annual report fiscal year 2014/15 - aurubis · antamina expansion (pe) los bronces toromocho...

TRANSCRIPT

December 2015 1 1 1

Erwin Faust Executive Board Spokesman

Analyst Conference on December 11, 2015

Annual Report

Fiscal Year 2014/15

December 2015

December 2015

Agenda

2

1. Current situation and market trends

2. Aurubis’ market position

3. Financial data

4. Strategy and outlook

December 2015

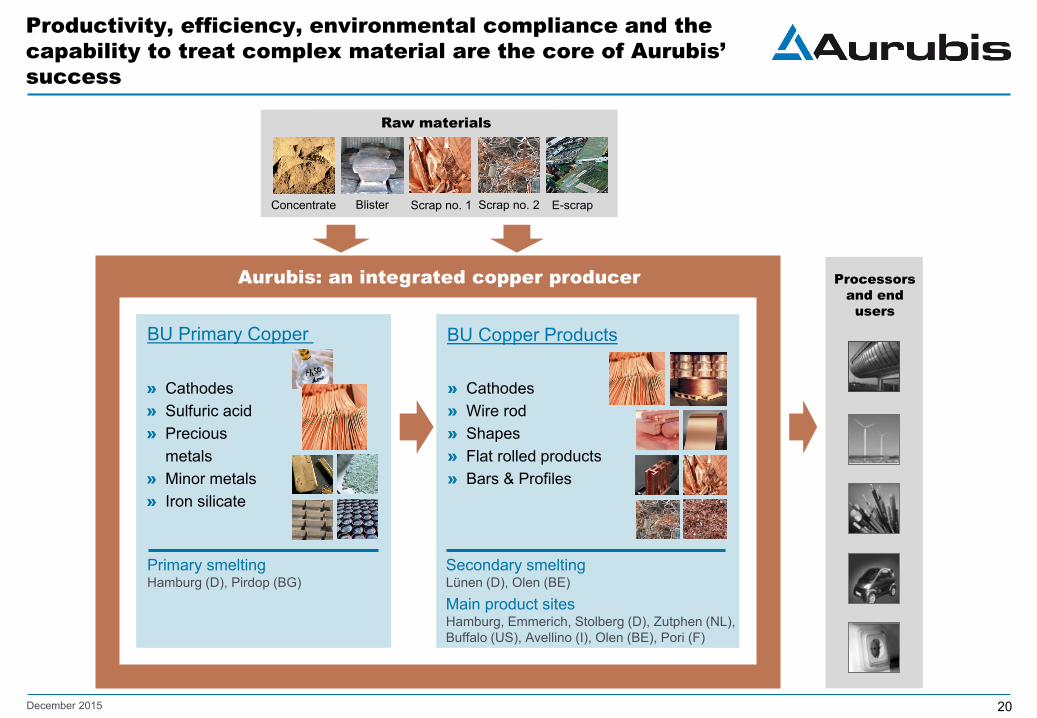

Productivity, efficiency, environmental compliance and the capability to treat complex material are the core of Aurubis’ success

Processors and end users

BU Copper Products

» Cathodes » Wire rod » Shapes » Flat rolled products » Bars & Profiles

BU Primary Copper

» Cathodes » Sulfuric acid » Precious

metals » Minor metals » Iron silicate

Secondary smelting Lünen (D), Olen (BE)

Main product sites Hamburg, Emmerich, Stolberg (D), Zutphen (NL), Buffalo (US), Avellino (I), Olen (BE), Pori (F)

Primary smelting Hamburg (D), Pirdop (BG)

Raw materials

Concentrate Blister Scrap no. 1 E-scrap Scrap no. 2

Aurubis: an integrated copper producer

3

December 2015

Aurubis achieves record earnings in 2014/15

4

12 months FY 2014/15

12 months FY 2013/14

Operating EBT (€ million) 343 137

Net cash flow (€ million) 365 401

ROCE (%) (operating) 18.7 8.5

December 2015

170

173

343

137

Substantial improvement in operating results compared to previous year

5

EBT 2014/15 (in € million, rounded)

FY 14/15

Operating EBT

Adjust- ments

Operating EBT

EBT IFRS

FY 13/14

Main factors influencing the results » Significantly higher treatment and refining charges

for copper concentrates

» A strong increase in sales prices for sulfuric acid

» Substantially increased refining charges for copper scrap

» Higher cathode premiums

December 2015

7.8 9.2 10.1 10.5 10.9 11.3 12.2

11.8 11.5 11.9 12.1 12.4 12.6

12.7

19.6 20.6 22.0 22.7 23.3 23.9

24.9

2013 2014 2015 2016e 2017e 2018e 2020e

Moderate growth expectations for China translate to lower copper demand forecasts

6

Global copper demand (in million t)

» The main drivers of copper demand are the infrastructure sector and consumer goods.

» Central applications include construction, energy production and distribution, electronics, cars and air conditioning.

» Despite slower growth, China is still the important driver of copper demand.

» Development in emerging countries and the use of new technologies will push copper demand outside of China in the future as well.

» Nevertheless, Chinese copper demand growth rates are falling from about 7 % in 2014 to an expected 3 to 4 % in the next few years.

China

Source: Wood Mackenzie 9/2015 + 11/2015

December 2015

Copper price: Downward trend with ongoing volatility

7

2000

3000

4000

5000

6000

7000

8000

9000

10000

0

250

500

750

1000

1250

1500

1750

2000

10/

10

04/

11

10/

11

04/

12

10/

12

04/

13

10/

13

04/

14

10/

14

04/

15

10/

15

in US$/t in 1,000 t Metal exchange inventories LME copper price (settlement)

Copper price and metal exchange inventories

Copper price December 10, 2015:

4,572.0

December 2015

From a euro perspective, the US dollar increase has mitigated the copper price reduction

8

2000

3000

4000

5000

6000

7000

8000

9000

10000

10/

10

04/

11

10/

11

04/

12

10/

12

04/

13

10/

13

04/

14

10/

14

04/

15

10/

15

LME copper price (settlement) – in US$/t

Copper price

LME copper price (settlement) – in €/t

December 2015

The European copper market traditionally exhibits a cathode deficit

9

• Copper demand by region in 2015 (in million t) • Copper surplus/deficit before adjustment (in million t)

Total demand 2015: 22.0 million t Global output 2015: 22.2 million t

2.4

13.8

0.6 0.1 0.2

-0.5

+2.8

+1.1 +0.4

-3.2

Source: Wood Mackenzie 11/2015

3.7 -0.7

0.7 -0.5

0.5 +0.8

December 2015

Additional projects will start up production before 2025

Size of deposits (in million t of copper content)

Copper price (in US$/t – 3-month quotation)

Source: info Mine, company data 10

Existing projects New projects

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

Collahuasi (CL)

Batu Hijau (ID)

Los Pelambres (CL)

Antamina (PE)

Esperanza (CL)

Los Pelambres Expansion (CL)

Antamina Expansion (PE)

Los Bronces Expansion (CL)

Salobo I (BR)

Toromocho (PE)

Caserones/Regalito (CL)

Oyu Tolgoi (MN)

Mina Ministro

Halees (CL)

Las Bambas

El Teniente (CL)

Quellaveco (PE)

Andina Expansion

(CL)

Chuquicamata underground (CL)

0

10

20

30

40

50

60

70

80

90

1995 2000 2005 2010 2015 2020 2025

December 2015

Chinese smelter capacities are increasing less than previously forecasted

11

Capacities of Chinese copper smelters incl. planned increases (in million t)

Source: Wood Mackenzie 09/2015

5

6

7

8

9

10

2014 2015 2016e 2017e 2018e 2019e

Forecast Jun 15 Forecast Sept 15

» In the short term, 10 leading Chinese copper smelters (including Jiangxi Copper and Tongling) want to reduce their refined copper output by 350,000 t in 2016.

» In the long term, these producers ask for increased approval hurdles for new smelting capacities.

December 2015

Agenda

12

1. Current situation and market trends

2. Aurubis’ market position

3. Financial data

4. Strategy and outlook

December 2015 13

Aurubis is a world leader in the copper value chain

Output FY 2014/15 Position

Concentrate processing 2,294,000 t No. 2 worldwide

Copper recycling 294,000 t No. 1 worldwide

Cathode production 1,138,000 t No. 3 worldwide

Rod production 764,000 t No. 1 worldwide

Shape production 170,000 t No. 1 in Europe

Strip production 216,000 t No. 1 worldwide

Gold production 45 t

Silver production 958 t

December 2015

Agenda

14

1. Current situation and market trends

2. Aurubis’ market position

3. Financial data

4. Strategy and outlook

December 2015

Record consolidated results – operating EBT and ROCE significantly up on previous year

15

FY FY Change

2014/15 2013/14 Absolute Relative

Revenues €m 10,995 11,241 -246 -2 %

Gross profit €m 1,173 937 +236 +25 %

EBITDA €m 500 288 +212 +74 %

EBIT €m 370 167 +203 >100 %

EBT €m 343 137 +206 >100 %

Consolidated net income €m 257 99 +158 >100 %

Net cash flow €m 365 401 -36 - 9 %

Return on capital employed (ROCE) % 18.7 8.5 - -

(operating IFRS)

December 2015

Reconciliation of balance sheet/income statement from IFRS (operating) to IFRS (average cost method)

16

IFRS based on operating

IFRS using average Adjustments

Balance sheet 9/30/2015

Total assets and liabilities 3,733 4,044 311 Assets Fixed assets Deferred tax assets Inventories

1,387

3 1,374

1,440

8 1,627

53

5 253

Equity and liabilities Equity Deferred tax liabilities

1,765

76

1,969

183

204 107

Income statement 10/1/2014 – 9/30/2015

Change in inventories 76 15 (61) Cost of materials (9,964) (10,067) (103) Gross profit 1,173 1,009 (164) Result from investments measured using the equity method

4 1 (3)

Earnings before taxes 343 170 (173) Income taxes (86) (36) 50 Consolidated net income 257 134 (123)

(in € million)

December 2015

Total assets and liabilities higher due to increased cash level, equity ratio improved

17

1,146 1,155

506 433

316 324

1,765 1,550

9/30/15 9/30/14

Assets

(operating IFRS in € million)

Equity and liabilities

3,462 3,733

Fixed assets

Inventories

Receivables, etc.

Cash and cash equivalents

453 187

519 570

1,374 1,298

1,387 1,407

9/30/15 9/30/14

(37%)

(37%)

(14%)

(12%)

(41%)

(37%)

(16%) (5%)

Equity*

Provisions

Borrowings

Other liabilities

* incl. consolidated profit, non-controlling interests

3,462 3,733

(47%)

(8%)

(14%)

(31%)

(45%)

(9%)

(13%)

(33%)

December 2015

Aurubis Group financial ratios reflect very good results of operations

18

9/30/2015 operating

9/30/2014 operating Target

Profitability ROCE*

18.7 %

8.5 %

15 %

Capital structure - Equity ratio (equity / total assets and liabilities) - Fixed asset cover (equity / fixed assets) - Intensity of investments (fixed assets / total assets and liabilities)

47.3 %

127.2 % 37.2 %

44.8 %

110.2 % 40.6 %

> 40 %

> 120 % < 40 %

Debt and interest coverage - Net debt / EBITDA

0.1

0.9

< 3

- EBITDA / net interest expense 18.3 9.2 > 5

Liquidity - Quick ratio (current assets - inventories + finished products + credit lines / current liabilities)

156.3 %

104.5 %

> 100 %

(operating IFRS)

* EBIT rolling last four quarters

December 2015

Change in the Aurubis Group’s organizational structure

» The previous organizational structure was based on three operating Business Units (BUs): Primary Copper, Recycling/Precious Metals and Copper Products

» Aurubis’ activities were reorganized into two operating BUs effective July 1, 2015 » BU Primary Copper includes

» The copper concentrate processing facilities and copper cathode production in Hamburg and Pirdop (Bulgaria)

» The Group’s precious metal division, which is centralized in Hamburg » BU Copper Products includes

» The recycling plant in Lünen and the production site in Olen (Belgium) for an extensive involvement of recycling in customer business

» The production and marketing of copper products » Group-wide functions support the operating BUs

» Newly established Supply Chain Management division: group-wide raw material management and sale of sulfuric acid and other specialty products

19

December 2015

Productivity, efficiency, environmental compliance and the capability to treat complex material are the core of Aurubis’ success

Processors and end users

BU Copper Products

» Cathodes » Wire rod » Shapes » Flat rolled products » Bars & Profiles

BU Primary Copper

» Cathodes » Sulfuric acid » Precious

metals » Minor metals » Iron silicate

Secondary smelting Lünen (D), Olen (BE)

Main product sites Hamburg, Emmerich, Stolberg (D), Zutphen (NL), Buffalo (US), Avellino (I), Olen (BE), Pori (F)

Primary smelting Hamburg (D), Pirdop (BG)

Raw materials

Concentrate Blister Scrap no. 1 E-scrap Scrap no. 2

Aurubis: an integrated copper producer

20

December 2015

Reconciliation of old and new Group structure

Operating EBT (in € million; previous year adjusted)

New structure FY 14/15

FY 13/14

Diff. 14/15 13/14

Primary Copper 256 130 126

Copper Products 130 55 75

Other/cons. (43) (48) 5

Consolidated earnings before taxes

343 137 206

Old structure FY 14/15

FY 13/14

Diff. 14/15 13/14

Primary Copper 281 141 140

Rec./Prec. Metals 55 15 40

Copper Products 50 29 21

Other/cons. (43) (48) 5 Consolidated earnings before taxes

343 137 206

» BU Primary Copper: includes precious metals (previously BU Recycling/Precious Metals)

» BU Copper Products: includes Lünen recycling plant (previously BU Recycling/Precious Metals) and Olen site (previously divided between BU Primary Copper and BU Copper Products)

21

December 2015

Reconciliation of old and new Group structure (Q4)

22

Operating EBT (in € million; previous year adjusted)

New structure Q4 14/15

Q4 13/14

Diff. Q4 14/15 13/14

Primary Copper 54 61 (7)

Copper Products 40 26 14

Other/cons. (12) (25) 13

Consolidated earnings before taxes

82 62 20

Old structure Q4 14/15

Q4 13/14

Diff. Q4 14/15 13/14

Primary Copper 74 75 (1)

Rec./Prec. Metals 8 4 4

Copper Products 12 8 4

Other/cons. (12) (25) 13 Consolidated earnings before taxes

82 62 20

» BU Primary Copper: includes precious metals (previously BU Recycling/Precious Metals)

» BU Copper Products: includes Lünen recycling plant (previously BU Recycling/Precious Metals) and Olen site (previously divided between BU Primary Copper and BU Copper Products)

December 2015

BU Primary Copper: All earnings drivers at a high level in a good market environment

23

Operating results in BU Primary Copper (fiscal year 2014/15)

BU Primary Copper

FY 14/15

FY 13/14

EBIT (in €m) 271.4 150.3

EBT (in €m) 256.2 130.2

ROCE (%) 31.1 16.9

(Quantities in 1,000 t)

Concentrates 2,294 2,221

Copper scrap 103 97

Cathodes 615 595

Sulfuric acid 2,200 2,125

Gold (t) 45 43

Silver (t) 958 1,000

» Significantly higher TC/RCs due to good availability on the concentrate markets with a very good metal gain

» Positive trends on the copper markets led to refining charges that were about 40 % up on the previous year

» Strong increase in sales prices (over 60 % compared to previous year) for sulfuric acid owing to good global demand

» Positive contribution to earnings due to higher cathode premiums

» The concentrate throughputs were only slightly up on the previous year and did not fully meet our expectations

» ROCE improved notably again compared to previous year » Prior-year earnings were strained by the extensive

maintenance and repair shutdown at the Hamburg site and delays during the restart of production

December 2015

BU Copper Products: Positive trend due to considerable increase in refining charges and higher cathode premiums

24

Operating results in BU Copper Products (fiscal year 2014/15)

» The recycling business benefited from a good supply with substantially increased refining charges; refining charges for copper scrap about 40 % above the previous year

» AURUBIS ROD recorded a slight increase compared to the previous year due to good ongoing European demand

» Cathode output was slightly down on the previous year. Higher cathode premiums led in total to positive earnings effects

» Higher contributions to earnings from BL Flat Rolled Products as restructuring continued

» KRS throughput lower than the previous year as a result of scheduled shutdowns

BU Copper Products

FY 14/15

FY 13/14

EBIT (in €m) 137.8 61.4

EBT (in €m) 130.1 55.2

ROCE (%) 12.9 6.0

(Quantities in 1,000 t)

Copper scrap 191 202

KRS throughput 269 301

Cathodes 523 531

Wire rod 764 742

Shapes 170 183

Strip and wire products 216 228

December 2015 25

Stable shareholder structure

Shareholder structure as of Dec 2014

» IPO in 1998 » Aurubis shares are in the Prime

Standard Segment of the Deutsche Börse

» Shares are listed in the MDAX and in the Global Challenges Index (GCX)

~25 %

~40 %

~35 %

Salzgitter AG

Institutional investors

Retail investors

December 2015

5 €

10 €

15 €

20 €

25 €

30 €

35 €

40 €

45 €

50 €

55 €

60 €

65 €

1/04

1/05

1/06

1/07

1/08

1/09

1/10

1/11

1/12

1/13

1/14

1/15

80%

90%

100%

110%

120%

130%

140%

150%

160%

170%

10/1

411

/14

12/1

41/

152/

153/

154/

155/

156/

157/

158/

159/

1510

/15

11/1

512

/15

AurubisDAXMDAX

Development of Aurubis share price

Closing prices of Aurubis shares (Xetra)

200 days average

Comparison of Aurubis shares with indices (September 30, 2014 = 100 %)

Market capitalization December 9, 2015: About € 2.6 billion

26

December 2015

1.20 1.35

1.10 1.00

1.35

10/11 11/12 12/13 13/14 14/15proposal

Executive Board and Supervisory Board propose a dividend payout of € 1.35 in line with the dividend policy

27

Aurubis dividend (in € per share)

51 54

46 51 53

10/11 11/12 12/13 13/14 14/15proposal

Payout ratio (in %)

December 2015

Agenda

28

1. Current situation and market trends

2. Aurubis’ market position

3. Financial data

4. Strategy and outlook

December 2015

Aurubis’ strategic orientation has proven itself and will continue

29

Markets

Solutions for customers &

suppliers

Full synergy potential of value chain

Multi-metal supply and recovery

Internation-alization

Sustainability Core metal copper

Production capability

& innovation

» The core metal, copper, is decisive for success

» Expand multi-metal supply and recovery by increasing production expertise

» Better understand the needs of customers and suppliers and develop new solutions

» Broaden the activities in the value chain – closer internal and external cooperation to achieve this objective

» More investments outside of Germany in order to enhance proximity to supply and sales markets

» Sustainability plays a central role in our activities » Production capability is a strength and driving force

of our success – innovation is the key factor

We will strengthen our leading market position and add more value for our suppliers and customers

December 2015

Main internal projects to enhance profitability

30

Fit for Future Pirdop: » Expanding capacity by about 170,000 t » Optimizing existing facilities Earnings Improvement Project: » Focus on Lünen and Hamburg sites » Improving productivity and processes » Optimizing throughput pix Review of Metallurgical Concepts: » Optimizing existing metallurgical flows for precious metals » Processing more complex input materials

Marketable Slag Product Project: » Reviewing technical possibilities for further reducing copper contents

in the slag » Exploring new sales options for slag

December 2015

Large-scale shutdown in Pirdop scheduled for Q3 2015/16

31

» Primary copper and sulfuric acid production facilities will be renovated in Bulgaria » The last shutdown of this kind in Pirdop was in 2007 » Scheduled shutdown period: about 50 days » Capital expenditure volume: approx. € 44 million » Expected EBT effect: about € 25 million

December 2015

We expect a good fiscal year in 2015/16 again

» Metal prices are currently very volatile and market opinions about future developments diverge considerably

» Continued good availability of copper concentrates should allow for a good volume supply with high TC/RCs

» Restrained market outlook for copper scrap at the moment due to reduced collecting activities resulting from lower metal prices

» Large-scale shutdown at the Pirdop site will cause a € 25 million strain on operating EBT » Sulfuric acid markets are currently under pressure due to a supply surplus and weak

fertilizer markets; ongoing short-term visibility makes a forecast difficult » Aurubis lowered the cathode premium for European customers from US$ 110/t to

US$ 92/t, taking into account expectations of weaker global demand » Current demand level expected to continue in copper product business » Improvement projects initiated in 2015 will partially influence earnings in the coming year,

but significant positive contributions to earnings are expected in future fiscal years

32

We expect both operating EBT and ROCE to be significantly lower in fiscal year 2015/16 compared to the reporting year.

December 2015 33 33 33

Erwin Faust Executive Board Spokesman

Analyst Conference on December 11, 2015

Annual Report

Fiscal Year 2014/15

December 2015

December 2015 34

Dieter Birkholz Senior Specialist +49 40 7883-3969 [email protected]

Angela Seidler Head of Investor Relations +49 40 7883-3178 [email protected]

Elke Brinkmann Senior Specialist +49 40 7883-2379 [email protected]

IR contacts:

Financial calendar

» Interim Report First 3 Months FY 2015/16 February 10, 2016 » Annual General Meeting 2016 February 24, 2016 » Interim Report First 6 Months FY 2015/16 May 10, 2016 » Interim Report First 9 Months FY 2015/16 August 10, 2016 » Annual Report 2015/16 December 14, 2016

December 2015 35

Annex 1: Company profile

» Founded in 1866 as Norddeutsche Affinerie AG in Hamburg » IPO in 1998 » Renamed in 2009 after the acquisition of Cumerio

» Production sites in European countries and North America with about

6,300 employees » Third largest producer of copper cathodes in the world with an annual

output of about 1.1 million t of copper cathodes » No. 1 copper recycler in the world » Largest rod producer in the world » One of the world’s leading copper foil and flat rolled product

manufacturers » Production capacities for approx. 1.3 million t of different copper

products » Global leader in environmental protection

Aurum + Rubrum = the red gold = Aurubis

December 2015

Annex 2: Primary copper production process

36

Copper concentrates

Flash smelter

Off-gas cleaning

Sulfuric acid plant

Anode furnace

Copper scrap

Copper matte (64 % Cu)

Blister copper (98 % Cu)

Converter

Copper (99.5 % Cu)

Anode casting wheel

Anode

Nickel sulfate

Precious metal refining

Anode slime Tankhouse

Cathode

December 2015 37

Annex 3: Aurubis AG’s sources of earnings

TC/RC Treatment and refining charge = Mines’ payments to smelters for processing copper concentrates into cathodes. Smelters’ central profit driver – primarily influenced by concentrate supply and demand

RC Refining charge = Fee for processing copper scrap, blister and recycling materials into cathodes; primarily influenced by the situation on the European scrap markets

Metal prices Price risks fundamentally eliminated at Aurubis by hedging; strong influence on revenues and working capital, also for our customers

Cathode premium Surcharge for high-quality cathodes (Grade A), premium for cathode delivery, paid by the customer; expresses the scarcity in structurally undersupplied markets

Shape surcharge Processing prices for converting cathodes into copper products (wire rod, shapes, flat rolled products, etc.), paid by the customer

Sulfuric acid Sulfuric acid (H2SO4) is a by-product of concentrate processing; 1 t of sulfuric acid is generally produced per t of concentrate treated

December 2015

Annex 4: European cathode premium

110

92

0

20

40

60

80

100

120

140

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

*201

2

2013

2014

2015

2016

(in US$/t; from June 1, 2012: Aurubis cathode premium )

* from June 1: US$ 86/t 38

December 2015 39

Disclaimer

Forward-looking statements This document contains forward-looking statements that involve risks and uncertainties, including statements about Aurubis’ plans, objectives, expectations and intentions. Readers are cautioned that forward-looking statements include known and unknown risks and are subject to significant business, economic and competitive uncertainties and contingencies, many of which are beyond the control of Aurubis. Should one or more of these risks, uncertainties or contingencies materialize, or should any underlying assumptions prove incorrect, actual results could vary materially from those anticipated, expected, estimated or projected.