asia pacific petroleum conference - platts · asia pacific petroleum conference ... middle east...

TRANSCRIPT

© OECD/IEA - 2016

Asia Pacific Petroleum Conference

“Where are oil prices headed"

Singapore, 7 September 2016

Mr. Keisuke Sadamori

Director, Directorate of Energy Markets and Security

© OECD/IEA - 2016

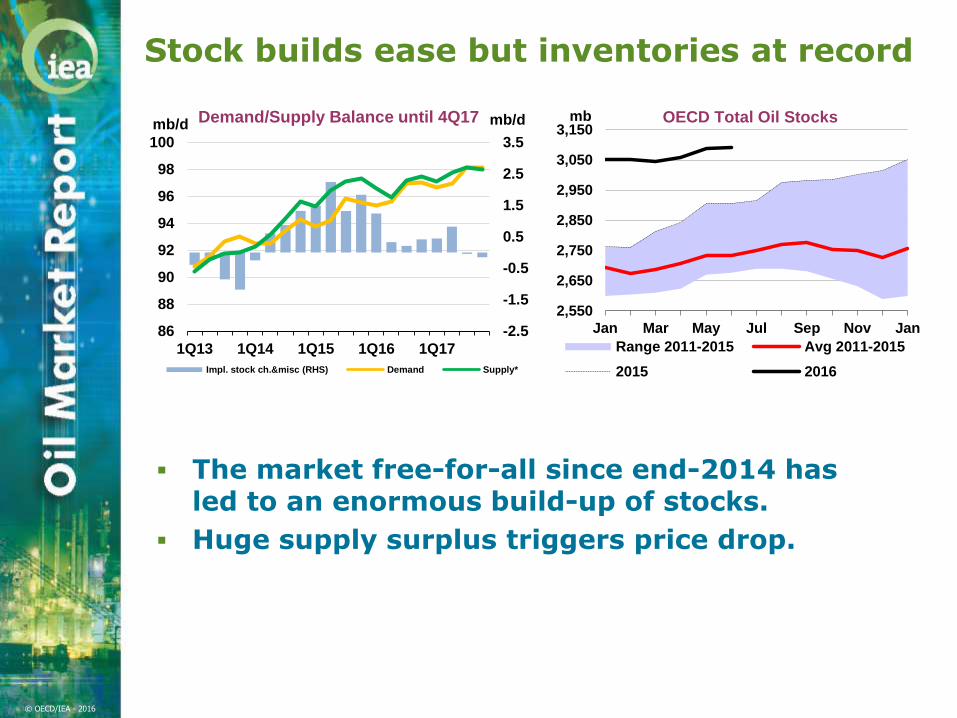

Stock builds ease but inventories at record

The market free-for-all since end-2014 has led to an enormous build-up of stocks.

Huge supply surplus triggers price drop.

-2.5

-1.5

-0.5

0.5

1.5

2.5

3.5

86

88

90

92

94

96

98

100

1Q13 1Q14 1Q15 1Q16 1Q17

mb/dmb/d Demand/Supply Balance until 4Q17

Impl. stock ch.&misc (RHS) Demand Supply*

2,550

2,650

2,750

2,850

2,950

3,050

3,150

Jan Mar May Jul Sep Nov Jan

mb OECD Total Oil Stocks

Range 2011-2015 Avg 2011-2015

2015 2016

© OECD/IEA - 2016

2016 demand growth eases from recent highs – but remains robust

-500

0

500

1000

1500

2000

2500

1Q2014 3Q2014 1Q2015 3Q2015 1Q2016

kb/d Global Oil Demand Growth, y-o-y

Japan China India US Total

© OECD/IEA - 2016

Chinese slowdown key to lower demand growth

-750

-500

-250

0

250

500

750

1000

1250

1500

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

kb/d Chinese Oil Demand Growth, y-o-y

Gasoline/Jet/Kerosene Gasoil

FO/other LPG/naphtha

Total

© OECD/IEA - 2016

India’s rapid demand growth eases

0

100

200

300

400

500

600

Jan-14 Jul-14 Jan-15 Jul-15 Jan-16

kb/d Indian Demand Growth, y-o-y

Gasoline/Jet/Kerosene Gasoil

FO/other LPG/naphtha

Total

© OECD/IEA - 2016

Global oil supply growth grinds to halt

-1.5-1.0-0.50.00.51.01.52.02.53.03.54.04.5

Jan 14 Jul 14 Jan 15 Jul 15 Jan 16 Jul 16

mb/d

Thousands

OPEC and Non-OPEC Oil Supply Year-on-Year Change

OPEC Crude Non-OPEC

OPEC NGLs Total Supply

© OECD/IEA - 2016

Record Mideast output boosts OPEC

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

Jan 14 Jun 14 Nov 14 Apr 15 Sep 15 Feb 16 Jul 16

mb/d OPEC Growth y-o-y

Other OPEC Iraq Saudi Arabia

Iran OPEC

© OECD/IEA - 2016

Middle East share rises to highest since 1970s

0%

10%

20%

30%

40%

0

20

40

60

80

100

mb/d Middle East Share of Global Supply*

Middle East Other

Middle East Share

*Excl. Biofuels and refinery processing gains

© OECD/IEA - 2016

Non-OPEC plunges but recovery on horizon

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

1Q13 1Q14 1Q15 1Q16 1Q17

mb/d

Other North America Total

Total Non-OPEC Supply, y-o-y Change

© OECD/IEA - 2016

US producers turn corner in 2017

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

1Q13 1Q14 1Q15 1Q16 1Q17

mb/d US Total Oil Supply - Yearly Change

Alaska California Texas

Gulf of Mexico NGLs North Dakota

Other Total

© OECD/IEA 2016

Looking further ahead

Demand growth solid at 1.2 mb/d through 2021

Production growth slashed as investment cuts bite

Crude trade shifts more and more eastwards

Huge uncertainties

OPEC production policy

Non-OPEC

World economy

Efficiency gains

© OECD/IEA 2016

World oil demand growth slows

Cools from 1.7%/yr in 2009-15 to 1.2%/yr in 2016-2021

2009-15

2015-21

© OECD/IEA, 2016(kb/d)

-179 -76138 52

283

27

164 215

104 155

Americas

Africa

Middle East

Europe

FSU

969826

Asia/Pacific

© OECD/IEA 2016

World supply growth plunges

2015-21 growth slows to 4.1 mb/d vs 11 mb/d in 2009-15

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2014 2015 2016 2017 2018 2019 2020 2021

mb/d

OPEC Non-OPEC

*2014 -15 shows actual output growth. 2016 assumes Iran ramp-up. OPEC capacity increases thereafter.

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2014 2015 2016 2017 2018 2019 2020 2021

mb/d

OPEC Non-OPEC World

*2014 -15 shows actual output growth. 2016 assumes Iran ramp-up. OPEC capacity increases thereafter.

© OECD/IEA 2016

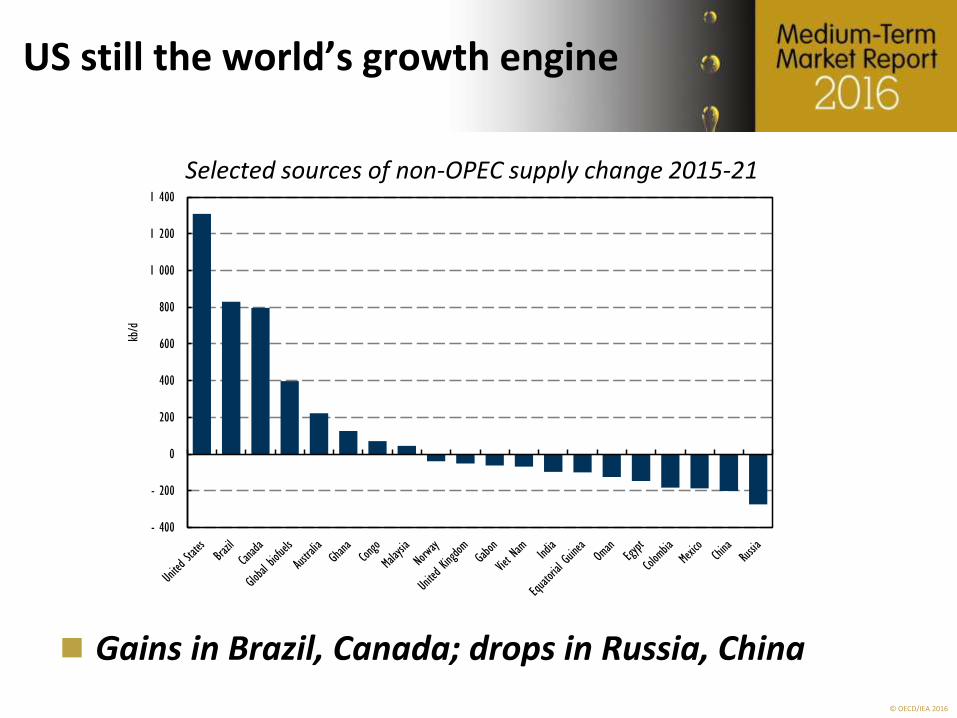

US still the world’s growth engine

Gains in Brazil, Canada; drops in Russia, China

Selected sources of non-OPEC supply change 2015-21

- 400

- 200

0

200

400

600

800

1 000

1 200

1 400

kb/d

© OECD/IEA 2016

Middle East leads OPEC growth

-0.10

-0.05

0.00

0.05

0.10

0.15

0.20

0.25

2016 2017 2018 2019 2020 2021

mb/d

Iran Iraq UAE Other Total OPEC

© OECD/IEA 2016

Crude trade to shift eastwards

Crude Exports in 2021 and Growth in 2015-21 for Key Trade Routes1

(million barrels per day)

0.1

(+0)

0.3 0.2

(+0) 2.2 (+0.2)

(-0.5) 4.0 0.1(-1) (+0)

0.3

(-0.1) 4.7

1.5 (+1.1)

1.8 (+0.2)

-0.2

1.0

1.4 (+0.1)

(-0.1)

0.4(+0)

Red number in brackets denotes growth in period 2015-21 0.81Excludes Intra-Regional Trade (+0)2 Includes Chile3 Includes Israel

6.1

(+0.9)

Other Asia

China

OECD Europe

2.4(+0.0)

1.2 (+0.3)

OECD Asia

Oceania3

0.5 (-0.2)

0.8(+0.3)

3.9 (-0.3)

OECDAmericas2

© OECD/IEA 2016

Oil markets return to balance

In 2014 and 2015, oil supply greatly exceeded demand; the oil market is likely to return to balance in 2017, with high stock levels dampening any price recovery

-2

-1

0

1

2

3

2014 2015 2016 2017 2018 2019 2020 2021

mb/d

Demand Growth Supply Growth Stock change

© OECD/IEA 2016

IEA Oil Market Analysis

Thank you for listening!