appalachian’s guide to lexington’s program connect · appalachian’s guide to lexington’s...

TRANSCRIPT

Appalachian’s Guide to Lexington’s Program Connect

1 | P a g e

This is for III Agents who have already signed up and received a Login and Password from AUI. Agents wanting to request access for first time, complete request here General Underwriting Guidelines & Highlights: (Not Availble in AR, NE, KY or WV)

Default Forms Available: HO3, HO4, HO6 AND DP3: 100% insurance to value product, inspected with

MSB Wind Always Included Important: Use our “Guide to Cov A” on page XX to

determine the appropriate amount to use in your quote. Regionality and Building materials major factor

Minimum Inland Coverage A is $150K, Except; o AL, CA, FL, GA & MS is $200K Min o LA, TX is $250K Min

Minimum Coastal Coverage A Now $300k, Except; o LA is $500K Min o TX is $500K Min within 10 miles of coast

Coverage to $10MM TIV available Risks with Up to 5 Losses Within the Last 5 Years Flexibility to reduce or remove underlying coverages Primary, Secondary, Seasonal, Tenant, Vacant Declined, Canceled, Non-Renewed all Eligible PC 1‐10 LLCs and Trusts Accepted No Bankruptcy past 7 years Agency Billed, Premium Finance Acceptable

Service Levels and Additional Information:

AUI strives to maintain the best industry service level on your submission, we currently maintain a 24 hours or less turnaround

In the event you need same day turnaround, review the email that is sent to you the moment the account is assigned to an underwriter, feel free to call them to prioritize your request

The firm quotes are good for 30 days only To request bind, follow the direction on the quote package sent to you. The earliest we can bind

coverage is the date we received written confirmation to bind coverage Note that 25% minimum earned premium applies, and all fee are fully earned

Every firm quote we release to you includes a “Sign and Send” premium finance agreement to assist you in offering installment terms to your customer

Appalachian’s Guide to Lexington’s Program Connect

2 | P a g e

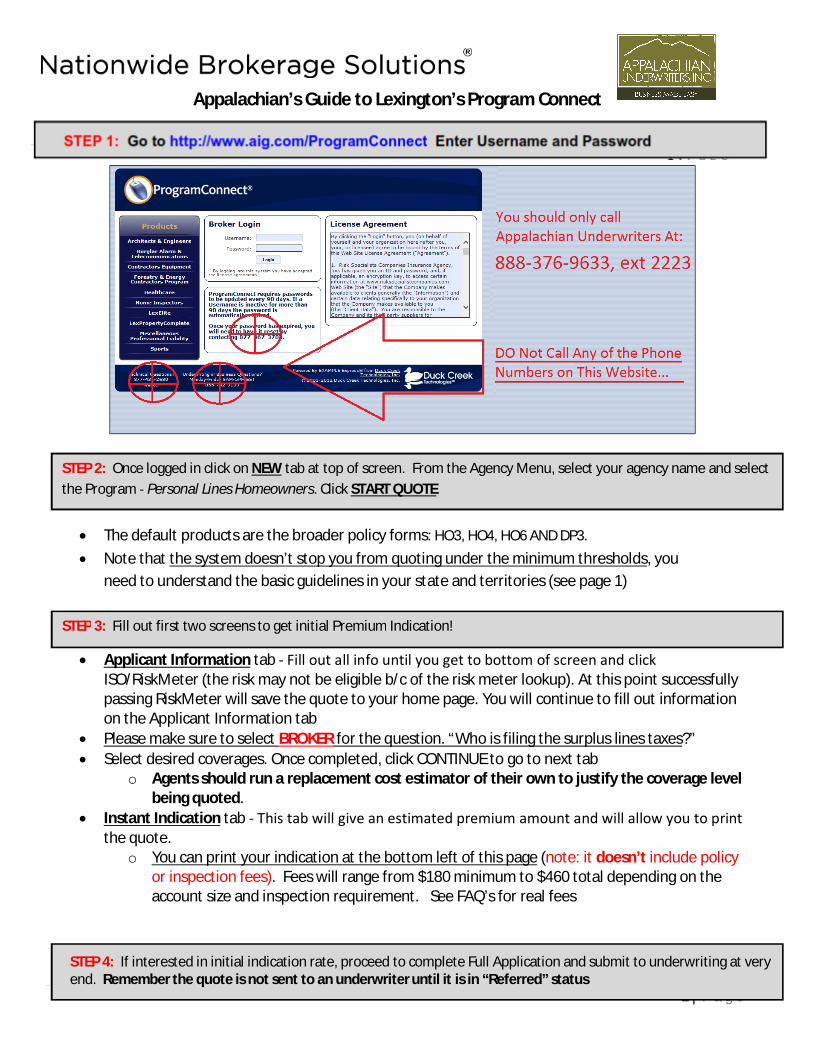

The default products are the broader policy forms: HO3, HO4, HO6 AND DP3. Note that the system doesn’t stop you from quoting under the minimum thresholds, you

need to understand the basic guidelines in your state and territories (see page 1)

Applicant Information tab ‐ Fill out all info until you get to bottom of screen and click ISO/RiskMeter (the risk may not be eligible b/c of the risk meter lookup). At this point successfully passing RiskMeter will save the quote to your home page. You will continue to fill out information on the Applicant Information tab

Please make sure to select BROKER for the question. “Who is filing the surplus lines taxes?” Select desired coverages. Once completed, click CONTINUE to go to next tab

o Agents should run a replacement cost estimator of their own to justify the coverage level being quoted.

Instant Indication tab ‐ This tab will give an estimated premium amount and will allow you to print the quote.

o You can print your indication at the bottom left of this page (note: it doesn’t include policy or inspection fees). Fees will range from $180 minimum to $460 total depending on the account size and inspection requirement. See FAQ’s for real fees

STEP 3: Fill out first two screens to get initial Premium Indication!

STEP 2: Once logged in click on NEW tab at top of screen. From the Agency Menu, select your agency name and select the Program ‐ Personal Lines Homeowners. Click START QUOTE

STEP 4: If interested in initial indication rate, proceed to complete Full Application and submit to underwriting at very end. Remember the quote is not sent to an underwriter until it is in “Referred” status

Appalachian’s Guide to Lexington’s Program Connect

3 | P a g e

Tax Filer tab - Once on this tab, we simply need you to input something in this field to get to your quote. It can be any random number or letters. An error may pop‐up Stating you have entered and invalid license number, however, this is completely fine as an AUI underwriter will update this correctly once submitted. This will allow you to CONTINUE

Below is a helpful guide to assist you on the tax filer page o Below are the questions , and answers in red that are required in order for you to

continue filling out the rest of the application to refer into Appalachian Underwriters

1. Who is filling the surplus lines Taxes? Broker 2. License Number, Put in a fake number or letter, doesn’t matter 3. By selecting this box, I agree to these: you are agreeing to the Terms and

Conditions (check box) Check the box 4. E‐signature and date, Sign your name (agent) and date

** ONCE YOU ANSWER THE 5 QUESTIONS AND HIT VALIDATE LICENSE THE CONTINUE BUTTON WILL APPEAR **

Application Information tab ‐ Please fill out all the information correctly and accurately. Click

CONTINUE Coverages and Endorsements tab ‐ These questions will automatically default to NO. Please

change to YES if any apply. Click CONTINUE Policy History tab ‐ Enter all prior carrier information and click CONTINUE Claim History tab ‐ It is VERY important to enter ALL claims. This will help our underwriters

provide you an accurate quote. Click CONTINUE Summary tab ‐ This tab will allow you to view your entire quote and estimated premium.

o PLEASE NOTE ALL Applications will be statused to “referred” o Once referred, your application with be automatically assigned to an underwriter, who will

then complete the underwriting to release bindable terms to you. Once released, it is a fully underwritten, with all fees and taxes for you to request bind on. If you have questions CALL 888‐376‐9633, ext 2223

Lexington is a registered trademark of Lexington Insurance Company. All rights reserved.

Lexington Insurance Company (Lexington Insurance), a Chartis Company, is the leading U.S.‐based surplus lines insurer. Chartis is the marketing name for the worldwide property‐casualty and general insurance operations of Chartis Inc. For additional information, please visit www.chartisinsurance.com. All products are written by insurance company subsidiaries or affiliates of Chartis Inc. Coverage may not be available in all jurisdictions and is subject to actual policy language. Non‐insurance products and services may be provided by independent third parties. Certain coverage may be provided by a surplus lines insurer. Surplus lines insurers do not generally participate in state guaranty funds and insureds are therefore not protected by such funds