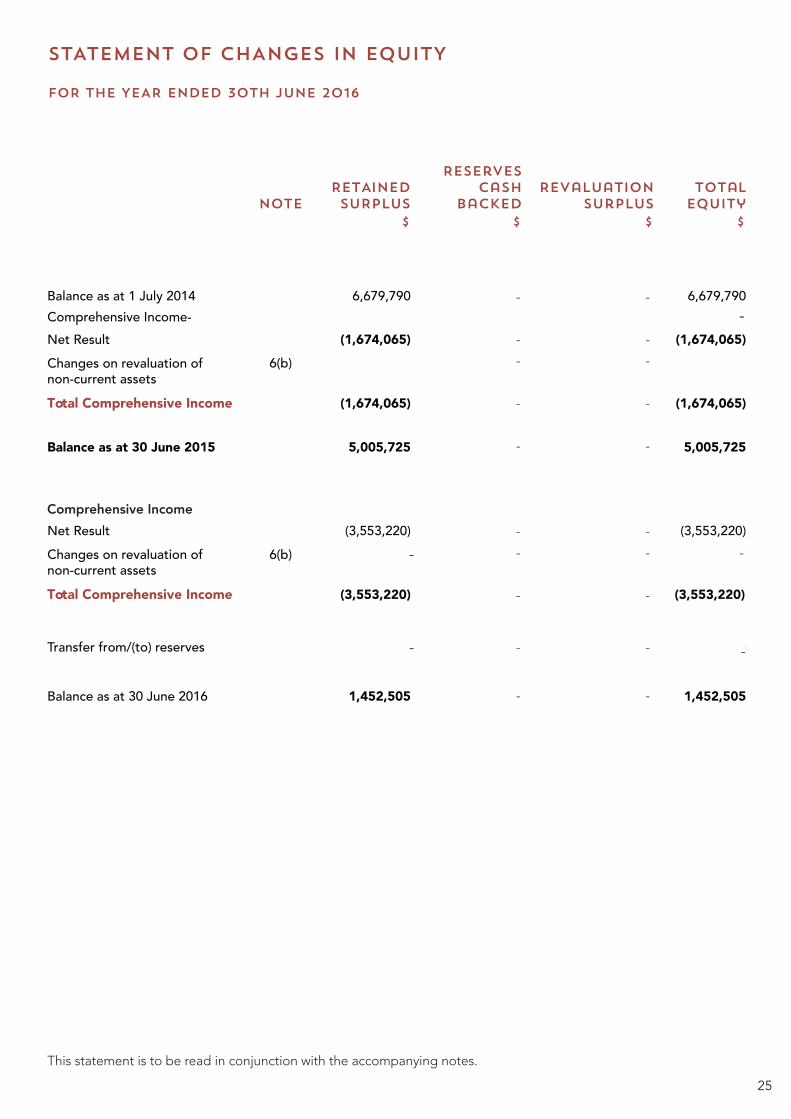

STATEMENT OF CHANGES IN EQUITY

FOR THE YEAR ENDED 30th June 2016

Revenue

noteRetAinedsuRplus

Revaluationsurplus

totalequity

Reservescash

backed

Balance as at 1 July 2014 6,679,790 6,679,790Comprehensive Income-Net Result (1,674,065)

6(b)

6(b)

(1,674,065)

Changes on revaluation ofnon-current assetsTotal Comprehensive Income

Net Result (3,553,220) (3,553,220)Changes on revaluation ofnon-current assets

Transfer from/(to) reserves

Balance as at 30 June 2016 1,452,505 1,452,505

Total Comprehensive Income

Balance as at 30 June 2015

(1,674,065)

5,005,725 5,005,725

(3,553,220) (3,553,220)

(3,553,220) (3,553,220)

(1,674,065)

$$ $$

-

-

-

$$ $ $

-

This statement is to be read in conjunction with the accompanying notes.

Comprehensive Income

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

-

- -

- -

26

Operating Grants, Subsidies and ContributionsFees and chargesInterest EarningsGoods and Services Tax

Payments for Purchase of Property, Plant & EquipmentProceeds from Sales of Fixed AssetsNet Cash Provided By (Used In)Investment Activities

Net Increase (Decrease) in Cash HeldCash at Beginning of the YearCash and Cash Equivalentsat the End of the Year

(3,243,673)4,992,462

1,748,789

(3,933,217)4,634,192

700,975

(2,007,273)6,999,735

4,992,462

Employee CostsMaterials and ContractsUtility ChargesInsurance ExpensesGoods and Services TaxOther Expenditure

2,092,062-

122,266306,288

2,520,616

(710,947)(4,246,464)

(13,445)(21,188)

(577,951)(194,294)

(5,764,289)

(584,254)(2,874,400)

(9,641)(23,431)

(570,747)(184,951)

(4,247,424)

1,830,05741,247

103,603268,652

2,243,559Payments

Net Cash Provided By (Used In)Operating Activities (3,243,673)12 (b)

12 (a)

note 2016$

2015$

---

---

(3,408)-

(3,408)

---

(754,795)(4,625,597)

(21,600)(25,000)

(330,000)(220,549)

(5,977,541)

1,613,92833,00067,396

330,0002,044,324

2016budget

$

(3,933,217) (2,003,865)

Net Cash Provided By (Used In)Financing Activities -- -

Cash Flows from Investing Activities

STATEMENT OF CASH FLOWS

FOR THE YEAR ENDED 30TH JUNE 2016

-

This statement is to be read in conjunction with the accompanying notes.

27

GovernanceGeneral Purpose FundingCommunity amenitiesRecreation and cultureTransportEconomic Services

1,505,862122,266

-346,664

-174,062

2,148,854

1,025,50067,396

-500,000

--

1,592,896

1,562,380103,603

-300,00067,818

-2,033,801

Governance

Community amenities

Recreation and culture

Transport

Economic Services

(Profit/Loss on Asset Disposals

Movement resulting in impairment of assets

Movement in Employee Benefit Provisions

(Non-Current)

Depreciation and Amortisation on Assets

Capital Expenditure and RevenuePurchase Furniture and Equipment

Proceeds from Disposal of Fixed Assets

Transfer to reserves (restricted assets)

Transfers to reserves (restricted assets)

ADD Estimated Surplus/(Deficit) July 1 B/Fwd

LESS Estimated Surplus/(Deficit) June 30 C/Fwd

Total Amount Raised from General Rate

19

2a

6b

19

10

10

21(a)

21(a)

21(a)

-

-

8,500

4,500

-

-

-

-

4,722,610

(683,110)-

-

-

(841)

3,118

-

-

-

-

5,017,372

1,466,429-

-

11,105

3,853

3,118

5,156

(3,408)

-

6,674,731

5,017,372-

(5,281,554)

-

(267,328)

-

(153,192)

(4,835,396)

-

(700,000)

-

(110,000)

(1,852,193)

(24,584)

(43,533)

-

Revenue

Expenses

Adjustments for Cash Budgets Requirements

Net Result Excluding Rates

note 2016$

2015Actual

$

2016budget

$

(5,702,074) (5,645,396) (3,707,866)

(3,553,220) (4,052,500) (1,674,065)

RATE SETTING STATEMENT

FOR THE YEAR ENDED 30TH JUNE 2016

5,156

-

-

(3,408)

This statement is to be read in conjunction with the accompanying notes.

(1,787,556)

28

1. SIGNIFICANT ACCOUNTING POLICIES

(a) Basis of Preparation

The financial report comprises general purpose financial statements which have been prepared in accordance with Australian Accounting Standards (as they apply to local governments and not-for-profit entities), Australian Accounting Interpretations, other authoritative pronouncements of the Australian Accounting Standards Board, the Local Government Act 1995 and accompanying regulations. Material accounting policies which have been adopted in the preparation of this financial report are presented below and have been consistently applied unless stated otherwise.

Except for cash flow and rate setting information, the report has been prepared on the accrual basis and is bases on historical costs, modified, where applicable, by the measurement at fair value of selected non-current assets, financial assets and liabilities.

Critical Accounting Estimates

The preparation of a financial report in conformity with Australian Accounting Standards requires management to make judgements, estimates and assumptions that effect the application of policies and reported amounts of assets and liabilities, income and expenses.

The estimates and associated assumptions are based on historical experience and various other factors that are believed to be reasonable under the circumstances; the results from which form the basis of making the judgments about carrying values of assets and liabilities that are not readily apparent form other sources. Actual results may differ from these estimates.

The Local Government Reporting Entity

All funds through which the Regional Council controls resources to carry on its functions have been included in the financial statements forming part of this financial report.

In the process of reporting on the local government as a single unit, all transactions and balances between those Funds (for example, loans and transfers between Funds) have been eliminated.

(b) Goods and Services Tax (GST)

Revenues, expenses and assets are recognised net of the amount of GST, except where the amount of GST incurred is not recoverable from the Australian Taxation Office (ATO).

Receivables and payables are stated inclusive of GST receivable or payable.

The net amount of GST recoverable from, or payable to, the ATO is included with receivables or payables in the statement of financial position.

Cash flows are presented on a gross basis. The GST components of cash flows arising from investing of financing activities which are recoverable from, or payable to, the ATO are presented as operating cash flows.

notes to And foRming pARt of the finAnciAl RepoRt

As of 30th June 2016

29

(c) Cash and Cash Equivalents

Cash and cash equivalents include cash on hand, cash at bank, deposits available on demand with banks and other short term highly liquid investments that are readily convertible to known amounts of cash and which are subject to an insignificant risk of changes in value and bank overdrafts.

Bank overdrafts are reported as short term borrowings in current liabilities in the statement of financial position.

(d) Trade and Other Receivables

Trade and other receivables include amounts due from ratepayers for unpaid rates and service charges and other amounts due from third parties for goods sold and services performed in the ordinary course of business.

Receivables expected to be collected within 12 months of the end of the reporting period are classified as non-current assets.

Collectability of trade and other receivables is reviewed on an ongoing basis. Debts that are known to be uncollectible are written off when identified. An allowance for doubtful debts is raised when there is objective evidence that they will not be collectible.

(e) Inventories

General

Inventories are measured at the lower of cost and net realisable value.

Net realisable value is the estimated selling price of the ordinary course of business less the estimated costs of completion and the estimated costs necessary to make the sale.

Land held for sale

Land held for development and sale is valued at the lower of cost and net realisable value. Cost includes the cost of acquisition, development, borrowing costs and holding costs until completion of development. Finance costs and holding charges incurred after development is completed are expensed.

Gains and losses are recognised in profit or loss at the time of signing an unconditional contract of sale if significate risks and rewards, and effective control over the land, are passed on to the buyer at this point.

Land held for sale is classified as current except where it is held as non-current based on the Council’s intentions to release for sale.

(f) Fixed Assets

Each class of fixed assets within either property, plant and equipment or infrastructure, is carried at cost or fair value as indicated, less where applicable, any accumulated depreciation and impairment losses.

Mandatory Requirement to Revalue Non-Current Assets

Effective from 1 July 2012, the Local Government (Financial Management) Regulations were amended and the measurement of non-current assets at Fair Value became mandatory.

The amendments allow for a phasing in of fair value in relation to fixed assets over three years as follows:

(a) for the financial year on 30 June 2013, the fair value of all the assets of the local government that are plant and equipment; and

(b) for the financial year ending on 30 June 2014, the fair value of all of the assets of the local government.

(i) that are plant and equipment and(ii) that are – (I) land and buildings: (II) infrastructure;and

(c) for a financial year ending on or after 30 June 2015, the fair value of all of the assets of the local government.

Thereafter, in accordance with the regulations, each asset class must be revalued at least every 3 years.

In 2013, the Regional Council commenced the process of adopting Fair Value in accordance with the regulations.

Relevant disclosures, in accordance with the requirements of Australian Accounting Standards, have been made in the financial report as necessary.

Land under control

In accordance with Local Government (Financial Management) Regulation 16(a), the Regional Council was required to include as an asset (by 30 June 2013), Crown Land operated by the local government as a golf course, showground, racecourse or other sporting or recreational facility of State or Regional significance.

30

Upon initial recognition, these assets were recorded at cost in accordance with AASB 116. They were then classified as land and revalued along with other land in accordance with the other policies detailed in this Note.

Initial Recognition and Measurement between Mandatory Revaluation Dates

All assets are initially recognised at cost and subsequently revalued in accordance with the mandatory measurement framework detailed above.

In relation to this initial measurement, cost is determined as the fair value of assets given as consideration plus costs incidental to the acquisition. For assets acquired at no cost for nominal consideration, cost is determined as fair value at the date of acquisition. The cost of non-current assets constructed by the Regional Council includes the cost of all materials used in construction, direct labour on the project and appropriate proportion of variable and fixed overheads.

Individual assets acquired between initial recognition and the next revaluation of the asset class in accordance with the mandatory measurement framework detailed above, are carried at costs less accumulated depreciation as management believes this approximates fair value. They will be subject to subsequent revaluation at the next anniversary date in accordance with the mandatory measurement framework detailed above.

Revaluation

Increases in the carrying amount arising on revaluation of assets are credited to a revaluation surplus in equity. Decreases that offset previous increases of the same asset are recognised against revaluation surplus directly in equity. All other decreases are recognised profit and loss.

Land Under Roads

In Western Australia, all land under roads is Crown Land, the responsibility for managing which, is vested in local government.

Effective as at 1 July 2008, Council elected not to recognise any value for land under roads acquired on or before 30 June 2008. This accords with the treatment

available in Australian Accounting Standards AASB 1051 Land Under Roads and the fact Local Government (Financial Management) Regulation 16(a)(i) prohibits local governments from recognising such land as an asset.In respect of land under roads acquired on or after 1 July 2008, as detailed above, Local Government (Financial Management) Regulation 16(a)(i) prohibits local governments from recognising such land as an asset.

Whist such treatment is inconsistent with the requirements of AASB 1051, Local Government (Financial Management) Regulation 4(2) provides in the event of such an inconsistency, the Local Government (Financial Management) Regulations prevail.

Consequently, any land under roads, acquired on or after 1 July 2008 is not included as an asset of the Council.

Depreciation

The depreciable amount of all fixed assets including buildings but excluding freehold land, are depreciated on a straight-line basis over the individual asset’s useful life from time to time the asset is held ready for use. Leasehold improvements are depreciated over the shorter of either the unexpired period of the lease or the estimated useful life of the improvements.

When an item of property, plant and equipment is revalued, any accumulated depreciation at the date of revaluation is treated in one of the following ways:

(a) Restated proportionately with the change in the gross carrying amount of the asset so that the carrying amount of the asset after revaluation equals its revalued amount; or

(b) Eliminated against the gross carrying amount of the asset and the net amount restated to the revalued amount of the asset.Major depreciation periods used for each class of depreciable asset are:

Furniture and (Internal) Equipment- computers and peripherals 32% 4 to 10 years- other electronic equipment 18% 4 to 10 years- furniture 9% 4 to 10 years

The assets residual values and useful lives are reviewed,

notes to And foRming pARt of the finAnciAl RepoRt

foR the YeAR ended 30th June 2016

1. significAnt Accounting policies >>

31

and adjusted if appropriate, at the end of each reporting period.

An asset’s carrying amount is written down immediately to its recoverable amount if the asset’s carrying amount is greater than its estimated recoverable amount.

Gains and losses on disposals are determined by the comparing proceeds with the carrying amount. These gains and losses are included in the statement of comprehensive income in the period in which they arise.

Capitalisation Threshold

Expenditure on items of equipment under $3,000 is not capitalised. Rather, it is expensed and is recorded on an asset inventory listing.

(g) Fair Value of Assets and Liabilities

When performing a revaluation, the Regional Council uses a mix of both independent and management valuations using the following as a guide.

Fair Value is the price that the Regional Council would receive to sell the asset or would have to pay to transfer a liability, in an orderly (i.e. unforced) transaction between independent, knowledgeable and willing market participants at the measurement date.

As far as value is a market-based measure, the closest equivalent observable market pricing information is used to determine fair value. Adjustments to market values may be made having regard to the characteristics of the specific asset or liability. The fair values of assets that are not traded in an active market are determined using one or more valuation techniques. These valuation techniques maximise, to the extent possible, the use of observable data.

To the extent possible, market information is extracted from either the principal market for the asset or liability (i.e. the market with the greatest volume and level of activity for the asset or liability) or, in the absence of such a market, the most advantageous market available to the entity at the end of the reporting period (i.e. the market that maximises the receipts from the sale of the asset after taking into account transaction costs and transport costs.

For non-financial assets, the fair value measurement also takes into account a market participants ability to use the assets in its highest and best use or to sell it to another market participant that would use the asset in its highest and best use.

Fair Value Hierarchy

AASB 13 requires the disclosure of fair value information of the fair value hierarchy, which categorises fair value measurement into one of the three possible levels based on the lowest level that an input is significant to the measurement can be categorised as follows:

Valuation techniquesThe Regional Council selects a valuation technique that is appropriate in the circumstances and for which sufficient data is available to measure fair value. The availability of sufficient and relevant data primarily depends on the specific characteristics of the asset or liability being measured. The valuation techniques selected by the Regional Council are consistent with one or more of the following valuation approaches:

Market approachValuation techniques that use prices and other relevant information generated by the market transactions for identical or similar assets or liabilities.

Income approachValuation techniques that convert estimated future cash flows or income and expenses into a single discounted present value.

Level 1Measurements based on quoted prices (unadjusted) in active markets for identical assets or liabilities that the entity can access at the measurement date.

Level 2Measurements based on the inputs other than quoted prices included in Level 1 that are observable for the assets or liability, either directly or indirectly.

Level 3Measurements based on unobservable inputs for the asset or liability.

The fair values of assets and liabilities that are not traded in an active market are determined using one or more valuation techniques. These valuation techniques maximise, to the extent possible, the use of observable market data. If all significant inputs required to measure fair value are observable, the asset or liability is included in Level 2. If one or more significant inputs are not based on observable market data, the asset or liability is included in Level 3.

32

Cost approachValuation techniques that reflect the current replacement cost of an asset at its current service capacity.

Each valuation technique requires inputs that reflect the assumptions that buyers and sellers would use when pricing the asset or liability., including assumptions about risks. When selecting a valuation technique, the Regional Council gives priority to those techniques that maximise the use of observable inputs and minimise the use of unobservable inputs. Inputs that are developed using market data (such as publicly available information on actual transactions) and reflect the assumptions that buyers and sellers would generally use when pricing the asset or liability are considered observable, whereas inputs for which market data is not available and therefore are developed using the best information available about such assumptions are considered unobservable.

As detailed above, the mandatory measurement framework imposed by the Local Government (Financial Management) Regulations requires, as a minimum, all assets carried at a revalued amount to be revalued at least every 3 years.

(h) Financial Instruments

Initial Recognition and MeasurementFinancial assets and financial liabilities are recognised when the Regional Council becomes a party to the contractual provisions to the instrument. For financial assets, this is equivalent to the dated that the Regional Council commits itself to either the purchase or sale of the asset (i.e. trade date accounting is adopted).

Financial instruments are initially measured at fair value plus transaction costs, except where the instrument is classified ‘at fair value through profit or loss’, in which case transaction costs are expensed to the profit or loss immediately.

Classification and Subsequent MeasurementFinancial instruments are subsequently measured at fair value, amortised cost using the effective interest rate method or cost.

Amortised cost is calculated as:

(a) the amount in which the financial asset or financial liability is measured at initial recognition;

(b) less principal repayments and any reduction for impairment and

(c) plus or minus the cumulative amortisation of the difference, if any, between the amount initially recognised and the maturity amount calculated using the effective interest rate method.

The effective interest method is used to allocate interest income or interest expense over the relevant period and is equivalent to the rate that discounts estimated future cash payments or receipts (including fees, transaction costs and other premiums or discounts) through the expected life (or when this cannot be reliably predicted, the contractual term of the financial instrument to the net carrying amount of the financial asset or financial liability. Revisions to expected future net cash flows will necessitate an adjustment to the carrying value with a consequential recognition of an income or expense in profit or loss.

(i) Financial assets at fair value through profit and loss

Financial assets are classified at “fair value through profit or loss” when they are held for trading for the purpose of short-term profit taking. Such assets are subsequently measured at fair value with changes in carrying amount being included in profit or loss. Assets in this category are classified as current assets.

(ii) Loans and receivables

Loans and receivables are non-derivative financial assets with fixed or determinable payments that are not quoted in an active market and are subsequently measured at amortised cost. Gains or losses are recognised in profit or loss.

Loans and receivables are included in current assets where they are expected to mature within 12 months after the end of the reporting period.

(iii) Held-to-maturity investments

notes to And foRming pARt of the finAnciAl RepoRt

foR the YeAR ended 30th June 2016

1. significAnt Accounting policies >>

33

Held-to-maturity investments are non-derivative financial assets with fixed maturities and fixed or determinable payments that the Regional Council has the positive intention and ability to hold onto maturity. They are subsequently measured at amortised cost. Gains or losses are recognised in profit or loss.

Held-to -maturity investments are included in non-current assets, where they are expected to mature within 12 months after the end of the reporting period. All other investments are classified non-current.

(iv) Available-for -sale financial assets

Available-for-sale financial assets are non-derivative financial assets that are either not suitable to be classified into other categories of financial assets due to their nature, or they are designated as such by management. They comprise investments in the equity of other entities where there is neither a fixed maturity nor fixed or determinable payments.

They are subsequently measured at fair value with changes in such fair value (i.e. gains or losses) recognised in other comprehensive income (except for impairment losses). When the financial asset is derecognised, the cumulative gain or loss pertaining to that asset previously recognised in other comprehensive income is reclassified into profit and loss.

Available-for-sale financial assets are included in current assets where they are expected to be sold within 12 months after the end of the reporting period. All other available-for-sale financial assets are classified as non-current.

(v) Financial Liabilities

Non-derivative liabilities (excluding financial guarantees) are subsequently measured at amortised cost. Gains and losses are recognised in profit or loss.

Impairment

A financial asset is deemed to be impaired if, and only it, there is objective evidence of impairment as a result of one or more events (a “loss event”) having occurred, which will have an impact on the estimated future cash flows of the financial asset(s).

In the case of available-for-sale financial assets, a significant or prolonged decline in the market value of the instrument is considered a loss event. Impairment losses are recognised in profit or loss immediately. Also, any cumulative decline in fair value previously recognised

in other comprehensive decline in fair value previously recognised in other comprehensive income is reclassified to profit or loss at this point.

In the case of financial assets carried at amortised cost, loss events may include: indications that the debtors or a group of debtors are experiencing significant financial difficulty, default or delinquency in interest or principal payments; indications that they will enter bankruptcy or other financial reorganisation; and changes in arrears or economic conditions that correlate with defaults.

For financial assets carried at amortised cost (including loans and receivables), a separate allowance account is used to reduce the carrying amount of financial assets impaired by credit losses after having taken all possible measures of recovery, if management establishes that the carrying amount cannot be recovered by any means, at that point the written-off amounts are charged to the allowance account or the carrying amount of impaired financial assets is reduced directly if no impairment amount was previously recognised in the allowance account.

Derecognition

Financial assets are derecognised where the contractual rights to receipt of cash flows expire or the asset is transferred to another party whereby the Regional Council is no longer has any significant continual involvement in the risks and benefits associated with the asset.

Financial liabilities are derecognised where the related obligations are discharged, cancelled or expired. The difference between the carrying amount of the financial liability extinguished or transferred to another party and the fair value of the consihhderation paid, including the transfer of non-cash assets or liabilities assumed, is recognised in profit or loss.

(i) Impairment of Assets

In accordance with Australian Accounting Standard the Regional Council’s assets, other than inventories, are assessed at each reporting date to determine whether there is any indication they may be impaired.

Where such an indication exists, and impairment test is carried out on the asset by comparing the recoverable amount of the asset, being the higher of the asset’s fair value less costs to sell ad value in use, to the asset’s carrying amount.

Any excess of the asset’s carrying amount over its

34

recoverable amount is recognised immediately in profit or loss unless the asset is carried and revalued amount in accordance with another Standard (e.g. AASB 116) whereby any impairment loss of a revalued asset is treated as a revaluation decrease in accordance with that other standard.

For non-cash generating assets such as roads, drains public buildings and the like, value in use is represented by the depreciated replacement cost of the asset.

(j) Trade and other Payables

Trade and other payables represent liabilities for goods and services provided to the Regional Council prior to the end of financial year that are unpaid and arise when the Regional Council becomes obliged to make future payments in respect of these good and services. The amounts are unsecured, are recognised as a current liability and are normally paid within 30 days of recognition.

(k) Employee Benefits

Short-Term Employee BenefitsProvision is made for the Regional Council’s obligations for short-term employee benefits. Short-term employee benefits are benefits (other than termination benefits) that are expected to be settled wholly before 12 months after the end of the annual reporting period in which the employees render the related service, including wages, salaries and sick leave. Short-term employee benefits are measured at the (undiscounted) amounts expected to be paid when the obligation is settled.

The Regional Council’s obligations for short-term employee benefits such as wages, salaries and sick leave are recognised as part of current trade and other payables in the statement of financial position. The Regional Council’s obligations for employees’ annual leave and long service leave entitlements are recognised as provisions in the statement of financial position.

Other Long-Term Employee BenefitsProvision is made for employees’ long service leave and annual leave entitlements not expected to be settled wholly within 12 months after the end of the annual reporting period in which the employees render the

related service. Other long-term employee benefits are measured at present value of the expected future payments to be made to employees. Expected future payments incorporate anticipated future wage and salary levels, durations of service and employee departures are discounted at rates determined by reference to market yields at the end of the reporting period on government bonds that have maturity dates that approximate the terms of the obligations. Any remeasurements for changes in assumptions of obligations for other long-term employee benefits are recognised in profit or loss in the periods in which changes occur.

The Regional Council’s obligations for long-term employee benefits are presented as non-current provisions in its statement of financial position, except where the Regional Council does not have an unconditional right to defer settlement for at least 12 months after the end of the reporting period, in which case the obligations are presented as current provisions.

(l) Borrowing Costs

Borrowing costs are recognised as an expense when incurred except where they are directly attributable to the acquisition, construction or production of a qualifying asset. Where in this case, they are capitalised as part of the particular asset is substantially ready for its intended use or sale.

(m) Provisions

Provisions are recognised when the Regional Council has a present legal or constructive obligation, as a result of past events, for which it its probable that an outflow of economic benefits will result and that outflow can be reliably measured.

(n) Leases

Leases of fixed assets where substantially all the risks and benefits incidental to the ownership of the asset, but not legal ownership, are transferred to the Regional Council, are classified as finance leases.

Finance leases are capitalised recording an asset and a liability at the lower amounts equal to the fair value of the leased property for the present value of the minimum

notes to And foRming pARt of the finAnciAl RepoRt

foR the YeAR ended 30th June 2016

1. significAnt Accounting policies >>

35

lease payments. Lease payments are allocated between the reduction of the lease liability and the lease interest expense for the period.

Leased assets are depreciated on a straight line basis over the shorter of the estimated useful lives or the lease term.

Lease payments for operating leases, where substantially all the risks and benefits remain with the lessor, are charged as expenses in the periods in which they are incurred.

Lease incentives under operating leases are recognised as a liability and amortised on a straight line basis over the life of the lease term.

(o) Investment in Associates

An associate is an entity over which the Regional Council has significant influence. Significant influence is the power to participate in the financial operating policy decisions of that entity but is not control or joint control of these policies. Investments in associates are accounted for in the financial statements by applying the equity method of accounting, whereby the investment is initially recognised at cost and adjusted thereafter for the post-acquisition change in the Regional Council’s share of net assets of the associate. In addition, the Regional Council’s share of the profit or loss of the associate is included in the Regional Council’s profit or loss.

The carrying amount of the investment includes, where applicable, goodwill relating to the associate.

Any discount on acquisition, whereby the Regional Council’s share of the net fair value of the associate exceeds the cost of the investment, is recognised in profit or loss in the period in which the investment is acquired.

Profits and losses resulting from transactions between the Regional Council and the associate are eliminated to the extent of the Regional Council’s interest in the associate.