annual review on the working of treasuries, pao’s …1 annual review on the working of treasuries,...

TRANSCRIPT

1

ANNUAL REVIEW ON THE WORKING OF TREASURIES, PAO’S & PPO

GOVERNMENT OF TAMIL NADU

2018-19

Office of the Accountant General (A&E) Tamil Nadu, Chennai‐600 018

Dated: 30‐08‐2019

2

TABLE OF CONTENTS

Title Page No.

Preface 3

Introductory 4

Highlights 5

Part 1

Organisational set up of Treasuries & Accounts Department

6 to10

Part 2

Defects noticed during Compilation and verification of accounts

11 to 22

Part 3

Defects and other Irregularities noticed during Inspection of Treasuries/ PAOs Sub Treasuries

23 to 38

Annexure ( 1 to 33 ) 39 to 91

3

Treasuries are important institutions of the State through which Resources of State are

collected, disbursed and accounted. Failure of Treasuries to observe the rules and regulations

laid down by Government for their effective functioning will adversely affect the process of

financial accountability of the State.

Treasury Inspection is a mechanism through which we can derive assurance that

the Treasuries are organised and functioning in an appropriate manner and have the

requisite internal control structure in place to ensure that accounts are free from material

mis-statements.

The report on the ‘Annual Review on the working of Treasuries Pay and

Accounts Offices and Pension Pay Office, Chennai, for the year 2018-19 has been prepared,

based on the directions issued by the Comptroller & Auditor General vide Para 20.17 of

Comptroller & Auditor General’s Manual of Standing Orders (A&E) Volume I.

The cases included in the report, are among those which came to the notice of this

office at the time of the inspection of Treasuries, Pay and Accounts offices and Pension

Pay Office, Chennai during the year 2018-19.

Date: 30.08.2019

Place: Chennai-18

ACCOUNTANT GENERAL (ACCOUNTS & ENTITLEMENTS)

AN

4

Introductory

The Annual Review Report on Treasuries provides an analytical review of working of

Treasuries and PAOs of the States with reference to the prevalent rules and procedure. The

report is based on the Compilation of Accounts, Inspection of Treasuries, Pay and Accounts

Offices in Tamil Nadu and Pension Pay Office, Chennai during the year 2018-19. This report

consists of 3 parts.

Part 1 provides an introduction to the Organisational set-up of Treasuries and Accounts

Department detailing the various schemes and functions executed by the Department. It

provides information on the status of computerization and the various modules of Integrated

Human Resource Management Systems (IFHRMS).

Part 2 is based on the Compilation of Accounts received in this office and provides

information based on the verification of the accounts.

Part 3 is based on the Inspection of Treasuries/Sub Treasuries and Pay and Accounts Offices

and the defects and other Irregularities noticed during the inspection of 2018-19.

The Report also includes 33 Annexures of data collected from the Commissioner of

Treasuries and Accounts and other sources in support of the observations.

5

Highlights

Highlights of the discrepancies noticed during Review of Treasuries and PAOs are:

Out of 40,03,008 vouchers drawn during 2018-19, 1398 Vouchers were not

received from Treasuries to the extent of Rs.405.08 crore (Para 2.1 / Annexure 2)

Challans pertaining to 248 items amounting to Rs.12.37 crore were not received

from the Treasuries (Para 2.8)

In 2018-19, 1769 Temporary Advances (TAs), to the extent of Rs.363.49 crore

were issued by the TOs/PAOs, out of which 889 TAs to the tune of Rs.237.97

crore remained unadjusted. Also, 99 TAs amounting to Rs.187.55 crore relating

to previous years also remained unadjusted (Para 2.2 / Annexure 3)

GPF credit schedules to the tune of Rs.49 lakhs pertaining to 367 items were not

received during 2018-19(Para 2.5.2 / Annexure 5)

The reconciliation of differences of Reserve Bank Deposits between Treasury

and Banks was not complete, leaving a credit difference of Rs. 503.21 crore as of

31 March 2019 (Para 2.5 / Annexure 7)

While checking vouchers selected by Stratified sampling technique, deficiencies

were noticed in calculation of GST, passing of pay order without proper

authorisation etc., (Para 2.8 / Annexure 8)

Reply to 391 Inspection Reports / 1564 objections were outstanding as of 31

March 2019 (Para 3.2 / Annexure 10)

Lapsed Deposits statement amounting to Rs 3.89 crore were not submitted to AG

as of 31 March 2019 (Para 3.5.1 / Annexure 21)

Pensionary benefits to the tune of Rs 2.08 crore was paid in excess to pensioners

during 2018-19 (Para 3.6.c / Annexure 24)

The stamps that were made available to the TOs/PAOs were retained by them to

an extent of Rs.128.88 crore (Para 3.8 a / Annexure 26)

613 Unencashed cheques for an amount of Rs.6.87 crore in respect of Treasuries

and 58073 Unencashed cheques for Rs.473.02 crore in respect of PAOs were not

cancelled and written back to Government Accounts as of 31 March 2019 (Para

3.12 / Annexure 29)

Return ECS to the extent of Rs.11.36 crore and Rs.2.64 crore, in r/o TOs and

PAOs respectively, were not paid to the beneficiaries and were also not written

back to Government account as of 31 March 2019 (Para 3.13/ Annexure 30)

6

PART-1

Organisational set-up of Treasuries and Accounts Department

1.1 The formation of Treasuries & Accounts Department:

The Treasuries were originally functioning under the control of Revenue Department.

In 1954, Pay and Accounts Office was formed in Chennai, (Madras City) combining

the work of Treasury functions and audit functions, under the administrative control

of Finance Department.

The Department of Treasuries and Accounts was formed as a separate Department

with effect from 01.04.1962 under the Administrative control of the Finance

Department.

With the formation of the Directorate, all the District Treasuries, Sub Treasuries, Pay

and Accounts Offices, were brought under the control of Treasuries and Accounts

Department with overall administrative control of Finance Department.

The Administrative structure of Department of Treasuries and Accounts is given in

Annexure 1

1.2 Organizational Setup

The Principal Secretary / Commissioner of Treasuries & Accounts Department,

Chennai is assisted by six Regional Joint Directors, two Joint Directors, two Personal

Assistants in the cadre of Chief Accounts Officers and five Accounts Officers.

The following offices fall under the purview of the Principal Secretary /

Commissioner of Treasuries and Accounts:

Sl. No

Office Name No. of Offices

1. Regional Joint Director Offices

Chennai, Vellore, Coimbatore, Trichy, Madurai and Tirunelveli

6

2. Pay and Accounts Offices

North, South, East, Secretariat, High Court & Madurai

6

3. Sub Pay and Accounts Offices

Chennai Corporation, High Court Bench at Madurai & New Delhi

3

7

4. District Treasuries (in all 32 Districts) 32

5. Sub Treasuries 243

6. Pension Pay Office, Chennai 1

7. Assistant Superintendent of Stamps 1

Total 292

1.3 The role of the Department of Treasuries & Accounts:

The Commissioner monitors and implements the following functions and Schemes in the

State through Pay and Accounts Offices, Regional Joint Directors, District Treasuries, Sub

Treasuries etc.

I. Departmental Functions:

1. Handling of all Receipts & Payments of the State Government

2. Rendering of State Government’s Monthly Accounts to the Accountant General

3. Disbursement of Stamp Papers to stamp vendors through Treasuries

4. Maintenance of Deposit Accounts of Courts (Civil and Criminal), Local Bodies,

Personal Deposit Accounts of the Departments

5. Strong Room – for safe custody of valuables

6. Allocation of funds and sanction of Loans to Government Employees (Motor

Car/Motor Cycle, Computer, Marriage)

7. Sale of opium

II. Schemes

The following Schemes and functions are being administered by the Department:

1. Integrated Human Resource Management Systems (IFHRMS)

2. New Health Insurance Scheme for Employees

3. New Health Insurance Scheme for Pensioners

4. Group Insurance Scheme for All India Service Officers

5. New Pension Scheme for All India Service Officers

6. Contributory Pension Scheme for Government Employees

7. Nodal Officer for Public Financial Management System

8. Nodal Officer for Government e-Market Place

8

III. Functions relating to Pension disbursement by Treasuries & Accounts

Department:

Pension is a periodic payment made to retired Government servants who have completed the

service eligible for pension. The pension rules provide for various kinds of pension based on

the nature of retirement and net qualifying service under Tamil Nadu Pension Rules.

The following kinds of pensions are paid to the retiring Government Servants, according to

the nature of retirement

1. Superannuation Pension

2. Retiring Pension or Pension on Voluntary Retirement

3. Pension on Absorption in/under the Corporation or Government or Body

4. Invalid Pension

5. Compensation Pension

6. Compulsory Retirement Pension

7. Compassionate Pension

Pension proposals are being sent to the Accountant General, Tamil Nadu by the departments

concerned before the retirement of employees. The Accountant General, after verification of

Pay Last Drawn and the qualifying service, issues Pension Payment Order to the Pension Pay

Officer, Chennai / District Treasury Officers in the State. The Pension payment is being

made by the District Treasuries / Sub Treasuries, as opted by the pensioners.

Besides the Service Pension, other types of pension’s viz. Family Pension, Special Pension

Payments like Pension Payment of other State Governments, Central Government, Pension

Payments of other Countries, Art and Culture Pensions, State and Central Freedom Fighters

Pensions, Ulema Pensions etc. are also being made in the Treasuries, on receipt of Pension

Pay Orders from Accountant General (A&E).

1.4 Position of Treasury Staff

1.4.1 The details of the total number of sanctioned posts and persons in position in various cadres are as follows

9

Sl. No Name of the Post Sanctioned Posts (In T&A Dept.)

Person in Position

1. Additional Director

4 4

2. Joint Director

14 14

3. Chief Accounts Officer / Treasury Officer

38 38

4. Accounts Officer

24 24

5. Assistant Accounts Officer

5 5

6 Additional Treasury Officer

32 23

7 Assistant Treasury Officer

349 349

8 Superintendent / ASTO / STO

806 652

1.4.2 The cadre wise details of sanctioned strength and the actual vacancies that exist in the T&A Department are furnished below:

Sl. No

Category Sanctioned Post Vacancy

P T Total P T Total

1. Accountant 2000 122 2122 545 50 595

2. Junior Assistant 683 81 764 330 51 381

3. Junior Assistant (S) 251 19 270 201 17 218

4. Typist 102 13 115 55 8 63

5. Office Assistant 421 112 533 88 20 108

1.4.3 Action taken by the Department of Treasuries & Accounts in respect of various

vacant posts:

The shortage in posts of Accountants was due to promotions, retirement and death and the

vacancies were being estimated and filled up by the Department by getting direct recruitment

of candidates from Tamil Nadu Public Service Commission (TNPSC)

10

The vacancies in the post of Junior Assistant / Junior Assistant (Security) / Typist were

periodically reviewed and were being filled by indenting required candidates from TNPSC by

way of recruitment, and by transfer from lower category, including compassionate ground

appointments.

1.5 Computerisation

1.5.1 Automated Treasury Bill Passing System (ATBPS)

In Tamil Nadu, Treasuries process their bills through the Automated Treasury Bill Passing

System (ATBPS), and the Accountant General compiles the accounts through the Voucher

Level Computerisation (VLC) system. Presently, the Treasury Accounts are being received in

the form of Main Accounts and Sub Accounts and data entry made into the VLC in the

Accountant General’s office.

1.5.2 Integrated Financial and Human Resources Management System (IFHRMS)

Efforts are being taken by the Government for moving forward from ATBPS to Integrated

Financial and Human Resources Management System (IFHRMS), in which Accountant

General is one of the Stakeholders.

The various modules in IFMS are Budget module, Receipts module, Personnel Management

(HRMS) & Payroll, Fund Management module, Pension module, Banking Interface module,

Accounts module, Interface module with AGTN, Strong Room Safety and Stamp

Management module, Inventory Management module, Insurance Module, Virtual module

Financial Data Warehouse / BI module, e-Office (DMS) including inspection and Audit,

Online Grievance module (including RTI) and Web Portal & others (Help Desk).

In the IFHRMS environment, an Interface will be provided by the State Government for

importing the data from IFHRMS module to the existing VLC application of Accountant

General (AG). After importing the data, the regular processing of Compilation of Monthly

Accounts will be done by AG, duly incorporating all the ‘Transactions Outside Treasuries’

and other periodical adjustments and finally, the data will be pushed back to IFHRMS

module. The implementation of IFHRMS is near completion. More than one lakh State

Government employees (staff engaged in Establishment and Bill preparation activity) have

been trained in the IFHRMS application

11

PART-2

Compilation of Accounts

.

2.1 Receipt of supporting Vouchers from Treasuries along with Monthly Accounts

Unlike many States, in Tamil Nadu, the Treasuries / Pay and Accounts Offices primarily

compiles the monthly accounts such as Main Accounts and Subsidiary Accounts, from the

original sources / basic records such as vouchers in respect of payments and challans in

respect of receipts, made or received by them throughout the month. At the end of the month,

they furnish the primarily compiled Accounts to Accountant General with all the supporting

documents, such as vouchers, schedules, list of payments, plus and minus memorandums etc.

Accordingly, every month the vouchers are received in Accountant General’s office from

various Treasuries. During the checking of *A, B C and D Vouchers with the List of

payments, it was observed, that many vouchers relating to payment of salaries, loans and

advances, gazetted vouchers, All India Services vouchers etc. were not enclosed with voucher

bundles handed over to Accountant General. As Accountant General is the custodian of

vouchers, it is mandatory on the part of all Treasuries to forward all the vouchers to

Accountant General (A&E), every month along with the compiled Main Accounts and

Subsidiary Accounts, without any omission.

Treasuries are addressed periodically to furnish such “Wanting vouchers’ omitted to be sent

along with the other vouchers. The receipts of wanting vouchers are monitored through

Register of wanting vouchers. Out of 40,03,008 vouchers drawn during 2018-19, 1398

wanting vouchers to the tune of Rs. 405.08 crore were not received by the Accountant

General, as on 31.03.2019 (Annexure 2).

*A - Salary vouchers, B - Contingent vouchers, C - Refund vouchers, D - Grants in Aid vouchers

12

The maximum number of wanting vouchers was noticed in the following departments.

Name of the Department Sub Account Number of vouchers

not submitted to AG

Amount

in crore

Revenue Administration

- Disaster Management

26 12 132.83

Social Security and

Welfare

26C 393 100.75

Education 15A 445 72.97

Public Works 21 37 32.95

Police 13 12 27.54

2.2 Review of Drawal of Temporary Advances under Article 99 of Tamil Nadu

Financial Code

As per article 99 of Tamil Nadu Financial Code Volume I, for the purpose of meeting

contingent expenditure of a specified kind or on a specific occasion and when it is not

covered by standing sanction given by the Government, an application for sanction of

Temporary Advances shall be submitted by the Drawing and Disbursing Officer (DDO) to

the Government. With the sanction of the Government, Temporary Advances may be drawn

by the DDO. Such Temporary Advances (TAs) drawn by the departmental officers shall be

adjusted within three months from the date of drawal of the advances. TAs pending

adjustment for more than three months shall be brought to the notice of the Heads of the

departments / Government respectively. A third advance drawn by the same Drawing and

Disbursement officer also cannot be sanctioned when two advances are already pending.

During the year 2018-19, 1769 Temporary Advances amounting to Rs.363.49 crore were

drawn up to 31.03.2019. Out of those, 889 items to the tune of Rs.237.96 crore were

pending to the end of 30.06.2019. Also, 99 TAs amounting to Rs.187.55 crore relating to

previous years remained unadjusted as on 30 June 2019.

The treasury wise and year wise details are shown in Annexure 3.

13

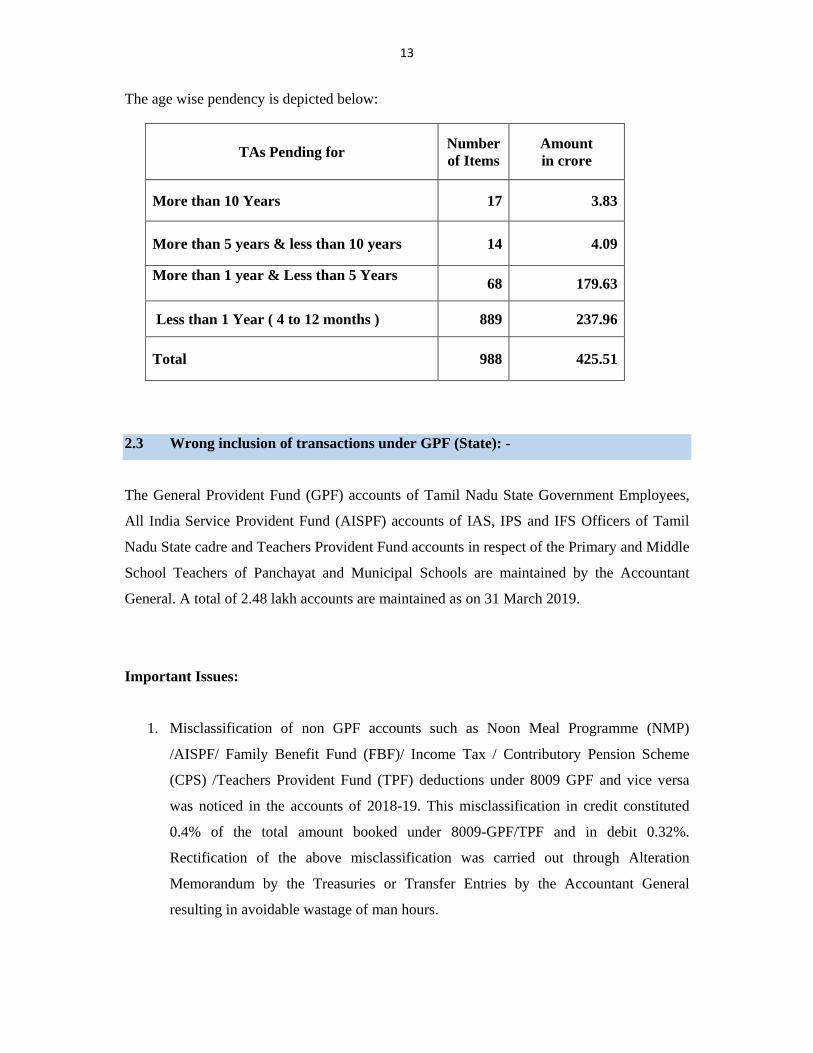

The age wise pendency is depicted below:

TAs Pending for Number of Items

Amount in crore

More than 10 Years 17 3.83

More than 5 years & less than 10 years 14 4.09

More than 1 year & Less than 5 Years

68 179.63

Less than 1 Year ( 4 to 12 months ) 889 237.96

Total 988 425.51

2.3 Wrong inclusion of transactions under GPF (State): -

The General Provident Fund (GPF) accounts of Tamil Nadu State Government Employees,

All India Service Provident Fund (AISPF) accounts of IAS, IPS and IFS Officers of Tamil

Nadu State cadre and Teachers Provident Fund accounts in respect of the Primary and Middle

School Teachers of Panchayat and Municipal Schools are maintained by the Accountant

General. A total of 2.48 lakh accounts are maintained as on 31 March 2019.

Important Issues:

1. Misclassification of non GPF accounts such as Noon Meal Programme (NMP)

/AISPF/ Family Benefit Fund (FBF)/ Income Tax / Contributory Pension Scheme

(CPS) /Teachers Provident Fund (TPF) deductions under 8009 GPF and vice versa

was noticed in the accounts of 2018-19. This misclassification in credit constituted

0.4% of the total amount booked under 8009-GPF/TPF and in debit 0.32%.

Rectification of the above misclassification was carried out through Alteration

Memorandum by the Treasuries or Transfer Entries by the Accountant General

resulting in avoidable wastage of man hours.

14

The details of Transfer Entries (TEs) proposed during 2018-19 in order to rectify the

above mentioned misclassifications are given below

Credit TEs Misclassified under No. Of items Amount (Rs.)

8009-01-101-AA 2271 (-) 9,21,46,716

8009-60-103-BC 1082 12,48,00,083

8009-60-103-BE 70 (-)2,86,392

Debit TEs

Misclassified under No. Of items Amount (Rs.)

8009-01-101-AA 331 (-) 9,43,82,842

8009-60-103-BC 327 6,56,62,764

8009-60-103-BE 48 1,07,68,641

2. GPF Deductions made in respect of Retired/Expired subscribers were noticed in few

cases. This indicates that pay had been drawn in respect of those persons even for the

period for which the subscriber was no longer in service. The lapse in the internal

control mechanism in this regard needs to be identified and rectified.

3. Some vouchers mentioned in the list of payments pertaining to loans, were not

enclosed with the debit vouchers sent to the Accountant General. This led to missing

debits in the accounts of the subscribers.

4. In around 500 accounts, the GPF deduction for March 2019 had been booked in the

month of March 2019 itself which clearly indicates violation of budget provisions as

Salary for March has to be claimed only in the month of April. This failure of internal

control mechanism requires remedial action.

5. The main account figure is the control total for the overall amount booked under GPF

for a month/Treasury. But in some cases, the differences are noticed between the

Main Account figures maintained at treasuries and the amount mentioned in the GPF

Credit List and GPF Loan List sent for credit schedules / debit vouchers. This leads to

15

accumulation of suspense balances under GPF Debits and Credits, which are later

rectified by AG only by addressing the Treasuries concerned for reconciliation.

6. Manual corrections made in the Credit List, Loan List and Main Accounts received

from Treasuries are not authenticated by the Competent Authority. Also, the

corrections carried out by Treasuries in the office copy are not properly reflected in

the fair copies sent to the AG.

7. In some sub accounts the CPS schedules are erroneously enclosed along with the

credit list of GPF and vice versa. This leads to wanting schedules and results in

missing credits to subscribers.

8. Sanction order list of 90% Part Final Withdrawal is not being sent to AG by some

Treasuries. While making GPF/TPF Final Withdrawal authorisation payment,

necessary certificates to be given by the Drawing and Disbursing Officers as

mentioned in the authorisation is not being insisted upon.

2.4 Non submission of Debit vouchers / credit schedules / challans along with the

Monthly Accounts

1. The detailed Broadsheets of long term advances under major head 7610 of All India

Service Officers alone are maintained in this office.

No significant lapses in the part of Treasuries / PAOs were noticed in

furnishing the debit vouchers of such advances. However, in respect of motor car

advances, non-receipt of credit schedules to the tune of Rs.1,05,563/- from some of

the Treasuries/ PAOs, resulted in missing credits in the individual’s account. The

district wise details are furnished in Annexure 4.

2. Challans pertaining to 248 items involving a money value of Rs.12.37 crore was

wanting from various Treasuries as on 31.3.2019, which led to incorrect compilation

of Accounts.

In respect of GPF subscriptions made as challan Remittances, a copy of the challan

as well as supporting schedules were not enclosed in many instances which resulted

in missing credits in the account of subscribers. A treasury wise list of GPF wanting

schedules for the year 2018-19 is given in Annexure 5. Out of this, the total challan

wanting alone was for Rs. 27 lakhs. As on 10.05.2019, the challans, for an amount of

Rs. 2.95 crore was wanting. However, it was reduced to Rs. 27 lakhs, due to repeated

16

correspondences between AG and the departments, before the issue of Annual

Accounts Statements of GPF .

3. Subscriptions towards Postal Life Insurance (PLI): The PLI recoveries are made

through the pay bills of the State Government employees and booked under the

suspense head “8658-00-102-AG” every month by the concerned Treasuries/ PAOs.

After the finalisation of Monthly Civil Accounts, Accountant General transfers the

net proceeds to the Chief Post Masters of General Post Office and Anna Road HO,

by means of cheque obtained from Pay and Accounts Officer (North).

The PLI credit schedules are handed over by all the TOs/PAOs every month to

Accountant General Office. Subsequently, after scrutinizing the bundles for the

availability of schedules and ascertaining the wanting / missing schedules, the PLI

schedules are forwarded to the respective Post Offices for making data entry at their

end. The list of wanting schedules is then communicated to concerned TOs/PAOs.

The following discrepancies were communicated by the Chief Post Masters in respect

of Goods and Service Tax (GST) which was implemented with effect from 01.07.17.

a. The arrear amount from 01.07.2017 to 30.11.2017 was not fully recovered

from most of the PLI policy holders in the State.

b. The Service Tax, Swachh Bharat Cess and Krish Kalyan Cess were still being

recovered from the subscribers by the DDOs.

c. While booking the PLI recoveries, the GST amount was not booked separately

under the prescribed head but included under Premium head of Account

notwithstanding necessary provisions made by National Informatics Centre.

d. Though the two components of GST, the Central and State GST were to be

recovered in equal percentage, huge variations were noticed between them, in

most of the Treasuries.

e. Challan remittances in respect of PLI recoveries were not booked / taken to

appropriate sub account depending upon the Department concerned, but

booked under the Sub Account 27 E – Suspense Accounts.

All of the above discrepancies have been directly brought to the notice of the

Commissioner of Treasuries by the respective Chief Post Master, in various

occasions. Examples are furnished in Annexure 6.

17

Recommendation:

As the shares of Central and State recoveries made towards Goods and Service

Tax, should be apportioned to respective Government’s by the Postal Authorities,

necessary directions are to be given to all Drawing and Disbursing Officers, to collect

and book the GST under proper head of accounts.

As on 30.06.2019, a net CREDIT difference of Rs. 5,03,21,21,279.86/- exists under the

Major Head “8675 Reserve Bank Deposits” between figures reported by the Banks and by

Treasuries. The year wise details are given in Annexure 7.

Recommendation

A Tripartite discussion between the Commissioner of Treasuries & Accounts,

Accountant General, and the related Bank Managers will help in sorting the problems

related to discrepancies under 8675 RBD.

2.6 Personal Deposit Accounts

The Personal Deposit Account is intended for a specific purpose for which it is created. It is

governed by Article 269 of Tamil Nadu Financial Code Volume I. The balances / drawals

from the Deposit Accounts are communicated by way of plus and minus memoranda. The

discrepancies under Personal Deposit Account and receipt of plus and minus memoranda are

brought in the succeeding paragraphs.

2.6.1 Operation of Personal Deposit Accounts

i. The Personal Deposit Accounts created by transferring Funds from the Consolidated Fund

to Public Account for discharging the liabilities of the Government arising out of special

enactments is operated during the period between 1st April and 31st March next year. It can be

opened by the State Government after obtaining permission from the Accountant General and

shall be closed on 31st March every year. During 2018-19, 78 such PD accounts (transferred

2.5 Un-reconciled Net (Dr.) differences of Reserve Bank Deposits (State) between

Treasuries and Banks

18

from Consolidated Fund) have been opened out of which 11 PD accounts were closed as on

31.03.2019.

Recommendation

Government may consider the discontinuance of operation of Personal Deposit

Accounts. Where it is absolutely necessary, PD Accounts may be opened giving full

justification and operated in strict adherence to rules.

ii. The details of balances of the PD accounts opened by the State Government from sources

other than the Consolidated Fund are as under:

8443-00-106-AC (Rupees in crore)

Opening Balance 58.04 Receipts 285.83 Payments 37.25 Closing Balance 306.62

2.6.2 Submission of Plus and Minus Memorandum

The Plus and Minus Memorandum for various deposits were submitted by Treasuries / PAOs regularly.

2.7 Submission of Monthly Account by Treasuries.

The compiled Main Accounts and Sub Accounts are received from Treasuries on the stipulated date every month without any delay.

2.8 Checking of vouchers selected by stratified sampling technique

As per the instructions of the C&AG of India issued vide letter dated 27.06.2014, vouchers

under Revenue and Capital Expenditure are being selected under stratified sampling method

and checked as per the guidelines prescribed therein. The discrepancies of the following

nature were noticed and they were communicated to the concerned Treasuries to take

appropriate action in this regard.

Discrepancies related to Goods & Services Tax (GST)

The GST amount at 12% shall be calculated and added to the value of work actually

measured and every bill presented to the Treasury for payment shall include GST at 12%. It

was found that instead of calculating 12% on the total value, it was calculated on “payment

19

now to be made”. In some cases, it was calculated for the amount actually arrived at after

deducting the withheld amount of 5% in the total value of work done.

The 2% GST amount shall also be calculated on the value of work done, similar to that of

income tax deduction and shall be shown in the running account bill. But it was noticed that,

in a few cases, deduction of 2% GST amount was not shown in the bill but mentioned in ECS

Data report.

Discrepancies related to Pay Order

Each and every bill submitted to the Treasury shall be scrutinized for the necessary checks

and pay order to be issued by the Sub Treasury Officer, for making the payment. It was

noticed that Payment was made without the necessary pay order in a few cases.

Pay order has to be issued for the Gross amount i.e. net amount plus deductions. In some

cases, the pay order was issued for net amount directly and in some cases, the deductions

were wrongly exhibited and the total of deductions plus net amount could not be tallied with

the gross amount of the bill.

Discrepancies related to Running Account Bill

After the withdrawal of Letter of Credit, the Division remits the Labour Welfare Fund (LWF)

calculated on the total value of work done and when the part bills are submitted, proceedings

will be issued for the work done alone without including the part of LWF. In some cases, it

was noticed that payment was made for the LWF also without including the same in the

sanction.

In a few cases, it was noticed that Running Account Bill was not enclosed with TNTC Form

59 in the absence of which the authenticity of the bill could not be ascertained. Variation was

found between the figures carried forward from the Part bill to Running Account Bill.

The District wise details of the deficiencies noted in the vouchers checked through this

methodology which were communicated to the concerned Treasuries to take appropriate

action in this regard are furnished in Annexure 8.

2.9 Other issues:

2.9.1 Pension Processing

Pension proposals along with Service Register (SR) received from Departments are received

approved after necessary checks and Electronic authorizations are being sent to the Treasuries

for payment and pensioners can download their copy of the authorizations from website of

the AG.

20

2.9.2 Instructions to be followed while forwarding the pension proposals

1. The Statement of service in respect of All India Service Officers/Self Drawing

Officers who are under the control of Pay and Accounts Officers (PAOs) are to be

sent by the PAOs, to the Heads of Departments before their retirement so that the

Heads of Departments may send the same along with pension proposals to Office of

the Accountant General (AG). But despite the instructions issued by Commissioner of

Treasuries and Accounts to all PAOs, this procedure is not being followed by PAOs.

The net qualifying service and the pay last drawn by the Government servant can be

calculated only from the Statement of service. In the past three years, around 200

cases of Self drawing officers and All India Service officers were received without

statement of service, and hence the pension proposals were returned to the

departments without admittance.

2. Department copy of Death cum Retirement Gratuity (DCRG) authorization is being

received for revalidation where payment was not made within one year validity

period. As the treasury copy in such cases is also to be revalidated, Treasury/PAO

was addressed to return their copy. But payment for the such authorisations was

already made based on party copy of authorisation by the treasuries which is highly

irregular. The correct procedure is, on receipt of Death cum Retirement Gratuity

(DCRG) authorisation from the Office of the AG, the Drawing and Disbursing

Officer shall prepare the bill and send the bill to concerned Treasury along with the

Department copy of DCRG authorisation. The treasury officer shall make payment

on the basis of the bill drawn by the DDO and the treasury copy of the DCRG

authorisation. DCRG payment shall not be made on the basis of Party copy of

DCRG authorization.

3. Both Halves (Disburser’s half and Pensioner’s half) of Pension Book have to be

returned to AG by the treasuries as and when the necessity for the same ceases.

4. The Department of Treasuries and Accounts was addressed (January 20181) to

instruct all Treasury officers/Sub treasuries/PPO Chennai 35 to revise the pension of

those Village Administrative Officers for whom minimum pension/Family pension

@ Rs.3050/- pm was admitted and for all beneficiaries as per GO 325 dated

28/11/2011 to Rs. 7850/- pm from 01/10/2017 without insisting revised authorisation

from this office. But still we continue to receive cases for which, pension has not

been revised to Rs.7850/- per month.

21

5. E-Authorisations (Authorisations relating to pensionary benefits are being sent to

Treasuries as pdf files encrypted with digital signature) are being sent for original

pension cases from August 2018 and subsequently it is being extended to Revision

and Family Pension cases also, with a facility to download the pensioner’s copy from

website of the Office of the AG. However, if the pensioners are not able to download

their copy due to technical issues, the same shall not be insisted by the treasuries for

production. As the photo identity document is scanned and sent along with the

authorisations there is no need to insist on party copy for original cases. In respect of

revision cases, as the pensioners are already getting their pension through Treasuries,

production of party copy is not required. This fact has already been conveyed (May

20192) to the Principal Secretary/Commissioner of Treasuries and Accounts for

communication to Treasury Officers. However, it has come to the notice of AG that

party copy is still insisted upon from the pensioners in some Treasuries for making

payment. It is understood that the Commissioner of Treasuries and Accounts has

taken up the matter (June 20193) with the Finance Department for amendment of

Treasury Code, wherein it has been prescribed that the payment is required to be

made by the Treasuries on production of party copy.

6. The Treasury Officers have been instructed to send the vouchers relating to first

payment of pension for the purpose of capturing these details in our system. But only

few Treasury Officers are sending the vouchers separately. If the first payment

vouchers are not sent separately, it is not possible to differentiate the same, and

pension payment could not be posted in such cases. Hence suitable instructions need

to be given again, reiterating the Circular instructions given (June 20094) by CTA in

this regard to all the Treasury officers to send the vouchers relating to first payment

in a separate bundle.

7. For non-self-drawing officers, if the pension proposals are received in advance of

retirement, the pension, commutation and DCRG authorizations will be issued before

retirement. If the Government servant is transferred to another office at the time of

retirement and the same is not intimated to AG, DCRG authorization will be issued to

the office mentioned in the proposals. Consequently, it requires change in DDO and

Treasury. Incomplete details furnished in Pension proposals will lead to change in

DDO or Treasury. In such cases, the treasury officer on intimation from the DDO,

shall forward his copy of authorisation to the concerned PAO/Treasury where

payment can be made instead of returning the authorisation to the AG for correction.

22

Similarly if the DCRG authorisation issued by AG does not come under the control

of the respective Treasury Officer noted in the authorisation, the same shall be

forwarded to the concerned PAO/Treasury by the Treasury Officer himself with a

copy endorsed to the departmental officer, so as to enable him to present the bill to

the concerned PAO / Treasury officer, instead of returning the same to this office.

Though clear instructions to this effect are clearly printed on the backside of the

Authorisation, the same is not being followed by some of the Treasuries resulting in

avoidable delay and hardships to the beneficiaries.

8. In respect of Post Audit Police pensioners, the part of the DCRG amount is being paid

at the first instance due to want of ‘NO DUES CERTIFICATE (NDC)’ and balance

amount is paid after issue of NDC and on the basis of amount noted in the

admissibility report. The admissibility report is not an authorization. Some of the

Treasury Officers/PAOs are sending the admissibility report for revalidation. No

revalidation is required for admissibility report, since no payment shall be made

based on admissibility report.

___________ 1

Letter No. Pen 30/2/1-82/2017-18/42/111896 dated 18/01/2018 2

Vide this office DO letter No.AG(A&E)/Pen 30/4/2019-20/11163 dated 13/05/2019 3

Vide his letter No.26243/Finance (Pension)/2019 dated 12/06/2019

4 RC No.22660/09/E2 dated 15.06.2009

23

PART-3

Defects and other irregularities noticed in the records during inspection of the

Treasury Offices, Sub-Treasury Offices and PAOs

3.1 Units inspected during 2018-2019

The Treasury Inspection is conducted based on the instructions issued by the C&AG vide

letter NO.352-AC.I/SP.III/50-99 dated 28.6.99 whereby Treasuries/PAOs which account for

significant volume of ‘Outgo’ are inspected annually and Sub-Treasuries (STs) are inspected

biennially.

The periodicity of the inspection of the various subordinate offices (i.e. inspecting units) of

Commissioner of Treasuries and Accounts is given below:

Accordingly, during 2018-19, 167 inspection units (i.e.) 32 District Treasuries, 6 Pay and

Accounts Offices, 1 Pension Pay Office, 125 Sub Treasuries and 3 Sub Pay and Accounts

Offices were inspected. The Sub Treasuries and other units other than DT/PAOs, inspected

during the year are listed in Annexure 9.

The Resident Audit Branches of the office of the Principal Accountant General (G&SSA),

Chennai attached to these Pay and Accounts Offices (except Pay& Accounts Office, New

Delhi) have also made observations on review of the accounts of the Pay and Accounts

offices for the year 2018-19 and these observations are included under the appropriate places.

Name of the category Number of units Periodicity

District Treasuries 32 Annual

Pay and Accounts Offices 7 Annual

Sub Treasuries 243 Biennial

Sub PAO High Court Bench, Madurai and

Sub PAO corporation, Chennai

2 Biennial

PAO New Delhi and

Assistant Superintendent of stamps, Chennai

2 Once in 4 years

Office of Commissioner of Treasuries and

Accounts

1 Biennial

Offices of the Regional Joint Director of

Treasuries and Accounts

6 Biennial

24

3.2 Outstanding Inspection Reports and Objections

The primary objective of Treasury Inspection is to assist the departmental authorities to

establish a system, where Treasuries work in accordance with the prescribed rules.

Irregularities pointed out by Treasury Inspection Parties need to be rectified at the earliest by

the Treasury Offices, thereby enhancing the efficiency of the working of Treasuries and

quality of Accounts.

Within 20 days of the completion of each Treasury Inspection, the Accountant General will

communicate the Inspection Report (IR) to respective units. Rectification reports on action

taken for the Inspection Reports are required to be furnished within a month from the receipt

of IRs by the concerned inspected units.

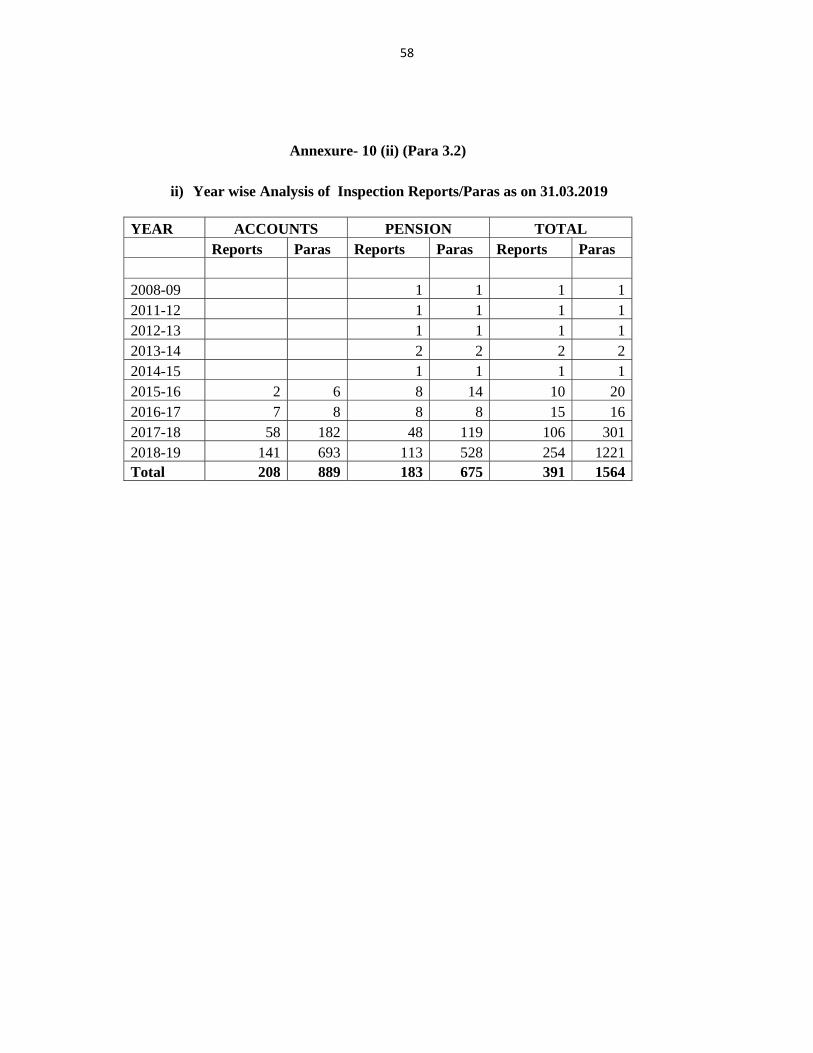

However, as on 31.03.2019, there are 391 Reports and 1564 objections for which such

rectification reports were not received. The details of pending Inspection Reports / objections

to the end of 31.03.2019 are furnished in the Annexure 10 (i) Region wise / District wise and

(ii) Year wise.

It would also be observed that for 137 reports comprising 323 objections, rectification

reports have not been received even after a lapse of one year from the date of issue.

Similarly, in respect of PAOs, 641 objections amounting to Rs.33.79 crore were

outstanding as on 31.3.2019. The details are noted below.

Name of the PAO

Items Amount

Madurai 180 21465542North 127 49695011Pension 98 6107021South 95 21410034East 53 156959922High Court 52 78223337 Secretariat 27 3733859High Court Bench at Madurai 9 349658 Total 641 337944384

25

3.3 Non revalidation of Gratuity payment authority after the expiry of one year

The DCRG and GPF authorizations issued by the AG, Tamil Nadu shall be valid for a period

of one year and 6 months respectively. If the authorization is not paid, the same shall be

returned to AG for revalidation. However, on a review of DCRG/GPF registers maintained in

various Treasuries/ Sub Treasuries, it was seen that though the validity had expired,

necessary action had not been taken by the treasury for revalidation. (Annexure 11)

3.4 Improper/Non maintenance of records

The Treasury Inspection Parties while inspecting the Treasuries noticed and pointed out the

following discrepancies in maintenance of records:

a) The pay and allowances of the Self drawing officers who are drawing grade pay of

Rs.7600/- and above are authorized by the Accountant General (A&E) and the same is

paid through 41C Pay Bill register. Whenever pay authorization received from the

Accountant General or Last Pay certificate is received from other station due to transfer,

it is mandatory to obtain the specimen signature of the concerned officer and affix the

same on the left hand side top corner of 41C register and get it attested by the Bill passing

officer. But, improper maintenance of 41 C Register such as (i) non attestation of

specimen signature (ii) non production of certificate for claiming HRA was noticed in 28

inspected units (Annexure 12).

b) According to Subsidiary Rule 32A under TR 16, every bill shall be presented by DDOs to

the Treasury / PAO along with TNTC 70 only. After ascertaining about the availability

of budget allocation, a system generated token number is allotted and noted in the TNTC

70 register. The bill shall also be noted in the movement register in Form 70A and

handed over to the bill passing Accountant. The bill passing accountant shall make

necessary entries in Form TNTC 70D and he shall either pass or audit the bill within

three days from the date of its receipt. Thereafter, passing and auditing of the bills shall

be entered in TNTC 70D register and the register shall be closed daily. It was observed

that Bills received and entered in 70A Register did not tally with 70 D Register in 38

inspected units (Annexure 13). Due to non-closure/non-updation of TNTC 70 D register,

it could not be ascertained whether bills had been passed at the Sub Treasuries within

stipulated time limit.

26

c) As per instructions 33 under Treasury Rule 16 every officer drawing bills shall enter the

particulars of all their bills in TNTC 70 register. Columns 8 to 10 shall be filled up by the

Treasury and the rest by the office concerned. However, it was observed that Column 11

(Voucher number) of TNTC 70 Register was not filled by 53 inspected units (Annexure

14).

d) According to note (2) under Article 126 of Tamil Nadu Account Code Volume II and

instruction 4 under chapter IV of Tamil Nadu Financial Code Volume I, Certificate of

acceptance of balances of various deposits as on 31st March every year, shall be obtained

from Administrators before 15th May and forwarded to the Accountant General (A & E),

Chennai before 30th June of that year. However, it was noticed, that Certificates of

acceptances of balances were not obtained by the Administrators in 37 inspected units

(Annexure 15).

e) Various Deposit Registers, viz., Repayment of Revenue Deposit Register, Security

Deposit Register, Revenue deposit & Criminal Courts deposit, Civil Court deposits, PWD

/Forest/Highways deposit register etc., are maintained by the Treasury Officer. In 19

inspected units, it was noticed that the Deposit registers were not updated and closed

(Annexure 16).

f) As per the provisions of para 128 of Tamil Nadu Budget Manual, reconciliation of

Departmental figures with those of Treasury / PAO shall be effected without fail by the

Departmental Officers every month in order to ensure that there is no embezzlement /

misappropriation of Government money which should be monitored through a Register. It

was noticed in 26 inspected units that the Reconciliation Register was not updated.

(Annexure 17).

g) According to Reserve bank of India’s recommendations of working group on accounting

reconciliation procedure of State Government transactions, the format of Treasury Pass

book has been modified. The revised format contains two parts i.e., Side ‘A’ and Side

‘B’. At the end of each days’ transactions, the total figure of receipt and payment of

Government are required to be entered in Side ‘A’ of the pass book by the bank manager

and the same should be acknowledged by the Treasury officer with detailed initials. The

total number of challans, cheques (with amount thereon) actually received by the

Treasury Officer are also required to be entered in Side ‘B’ of the pass book and the same

has to be got acknowledged by the Bank Manager with dated initials. Thus, the

27

maintenance of Treasury Pass book will help the Sub treasury to reconcile the differences

if any noticed between the treasury and bank figures then and there. It was noticed that 52

inspected units failed to maintain the Treasury Pass Book in the revised format

(Annexure 18).

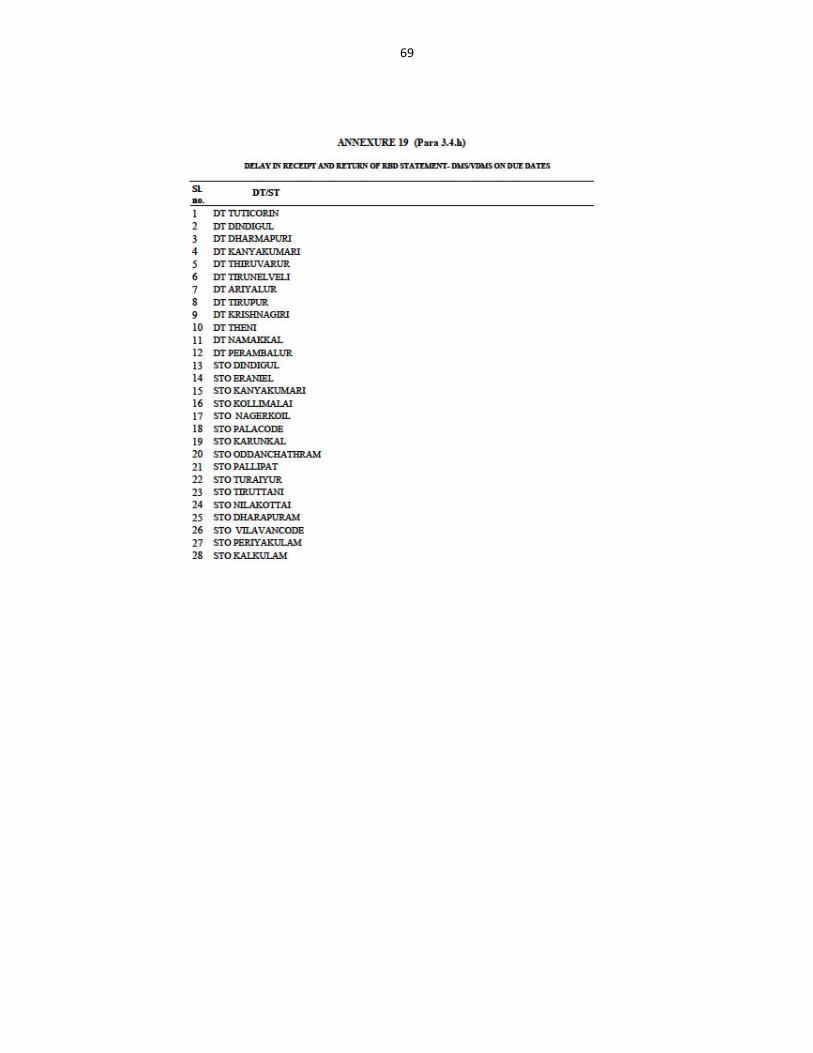

h) Treasury shall receive date wise monthly statement (DMS) from the connected Bank

Branch on first working day of the following month and check the correctness of the

transactions recorded and certify it within two days and return to the Bank Branch. This

will, in turn, be transmitted by the Branch to the Link Bank for incorporation of the figure

in the Statement forwarded to RBI which is retransmitted by RBI to this office. Delay in

receipt of DMS and verification by TO will result in adopting the incorrect figure by the

Link Bank which will cause a difference under 8675 RBD. Timely receipt of verified date

wise monthly statement (VDMS) in the Link Bank will avoid discrepancy under 8675

RBD. However, such delay in receipt and return of Date wise monthly statement was

found in 28 inspected units (Annexure 19).

i) Improper maintenance of Padlock register and key register was noticed in District

Treasury Sivaganga, Thiruvallur, Sub Treasuries Pallipat, Tirutani, Attur, Chengalpattu,

Tirupur, Ponneri and Salem.

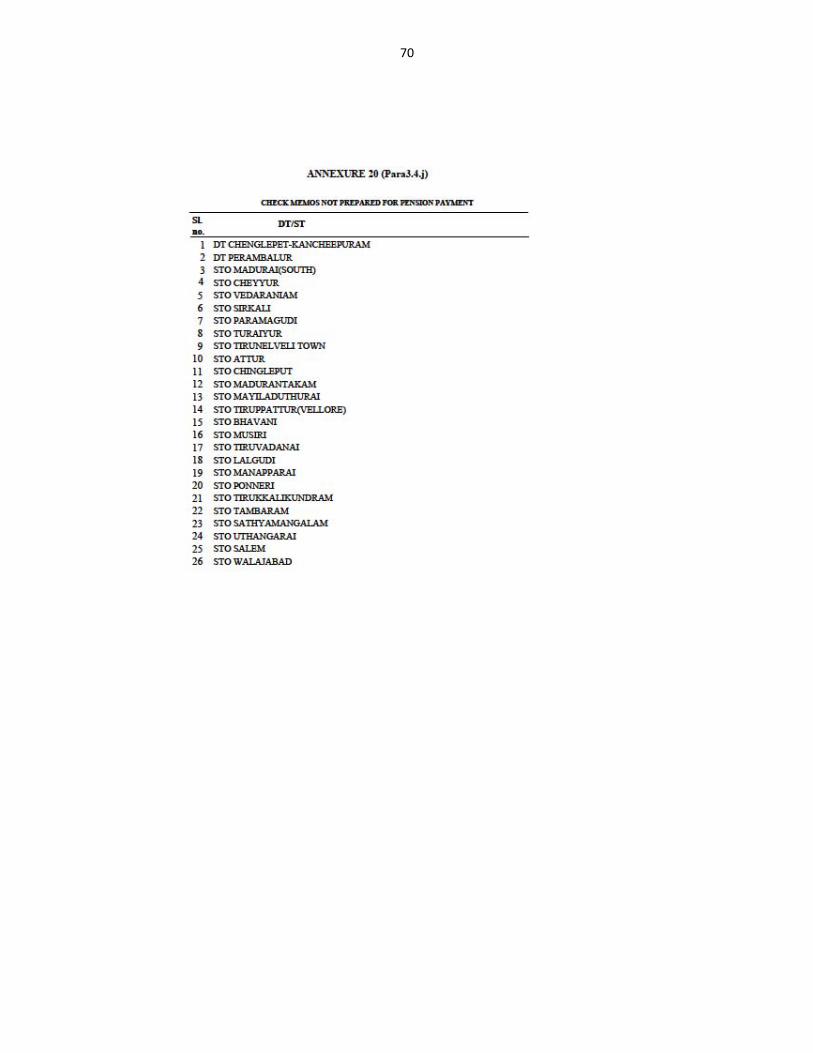

j) As per the circular issued by the Commissioner of Treasuries and Accounts in 3/2004, the

treasuries shall prepare a check memo for each category of pension payments. The check

memo which should be in the form of plus and minus memo shall guard against any

incorrect / excess payment and also serve as an easy mode of check by the Accountant

General (A&E) / Regional Joint Director. The same is reiterated by the Commissioner of

Treasuries and Accounts in circular number Rc. No.39509/2011/E2 dt.27/9/2011. In 26

inspected units, it was noticed that check memos in the form of plus and minus memo to

guard against any incorrect / excess payment were not prepared for making pension

payment. (Annexure 20).

3.5 Observations relating to Deposits

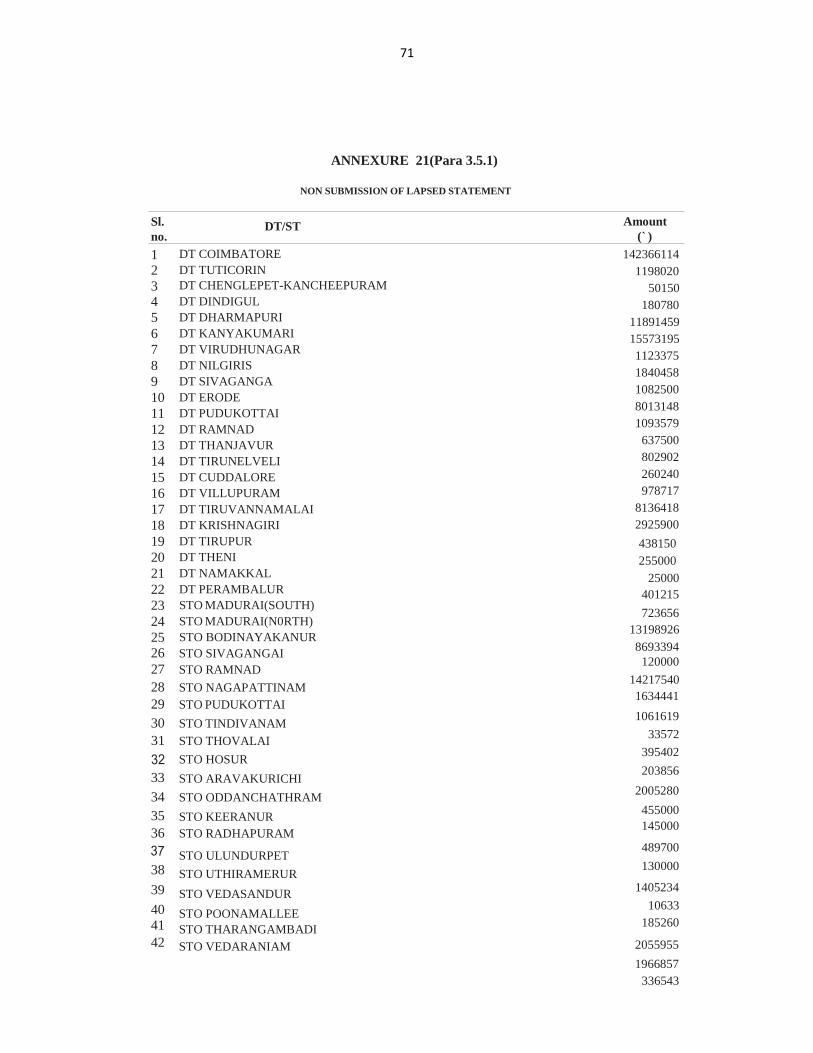

1. Deposits not lapsed to Government:

As per the provisions of Article 271 of Tamil Nadu Financial Code Volume I, deposits lying

unclaimed for more than 4 years shall lapse to Government. However, from the Deposit

records, it was noticed in most of the Treasuries / Sub Treasuries that an amount of Rs.3.89

28

crore remained unclaimed for more than four years and yet not lapsed to Government.

(Annexure 21)

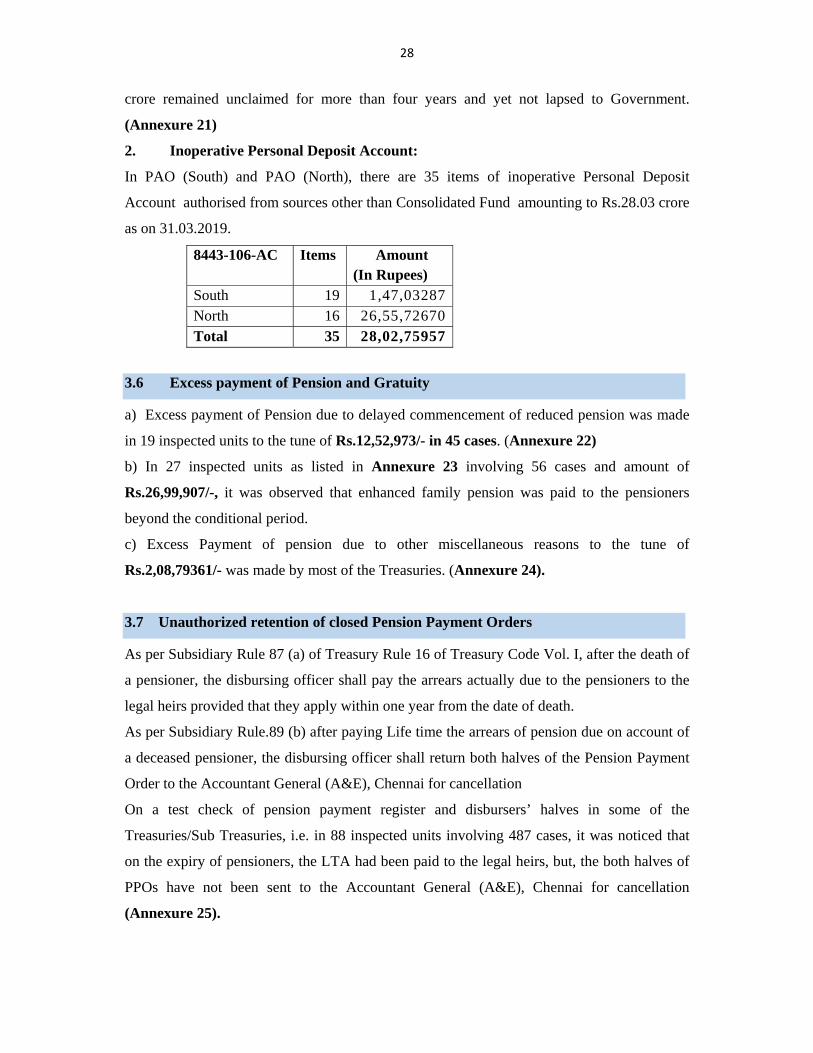

2. Inoperative Personal Deposit Account:

In PAO (South) and PAO (North), there are 35 items of inoperative Personal Deposit

Account authorised from sources other than Consolidated Fund amounting to Rs.28.03 crore

as on 31.03.2019.

8443-106-AC Items Amount (In Rupees)

South 19 1,47,03287North 16 26,55,72670Total 35 28,02,75957

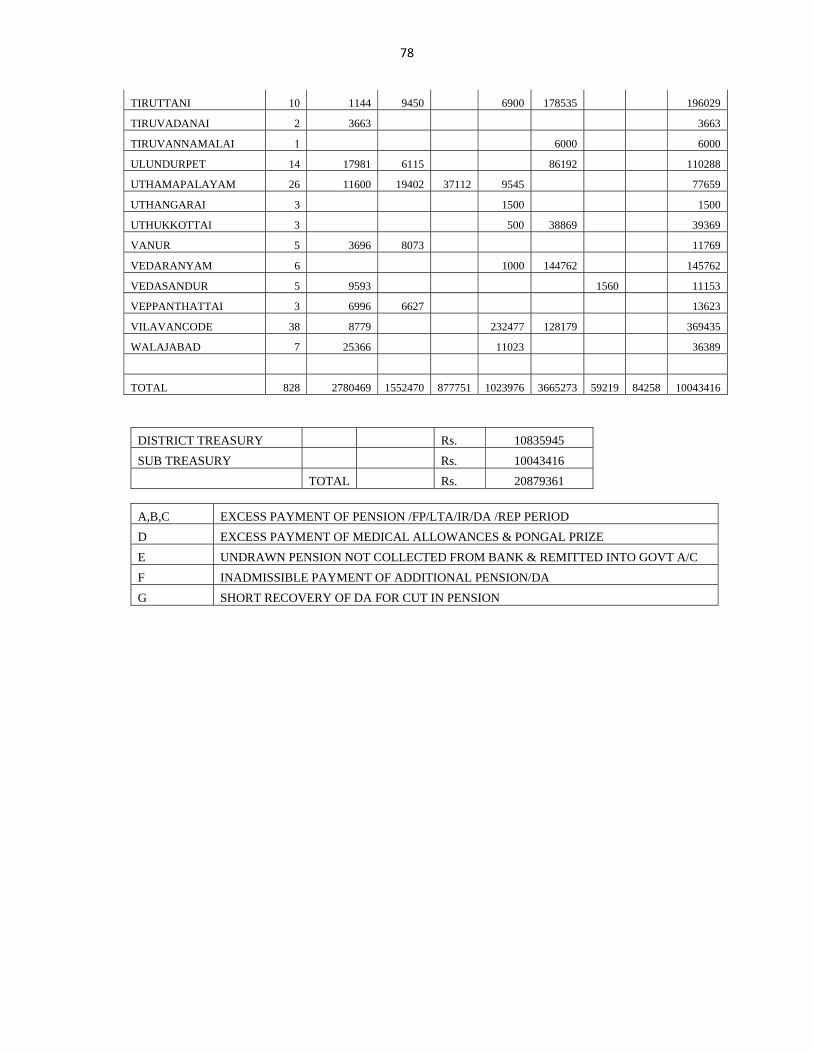

3.6 Excess payment of Pension and Gratuity

a) Excess payment of Pension due to delayed commencement of reduced pension was made

in 19 inspected units to the tune of Rs.12,52,973/- in 45 cases. (Annexure 22)

b) In 27 inspected units as listed in Annexure 23 involving 56 cases and amount of

Rs.26,99,907/-, it was observed that enhanced family pension was paid to the pensioners

beyond the conditional period.

c) Excess Payment of pension due to other miscellaneous reasons to the tune of

Rs.2,08,79361/- was made by most of the Treasuries. (Annexure 24).

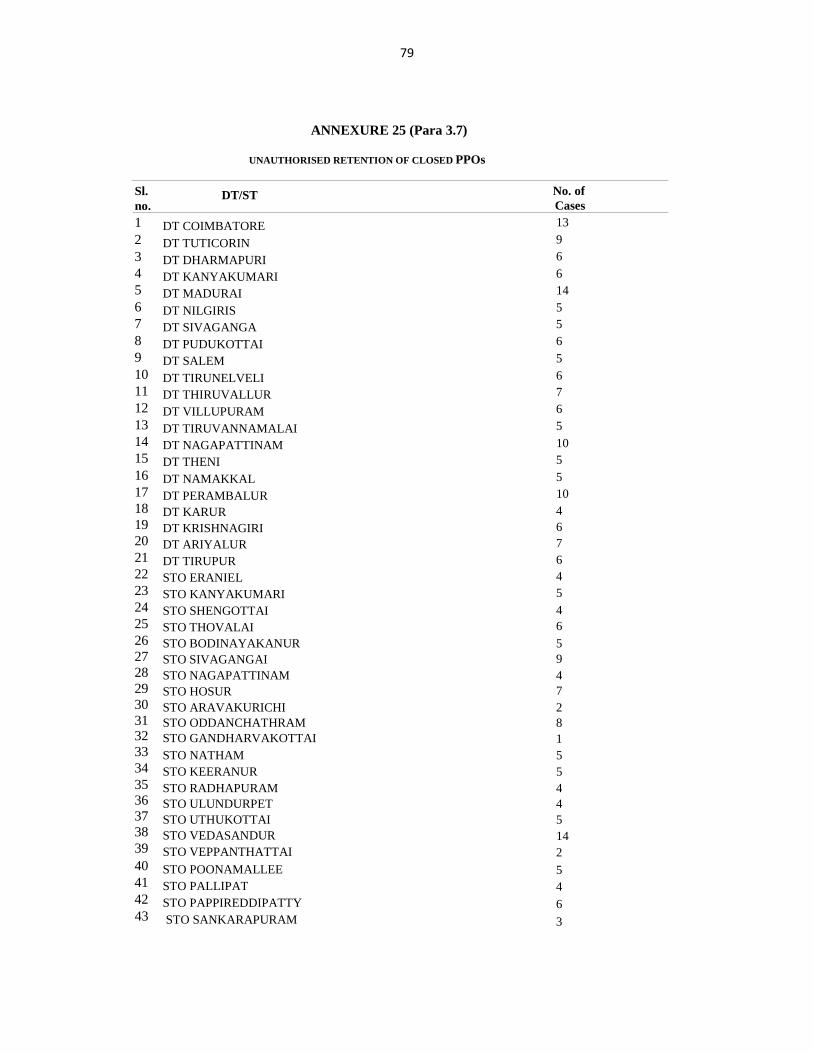

3.7 Unauthorized retention of closed Pension Payment Orders

As per Subsidiary Rule 87 (a) of Treasury Rule 16 of Treasury Code Vol. I, after the death of

a pensioner, the disbursing officer shall pay the arrears actually due to the pensioners to the

legal heirs provided that they apply within one year from the date of death.

As per Subsidiary Rule.89 (b) after paying Life time the arrears of pension due on account of

a deceased pensioner, the disbursing officer shall return both halves of the Pension Payment

Order to the Accountant General (A&E), Chennai for cancellation

On a test check of pension payment register and disbursers’ halves in some of the

Treasuries/Sub Treasuries, i.e. in 88 inspected units involving 487 cases, it was noticed that

on the expiry of pensioners, the LTA had been paid to the legal heirs, but, the both halves of

PPOs have not been sent to the Accountant General (A&E), Chennai for cancellation

(Annexure 25).

29

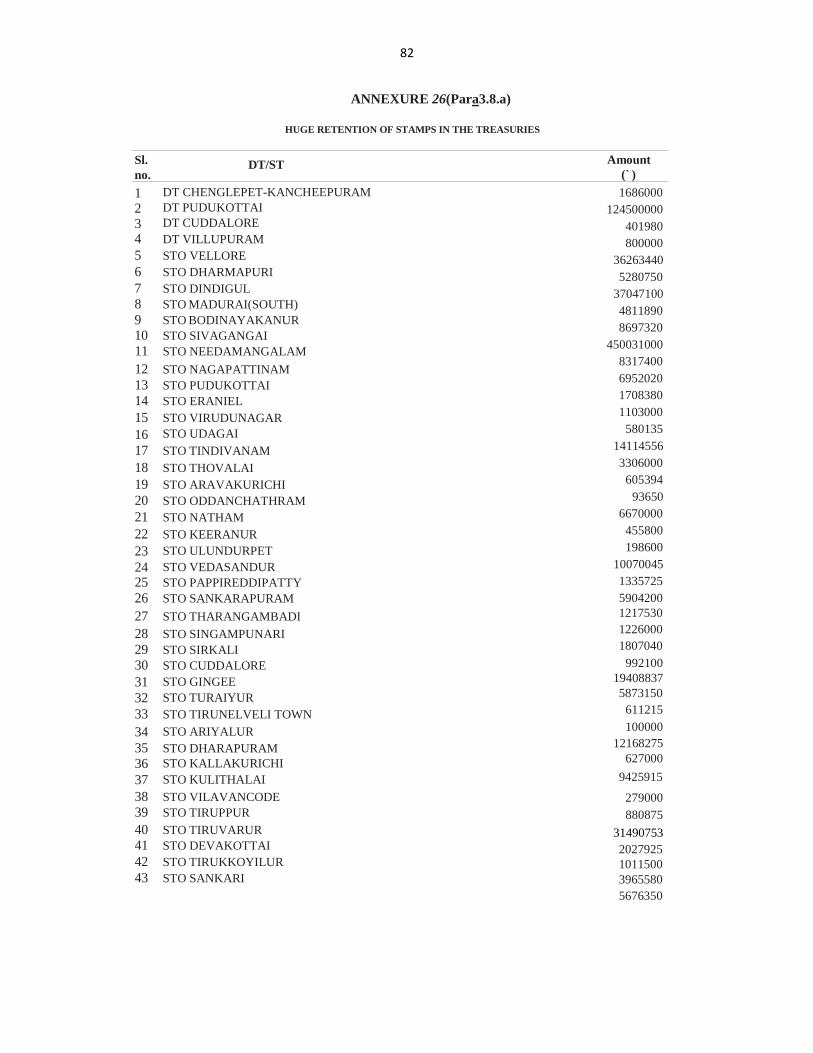

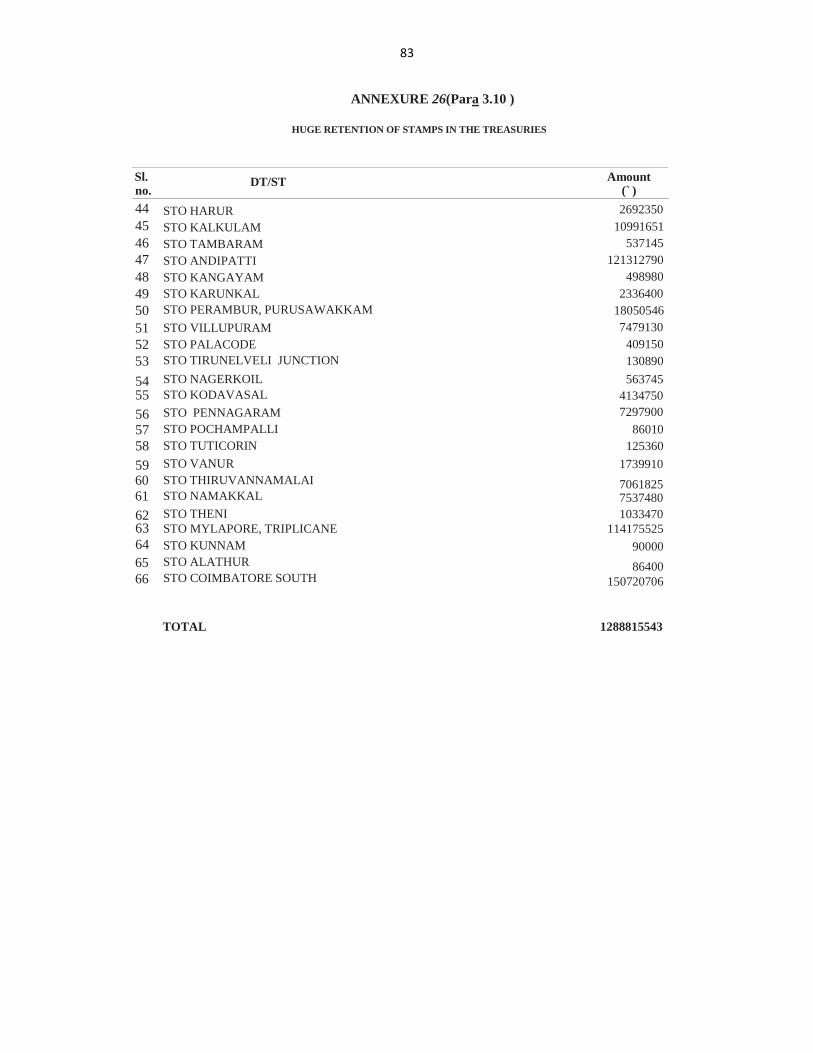

3.8 Stamp Account : Huge retention of stamps in the Treasuries

a) Stamps of huge value were kept in stock for long period in 66 inspected units as listed in

Annexure 26 which involves an amount of Rs.128.88 crore, without transferring them

to the other Treasuries / Sub- Treasuries with requirements.

b) No steps were taken by the following Sub Treasury Officers, for removal of damaged

stamps.

Sl.

No

Name of the Sub Treasury Number of cases Amount

In Rupees

1 Ramnad 42 129840

2 Perambur-Purasawakkam 8 102320

3 Kodavasal 2 8200

4 Mylapore- Triplicane 11 39525

5 Coimbatore South 18 274500

Total 83 8783910

c) Destruction of soiled / obsolete stamps:

The Superintendent of Stamps, Chennai had instructed (May 2018 and July 2018†) all the

Treasury Officers to furnish the destruction proposals for the soiled stamps along with the

Form No.XVIII to the General Stamp Office, Chennai for submitting the consolidated

destruction proposals to the Principal Secretary / Commissioner of Treasuries and Accounts.

During the Treasury Inspection at District Treasury Chennai during March 2019, it was

observed that the following stamps are non-moving for longer period at Sub Treasuries in

Chennai as well as at this District Treasury and became soiled / obsolete as on date.

Sl. No. Name of Stamp Face Value

(in Rupees)

1. Non Judicial 5,24,920

2. Court Fee Paper 30,975

3. Court Fee Label 1,260

† Letters No.Rc.No.923/2018/S2 dated 15/5/2018 and 23/7/2018

30

4. Foreign Bill 10,88,35,732

5. IALF 1,73,83,175

6. Brokers Note 2,92,67,020

7. Insurance 42,32,63,153

Total 57,93,06,235

Necessary proposal for destruction of soiled stamps and to write off the face value of above

stamps had been submitted (February 2019‡) by the Additional Treasury Officer, Chennai to

the Assistant Superintendent of Stamps Chennai, however, no action was taken in this regard

(July 2019),

d) Disposal of damaged / manufacturing defective sheets of stamps

The manufacturing defective / damaged stamps available at all the District / Sub Treasuries

had been returned to District Treasury, Chennai. The District Treasury had consolidated such

stamps and sent necessary proposals to Nasik / Hyderabad in the year 2011 for exchange of

those defective stamps with good sheets.

The Deputy Controller of Stamps, Central Stamp Depot, Nasik / Hyderabad had returned

most of the stamps without exchange with new ones in various batches by quoting the

reasons namely –“due to change in design and water mark, no pocket slips are available,

some items are old design”.

Therefore, the Deputy Controller of Stamps, Central Stamp Depot, Nasik/Hyderabad

recommended to take necessary action to dispose of those stamps as per Rule 49(2) of Supply

and Distribution of Stamps as in force in the State of Tamil Nadu, which empowers Principal

Secretary / Commissioner of Treasuries and Accounts, Chennai 35, to accord approval for

destruction and write off the value of stamps, wherein the value exceeds Rs.300/ -.

Accordingly, the following proposals for the disposal of damaged / defective sheets of stamps

which were sent to the Assistant Superintendent of Stamps, Chennai, through CTA, by the

Treasury Officer, was pending for more than three years.

‡ Letter Rc.No.255/2019/C2 dated 15/2/2019

31

File No. &

Date

Face Value

(Rs.)

Details of correspondences made

2586/09/C1 dt.27/01/2012

34,01,180 Prl. Secy. / CTA, Chennai in Lr.No.48635/L2/2017 dt.23/11/2017, requested the Govt. to issue destruction order and write off the value of defective stamps

2055/2013/C1 dt.07/07/2014

34,81,980 Prl. Secy. / CTA, Chennai in Lr.No.48636/L2/2017 dt.27/6/2018, requested the Govt. to issue destruction order and write off the value of defective stamps

3218/2014/C1 13,46,365 T.O., Chennai in Lr.No.3238/C1/2014 dated 8/2/2018 requested Assistant Superintendent of Stamps Chennai to take action for disposal of defective stamps.

3.9 Inspection of Strong Room and Issuance of Safety Certificate

With a view to ensuring the safety and security of the Strong room of the Treasuries/Sub-

Treasuries, where valuables of the Government, are stored, it is provided that Strong Room of

the Treasury shall be inspected annually by the P.W.D. Executive Engineer, or by his

Subordinate Officer nominated for the purpose and a certificate of safety to be issued by such

inspecting officer.

But in 16 inspected units as listed in Annexure 27, it was noticed that such certificates have

not been obtained.

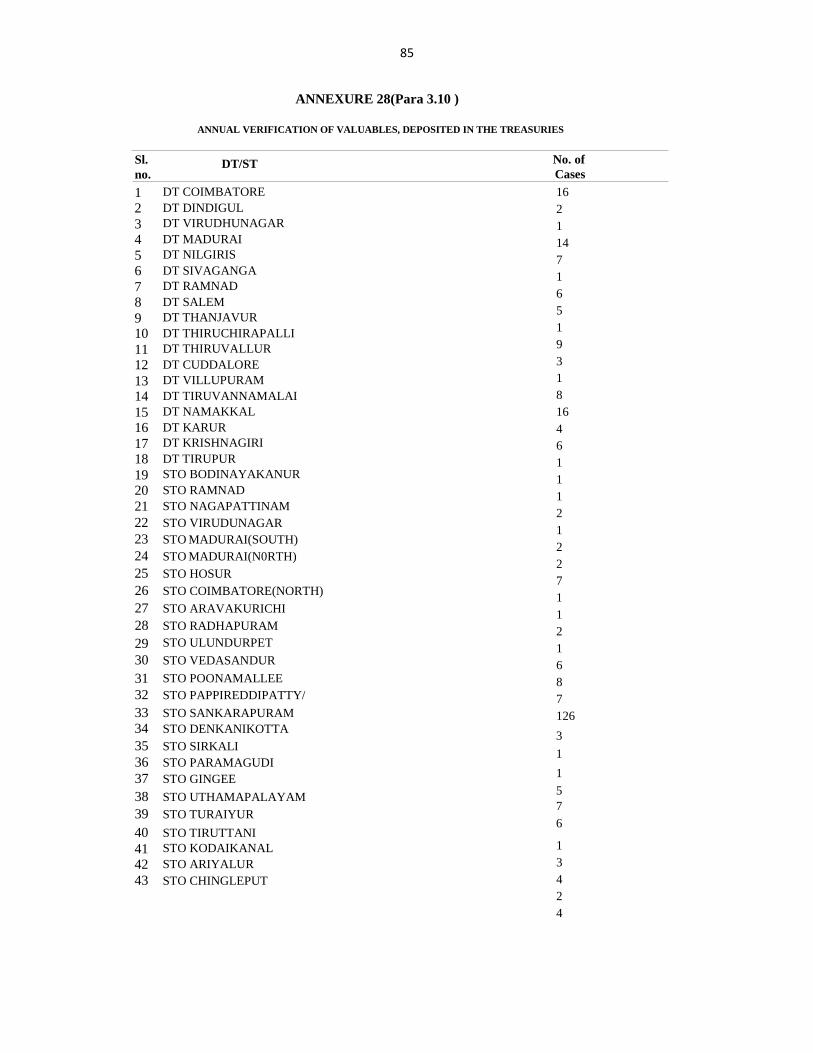

3.10 Annual Verification of Valuables, deposited in the Treasuries

Sealed packets/bags containing valuables which are lodged by different Drawing Officers in

the Treasury for safe custody are required to be verified by the depositing officers.

Non-verification of valuables deposited in the Treasuries prevents the depositors from

ascertaining the present status of sealed packets/sealed bags i.e. whether the valuables are

present or lost, sealed articles are intact or not.

In 69 inspected units given in Annexure 28, such annual verification of valuables was not

done by the depositors.

32

3.11 Inspection of Treasuries conducted by the Commissioner of Treasuries and

Accounts and Regional Joint Director of Treasuries & Accounts

As per the provision of Tamil Nadu Treasury Rule 4, the Commissioner of Treasuries &

Accounts Department (PS/CTA) and Regional Joint Director of Treasuries & Accounts

(RJDs) are periodically inspecting District Treasuries and Sub Treasuries.

The PS/CTA has conducted the Inspection of District Treasuries on the dates given below:

Sl. No Name of the District Period of Inspection

1 Tirunelveli 07/05/2018 to 08/06/2018

2 Dindigul 02/07/2018 to 27/07/2018

3 Tuticorin 27/08/2018 to 28/09/2018

4 Ramanathapuram 01/10/2018 to 26/10/2018

5 Sivagangai 08/11/2018 to 23/11/2018

6 Virudhunagar 10/12/2018 to 31/01/2019

7 Kanyakumari 04/02/2019 to 22/03/2019

The number of Sub Treasuries inspected by the Regional Joint Directors of all the six regions

Coimbatore, Vellore, Tirunelveli, Madurai, Trichy and Chennai, during the year 2018-19 is

furnished below:

Sl. No Name of the Regional Joint Director of Treasuries & Accounts Department

Number of Sub Treasuries inspected during the year

1 Madurai 37

2 Trichy 37

3 Tirunelveli 25

4 Chennai 22

5 Coimbatore 14

6 Vellore 9

33

3.12 Unencashed cheques not cancelled

As per Rule 47 (2) of the Central Government Account (Receipts and Payments) Rules, a

cheque remaining unpaid for any cause shall be cancelled and the amount written back in the

accounts. In respect of unencashed cheques lying under 8670, the Treasury offices have to

address the concerned DDOs to confirm the fact of payment or otherwise the unencashed

cheque amount shall be got written back or credited to Government Account by crediting the

original expenditure head of account. However, to the end of 31.03.2019, 613 cheques

amounting to Rs.6.87 crore are still remaining unencashed, in some of the Treasuries.

The Treasury wise details have been provided in Annexure 29.

Similarly, the details of cheques remaining unencashed in various PAOs are given below:

Name of the PAO Unencashed cheques Item Amount

South 33203 1793846324East 12082 2737834167North 6084 97579896Secretariat 4556 68356412Madurai 1748 30489027High Court 364 1999997Corporation 21 14862Pension 15 117323Total 58073 4730238008

3.13 Amount returned by Banks under Electronic Clearance System (ECS) not settled to

beneficiaries.

As on 31.03.2019, an amount of Rs.11.36 crore pertaining to 26154 beneficiaries were

returned by bank under ECS and remain under suspense account in various TOs/STs, for

want of correct details such as Name of the beneficiary, savings Bank Account Number etc

(Annexure 30).

34

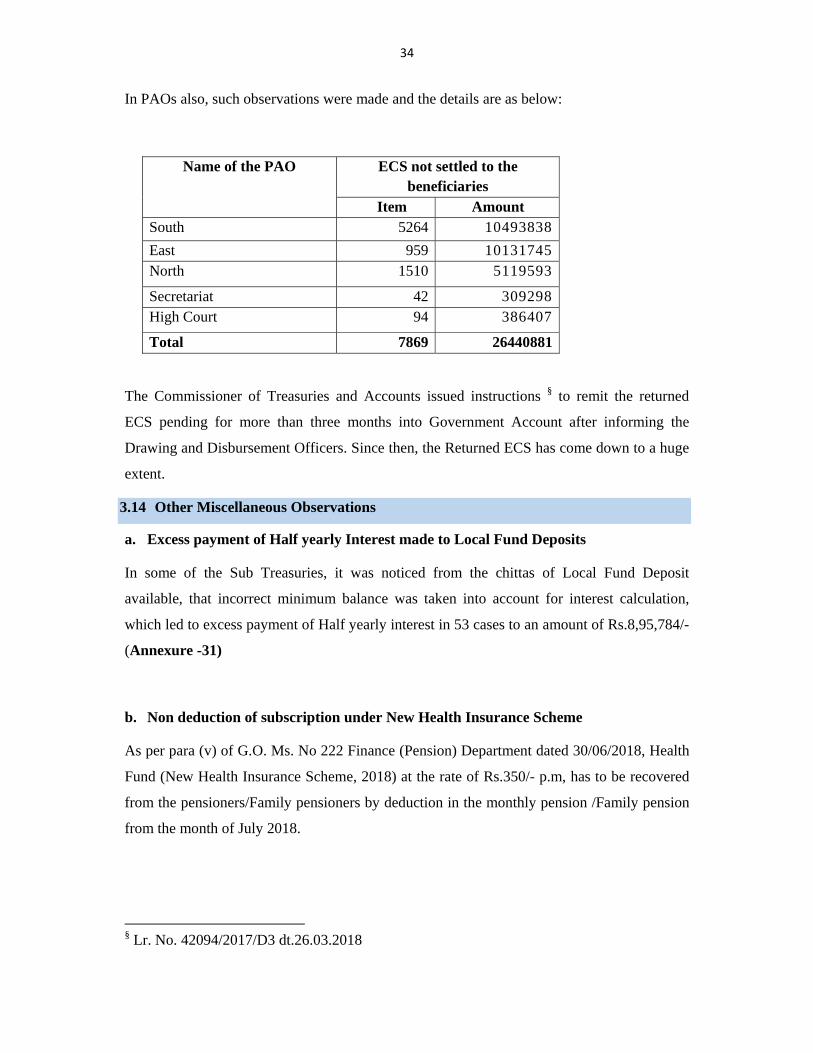

In PAOs also, such observations were made and the details are as below:

Name of the PAO ECS not settled to the beneficiaries

Item Amount South 5264 10493838

East 959 10131745North 1510 5119593

Secretariat 42 309298High Court 94 386407

Total 7869 26440881

The Commissioner of Treasuries and Accounts issued instructions § to remit the returned

ECS pending for more than three months into Government Account after informing the

Drawing and Disbursement Officers. Since then, the Returned ECS has come down to a huge

extent.

3.14 Other Miscellaneous Observations

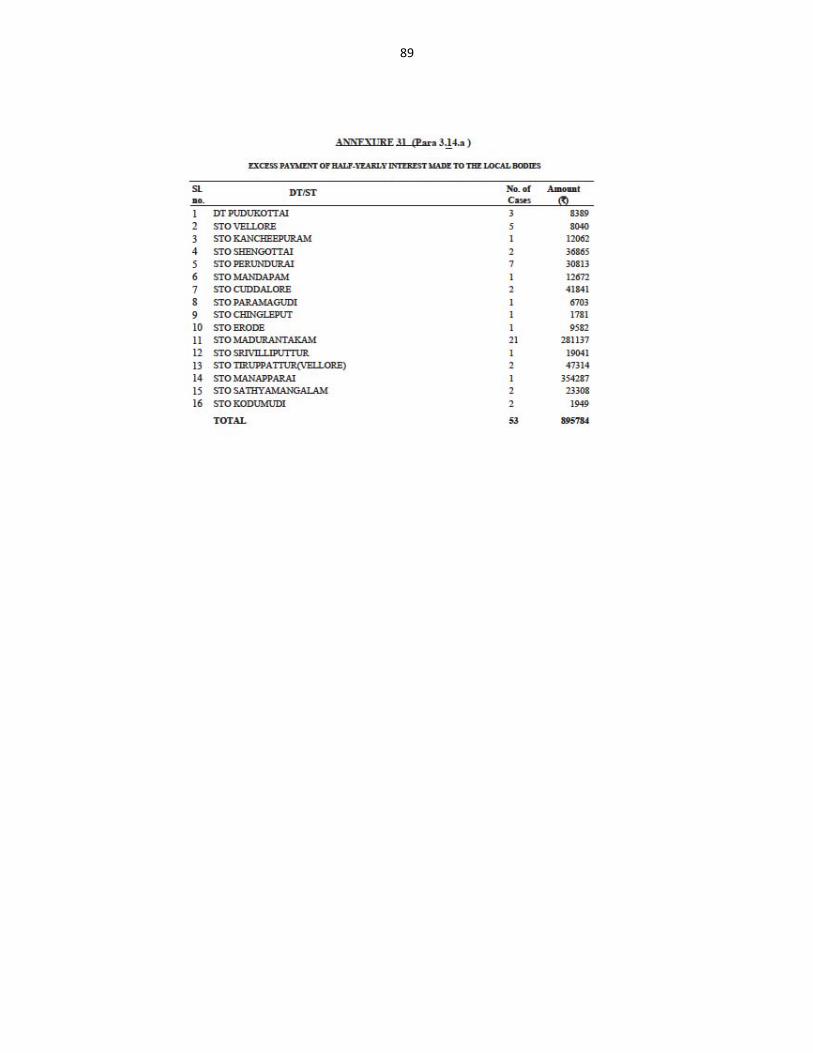

a. Excess payment of Half yearly Interest made to Local Fund Deposits

In some of the Sub Treasuries, it was noticed from the chittas of Local Fund Deposit

available, that incorrect minimum balance was taken into account for interest calculation,

which led to excess payment of Half yearly interest in 53 cases to an amount of Rs.8,95,784/-

(Annexure -31)

b. Non deduction of subscription under New Health Insurance Scheme

As per para (v) of G.O. Ms. No 222 Finance (Pension) Department dated 30/06/2018, Health

Fund (New Health Insurance Scheme, 2018) at the rate of Rs.350/- p.m, has to be recovered

from the pensioners/Family pensioners by deduction in the monthly pension /Family pension

from the month of July 2018.

§ Lr. No. 42094/2017/D3 dt.26.03.2018

35

However, on a scrutiny of the Civil Pension audit register, and pension schedule in various

District Treasuries and Sub Treasuries, it was noticed that the Health fund at the rate of Rs.

350/- p.m, totalling to Rs.7,48,650/- was not recovered from the pensioners (Annexure 32).

c. Expenditure incurred against Budget provision of works under the head 8443-

Depostis - Class III has lead to minus balances

While scrutinising the records at Dharmapuri District Treasury, it was observed that the

Divisional Engineer (H) NABARD and Rural Roads Division, had submitted proposals to the

Treasury to a tune of Rs.22,47,678/- for making payments under the Head 8443-Deposits

(Class-III) for the year 2017-18. There was no change in figures for the period 2016-17 also.

Further, it was noticed that there were minus figures against some works as detailed in

Annexure 33. It is construed that excess payments could have been made to the contractors

against the budget provisions of that particular work.

d. Minus balances under Deposit Register due to misclassification

i) It was seen from the Criminal Court Deposit register of Special Sub Judge (LOAP) Vellore

that, the deposit account has ended with a adverse balance of Rs. (-) 71,641/- as on 05-11-

2018. In spite of the existence of minus balance in the deposit account, payments were

continued to be paid and the adverse balance increased to Rs.(-) 51,49,325/- as on 31-12-

2018.

ii) It was seen from the T Deposit Register of Executive Officer, Town Panchayat, Thorapadi,

that the deposit account ended with an adverse balance of Rs. (-) 66040.63 on 30/ 11/2017

and no transactions have taken place thereafter.

The existence of minus balance in the deposit account shall be due to either over drawal or

misclassifications made in the Treasury Account.

e. Wrong classification of Revenue Receipts

The finance department vide Lr. No.22400/LC /2016-1,dt.31/03/2016 read with GO 72 dt

29/02/2016 stipulated that the existing Letter of Credit system for PWD

(Buildings/Irrigation), Highways and Forests or cheque system of Technical Education, shall

remain suspended and all transactions of the above departments will be made by presenting

bills in the PAO/DTO/STOs under the ECS system with effect from 01/04/2016. Further, it

36

was stated in the letter that all concerned PAOs/DTs/STOs shall open the following new

heads of account as detailed below:

Head of A/C Nomenclature

8443-00-109-AB Class-I, cash deposits of subordinates as secured deposits

AB-0007 Out go: 000D- Receipts

8443-00-109-AC Class-II, cash deposits of Contractors as security Forests

AC-0005 Out go: 000F- Receipts

8443-00-109-AD Class-III, cash deposits for works to be done

AD-0003 Out go: 000H- Receipts

8443-00-109-AE Class-IV, Sum due to contractor on closed account

AE-0001 Out go: 000J- Receipts

8443-00-109-AF Class-V, Miscellaneous deposits-

AB-0009 Out go: 000B- Receipts

While reviewing the accounts of the Forest department, it was noticed that the department

had received various receipts from the individuals through sales, fee collection - permit fees,

sale of permit, C Fees collection, property mark registration etc. which was credited into

‘8443-00-109-AF-00B (Class-V)’ and was also accounted for under the same head of

account. The procedure adopted for accounting is not in order. 109 such cases were observed

in 4 inspected units as given below:

Sl. No Name of the District Number of cases

1 Nagercoil 12

2 Nilgiris 70

3 Villupuram 13

4 Namakkal 14

Total 189

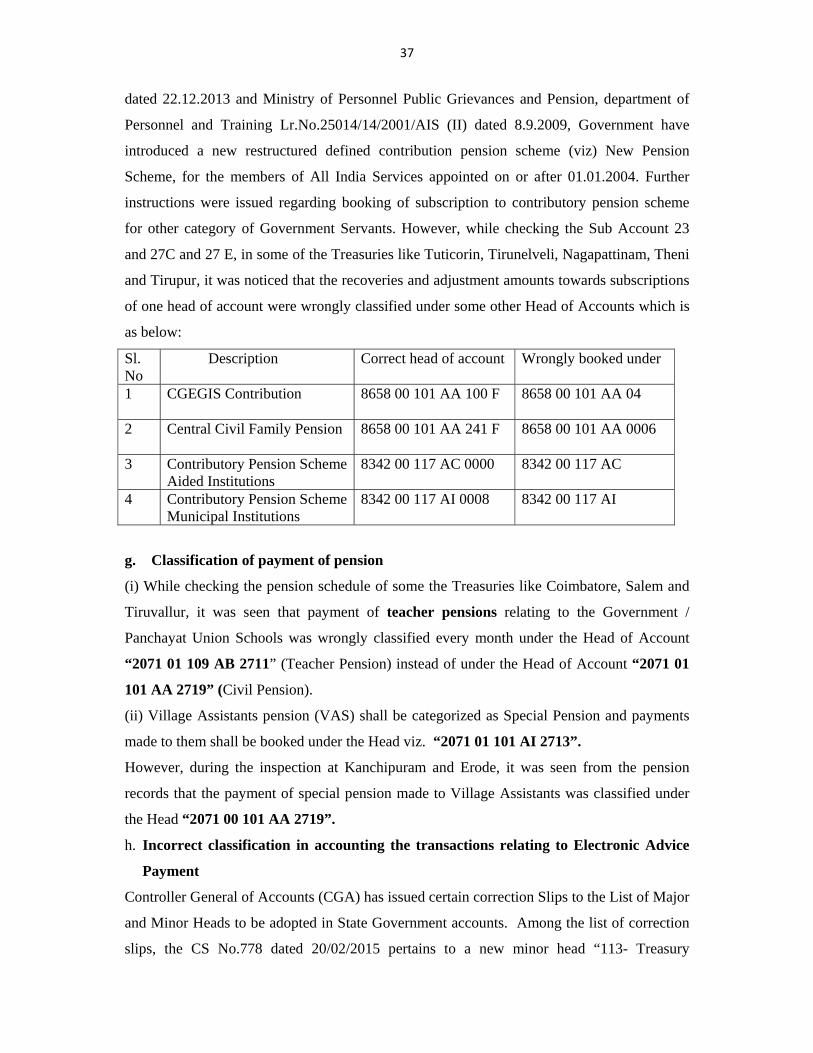

f. Incorrect classification of CPS contributions

According to G.O.M.S.No.1155 (Public) (Special B) department dated 8.12.2011 read with

Ministry of Finance, Department of Economic Affairs notification No.5/7/2003/ECB/&PBR

37

dated 22.12.2013 and Ministry of Personnel Public Grievances and Pension, department of

Personnel and Training Lr.No.25014/14/2001/AIS (II) dated 8.9.2009, Government have

introduced a new restructured defined contribution pension scheme (viz) New Pension

Scheme, for the members of All India Services appointed on or after 01.01.2004. Further

instructions were issued regarding booking of subscription to contributory pension scheme

for other category of Government Servants. However, while checking the Sub Account 23

and 27C and 27 E, in some of the Treasuries like Tuticorin, Tirunelveli, Nagapattinam, Theni

and Tirupur, it was noticed that the recoveries and adjustment amounts towards subscriptions

of one head of account were wrongly classified under some other Head of Accounts which is

as below:

Sl. No

Description Correct head of account Wrongly booked under

1 CGEGIS Contribution

8658 00 101 AA 100 F 8658 00 101 AA 04

2 Central Civil Family Pension

8658 00 101 AA 241 F 8658 00 101 AA 0006

3 Contributory Pension SchemeAided Institutions

8342 00 117 AC 0000 8342 00 117 AC

4 Contributory Pension SchemeMunicipal Institutions

8342 00 117 AI 0008 8342 00 117 AI

g. Classification of payment of pension

(i) While checking the pension schedule of some the Treasuries like Coimbatore, Salem and

Tiruvallur, it was seen that payment of teacher pensions relating to the Government /

Panchayat Union Schools was wrongly classified every month under the Head of Account

“2071 01 109 AB 2711” (Teacher Pension) instead of under the Head of Account “2071 01

101 AA 2719” (Civil Pension).

(ii) Village Assistants pension (VAS) shall be categorized as Special Pension and payments

made to them shall be booked under the Head viz. “2071 01 101 AI 2713”.

However, during the inspection at Kanchipuram and Erode, it was seen from the pension

records that the payment of special pension made to Village Assistants was classified under

the Head “2071 00 101 AA 2719”.

h. Incorrect classification in accounting the transactions relating to Electronic Advice

Payment

Controller General of Accounts (CGA) has issued certain correction Slips to the List of Major

and Minor Heads to be adopted in State Government accounts. Among the list of correction

slips, the CS No.778 dated 20/02/2015 pertains to a new minor head “113- Treasury

38

Electronic Advice Payments (ECS)” to be opened under the Major Head “8670” and all the

ECS transactions have to be classified under this Head and the fact has been communicated

to the Commissioner of Treasuries and Accounts Chennai vide Lr.No.AG(A&E)/Book

I/GL/2017-18/8073 dated 24/04/2017 to make necessary arrangements to provide figures

relating to “cheques-issued” to be booked under 8670-104 and ECS transaction under the

Minor Head 8670-113 distinctively.

However, it was observed that in some of the Treasuries listed below, the transactions

relating to the ECS payment transaction made by the District Treasury through agency bank

are still being booked under “8670-104” instead of “8670-113”.

Sl. No Name of the District

1 Coimbatore

2 Dharmapuri

3 Sivagangai

4 Tiruvarur

5 Tirunelveli

6 Perambalur

7 Kanchipuram

8 Nagapattinam

9 Krishnagiri

10 Erode

11 Theni

12 Salem

i. Non-Mustering by pensioners resulting in stoppage of Pension

According to Government letter No.2428/98-5 dated 21/07/2009 of Finance (Pension)

Department, all pension disbursing officers should make arrangement for annual mustering of

pensioners from April to June every year if they do not produce life certificate. If they

produce life certificate, the same can be accepted.

But during the Treasury Inspection conducted in various Treasuries / Sub Treasuries, it was

noticed from the check register and pension schedule, the pension payments were stopped

due to non-mustering in 333 cases. The life certificate was also not received. Especially, in

Vilavancode Sub Treasury, 103 pensioners have not done their annual mustering.

39

Annexure 1 (Para 1.1)

1

Additional Director (Admin)

Personal Assistant(Admin)(In Chief Accounts Officer Cadre)

Personal Assistant(Treasury Control)(In Chief Accounts Officer Cadre)

Additional Director

(e-Governance)

*Regional Joint Directors (Chennai, Madurai, Trichy, Coimbatore, Vellore, Tirunelveli)

Pension Pay Officer, Chennai (Chief Accounts

Officer Cadre)

32, District Treasury Officers - In Chief

Accounts Officer Cadre

Pay and Accounts Officer (North)

Chennai*

Pay and Accounts Officer (South)

Chennai*

Pay and Accounts Officer (East)Chennai*

Pay and Accounts Officer (Secretariat)

Chennai*

Pay and Accounts Officer Madurai*

Pay and Accounts Officer (High Court)

Chennai*

Sub Pay and Accounts Officer (Corporation)

Chennai* *

Sub Pay and Accounts Officer (High Court Branch, Chennai)

Madurai* *

Sub Pay and Accounts OfficerNew Delhi* *

Principal Secretary / Commissioner of Treasuries and Accounts

Assistant Superintendent of Stamps, Chennai

( Chief Accounts Officer Cadre)

Joint Director (New Health Insurance

Scheme)

1. Accounts Officer (Bills)2. Accounts Office(IFHRMS)3. Accounts Officer (New Health Insurance Scheme)

4. Accounts Officer (Pensioner New Health Insurance Scheme )

5. Accounts Officer (System Analyst)

6.Accounts Officer (GeM)

Joint Director (e-Governance)

OVERALL CHART OFDEPARTMENT OF TREASURIES AND ACCOUNTS

Additional Director(Schemes)

Additional Director (New Pension Scheme)

* In Joint Director Cadre

* * In Accounts Officer Cadre

243 Sub Treasuries-(Assistant Treasury

Officer)

1. Chief Accounts Officer (New Pension Scheme)

2. Assistant Accounts Officer (New Pension Scheme)

1. Chief Accounts Officer (Legal Cell)

2. Assistant Accounts Officer (Legal Cell)

40

Annexure 2 (Para 2.1)

DISTRICT WISE DETAILS OF WANTING VOUCHERS FOR THE YEAR 2018-19

NAME OF DISTRICT NUMBER OF VOUCHERS AMOUNT DINDIGUL 70 118730291SIVAGANGAI 68 102093539KANCHEEPURAM 54 238721435TIRUPPUR 32 166660787VILLUPURAM 59 485810000COIMBATORE 63 96998834DHRAMAPURI 37 36817058NAGERKOIL 27 85546162PERAMBALUR 17 7810934PUDUKOTTAI 46 52784807RAMNAD 27 49767032TRICHY 71 155235311TIRUVALLUR 58 214311698CUDDALORE 41 99695445MADURAI 31 47859631ARIYALUR 24 21613081KARUR 12 63353850NAMAKKAL 12 20816485SALEM 102 306401568KRISHANGIRI 18 99046131THANJAVUR 30 185937676TIRUVARUR 23 86937422THENI 23 37621797TIRUVANNAMALAI 126 286520354VIRUDHUNAGAR 26 220145923VELLORE 111 442093053ERODE 40 78600967NAGAPATTINAM 25 66060031TUTICORIN 30 51453689TIRUNELVELI 73 104034067NILGIRIS 22 21332294 GRAND TOTAL 1398 4050811352

41

Annexure 3 (Para 2.2)

Treasury wise details of pending Temporary Advances drawn up to 31.03.2019 Sl. No Name of the Treasury/PAO Number of items Amount

1 DT Ariyalur 24 11573114 2 DT Coimbatore 38 22931027 3 DT Kancheepuram 35 29905134 4 DT Cuddalore 53 62460293 5 DT Dharmapuri 22 15140342 6 DT Krishnagiri 17 9978256 7 DT Erode 4 6041380 8 DT Karur 27 14521122 9 DT Madurai 19 16808250

10 DT Nagapattinam 23 10777800 11 DT Namakkal 5 4029739 12 DT Perambalur 13 3900490 13 DT Salem 25 22877769 14 DT Thanjavur 5 8639200 15 DT Tiruvarur 20 11628060 16 DT Udhagamandalam 2 100000 17 DT Tiruppur 14 8410650 18 DT Tirchy 21 13323243 19 DT Pudukkottai 28 21610389 20 DT Sivagangai 18 21345472 21 DT Dindigul 4 4974135 22 DT Tirunelveli 24 6446840 23 DT Nagarcoil 10 4361251 24 DT Virudhunagar 9 5738200 25 DT Thoothukudi 15 11319505 26 DT Ramanathapuram 35 12974424 27 DT Tiruvallur 31 29430360 28 DT Villupuram 24 23209020 29 DT Vellore 18 19717623 30 DT Tiruvannamalai 21 13828970 31 PAO (South) 81 2596069959 32 PAO (North) 38 78545656 33 PAO (East) 39 320256007 34 PAO (Secretariat) 74 46987887 35 PAO (High Court), Chennai 91 720245908 36 PAO Madurai 61 45091366

GRAND TOTAL 988 4255198841

42

Annexure 4 (Para 2.4.1)

Details of wanting MCA credit schedule in respect of All India Service Officers

Sl. No

Month District Sub Account Amount

1 Sep-18 Ariyalur 20B 3300

2 Nov-18 Kanchipuram 10 17800

3 Sep-18 Cuddalore 10 4000

4 Mar-19 Cuddalore 11 490

5 Mar-19 Cuddalore 4 1000

6 Feb-19 Nagercoil 18D 1400

7 Feb-19 Nagercoil 11 840

8 Mar-19 Nagercoil 11 840

9 Feb-19 Nilgiris 26C 4380

10 Jan-19 PAO Madurai 11 6000

11 Feb-19 PAO Madurai 26E 3050

12 Aug-18 Sivagangai 26E 1000

13 Mar-19 Sivagangai 16A 5000

14 Mar-19 Erode 8 1500

15 Nov-18 Nagapattinam 10 3000

16 Sep-18 Nagapattinam 11 1480

17 Feb-19 Nagapattinam 11 1000

18 Feb-19 Nagapattinam 18B 7330

19 Mar-19 Nagapattinam 11 1000

20 Oct-19 Salem 5 3000

21 Feb-19 Salem 16 830

22 Aug-18 Tiruvallur 12 4000

23 Sep-18 Tiruvallur 12 2000

24 Oct-18 Tiruvallur 10 4500

25 Oct-18 Tiruvallur 11 1000

26 Oct-18 Tiruvallur 17 3000

27 Nov-18 Tiruvallur 12 2000

28 Dec-18 Tiruvallur 13 1000

29 Jan-19 Tiruvallur 12 1000

43

30 Feb-19 Tiruvallur 12 2000

31 Feb-19 Tiruvallur 13 3423

32 Feb-19 Tiruvallur 18A 3700

33 Feb-19 Tiruvallur 26D 2500

34 Mar-19 Tiruvallur 13 7200

GRAND TOTAL 105563

44

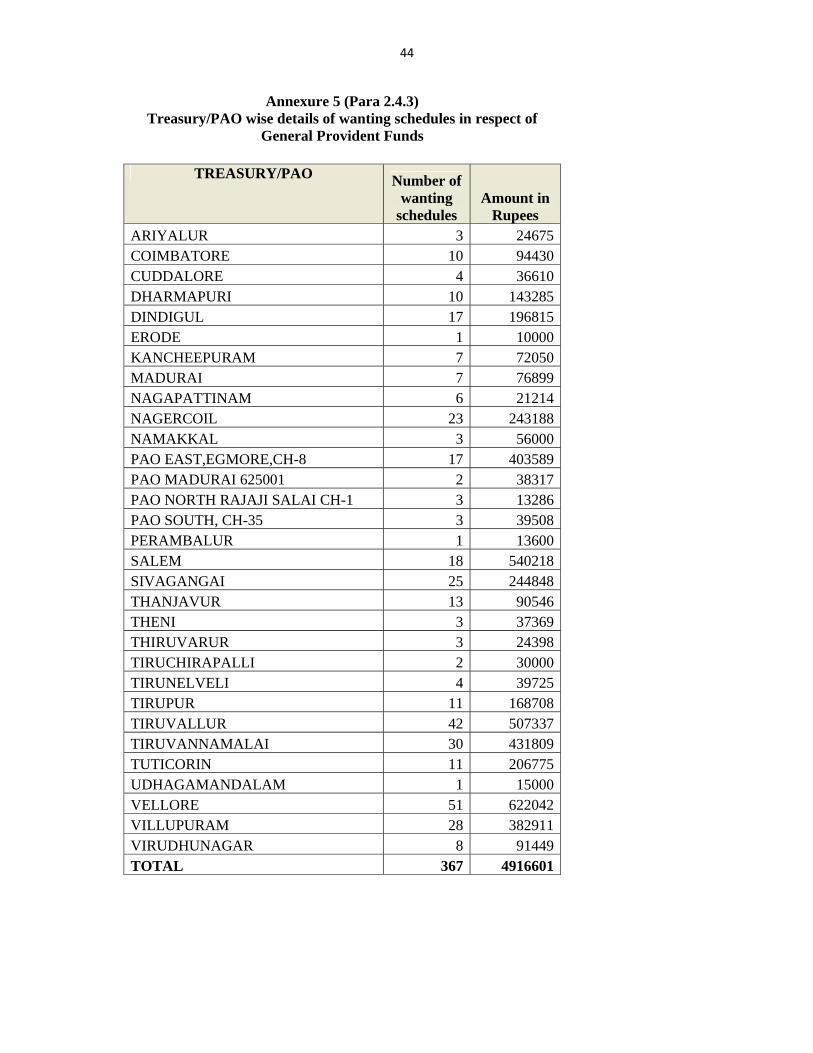

Annexure 5 (Para 2.4.3) Treasury/PAO wise details of wanting schedules in respect of

General Provident Funds

TREASURY/PAO Number of wanting

schedules Amount in

Rupees ARIYALUR 3 24675COIMBATORE 10 94430CUDDALORE 4 36610DHARMAPURI 10 143285DINDIGUL 17 196815ERODE 1 10000KANCHEEPURAM 7 72050MADURAI 7 76899NAGAPATTINAM 6 21214NAGERCOIL 23 243188NAMAKKAL 3 56000PAO EAST,EGMORE,CH-8 17 403589PAO MADURAI 625001 2 38317PAO NORTH RAJAJI SALAI CH-1 3 13286PAO SOUTH, CH-35 3 39508PERAMBALUR 1 13600SALEM 18 540218SIVAGANGAI 25 244848THANJAVUR 13 90546THENI 3 37369THIRUVARUR 3 24398TIRUCHIRAPALLI 2 30000TIRUNELVELI 4 39725TIRUPUR 11 168708TIRUVALLUR 42 507337TIRUVANNAMALAI 30 431809TUTICORIN 11 206775UDHAGAMANDALAM 1 15000VELLORE 51 622042VILLUPURAM 28 382911VIRUDHUNAGAR 8 91449TOTAL 367 4916601

45

Annexure 6 (Para 2.4.3)

Copies of Letters addressed to Commissioner of Treasuries & Accounts & Treasuries

46

47

48

Annexure 7 (Para 2.5)

YEAR WISE ANALYSIS OF THE DIFFERENCES OF RESERVE BANK DEPOSITS

Year for the previous years and month for the current

year

DEBIT CREDIT

Number of items Amount in Rs.

Number of items Amount in Rs.

2009-2010 6 1,17,29,520.73 9 61,26,561.612010-2011 14 4,68,89,169.41 13 2,67,78,460.372011-2012 34 8,82,76,093.96 27 3,57,99,517.822012-2013 70 41,83,77,296.28 66 24,59,65,092.632013-2014 125 65,08,92,085.00 155 69,06,55,259.712014-2015 162 6,71,10,99,159.75 195 6,85,85,09,609.992015-2016 230 4,92,51,24,525.58 312 4,97,89,55,131.682016-2017 261 33,23,05,46,083.59 372 35,96,88,97,258.542017-2018 285 5,36,22,67,489.66 334 3,60,16,88,260.17

Apr-18 19 3,16,01,119.00 24 47,70,44,614.04May-18 18 54,18,02,888.93 32 1,21,33,97,453.98Jun-18 32 1,65,97,79,605.10 25 1,09,56,31,218.97Jul-18 16 63,83,00,986.30 25 96,20,27,615.50Aug-18 18 67,07,74,358.50 28 1,09,68,56,901.09Sep-18 16 10,35,11,329.62 17 30,07,38,810.26Oct-18 13 6,86,73,424.00 27 89,10,65,901.15Nov-18 23 83,30,26,230.85 23 49,96,41,046.36Dec-18 15 29,31,91,111.28 41 69,51,89,200.76Jan-19 20 2,03,26,705.50 23 69,85,91,747.98Feb-19 20 32,39,72,808.90 29 1,27,91,02,970.10Mar-19 22 1,03,66,06,268.54 32 1,07,62,26,907.63

TOTAL

1419 57,66,67,68,260.48 1809 62,69,88,89,540.34

NET DIFFERENCE 5,03,21,21,279.86 CR

49

Annexure -8 (Para 2.8)

Types of objections noticed while checking vouchers selected through Stratified Sampling

Treasury Findings Sub-Account

Month References issued vide

Remarks