anz v2 plus product disclosure statement

TRANSCRIPT

ANZ V2 PLUSProduct Disclosure Statement

November 2005

ANZ Financial Services Licence Number 234527.

What is a Product Disclosure Statement (PDS)?

This booklet contains the terms and conditions for ANZ V2 PLUS with direct banking, ANZ V2 PLUS withoutdirect banking and ANZ V2 PLUS Intermediary investments.It is important that you read the terms and conditionscarefully before deciding to invest in ANZ V2 PLUS.

This document must be read in conjunction with the ANZ Personal Banking Account Fees & Charges booklet.Together they form your Product Disclosure Statementfor ANZ V2 PLUS, Direct Debits, Periodical Payments,Internet and Phone Banking and BPAY

®.

® Registered to BPAY Pty Ltd ABN 69 079 137 518

ANZ V2 PLUS awarded five stars in the 2005CANNEX deposit

account star ratingsTM

s t a r r a t i n g s

de p o s i t a c c o un t

Should you have any additional questions about the ANZ V2 PLUS account:

• Call into any ANZ branch

• Phone the V2 PLUS Service Centre on 13 28 33

• Fax the V2 PLUS Service Centre on 1800 671 800

Further contact details are provided on the inside back cover.

1

Table of Contents1. Your V2 PLUS Investment

1.1 What is V2 PLUS? 31.2 Who can invest? 31.3 Identification 41.4 How to invest? 41.5 Additional investments 51.6 Appointment of an intermediary/

authorised representative 5

2. Account Operation

2.1 Withdrawing funds via the V2 PLUSService Centre 6

2.2 Withdrawing funds via direct banking facilities 72.3 Operation of the account by an

intermediary/authorised representative 82.4 Cheques 82.5 Bank cheques 92.6 Inactive accounts 102.7 Disruption to service 102.8 Maintaining your minimum balance 102.9 Interest rate 112.10 Interest payments 112.11 Investor statements 112.12 Changes to fees and charges, interest

rates and terms and conditions 122.13 Customer details 122.14 Joint investments 132.15 Third party signatories for V2 PLUS with direct

banking facilities 142.16 Investment by companies 142.17 Investments by partnerships, trusts and

unincorporated associations 142.18 Periodical Payments for V2 PLUS

with direct banking facilities 152.19 Direct debiting for V2 PLUS with

direct banking facilities 152.20 Stopping payments for periodical

payments and direct debits 152.21 Closure 162.22 Indemnity 162.23 Anti-Money Laundering 16

2

3. Fees and Charges

3.1 Bank fees and charges 173.2 Government charges 17

4. Disclosures

4.1 Personal advice 184.2 Monitoring enquiries and transactions 184.3 Privacy and confidentiality 184.4 Tax File Number 204.5 Code of Banking Practice 20

5. Enquiries and Complaint resolution 20

6. Electronic Banking 21

6.1 EFTPOS 216.2 MAESTRO and CIRRUS 226.3 Fees and charges, MAESTRO and CIRRUS 226.4 Surcharging, MAESTRO and CIRRUS 226.5 Exchange rates and conversion,

MAESTRO and CIRRUS 226.6 Daily withdrawal limit 226.7 PLUS 236.8 Fees and charges, PLUS 236.9 Surcharging, PLUS 236.10 Exchange rates and conversion, PLUS 246.11 Lost and stolen Card and PIN within Australia 246.12 Lost and stolen Card and PIN while overseas 24

7. Electronic Banking Conditions of Use 25

References to ANZ and ANZ Trustees

• “ANZ” refers to Australia and New Zealand BankingGroup Limited ABN 11 005 357 522 and its relatedentities.

• “ANZ Trustees” refers to ANZ Executors and TrusteeCompany Limited ABN 33 006 132 332 which is awholly owned subsidiary of ANZ.

3

1. Your V2 PLUS Investment1.1 What is V2 PLUS?

An investment in V2 PLUS is the acquisition from ANZTrustees of an interest in a certificate of deposit issued by ANZ to ANZ Trustees. ANZ Trustees has been appointedby ANZ to administer V2 PLUS. ANZ Trustees is a whollyowned subsidiary of ANZ.

When you open a V2 PLUS investment, ANZ Trusteesassigns to you, absolutely, an interest in a certificate ofdeposit issued by ANZ corresponding to the amount youinvest. ANZ has the right to replace a V2 PLUS certificatefrom time to time if the amount to which it relates ispartially paid or if ANZ Trustees wishes to acquire a furtherV2 PLUS certificate.

V2 PLUS is available with or without direct bankingfacilities. Direct banking facilities enable you to accessyour V2 PLUS investment via electronic methods such asATMs, EFTPOS, ANZ Phone and ANZ Internet Banking inaddition to performing transactions at ANZ branches or viathe V2 PLUS Service Centre. With V2 PLUS without directbanking facilities you can only make withdrawals via the V2 PLUS Service Centre.

1.2 Who can invest?

You can open a V2 PLUS investment if you are:

• an individual over 18 years of age;• joint individuals over 18 years of age;• a company;• a partnership;• an unincorporated association; or• a trustee.

If the V2 PLUS investment is for anyone under the age of 18years, the investment must be made in either the parent’sor guardian’s name.

ANZ Trustees has the right, at its discretion, to accept orreject your application for a V2 PLUS investment.

4

1.3 Identification

The Financial Transaction Reports Act – 100-pointidentification requirement applies to the opening ofV2 PLUS with or without direct banking facilities. If you wishto open a V2 PLUS investment and have not completed a100-point check with ANZ, you will need to do so, as willeach person who is authorised to operate the investment. (If you have already identified yourself with ANZ, you willonly need to advise the name of the branch whereidentification was presented and your account number).

The identification requirements for a 100-point check canbe satisfied if you bring four of the following documentswhen you open your account:

• drivers license;• credit card;• Medicare card;• electricity or gas bill; or• current rates notice.

Only two of the above documents are required if you alsobring one of the following:

• birth certificate;• passport; or• citizenship certificate.

Note: One of the documents provided must contain yourphotograph or signature. Some other documents thatestablish your identity and name will also be accepted. Ask ANZ staff for help.

Listed below are the additional documents andidentification you may need to bring with you when youopen your account:

• Tax File Number (optional); and• Trust Deed (for Super Funds, Family and Unit Trusts

only)

1.4 How to invest?

The minimum investment needed to open a V2 PLUSinvestment is $5,000. Initial investments can be made incash at any ANZ branch, by cheque crossed not negotiableand made payable to the account holder or via electronictransfer.

5

1.5 Additional investments

Additional investments can be made:

• by automatic direct credits into your investment;• in person at any ANZ branch;• by mail to the V2 PLUS Service Centre (via cheque);• at V2 PLUS shop fronts (via cheque);• by ANZ Phone Banking or ANZ Internet Banking transfer

from another ANZ account; or• at any ANZ ATM which accepts deposits with your

linked card.

Any subsequent and additional investments made toacquire a further interest in V2 PLUS will be on the sameterms and conditions as the initial investment (subject toany changes made in accordance with these terms andconditions) and will constitute an offer to purchase fromANZ Trustees an interest in a certificate of deposit issuedby ANZ to the extent of the additional amount invested.

1.6 Appointment of an intermediary/authorised

representative

An ‘authorised representative’ is any company, partnershipor individual appointed by you to invest in or withdrawmonies from V2 PLUS.

To appoint an intermediary, or authorised representative to transact on your V2 PLUS investment, the accountholder, together with the person authorised to operate theinvestment, will need to sign the relevant form dependingon whether you have direct banking facilities or not. Where the authorised representative is a corporation or a partnership, a duly authorised officer or partner ofthe authorised representative must sign the authority. ANZ Trustees may ask the representative for proof ofauthorisation.

Any person authorised to operate the investment mustcomplete, or must have completed, a 100-point checkwith ANZ.

You may at any time notify ANZ Trustees of your revocation of the appointment of an authorisedrepresentative. Such revocation, however, will not beeffective until the revocation has been acknowledged in writing by ANZ Trustees.

6

2. Account Operation 2.1 Withdrawing funds via the V2 PLUS Service Centre

When you make requests to the V2 PLUS Service Centre fora withdrawal, ANZ Trustees requests a payment (in part orwhole) by ANZ of a V2 PLUS certificate. Any amount thatANZ Trustees receives (to the extent that it is attributable tothe withdrawal) will be paid to you.

Telephone or Written Requests

You may withdraw funds for a self-titled cheque or third party cheque or transfer funds to any other bank accountby written request signed and hand delivered to a V2 PLUSshop front or mailed or faxed to the V2 PLUS Service Centre.

Where you have requested the telephone withdrawalfacility you may also withdraw funds by telephone via theV2 PLUS Service Centre for:

• a self titled cheque or transfer to a nominated account; and

• a third party cheque or transfer to any bank accountother than the nominated account (but only if you areauthorised to operate the V2 PLUS investmentindependently).

Please note that:

• if the nominated account is not with ANZ, the creditingmay take longer than 24 hours;

• payment of cheques issued can be stopped bynotifying the V2 PLUS Service Centre in writing prior tothe payments being made. A fee may be charged forthis service; and

• withdrawals will be paid net of all taxes, duties andcharges.

Minimum withdrawal amount

The minimum withdrawal amount for all withdrawals fromthe V2 PLUS Service Centre is $500.

Access to funds

The V2 PLUS Service Centre will take reasonable stepsto ensure that withdrawals are made within the specifiedtime, but accepts no responsibility for delays in transitwhich may occur and which are beyond its control. Anydeposits received from overseas in Australian dollars willtake up to 30 days before funds can be considered cleared.

Although funds can be transmitted on the same day, theymay not be visibly reflected in your bank account. In thissituation the bank officers will contact our V2 PLUS ServiceCentre for confirmation of the remitted funds.

Where a withdrawal request is received by the V2 PLUSService Centre before 11.00am EST for cheque withdrawalsor 1pm EST for nominated account transfers, on anybanking day, same day withdrawals can be made (allwithdrawals are subject to cleared funds being available).

Where a request for withdrawal is received after thesetimes or on a day on which the V2 PLUS Service Centre orANZ is closed for business, payment will be made on thenext banking day following the request. Your investmentwill continue to earn interest until the time the requestis actioned.

2.2 Withdrawing funds via direct banking facilities

For V2 PLUS with direct banking facilities, in addition to theability to withdraw funds via the V2 PLUS Service Centre,withdrawals may be made:

• at any ANZ branch or ATM; • via electronic debit, for example direct debit or

periodical payment; and • via ANZ Phone Banking, ANZ Internet Banking, BPAY®

and EFTPOS;

(subject to the terms and conditions that attach to thesefacilities).

Withdrawals (and balance enquiries) at non-ANZ ATMs mayattract a service fee from that financial institution. Thesefees will be itemised on your V2 PLUS statement. However,the use of non-ANZ ATMs for withdrawals from yourV2 PLUS account will not be counted as one of your freewithdrawal transactions each month.

Each withdrawal made with the direct banking facilitiesoption is made with the authority of ANZ Trustees andresults in a payment (in whole or in part) of a V2 PLUScertificate.

7

8

2.3 Operation of the account by an

intermediary/authorised representative

An authorised representative may have the same authorityas you have to make further investments in andwithdrawals from V2 PLUS.

2.4 Cheques

How long does it take to clear a cheque?

Usually five to seven working days, however you willgenerally be able to draw on the funds after three workingdays.

When you pay a cheque into your V2 PLUS account, ANZmay allow you to draw on the cheque before it has cleared.However, your account will be charged an honour fee fortransactions that are paid against uncleared funds.

What if the cheque is dishonoured?

ANZ will debit your account by the amount of the chequeand may also charge you a dishonour fee.

What happens to the original cheque once paid?

For cheques drawn on ANZ and paid prior to 1 December2005, ANZ will keep a copy of the cheque for seven yearsbut will destroy the original.

For cheques drawn on ANZ and paid on or after 1December 2005, ANZ will destroy the original cheque butkeep a copy of the cheque for:

• 13 months, if the cheque amounts to less than$200; or

• seven years, if the cheque amounts to $200 ormore.

Third Party Cheques

If you present a cheque which is payable to someone elseor it appears to belong to someone else (third partycheque), ANZ may, in its discretion, refuse to accept thatcheque for deposit or refuse to cash it or may require youto comply with some conditions before it will accept thatcheque for deposit or cash it.

Stopping a cheque

If you have lost a cheque you received from someone else,notify that person so they may stop the cheque.

9

When should a cheque be dishonoured or payment

refused?

At the bank’s discretion, a cheque may be dishonoured orpayment refused where:

• there are insufficient funds in the account of thedrawer;

• the cheque is unsigned;• the cheque is more than 15 months old;• the cheque is future dated;• the cheque has been materially altered and the

alteration has not been signed;• there is a legal impediment to payment;• the cheque has been stopped; or• the paying bank has been notified of the mental

incapacity, bankruptcy or death of the drawer. ANZ may charge a dishonour fee.

2.5 Bank cheques

Bank cheques are cheques instructing payment from thebank itself rather than from a customer’s account. They aredesigned to provide an alternative to carrying largeamounts of cash when a personal cheque is notacceptable. Bank cheques are usually requested becauseof the higher likelihood that they will be paid. Howeverbank cheques should not be regarded as equivalent tocash.

Bank cheques can be purchased by ANZ and non-ANZcustomers and a fee is charged. A bank may dishonour abank cheque if:

• the bank cheque is forged or counterfeit;• the bank cheque has been fraudulently and materially

altered;• a fraud or other crime has been committed;• the bank is told the bank cheque has been lost or

stolen;• there is a court order restraining the bank from paying a

bank cheque;• the bank has not received payment or value for the

issue of the bank cheque; or• if a bank cheque is presented by a person who is not

entitled to the cheque proceeds.

If a bank cheque is lost or stolen, ANZ will, on certainconditions, provide a replacement cheque for a fee.

10

2.6 Inactive accounts

If you do not operate your account for seven years and thereis $500 or more in your account, ANZ is required by law tosend your money to the Government as unclaimed money.

2.7 Disruption to service

When planning transactions, please allow sufficient time.You should bear in mind that occasionally a bankingservice may be disrupted. A ‘disruption’ is where a serviceis temporarily unavailable or where a system or equipmentfails to function in a normal or satisfactory manner.

ANZ or ANZ Trustees will correct any incorrect or unappliedentry which is made or not made to your account as aresult of a disruption and will adjust any fees or chargeswhich have been or have not been applied as a result ofthe incorrect or unapplied entry.

To the maximum extent permitted by law, neither ANZnor ANZ Trustees will be liable for any loss or damage,including consequential loss or damage and legal costs,suffered because of a disruption.

If you have opened a V2 PLUS investment as an individualfor personal use, this disclaimer of liability does not applyto electronic banking transactions (see section 7.‘Electronic Banking Conditions of Use’ for conditions whichapply to those transactions). This disclaimer is in additionto, and does not restrict, any other provision contained inthese terms and conditions which limits ANZ’s liability.

2.8 Maintaining your minimum balance

You need to maintain a minimum balance of $5,000 atall times. Where a withdrawal would reduce your balancebelow $5,000, ANZ Trustees may, at its discretion, requireyou to withdraw the whole balance. Withdrawal of thewhole balance can only be arranged by contacting the V2 PLUS Service Centre. Balances of less than $5,000 inyour V2 PLUS will not earn any interest.

If you have V2 PLUS with direct banking facilities and aremaking a withdrawal using EFTPOS, an ATM, ANZ PhoneBanking, ANZ Internet Banking or BPAY®, your transactionwill be rejected if it causes the balance in your accountto fall below the $5,000 minimum.

11

2.9 Interest rate

The interest rate paid on your V2 PLUS is determined byANZ having regard to prevailing money market interestrates. The interest rate may change from day to day. Thedaily interest rate is the annual rate divided by the numberof calendar days in a year.

Rates apply until a new rate is advertised. The currentinterest rate can be obtained by telephoning V2 PLUSRateline on FREECALL 1800 033 043, 24 hours a dayAustralia-wide or by visiting www.anz.com or anyANZ branch.

2.10 Interest payments

Interest is calculated daily and paid quarterly on the firstday of January, April, July and October. Interest on amountswithdrawn will be paid on the next interest payment dateexcept where you fully withdraw your investment theninterest will be paid at that time. You may elect to haveyour interest credited to a nominated bank account byadvising the V2 PLUS Service Centre in writing or re-invested in V2 PLUS. Unless otherwise directed, interestpayments will be reinvested into V2 PLUS.

If the account you nominate is a non-ANZ account, thecrediting may take longer than 24 hours.

2.11 Investor statements

You will receive a quarterly statement detailing interestpaid and your investment balance. This will be forwardedto you after each interest distribution. Monthly statementsare issued at the end of each month but only if awithdrawal or deposit has been made in the month. Themonthly statement will detail all transactions made duringthe month and your account balance. These statementsshould be retained for your individual tax purposes.

A statement detailing all transactions and interest paid fora specified period or an audit certificate, is available uponrequest. A fee may apply for this service.

You must carefully review your statements so you are awareof the status of your account. If you believe there are errorsor unauthorised transactions shown on your statement,you must contact the V2 PLUS Service Centre as soon aspossible.

12

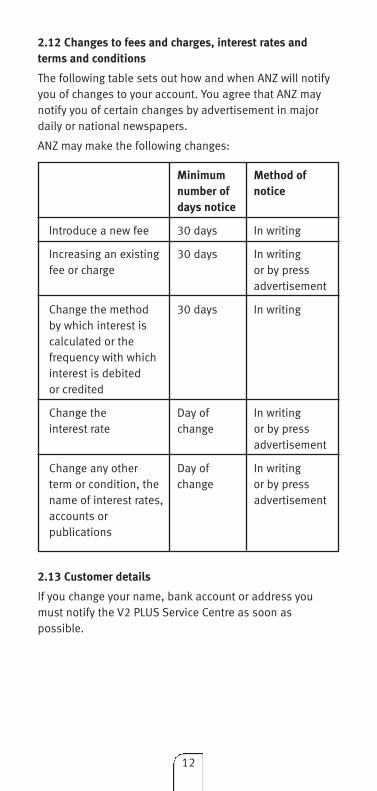

2.12 Changes to fees and charges, interest rates and

terms and conditions

The following table sets out how and when ANZ will notifyyou of changes to your account. You agree that ANZ maynotify you of certain changes by advertisement in majordaily or national newspapers.

ANZ may make the following changes:

2.13 Customer details

If you change your name, bank account or address youmust notify the V2 PLUS Service Centre as soon aspossible.

Minimum Method of

number of notice

days notice

Introduce a new fee 30 days In writing

Increasing an existing 30 days In writing fee or charge or by press

advertisement

Change the method 30 days In writingby which interest iscalculated or the frequency with which interest is debitedor credited

Change the Day of In writing interest rate change or by press

advertisement

Change any other Day of In writing term or condition, the change or by pressname of interest rates, advertisementaccounts or publications

13

2.14 Joint investments

Where your V2 PLUS investment is held jointly with one ormore investors, the following shall apply:

• ANZ Trustees can send statements to any of the jointinvestors and each one will be deemed to havereceived them;

• If any investor dies, ANZ Trustees will treat theinvestment as belonging to the survivors; and

• Each joint investor releases, discharges and agrees toindemnify each of ANZ and ANZ Trustees from andagainst any action, proceeding, claim or demand andany loss or damage suffered by any investor, ANZ orANZ Trustees and howsoever arising by reason of theoperation of the investment by any of you.

V2 PLUS without direct banking facilities

Funds can be withdrawn only in accordance with theinstructions given by you and other authorised operators.For example, if your joint account arrangement requires ‘allparties to sign jointly’, any request (such as the drawing ofa third party cheque) that requires written authority mustbe signed by all parties. If you elect to have the telephonewithdrawal facility, then any one of the parties to a jointinvestment can make telephone withdrawal requestsalone. The telephone withdrawal facility must, however, besuspended if any single party to a joint investment advisesthe V2 PLUS Service Centre that the telephone withdrawalfacility for the joint investment is not to be operated by oneperson alone.

V2 PLUS with direct banking facilities

Where an investment is made in the names of more thanone individual any of you will be entitled to operate theinvestment without the consent of the others (including theprovision of signed written instructions authorising acheque withdrawal). However, if as a party to a jointinvestment, you wish to suspend or terminate the authoritythat each joint investor has to operate the investment, youcan do so by notifying ANZ Trustees in writing. Thesuspension or termination will not be effective, however,until ANZ Trustees has acknowledged it in writing. In thesecircumstances your investment will cease to have directbanking facilities.

14

2.15 Third party signatories for V2 PLUS with direct

banking facilities

Any individual appointed as a third party signatory will beentitled to operate the investment without your consent andwill have the same powers as you to make additionalinvestments and withdrawals from your investment.

To authorise a third party signatory to use ANZ Phone Bankingand ANZ Internet Banking in connection with your investment,you will also need to complete a separate ANZ Phone Bankingand ANZ Internet Banking Authorised User Authority.

Third party signatories must complete a 100-point checkwith ANZ.

You will be able to revoke the appointment of a third partysignatory at any time by notifying ANZ Trustees in writing.The revocation will not be effective, however, until ANZTrustees has acknowledged it in writing.

2.16 Investment by companies

For V2 PLUS with direct banking facilities each director orsecretary who signs the application form will haveauthority to operate the account alone. For V2 PLUSwithout direct banking, authorised representatives may beappointed to operate the account jointly. If a companywants further third parties to operate the account thecompany will need to appoint them.

2.17 Investments by partnerships, trusts and

unincorporated associations

Where a partnership or an unincorporated associationwants more than one representative to operate theinvestment, the persons who are authorised to operate theinvestment, by the partnership or unincorporatedassociation, can apply as joint investors or some of themmay so apply and others may be appointed as third partysignatories or authorised representative.

Similarly, an individual trustee may appoint a third partysignatory or authorised representative. In the case of jointtrustees (individuals), they may apply as joint investors orsome of them may so apply and the others may beappointed as third party signatories or authorisedrepresentative.

15

2.18 Periodical Payments for V2 PLUS with direct banking

facilities.

A periodical payment is a debit from your V2 PLUS account,which you instruct ANZ Trustees to make to the account ofanother person or business. You will need to complete aperiodical payment request form with ANZ Trustees at anANZ Branch or call the V2 PLUS Service Centre to apply overthe phone. You can only apply for a Periodical Paymentover the phone if the periodical payment amount is lessthan $1000.

If your periodical payment falls on a non business day, yourpayment will be made on the next business day followingthe payment date, unless you request otherwise. If adeposit is made at another bank or financial institution,there may be a delay of several days before the account iscredited with your deposit.

A Non-Payment Fee is charged if you have authorised aPeriodical Payment that is not made because there areinsufficient cleared funds in your account.

2.19 Direct debiting for V2 PLUS with direct banking

facilities

You can arrange for a third party to direct debit from yourV2 PLUS account. By doing so, you can arrange paymentfor regular expenses such as health cover, insurancepremiums and credit card accounts. You will need tocomplete a direct debit authority form with the third partyand quote the V2 PLUS BSB and the investment accountnumber we give you. Direct debits cannot be arranged foryou by the V2 PLUS Service Centre.

A Dishonour Fee is charged if you authorise a third partyto direct debit your account and payment is not madebecause there are insufficient cleared funds in youraccount.

2.20 Stopping payments for periodical payments and

direct debits

You can:

• arrange for a periodical payment or direct debit to bestopped if you notify the V2 PLUS Service Centre inwriting at least 2 banking days before the paymentis made. A Stop Payment fee may be charged for thisservice;

16

• arrange for payment of a periodical payment or a directdebit to be altered if you notify the V2 PLUS ServiceCentre in writing at least two banking days before thepayment is made; and

• cancel a periodical payment request or a direct debitrequest by notifying the V2 PLUS Service Centre inwriting at least 2 banking days before the payment ismade.

Speed is important

You may notify the V2 PLUS Service Centre initially bytelephone. This may temporarily stop your periodicalpayment or direct debit until you call at your branch orsend written instructions.

ANZ may charge you a fee for canceling a direct debit orperiodical payment.

2.21 Closure

ANZ Trustees may choose at any time to repay a part or thewhole of your investment to you. Should this occur you willreceive the interest to which you are entitled at that time.

2.22 Indemnity

Each investor releases, discharges and indemnifies ANZTrustees and ANZ from and against all actions,proceedings, accounts, claims, demands, losses anddamages arising from or in any way relating to ANZTrustees or ANZ in good faith:

• acting on instructions received by mail or electronicmeans (whether by facsimile, telephone, internet,ATM or EFTPOS) which are, or are purported to be,given or signed by the investor, an authorisedrepresentative or an authorised third partysignatory or, in the case of joint investors, by any ofthem; and

• releasing information about the investor or theinvestment to any authorised representative orthird party signatory appointed by the investor.

2.23 Anti-Money laundering

You agree ANZ or ANZ Trustees may delay, block or refuseto make a payment if it believes on reasonable groundsthat making a payment may breach any law in Australia orany other country, and ANZ or ANZ Trustees will incur noliability to you if it does so.

17

You agree to provide all information to ANZ or ANZTrustees, which it reasonably requires to comply with anylaws in Australia or other country.

You agree ANZ or ANZ Trustees may disclose informationwhich you provide to it where required by any laws inAustralia or any other country.

Unless you have disclosed that you are acting in a trusteecapacity or on behalf of another party, you warrant that youare acting on your own behalf in entering into thisagreement.

You declare and undertake to ANZ and ANZ Trustees thatthe payment of monies in accordance with yourinstructions by ANZ or ANZ Trustees will not breach anylaws in Australia or any other country.

3. Fees and Charges3.1 Bank Fees and Charges

There are no entry or exit fees charged on V2 PLUS. ANZpays a fee to ANZ Trustees for administering V2 PLUS. Thefee has already been taken into account in setting theinterest rate.

If ANZ fails to collect a fee to which it is entitled, ANZ hasnot waived its right to collect the fee for future transactionsof the same nature.

Fees specific to V2 PLUS with direct banking facilities

For information about specific account fees and charges(including the types of transactions you can make, monthlywithdrawal quotas and specific fee amounts) please referto the ‘ANZ Personal Banking– Account Fees and Charges’.

General Fees and Charges

For further information on other general fees charged byANZ, please refer to the ‘ANZ Personal Banking – GeneralFees and Charges’ booklet. This booklet is available fromany ANZ branch or on-line at www.anz.com.

3.2 Government charges

Government charges may be levied on debiting andcrediting in respect of your investment. Any charges thatare levied are the liability of the investor and will bededucted quarterly from the investment or any interest.You can obtain exact details of any appliciable chargesfrom the V2 PLUS Service Centre.

18

4. Disclosures4.1 Personal advice

ANZ staff are eligible to receive an individual reward basedon their monthly sales performance. This reward will neverexceed $3,500 per month per staff member. In addition,ANZ branch staff are eligible to receive a reward if theirparticular branch reaches its profitability target. Thisreward will never exceed $12,000 per half year per staffmember.

Each month, ANZ staff may also be eligible to receive non-monetary benefits such as movie tickets, gift vouchersrecognition dinners and travel vouchers for meeting orexceeding promotion targets. The value of non-monetarybenefits received by eligible staff will not exceed $2,000per promotion per month.

4.2 Monitoring enquiries and transactions

ANZ Trustees may, at its discretion, monitor enquiries ormonitor or tape-record transactions made over thetelephone. This is done for transaction verification,security, quality control and training.

4.3 Privacy and confidentiality – ANZ and ANZ Trustees

collection, use and disclosure of personal information

When you deal with ANZ and ANZ Trustees, they are likelyto collect and use some of your personal information. Set out below are the instances in which ANZ and ANZTrustees may collect and use your personal information.

Collection of your personal information by ANZ and

ANZ Trustees

ANZ and ANZ Trustees may collect your personalinformation:

• to assist in providing information about a product orservice;

• to consider your request for a product or service;• to enable ANZ and ANZ Trustees to provide a product or

service;• to tell you about other products or services that may be

of interest to you;• to assist in arrangements with other organisations

(such as loyalty partners) in relation to the promotionand provision of a product or service;

19

• to perform other administrative and operational tasks(including risk management, systems development andtesting, credit scoring, staff training, and market orcustomer satisfaction research);

• to prevent or investigate any fraud or crime (or asuspected fraud or crime); and

• as required by relevant laws, regulations, Codes andexternal payment systems.

Absence of relevant personal information

If you do not provide some or all of the informationrequested, ANZ or ANZ Trustees may be unable to provideyou with a product or service.

Disclosures by ANZ and ANZ Trustees

Subject to our general duties of confidentiality towards ourcustomers, ANZ and ANZ Trustees may need to discloseyour personal information to:

• your referee(s);• credit reporting or debt collection agencies;• an organisation that is in an arrangement or alliance

with ANZ or ANZ Trustees for the purpose of promotingor using their respective products or services (and anyagents used by that organisation in administering suchan arrangement or alliance);

• any service provider ANZ or ANZ Trustees engage tocarry out or assist its functions and activities;

• regulatory bodies, government agencies, lawenforcement bodies and courts;

• other parties ANZ or ANZ Trustees are authorised orrequired by law to disclose information to;

• other financial institutions (such as banks);• any person who introduces you to ANZ or ANZ Trustees;• your authorised agents or your executor, administrator

or your legal representative.

Accessing your personal information held by ANZ or

ANZ Trustees

Subject to the provisions of the Privacy Act, you may accessyour personal information at any time by asking to do so atany ANZ branch. ANZ or ANZ Trustees may charge you areasonable fee for access. If you can show that informationabout you is not accurate, complete and up to date, ANZ orANZ Trustees must take reasonable steps to ensure it isaccurate, complete and up to date.

20

Collecting your sensitive information

ANZ or ANZ Trustees will not collect sensitive informationabout you, such as health information, without yourconsent.

Where you supply an ANZ or ANZ Trustees member with

personal information about someone else

If you give ANZ or ANZ Trustees personal information aboutsomeone else, please show them a copy of this clause sothat they may understand the manner in which theirpersonal information may be used or disclosed by ANZ orANZ Trustees in connection with your dealings with ANZand ANZ Trustees.

4.4 Tax File Number (TFN)

It is not compulsory for you to provide your TFN. However, if you choose not to do so, ANZ Trustees is required todeduct withholding tax from any interest earned unless youare in an exempt category. Withholding tax is calculated atthe highest marginal tax rate plus Medicare Levy. ANZ arerequired to preserve the confidentiality of your TFN, whichcan be recorded for all your accounts, in accordance withthe Privacy Act. Investors who are not Australian residentsfor tax purposes will have a withholding tax deducted fromtheir interest entitlement. You should obtain your owntaxation advice specific to your individual needs.

4.5 Code of Banking Practice

If you are an individual or a small business (as defined inthe Code of Banking Practice) ANZ is bound by the Code ofBanking Practice when it provides its products and servicesto you.

5. Enquiries and ComplaintresolutionFor the fastest possible resolution to your complaint:• Call the V2 PLUS Service Centre on 13 28 33 or fax

1800 671 800; or• Talk to staff at your local ANZ branch or business

centre; or• Send a letter to ANZ Customer Response Centre via

> Mail: Locked Bag 4050, South Melbourne VIC 3205

> Email: [email protected]> Fax: +61 3 9683 9267

21

Most often the problem will be able to be solved on the spot.If it cannot be resolved promptly a specialist complaintsteam, ANZ Customer Response Centre, will take responsibilityand work with you to fix the matter quickly. ANZ’s aim is toresolve the complaint within 10 working days.

If this is not possible, ANZ will keep you informed on theprogress of your matter and how long it expects it will taketo resolve your complaint.

ANZ Customer Advocate

If your complaint is not resolved to your satisfaction, youcan ask to have it reviewed by ANZ’s Customer Advocatewho will provide a free review of more difficult complaintsto help achieve a prompt solution.

Contact details:ANZ Customer Advocate100 Queen StreetMelbourne VIC 3000Tel: +61 3 9273 6523Email: [email protected]

Financial Services Dispute Resolution Schemes

If you are not satisfied with the steps taken by ANZ toresolve the complaint, or with the result of ourinvestigation, you may wish to contact an alternativedispute resolution scheme.

Banking and Financial Services Ombudsman LimitedGPO Box 3AMelbourne VIC 3001Telephone: 1300 780 808Fax: +61 3 9613 7345Internet: http://www.abio.org.au/

6. Electronic BankingThis section applies to V2 PLUS with direct bankingfacilities only. Please also refer to the ‘Electronic BankingConditions of Use’ in section 7 if you conduct electronictransactions on your account.

6.1 EFTPOS

EFTPOS is Electronic Funds Transfer at Point of Sale. Thisretail facility allows you to debit the cost of your purchaseto your V2 PLUS account where this is linked as the primeaccount. Depending on the retailer, you may also be ableto withdraw cash.

22

6.2 MAESTRO and CIRRUS

MAESTRO and CIRRUS are international EFTPOS and ATMnetworks, which enable you to access available funds inyour V2 PLUS account by using your linked ANZ debit cardor linked ANZ MasterCard whilst overseas.

6.3 Fees and charges, MAESTRO and CIRRUS

Transaction fees and currency conversion fees apply for theuse of CIRRUS ATMs and MAESTRO EFTPOS overseas. If theamount of the transaction would reduce your accountbalance to an amount less than $5000, the transactionmay be rejected and no fees will be charged. At overseasCIRRUS ATMs, you cannot use your ANZ debit card or ANZMasterCard card to make deposits or transfer fundsbetween linked accounts.

6.4 Surcharging, MAESTRO and CIRRUS

Some overseas ATM locations may impose a surchargewhen you use their ATM to effect a withdrawal. Surchargeswill not appear as a separate item on the accountstatement, but will be included in the total transactionamount shown.

6.5 Exchange rates and conversion, MAESTRO and CIRRUS

All transactions will be processed through MasterCardInternational Incorporated using conversion rates set inaccordance with its rules.

• Transactions in United States Dollars will be convertedinto Australian Dollars as at the date they areprocessed by ANZ in Australia.

• Transactions in other currencies will be converted intoUnited States Dollars as at the date they are processedin the United States by MasterCard InternationalIncorporated, and then further converted to AustralianDollars on the same date.

In most cases, the conversion rate applied to refunds of atransaction will be different to the conversion rate appliedto the original transaction.

6.6 Daily withdrawal limit

Unless you have made arrangements with your branch foran increased or decreased limit, your combined ATM,EFTPOS, MAESTRO and CIRRUS daily withdrawal limit isAUD$1,000 per ANZ Card. This means you can use your

23

ANZ Card to withdraw a total of AUD$1,000 per day fromthe account(s) to which it is linked, provided youraccount(s) contain sufficient funds. In the event of asystem failure, the daily withdrawal limit is AUD$200.

6.7 PLUS

PLUS is an international ATM network through which youcan access funds in your linked V2 PLUS account by usingyour ANZ Visa card and PIN while overseas. If you have notpreviously agreed in writing to accept these terms andconditions, first use of your ANZ Visa card overseas at aPLUS ATM will automatically constitute your agreement tothese terms and conditions.

At overseas PLUS ATMs, you cannot use your ANZ Visa cardto make deposits or transfer funds between linkedaccounts. When you use your ANZ Visa card to access alinked ANZ account, you can usually access funds fromeither your linked primary savings or cheque account*.

However, some overseas ATMs do not offer this choice:

• If you have a linked primary savings and primarycheque account, when you press 'debit' the ATM willautomatically select your primary savings account.

• Some ATMs have no account selection facility at all.In this case, the ATM will automatically select a cashadvance from your ANZ Visa credit card account if youproceed with the transaction.

* Linked primary accounts refer to ANZ accounts you have nominated as

your primary savings or cheque account linked to your credit card

6.8 Fees and charges, PLUS

Transaction fees and currency conversion fees apply for theuse of PLUS ATMs overseas. If the amount of thetransaction would reduce your account balance to anamount less than $5000, the transaction may be rejectedand no fees will be charged.

6.9 Surcharging, PLUS

Some overseas ATM locations may impose a surchargewhen you use their ATM to make a withdrawal. Surchargeswill not appear as a separate item on the accountstatement, but will be included in the total transactionamount shown.

24

6.10 Exchange rates and conversions, PLUS

All transactions will be converted into Australian Dollars byVisa International in accordance with its rules. Transactionswill either be converted directly to Australian dollars or will befirst converted from the currency in which the transaction wasmade to US dollars and then converted to Australian dollars.

The conversion rate used is a wholesale market rateselected by Visa International from a range of wholesalerates one day before Visa processes the transaction. Inmost cases, the conversion rate applied to refunds of atransaction will be different to the conversion rate appliedto the original transaction.

6.11 Lost and stolen Card and PIN within Australia

If your card to which your V2 PLUS account is linked or PIN islost or stolen, or if your PIN has become known to someoneelse, you must notify ANZ as soon as possible. The best wayto minimise your liability is to contact ANZ by telephone. Theemergency telephone numbers are listed at the end of thisPDS. An ANZ ATM debit card replacement fee applies forreplacement of a card except if damaged (and returned toANZ) or stolen and a copy of a police report is provided.

6.12 Lost and stolen Card and PIN while overseas

If your card to which your V2 PLUS account is linked or PINis lost or stolen, or if your PIN has become known tosomeone else, you must notify ANZ as soon as possible.

The best way to minimise your liability is to contact ANZ bytelephone. The emergency telephone numbers are listed atthe end of this PDS.

• ANZ linked debit CardANZ cannot issue you with an emergency replacement cardand PIN until you return to Australia. An ANZ linked debitcard replacement fee applies for replacement of a cardexcept if damaged (and the card is returned to ANZ) orstolen and a copy of a police report is provided.

• ANZ MasterCard or ANZ Visa CardANZ can provide an emergency replacement card. However,you will not be able to use it in EFTPOS or ATM facilitiesuntil you have selected a new PIN for the card after youhave returned to Australia. You will still be able to makepurchases and obtain cash advances on your ANZ CreditCard account over the counter at institutions displaying theMasterCard or Visa logos/symbols.

25

7 Electronic Banking Conditionsof Use ANZ warrants that it will comply with the requirements ofthe Electronic Funds Transfer Code of Conduct. This sectionapplies to all electronic transactions except those whereyour signature may also be required.

Definitions

‘ANZ Business Day’ means any day from Monday to Fridayon which ANZ is open for business in at least one of itsbranch locations in Australia.

‘Banking Business Day’ refers to any day on which banksin Melbourne or Sydney are able to effect settlementthrough the Reserve Bank of Australia.

‘CRN’ means the Customer Registration Number issued byANZ to you.

‘PIN’ means Personal Identification Number and includesan action number.

‘Pay Anyone Processing Day’ means any day from Mondayto Friday that is not a public holiday in both Sydney andMelbourne.

‘Securemail’ means the electronic messaging system whichenables communications to be sent to or from ANZ as partof ANZ Internet Banking.

‘Telecode’ means the 4-7 digit number issued to accessANZ Phone Banking.

Transaction limits

ANZ or another party such as a merchant may limit theamount of any electronic transaction you can make overcertain periods (e.g. during any day or in a singletransaction).

ANZ may change any electronic transaction limit or imposenew transaction limits by giving you notice. You can findout current electronic transaction limits for your accountsby calling ANZ on the relevant enquiries number listed atthe back of this booklet.

How you can use ANZ Internet Banking

You can use ANZ Internet Banking to make transactions onyour linked accounts, as set out in your account terms andconditions. You can also use ANZ Internet Banking to

26

purchase and order a range of financial services andproducts. Details can be found at www.anz.com.

ANZ does not authorise, promote or endorse the use ofaccount access services offered by third parties to accessyour ANZ accounts (including account aggregation services,such as may be provided by other financial institutions).

Access to and Use of Pay Anyone and International

Services

(A) Obtaining Pay Anyone

When applying for Pay Anyone, you must request a PayAnyone daily limit which is subject to approval by ANZ. Theoptions for the daily limits are set out www.anz.com whenyou apply. Restrictions apply depending on whether youare using Pay Anyone for personal or business purposes.

If you require your password for Pay Anyone to be re-set orre-issued ANZ may reduce your current daily Pay Anyonelimit. You will need to re-apply if you wish to reinstate thatlimit.

Please allow sufficient time for the change to be madebefore you attempt to use the higher daily transfer limit.You can increase or decrease your daily transfer limit byapplying through ANZ Internet Banking.

(B) Obtaining International Services

You can apply for International Services after you havebeen granted Pay Anyone access. The total of all PayAnyone and International Services transfers (converted intoAustralian dollars) on any day cannot exceed your PayAnyone daily transaction limit.

Access Levels For ANZ Phone Banking and ANZ Internet

Banking

Access Levels:

• ‘All transactions’ – Access every function within ANZPhone Banking and ANZ Internet Banking for theaccount;

• ‘Transaction History Details only and BPAY® – includes

BPAY®, account balance information, transaction historydetails, ordering a cheque/deposit book but excludestransfers between accounts, increasing a credit cardlimit, redrawing on a home loan, direct loan paymentsand BPAY® View;

27

• ‘Deposit and Transaction History Details only’ –

includes transfers between accounts, transactionshistory details, account balance information andordering a cheque/deposit book but excludeswithdrawals from accounts, increasing credit card limit,redrawing on a home loan, direct loan payments, BPAY®

View and BPAY®;• ‘Deposit only’ – includes transfers between accounts

but excludes withdrawals from accounts, BPAY®,increasing credit card limit, redrawing on a home loan,direct loan payments, BPAY® View, account balanceinformation, transaction history details and ordering acheque/deposit book;

• ‘Transaction History Details only’ – includes enquirieson past transactions about the account but excludes alltransactions on the account, transfers betweenaccounts, increasing credit card limit, redrawing on ahome loan, direct loan payments, BPAY® View and BPAY®.

Only the account holder or account signatories can selectan access level. The account holder or account signatoriesmay authorise another person (an ‘authorised user’) tooperate the account and that person may have a differentaccess level to the account holder. The account holder isresponsible for the operation of the account by theauthorised user within that user’s level of access.

The account holder or account signatories may cancel orchange any access level by sending a written request orSecuremail to ANZ, or calling ANZ on the relevant numberlisted at the back of this booklet. ANZ may require writtenconfirmation. ANZ may take several days to process thischange.

Authorised users, regardless of their level of access,cannot access ANZ Pay Anyone, ANZ International Services,increase a credit card limit, redraw on a home loan, or useSecuremail to change any of the account holder’s accountor other personal details. However, all authorised userscan use ANZ Internet Banking to change their own profile,access their own Securemail and select and change theirown password.

If you are an ANZ credit card account holder and nominateaccess to this account via ANZ Internet Banking, eachadditional cardholder will be an authorised user.

28

Processing instructions – general

The account holder authorises ANZ to act on theinstructions you enter into electronic equipment. Anyelectronic transaction made by you cannot be cancelled,altered or changed by you unless allowed by the applicableterms and conditions.

ANZ may delay acting on or may ask you for furtherinformation before acting on an instruction. Where ANZ hasinstructions for more than one payment from youraccount(s), ANZ will determine the order of priority in whichpayments are made.

If you make a cash withdrawal from an account by makingan electronic transaction and there is a difference betweenthe amount of cash received and the amount shown on thereceipt, you must report this to ANZ and to the merchant (ifapplicable) as soon as possible. You can make your reportto ANZ by calling ANZ on the number listed at the back ofthis booklet.

If you make a deposit of funds to an account by making anelectronic transaction and there is a difference betweenthe amount recorded as having been deposited and theamount ANZ receives, the account holder will be notified ofthe difference as soon as possible and will be advised ofthe actual amount which has been credited to the account.

ANZ is not liable for the refusal of any merchant to acceptan electronic transaction and, to the extent permitted bylaw, is not responsible for the goods and services suppliedby a merchant.

You accept that:

• not all electronic equipment from which cash can bewithdrawn will always contain cash;

• any cash dispensed at electronic equipment is at yourrisk once it becomes visible or available for you tocollect; and

• not all electronic equipment will allow you to makedeposits.

An immediate transfer, Pay Anyone or BPAY®‚ cannot berevoked or stopped once ANZ receives your instruction.Future dated transfers, Pay Anyone or BPAY®‚ instructionscan only be revoked or changed if instructions to delete thetransaction are given to ANZ through ANZ Internet Bankingbefore midnight Sydney time on the ANZ Business Day (or,

29

for Pay Anyone, the Pay Anyone Processing Day) before thetransaction is scheduled to occur. After this time, theinstruction cannot be revoked.

Processing Instructions – ANZ Phone Banking and ANZ

Internet Banking

Any ANZ Phone Banking or ANZ Internet Bankingtransaction (other than a BPAY®) will generally be processedto your account on the same day ANZ receives yourinstructions, if given before 10.00pm Melbourne timeMonday to Friday (except national public holidays). Anytransaction made after this time may be processed on thefollowing ANZ Business Day.

Account information accessed using ANZ Phone Banking orANZ Internet Banking will generally reflect the position ofthe account at that time, except for transactions not yetprocessed by ANZ (including uncleared cheques andunprocessed credit card transactions) or cleared chequesand direct debits processed by ANZ that day.

Processing Instructions - ANZ ATMs

Generally, any transaction on your account via an ANZ ATMwill be processed to your account on the same day if it isconducted before 4pm on an ANZ Business Day. Anytransaction conducted after this time or on a non ANZBusiness Day may be processed the next ANZ BusinessDay. Cash deposits made at ANZ ATMs may take one to twoANZ Business Days to clear. Cheque deposits at ANZ ATMsmay take five to seven ANZ Business Days to clear.

Processing Instructions – Pay Anyone and International

Services

ANZ will generally process Pay Anyone instructions:

• for immediate Pay Anyone transfers, on the day theinstruction is given, if ANZ receives the instructionbefore 6.00pm Melbourne time on a Pay AnyoneProcessing Day;

• for immediate international transfers, on the day theinstruction is given, if ANZ receives the instructionbefore 6.00pm Melbourne time on a Pay AnyoneProcessing Day;

• for future dated transfers, on the relevant future dayyou select if it is a Pay Anyone Processing Day (or if it isnot, on the Pay Anyone Processing Day after that day).

30

Instructions you give will be delivered to the payee’sfinancial institution on the day that ANZ processes themexcept where:

• ANZ is not obliged to process your instructions;• there is a technical failure; or• there is a delay or error in accepting the instructions

caused by the financial institution to which the transferis to be made; or

• the instructions are for a transfer by way of aninternational draft or telegraphic draft.

• Where your instruction is for a transfer by way of ANZissuing an international draft:

• ANZ will send the draft by post to the delivery addressnotified by you;

• You acknowledge that it is your responsibility toforward the draft to the intended recipient.

ANZ cannot control (and is not responsible for) when, or if,the payee’s financial institution processes yourinstructions or the fees that financial institutions maycharge to process your instructions.

Once ANZ processes your transfer instruction, ANZ is relianton the payee’s financial institution to advise whether yourinstructions have been successfully processed. If thepayee’s financial institution advises that your transferinstruction has not been successful, it may take a numberof weeks, depending on the financial institution, to reversethe relevant withdrawal from your linked account.

If the transfer is to be made from a credit card, it will betreated as a cash advance and interest and fees may apply.

Processing Instructions – BPAY®

ANZ is a member of the BPAY® Scheme. This is an electronicpayments scheme through which ANZ can be asked tomake payments on your behalf to billers. ANZ will tell you ifit ceases to be a member of the BPAY® Scheme. For thepurposes of the BPAY® Scheme, ANZ may also be a biller.

You must comply with the terms and conditions for theaccount which you ask ANZ to debit a BPAY® (to the extentthat those terms are not inconsistent with or expresslyoverridden by these Conditions of Use).

To make a BPAY® the following information must be given to ANZ:

31

• your CRN and password or Telecode;• the biller code from the bill;• your customer reference number (e.g. your account

number) with that biller;• the amount you want to pay; and• the account from which you want the payment to be

made.

Once this information is provided, ANZ will treat yourinstructions as valid and will debit the relevant account.ANZ will not be obliged to effect a BPAY® instruction if it isnot made in accordance with these Conditions of Use or ifthe information given is incomplete and/or inaccurate.

Limits apply to your use of BPAY® on both a per transactionand daily limit (per CRN) basis. Separate daily limits applyfor BPAY® Tax Payments, independent of the general BPAY®

limits. For more information on available limits seewww.anz.com.

Subject to the ‘Processing Instructions’ conditions set outabove:

• any BPAY® made by you will be processed on the dayyou tell ANZ to make that BPAY® if ANZ receives yourinstructions before 6pm Sydney time on a BankingBusiness Day (ANZ’s cut-off time);

• BPAY® instructions received after 6pm Sydney time on aBanking Business Day, or on a day that is not a BankingBusiness Day, will be processed on the next BankingBusiness Day.

A delay may occur in processing a BPAY® where:

• there is a public or bank holiday on the day after youtell ANZ to make a BPAY®;

• you tell ANZ to make a BPAY® after ANZ’s cut-off time; or• another participant in the BPAY® Scheme, such as

another financial institution or a biller does not processa payment as soon as it receives details of the paymentor does not otherwise comply with its obligations underthe BPAY® Scheme.

While it is expected that any such delay will not continuefor more than one Banking Business Day, it may continuefor a longer period.

ANZ will attempt to ensure a BPAY® is processed promptlyby billers and other participants in the BPAY® Scheme.

32

You should check your account records carefully and tellANZ as soon as possible if you become aware of:

• a BPAY® which has been made from your linked accountwhich was not authorised;

• the possibility that you have been fraudulently inducedto make a BPAY®; or

• any delay or mistake in processing of your BPAY®.

If ANZ is advised by a biller that it cannot process yourBPAY®, ANZ will:

• advise you of this;• credit your account with the amount of that BPAY®; and • tell you how ANZ can assist you, if possible, in making

the payment as soon as possible.

A linked ANZ credit card account can only be used to makea BPAY® if the biller accepts credit card payments. If thebiller does not accept credit card payments but you want topay from a credit card account, payment will be by way of acash advance.

You are not authorised to give a biller code to any personin order to receive payments owing to you. Biller codes mayonly be used by authorised billers to receive payment ofbills issued by that biller. The terms and conditions of useof BPAY® will not apply to any use by you of biller codes inthis way.

Card Validity

Your card remains ANZ’s property at all times.

A card must be signed immediately by the person in whosename it has been issued and must only be used within the‘valid from’ and ‘until end’ dates shown on the card. Forsecurity reasons you must, as soon as the card expires,destroy it by cutting it (including an embedded microchipon the card) diagonally in half.

Lost or Stolen Cards, Password, Pin or Telecode

If you report that a card has been lost or stolen the card willbe cancelled as soon as the report is made. You must not usethe card once the report is made. If you recover the lost orstolen card, you must destroy the card by cutting it (includingan embedded microchip on the card) diagonally in half andreturning it to an ANZ branch as soon as possible.

You must make a report to ANZ (and the relevant thirdparty, if a third party issued the username, password,

33

PIN or card to you) immediately after you become aware or suspect that your password, username, PIN, CRN orTelecode is disclosed or used without your authority, orlost. You must not then continue to use your password,username, PIN, CRN or Telecode. ANZ will cancel it andarrange for you to select a new username, password, PIN or Telecode, or to be provided with a new CRN.

The best way to make the report is to call ANZ on thetelephone numbers listed on the back of this booklet. If ANZ’s telephone reporting service is unavailable, youmust report the loss, theft or misuse to any ANZ branch.Your account terms and conditions outline how you canmake a report if ANZ’s telephone reporting service isunavailable or you are overseas.

Cancellation of Cards or Electronic Access

ANZ may cancel any card, CRN or electronic access

• without prior notice if:> ANZ believes that use of the card or electronic

access may cause loss to the account holder or to ANZ;

> the account is an inactive account;> all the accounts which the card may access have

been closed; or> the account has been overdrawn, or you have

exceeded your agreed credit limit; or• on giving you no less than three months written notice.

ANZ may also at any time suspend your right to participatein the ANZ BPAY® Scheme.

The account holder may cancel a card at any time bysending ANZ a written request or by calling ANZ on therelevant number listed on back of this booklet. ANZ mayrequire written confirmation. The card must be cutdiagonally in half (including an embedded microchip on the card) and returned to ANZ.

You can request ANZ to de-register you from ANZ InternetBanking at any time by Securemail or by calling therelevant number listed at the back of this booklet.

Withdrawal of Electronic Access

ANZ may withdraw your electronic access to accounts(including by BPAY®) without prior notice if:

• electronic equipment malfunctions or is otherwiseunavailable for use;

34

• a merchant refuses to accept your card;• any one of the accounts is overdrawn or will become

overdrawn, or is otherwise considered out of order byANZ;

• ANZ believes your access to accounts throughelectronic equipment may cause loss to the accountholder or to ANZ;

• ANZ believes that the quality or security of yourelectronic access process or ANZ’s systems may havebeen compromised;

• all the accounts which you may access using ANZPhone Banking or ANZ Internet Banking have beenclosed or are inactive; or

• ANZ suspects you of being fraudulent or engaging in inappropriate behaviour;

unless this is prohibited by law.

ANZ may at any time change the types of accounts that maybe operated, or the types of electronic transactions thatmay be made through particular electronic equipment.

Password, Pin and Telecode Security

You must keep your password, PIN and Telecode secure.Failure to do so may increase your liability for any loss.Warning: You must not use your birth date or analphabetical code which is a recognisable part of your nameas a password, or select a Telecode which has sequentialnumbers, for example, ‘12345’ or where all numbers are thesame, for example, ‘11111’. If you do, you may be liable forany loss suffered from an unauthorised transaction.

You must not:

• disclose your password, PIN or Telecode to any otherperson;

• allow any other person to see you entering, or overhearyou providing, your password, PIN or Telecode;

• record your password, PIN or Telecode on your card oron any article carried with or placed near your card thatis liable to loss, theft or abuse at the same time as yourcard (unless your password, PIN or Telecode isreasonably disguised).

Warning: You should avoid accessing ANZ Phone Bankingthrough telephone services which record numbers dialed –for example hotels which do this for billing purposes. Inthese situations you should obtain access to ANZ PhoneBanking through an ANZ customer service operator.

35

To assist you, ANZ publishes security guidelines. A copy ofthe current guidelines is available at www.anz.com.

Unauthorised Transactions

(a) When ANZ is liable

ANZ will be liable for losses incurred by the account holderthat:

• are caused by the fraudulent or negligent conduct ofANZ’s employees or agents or companies involved innetworking arrangements or of merchants or theiragents or employees;

• relate to any forged, faulty, expired or cancelled part ofthe electronic access process;

• arise from transactions that require the use of any card,password, PIN or Telecode that occur before you havereceived or selected the card, password, PIN orTelecode (including a reissued card, password, PIN orTelecode);

• result from the same electronic transaction beingincorrectly debited a second or more subsequent timeto the same account;

• result from an unauthorised transaction that occursafter you have notified ANZ that any card has beenmisused, lost or stolen or that the security of yourpassword, PIN or Telecode has been breached; or

• result from an unauthorised transaction if it is clear thatyou have not contributed to the losses.

(b) When the account holder is liable

If ANZ can prove on the balance of probability that youcontributed to the loss arising from the unauthorisedtransaction:

• through your fraud;• by voluntarily disclosing a password, PIN or Telecode to

anyone, including a family member or friend;• by keeping a record of the password, PIN or Telecode

(without making any reasonable attempt to disguise it):(i) on the card or with the CRN;(ii) on any article carried with the card or the CRN; or(iii) which may be lost or stolen at the same time as the

card or CRN.• by using your birth date or an alphabetic code which is

a recognisable part of your name as a password, PIN orTelecode; or

36

• by otherwise acting with extreme carelessness in failing to protect the security of your password, PIN or Telecode;

the account holder is liable for the actual losses whichoccur before ANZ is notified of the loss or disclosure of yourpassword, PIN or Telecode.

Where you must use more than one of your passwords, PINs or Telecodes to perform an ANZ Internet Bankingtransaction, and you voluntarily disclose, or keep a recordof, one or more of them (but not all of them) the accountholder will only be liable under this clause if the disclosureor record was the dominant contributing cause of thelosses.

If, after you become aware of the loss, theft or breach of thesecurity of your password, PIN, Telecode or card, youunreasonably delay notifying ANZ, the account holder willbe liable for losses incurred between:

• the time you first became aware of any of the eventsdescribed above, or in the case of loss or theft of a card,should reasonably have become aware of the loss ortheft; and

• the time ANZ is actually notified of the relevant event.

However, you are not liable for any loss:

• which, over a set period of time, is greater than thetransaction limit for that period;

• caused by overdrawing your account or exceeding anyagreed credit limit;

• where ANZ has agreed the account could not beaccessed electronically; or

• as a result of conduct that ANZ expressly authorised you to engage in, or losses incurred as a result of youdisclosing, recording or storing a password, PIN orTelecode in a way that is required or recommended byANZ for the purposes of you using an account accessservice expressly or impliedly promoted, endorsed orauthorised by ANZ.

If it is not clear whether you have contributed to the losscaused by an unauthorised transaction and where apassword, PIN or Telecode was required to perform theunauthorised transaction, the account holder is liable forthe least of:• $150 (unless the account is used for business

purposes); or

37

• the actual loss at the time ANZ is notified of the loss,theft or unauthorised use of the card or that thesecurity of the password, PIN or Telecode has beenbreached (but not any loss incurred on any one day ifthe amount is greater than the daily transaction limit orother periodic transaction limit if any); or

• the balance of the account, including any pre-arrangedcredit from which value was transferred in theunauthorised transaction.

Equipment Malfunction

ANZ is responsible to the account holder for any losscaused by the failure of equipment to complete atransaction that was accepted in accordance with yourinstructions.

However, if you were aware or should have been aware thatthe equipment was unavailable for use or malfunctioning,ANZ’s responsibility will be limited to correcting errors inthe account and refunding any charges or fees imposed asa result.

You are solely responsible for your own PC anti-virus andsecurity measures, and those of any authorised user, tohelp prevent unauthorised access via ANZ Internet Bankingto your transactions and linked accounts.

Liability Under The BPAY® Scheme

(A) General

You should note that:

• if you advise ANZ that a BPAY® made from a linkedaccount is unauthorised, you should first give ANZ yourwritten consent to obtain from the biller informationabout your linked account with that biller or the BPAY®

payment, (including your CRN) as ANZ reasonablyrequires to investigate the BPAY®. This should beaddressed to the biller who received the BPAY®. If youdo not do this, the biller may not be permitted by law todisclose to ANZ the information ANZ needs toinvestigate or rectify that BPAY® payment;

• If you discover that the amount you instructed ANZ topay was less than the amount you needed to pay, youcan make another BPAY® for the shortfall. If for anyreason you cannot make a BPAY® for the shortfall, youcan ask ANZ to arrange for a reversal of the initialpayment and you can make a second payment for the

38

correct amount. If you discover that the amount youinstructed ANZ to pay was more than the amount youneeded to pay, you can ask ANZ to request a reversal ofthe initial payment from the biller on your behalf, and ifthis occurs, you can make a second payment for thecorrect amount.

(B) ANZ’s Liability

Where you use your account for personal purposes, ANZ’sliability under the BPAY® Scheme is as set out under‘Unauthorised Transactions’.

Where you use your account for business purposes, ANZwill not be liable to you under the BPAY® Scheme except inthe circumstances set out in this clause.

Unauthorised Payments

If a BPAY® is made in accordance with a payment direction,which appeared to ANZ to be from you or on your behalf,but which you did not in fact authorise, ANZ will credit youraccount with the amount of that unauthorised payment.However, you must pay ANZ the amount of that payment if:

(i) ANZ cannot recover the amount from the person whoreceived it within 20 Banking Business Days of ANZattempting to do so; and

(ii) the payment was made as a result of a paymentdirection which did not comply with ANZ’s prescribedsecurity procedures.

Fraudulent Payments

If a BPAY® is induced by the fraud of a person involved inthe BPAY® Scheme, then that person should refund you theamount of the fraud-induced payment. However, if thatperson does not refund you that amount, you must bearthe loss unless some other person involved in the BPAY®

Scheme knew of the fraud or would have detected it withreasonable diligence, in which case that person mustrefund you the amount of the fraud-induced payment.

Mistaken Payments

If you discover that a BPAY® has been made to a person, orfor an amount, which is not in accordance with yourinstructions (if any), and your account was debited for theamount of that payment, ANZ will credit that amount toyour account. However, if you were responsible for amistake resulting in that payment and ANZ cannot recoverthe amount of that payment from the person who received

39

it within 20 Banking Business Days of ANZ attempting todo so, you must pay that amount to ANZ.

You acknowledge that the receipt by a biller of a mistakenor erroneous payment does not or will not, under anycircumstances, constitute part or whole satisfaction of anyunderlying debt owed between you and that biller.

(C) Consequential Loss

ANZ is not liable for any consequential loss or damage yousuffer as a result of using the BPAY® Scheme, other thandue to any loss or damage you suffer due to ANZ’snegligence or in relation to any breach of a condition orwarranty implied by law in contracts for the supply ofgoods and services and which may not be excluded,restricted or modified at all or only to a limited extent.

(D) Indemnity

To the extent permitted by law, you indemnify ANZ againstany loss or damage ANZ may suffer due to any claim,demand or action of any kind brought against ANZ arisingdirectly or indirectly because you:

(i) did not observe your obligations under; or(ii) acted negligently or fraudulently in connection with

these Conditions of Use.

Changes to the Electronic Banking Conditions of Use

ANZ can change the Electronic Banking Conditions of Useat any time. ANZ will give you 20 Banking Business daysprior written notice of any changes which:

• impose or increase charges relating solely to the use ofelectronic equipment;

• increase your liability for losses relating to electronictransactions; or

• change your daily transaction limit or other periodicaltransaction limit applying to the use of electronicequipment.

40

This page has been left blank intentionally

Contact detailsV2 PLUS Service Centre

V2 PLUSLocked Bag 3000Collins Street WestMelbourne VIC 8007Ph: 13 28 33Fax: 1800 671 800TTY : 1300 366 255

International customers

Ph: +61 3 8699 6994Fax: +61 3 9277 1315

V2 PLUS rate line

Ph: 1800 033 043

V2 PLUS Shop-fronts

Ground Floor, 20 Martin PlaceSydney NSW 2000;21/530 Collins StreetMelbourne VIC 3000

ANZ Personal Banking

Contact your nearest ANZ branch or phone 13 13 14.

ANZ Internet Banking

Including lost, stolen or divulged passwordsPh: 13 33 50Ph: + 61 3 9683 8833 (International customers)

Lost or stolen cards, suspected unauthorised transactions

or divulged passwords

1800 033 844; orPh: +61 3 9683 7047 (International Customers)(24 hours a day).

Au

str

ali

a a

nd

Ne

w Z

ea

lan

d B

an

kin

g G

rou

p L

imit

ed

AB

N 1

1 0

05

35

7 5

22

. I

tem

No

. 8

00

88

1

1.2

00

5

W8

06

99