asean and ftas implications for business-82246-v4-handms

TRANSCRIPT

ASEAN and FTAs: Implications For Business

James Lockett, Hanoi

Vietnam Supply Chain

HCMC, 27 April 2011

2 ©2011 Baker & McKenzie

Overview of Presentation

–Key Elements of ASEAN;

–FTAs involving ASEAN, and

their impact;

–Trans-Pacific Partnership;

–Examples of the benefits of

FTAs;

–Utilization of FTAs and

Recommendations.

3 ©2011 Baker & McKenzie

Key Elements of ASEAN

4 ©2011 Baker & McKenzie

GENERAL INFORMATION

– The Association of Southeast Asian Nations

– Establishment: 8 August 1967 (Bangkok)

– Members:– Original members: Indonesia, Malaysia, Philippines, Singapore, and

Thailand

– Other members: Brunei Darussalam, Vietnam, Laos, Myanmar and

Cambodia

– As of July 2010:– Total population: approx. 590 million

– Total Area: approx. 4.46 million Km

– Combined GDP: Approx. US$ 1,500 billion

– Total trade: Approx. US$ 1,536 billion

– FDI inflow: Approx. US$ 39.6 billion

5 ©2011 Baker & McKenzie

ASEAN SECRETARIAT

Secretary General

Deputy Secretary General(Economic Cooperation) Office of Secretary General

Deputy Secretary General(Functional Cooperation

Bureau for EconomicIntegration and Finance

Bureau for External Relations and Coordination

Bureau for Resources Development

6 ©2011 Baker & McKenzie

ASEAN COMMUNITY

– Declaration of ASEAN Concord II (Bali Concord II)

– 7 October 2003

– Bali, Indonesia

– Three Pillars:

– ASEAN Security Community;

– ASEAN Socio-Cultural Community;

– ASEAN Economic Community.

→ ASEAN Community shall be established upon the realization of

these three pillars.

One VisionOne IdentityOne Community

7 ©2011 Baker & McKenzie

ASEAN ECONOMIC COMMUNITY (AEC)

– To be created by 2015. Blueprint agreed in November 2007.

– The end goal of economic integration:

– Single market;

– Fair competition;

– Production base.

– Steps in moving forwards the AEC:

– Strengthen the implementation of AFTA, AFAS and AIA/ACIA.

– Accelerate regional integration in priority sectors.

– Facilitate movement of business persons, skilled labor and talents.

– Strengthen the institutional mechanism, including improvement of ASEAN

Dispute Settlement Mechanism.

8 ©2011 Baker & McKenzie

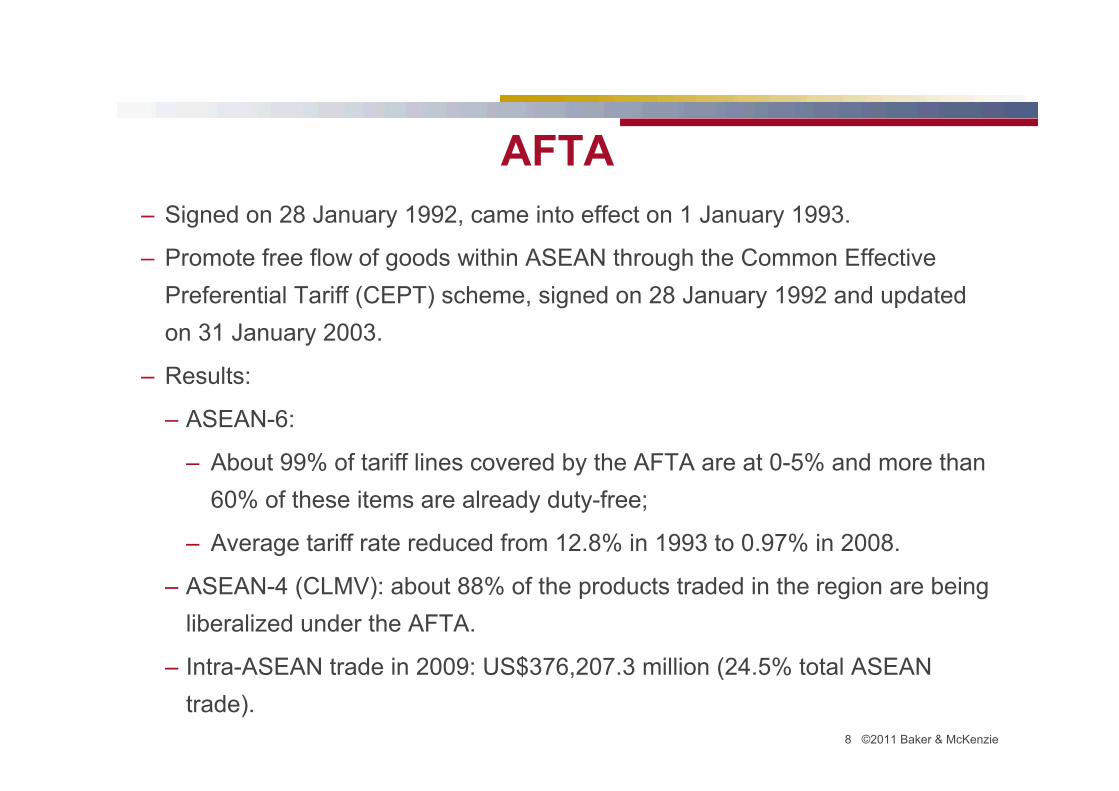

AFTA

– Signed on 28 January 1992, came into effect on 1 January 1993.

– Promote free flow of goods within ASEAN through the Common Effective

Preferential Tariff (CEPT) scheme, signed on 28 January 1992 and updated

on 31 January 2003.

– Results:

– ASEAN-6:

– About 99% of tariff lines covered by the AFTA are at 0-5% and more than

60% of these items are already duty-free;

– Average tariff rate reduced from 12.8% in 1993 to 0.97% in 2008.

– ASEAN-4 (CLMV): about 88% of the products traded in the region are being

liberalized under the AFTA.

– Intra-ASEAN trade in 2009: US$376,207.3 million (24.5% total ASEAN

trade).

9 ©2011 Baker & McKenzie

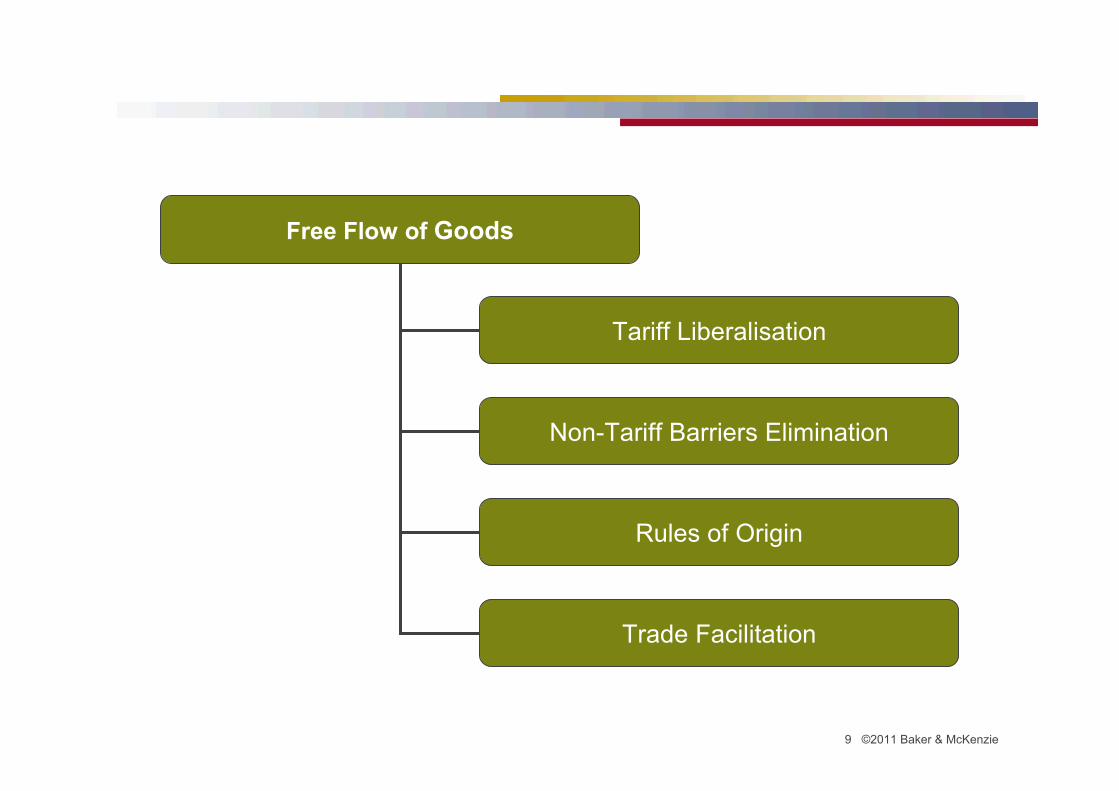

Free Flow of Goods

Tariff Liberalisation

Non-Tariff Barriers Elimination

Rules of Origin

Trade Facilitation

10 ©2011 Baker & McKenzie

ASEAN Progress in Services Integration

– ASEAN Framework Agreement on Trade in Services (AFAS) is

consistent with the GATS (General Agreement on Trade in Services)

of the WTO, and is intended to be “GATS-Plus”;

– Eight packages of liberalisation commitments have been concluded

and signed by AEM;

– In addition, there are additional 4 packages of commitments in

financial services and 3 packages in air transport.

11 ©2011 Baker & McKenzie

ASEAN Progress in Investment Integration (AIA/ACIA)

– ASEAN Ministers signed the Framework Agreement on the ASEAN Investment

Area (AIA) on 7 October 1998 in Manila:

– Key concept: “ASEAN Investor”. Defined as being equal to a national investor

in terms of the equity requirements of the member country in which the

investment is made. Thus, a foreign firm with a majority interest can avail

itself of national treatment and investment market access privileges, in

addition to the other benefits provided under the AIA Agreement and other

regional economic schemes.

– Immediate opening up of all industries for investment, with some exceptions

as specified in the Temporary Exclusion List (TEL) and the Sensitive List

(SL), to ASEAN investors by 2010 and to all investors by 2020.

– Immediate national treatment, with some exceptions.

– In 2009, via ASEAN Comprehensive Investment Agreement, AIA extended to

ACIA.

12 ©2011 Baker & McKenzie

ASEAN Progress in Investment Integration (AIA/ACIA) – Cont.

– ASEAN Ministers signed the ASEAN Comprehensive Investment Agreement

(ACIA) on 26 February 2009.

– Key concepts: “ASEAN Investor” extended to foreign-owned ASEAN based

investors.

– However, a Member State may deny the benefits of the ACIA to a ASEAN

Investor if, inter alia, a non-ASEAN investor owns or controls that juridical

person and the juridical person has no substantive business operation in

the territory of the host state.

– In addition, a covered investment needs to be admitted according to laws,

regulations and national policies, and where applicable, specifically

approved in writing by the competent authority of a Member State.

13 ©2011 Baker & McKenzie

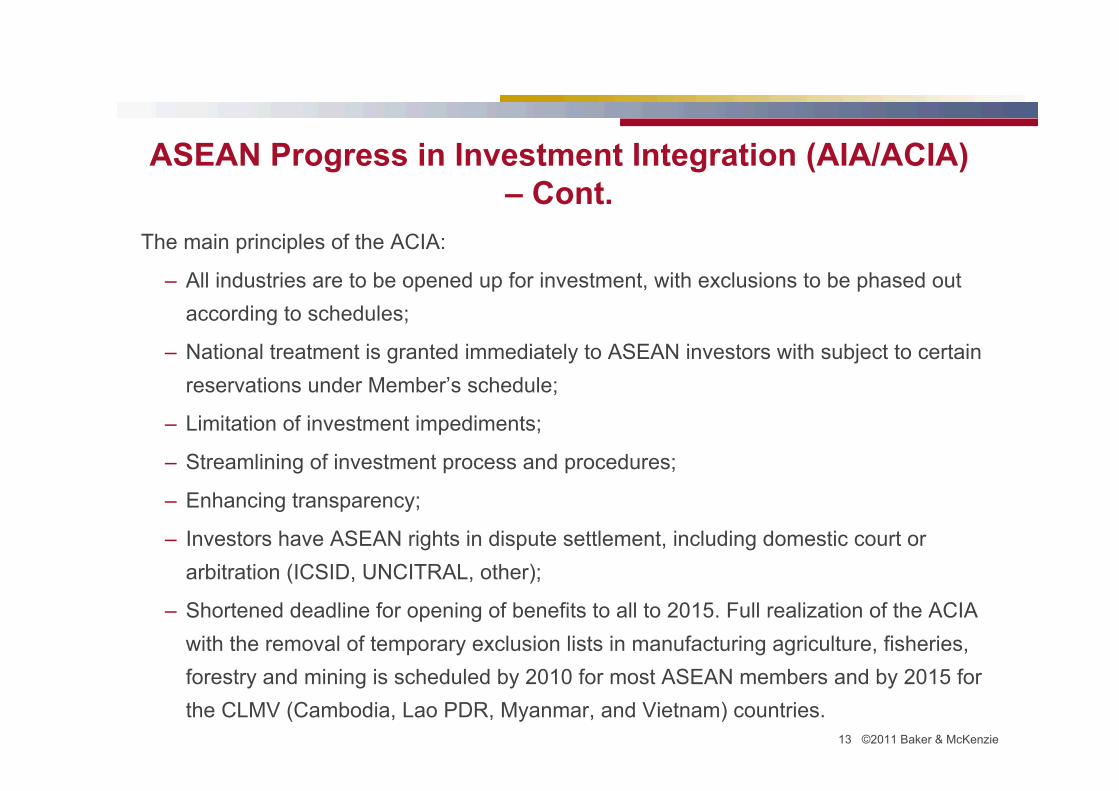

The main principles of the ACIA:

– All industries are to be opened up for investment, with exclusions to be phased out

according to schedules;

– National treatment is granted immediately to ASEAN investors with subject to certain

reservations under Member’s schedule;

– Limitation of investment impediments;

– Streamlining of investment process and procedures;

– Enhancing transparency;

– Investors have ASEAN rights in dispute settlement, including domestic court or

arbitration (ICSID, UNCITRAL, other);

– Shortened deadline for opening of benefits to all to 2015. Full realization of the ACIA

with the removal of temporary exclusion lists in manufacturing agriculture, fisheries,

forestry and mining is scheduled by 2010 for most ASEAN members and by 2015 for

the CLMV (Cambodia, Lao PDR, Myanmar, and Vietnam) countries.

ASEAN Progress in Investment Integration (AIA/ACIA) – Cont.

14 ©2011 Baker & McKenzie

KEY SIMILARITIES TO EUROPEAN COMMUNITY

– Three Pillars: Economic, Political/Social, Defense;

– “Four Freedoms”: Free movement of goods, services,

people and capital;

– Increasing measure of intra-community trade and

investment;

– Fear of losing to other competitors (India, China);

– Political will, driven by need for competitiveness.

15 ©2011 Baker & McKenzie

KEY DIFFERENCES TO EUROPEAN COMMUNITY

– No common external tariff policy (not a customs union);

– No common competition rules;

– No private remedies (i.e., no available mechanism for

individuals or companies to contest a decision of an

ASEAN member country);

– No strong Secretariat;

– No common currency.

16 ©2011 Baker & McKenzie

FTAs involving ASEAN, and their impact

17 ©2011 Baker & McKenzie

Still Alphabet Soup…

ASEAN-China FTA

AFTA

US-Singapore FTA

Thailand-Australia FTASAPTA

GCC CEPA

Pacific Three

Singapore-Korea FTAAsia Pacific TA

China-Chile FTA Singapore-GCC

ASEAN-India FTA

18 ©2011 Baker & McKenzie

FTAs Between ASEAN and Other Countries

– ASEAN – Australia – New Zealand (AANZFTA)

– ASEAN – China (ACFTA)

– ASEAN – Japan (AJCEP)

– ASEAN – Korea (AKFTA)

– ASEAN – India (AIFTA)

– Pending negotiations

– EU bilateral negotiations with individual ASEAN members.

19 ©2011 Baker & McKenzie

Rules of Origin under Asian FTAs

– Value-Added Rules – AFTA, ASEAN-China, ASEAN-India

– Other Types of Rules:

– Change in tariff classification (shift between chapters, headings or sub-headings);

– Processing (product to undergo specific processing operations or chemical reaction);

– Product specific rules (can be a combination of one or more of the other rules).

20 ©2011 Baker & McKenzie

Rules of Origin under Asian FTAs

Source: ASEAN-Australia-NZ FTA, Primer on Rules of Origin, ASEAN Secretariat

21 ©2011 Baker & McKenzie

What is the benefit?

- Example: Use Vietnam to produce/export:9 other ASEAN countries

Exporters of Vietnam

Australia

New Zealand

China

Japan

Korea

EU

India

TPP

22 ©2011 Baker & McKenzie

Trans-Pacific Strategic Economic Partnership Agreement (TPP)

23 ©2011 Baker & McKenzie

TPP: Background

– History

Originally signed in 2005 between 4 countries;

Current negotiations began in 2009.

– Negotiation Schedule

4 rounds held through December 2010;

5 rounds scheduled for 2011.

24 ©2011 Baker & McKenzie

Negotiating the TPP

25 ©2011 Baker & McKenzie

Negotiating the TPP

– Negotiation Schedule for 2011

5th round of negotiation in Santiago, Chile: 14-18 February 2011;

6th round of negotiation in Singapore: 28 March to 2 April 2011;

7th round expected to be in Hochiminh City, Vietnam: 20-24 June

2011;

8th round expected to be in San Francisco, US: 6-11 September

2011; and

9th round expected to be in Lima, Peru: 24-28 October 2011.

–Aim to conclude by APEC Summit in November 2011

(but mid-2012 more likely).

26 ©2011 Baker & McKenzie

Parties

– Full Members:

Singapore, Brunei, Chile, New Zealand, United States,

Australia and Peru;

Recently: Malaysia and Vietnam.

– Interested in Joining:

Japan

Canada

Others (including several ASEAN countries)

27 ©2011 Baker & McKenzie

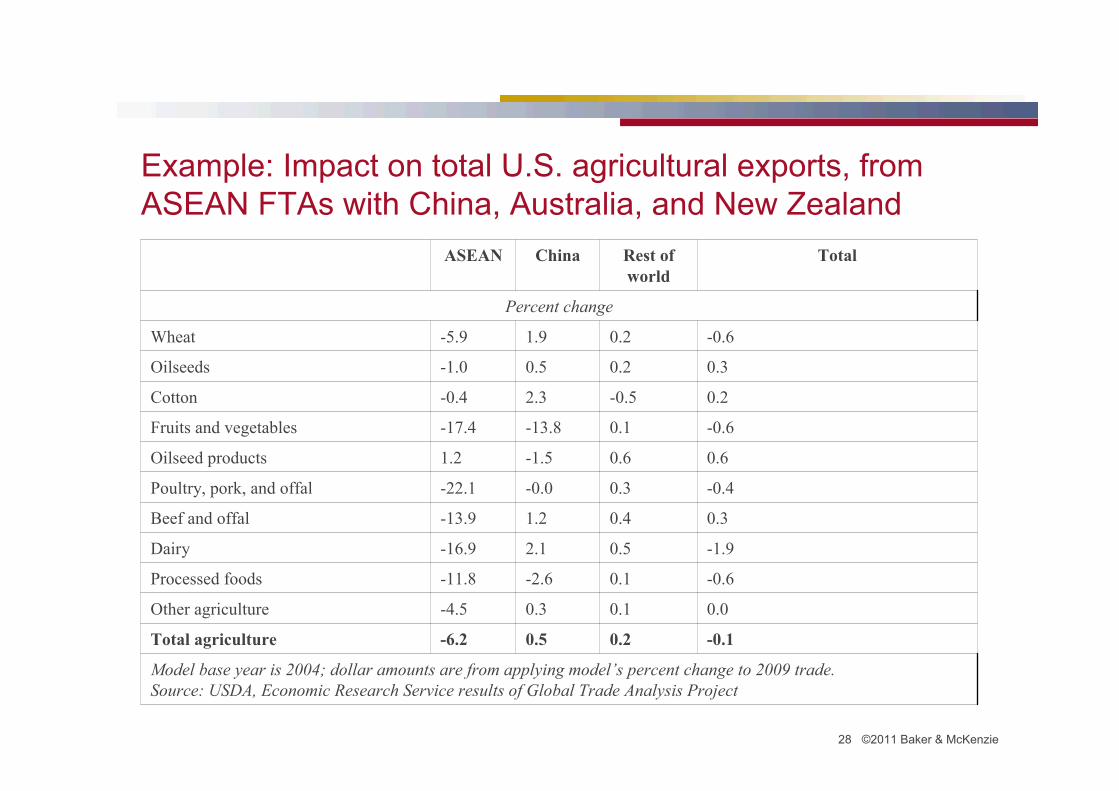

U.S. objectives in joining TPP

– To create a platform for broader economic integration in the

Asia – Pacific Region;

– Expansion of U.S. export markets to other parts in the world;

– Concern of the U.S. of being blocked out of the world’s fastest

growing region because of the proliferation of regional FTAs

that exclude the U.S., e.g., ASEAN+ FTAs. E.g., U.S.

Department of Agriculture study showing US agricultural

exports decreased 6% because of ASEAN+ FTAs.

28 ©2011 Baker & McKenzie

Example: Impact on total U.S. agricultural exports, from ASEAN FTAs with China, Australia, and New Zealand

Model base year is 2004; dollar amounts are from applying model’s percent change to 2009 trade. Source: USDA, Economic Research Service results of Global Trade Analysis Project

-0.1 0.2 0.5 -6.2 Total agriculture

0.0 0.1 0.3 -4.5 Other agriculture

-0.6 0.1 -2.6 -11.8 Processed foods

-1.9 0.5 2.1 -16.9 Dairy

0.3 0.4 1.2 -13.9 Beef and offal

-0.4 0.3 -0.0 -22.1 Poultry, pork, and offal

0.6 0.6 -1.5 1.2 Oilseed products

-0.6 0.1 -13.8 -17.4 Fruits and vegetables

0.2 -0.5 2.3 -0.4 Cotton

0.3 0.2 0.5 -1.0 Oilseeds

-0.6 0.2 1.9 -5.9 Wheat

Percent change

Total Rest of world

China ASEAN

29 ©2011 Baker & McKenzie

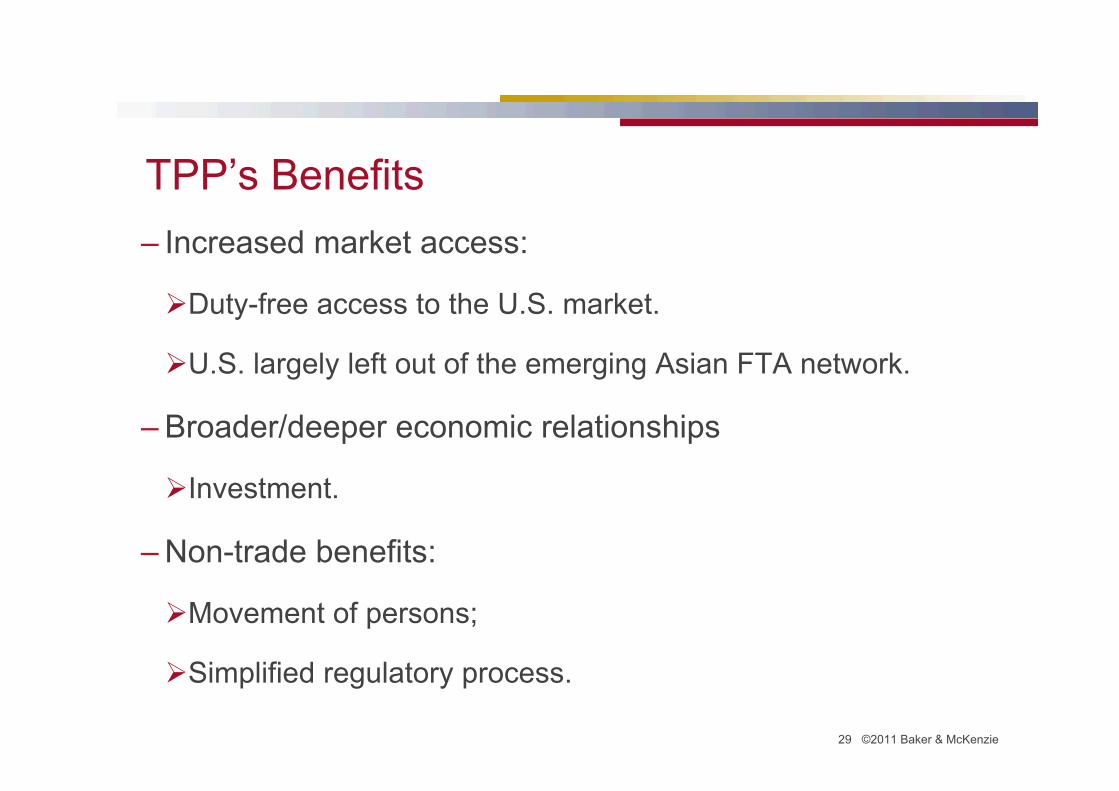

TPP’s Benefits

– Increased market access:

Duty-free access to the U.S. market.

U.S. largely left out of the emerging Asian FTA network.

– Broader/deeper economic relationships

Investment.

– Non-trade benefits:

Movement of persons;

Simplified regulatory process.

30 ©2011 Baker & McKenzie

TPP’s Challenges

– Difficult to implement:

Integration of existing FTAs;

More similar to WTO accession than ASEAN+ agreements.

– Rice and other agricultural issues:

Beef;

Dairy.

– Concerns about Malaysia and Vietnam (textiles/apparel; labor

protections, financial services, government procurement, etc.)

– Problematic U.S. Political Approval Process.

31 ©2011 Baker & McKenzie

Examples of Benefits of ASEAN and Its FTAs

32 ©2011 Baker & McKenzie

Examples of Duty Savings

2015200620052004

AFTA CEPTMFNDescriptionVietnam

0551540Microwave ovens85165000

Vietnam-ASEAN (under ASEAN FTA)

Malaysia-China (under ASEAN-China FTA)

005122034.6Homogenized composite Food Preparations: Other2104.2090

00581521Soups and broths and preparations thereof: Other2104.1090

005122028.8Other Sauces other than those of heading 2103.10.000 and 2103.20.000

2103.9010-9030

00581518Tomato Ketchup and other Tomato Sauces2103.2000

005122028Soya Sauce2103.1000

20112010200920072005MfnDescriptionHS Code

33 ©2011 Baker & McKenzie

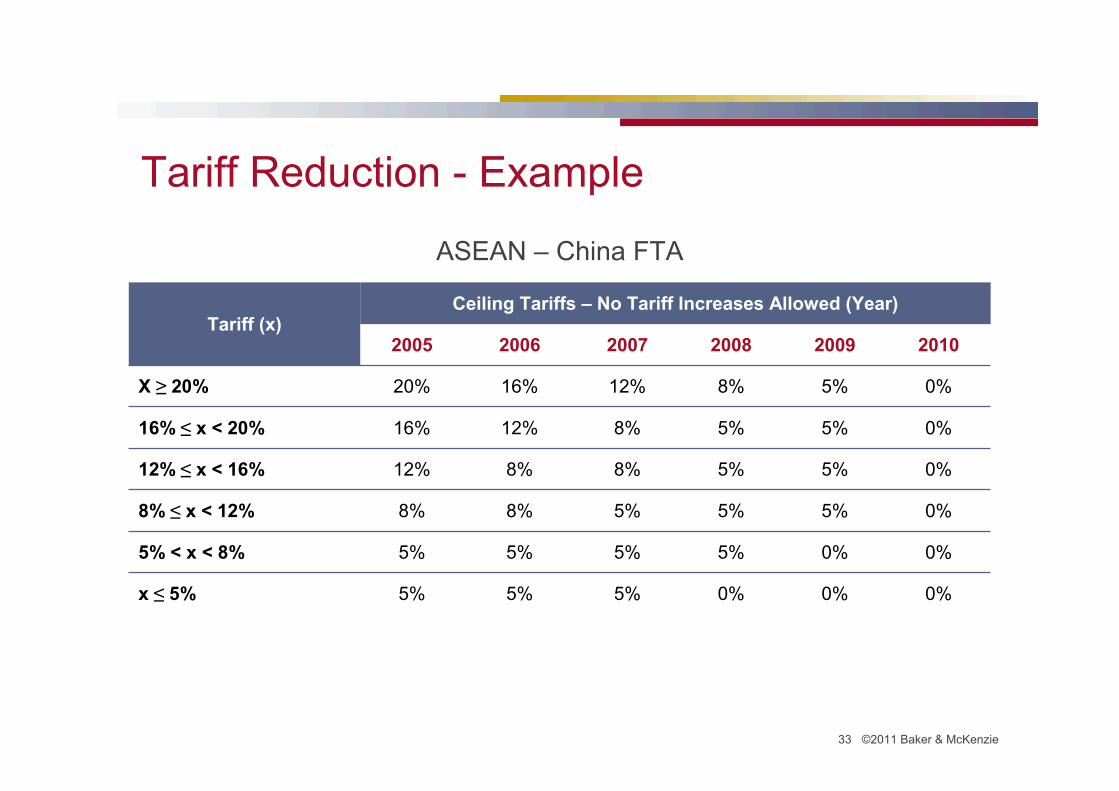

Tariff Reduction - Example

ASEAN – China FTA

0%0%0%5%5%5%x ≤ 5%

0%0%5%5%5%5%5% < x < 8%

0%5%5%5%8%8%8% ≤ x < 12%

0%5%5%8%8%12%12% ≤ x < 16%

0%5%5%8%12%16%16% ≤ x < 20%

0%5%8%12%16%20%X ≥ 20%

201020092008200720062005

Ceiling Tariffs – No Tariff Increases Allowed (Year)Tariff (x)

34 ©2011 Baker & McKenzie

The Impact of ‘Free Trade’

Cost Of Production Tpt Ins. Customs Duties Local Tpt / Distribution

Cost Of Production Tpt Ins. Customs Duties Local Tpt / Distribution

Cost Of Production Tpt Ins. Local Tpt / Distribution

1.

2.

3.

35 ©2011 Baker & McKenzie

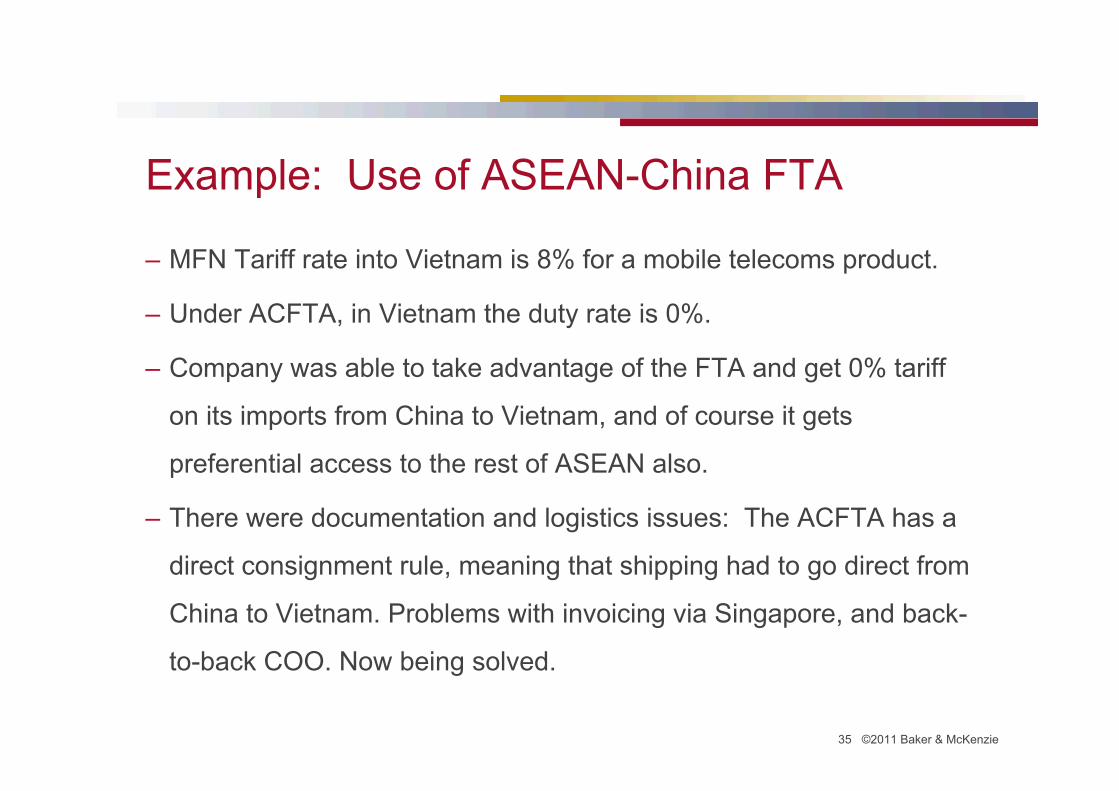

Example: Use of ASEAN-China FTA

– MFN Tariff rate into Vietnam is 8% for a mobile telecoms product.

– Under ACFTA, in Vietnam the duty rate is 0%.

– Company was able to take advantage of the FTA and get 0% tariff

on its imports from China to Vietnam, and of course it gets

preferential access to the rest of ASEAN also.

– There were documentation and logistics issues: The ACFTA has a

direct consignment rule, meaning that shipping had to go direct from

China to Vietnam. Problems with invoicing via Singapore, and back-

to-back COO. Now being solved.

36 ©2011 Baker & McKenzie

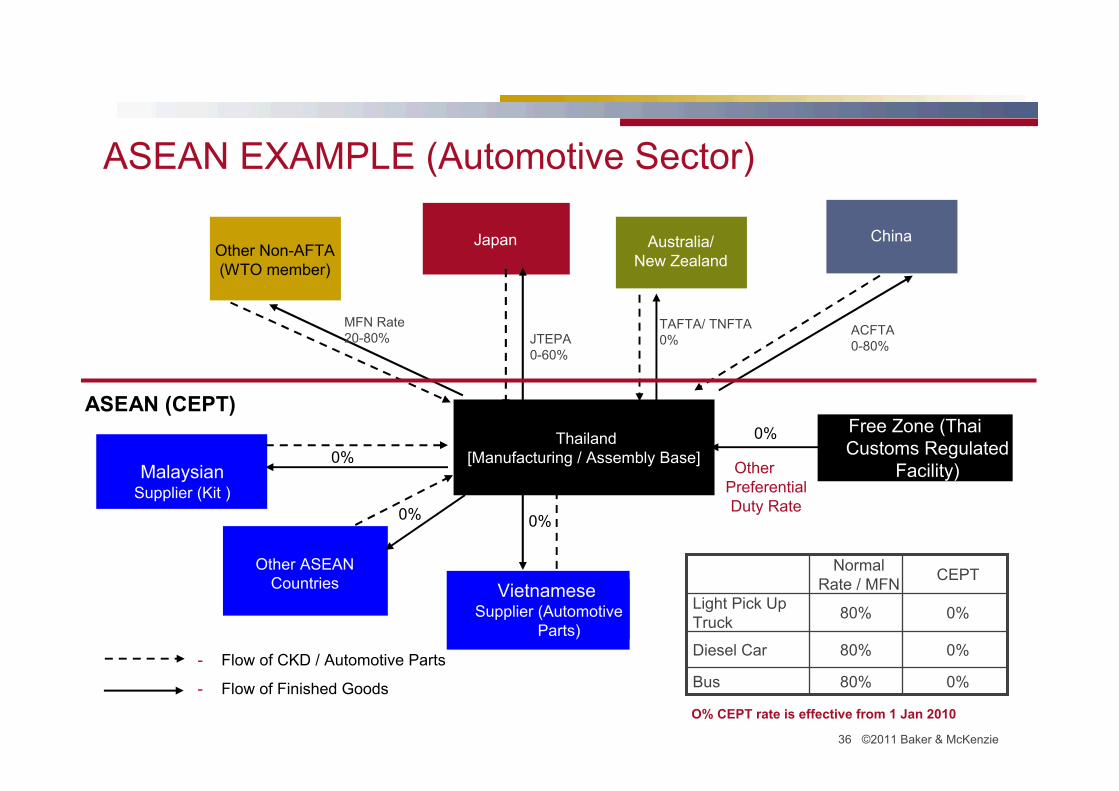

ASEAN EXAMPLE (Automotive Sector)

Thailand [Manufacturing / Assembly Base]

Malaysian Supplier (Kit )

VietnameseSupplier (Automotive

Parts)

Other ASEAN Countries

ChinaAustralia/ New Zealand

JapanOther Non-AFTA (WTO member)

0%80%Bus

0%80%Diesel Car

0%80%Light Pick Up Truck

CEPTNormal

Rate / MFN

O% CEPT rate is effective from 1 Jan 2010

- Flow of CKD / Automotive Parts

- Flow of Finished Goods

MFN Rate20-80% JTEPA

0-60%

TAFTA/ TNFTA 0%

ACFTA 0-80%

0%

0%0%

Free Zone (Thai Customs Regulated

Facility)Other Preferential Duty Rate

0%

ASEAN (CEPT)

37 ©2011 Baker & McKenzie

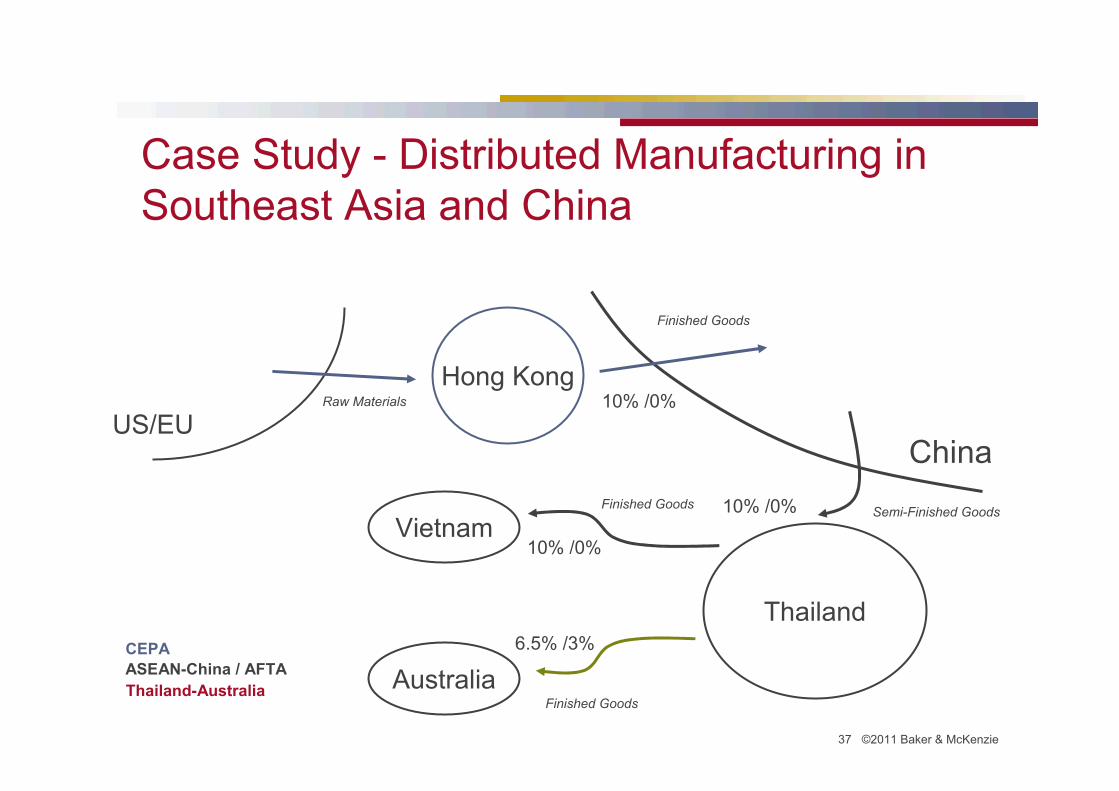

Case Study - Distributed Manufacturing in Southeast Asia and China

Thailand

China

Australia

10% /0%

6.5% /3%

Hong Kong10% /0%

US/EU

Vietnam10% /0%

Raw Materials

Finished Goods

Semi-Finished GoodsFinished Goods

Finished Goods

CEPA

ASEAN-China / AFTA

Thailand-Australia

38 ©2011 Baker & McKenzie

Utilization of FTAs and Recommendations

39 ©2011 Baker & McKenzie

Company Survey - Savings & Utilization Rates

Source: VRIENS & PARTNERS - Utilizing FTAs: Problems, Benefits & Best Practices for Companies

BMCK1

Slide 39

BMCK1 Baker & McKenzie, 11/22/2010

40 ©2011 Baker & McKenzie

FTAs: Considerable savings, but low utilization rates – WHY?

– Administration of FTAs is complicated:

Comparing MFN/ FTA tariffs by HS Code (once per year);

Examining ROO, aligning ROO with BOM (~once per year);

Preparing cost statement (~once per year);

Applying for CO, complying with other documentary requirements (every

shipment);

Accrediting manufacturing site (once).

– Information costs/ search for information.

– Time delays.

– Variety of different FTAs/ multiple ROO/ different formats.

– Education & training of staff.

41 ©2011 Baker & McKenzie

Solutions and Recommendations

– Hierarchic Responsibility.

– Functional Responsibility.

– Processes & Systems.

42 ©2011 Baker & McKenzie

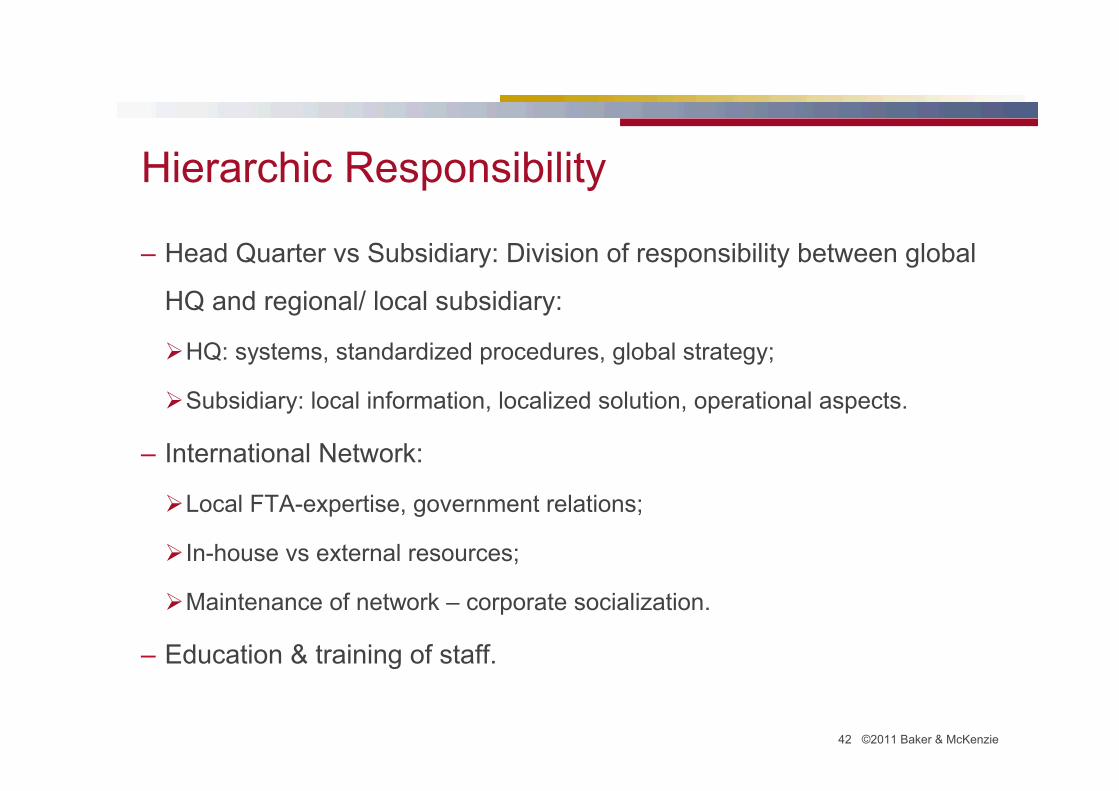

Hierarchic Responsibility

– Head Quarter vs Subsidiary: Division of responsibility between global

HQ and regional/ local subsidiary:

HQ: systems, standardized procedures, global strategy;

Subsidiary: local information, localized solution, operational aspects.

– International Network:

Local FTA-expertise, government relations;

In-house vs external resources;

Maintenance of network – corporate socialization.

– Education & training of staff.

43 ©2011 Baker & McKenzie

Functional Responsibility

• Overseeing entire supply chain.

• Analyzing impact of new and reviewed FTAs.

Source: VRIENS & PARTNERS - Utilizing FTAs: Problems, Benefits & Best Practices for Companies

44 ©2011 Baker & McKenzie

Processes and Systems

– Processes: Steps to use FTAs

1. Comparing MFN/ FTA tariffs by HS Code (once/ year);

2. Examining ROO (~once/ year);

3. Preparing cost statement (~once/ year);

4. Applying for CO, other documentary requirements (per shipment).

– Systems:

Manual: when only few different products;

Automated: when many different products.

– Automation Issues:

Programming challenges, compliance risks;

Authorized CO vs self-/ invoice declaration.

45 ©2011 Baker & McKenzie

Conclusions

46 ©2011 Baker & McKenzie

CONCLUSIONS

– ASEAN is engaging in a strong economic integration process, including:

– Internal integration – AEC, ATIGA; AFAS; ACIA;

– Entering into FTAs with key economies in the region;

– Extending FTA negotiation with other regions.

– Opportunities for ASEAN countries and FTA partners:

– Promote intra-trade with other ASEAN countries and partners;

– Opening potential markets with preferential access;

– Increase attractiveness for goods, services and FDI in the countries.

– Both opportunities and challenges to companies.

47 ©2011 Baker & McKenzie

–Any Questions?

–Thank You!

48 ©2011 Baker & McKenzie

Baker & McKenzie Vietnam Contacts:

HCMC Office

12/F, Saigon Tower

29 Le Duan Blvd.

District 1, HCMC

Vietnam

Tel: 84-8 3829-5585

Fax: 84-8 3829-5618

Hanoi Office

13/F, Vietcombank Tower

198 Tran Quang Khai St.

Hoan Kiem District, Hanoi

Vietnam

Tel: 84-4 3825-1428

Fax: 84-4 3825-1432

Website: www.bakermckenzie.com

Speaker:James Lockett,

Special Counsel, Hanoi

Baker & McKenzie Vietnam Ltd.

Tel: +84 4 3936 9397