apimec 2012 eng

TRANSCRIPT

APIMEC 2012 December 14th 2012

2

The material that follows is a confidential presentation of general background information about Magnesita Refratários S.A. and its consolidated subsidiaries

(“Magnesita" or the "Company") as of the date of the presentation. It is information in summary form and does not purport to be complete and is not intended to

be relied upon as advice to potential investors.

No representations or warranties, express or implied, are made as to, and no reliance should be placed on, the accuracy, fairness or completeness of the

information presented or contained in this presentation. Neither the Company nor any of its affiliates, advisers or representatives, accepts any responsibility

whatsoever for any loss or damage arising from any information presented or contained in this presentation. The information presented or contained in this

presentation is current as of the date hereof and is subject to change without notice and its accuracy is not guaranteed. Neither the Company nor any of its

affiliates, advisers or representatives make any undertaking to update any such information subsequent to the date hereof. This presentation should not be

construed as legal, tax, investment or other advice.

[Data in this presentation was obtained from various external data sources, and the Company has not verified such data with independent sources. Accordingly,

the Company makes no representations as to the accuracy or completeness of such data, and such data involves risks and uncertainties and is subject to change

based on various factors].

This presentation contains forward-looking statements. Such statements are not statements of historical facts, and reflect the beliefs and expectations of

Magnesita’s management. The words "anticipates", "wishes", "expects", "estimates", "intends", "forecasts", "plans", "predicts", "projects", "targets" and similar

words are intended to identify these statements. Although the Company believes that expectations and assumptions reflected in the forward-looking statements

are reasonable based on information currently available to the Company's management, the Company cannot guarantee future results or events. You are

cautioned not to rely on forward-looking statements as actual results could differ materially from those expressed or implied in the forward-looking statements.

This presentation does not constitute an offer, or invitation, or solicitation of an offer, to subscribe for or purchase any securities, and neither any part of this

presentation nor any information or statement contained therein shall form the basis of or be relied upon in connection with any contract or commitment

whatsoever.

Disclaimer

Index

Magnesita Overview

Refractory Sector

Company’s Strategy

Growth and Opportunities Drivers

Financial Highlights

Company History

Over 70 years of experience in refractory and mining business

Magnesita’s fundation after the discovery of a large amount of magnesite in Brumado (BA)

1939

Beginning of magnesite sinter

production in Brumado

Beginning of refractories production

in Contagem (MG)

40’s

Company’s IPO

1973

Expansion of operations in

Brazil and export

beginning to South America

60’s

Foundation of the Center of Research

and Development in Contagem (MG)

Beginning of service

segment

70’s

Refratec acquisition

Beggining of slide gates production

80’s

Beginning of CPP model (Cost per

Performance)

Initiation in the cement sector

90’s

GP Investments acquire control

of Magnesita S.A.

2007

LWB acquisition,

becoming the 3rd largest

company in the sector

Novo Mercado

listing

2008

New strategy view

2012

Investments approval to

increase verticalization

2010

Magnesita Overview

Magnesita is a leading global refractory and industrial mining company

3rd largest player in the refractory sector worldwide

Revenues of R$ 2.3 billion in 2011 (R$1.9 billion 9M12)

7,000 employees, 28 industrial facilities with a nominal capacity of 1.6 million tons/year of

refractories

Presence in 4 continents, supplying more than 850 clients worldwide

Leader in the steel and cement industries in Brazil and South America

Leader in the stainless steel industry in North America and Europe

High-quality raw materials: Better, largest and lowest cost magnesita mine in the world outside

China.

Significant number of unexplored mineral rights

Magnesita: 3 Businesses Across the Value Chain

Net revenues (2011)

R$ 2,034.1 million

(87.7% of the total revenues)

R$ 152.6 million

(6.6% of the total revenues)

R$ 132.2 million

(5.7% of the total revenues)

Gross margin (2011)

32.1% 11.3% 45.8%

Details/ description

Refractories with tailor made

formulations and shapes as

well as strong technical service

Two commercial models (CPP

and conventional)

Industrial minerals primarily talc and caustic magnesia

Excess minerals not utilized for internal production of refractories primarily magnesia sinter

Assembly and installation of

refractories

Other adjacent services inside

the mill, including spot

contracts

Bu

sin

ess

line

Services Refractories Solutions Industrial Minerals

Applications

Steel, cement, non-ferrous

(aluminum, nickel, copper,

etc.) and non-metallic (glass,

petrochemical, pulp and

paper)

Steel, cement and mining

Talc: Plastic industry, cosmetics, pharmaceuticals, food, ceramics, pulp and paper, etc.. Caustic magnesia: Fertilizers, abrasives, animal nutrition, etc.. Sinter: refractories industry

USA

Germany

China

Brazil

Headquarter

Sales Office

Raw material and refractory production

Port (BA)

Raw Material Flow

Final Product Flow

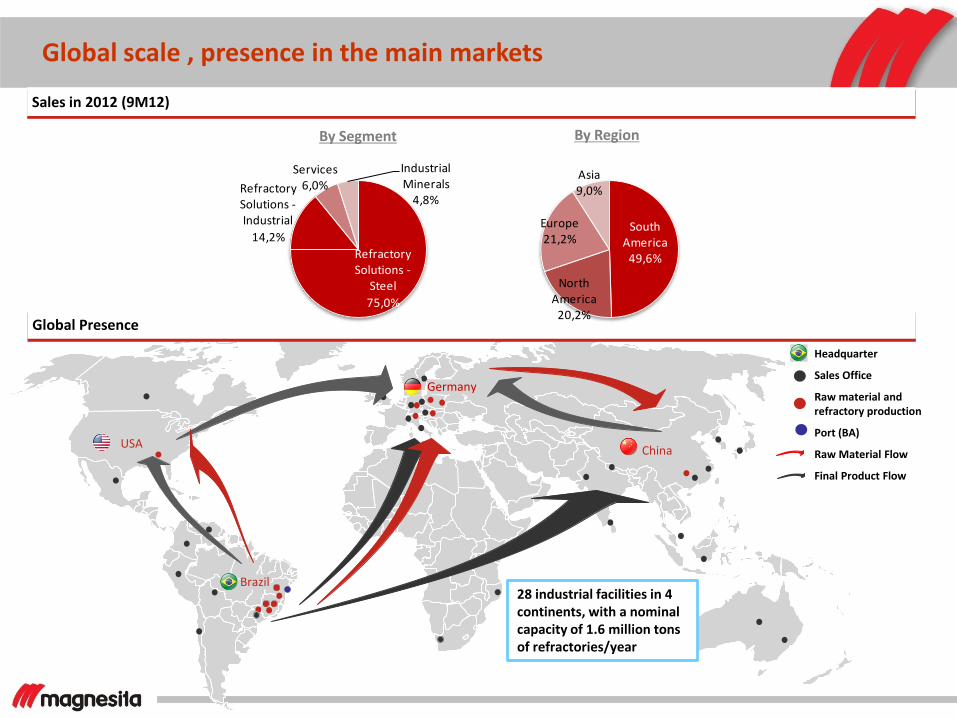

Global scale , presence in the main markets

Global Presence

Sales in 2012 (9M12)

By Segment By Region

Refractory Solutions -

Steel

75,0%

Refractory Solutions -Industrial

14,2%

Services6,0%

Industrial Minerals

4,8%

South America

49,6%

North America

20,2%

Europe21,2%

Asia9,0%

28 industrial facilities in 4 continents, with a nominal capacity of 1.6 million tons of refractories/year

Great availability of high quality minerals

Magnesite Mine in Brumado (BA)

• Reserve estimated of 830 mln tons

•Expected life: over 200 years

• The mine is connected to the port of Aratu by the FCA railway

Dolomite Mine in York (USA)

• Reserve of 25 mln tons

• Expected life: 50 years

Dolomite Mine Sinterco (JV - Belgium)

• Reserve of 31 mln tons

• Expected life: 30 years

Dolomite Mine in Qingyang (China) • Reserve of 18 mln tons

• Expected life: 50 years

Graphite Mine in Almenara (MG)

* Still under geological study

Other reserves

• Talc

•Chromite

• Clays

• Pirofilite 78 active mineral concessions

in Brazil (several of which unexplored)

Controlling

Group

%

Rhone 7,2%

Raising standards of corporate governance

Novo Mercado

Member since 2008, Novo Mercado correspond to the best practices of corporate governance,

ensuring and improving the transparency of companies with its shareholders

2 independent Board members

Financial statements in English in accordance with International Financing Report Standards (IFRS)

Stocks are included in the IGC (Index of Differentiated Corporate Governance) and ITAG (Index of

Differentiated Tag Along)

Controlling Group

GP

- Latin America leadership in Private Equity

- Culture of promotion by merit

- Proven track record

Rhône: Prior LWB controllers group

Free Float

58,8%

GP 34,0%

Continuous effort in Corporate Social Responsibility

Environmental Responsibility

Project of logistic reverse: 100% of refractories residues recycling

Certifications: ISO 14001 (environmental), ISO 9001 (quality) e OHSAS 18001 (health and safety)

Social Responsibility

Project “Citizen of the Future”: Sports and musical activities for more than 200 children in Brumado (BA)

Project of Social inclusion in Magnesita (PRISMA): Inclusion of deaf people as Magnesita’s employees

Withdraw of refractories residues after clients use

Residues are sent to the recycling units

Processing and transformation in raw material

Use of the raw material in our industrial facilities

Index

Magnesita Overview

Refractory Sector

Company’s Strategy

Growth and Opportunities Drivers

Financial Highlights

12

What is a Refractory?

Refractories are crucial for manufacturing processes with high temperatures

Product Overview Main Consumers Worldwide

Fireproof materials consumed within various production processes, retaining

physical and chemical characteristics when exposed to extreme conditions

Provides heat, chemical and mechanical resistance in industrial furnaces and

other equipments in iron and steel production and kilns in cement and lime

production

Raw material quality and ensure supply are essential

~US$ 25 billion industry globally

Represents only ~3% of the production costs in steel manufacturing Source: Industrial Minerals Magazine, December 2010.

Others 5%

Steel 70%

Cement 7%

Glass 4%

Chemical 4%

Non-ferrous 5%

Ceramic 5%

Types of refractories

Bricks

Valves and slide gates

Monolithics

Main raw material families

Magnesite Application: steel and cement Dolomite Application: mini mills and stainless steel Alumina Application: steel and cement

Consumption (average)

1 tonne of steel = ~10 Kg

1 ton of cement = ~0.6 Kg

13

Electric Arc Fumace

Steel Refining Facility

Continuos Casting

Basic Oxygen Furnace Recycled Steel

Direct Reduction

Coal Injection

Iron Ore

Coal

Coke Oven

Limestone Blast Furnace

Natural Gas

ELECTRIC ARC FURNACE

Volume: 120 tonnes

Life Expectancy: 1 month

BLAST FURNACE

Refractory Volume: 900

tonnes

Life Expectancy: 15 years

TORPEDO CAR

Volume: 200 tonnes

Life Expectancy: 2 years

CONVERTER

Volume: 800 tonnes

Life Expectancy: 6 months

CONTINUOUS CASTING

Volume: 25 tonnes

Life Expectancy: 10 hours

STEEL LADLES

Volume: 70 tonnes

Life Expectancy: 1 month

Source: Company

Steel industry: represents approximately 85% of Magnesita’s refractories revenues

Refractories are Continuously Consumed During Steel Production…

14

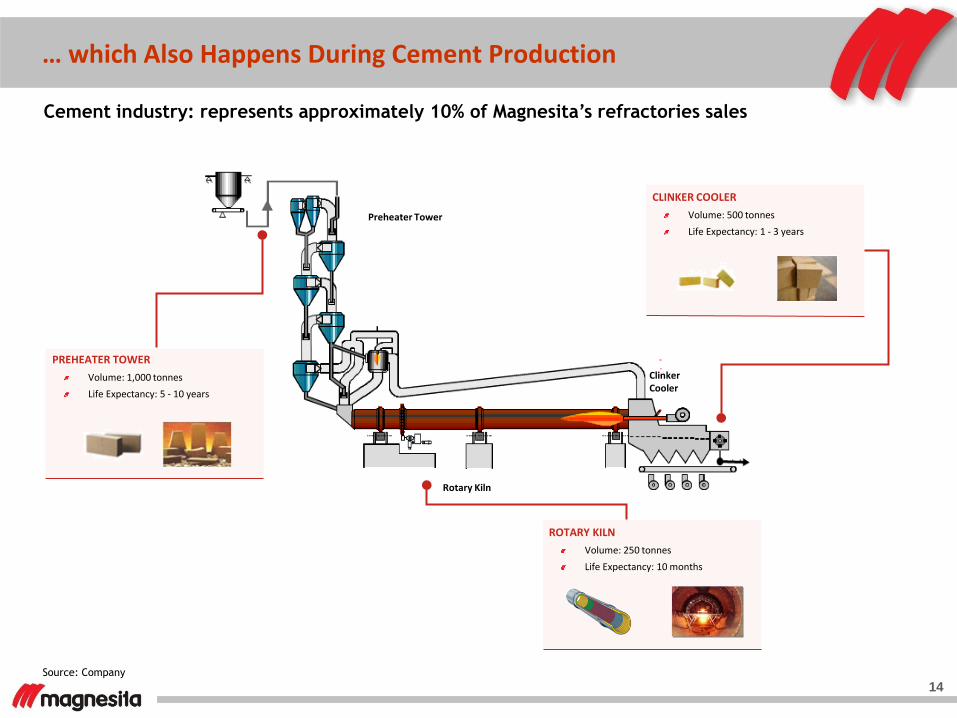

Rotary Kiln

Preheater Tower

PREHEATER TOWER

Volume: 1,000 tonnes

Life Expectancy: 5 - 10 years

… which Also Happens During Cement Production

ROTARY KILN

Volume: 250 tonnes

Life Expectancy: 10 months

CLINKER COOLER

Volume: 500 tonnes

Life Expectancy: 1 - 3 years

Cement industry: represents approximately 10% of Magnesita’s refractories sales

Clinker Cooler

Source: Company

Magnesita: Integration in the refractory supply chain

Mine

Magnesite sinter

Raw material Refractory Solutions

Bricks

Valves and slide gates

Services

Installation of refractories

Technical Assistance

Magnesite Mine in Brumado (BA)

Furnace (HW) of sinter production

Monolithics

Index

Magnesita Overview

Refractory Sector

Company’s Strategy

Growth and Opportunities Drivers

Financial Highlights

The new vision and the 4 strategy pillars

Vision: Be the best provider of refractories solutions and industrial minerals,

leveraging and developing our minerals base

Continue to develop high quality, low cost raw material sources to support our current busi-nesses as well as new businesses where we can have a sustainable competitive advantage

Strive to keep offering high quality and innovative products, unrivaled services and cost performance

Optimize production globally to improve efficiency and support growth

Develop global supply chain management

Pursue long term growth opportunities in selected markets where we can deliver superior value to our customers and shareholders

Expand industrial minerals base

Ensure leadership in our core markets

Maintain a global low cost production base

Grow selectively and aggressively

▪ Meritocracy

▪ Ethics

▪ Profit

▪ Management and Method

▪ Customer

▪ People

▪ Agility and Transparency

▪ Respect for Safety, Environment and Communities

Our values

On

e g

lob

al o

rga

niz

ati

on

Industrial Minerals

Initial portfolio of attractive mineral rights

Very favorable geography for industrial minerals in Brazil

Possibility to occupy a “white space” in the market and become most important (if not sole) player in it

0 1

2

3

Magnesita’s strategic

positioning

Privileged access to deal flow and other unique resources: ▪ Geological and

research skills ▪ knowledge of

local licensing requirements

▪ Knowledge of local stake-holder management

Magnesita 2017

Industrial Minerals

New

refractories markets

Core refractories Markets

Integrated product offer:

•Raw materials •Refractory Solutions •Services

• Largest magnesite mine ex-China • Low-cost/high quality source for a relevant refractories raw materials • Portfolio of industrials minerals in Brazil

•Leadership in South America and dolomite products

• Sustainable position in selected markets with focus in growth and industrial applications

Index

Magnesita Overview

Refractory Sector

Company’s Strategy

Growth and Opportunities Drivers

Financial Highlights

11,.%2.5%

7.4%

8,.%

3.1%

1.0%

1.3%

46.9%

18.0%

0.4%European Union (27) Other EuropeC.I.S. (6)North AmericaSouth AmericaAfricaMiddle EastChinaAsia (ex-China)Oceania

Refractories Solutions - Opportunities

Strategic Focus Ensure our leadership in key markets and follow its growth Increase presence in markets where our participation is low or nil, with geographic and industry diversity

Competitive advantages Global player, with local presence in key markets High raw materials verticalization and low cost production High technology and specialized technical assistance Long term relationship with clients Experienced management

Refractories comsumption - Global Market Magnesita – Refractories Solutions by segment (9M12)

Global Steel Production by region (2012 until oct.) Magnesita – Refractories Solutions by region (9M12)

70.0%

30.0% Steel

Industrial84.0%

16.0%

Steel

Industrial

49.6%

202%

21.2%

9.0% South America

North America

Europe

Asia

Services - Opportunities

Strategic Focus

Focus on segments with higher added value :

Service contracts related to the maintenance, assembly and installation of refractories

Longer and bigger spot contracts

Expand to other segments such as mining and cement

Geographic expansion

Competitive advantages

Expertise

High qualified technical staff

Ensure that the quality of installation is adding value to our clients, besides offering a better package solutions for

them

Assembly of refractories

Minerals - Opportunities

Strategic Focus

Development of Graphite Project

Expand Talc business

New minerals

Competitive advantages

70 years of mining experience in Brazil

Dedicated team to prospect, analyze and develop business

78 active mineral concessions

Index

Magnesita Overview

Refractory Sector

Company’s Strategy

Growth and Opportunities Drivers

Financial Highlights

Financial Highlights (R$ mln)

Revenues

1.389

1.688 1.720 1.853

9M09 9M10 9M11 9M12

Gross Profit and margin

443

591 547 569

31,9% 35,0%

31,8% 30,7%

9M09 9M10 9M11 9M12

EBITDA and margin EBITDA* and margin*

-49

72 87

76

9M09 9M10 9M11 9M12

Net Income (R$ mln)

Net Income

226,2

352,8 315,7

277,0

16,3%

20,9% 18,4%

15,0%

9M09 9M10 9M11 9M12

229,4

328,8

269,2 292,2

16,5%

19,5%

15,7% 15,8%

9M09 9M10 9M11 9M12

*not considering one-off revenues/expenses

Performance by segment

Refractory Solution

Services

1.518 1.652

494 519

32,6% 31,4%

9M11 9M12

Revenues Gross Profit Gross Margin

496 525 497 516 550 567 535

166 168 160 158 170 184 166

33,5% 32,1% 32,2% 30,6% 30,8% 32,4% 31,0%

1T11 2T11 3T11 4T11 1T12 2T12 3T12

Revenues Gross Profit Gross Margin

Industrial Minerals

84 89

39 39

46,2% 43,5%

9M11 9M12

Revenues Gross Profit Gross Margin

34

21 28

49

25 34 30

14 11 14 22

10 15 14

39,7%

51,2% 50,6% 44,9% 41,4% 43,7% 45,0%

1T11 2T11 3T11 4T11 1T12 2T12 3T12

Revenues Gross Profit Gross Margin

45 37 37 34 31

37 43

6 4 4 3 2 3 6

13,4% 11,3% 10,4% 9,7%

5,5%

8,6%

13,9%

1T11 2T11 3T11 4T11 1T12 2T12 3T12

Revenues Gross Profit Gross Margin

118 111

14 11

11,8% 9,8%

9M11 9M12 Revenues Gross Profit Gross Margin

Cash flow from operations, CAPEX and Cash cycle

Cash flow and CAPEX R$ million

Cash conversion cycle Days

146 138 143 143 145

76 79 67 69 68

144 138

131 131 136

78 80 79 82 78

3Q11 4Q11 1Q12 2Q12 3Q12

Cash conversion cycle (days)¹

Cash conversion cycle Suppliers Inventories Clients

188,4

96,9 90,0

39,462,4 61,7

3Q11 (c) 2Q12 (b) 3Q12 (a)

FCO CAPEX

460,6

250,6

86,8

179,9

9M11 9M12

FCO CAPEX

900.2 957.3 968.0

1,060.0 1,074.4

787.7 761.2 791.8 819.1 834.7

2.11x2.24x 2.30x

2.51x

2.76x

3Q11 4Q11 1Q12 2Q12 3Q12

Net Debt Working capital Net Debt/EBITDA

Debt and leverage

Net debt and leverage R$ million

Debt profile

6.8%

93.2%

Short term Long term

16.9%

83.1%

Local currency (BRL) Foreign currencies

Investor Relations Contacts Octavio Pereira Lopes

CEO and IRO

Daniel Domiciano Silva Investor Relations

Phone: 55 11 3152-3202/3241

[email protected] www.magnesita.com

Thank you!

MAGNESITA REFRATÁRIOS S.A.