asia pacific dailyasiaresearch.daiwacm.com/eg/cgi-bin/files/daily01apr13.pdf · profiting from...

TRANSCRIPT

Asia Pacific Daily

See important disclosures, including any required research certifications, beginning on page 51.

1 April 2013

Company Roadshows Date Company Event Venue 2 Apr Rexlot (555 HK) NDR SG 2-3 Apr CSCI (3311 HK) NDR Tokyo 5 Apr GMR Infrastructure (GMRI IN) Video Con. UK 8 Apr Lai Sun Development (488 HK) NDR HK 8 Apr Lai Sun Development (488 HK) Video Con. SG 8 Apr Lai Sun Development (488 HK) Video Con. UK 8 Apr First Financial (2892 TT) NDR SG 8 Apr Chiho Tiande (976 HK) NDR HK 8-9 Apr Shenzhen International (152 HK) NDR Tokyo 8-12 Apr Orion Corp (001800 KS) NDR US 8-16 Apr Shui On Land (272 HK) NDR US 9-10 Apr First Financial (2892 TT) NDR HK 11 Apr CR Cement (1313 HK) NDR HK 11 Apr CR Cement (1313 HK) Video Con. UK 12 Apr Wharf (4 HK) NDR HK 12 Apr Wharf (4 HK) Video Con. SG 12 Apr Wharf (4 HK) Video Con. UK 12 Apr Wharf (4 HK) Video Con. Tokyo 15-16 Apr Hopefluent (733 HK) NDR Tokyo 15-19 Apr ENN Energy (2688 HK) NDR US 16 Apr Techtronic Industries (669 HK) NDR US 16 Apr Dah Chong Hong (1828 HK) NDR SG 6-10 May KT Corp (30200 KS) NDR US 20-21 May Advanced Info Service

(ADVANC TB) NDR Tokyo

6-7 Jun Sansiri (SIRI TB) NDR SG

Daiwa Asian Events Date Company Venue 15-17 Apr Daiwa Consumer and Gaming Forum 2013 HK 22-23 May Daiwa Investment Conference London 2013 London 24 May Daiwa Investment Water Conference Zurich 28-29 May Daiwa Investment Conference NY 2013 New York 31 May Daiwa Investment Conference SF 2013 San

Francisco Source: Daiwa

Regional indices

Performance chg

(%) EPS growth

(%) PER (x)

Market 1D 1M YTD 12E 13E 12E 13E HSI (0.7) (3.1) (1.6) 9.4 8.6 10.5 9.6 HSCEI (1.2) (4.7) (4.7) 7.4 10.0 7.2 6.6 SENSEX* 0.7 (1.7) (3.0) 15.1 15.4 13.5** 11.7** KOSPI 0.0 (1.6) (0.2) 34.1 14.6 9.4 8.1 TWSE (0.3) (0.4) 2.2 37.5 12.1 14.2 13.2 FSSTI (0.1) 1.2 4.5 3.4 10.3 14.8 13.4 ASX 200 (0.6) (2.7) 6.8 (0.2) 12.0 15.4 13.8 TOPIX (0.9) 6.3 20.6 22.8 46.1 20.5 14.2 Source: Thomson Reuters *Valuation based on MSCI India **MSCI India price as of 27 Mar

Analyst Rating Page

Daiwa’s Banner Products P.2 Major changes

Bangkok Chain Hospital (BCH TB) Siriporn Arunothai

Buy P.3

New price point

Target price ↑20.2% to THB13.8 Macro research

Asia economic calendar Kevin Lai P.4

Macro preview: 1Q13 GDP and other data

Taiwan Economy Christie Chien P.6

Free economic pilot zone gets the nod

Technical Daily Comment Eiji Kinouchi P.7

Kinouchi’s Technical Tips for Institutions

Euro 4Sight Tobias S. Blattner P.9

Highlights Other research

Discovery John Choi P.12

Asia small-cap weekly

China COSCO (1919 HK) Kelvin Lau Buy P.13

Profitability upturn expected

AirChina (753 HK) Kelvin Lau Buy P.17

Expect 2013 profitability to improve

Daphne International (210 HK) Bing Zhou Outperform P.21

Operating leverage intact

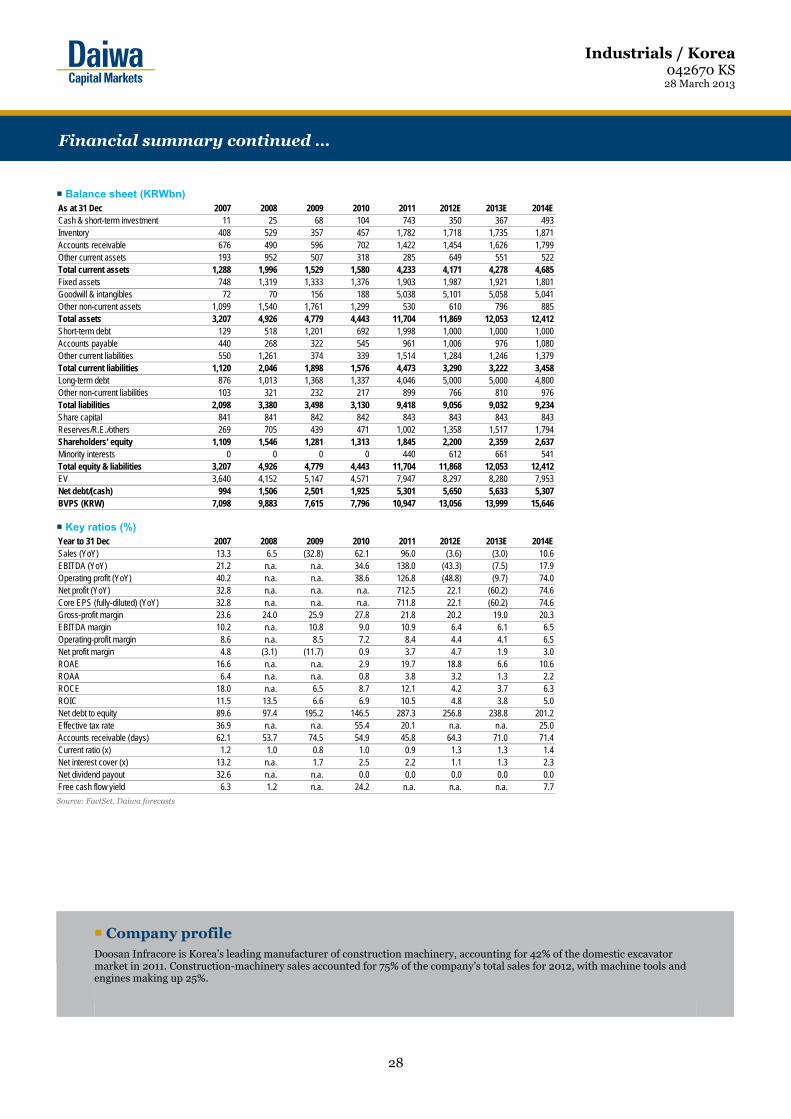

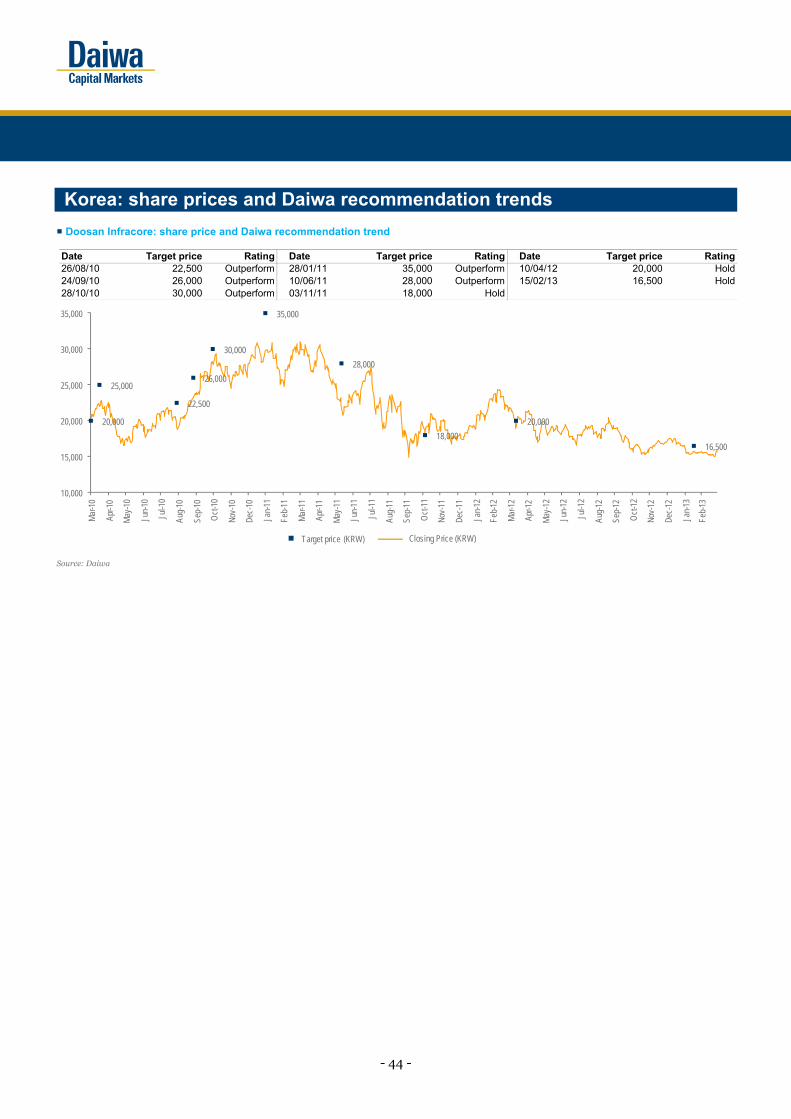

Doosan Infracore (042670 KS) Mike Oh Hold P.25

Visit: expect a YoY earnings recovery from 2H13

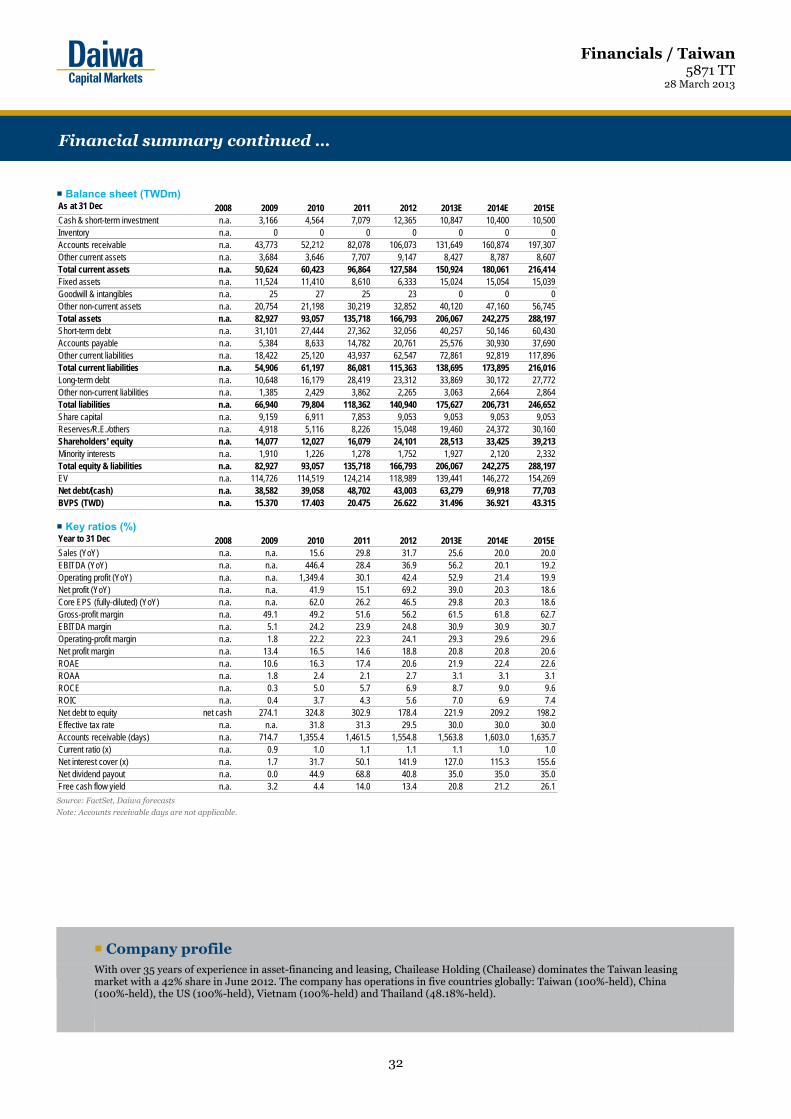

Chailease Holding (5871 TT) Rita Hsu Buy P.29

China the focus

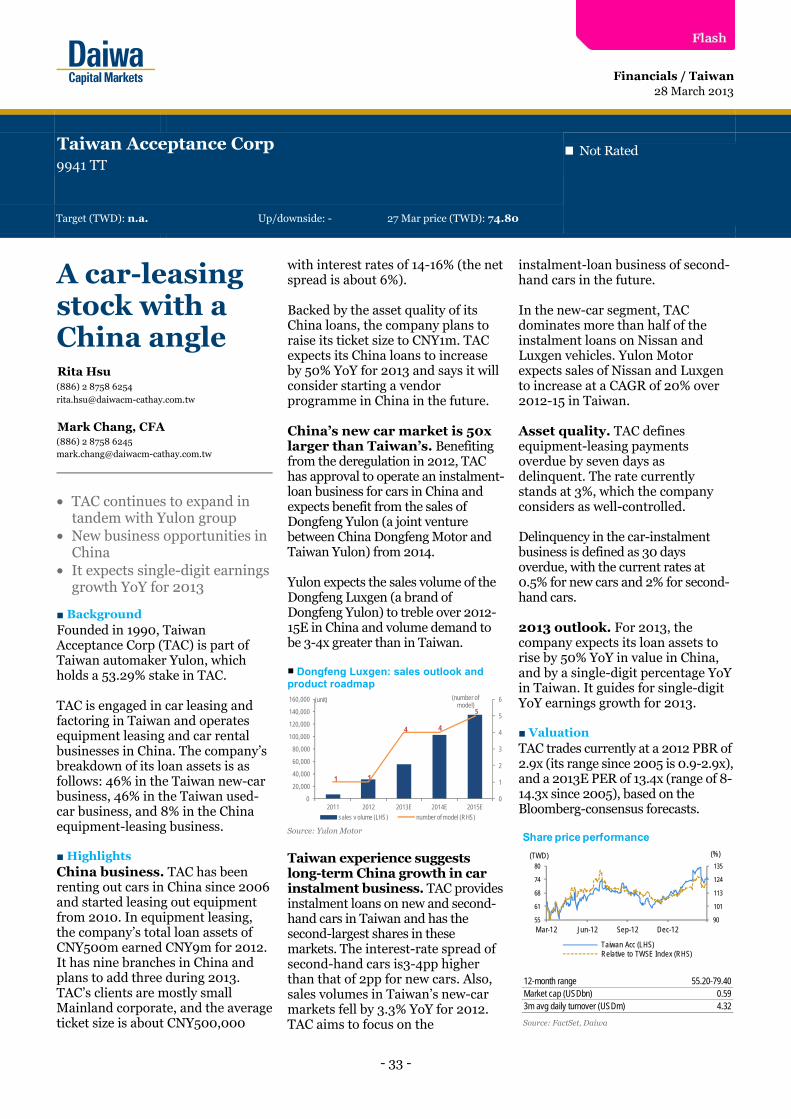

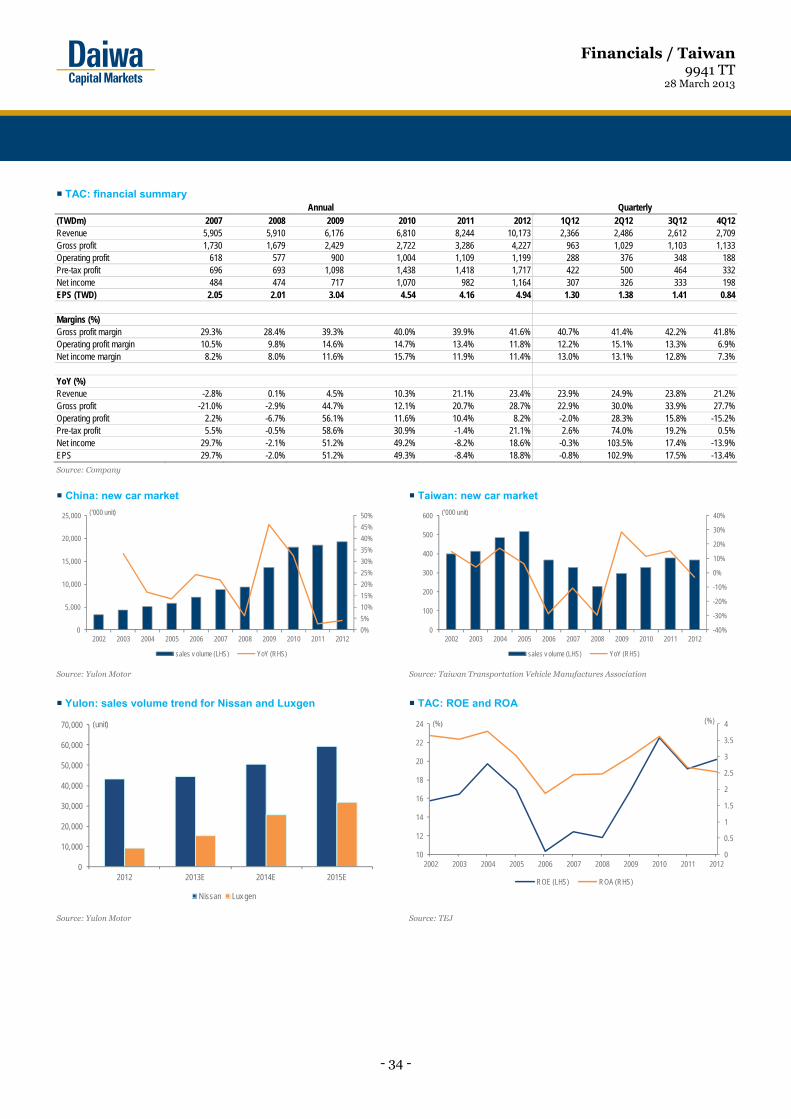

Taiwan Acceptance Corp (9941 TT) Rita Hsu Not Rated P.33

A car-leasing stock with a China angle

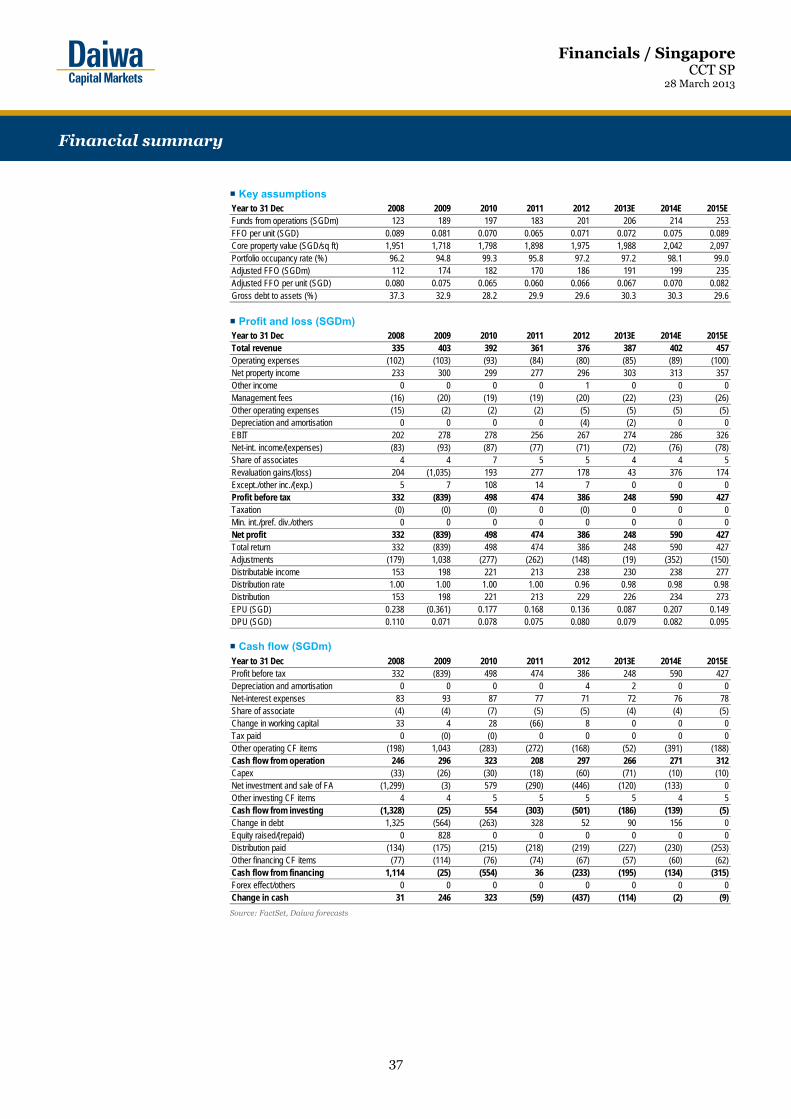

CapitaCommercial Trust (CCT SP) David Lum Hold P.35

Showcasing CapitaGreen

PTT Global Chemical (PTTGC TB) Supanna

Suwankird

Buy P.39

Tokyo NDR Feedback

Japan equity research

Capital Goods Sector Update Volume 16 Hirokazu Miyagi P.40

China research trip

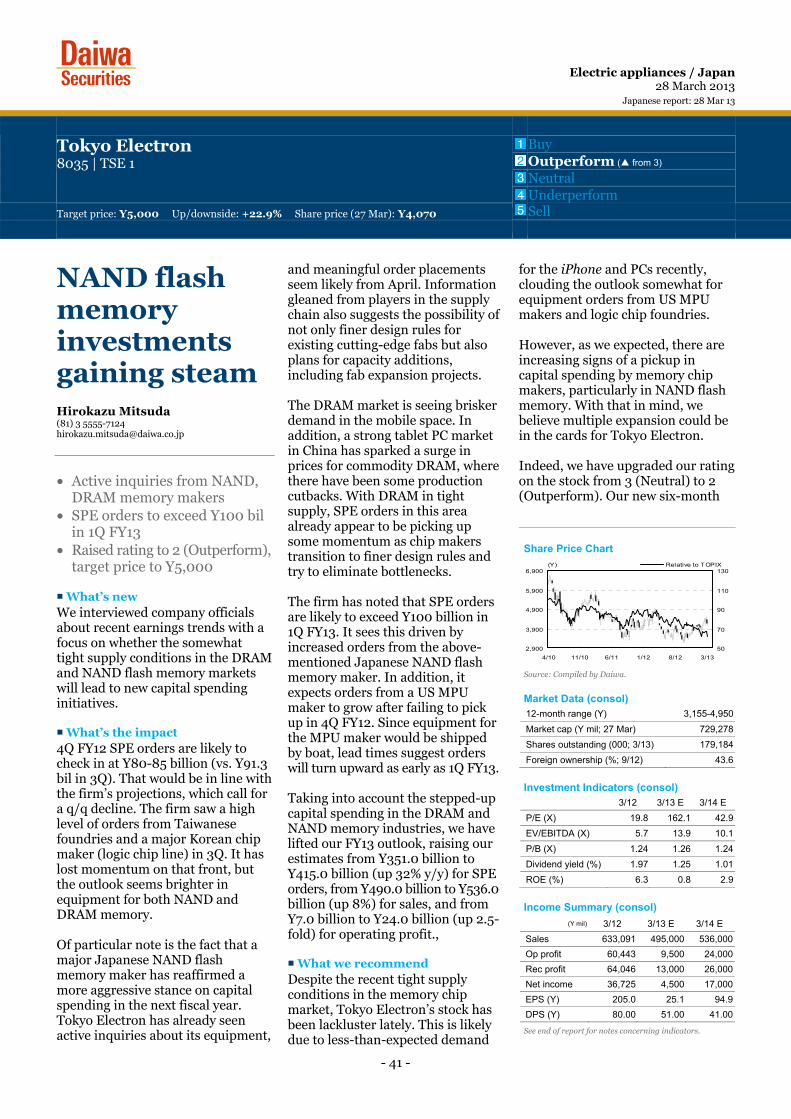

Tokyo Electron (8035 JP) Hirokazu Mitsuda 3 → Outperform

P.41

NAND flash memory investments gaining steam

Korea: share prices and Daiwa recommendation trends P.44 Analysts’ company visits P.45 Economic calendar – April 2013 P.46 Rating and target-price information P.47 Recently published reports P.47

- 2 -

Click for our latest editions

Strategy

Hong Kong &

China

Hong Kong Strategy: Is Hong Kong Inc. ready to make the jump? 22 March 2013

Integration with China promises to transform Hong Kong’s finance, property and rail sectors

Some Hong Kong companies are already reaping the rewards

We highlight 30 companies that offer exposure to six integration-related investment themes for 2013 and beyond

Jonas Kan, CFA (852) 2848 4439 ([email protected]) Grace Wu (852) 2532 4383 ([email protected]) Kelvin Lau (852) 2848 4467 ([email protected])

Capital Goods Sector

China

China Capital Goods Sector: Profiting from industry upcycles 8 March 2013

The China Capital Goods Sector has outperformed the MSCI Asia ex-Japan Index in most market upturns over the past 10 years

We highlight favourable industry cycles in the agriculture, aviation, traditional power and railway equipment sub-sectors

At the stock level, our picks are First Tractor (Outperform [2]), AviChina, Shanghai Electric, and CSR Corp (all rated Buy [1])

Joseph Ho, CFA (852) 2848 4443 ([email protected]) Dave Dai, CFA (852) 2848 4068 ([email protected]) China Research Team

Back in Form

Japan

Japan Back in Form: Abe's Three Arrows Catalysts for Change 4 March 2013

PM Abe’s three arrows: bold monetary easing, flexible fiscal policy, growth strategy to spur private-sector investment

Japan’s energy problems

Sino-Japanese relations a notable risk factor

Masahiro Kushida (81) 3 5555 7137 ([email protected]) Makoto Morita (81) 3 5555 7153 ([email protected]) Japan strategy tam / Japan equity analysts / DIR econnomist team

Real Estate Investment

Trusts

Pan Asia

Pan Asia Real Estate Investment Trusts: More acquisitions? 26 February 2013

Since the start of 2013, acquisitions, fund-raising, and acquisition appetite have accelerated in the J-REIT market

Open-market acquisitions face structural difficulties in Hong Kong and H-REITs have had to focus on asset enhancements

Investment conditions remain favourable in Singapore, with near record high prices and the likelihood of DPU and NAV-accretion

David Lum, CFA (65) 6329 2102 ([email protected]) Tomohiro Sumiya (81) 3 5555 7014 ([email protected]) Jonas Kan, CFA (852) 2848 4439 ([email protected])

Daiwa research is available electronically on Bloomberg, Reuters, Thomson One Analytics, FactSet, TMC, Capital IQ and Daiwa’s L-ZONE. Please contact your Daiwa sales representative for more information.

Daiwa’s Banner Products

Important

BUY (Unchanged) TP: Bt 13.80 (Pre XD) (From Bt 11.00 ) 28 MARCH 2013

TP : Bt 11.00 (Post XD)

Change in Numbers Upside: 16.9%

Bangkok Chain Hospital (BCH TB)

SIRIPORN ARUNOTHAI

662 – 617 4900 [email protected]

New price point

The WMC has just been officially opened and BCH plans to open another one in Pattaya to upgrade its market segmentation to a higher price point. We include all new hospitals for the next few years in our forecast. Our long-term EPS estimates are raised by 12% on average from 2016 and our TP lifted to Bt13.8; BUY.

World Medical Center officially opened The World Medical Center (WMC) which is BCH’s new price point hospital, had its grand opening late last week. This hospital is BCH’s new product line to diversify into the middle-to-high market from its existing middle-to-low market. Thanks to its prime location on Chaengwattana road close to Central Chaengwattana mall, many office buildings and communities, plus healthcare demand shifting down from premium hospitals and up from mid-tier hospitals due to higher bills at the premium end and people’s rising incomes, we expect WMC to succeed in the longer term but it may make losses in the first two years of operation which we already factored into our previous projection.

Earnings upgrade reflects future expansion Besides the WMC, BCH plans to open another WMC in Pattaya with capacity of 200-250 beds. In addition, BCH plans a 250-300-bed hospital on Ramkhamhaeng road under the Kasemrad brand and a 100-bed new building at Kasemrad Sriburin Hospital in Chiang Rai to serve expected rising demand. BCH needs around Bt3.0bn-3.5bn for all the new projects (excluding land which is already secured) and plans to finance them using internal cash flow and debt. We factor in all of these new projects in our projection. Our earnings forecasts are lowered by 1-2% in 2013-15 but we raise our estimates from 2016 onwards by 12% on average.

Short-term earnings are less exciting We project BCH’s earnings to slow in the next few years due to some loss contribution from new hospitals and its new building in the early years of their operations. However, we expect strong operations of six Kasemrad hospitals at Prachachuen, Sukhapiban 3, Bangkae, Rattanatibeth, Saraburi and Sriburin and for this to be enough to offset losses from new hospitals and still allow EPS growth of 7%, 14% and 9% in 2013-15, respectively compared to 36% EPS growth in 2012. BCH’s growth drivers at existing hospitals are cash patient numbers growing by 3-8% p.a., billing per cash patient rising 4% p.a. and gross margin forecast to fatten to 39.4-39.5% in 2013-15 from 39.2% in 2012.

Reaffirm BUY with new TP of Bt13.8/share Given our earnings upgrade to reflect its capacity expansion, our 12-month DCF-based TP is raised from Bt11.0/share to Bt13.8. Despite uninspiring forecast EPS growth in the next few years, we see limited downside risk to our earnings projections for BCH, supported by our expectation for rising demand and limited supply in the healthcare industry as well as BCH’s strong competitiveness versus peers. We reaffirm our BUY call.

Please see the important notice on the back page

COMPANY VALUATION

Y/E Dec (Bt m) 2012A 2013F 2014F 2015F

Sales 4,466 5,356 5,866 6,679

Net profit 910 970 1,102 1,203

Consensus NP ⎯ 937 1,078 1,126

Diff frm cons (%) ⎯ 3.5 2.2 6.9

Norm profit 910 970 1,102 1,203

Prev. Norm profit ⎯ 982 1,118 1,230

Chg frm prev (%) ⎯ (1.2) (1.4) (2.2)

Norm EPS (Bt) 0.5 0.5 0.6 0.6

Norm EPS grw (%) 36.3 6.5 13.7 9.1

Norm PE (x) 25.9 24.3 21.4 19.6

EV/EBITDA (x) 16.4 14.3 13.1 12.0

P/BV (x) 6.5 5.7 5.1 4.6

Div yield (%) 1.5 2.5 2.8 3.1

ROE (%) 26.6 25.0 25.3 24.8

Net D/E (%) 36.6 29.9 23.2 22.0

PRICE PERFORMANCE

COMPANY INFORMATION

Price as of 28-Mar-13 (Bt) 11.80

Market cap (US$ m) 792.4

Listed shares (m shares) 1,995.0

Free float (%) 26.4

Avg daily turnover (US$ m) 3.1

12M price H/L (Bt) 13.7/7.5

Sector Healthcare

Major shareholder Harnphanich Family 49.9%

Sources: Bloomberg, Company data, Thanachart estimates

6

8

10

12

14

M ar-12 Jul-12 Nov-12 M ar-13

(Bt /shr)

(10)

0

10

20

30

40

50

(%)BCH Rel to SET Index

Th

an

ach

art

Sec

uri

ties

Th

an

ach

art

Sec

uri

ties

- 4 -

■ Summary As China’s recovery remains on track, it continues to extract sizable surpluses from its neighbours. This trend suggests that the positive spillover of this recovery has been less exciting than previous episodes. Some demand disappointment for the region may be inevitable, in our view.

■ Fundamentals 1Q13 GDP: There are four GDP releases in April. China’s cyclical uptrend looks to be on track. We expect GDP growth to pick up further to 8.1% YoY for 1Q13, on stronger exports. For the rest of Asia, the positive spillover of China’s recovery seems to be less exciting this time round, however, as China’s import demand has been quite soft for numerous reasons as discussed in our report, QE uncertainty, China’s import shortfall and other crosswinds, 26 March 2013. We see potential GDP disappointment for economies more exposed to these challenges. Especially for Korea, which is very dependent on China, as its economy is already weighed down by ongoing Yen depreciation and domestic-demand sluggishness. With the help of a low base, however, we look for 1Q13 GDP to be up 2.3% YoY. Similarly for Singapore, a range of indicators including exports, retail sales and industrial production have taken a big hit. Much of the regional export recovery has been led by a surge in smartphone demand but Singapore is unable to benefit as it is more specialised in other types of

electronics such as PCs and ICs. For 2M13, electronics exports were still down by 16.8% YoY. We look for 1Q13 GDP growth to be just 0.3% YoY. Interest rate decision: Korea’s GDP growth has been lacklustre and well below its potential level. CPI inflation has eased further from 1.7% YoY for 4Q12 to 1.5% YoY for 2M13. We believe the pressure is on the BOK again to deliver another 25bps interest-rate cut in their next meeting on 11 April. After that, we expect it to stay on hold again for the rest of the year. Otherwise, we do not expect any actions from ASEAN central banks in April, given both growth and inflation dynamics remain in a fine balance. China’s imports from Asia: Trade data for Korea, Taiwan and Hong Kong should be interesting to watch as the data for the first two months was somewhat distorted by the different timing of the Lunar New Year holiday. As a result, the trade data for March should be more telling. In particular, if China’s import demand for Asian goods continues to disappoint, there will be a legitimate cause for concern, in our view.

■ GDP growth

■ Korea: CPI inflation and policy rate

Source: CEIC, Daiwa forecasts Source: CEIC, Daiwa

7.9

3.7

1.5 1.5

8.1

3.2

2.3

0.3

0

1

2

3

4

5

6

7

8

9

China Taiwan Korea Singapore

4Q12 1Q13E

(% YoY)

0

1

2

3

4

5

6

Feb-

06

Aug-

06

Feb-

07

Aug-

07

Feb-

08

Aug-

08

Feb-

09

Aug-

09

Feb-

10

Aug-

10

Feb-

11

Aug-

11

Feb-

12

Aug-

12

Feb-

13

CPI, YoY % Policy rate

(%)

28 March 2013

Asia economic calendar

Macro preview: 1Q13 GDP and other data

• China’s GDP growth looks set to pick up further to 8.1%

• Its Asian neighbours, however, could disappoint

• BOK should be under pressure to deliver a 25bps cut in April

Economy / Asia ex Japan

Kevin Lai(852) 2848 [email protected]

Christie Chien(852) 2848 [email protected]

Economy / Asia ex Japan 28 March 2013

- 5 -

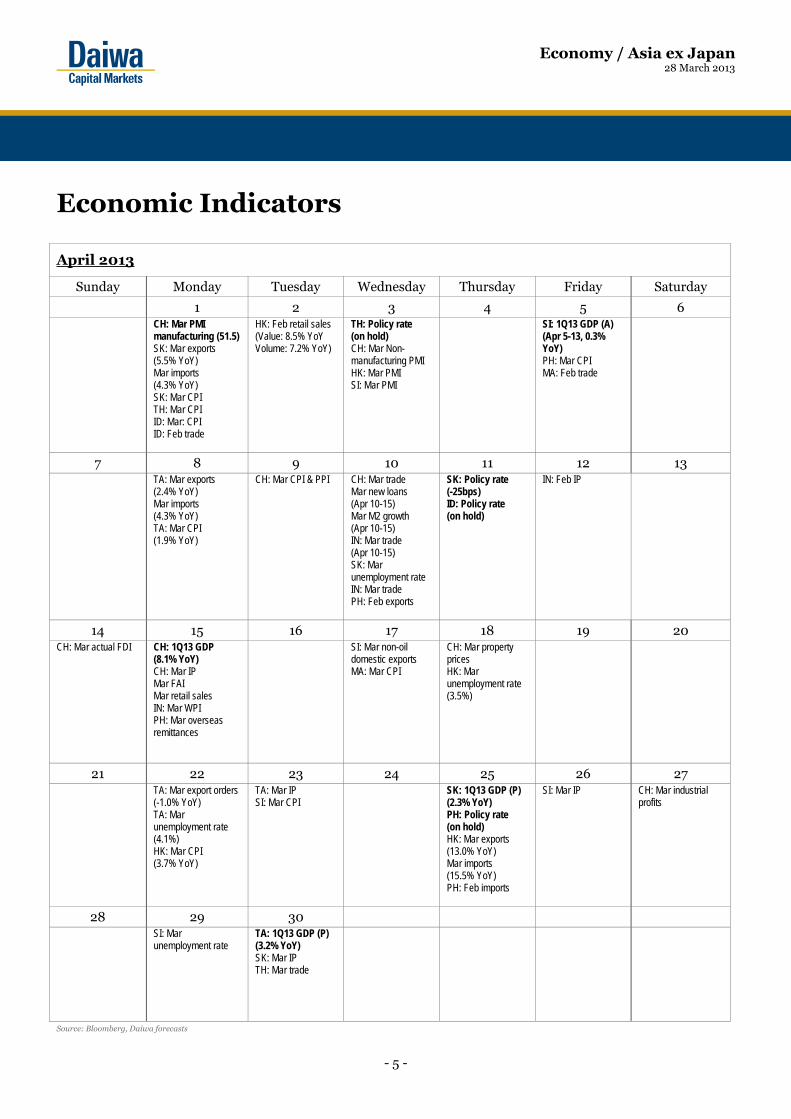

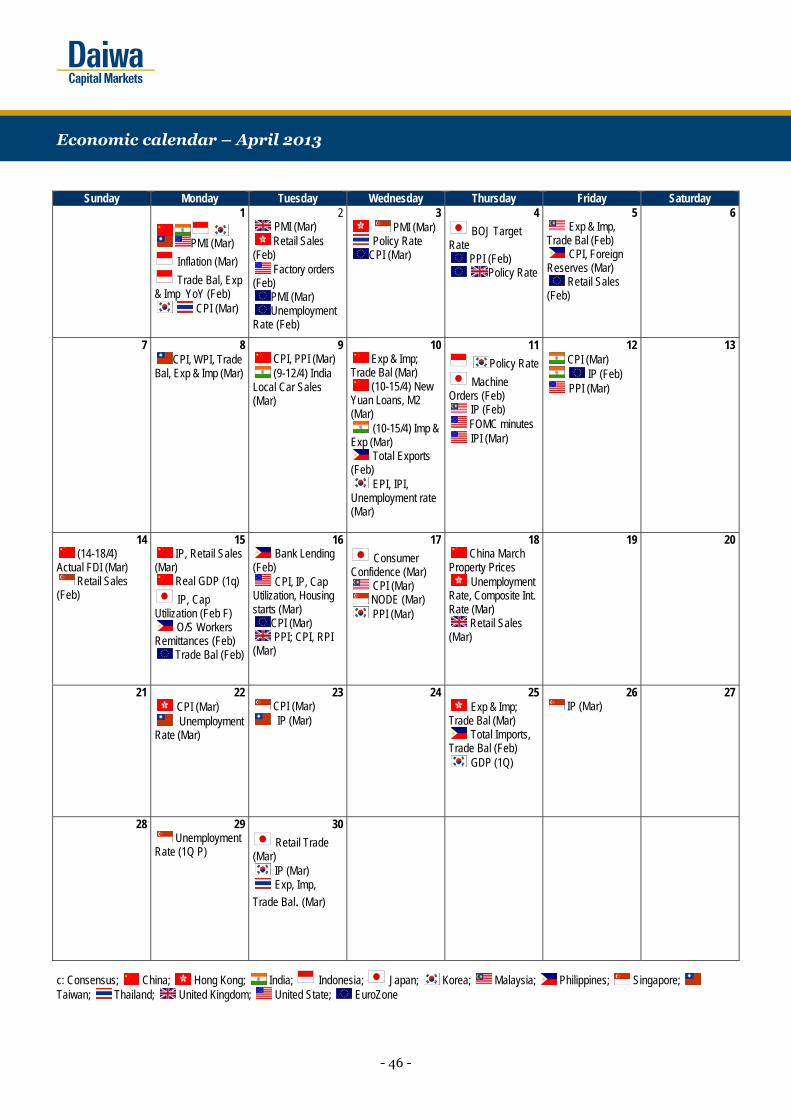

Economic Indicators

April 2013

Sunday Monday Tuesday Wednesday Thursday Friday Saturday

1 2 3 4 5 6

CH: Mar PMI manufacturing (51.5) SK: Mar exports (5.5% YoY) Mar imports (4.3% YoY) SK: Mar CPI TH: Mar CPI ID: Mar: CPI ID: Feb trade

HK: Feb retail sales (Value: 8.5% YoY Volume: 7.2% YoY)

TH: Policy rate(on hold) CH: Mar Non-manufacturing PMI HK: Mar PMI SI: Mar PMI

SI: 1Q13 GDP (A) (Apr 5-13, 0.3% YoY) PH: Mar CPI MA: Feb trade

7 8 9 10 11 12 13 TA: Mar exports

(2.4% YoY) Mar imports (4.3% YoY) TA: Mar CPI (1.9% YoY)

CH: Mar CPI & PPI

CH: Mar trade Mar new loans (Apr 10-15) Mar M2 growth (Apr 10-15) IN: Mar trade (Apr 10-15) SK: Mar unemployment rate IN: Mar trade PH: Feb exports

SK: Policy rate(-25bps) ID: Policy rate (on hold)

IN: Feb IP

14 15 16 17 18 19 20 CH: Mar actual FDI

CH: 1Q13 GDP (8.1% YoY) CH: Mar IP Mar FAI Mar retail sales IN: Mar WPI PH: Mar overseas remittances

SI: Mar non-oil domestic exports MA: Mar CPI

CH: Mar property prices HK: Mar unemployment rate (3.5%)

21 22 23 24 25 26 27 TA: Mar export orders

(-1.0% YoY) TA: Mar unemployment rate (4.1%) HK: Mar CPI (3.7% YoY)

TA: Mar IP SI: Mar CPI

SK: 1Q13 GDP (P)(2.3% YoY) PH: Policy rate (on hold) HK: Mar exports (13.0% YoY) Mar imports (15.5% YoY) PH: Feb imports

SI: Mar IP

CH: Mar industrial profits

28 29 30 SI: Mar

unemployment rate

TA: 1Q13 GDP (P)(3.2% YoY) SK: Mar IP TH: Mar trade

Source: Bloomberg, Daiwa forecasts

- 6 -

■ Summary On 27 March, the cabinet released the blueprint for its free economic pilot zone, which we see as the most ambitious plan to promote the liberalisation of trade and upgrade the industrial value chain in recent years. ■ Fundamentals Taiwan Vice-Premier Mao Chih-Kuo said the aim of the zone is to boost economic growth through further economic and trade liberalisation. The plan sets out two stages for the implementation of the zone. The first will focus on expanding the existing free trade zone (covering five ports and one airport zone) to boost economic growth. Easing regulations on hiring foreign workers is also a highlight (skilled foreign workers no longer need to have two years’ work experience before applying for a working visa in

Taiwan). Qualified Mainlanders can now apply for a three-year multiple visa. Meanwhile, there are no longer limitations on Mainland investment in the zone’s manufacturing sector, as long as the industry itself is not related to national security. This is a big step forward, in our view, as it opens the door for more cross-strait industrial strategic alliances. The second stage aims to give better terms to foreign investors than currently provided for under the WTO. It plans to give tax breaks to foreign workers and residency rights to Mainlanders who need to work in the zone. Stage one will likely be implemented in July 2013, while changes to Taiwan law are needed for stage two, which means the Legislative Yuan will be involved. Even though there is a high risk that the Legislative Yuan will reduce the proposed tax benefits, and narrow the scale of liberalisation and the proposed relaxation of certain regulations, the plan itself shows the Taiwan Government’s determination to embrace free trade. We regard this as a step in the right direction to prepare Taiwan for further Trans-Pacific Strategic Economic Partnership (TPP) talks. Foreign investment in Taiwan has been sluggish in recent years, as shown by the growing deficit in its direct investment balance. While we hope the free trade zone will be a watershed, it remains to be seen whether such a scheme could be eventually successfully applied to the whole island.

■ Balance of payments: net direct investment into Taiwan

Source: CEIC, Daiwa

If the zone is successfully implemented, we believe Taiwan will have the edge regionally in being able to attract foreign investment, even despite fierce competition from other Asian economies. Taiwan could even become the gateway for foreign investors looking to play the China market. In addition, we believe Taiwan has a strong manufacturing base with the ability to innovate. This is attractive to investors. ■ Taiwan: unit labour cost index

Source: CEIC, Daiwa

Over the near term, however, the upside to GDP growth may be limited. We are leaving our real GDP growth forecast unchanged at 3% YoY for 2013.

(16)

(14)

(12)

(10)

(8)

(6)

(4)

(2)

0

2

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

(USD bn)

7580859095

100105110

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

2011

(1990=100)

28 March 2013

Taiwan Economy

Free economic pilot zone gets the nod

• First stage of the zone will be set up in 2H13

• More relaxed regulations on hiring and more favourable investment terms highlighted

• A long-term positive but limited near-term upside

Economy / Taiwan

Christie Chien(852) 2848 [email protected]

Kevin Lai(852) 2848 [email protected]

- 7 -

Eiji Kinouchi (81) 3 5555-7230 [email protected] Hikaru Sato (81) 3 5555-7330 [email protected]

Slight setback at opening

The Tokyo stock market opened slightly below the flat line, probably due to fears over a possible change in foreign investors’ stance on Japanese shares. Japan’s Ministry of Finance released International Transactions in Securities before the opening this morning. The data shows nonresidents were net sellers of Japanese equities worth Y267.6 billion on the week ended 23 March. Also, buy orders placed by foreign brokers before the opening

reportedly outweighed sell orders only modestly compared with recent strong buying interest. The news apparently added to concerns. Given the turmoil in Cyprus last week, we fear that European investors may have changed their investment stance. Japanese shares broadly faced a slight setback, except for electric utilities, telecommunications, and Internet plays. Euro/yen below 52W MA, European

banks below recent range The euro/dollar rate fell to the 1.270-1.279 range, below the key support level of the 52-week moving average (see chart). Given the roughly 18-month cycle in the currency exchange rate, the euro could remain weak in 2013 if it stays below the moving average (see chart).

We think a modest decline below the key level does not necessarily suggest that the above-noted scenario will materialize. Still, we should remain cautious until around the ECB Governing Council meeting on 4 April. Furthermore, shares of European banks (not only those in southern Europe but also those in countries with solidest finances) have increasingly fallen below their six-month trading ranges at higher levels. With this in mind, we need to stay alert at least over the short term. At the same time, we expect selling pressure from pension funds to ease early in the new fiscal year. Tighter bank regulations warrant

caution Visibility is murky on banking-sector regulations, with the deposit

Technical analysis / Japan

28 March 2013Japanese report: 28 Mar 13

Kinouchi’s Technical Tips for Institutions

Technical Daily Comment

• Tokyo opened lower; watch for possible impact of G20

Source: Bloomberg; compiled by Daiwa.

1/41.184

10/151.089

1/50.957 9/20

0.928

7/161.012

5/291.191

2/171.284

12/301.364

9/51.254

5/121.293

12/41.334

4/221.599

11/251.513

11/41.421

5/21.483

2/11.364

1.0147/14

0.8905/4

0.82710/25

0.8367/5

0.8591/31

1.0819/2

1.1825/13

1.1907/4 1.167

11/16

1.24511/20 1.192

6/7

1.2911/7 1.267

1/161.2067/24

1.2783/27

0.7

0.8

0.9

1

1.1

1.2

1.3

1.4

1.5

1.6

1.7

23 mos.20 mos.

19 mos.

23 mos.

16 mos.

19 mos.

18 mos.

21 mos.$/€(weekly; 52W MA)

99 00 01 02 03 04 05 06 07 08 09 10 11 12 13

Prospectivetrend

52W MA simulatedassuming constantvalue at current level

($/€)

Technical Daily Comment

28 March 2013

- 8 -

haircut expected in Cyprus and the separation called for commercial and investment banking operations. A change in bank regulations tends to have a meaningful impact on European brokers’ open positions in Nikkei 225 futures. They started to close out their positions ahead of the introduction of tighter capital requirements and the Greek election in June 2012, and the Nikkei Stock Average began pulling back. This time, we think European brokers will start to reduce open positions around September with an eye on the January 2014 application of Basel III requirements in the region. As such, deleveraging appears unlikely anytime soon. In our view, however, the 18-19 April meetings of G20 finance ministers and central bank governors warrant attention as they could temporarily spur position squaring by European brokers. (Comment following opening of morning session—28 March 2013)

Translation: K.T. Style check: K.R. Accuracy check: K.T.

- 9 -

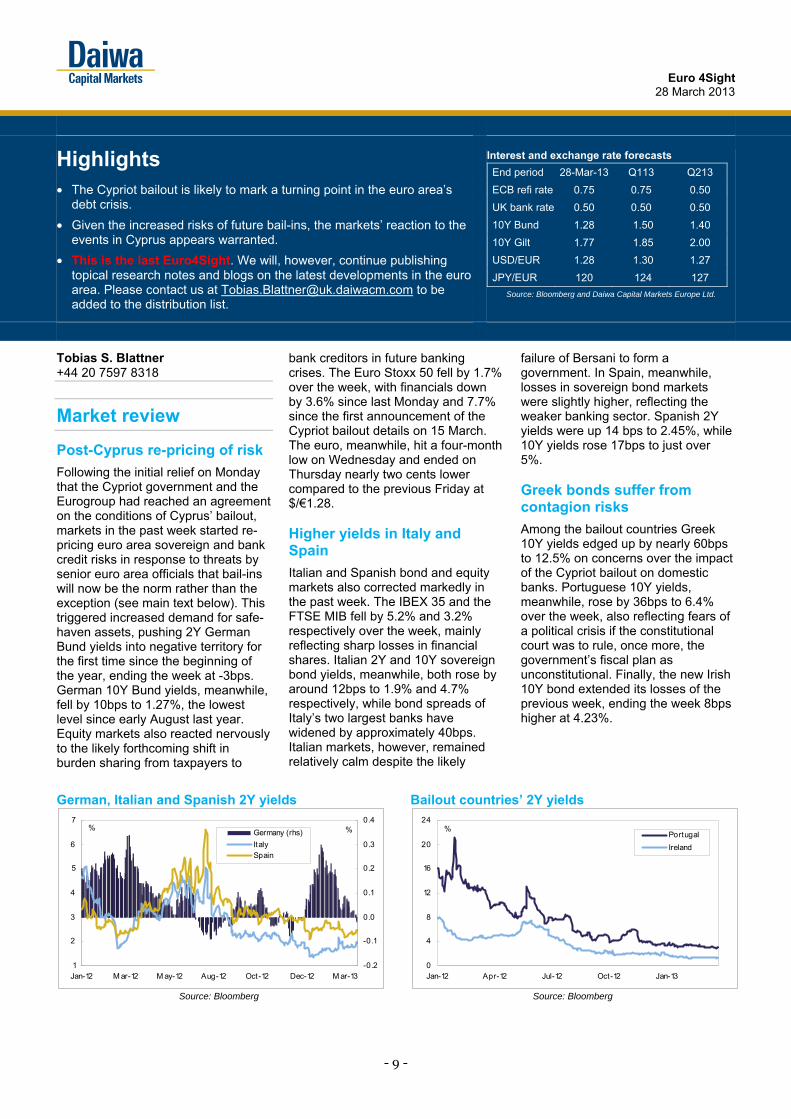

Tobias S. Blattner +44 20 7597 8318

Market review

Post-Cyprus re-pricing of risk

Following the initial relief on Monday that the Cypriot government and the Eurogroup had reached an agreement on the conditions of Cyprus’ bailout, markets in the past week started re-pricing euro area sovereign and bank credit risks in response to threats by senior euro area officials that bail-ins will now be the norm rather than the exception (see main text below). This triggered increased demand for safe-haven assets, pushing 2Y German Bund yields into negative territory for the first time since the beginning of the year, ending the week at -3bps. German 10Y Bund yields, meanwhile, fell by 10bps to 1.27%, the lowest level since early August last year. Equity markets also reacted nervously to the likely forthcoming shift in burden sharing from taxpayers to

bank creditors in future banking crises. The Euro Stoxx 50 fell by 1.7% over the week, with financials down by 3.6% since last Monday and 7.7% since the first announcement of the Cypriot bailout details on 15 March. The euro, meanwhile, hit a four-month low on Wednesday and ended on Thursday nearly two cents lower compared to the previous Friday at $/€1.28. Higher yields in Italy and Spain

Italian and Spanish bond and equity markets also corrected markedly in the past week. The IBEX 35 and the FTSE MIB fell by 5.2% and 3.2% respectively over the week, mainly reflecting sharp losses in financial shares. Italian 2Y and 10Y sovereign bond yields, meanwhile, both rose by around 12bps to 1.9% and 4.7% respectively, while bond spreads of Italy’s two largest banks have widened by approximately 40bps. Italian markets, however, remained relatively calm despite the likely

failure of Bersani to form a government. In Spain, meanwhile, losses in sovereign bond markets were slightly higher, reflecting the weaker banking sector. Spanish 2Y yields were up 14 bps to 2.45%, while 10Y yields rose 17bps to just over 5%. Greek bonds suffer from contagion risks

Among the bailout countries Greek 10Y yields edged up by nearly 60bps to 12.5% on concerns over the impact of the Cypriot bailout on domestic banks. Portuguese 10Y yields, meanwhile, rose by 36bps to 6.4% over the week, also reflecting fears of a political crisis if the constitutional court was to rule, once more, the government’s fiscal plan as unconstitutional. Finally, the new Irish 10Y bond extended its losses of the previous week, ending the week 8bps higher at 4.23%.

German, Italian and Spanish 2Y yields Bailout countries’ 2Y yields

Source: Bloomberg Source: Bloomberg

1

2

3

4

5

6

7

Jan-12 M ar-12 M ay-12 Aug-12 Oct-12 Dec-12 M ar-13-0.2

-0.1

0.0

0.1

0.2

0.3

0.4

Germany (rhs)

Italy Spain

% %

0

4

8

12

16

20

24

Jan-12 Apr-12 Jul-12 Oct-12 Jan-13

Portugal

Ireland

%

Euro 4Sight

28 March 2013

Highlights • The Cypriot bailout is likely to mark a turning point in the euro area’s

debt crisis.

• Given the increased risks of future bail-ins, the markets’ reaction to the events in Cyprus appears warranted.

• This is the last Euro4Sight. We will, however, continue publishing topical research notes and blogs on the latest developments in the euro area. Please contact us at [email protected] to be added to the distribution list.

Interest and exchange rate forecasts

End period 28-Mar-13 Q113 Q213

ECB refi rate 0.75 0.75 0.50

UK bank rate 0.50 0.50 0.50

10Y Bund 1.28 1.50 1.40

10Y Gilt 1.77 1.85 2.00

USD/EUR 1.28 1.30 1.27

JPY/EUR 120 124 127

Source: Bloomberg and Daiwa Capital Markets Europe Ltd.

Euro 4Sight 28 March 2013

- 10 -

Review & Outlook

Markets started re-pricing risks…

The Cypriot bailout is likely to mark a new turning point in the euro area’s debt crisis. Akin to the declaration of Deauville in October 2010, when German Chancellor Merkel and then French President Sarkozy first threatened private creditors with losses in future rescue packages, post-Cyprus bailout comments by Eurogroup Chairman Dijsselbloem (and others) sent a strong signal to markets that bail-ins of bank creditors will now be the norm rather than the exception. As we argued last week, bailing-in bank creditors is not inappropriate per se. But it is dangerous when the banking sector as a whole remains fragile and funding remains constrained. Market developments over the past few days have clearly highlighted these risks. Since the Eurogroup announcement of the details of the Cypriot bailout deal on 15 March, European banks’ generic 5Y CDS index has risen by more than 35% to its highest level since October last year. European financial CDS index

Source: Bloomberg and Daiwa Capital Markets Europe Ltd.

…intensifying the pressure on bank funding

Similarly, financing costs for banks in the periphery have also risen sharply since the decision to bail-in depositor in Cyprus. Bond spreads of Italy’s two largest banks have widened by approximately 40bps and by as much as 80bps for more vulnerable second-tier banks in Italy, Portugal and elsewhere in the periphery. This will not only put further upward pressure on bank lending rates, but also aggravate peripheral banks’ already strained market access. Indeed, a continuation of the recent successful bond market returns of many peripheral banks seems unlikely. Moreover, downward pressure on deposits is likely to increase too in coming months, further adding to peripheral banks’ funding constrains. With household net disposable income expected to decline, on average, by around 2%Y/Y this and next year, negatively affecting savings rates, deposit growth will slow considerably or remain negative in the periphery in the foreseeable future. And having seen what's happened in Cyprus, depositors will now be much more careful about where they put their

money for fear that it will be frozen or, even worse, expropriated. …and hence bank lending…

But the ramifications are broader than this. With funding pressure on peripheral banks intensifying, their dependency on cheap ECB liquidity is bound to increase. This comes amid pressure on banks in Portugal and Spain to lower their reliance on ECB liquidity as part of their respective adjustment programmes, substantially aggravating the required deleveraging process in these economies. Portuguese banks, for example, are required to lower their loan-to-deposit ratio to 120% by end-2014, from currently close to 150%. Of course, all of this will contribute to deepen the credit crunch in the periphery, choking economic recovery. The latest ECB data released today highlight the scale of the problem. In February, compared to a year earlier, loans to non-financial companies were down by 12% in Spain, and by 8% in Portugal, crushing investment. And in light of the renewed deterioration in business sentiment amid the broad-based return of political uncertainty, downside risks to the euro area’s growth outlook have clearly increased in recent weeks. Euro area: Loans to non-financial corporations

Source: Datastream

…thereby affecting sovereign spreads too

This has not left sovereign bond spreads unaffected. Although a stronger focus on private sector involvement (PSI) should arguably have reduced the potential bailout costs of weak sovereigns in the absence of a true banking union, Italian and Spanish 10Y sovereign bond spreads edged up by around 30bps in the past few days and by 50bps in Portugal. Indeed, if the Cypriot bailout creates a precedent, which we think it does, the risks of a restructuring, sovereign or otherwise, have clearly increased in the periphery. Even if a sizable share of creditors are non-residents as in the case of Cyprus, any decision ultimately to go down the PSI route in Spain, Italy or Portugal would almost certainly go hand-in-hand with a deeper recession and a steeper rise in the debt-to-GDP ratio than otherwise would be the case. Moreover, if accompanied by eye-watering fiscal consolidation, which seems likely to be the norm in the euro area, bail-ins

100

150

200

250

300

350

400

Jan-11 Apr-11 Jul-11 Oct-11 Jan-12 Apr-12 Jul-12 Oct-12 Jan-13

bps

Draghi's pledge tosave the euro

ECB announces

LTROs

-15

-10

-5

0

5

10

15

20

25

Jan-08 Jan-09 Jan-10 Jan-11 Jan-12 Jan-13

Euro area Italy

Portugal Spain

% , Y/Y

Euro 4Sight 28 March 2013

- 11 -

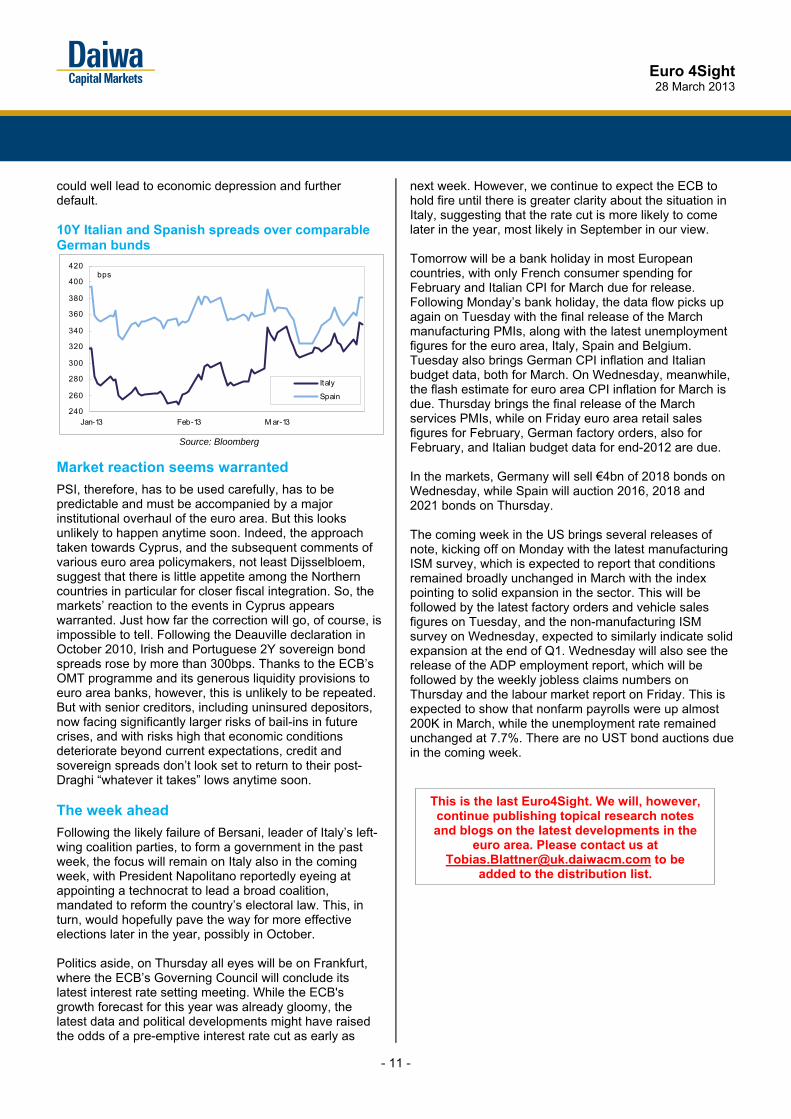

could well lead to economic depression and further default. 10Y Italian and Spanish spreads over comparable German bunds

Source: Bloomberg

Market reaction seems warranted

PSI, therefore, has to be used carefully, has to be predictable and must be accompanied by a major institutional overhaul of the euro area. But this looks unlikely to happen anytime soon. Indeed, the approach taken towards Cyprus, and the subsequent comments of various euro area policymakers, not least Dijsselbloem, suggest that there is little appetite among the Northern countries in particular for closer fiscal integration. So, the markets’ reaction to the events in Cyprus appears warranted. Just how far the correction will go, of course, is impossible to tell. Following the Deauville declaration in October 2010, Irish and Portuguese 2Y sovereign bond spreads rose by more than 300bps. Thanks to the ECB’s OMT programme and its generous liquidity provisions to euro area banks, however, this is unlikely to be repeated. But with senior creditors, including uninsured depositors, now facing significantly larger risks of bail-ins in future crises, and with risks high that economic conditions deteriorate beyond current expectations, credit and sovereign spreads don’t look set to return to their post-Draghi “whatever it takes” lows anytime soon. The week ahead

Following the likely failure of Bersani, leader of Italy’s left-wing coalition parties, to form a government in the past week, the focus will remain on Italy also in the coming week, with President Napolitano reportedly eyeing at appointing a technocrat to lead a broad coalition, mandated to reform the country’s electoral law. This, in turn, would hopefully pave the way for more effective elections later in the year, possibly in October. Politics aside, on Thursday all eyes will be on Frankfurt, where the ECB’s Governing Council will conclude its latest interest rate setting meeting. While the ECB's growth forecast for this year was already gloomy, the latest data and political developments might have raised the odds of a pre-emptive interest rate cut as early as

next week. However, we continue to expect the ECB to hold fire until there is greater clarity about the situation in Italy, suggesting that the rate cut is more likely to come later in the year, most likely in September in our view. Tomorrow will be a bank holiday in most European countries, with only French consumer spending for February and Italian CPI for March due for release. Following Monday’s bank holiday, the data flow picks up again on Tuesday with the final release of the March manufacturing PMIs, along with the latest unemployment figures for the euro area, Italy, Spain and Belgium. Tuesday also brings German CPI inflation and Italian budget data, both for March. On Wednesday, meanwhile, the flash estimate for euro area CPI inflation for March is due. Thursday brings the final release of the March services PMIs, while on Friday euro area retail sales figures for February, German factory orders, also for February, and Italian budget data for end-2012 are due. In the markets, Germany will sell €4bn of 2018 bonds on Wednesday, while Spain will auction 2016, 2018 and 2021 bonds on Thursday. The coming week in the US brings several releases of note, kicking off on Monday with the latest manufacturing ISM survey, which is expected to report that conditions remained broadly unchanged in March with the index pointing to solid expansion in the sector. This will be followed by the latest factory orders and vehicle sales figures on Tuesday, and the non-manufacturing ISM survey on Wednesday, expected to similarly indicate solid expansion at the end of Q1. Wednesday will also see the release of the ADP employment report, which will be followed by the weekly jobless claims numbers on Thursday and the labour market report on Friday. This is expected to show that nonfarm payrolls were up almost 200K in March, while the unemployment rate remained unchanged at 7.7%. There are no UST bond auctions due in the coming week.

240

260

280

300

320

340

360

380

400

420

Jan-13 Feb-13 M ar-13

Italy

Spain

bps

This is the last Euro4Sight. We will, however, continue publishing topical research notes and blogs on the latest developments in the

euro area. Please contact us at [email protected] to be

added to the distribution list.

12

What's new This is the final week of the results season in Hong Kong/China, with many of the stocks that we cover reporting their full-year 2012 results. Chaowei Power’s 2012 results highlighted the tough market conditions in 2H12; its gross margin declined to 14.1% in 2H12 (27.1% in 1H12). However, during an investor roadshow we hosted in Hong Kong and Singapore over 25-28 March, management said the pricing situation should improve in 2H13, especially due to the Mainland government’s requirement to shut down production of lead-acid batteries and lead-based cadmium components using sub-standard cadmium by end-2013. As at the end of 2012, the enclosed battery formation process accounted for some 83% of the company’s capacity. Meanwhile, Shenzhou International announced a 5% YoY decline in its 2012 net profit, its first such decline, owing to sluggish sales in Japan and China. Still, Shenzhou generated very strong cash flow last year and now has a net

cash position. It declared a special dividend per share of HKD0.20. Discovery idea Founded in 1990, Taiwan Acceptance Corp (TAC) is part of Taiwan automaker Yulon, which has a 53.29% stake in TAC, which engages in car leasing and factoring in Taiwan and operates equipment leasing and car rental businesses in China. TAC continues to expand in tandem with Yulon group. Backed by the asset quality of its China loans, it plans to raise its ticket size to CNY1m. TAC expects its China loans to increase by 50% YoY for 2013 and says it will consider starting a vendor programme in China. Picks of the week Ilvin Cornelis initiated coverage on Singapore’s third-largest grocery retailer, Sheng Siong Group, with a Buy (1) call. He forecasts a 2013-15 sales CAGR of 11%, on floor-space expansion and improvements in same-store sales (SSS), and sees room for the company to win market share from inefficient grocery retailers. Also, he expects demand for its low-priced supermarket products to remain strong, supported by overall population growth and the price-sensitivity of many consumers. Techtronic Industrial’s (TTI) 2012 gross margin was 33.5% (2011: 32.6%). We believe TTI will expand its gross margin in 2013 as the company continues to increase the proportion of sales of high-margin power-tool products. We are also

positive on the power-tool business, on strong sales of the Milwaukee Red Lithium cordless platform and the launch of a sub-compact product line. Besides, with a new generation of products (higher ASPs and profit margins) expected by management to account for 80% of total floor-care products by year-end (40% currently), we believe sales growth and margin increases for its floor-care business are likely over 2013-14. Corporate events Date Company Event Venue Mar 28 & Apr 2

REXLot (555 HK) NDR HK & SG

Mar 28 Shenzhou Int’l (2313 HK) NDR HK Apr 16 Techtronic (669 HK) NDR Boston

Source: Daiwa

Recent company visits (18 Mar – 28 Mar) Name Ticker Chailease Holdings* 5871 TT Chaowei Power* 951 HK China Financial Services* 605 HK China Outfitters* 1146 HK Kingsoft* 3888 HK REXLot* 555 HK Shenzhou Int'l* 2313 HK Stella* 1836 HK Techtronic Industries* 669 HK Weiqiao Textile* 2698 HK Win Hanverky 3322 HK

Source: Daiwa; * Results

MSCI small-cap index MSCI Small Cap

Chg (%) 27-Mar-13 1-week 1-month 3-month 6-month

Asia 1.8 4.5 9.9 13.4Asia ex-Japan 0.9 0.9 5.8 11.4China 0.2 (0.2) 7.9 29.8Hong Kong 1.5 2.0 8.8 18.1Taiwan 1.3 1.5 6.6 3.8Korea 0.8 3.9 7.0 2.5India (1.9) (6.8) (15.3) (8.9)Singapore 2.5 0.8 6.3 11.3Indonesia 0.5 8.2 22.7 25.0Malaysia 0.2 3.7 2.9 3.8Philippines 3.1 0.3 19.1 31.6Source: Bloomberg

28 March 2013

Asia small-cap weekly

• Despite falling short of expectations in 2012, Chaowei Power and Shenzhou International should resume positive growth in 2013

• Discovery idea: Taiwan Acceptance • Pick of the week: Sheng Siong Group and Techtronic

Discovery

Small Cap / Asia ex Japan

John Choi(852) 2773 8730

Regional Small-cap Team

- 13 -

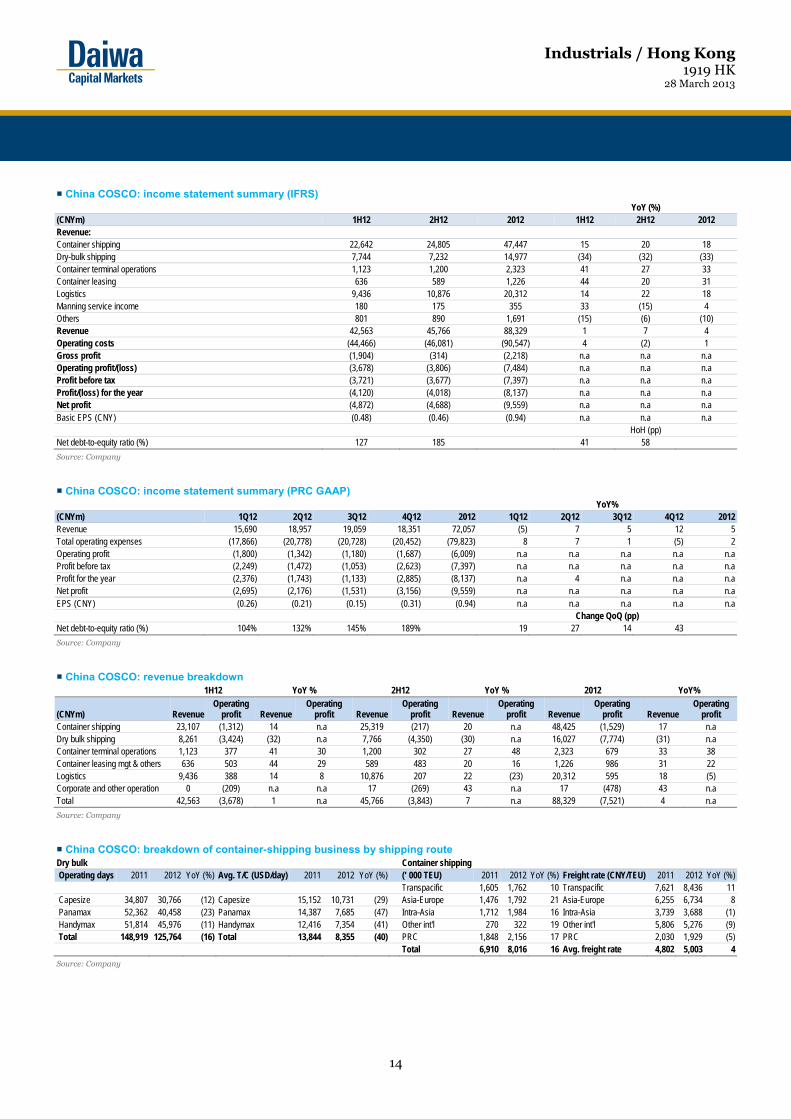

■ What's new China COSCO (COSCO) posted a net loss of CNY9.6bn for 2012, worse than we and the market expected. Still, we believe the worst is behind us and expect the industry to recover gradually from 2013 onwards, underpinning a profitability upturn for COSCO. ■ What's the impact We envisage only short-term share-price pressure on the back of the weak 2012 results, as COSCO had already issued a profit warning on 25 January stating that it expected a significant net loss for 2012. Weakness in dry-bulk demand was the main reason for its net loss. Its full-year operating loss was CNY7.8bn, with no improvement in 2H12. Management expects a net capacity increase for the company after scrapping of about 6-7% YoY in 2013, which should match closely to the dry-bulk demand growth,

projected at 5% YoY. Though the shipping industry’s overcapacity accumulated in the past years would need time to be absorbed, management believes the worst situation is already over. COSCO has announced that it will record a one-off disposal gain of CNY1.96bn from the planned disposal of its logistics business for 2013. We expect the transaction to be completed in 1H13, and our 2013-14 forecasts now incorporate the financial impact of the disposal. Though we do not consider the disposal as a long-term positive for COSCO, it concurs with our and the market’s expectation that the company would need to sell this business to avoid a delisting from the A-share market. COSCO’s share price has moved in line with those of its peers since it announced the disposal, and thus we do not see major negative sentiment on the transaction. The company’s container-shipping business reduced its operating loss to CNY1.5bn for 2012 (from CNY6.4bn for 2011), due we believe to consistent freight rate hikes. We expect better profitability in 2013 assuming a continued freight rate improvement. Our revenue and bottom-line revisions for COSCO for 2013-14E reflect primarily the exclusion of the logistics business. ■ What we recommend We believe COSCO’s current share price already factors in the negatives and reiterate our Buy (1) rating. Going forward, as well as an industry recovery, we expect another share-price catalyst from supportive policies from the PRC Government, which could be in the form of subsidies for the scrapping of aged vessels.

We lower our six-month target price to HKD4.50 (from HKD5.60), reflecting mainly the exclusion of the logistics business which reduces our 2013E BVPS, to which we assign an unchanged PBR of 1.8x, in line with COSCO’s average trading PBR before it acquired the logistics business. Risks to our call would include weaker-than-expected cargo traffic and freight-rate increases, and further asset disposals. ■ How we differ We are more optimistic than the market about a recovery in COSCO’s profitability.

28 March 2013

Profitability upturn expected

• Disposal of its logistics business should suffice to turn COSCO back to a reported-basis profit in 2013

• Worst of the dry-bulk industry appears over and we expect a gradual recovery this year

• Additional catalyst from potentially supportive government policies

Source: Daiwa forecasts

Source: FactSet, Daiwa forecasts

Industrials / Hong Kong

China COSCO1919 HK

Buy (unchanged)

OutperformHoldUnderperformSell

1

2

3

4

5Target (HKD): 5.60 4.50 Upside: 23.0% 28 Mar price (HKD): 3.66

Kelvin Lau(852) 2848 [email protected]

Forecast revisions (%)Year to 31 Dec 13E 14E 15ERevenue change (10.4) (24.3) n.a.Net profit change n.a. (13.1) n.a.Core EPS (FD) change n.a. (13.1) n.a.

65

78

90

103

115

2.5

3.3

4.0

4.8

5.5

Mar-12 Jun-12 Sep-12 Dec-12 Mar-13

Share price performance

Ch COSCO (LHS) Relative to HSI (RHS)

(HKD) (%)

12-month range 2.76-5.10Market cap (USDbn) 4.823m avg daily turnover (USDm) 11.13Shares outstanding (m) 10,216Major shareholder China Ocean Shipping (52.8%)

Financial summary (CNY)Year to 31 Dec 13E 14E 15ERevenue (m) 88,677 85,097 91,649Operating profit (m) (1,289) 3,071 4,025Net profit (m) (624) 2,753 3,610Core EPS (fully-diluted) (0.061) 0.269 0.353EPS change (%) n.a. n.a. 31.2Daiwa vs Cons. EPS (%) n.a. 30.2 135.6PER (x) n.a. 10.9 8.3Dividend yield (%) 0.0 0.0 0.0DPS 0.000 0.000 0.000PBR (x) 1.4 1.3 1.1EV/EBITDA (x) 27.9 10.3 8.6ROE (%) n.a. 12.3 14.3

Industrials / Hong Kong 1919 HK

28 March 2013

14

China COSCO: income statement summary (IFRS) YoY (%)

(CNYm) 1H12 2H12 2012 1H12 2H12 2012 Revenue: Container shipping 22,642 24,805 47,447 15 20 18 Dry-bulk shipping 7,744 7,232 14,977 (34) (32) (33) Container terminal operations 1,123 1,200 2,323 41 27 33 Container leasing 636 589 1,226 44 20 31 Logistics 9,436 10,876 20,312 14 22 18 Manning service income 180 175 355 33 (15) 4 Others 801 890 1,691 (15) (6) (10) Revenue 42,563 45,766 88,329 1 7 4 Operating costs (44,466) (46,081) (90,547) 4 (2) 1 Gross profit (1,904) (314) (2,218) n.a n.a n.a Operating profit/(loss) (3,678) (3,806) (7,484) n.a n.a n.a Profit before tax (3,721) (3,677) (7,397) n.a n.a n.a Profit/(loss) for the year (4,120) (4,018) (8,137) n.a n.a n.a Net profit (4,872) (4,688) (9,559) n.a n.a n.a Basic EPS (CNY) (0.48) (0.46) (0.94) n.a n.a n.a

HoH (pp) Net debt-to-equity ratio (%) 127 185 41 58

Source: Company

China COSCO: income statement summary (PRC GAAP) YoY%

(CNYm) 1Q12 2Q12 3Q12 4Q12 2012 1Q12 2Q12 3Q12 4Q12 2012Revenue 15,690 18,957 19,059 18,351 72,057 (5) 7 5 12 5Total operating expenses (17,866) (20,778) (20,728) (20,452) (79,823) 8 7 1 (5) 2Operating profit (1,800) (1,342) (1,180) (1,687) (6,009) n.a n.a n.a n.a n.a Profit before tax (2,249) (1,472) (1,053) (2,623) (7,397) n.a n.a n.a n.a n.aProfit for the year (2,376) (1,743) (1,133) (2,885) (8,137) n.a 4 n.a n.a n.aNet profit (2,695) (2,176) (1,531) (3,156) (9,559) n.a n.a n.a n.a n.aEPS (CNY) (0.26) (0.21) (0.15) (0.31) (0.94) n.a n.a n.a n.a n.a

Change QoQ (pp) Net debt-to-equity ratio (%) 104% 132% 145% 189% 19 27 14 43

Source: Company

China COSCO: revenue breakdown 1H12 YoY % 2H12 YoY % 2012 YoY%

(CNYm) Revenue Operating

profit Revenue Operating

profit RevenueOperating

profit RevenueOperating

profit Revenue Operating

profit Revenue Operating

profit Container shipping 23,107 (1,312) 14 n.a 25,319 (217) 20 n.a 48,425 (1,529) 17 n.a Dry bulk shipping 8,261 (3,424) (32) n.a 7,766 (4,350) (30) n.a 16,027 (7,774) (31) n.a Container terminal operations 1,123 377 41 30 1,200 302 27 48 2,323 679 33 38 Container leasing mgt & others 636 503 44 29 589 483 20 16 1,226 986 31 22 Logistics 9,436 388 14 8 10,876 207 22 (23) 20,312 595 18 (5) Corporate and other operation 0 (209) n.a n.a 17 (269) 43 n.a 17 (478) 43 n.a Total 42,563 (3,678) 1 n.a 45,766 (3,843) 7 n.a 88,329 (7,521) 4 n.a

Source: Company

China COSCO: breakdown of container-shipping business by shipping route Dry bulk Container shipping Operating days 2011 2012 YoY (%) Avg. T/C (USD/day) 2011 2012 YoY (%) (‘ 000 TEU) 2011 2012 YoY (%) Freight rate (CNY/TEU) 2011 2012 YoY (%)

Transpacific 1,605 1,762 10 Transpacific 7,621 8,436 11 Capesize 34,807 30,766 (12) Capesize 15,152 10,731 (29) Asia-Europe 1,476 1,792 21 Asia-Europe 6,255 6,734 8 Panamax 52,362 40,458 (23) Panamax 14,387 7,685 (47) Intra-Asia 1,712 1,984 16 Intra-Asia 3,739 3,688 (1) Handymax 51,814 45,976 (11) Handymax 12,416 7,354 (41) Other int'l 270 322 19 Other int'l 5,806 5,276 (9) Total 148,919 125,764 (16) Total 13,844 8,355 (40) PRC 1,848 2,156 17 PRC 2,030 1,929 (5)

Total 6,910 8,016 16 Avg. freight rate 4,802 5,003 4

Source: Company

Industrials / Hong Kong 1919 HK

28 March 2013

15

Key assumptions

Profit and loss (CNYm)

Cash flow (CNYm)

Source: FactSet, Daiwa forecasts

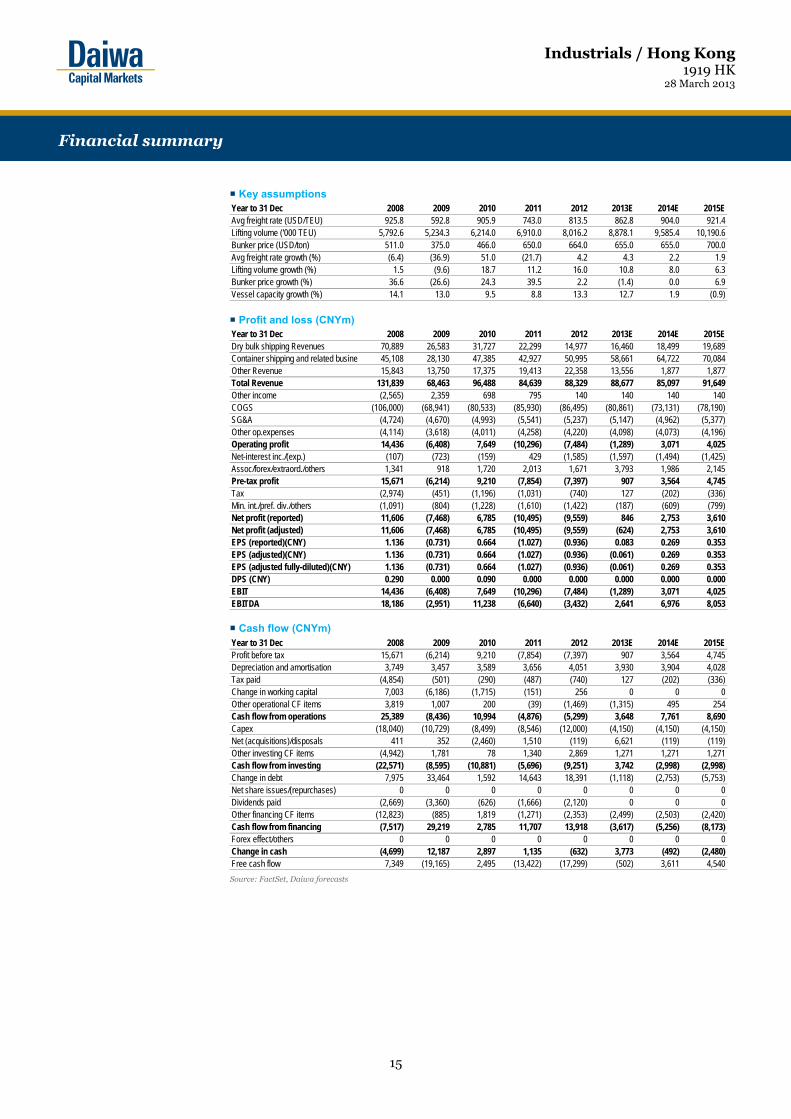

Year to 31 Dec 2008 2009 2010 2011 2012 2013E 2014E 2015EAvg freight rate (USD/TEU) 925.8 592.8 905.9 743.0 813.5 862.8 904.0 921.4Lifting volume ('000 TEU) 5,792.6 5,234.3 6,214.0 6,910.0 8,016.2 8,878.1 9,585.4 10,190.6Bunker price (USD/ton) 511.0 375.0 466.0 650.0 664.0 655.0 655.0 700.0Avg freight rate growth (%) (6.4) (36.9) 51.0 (21.7) 4.2 4.3 2.2 1.9Lifting volume growth (%) 1.5 (9.6) 18.7 11.2 16.0 10.8 8.0 6.3Bunker price growth (%) 36.6 (26.6) 24.3 39.5 2.2 (1.4) 0.0 6.9Vessel capacity growth (%) 14.1 13.0 9.5 8.8 13.3 12.7 1.9 (0.9)

Year to 31 Dec 2008 2009 2010 2011 2012 2013E 2014E 2015EDry bulk shipping Revenues 70,889 26,583 31,727 22,299 14,977 16,460 18,499 19,689Container shipping and related busines 45,108 28,130 47,385 42,927 50,995 58,661 64,722 70,084Other Revenue 15,843 13,750 17,375 19,413 22,358 13,556 1,877 1,877Total Revenue 131,839 68,463 96,488 84,639 88,329 88,677 85,097 91,649Other income (2,565) 2,359 698 795 140 140 140 140COGS (106,000) (68,941) (80,533) (85,930) (86,495) (80,861) (73,131) (78,190)SG&A (4,724) (4,670) (4,993) (5,541) (5,237) (5,147) (4,962) (5,377)Other op.expenses (4,114) (3,618) (4,011) (4,258) (4,220) (4,098) (4,073) (4,196)Operating profit 14,436 (6,408) 7,649 (10,296) (7,484) (1,289) 3,071 4,025Net-interest inc./(exp.) (107) (723) (159) 429 (1,585) (1,597) (1,494) (1,425)Assoc/forex/extraord./others 1,341 918 1,720 2,013 1,671 3,793 1,986 2,145Pre-tax profit 15,671 (6,214) 9,210 (7,854) (7,397) 907 3,564 4,745Tax (2,974) (451) (1,196) (1,031) (740) 127 (202) (336)Min. int./pref. div./others (1,091) (804) (1,228) (1,610) (1,422) (187) (609) (799)Net profit (reported) 11,606 (7,468) 6,785 (10,495) (9,559) 846 2,753 3,610Net profit (adjusted) 11,606 (7,468) 6,785 (10,495) (9,559) (624) 2,753 3,610EPS (reported)(CNY) 1.136 (0.731) 0.664 (1.027) (0.936) 0.083 0.269 0.353EPS (adjusted)(CNY) 1.136 (0.731) 0.664 (1.027) (0.936) (0.061) 0.269 0.353EPS (adjusted fully-diluted)(CNY) 1.136 (0.731) 0.664 (1.027) (0.936) (0.061) 0.269 0.353DPS (CNY) 0.290 0.000 0.090 0.000 0.000 0.000 0.000 0.000EBIT 14,436 (6,408) 7,649 (10,296) (7,484) (1,289) 3,071 4,025EBITDA 18,186 (2,951) 11,238 (6,640) (3,432) 2,641 6,976 8,053

Year to 31 Dec 2008 2009 2010 2011 2012 2013E 2014E 2015EProfit before tax 15,671 (6,214) 9,210 (7,854) (7,397) 907 3,564 4,745Depreciation and amortisation 3,749 3,457 3,589 3,656 4,051 3,930 3,904 4,028Tax paid (4,854) (501) (290) (487) (740) 127 (202) (336)Change in working capital 7,003 (6,186) (1,715) (151) 256 0 0 0Other operational CF items 3,819 1,007 200 (39) (1,469) (1,315) 495 254Cash flow from operations 25,389 (8,436) 10,994 (4,876) (5,299) 3,648 7,761 8,690Capex (18,040) (10,729) (8,499) (8,546) (12,000) (4,150) (4,150) (4,150)Net (acquisitions)/disposals 411 352 (2,460) 1,510 (119) 6,621 (119) (119)Other investing CF items (4,942) 1,781 78 1,340 2,869 1,271 1,271 1,271Cash flow from investing (22,571) (8,595) (10,881) (5,696) (9,251) 3,742 (2,998) (2,998)Change in debt 7,975 33,464 1,592 14,643 18,391 (1,118) (2,753) (5,753)Net share issues/(repurchases) 0 0 0 0 0 0 0 0Dividends paid (2,669) (3,360) (626) (1,666) (2,120) 0 0 0Other financing CF items (12,823) (885) 1,819 (1,271) (2,353) (2,499) (2,503) (2,420)Cash flow from financing (7,517) 29,219 2,785 11,707 13,918 (3,617) (5,256) (8,173)Forex effect/others 0 0 0 0 0 0 0 0Change in cash (4,699) 12,187 2,897 1,135 (632) 3,773 (492) (2,480)Free cash flow 7,349 (19,165) 2,495 (13,422) (17,299) (502) 3,611 4,540

Financial summary

Industrials / Hong Kong 1919 HK

28 March 2013

16

Balance sheet (CNYm)

Key ratios (%)

Source: FactSet, Daiwa forecasts

Company profile

China COSCO is the world’s second-largest integrated shipping company in terms of capacity. The company provides a wide range of container shipping, dry-bulk shipping, logistics services, terminal and container leasing services for both international and domestic customers. As at the end of 2011, the company had 332 dry-bulk vessels with a total capacity of 30m DWT, and 174 container vessels with a total capacity of 0.76m TEUs (and an average age of 10 years).

As at 31 Dec 2008 2009 2010 2011 2012 2013E 2014E 2015ECash & short-term investment 32,356 44,280 47,381 47,473 46,765 50,538 50,045 47,565Inventory 1,539 1,783 2,117 3,387 2,731 2,731 2,731 2,731Accounts receivable 10,543 8,700 10,961 11,899 13,564 10,121 9,727 10,447Other current assets 650 464 152 0 54 54 54 54Total current assets 45,088 55,227 60,610 62,759 63,114 63,444 62,558 60,797Fixed assets 55,849 63,025 67,096 73,030 80,643 75,158 75,577 75,874Goodwill & intangibles 186 214 210 196 202 151 100 49Other non-current assets 18,887 20,356 23,065 21,474 21,248 19,109 19,082 19,056Total assets 120,010 138,822 150,982 157,459 165,208 157,861 157,317 155,776Short-term debt 3,650 7,233 5,870 21,713 14,118 10,753 10,753 10,753Accounts payable 15,412 17,799 20,392 23,799 24,213 21,019 19,594 20,546Other current liabilities 10,284 2,508 2,281 2,481 2,082 2,082 2,082 2,082Total current liabilities 29,345 27,540 28,543 47,993 40,413 33,854 32,428 33,381Long-term debt 23,296 53,117 54,927 55,314 79,086 82,586 79,586 73,586Other non-current liabilities 5,462 4,630 5,211 3,982 4,011 4,011 4,011 4,011Total liabilities 58,104 85,287 88,681 107,288 123,510 120,451 116,026 110,978Share capital 10,216 10,216 10,216 10,216 10,216 10,216 10,216 10,216Reserves/R.E./others 41,927 32,720 37,613 24,479 14,921 10,446 13,718 16,425Shareholders' equity 52,144 42,936 47,829 34,695 25,137 20,662 23,935 26,641Minority interests 9,763 10,599 14,472 15,475 16,561 16,748 17,357 18,156Total equity & liabilities 120,010 138,822 150,982 157,459 165,208 157,861 157,317 155,776EV 23,875 45,929 42,335 58,815 76,313 73,813 71,914 69,194Net debt/(cash) (5,410) 16,070 13,416 29,553 46,439 42,801 40,294 36,774BVPS (CNY) 5.104 4.203 4.682 3.396 2.460 2.022 2.343 2.608

Year to 31 Dec 2008 2009 2010 2011 2012 2013E 2014E 2015ESales (YoY) 17.5 (48.1) 40.9 (12.3) 4.4 0.4 (4.0) 7.7EBITDA (YoY) (35.6) n.a. n.a. n.a. n.a. n.a. 164.1 15.4Operating profit (YoY) (40.1) n.a. n.a. n.a. n.a. n.a. n.a. 31.1Net profit (YoY) (40.4) n.a. n.a. n.a. n.a. n.a. n.a. 31.2Core EPS (fully-diluted) (YoY) (47.9) n.a. n.a. n.a. n.a. n.a. n.a. 31.2Gross-profit margin 19.6 n.a. 16.5 n.a. 2.1 8.8 14.1 14.7EBITDA margin 13.8 n.a. 11.6 n.a. n.a. 3.0 8.2 8.8Operating-profit margin 10.9 n.a. 7.9 n.a. n.a. n.a. 3.6 4.4Net profit margin 8.8 (10.9) 7.0 (12.4) (10.8) (0.7) 3.2 3.9ROAE 23.5 n.a. 15.0 n.a. n.a. n.a. 12.3 14.3ROAA 9.8 n.a. 4.7 n.a. n.a. n.a. 1.7 2.3ROCE 17.5 n.a. 6.5 n.a. n.a. n.a. 2.3 3.1ROIC 24.5 (10.2) 9.2 (13.2) (8.9) (1.5) 3.6 4.6Net debt to equity net cash 37.4 28.1 85.2 184.7 207.1 168.3 138.0Effective tax rate 19.0 n.a. 13.0 n.a. n.a. n.a. 5.7 7.1Accounts receivable (days) 33.0 51.3 37.2 49.3 52.6 48.7 42.6 40.2Current ratio (x) 1.5 2.0 2.1 1.3 1.6 1.9 1.9 1.8Net interest cover (x) 135.3 n.a. 48.0 n.a. n.a. n.a. 2.1 2.8Net dividend payout 25.5 n.a. 13.6 n.a. n.a. 0.0 0.0 0.0Free cash flow yield 24.6 n.a. 8.3 n.a. n.a. n.a. 12.1 15.2

Financial summary continued …

- 17 -

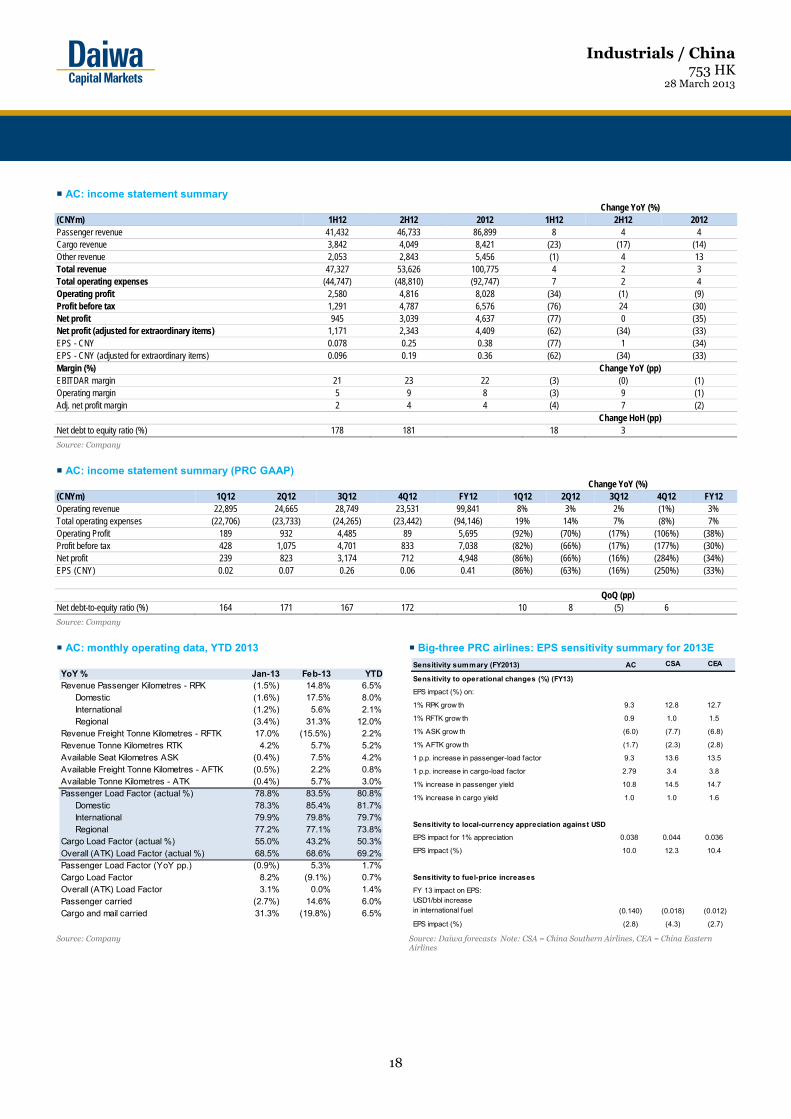

■ What's new We have reassessed our forecasts for Air China (AC) post our meeting with management on 27 March, and expect profitability for AC and its PRC peers to improve substantially this year. ■ What's the impact AC’s recurring net profit for 2012 was CNY4.4bn, down 33% YoY, which was better than market expectations but lower than ours. The major disappointment was the 1.3% YoY decline in yield for 2H12. Management is optimistic about a recovery in passenger traffic in 2013 and plans to increase domestic passenger capacity by 15% YoY and international passenger capacity by 13% YoY this year. AC is bullish on the US market, where it aims to raise capacity by 35% YoY this year, whereas it plans only a 6% YoY capacity increase in Europe. We believe demand growth should able to match the planned capacity

rises and thus forecast a stable passenger load factor of 80% for AC for 2013. We are positive about the pick-up in premium traffic of 13% YoY over January-February, but remain cautious on a passenger yield recovery as the big-three PRC airlines target to raise capacity this year by 11-14% YoY, which we consider aggressive. We reduce slightly our 2013 passenger yield growth forecast for AC to 2% YoY (from 3% YoY). On the cargo market, AC does not see a significant recovery and expects demand to remain weak in 2013. It expects to increase cargo capacity by 5% YoY this year. The negative impact of increases in landing and take-off charges and parking charges should be about CNY750m a year for AC, according to management. We now include this additional cost impact in our forecasts. ■ What we recommend We reduce our 2013-14E EPS by 12% to factor in the lower-than-expected 2012 results, along with the impact of increased landing/take-off charges and lower-than-previously-assumed passenger yields. As such, we lower our six-month target price to HKD8.00 (from HKD8.60), based on our revised 2013E BVPS and an unchanged PBR of 1.4x, corresponding to the industry’s adjusted average PBR for 2010. We reaffirm our Buy (1) rating on AC. We expect profitability to improve significantly this year and are positively surprised by the improving premium traffic and sound traffic growth for January-February. In the long run, AC still looks the best-positioned PRC airline to capture growing PRC outbound traffic,

premium-class travel and a recovery in the air freight market. The stock trades at a 2013E PBR of 1.2x, which is below its past-five-year average PBR of 1.5x and looks undemanding to us. Risks to our call would include lower-than-expected traffic and yield increases. ■ How we differ Our 2013-14E EPS are 7-10% higher than the Bloomberg consensus forecasts as we are more positive about a traffic improvement in 2013.

28 March 2013

Expect 2013 profitability to improve

• AC’s 2012 results beat market expectations but missed ours

• We expect passenger traffic growth to match planned capacity growth of 13-15% YoY for 2013

• We have slight yield concerns but still expect a strong profitability improvement

Source: Daiwa forecasts

Source: FactSet, Daiwa forecasts

Industrials / China

Air China753 HK

Buy (unchanged)

OutperformHoldUnderperformSell

1

2

3

4

5Target (HKD): 8.60 8.00 Upside: 15.9% 28 Mar price (HKD): 6.90

Kelvin Lau(852) 2848 [email protected]

Forecast revisions (%)Year to 31 Dec 13E 14E 15ERevenue change 0.2 (0.2) n.a.Net profit change (12.9) (12.8) n.a.Core EPS (FD) change (12.1) (12.0) n.a.

90

100

110

120

130

4.0

4.9

5.8

6.6

7.5

Mar-12 Jun-12 Sep-12 Dec-12 Mar-13

Share price performance

Air China (LHS) Relative to HSI (RHS)

(HKD) (%)

12-month range 4.45-7.39Market cap (USDbn) 10.793m avg daily turnover (USDm) 11.53Shares outstanding (m) 12,137Major shareholder CNAHC (51.5%)

Financial summary (CNY)Year to 31 Dec 13E 14E 15ERevenue (m) 116,439 128,005 140,787Operating profit (m) 10,213 11,008 11,515Net profit (m) 6,358 7,504 8,266Core EPS (fully-diluted) 0.520 0.613 0.676EPS change (%) 43.1 18.0 10.2Daiwa vs Cons. EPS (%) 9.7 6.5 6.9PER (x) 10.6 9.0 8.2Dividend yield (%) 1.1 1.2 1.4DPS 0.060 0.068 0.076PBR (x) 1.2 1.1 1.0EV/EBITDA (x) 5.1 4.6 4.2ROE (%) 11.8 12.1 11.8

Industrials / China 753 HK

28 March 2013

18

AC: income statement summary Change YoY (%)

(CNYm) 1H12 2H12 2012 1H12 2H12 2012 Passenger revenue 41,432 46,733 86,899 8 4 4 Cargo revenue 3,842 4,049 8,421 (23) (17) (14) Other revenue 2,053 2,843 5,456 (1) 4 13 Total revenue 47,327 53,626 100,775 4 2 3 Total operating expenses (44,747) (48,810) (92,747) 7 2 4 Operating profit 2,580 4,816 8,028 (34) (1) (9) Profit before tax 1,291 4,787 6,576 (76) 24 (30) Net profit 945 3,039 4,637 (77) 0 (35) Net profit (adjusted for extraordinary items) 1,171 2,343 4,409 (62) (34) (33) EPS - CNY 0.078 0.25 0.38 (77) 1 (34) EPS - CNY (adjusted for extraordinary items) 0.096 0.19 0.36 (62) (34) (33) Margin (%) Change YoY (pp) EBITDAR margin 21 23 22 (3) (0) (1) Operating margin 5 9 8 (3) 9 (1) Adj. net profit margin 2 4 4 (4) 7 (2)

Change HoH (pp) Net debt to equity ratio (%) 178 181 18 3

Source: Company

AC: income statement summary (PRC GAAP)

Change YoY (%) (CNYm) 1Q12 2Q12 3Q12 4Q12 FY12 1Q12 2Q12 3Q12 4Q12 FY12 Operating revenue 22,895 24,665 28,749 23,531 99,841 8% 3% 2% (1%) 3% Total operating expenses (22,706) (23,733) (24,265) (23,442) (94,146) 19% 14% 7% (8%) 7% Operating Profit 189 932 4,485 89 5,695 (92%) (70%) (17%) (106%) (38%) Profit before tax 428 1,075 4,701 833 7,038 (82%) (66%) (17%) (177%) (30%) Net profit 239 823 3,174 712 4,948 (86%) (66%) (16%) (284%) (34%) EPS (CNY) 0.02 0.07 0.26 0.06 0.41 (86%) (63%) (16%) (250%) (33%)

QoQ (pp)

Net debt-to-equity ratio (%) 164 171 167 172 10 8 (5) 6

Source: Company

AC: monthly operating data, YTD 2013 Big-three PRC airlines: EPS sensitivity summary for 2013E

Source: Company

Source: Daiwa forecasts Note: CSA = China Southern Airlines, CEA = China Eastern Airlines

YoY % Jan-13 Feb-13 YTDRevenue Passenger Kilometres - RPK (1.5%) 14.8% 6.5%

Domestic (1.6%) 17.5% 8.0%International (1.2%) 5.6% 2.1%Regional (3.4%) 31.3% 12.0%

Revenue Freight Tonne Kilometres - RFTK 17.0% (15.5%) 2.2%Revenue Tonne Kilometres RTK 4.2% 5.7% 5.2%Available Seat Kilometres ASK (0.4%) 7.5% 4.2%Available Freight Tonne Kilometres - AFTK (0.5%) 2.2% 0.8%Available Tonne Kilometres - ATK (0.4%) 5.7% 3.0%Passenger Load Factor (actual %) 78.8% 83.5% 80.8%

Domestic 78.3% 85.4% 81.7%International 79.9% 79.8% 79.7%Regional 77.2% 77.1% 73.8%

Cargo Load Factor (actual %) 55.0% 43.2% 50.3%Overall (ATK) Load Factor (actual %) 68.5% 68.6% 69.2%Passenger Load Factor (YoY pp.) (0.9%) 5.3% 1.7%Cargo Load Factor 8.2% (9.1%) 0.7%Overall (ATK) Load Factor 3.1% 0.0% 1.4%Passenger carried (2.7%) 14.6% 6.0%Cargo and mail carried 31.3% (19.8%) 6.5%

Sensitivity summary (FY2013) AC CSA CEA

Sensitivity to operational changes (%) (FY13)

EPS impact (%) on:

1% RPK grow th 9.3 12.8 12.7

1% RFTK grow th 0.9 1.0 1.5

1% ASK grow th (6.0) (7.7) (6.8)

1% AFTK grow th (1.7) (2.3) (2.8)

1 p.p. increase in passenger-load factor 9.3 13.6 13.5

1 p.p. increase in cargo-load factor 2.79 3.4 3.8

1% increase in passenger yield 10.8 14.5 14.7

1% increase in cargo yield 1.0 1.0 1.6

Sensitivity to local-currency appreciation against USD

EPS impact for 1% appreciation 0.038 0.044 0.036

EPS impact (%) 10.0 12.3 10.4

Sensitivity to fuel-price increases

FY 13 impact on EPS:USD1/bbl increasein international fuel (0.140) (0.018) (0.012)

EPS impact (%) (2.8) (4.3) (2.7)

Industrials / China 753 HK

28 March 2013

19

Key assumptions

Profit and loss (CNYm)

Cash flow (CNYm)

Source: FactSet, Daiwa forecasts

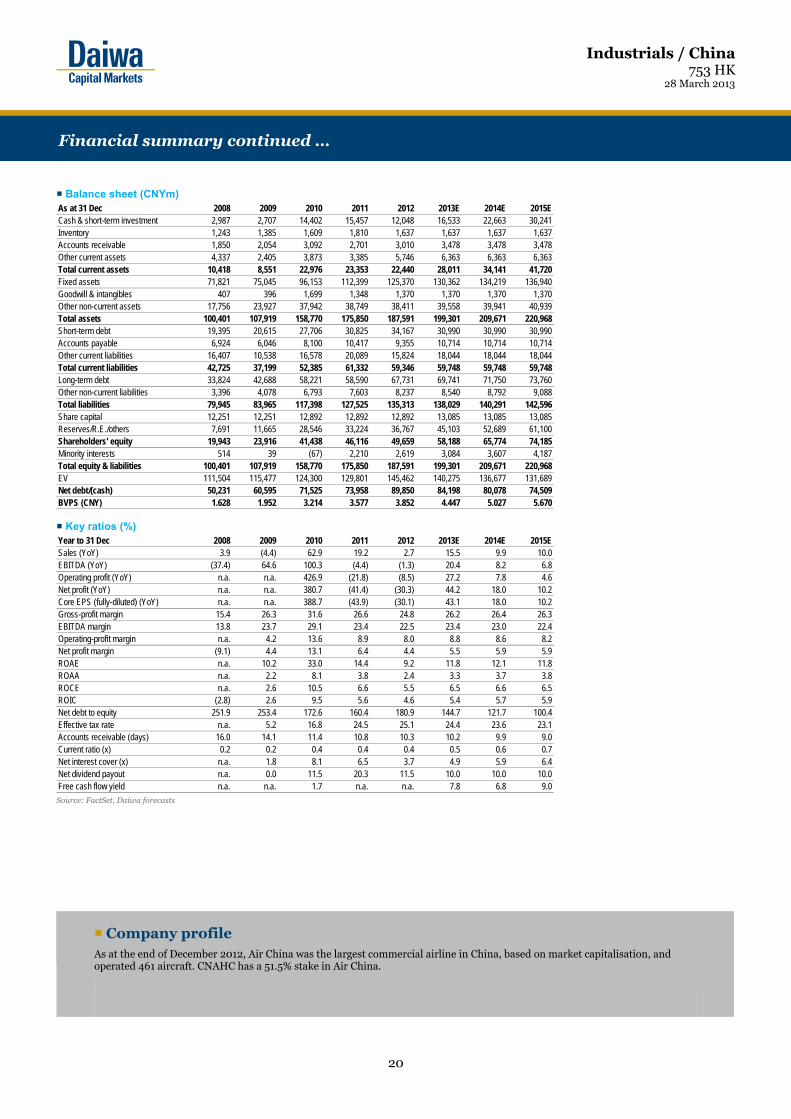

Year to 31 Dec 2008 2009 2010 2011 2012 2013E 2014E 2015EOverall RPK growth (%) (1.8) 9.8 40.0 16.8 5.1 14.3 7.9 8.1Overall RFTK growth (%) (6.8) (2.3) 37.2 0.1 (6.2) 7.0 10.0 10.0Overall ASK growth (%) 2.9 7.4 33.9 14.8 6.5 14.3 7.9 8.4Overall AFTK growth (%) (7.5) 2.4 20.7 4.1 (4.1) 5.0 9.0 10.0Overall PLF (%) 74.9 76.5 80.0 81.5 80.4 80.4 80.4 80.1Overall CLF (%) 56.8 54.2 61.6 59.3 58.0 59.2 59.7 59.7Overall passenger yield growth (%) 1.8 (10.3) 14.0 4.9 (1.0) 2.1 2.0 1.8Cargo Yield growth (%) 5.1 (23.1) 21.0 (5.4) (3.3) 3.0 2.0 2.0Int'l jet-fuel price (USD/bbl) 122.1 70.1 90.1 126.0 126.9 126.0 126.0 126.0

Year to 31 Dec 2008 2009 2010 2011 2012 2013E 2014E 2015EPassenger revenue 43,352 42,695 68,138 83,510 86,899 101,399 111,529 122,700Cargo revenue 7,185 5,396 10,072 9,833 8,421 9,281 10,413 11,683Other Revenue 2,342 2,435 4,119 4,813 5,456 5,759 6,063 6,404Total Revenue 52,879 50,527 82,329 98,157 100,775 116,439 128,005 140,787Other income (3,692) (4,101) (6,241) (7,742) (6,566) (8,026) (9,356) (10,987)COGS (44,758) (37,243) (56,291) (72,078) (75,805) (85,892) (94,198) (103,706)SG&A 0 0 0 0 0 0 0 0Other op.expenses (6,365) (7,051) (8,569) (9,561) (10,376) (12,308) (13,443) (14,579)Operating profit (1,937) 2,131 11,227 8,775 8,028 10,213 11,008 11,515Net-interest inc./(exp.) (1,696) (1,174) (1,389) (1,354) (2,163) (2,105) (1,852) (1,793)Assoc/forex/extraord./others (7,344) 4,109 4,995 1,933 710 2,286 2,430 3,045Pre-tax profit (10,978) 5,066 14,834 9,355 6,576 10,395 11,585 12,766Tax 1,611 (263) (2,498) (2,292) (1,648) (2,534) (2,736) (2,943)Min. int./pref. div./others 111 51 (331) 20 (291) (465) (523) (581)Net profit (reported) (9,256) 4,854 12,005 7,082 4,637 7,396 8,326 9,243Net profit (adjusted) (4,827) 2,245 10,790 6,321 4,409 6,358 7,504 8,266EPS (reported)(CNY) (0.780) 0.410 1.031 0.582 0.382 0.605 0.681 0.756EPS (adjusted)(CNY) (0.407) 0.190 0.927 0.520 0.363 0.520 0.613 0.676EPS (adjusted fully-diluted)(CNY) (0.407) 0.190 0.927 0.520 0.363 0.520 0.613 0.676DPS (CNY) 0.000 0.000 0.118 0.118 0.044 0.060 0.068 0.076EBIT (1,937) 2,131 11,227 8,775 8,028 10,213 11,008 11,515EBITDA 7,276 11,979 23,997 22,937 22,631 27,247 29,490 31,496

Year to 31 Dec 2008 2009 2010 2011 2012 2013E 2014E 2015EProfit before tax (10,978) 5,066 14,834 9,355 6,576 10,395 11,585 12,766Depreciation and amortisation 6,365 7,051 8,569 9,561 10,831 12,308 13,443 14,579Tax paid (650) 28 (503) (3,466) (1,648) (2,534) (2,736) (2,943)Change in working capital 3,302 (644) 678 6,798 (4,454) 2,797 251 296Other operational CF items 6,954 (6,037) (5,213) (2,577) (1,845) (2,434) (2,652) (3,369)Cash flow from operations 4,994 5,465 18,366 19,670 9,460 20,532 19,891 21,329Capex (7,552) (7,916) (17,246) (22,750) (15,300) (15,300) (15,300) (15,300)Net (acquisitions)/disposals 159 (165) 1,928 3,914 4,137 0 0 0Other investing CF items 191 (4,585) 1,260 (2,833) (366) 254 330 433Cash flow from investing (7,202) (12,666) (14,058) (21,669) (11,529) (15,046) (14,970) (14,867)Change in debt 3,866 6,813 1,042 92 2,175 (1,167) 2,010 2,010Net share issues/(repurchases) 0 0 6,421 0 788 1,051 0 0Dividends paid (838) 0 0 (1,524) (1,521) (777) (740) (833)Other financing CF items (157) 136 0 0 234 0 0 0Cash flow from financing 2,870 6,948 7,463 (1,432) 1,676 (892) 1,270 1,177Forex effect/others (190) (20) (71) (161) (61) (61) (61) (61)Change in cash 472 (273) 11,700 (3,593) (454) 4,533 6,130 7,579Free cash flow (2,558) (2,451) 1,120 (3,080) (5,840) 5,232 4,591 6,029

Financial summary

Industrials / China 753 HK

28 March 2013

20

Balance sheet (CNYm)

Key ratios (%)

Source: FactSet, Daiwa forecasts

Company profile

As at the end of December 2012, Air China was the largest commercial airline in China, based on market capitalisation, and operated 461 aircraft. CNAHC has a 51.5% stake in Air China.

As at 31 Dec 2008 2009 2010 2011 2012 2013E 2014E 2015ECash & short-term investment 2,987 2,707 14,402 15,457 12,048 16,533 22,663 30,241Inventory 1,243 1,385 1,609 1,810 1,637 1,637 1,637 1,637Accounts receivable 1,850 2,054 3,092 2,701 3,010 3,478 3,478 3,478Other current assets 4,337 2,405 3,873 3,385 5,746 6,363 6,363 6,363Total current assets 10,418 8,551 22,976 23,353 22,440 28,011 34,141 41,720Fixed assets 71,821 75,045 96,153 112,399 125,370 130,362 134,219 136,940Goodwill & intangibles 407 396 1,699 1,348 1,370 1,370 1,370 1,370Other non-current assets 17,756 23,927 37,942 38,749 38,411 39,558 39,941 40,939Total assets 100,401 107,919 158,770 175,850 187,591 199,301 209,671 220,968Short-term debt 19,395 20,615 27,706 30,825 34,167 30,990 30,990 30,990Accounts payable 6,924 6,046 8,100 10,417 9,355 10,714 10,714 10,714Other current liabilities 16,407 10,538 16,578 20,089 15,824 18,044 18,044 18,044Total current liabilities 42,725 37,199 52,385 61,332 59,346 59,748 59,748 59,748Long-term debt 33,824 42,688 58,221 58,590 67,731 69,741 71,750 73,760Other non-current liabilities 3,396 4,078 6,793 7,603 8,237 8,540 8,792 9,088Total liabilities 79,945 83,965 117,398 127,525 135,313 138,029 140,291 142,596Share capital 12,251 12,251 12,892 12,892 12,892 13,085 13,085 13,085Reserves/R.E./others 7,691 11,665 28,546 33,224 36,767 45,103 52,689 61,100Shareholders' equity 19,943 23,916 41,438 46,116 49,659 58,188 65,774 74,185Minority interests 514 39 (67) 2,210 2,619 3,084 3,607 4,187Total equity & liabilities 100,401 107,919 158,770 175,850 187,591 199,301 209,671 220,968EV 111,504 115,477 124,300 129,801 145,462 140,275 136,677 131,689Net debt/(cash) 50,231 60,595 71,525 73,958 89,850 84,198 80,078 74,509BVPS (CNY) 1.628 1.952 3.214 3.577 3.852 4.447 5.027 5.670

Year to 31 Dec 2008 2009 2010 2011 2012 2013E 2014E 2015ESales (YoY) 3.9 (4.4) 62.9 19.2 2.7 15.5 9.9 10.0EBITDA (YoY) (37.4) 64.6 100.3 (4.4) (1.3) 20.4 8.2 6.8Operating profit (YoY) n.a. n.a. 426.9 (21.8) (8.5) 27.2 7.8 4.6Net profit (YoY) n.a. n.a. 380.7 (41.4) (30.3) 44.2 18.0 10.2Core EPS (fully-diluted) (YoY) n.a. n.a. 388.7 (43.9) (30.1) 43.1 18.0 10.2Gross-profit margin 15.4 26.3 31.6 26.6 24.8 26.2 26.4 26.3EBITDA margin 13.8 23.7 29.1 23.4 22.5 23.4 23.0 22.4Operating-profit margin n.a. 4.2 13.6 8.9 8.0 8.8 8.6 8.2Net profit margin (9.1) 4.4 13.1 6.4 4.4 5.5 5.9 5.9ROAE n.a. 10.2 33.0 14.4 9.2 11.8 12.1 11.8ROAA n.a. 2.2 8.1 3.8 2.4 3.3 3.7 3.8ROCE n.a. 2.6 10.5 6.6 5.5 6.5 6.6 6.5ROIC (2.8) 2.6 9.5 5.6 4.6 5.4 5.7 5.9Net debt to equity 251.9 253.4 172.6 160.4 180.9 144.7 121.7 100.4Effective tax rate n.a. 5.2 16.8 24.5 25.1 24.4 23.6 23.1Accounts receivable (days) 16.0 14.1 11.4 10.8 10.3 10.2 9.9 9.0Current ratio (x) 0.2 0.2 0.4 0.4 0.4 0.5 0.6 0.7Net interest cover (x) n.a. 1.8 8.1 6.5 3.7 4.9 5.9 6.4Net dividend payout n.a. 0.0 11.5 20.3 11.5 10.0 10.0 10.0Free cash flow yield n.a. n.a. 1.7 n.a. n.a. 7.8 6.8 9.0

Financial summary continued …

- 21 -

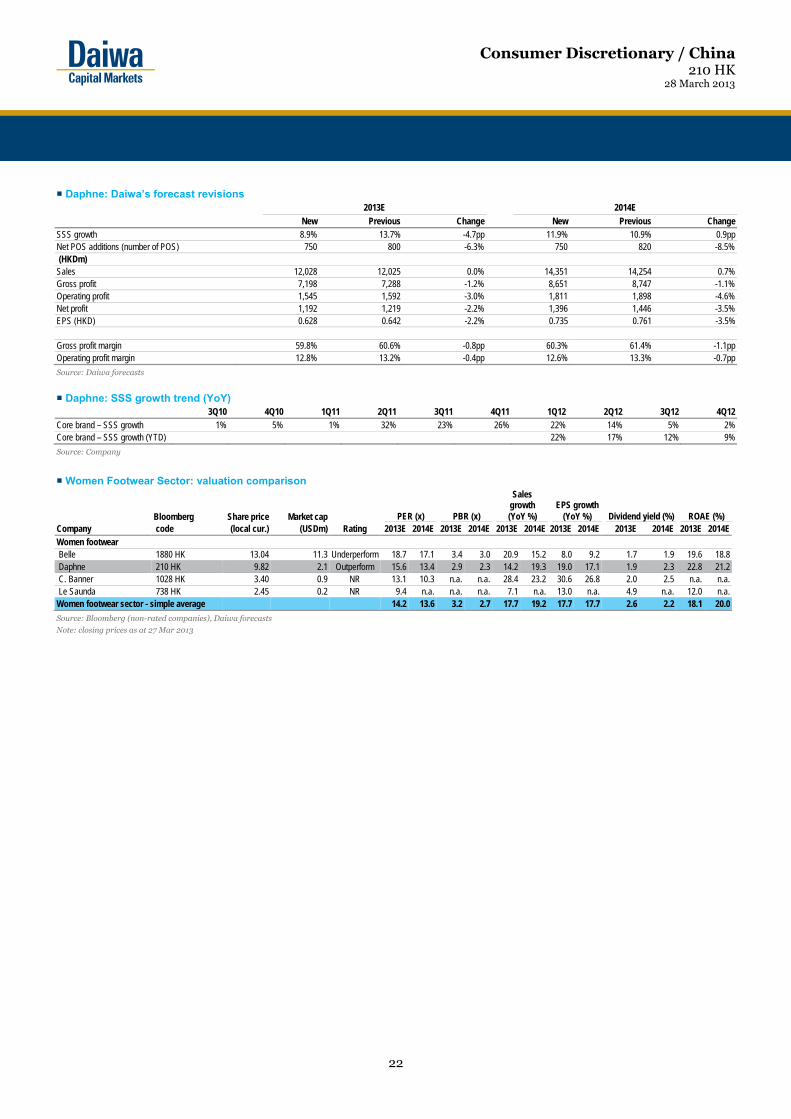

■ What's new We hosted investor meetings with Daphne in Singapore on 27 March 2013, during which we learned that the company plans to focus on its core brands this year, and implement more cost-cutting measures to boost its bottom line. ■ What's the impact SSS growth. We expect Daphne’s 1Q13 SSS growth to be flat YoY. In terms of monthly trends, we expect the combined January-February SSS growth to decline by a double-digit percentage, while strong double-digit growth for March is likely to have been driven by both sales volume and an ASP recovery. We still think the 1H13 SSS growth will be soft due to China’s slower-than-expected macro recovery, and a very high base for the same period last year (1H12 SSS growth: 17%). Store expansion strategy. Daphne has more than 7,000 points of sale (POS) and expects to add 700 core brands a year from 2013, with an annual increase of 50 POS for its mid- to high-end brands over 2013-

15, based on our estimates (a far cry from last year’s target POS growth of 200 a year). In terms of expanding its core brands, Daphne continues to increase its store count, predominantly in China’s third/fourth-tier cities. However, we do not rule out possible expansion in areas that are on the outskirts of the first/second-tier cities. It is worth noting that of the 767 new store additions in 2012, 46% of them were in the rural areas of these first/second-tier cities. We have found that purchasing habits and demand in these rural regions are similar to those in the third/fourth-tier cities. While the company’s promotional patterns and products vary across China, we do not think lower ASPs necessarily translate into smaller margins. Moreover, management said that the ramp-up of new stores in the lower-tier cities has been good, and that in their first year of operation most of them were running at 70-75% of the efficiency of a well-established (mature) store. Cost-cutting measures. Management’s 2013 cost-cutting strategy includes: 1) staff-related costs and productivity enhancement, 2) carefully selecting locations for new POS and closing poorly performing stores, and 3) the opening of smaller stores and maximising floor space, which should improve rent/sales ratios. ■ What we recommend We are cutting our 2013 earnings forecast by 2.2% as we are lowering our SSS growth forecast to 8.9% YoY (13.7% YoY previously) to reflect potentially weak 1H13 SSS. As a result of these changes, we are

cutting our six-month target price to HKD11.10 (from HKD11.40), based on an unchanged target PER of 17.7x, which is 1SD above Daphne’s average forward PER for 2010-12. We maintain our Outperform (2) rating. Risks to our call would include lower-than-expected SSS growth in 2013. ■ How we differ Our 2013 net-profit forecast is 5.6% higher than that of the Bloomberg consensus, probably because we are more positive on the company’s operating leverage.

28 March 2013

Operating leverage intact

• SSS growth likely to have rebounded strongly in March

• Management is making tangible cost cuts this year

• Maintain Outperform rating

Source: Daiwa forecasts

Source: FactSet, Daiwa forecasts

Consumer Discretionary / China

Daphne International210 HK

BuyOutperform (unchanged)

HoldUnderperformSell

1

2

3

4

5Target (HKD): 11.40 11.10 Upside: 13.0% 27 Mar price (HKD): 9.82

Bing Zhou(852) 2773 [email protected]

Cris Xu(852) 2773 [email protected]

Forecast revisions (%)Year to 31 Dec 13E 14E 15ERevenue change - 0.7 n.a.Net profit change (2.2) (3.5) n.a.Core EPS (FD) change (2.2) (3.5) n.a.

65

76

88

99

110

6

8

9

11

12

Mar-12 Jun-12 Sep-12 Dec-12 Mar-13

Share price performance

Daphne Int (LHS) Relative to HSI (RHS)

(HKD) (%)

12-month range 6.67-11.78Market cap (USDbn) 2.083m avg daily turnover (USDm) 5.87Shares outstanding (m) 1,644Major shareholder Chen Family (24.4%)

Financial summary (HKD)Year to 31 Dec 13E 14E 15ERevenue (m) 12,028 14,351 17,130Operating profit (m) 1,545 1,811 2,135Net profit (m) 1,192 1,396 1,648Core EPS (fully-diluted) 0.628 0.735 0.867EPS change (%) 19.0 17.1 18.1Daiwa vs Cons. EPS (%) (2.4) (4.5) (4.4)PER (x) 15.6 13.4 11.3Dividend yield (%) 1.9 2.3 2.7DPS 0.187 0.224 0.269PBR (x) 2.9 2.3 2.1EV/EBITDA (x) 7.4 5.9 4.4ROE (%) 22.8 21.2 20.3

Consumer Discretionary / China 210 HK

28 March 2013

22

Daphne: Daiwa’s forecast revisions 2013E 2014E

New Previous Change New Previous ChangeSSS growth 8.9% 13.7% -4.7pp 11.9% 10.9% 0.9ppNet POS additions (number of POS) 750 800 -6.3% 750 820 -8.5% (HKDm) Sales 12,028 12,025 0.0% 14,351 14,254 0.7%Gross profit 7,198 7,288 -1.2% 8,651 8,747 -1.1%Operating profit 1,545 1,592 -3.0% 1,811 1,898 -4.6%Net profit 1,192 1,219 -2.2% 1,396 1,446 -3.5%EPS (HKD) 0.628 0.642 -2.2% 0.735 0.761 -3.5% Gross profit margin 59.8% 60.6% -0.8pp 60.3% 61.4% -1.1ppOperating profit margin 12.8% 13.2% -0.4pp 12.6% 13.3% -0.7pp

Source: Daiwa forecasts

Daphne: SSS growth trend (YoY)

3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12

Core brand – SSS growth 1% 5% 1% 32% 23% 26% 22% 14% 5% 2%Core brand – SSS growth (YTD) 22% 17% 12% 9%

Source: Company

Women Footwear Sector: valuation comparison

Bloomberg Share price Market cap PER (x) PBR (x)

Sales growth (YoY %)

EPS growth (YoY %) Dividend yield (%) ROAE (%)

Company code (local cur.) (USDm) Rating 2013E 2014E 2013E 2014E 2013E 2014E 2013E 2014E 2013E 2014E 2013E 2014E Women footwear Belle 1880 HK 13.04 11.3 Underperform 18.7 17.1 3.4 3.0 20.9 15.2 8.0 9.2 1.7 1.9 19.6 18.8 Daphne 210 HK 9.82 2.1 Outperform 15.6 13.4 2.9 2.3 14.2 19.3 19.0 17.1 1.9 2.3 22.8 21.2 C. Banner 1028 HK 3.40 0.9 NR 13.1 10.3 n.a. n.a. 28.4 23.2 30.6 26.8 2.0 2.5 n.a. n.a. Le Saunda 738 HK 2.45 0.2 NR 9.4 n.a. n.a. n.a. 7.1 n.a. 13.0 n.a. 4.9 n.a. 12.0 n.a.Women footwear sector - simple average 14.2 13.6 3.2 2.7 17.7 19.2 17.7 17.7 2.6 2.2 18.1 20.0

Source: Bloomberg (non-rated companies), Daiwa forecasts

Note: closing prices as at 27 Mar 2013

Consumer Discretionary / China 210 HK

28 March 2013

23

Key assumptions

Profit and loss (HKDm)

Cash flow (HKDm)

Source: FactSet, Daiwa forecasts

Year to 31 Dec 2008 2009 2010 2011 2012 2013E 2014E 2015Enumber of stores 3,642 4,225 5,199 6,165 6,881 7,631 8,381 9,131Core-brand same store sales growth n.a. 5.0 4.6 21.0 9.0 9.0 12.5 12.5Gross margin (%) 52.7 55.0 57.4 61.1 59.2 59.8 60.3 60.7EBIT margin (%) 12.8 14.7 14.1 15.2 12.6 12.8 12.6 12.5

Year to 31 Dec 2008 2009 2010 2011 2012 2013E 2014E 2015ECore brands 4,265 5,018 5,697 7,671 9,592 11,135 13,429 16,096Other brands 404 279 430 530 691 683 744 882Other Revenue 620 536 497 376 246 210 179 151Total Revenue 5,289 5,832 6,624 8,577 10,529 12,028 14,351 17,130Other income (8) 21 63 (16) 47 39 41 42COGS (2,502) (2,625) (2,823) (3,333) (4,300) (4,830) (5,701) (6,727)SG&A (2,103) (2,371) (2,930) (3,922) (4,954) (5,692) (6,881) (8,310)Other op.expenses 0 0 0 0 0 0 0 0Operating profit 676 856 935 1,305 1,322 1,545 1,811 2,135Net-interest inc./(exp.) (11) (20) (8) 16 (6) 17 60 108Assoc/forex/extraord./others 1 1 1 0 (8) (2) 0 2Pre-tax profit 666 837 927 1,322 1,307 1,560 1,871 2,245Tax (169) (233) (239) (377) (333) (397) (476) (571)Min. int./pref. div./others (4) (7) (16) (12) (19) (18) (23) (26)Net profit (reported) 493 597 673 933 956 1,146 1,372 1,648Net profit (adjusted) 493 823 792 979 1,002 1,192 1,396 1,648EPS (reported)(HKD) 0.301 0.365 0.411 0.570 0.581 0.697 0.775 0.898EPS (adjusted)(HKD) 0.301 0.502 0.483 0.597 0.610 0.725 0.788 0.898EPS (adjusted fully-diluted)(HKD) 0.301 0.474 0.424 0.522 0.528 0.628 0.735 0.867DPS (HKD) 0.055 0.075 0.105 0.149 0.156 0.187 0.224 0.269EBIT 676 856 935 1,305 1,322 1,545 1,811 2,135EBITDA 794 992 1,077 1,491 1,579 1,934 2,293 2,721