annual results - stagecoach group

TRANSCRIPT

1

Annual ResultsYear ended 30 April 2013

26 June 2013

2

Cautionary statement

This document is solely for use in connection with a briefing on Stagecoach Group plc (“the Group”).

This document contains forward-looking statements that are subject to risk factors associated with, amongst other things, the economic and business circumstances occurring from time to time in the countries, sectors and markets in which the Group operates. It is believed that the expectations reflected in these statements are reasonable but they may be affected by a wide range of variables which could cause actual results to differ materially from those currently anticipated. No assurances can be given that the forward-looking statements in this presentation will be realised. The forward-looking statements reflect the knowledge and information available at the date of preparation.

This document is not a full record of the presentation because it does not include comments made verbally by Stagecoach Group management or by others.

3

ROSS PATERSONFINANCE DIRECTOR

4

A record of achievement...

Stagecoach continues to deliver

− 2012/13 results ahead of expectations – adjusted EPS up 19% to over 30p

− Adjusted EPS of 2.6 times pre-recession level

• 2012/13 30.2p versus 2006/7 11.7p

− Dividend up 10.3% to 8.6p

− Underpinned by robust and growing UK Bus profit

* Ten years ended 30 April 2013

5

And significant opportunities ahead

Development of further new products – e.g. UK sleepercoach

Continued confidence in the prospects for megabus.com

Deliver further value from UK Rail – extensions and bids

Strong financial position enables us to seize the opportunities

6

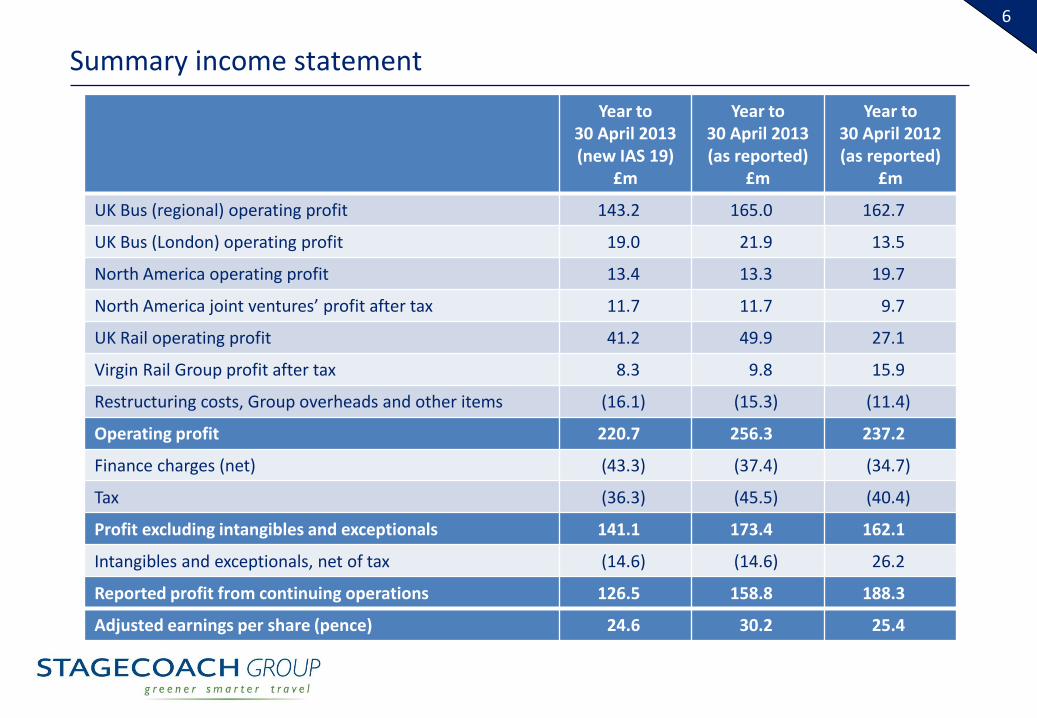

Summary income statement

Year to 30 April 2013(new IAS 19)

£m

Year to 30 April 2013(as reported)

£m

Year to 30 April 2012(as reported)

£m

UK Bus (regional) operating profit 143.2 165.0 162.7

UK Bus (London) operating profit 19.0 21.9 13.5

North America operating profit 13.4 13.3 19.7

North America joint ventures’ profit after tax 11.7 11.7 9.7

UK Rail operating profit 41.2 49.9 27.1

Virgin Rail Group profit after tax 8.3 9.8 15.9

Restructuring costs, Group overheads and other items (16.1) (15.3) (11.4)

Operating profit 220.7 256.3 237.2

Finance charges (net) (43.3) (37.4) (34.7)

Tax (36.3) (45.5) (40.4)

Profit excluding intangibles and exceptionals 141.1 173.4 162.1

Intangibles and exceptionals, net of tax (14.6) (14.6) 26.2

Reported profit from continuing operations 126.5 158.8 188.3

Adjusted earnings per share (pence) 24.6 30.2 25.4

7UK Bus (regional operations)Leading the sector

* Excludes inter-city coach services operated as a sub-contractor

Year to 30 April 2013

Year to 30 April 2012 Change

Revenue (£m) 966.7 909.7 6.3%

Like-for-like revenue (£m) 938.4 908.1 3.3%

Operating profit (£m) 165.0 162.7 1.4%

Operating margin (%) 17.1% 17.9% (80)bp

Estimated like-for-like passenger journeys* (m) 670.8 673.4 (0.4)%

Sector-leading profit margin underpinned by operational performance, low fares, continued investment

Over 5% commercial revenue growth

Profit growth notwithstanding c.£22m increase in fuel costs, net of duty rebate

c.£4m operating profit from Olympics and Paralympics contracts

Reducing reliance on under-pressure Government funding

8

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0%

Average Capex/

Revenue %

Operating margin

UK Bus capital expenditure v operating margin

Stagecoach

Major operator 1

Major operator 2

Major operator 3

Continued investment drives good profit margins

UK Bus (regional and London) additions to property, plant and equipment over the last reported five years have been measured as a percentage of revenue and then compared to the most recently reported operating margin (after applying any unallocated group overheads proportionate to revenue).

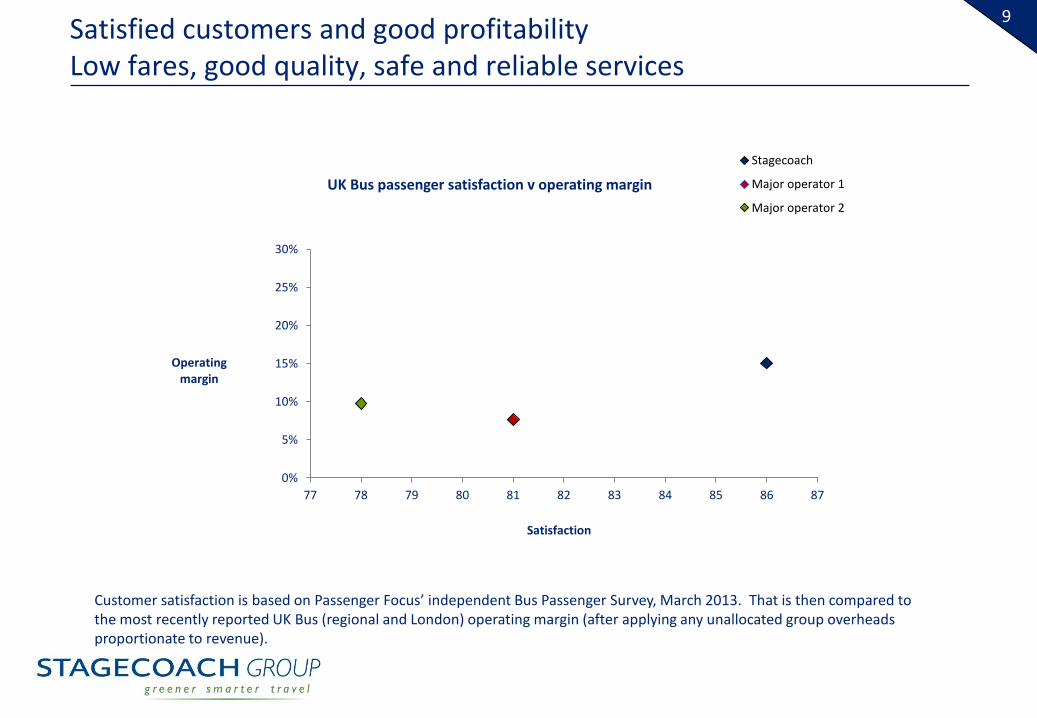

9Satisfied customers and good profitabilityLow fares, good quality, safe and reliable services

Customer satisfaction is based on Passenger Focus’ independent Bus Passenger Survey, March 2013. That is then compared to the most recently reported UK Bus (regional and London) operating margin (after applying any unallocated group overheads proportionate to revenue).

0%

5%

10%

15%

20%

25%

30%

77 78 79 80 81 82 83 84 85 86 87

Operating margin

Satisfaction

UK Bus passenger satisfaction v operating margin

Stagecoach

Major operator 1

Major operator 2

10

Developing further new products... with some free publicity

11UK Bus (London)Initial targets achieved

Year to 30 April 2013

Year to 30 April 2012 Change

Revenue and like-for-like revenue (£m) 232.7 230.5 1.0%

Operating profit (£m) 21.9 13.5 62.2%

Operating margin (%) 9.4% 5.9% 350bp

Successful turnaround of business acquired in 2010 for £59.5m

Targets set at time of acquisition now achieved

Cost savings from synergies

Restructured cost base enables business to effectively compete for new contracts

Better use of depot capacity

Market remains competitive

Focus turns to retaining tight control of costs and growing through new contract wins

12North AmericaA period of rapid expansion

Year to 30 April 2013

Year to 30 April 2012 Change

Revenue (US$m) 641.2 498.0 28.8%

Like-for-like revenue (US$m) 518.0 475.9 8.8%

Operating profit (US$m) 21.0 31.4 (33.1)%

Operating margin (%) 3.3% 6.3% (300)bp

Building for the future through acquisition and strong organic growth

July 2012 acquisitions from Coach America added over US$160m of annualised revenue

32% growth in megabus.com revenue

Annualised revenue (including share of joint venture) now over US$750m

Time to pause for breath at megabus.com and drive up profitability

Some development of services – Cleveland re-launch; Megabus Gold; Sleepercoach

Potential for significant step up in profit in 2013/14

− Full year effect of July 2012 acquisitions

− Improved megabus.com profit

13megabus.com in North AmericaA pathway to profitable growth

Features of 2012/13 Outlook for 2013/14

Increased price competition from other operators Not assuming any lessening of price competition

Start-up losses from new and fast-growing services Fewer new services to be added in 2013/14

Improved profitability of existing services

Precautionary measures following unrelated major accidents in first half of 2012/13

Maintain industry-leading safety record

Improved profitability from return to full operating capacity on all vehicles

Adverse weather Opportunity if weather is more “normal”

Lower load factors during winter Developing new timetables for winter 2013/14

Improved profitability from improved load factors

OVERALL Potential for significant step up in profitability

14

Successful integration of businesses acquired in 2012

Good progress integrating businesses acquired from Coach America

Revised network and restructured cost base at two businesses affected by competitor action post-acquisition

Progressing potential sale of one small business unit

Acquired depot infrastructure in Georgia, Texas, California and Ohio supporting megabus.com services

15UK RailThe right balance of risk and reward

Year to 30 April 2013

Year to 30 April 2012 Change

Revenue (£m) 1,201.3 1,140.7 5.3%

Like-for-like revenue (£m) 1,185.6 1,119.1 5.9%

Operating profit (£m) 49.9 27.1 84.1%

Operating margin (%) 4.2% 2.4% 180bp

Estimated passenger miles – S West (m) 3,600.7 3,535.5 1.8%

Estimated passenger miles – E Midlands (m) 1,380.5 1,344.7 2.7%

c.4% operating margin from lower risk (revenue support), low cash invested franchises

Full year of revenue support at East Midlands Trains

Significant opportunities to add value

16Virgin Rail GroupMaintained incumbent position on West Coast franchise

Year to 30 April 2013

Year to 30 April 2012 Change

Revenue – 49% share (£m) 441.5 429.5 2.8%

Like-for-like revenue – 49% share (£m) 440.9 425.8 3.5%

Operating profit – 49% share (£m) 12.8 21.5 (40.5)%

Operating margin (%) 2.9% 5.0% (210)bp

Dividends received (£m) 13.2 15.7 (15.9)%

Estimated passenger miles (m) 3,723.3 3,691.9 0.9%

Terms of West Coast franchised re-based from March 2012 and again, from December 2012

West Coast Trains management contract – profit before tax of 1% of revenue

Discussions continuing to move to a more risk-based contract through to April 2017

£12.7m (Stagecoach share: £6.2m) of bid costs for aborted West Coast franchise competition now recovered from Government - £11.3m prior to 30 April 2013 and £1.4m since

17

Significant value opportunities in UK Rail over next two years

West Coast Trains (through Virgin Rail Group joint venture)

Planned extension from Nov 2014 to Apr 2017

Significant upside from current 1% management contract

Virgin Rail Group in discussions with Department for Transport

South Western Trains Capital projects in Alliance from Apr 2013

Planned extension from Feb 2017 to Apr 2019

Alignment with Network Rail Control Period 5 (“CP5”)

Aiming to agree terms of extension by Apr 2014 (when CP5 begins)

East Midlands Trains Planned extension from Apr 2015 to Oct 2017

Thameslink Shortlisted for new franchise to start Sep 2014

Docklands Light Railway Shortlisted for new franchise to start Sep 2014

New franchises New model for UK rail franchising emerging

More appropriate allocation of risk

Significant new opportunities beginning with East Coast, due to start Feb 2015

18

A strong financial position

Year to 30 April 2013

Year to 30 April 2012 Change

Net finance charges (including share of net finance income of joint ventures) (£m) (37.2) (34.4) (2.8)

EBITDA from continuing operations and joint ventures* (£m) 370.3 343.9 26.4

Year-end net debt (£m) (538.0) (523.8) (14.2)

Net Debt/EBITDA* 1.5x 1.5x -

EBITDA*/Net finance charges* (including share of net finance income of joint ventures) 10.0x 10.0x -

Good bank relationships

c.£350m of committed bank facility headroom (available for loans) and unrestricted cash

Re-financing of acquisition from Coach America

USPP diversifies funding sources and extends average debt maturity at attractive cost

Objective to maintain an investment grade credit rating

Strong financial position supports pursuit of growth opportunities

* excluding exceptional items

19

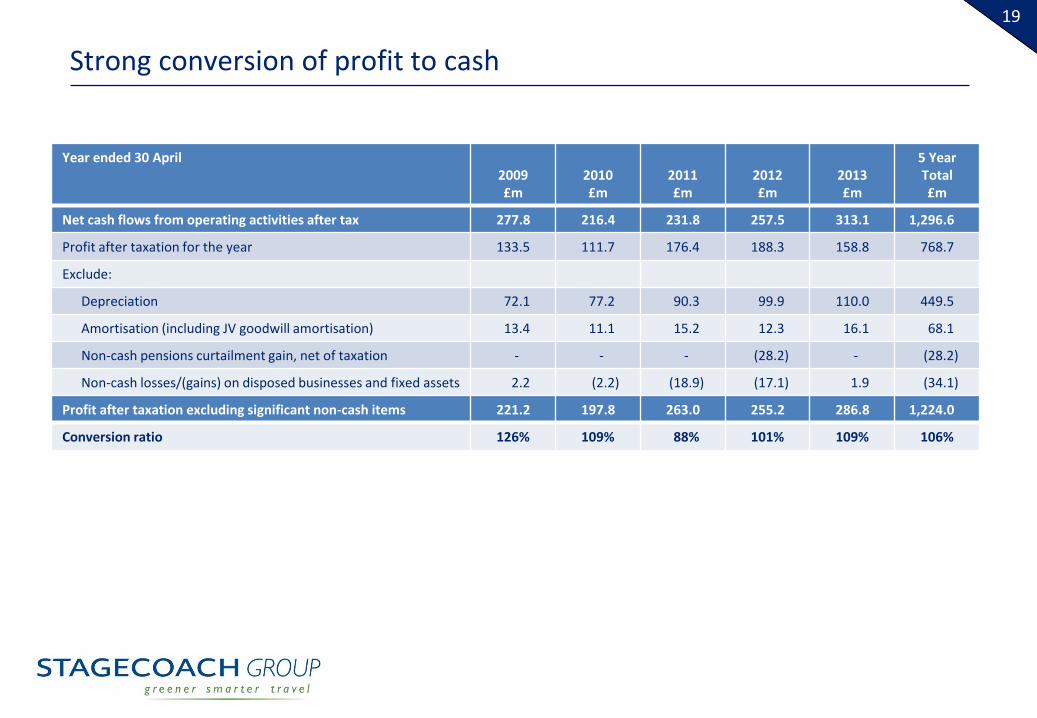

Strong conversion of profit to cash

Year ended 30 April2009£m

2010£m

2011£m

2012£m

2013£m

5 Year Total£m

Net cash flows from operating activities after tax 277.8 216.4 231.8 257.5 313.1 1,296.6

Profit after taxation for the year 133.5 111.7 176.4 188.3 158.8 768.7

Exclude:

Depreciation 72.1 77.2 90.3 99.9 110.0 449.5

Amortisation (including JV goodwill amortisation) 13.4 11.1 15.2 12.3 16.1 68.1

Non-cash pensions curtailment gain, net of taxation - - - (28.2) - (28.2)

Non-cash losses/(gains) on disposed businesses and fixed assets 2.2 (2.2) (18.9) (17.1) 1.9 (34.1)

Profit after taxation excluding significant non-cash items 221.2 197.8 263.0 255.2 286.8 1,224.0

Conversion ratio 126% 109% 88% 101% 109% 106%

20

Strong performance and healthy outlook

Stagecoach’s record of short and long-term delivery

− Good 2012/13 results

Current trading as expected

Significant opportunities to add value

− Extensions and new franchises in UK Rail

− Further strong growth in North America

− New products

Strong financial position

21

MARTIN GRIFFITHSCHIEF EXECUTIVE

22

Proven, consistent strategy delivering for shareholders

Organic growth in commercial bus/coach

Selected rail franchises with the

right risk-return profile

Complementary acquisitions

10-year

total shareholder return: over

800%*

Strong financial position to capitalise on opportunities

Plan to grow in all four segments: UK Bus (regions), UK Bus (London), UK Rail, North America

* Ten years ended 30 April 2013

23

UK Bus Stagecoach formula for growth

Devolved management

Strong operational delivery

Consistent investment

Value-for-money travel

High quality of service

New product development

Effective partnerships

A focus on organic

passenger volume growth

Embedded in management approach

Sector-leading bus customer satisfaction

24

North America: transforming the inter-city coach market

Source: Chaddick Institute, De Paul University, Chicago

Changing level of inter-city bus service in United States, % annual growth/decline

25

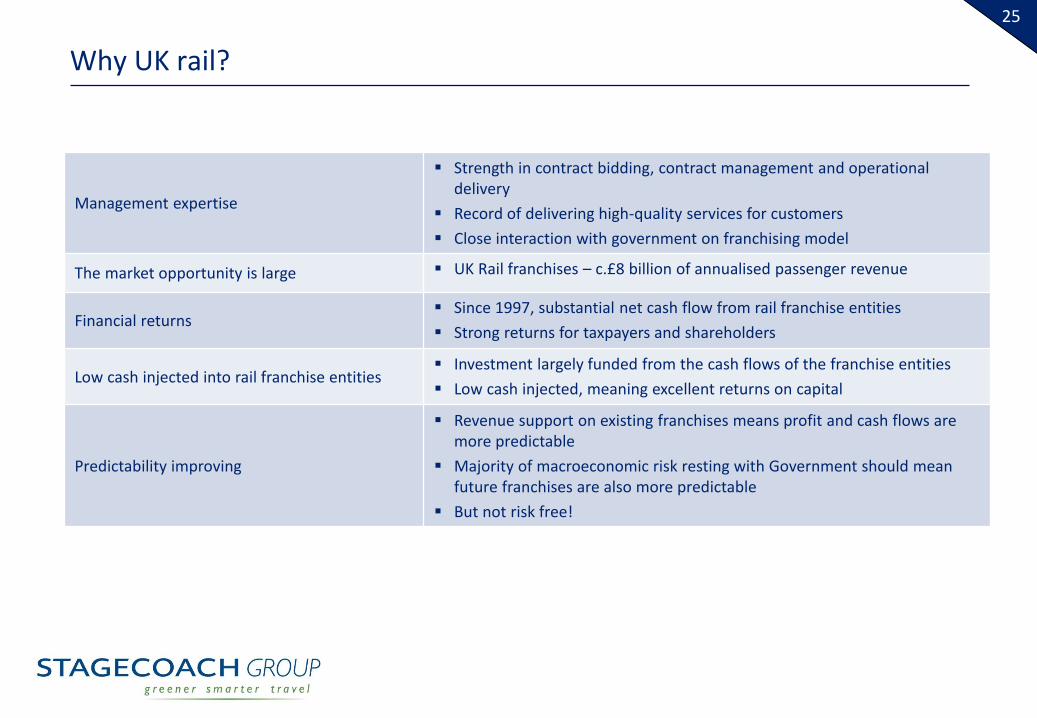

Why UK rail?

Management expertise

Strength in contract bidding, contract management and operational delivery

Record of delivering high-quality services for customers

Close interaction with government on franchising model

The market opportunity is large UK Rail franchises – c.£8 billion of annualised passenger revenue

Financial returns Since 1997, substantial net cash flow from rail franchise entities

Strong returns for taxpayers and shareholders

Low cash injected into rail franchise entities Investment largely funded from the cash flows of the franchise entities

Low cash injected, meaning excellent returns on capital

Predictability improving

Revenue support on existing franchises means profit and cash flows are more predictable

Majority of macroeconomic risk resting with Government should mean future franchises are also more predictable

But not risk free!

26

Experienced executive management team with strong track-record

Person Role Years at Stagecoach Years in industry

Gro

up

Martin Griffiths Chief Executive 16 16

Ross Paterson Finance Director 14 14

Steven Stewart Director of Corporate Communications 12 12

UK

Bu

s Robert Montgomery Managing Director 11 40

Mark Threapleton Managing Director, London 18 38

UK

Rai

l

Tim Shoveller Managing Director, South West Trains-Network Rail Alliance 6 22

David Horne Managing Director, East Midlands Trains 15 20

Margaret Kay Managing Director, Supertram 13 13

Graeme Hampshire Business Development Director 7 37

No

rth

A

me

rica

Dale Moser Chief Operating Officer 13 34

+ effective devolved management teams

27

Factors underpinning future growth

People: commercial/customer service appointments

New technology: smartcards, social media

Commercial focus: reduced dependence on public sector funding

Policy environment: influencing national/local transport decision-making through partnership

Maximise commercial opportunities

Drive improved customer service

Promote customer and taxpayer benefits

of private sector model

28

Growth opportunities across portfolio

Wh

at w

e h

ave

de

live

red

UK Bus UK Rail North America

Futu

re g

row

th

op

po

rtu

nit

ies

Growing customer base and modal shift driven by value fares strategy

Sector-leading profit margin and good financial returns

Resilient business, less dependent on Government spending

London Bus turnaround strategy delivered

Maximise potential of bus to deliver modal shift, support economic growth, tackle road congestion and deliver carbon reduction

Alliance with Network Rail Passenger improvements: new

capacity, fleet renewals and station investment

Continued high performance and customer satisfaction

Immediate-term rail franchise opportunities

Shaping improved franchising model for long-term on right risk-reward profile

First mover benefits from Alliancing

Fastest growing division in the Group

Strong portfolio focused on megabus.com and scheduled/commuter services

Integration of acquired businesses into North America division

Profitable growth from expanded megabus.com footprint

Huge scope for modal shift Scheduled/commuter services

Supported by strong financial position

29

Current trading and outlook: building on track record

Current trading in line with expectations

Positive outlook for all divisions

Public transport key to economic growth, global environmental targets

and future of communities

Continue to focus on opportunities to deliver value to shareholders

30

ANNUAL RESULTSYEAR ENDED 30 APRIL 2013

31

APPENDICES

32

Divisional income statements – Year ended 30 April 2013

UK Bus (Regional)

£m

UK Bus (London)

£m

North America

£mUK Rail

£m

Revenue 966.7 232.7 407.2 1,201.3

Rail franchise premia - - - (531.4)

Rail revenue support - - - 256.4

Other operating income 23.2 2.9 4.4 81.6

Staff costs (459.7) (139.8) (168.4) (283.4)

Fuel costs (i.e. diesel) (134.6) (28.5) (57.3) (49.8)

Insurance and claims costs (28.8) (4.5) (26.8) (4.9)

Depreciation (62.2) (6.0) (31.3) (10.3)

Rolling stock costs – lease & maintenance - - - (201.9)

Other operating leases (12.5) (13.9) (11.2) (2.1)

Network Rail - - - (211.5)

Electricity for trains - - - (31.3)

Commissions payable - - - (31.0)

Materials & consumables (36.8) (12.5) (30.9) (28.9)

Other costs (90.3) (8.5) (72.4) (102.9)

Operating profit 165.0 21.9 13.3 49.9

33

Rail premium profiles

The above amounts are subject to adjustment for: (1) various inflation measures (2) risks borne by the Department for Transport (3) called options and (4) changes in Regulated Network Rail charges. The amounts shown above are based on estimated inflation and options called to date, and exclude revenue support.

Year to 31 March:

South Western

£mEast Midlands

£m

2013 (395.2) (114.4)

2014 (465.4) (123.5)

2015 (518.9) (183.0)

2016 (606.8) -

2017 (594.7) -

34

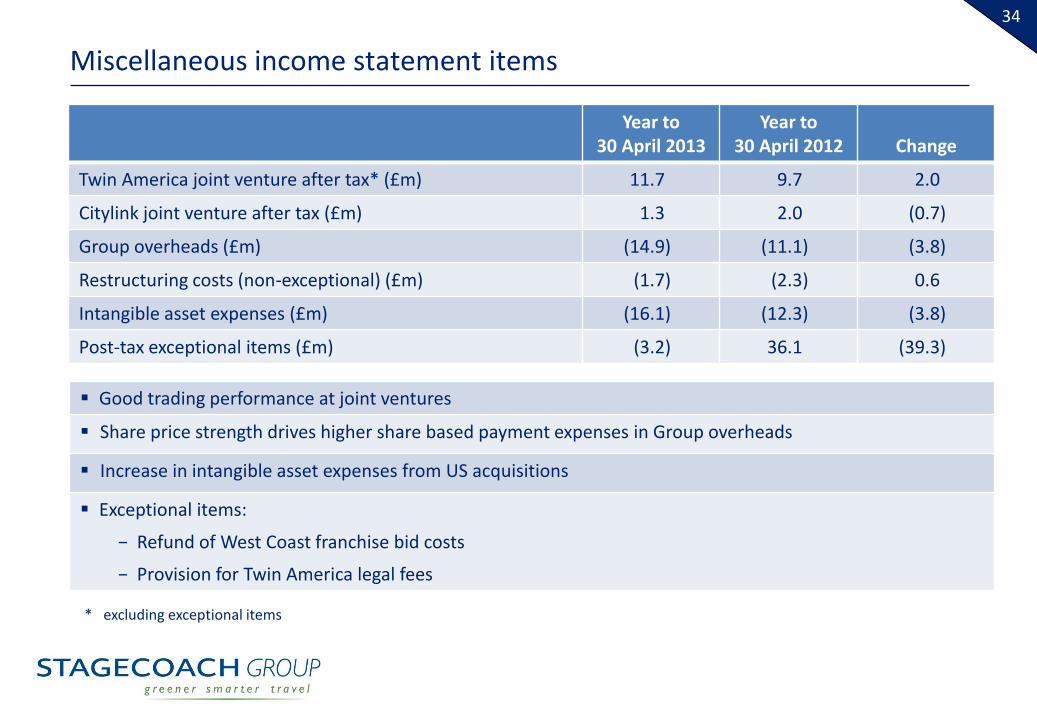

Miscellaneous income statement items

Year to 30 April 2013

Year to 30 April 2012 Change

Twin America joint venture after tax* (£m) 11.7 9.7 2.0

Citylink joint venture after tax (£m) 1.3 2.0 (0.7)

Group overheads (£m) (14.9) (11.1) (3.8)

Restructuring costs (non-exceptional) (£m) (1.7) (2.3) 0.6

Intangible asset expenses (£m) (16.1) (12.3) (3.8)

Post-tax exceptional items (£m) (3.2) 36.1 (39.3)

Good trading performance at joint ventures

Share price strength drives higher share based payment expenses in Group overheads

Increase in intangible asset expenses from US acquisitions

Exceptional items:

− Refund of West Coast franchise bid costs

− Provision for Twin America legal fees

* excluding exceptional items

35

Taxation

Year to 30 April 2013

Pre-tax profit£m

Tax£m

Rate%

Excluding intangible asset expenses and exceptional items 223.1 (49.7) 22.3%

Intangible asset expenses (16.1) 4.7 29.2%

Exceptional items (5.7) 2.5 43.9%

201.3 (42.5) 21.1%

Reclassify joint venture taxation for reporting purposes (5.5) 5.5

Reported in income statement 195.8 (37.0) 18.9%

Cash tax paid (net) (16.1)

36

New pensions accounting standard

New IAS 19 applicable from 2013/14

No effect expected on:

− Cashflow

− Covenants

− Credit ratings

Improved net assets position due to revised determination of rail deficits

Reduced profit offset by increased other comprehensive income

2012/13 adjusted EPS would be 24.6p under new IAS 19

− 5.6p or 19% lower than reported 30.2p

37

Pensions

Post-tax deficit of £121.5m (2012 restated: £92.3m)

Accounting value of pension assets, liabilities and costs will continue to vary with market fluctuations and assumptions

Rail – risks mitigated with obligations limited to contributions payable over duration of franchises

Bus – defined benefit schemes closed to new entrants and contributions have stabilised

Expense and contributions includes £8.6m (2012: £6.9m) for defined contribution arrangements

Year ended 30 April

2013 Pension expense

£m

2012 Pension expense*

£m

2013Cash

contributions£m

2012 Cash

contributions£m

UK Bus/Central 1.1 9.8 30.3 34.4

North America 1.8 1.8 1.7 1.3

UK Rail 23.1 24.4 30.5 29.0

26.0 36.0 62.5 64.7

* excluding exceptional 2011/12 £38m curtailment gain

38

Movement in net debt – Year ended 30 April 2013

£523.8m£538.0m

£(313.1)m

£155.3m

£6.2m

£107.7m

£6.7m £0.3m

£51.1m

250.0

270.0

290.0

310.0

330.0

350.0

370.0

390.0

410.0

430.0

450.0

470.0

490.0

510.0

530.0

550.0

570.0

590.0

610.0

630.0

650.0

Net

de

bt

(£m

)

39

Fuel hedging

UK Bus (Regional) UK Bus (London)

North America (including

Coach America) UK Rail

2012/13 - % of consumption hedged 97% 51% 80% 77%

- average effective price (per litre) 47.7p 49.4p 78.3 cents 49.1p

2013/14 - % of forecast consumption hedged 97% 50% 75% 76%

- average hedge price (per litre) 50.0p 49.3p 77.3 cents 51.3p

2014/15 - % of forecast consumption hedged 36% 38% 30% 61%

- average hedge price (per litre) 49.9p 51.1p 77.3 cents 49.5p

2015/16 - % of forecast consumption hedged - 25% - 5%

- average hedge price (per litre) - 49.8p - 50.3p

2016/17 - % of forecast consumption hedged - 13% - -

- average hedge price (per litre) - 49.2p - -

Market price (per litre) 48.4p 48.4p 72.6 cents 48.7p

Market prices are as at 31 May 2013

Prices exclude delivery margins, duty, taxes and Bus Services Operators Grant

40

Definitions

Like-for-like amounts are derived, on a constant currency basis, by comparing the relevant year-to-date amount with the equivalent prior year period for those businesses and individual operating units that have been part of the Group throughout both periods.

Operating profit or loss for a particular business unit or division within the Group refers to profit or loss before net finance income/charges, taxation, intangible asset expenses, exceptional items and restructuring costs.

Operating margin for a particular business unit or division within the Group means operating profit or loss as a percentage of revenue.

Exceptional items means items which individually or, if of a similar type, in aggregate need to be disclosed by virtue of their nature, size or incidence in order to allow a proper understanding of the underlying financial performance of the Group.

Gross debt is borrowings as reported on the consolidated balance sheet, adjusted to exclude accrued interest, the effect of fair value hedges on the carrying value of borrowings and unamortised gains on the early settlement of interest rate swaps.

Net debt (or net funds) is the net of cash and gross debt.

41

ANNUAL RESULTSYEAR ENDED 30 APRIL 2013