assignment on financial management

TRANSCRIPT

ASSIGNMENT ON FINANCIAL MANAGEMENT

ASSIGNMENT ON FINANCIAL

MANAGEMENT

BY RAHUL GUPTAQ.1: Is Equity Capital Free of cost? Substantiate your statement.

Answer:

No. Equity Capital is not free of cost. Some people are of the opinion that equity capital is free of cost for the reason that a company is not legally bound to pay dividends and also the rate of equity dividend is not fixed like preference dividends.

This is not a correct view as equity shareholders buy shares with the expectation of dividends and capital appreciation.

Dividends enhance the market value of shares and therefore equity capital is not free of cost.

RAHUL GUPTA, MBAHCS (2ND SEM), SUNJECT CODE-MB0029, SET-2 Page 1

ASSIGNMENT ON FINANCIAL MANAGEMENT

Equity shareholders do not have a fixed rate of return on their investment.

There is no legal requirement (unlike in the case of loans or debentures where the rates are governed by the deed) to pay regular dividends to them.

Measuring the rate of return to equity holders is a difficult and complex exercise.

There are many approaches for estimating return - the dividend forecast approach, capital asset pricing approach, realized yield approach, etc.

According to dividend forecast approach, the intrinsic value of an equity share is the sum of present values of dividends associated with it.

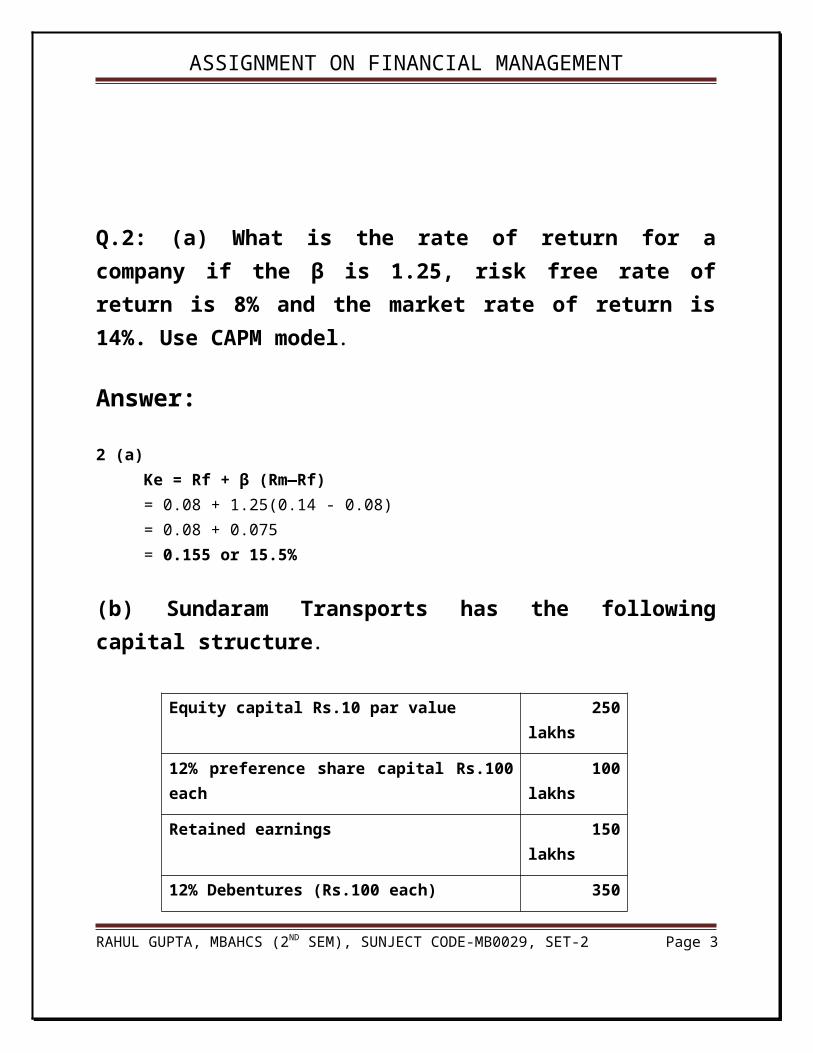

Q.2: (a) What is the rate of return for a company if the β is 1.25, risk free rate of return is 8% and the market rate of return is 14%. Use CAPM model.

Answer:

2 (a)Ke = Rf + β (Rm—Rf) = 0.08 + 1.25(0.14 - 0.08) = 0.08 + 0.075= 0.155 or 15.5%

(b) Sundaram Transports has the following capital structure.

Equity capital Rs.10 par value 250 lakhs

RAHUL GUPTA, MBAHCS (2ND SEM), SUNJECT CODE-MB0029, SET-2 Page 2

ASSIGNMENT ON FINANCIAL MANAGEMENT

12% preference share capital Rs.100 each 100 lakhs

Retained earnings 150 lakhs

12% Debentures (Rs.100 each) 350 lakhs

14% Term loan from SBI 150 lakhs

Total 1000 lakhs

The market price per equity is Rs 54. The company is expected to declare a dividend per share of Rs.2 per share and there will be a growth of 10% in the dividends for the next 5 years. The preference shares are redeemable at a premium of Rs.5 per share after 8 years. The current market price of preference share is Rs.92. Debenture redemption will take place after 7 years at a discount of 2% and the current market price is Rs.91 per debenture. The corporate tax rate is 40%. Calculate WACC.

Answer:

2(b)Ke is the cost of external equity, D1 is the dividend expected at the end of year 1 = 2, P 0 is the current market price per share = Rs. 92, g is the constant growth rate of dividends = 10%, f is the floatation costs as % of current market price.

Step I is to determine the cost of each component.

Cost of external equity: Ke =( D1/P0) + g = (2/54) + 0.1 = 0.137 or 13.7%

RAHUL GUPTA, MBAHCS (2ND SEM), SUNJECT CODE-MB0029, SET-2 Page 3

ASSIGNMENT ON FINANCIAL MANAGEMENT

Cost of preference capital:

Kp = D + {(F—P)/n} / (F+P)/2

D is the preference dividend per share payable=11

F is the redemption price=105

P is the net proceeds per share = 92

n is the maturity period =8

Kp = D + {(F—P)/n} / (F+P)/2

= 11 + (105—92)/8] / (105+92)/2 =12.625/98.5 = 0.1281 or 12.81%

Cost of Retained Earnings:Kr=Ke which is 13.7%

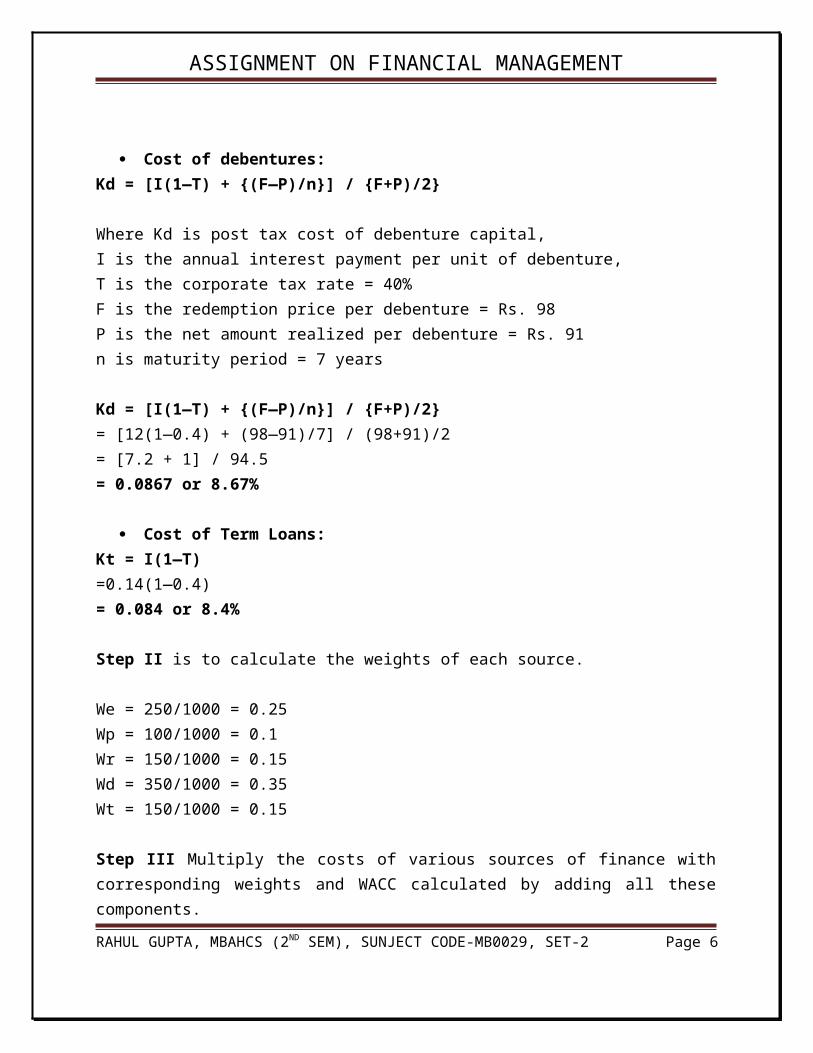

Cost of debentures:Kd = [I(1—T) + {(F—P)/n}] / {F+P)/2}

Where Kd is post tax cost of debenture capital, I is the annual interest payment per unit of debenture, T is the corporate tax rate = 40%F is the redemption price per debenture = Rs. 98 P is the net amount realized per debenture = Rs. 91 n is maturity period = 7 years

Kd = [I(1—T) + {(F—P)/n}] / {F+P)/2} = [12(1—0.4) + (98—91)/7] / (98+91)/2 = [7.2 + 1] / 94.5 = 0.0867 or 8.67%

RAHUL GUPTA, MBAHCS (2ND SEM), SUNJECT CODE-MB0029, SET-2 Page 4

ASSIGNMENT ON FINANCIAL MANAGEMENT

Cost of Term Loans:Kt = I(1—T) =0.14(1—0.4) = 0.084 or 8.4%

Step II is to calculate the weights of each source.

We = 250/1000 = 0.25 Wp = 100/1000 = 0.1 Wr = 150/1000 = 0.15Wd = 350/1000 = 0.35 Wt = 150/1000 = 0.15

Step III Multiply the costs of various sources of finance with corresponding weights and WACC calculated by adding all these components.

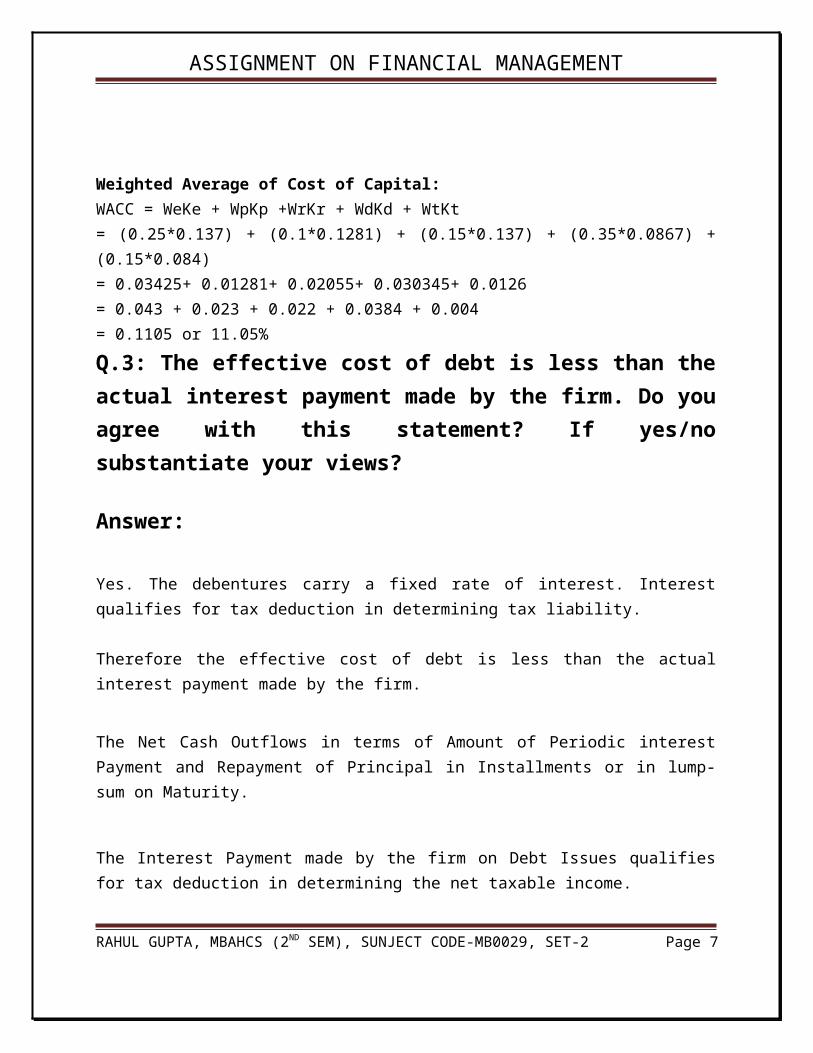

Weighted Average of Cost of Capital:WACC = WeKe + WpKp +WrKr + WdKd + WtKt = (0.25*0.137) + (0.1*0.1281) + (0.15*0.137) + (0.35*0.0867) + (0.15*0.084) = 0.03425+ 0.01281+ 0.02055+ 0.030345+ 0.0126= 0.043 + 0.023 + 0.022 + 0.0384 + 0.004 = 0.1105 or 11.05%

Q.3: The effective cost of debt is less than the actual interest payment made by the firm. Do you agree with this statement? If yes/no substantiate your views?

Answer:

Yes. The debentures carry a fixed rate of interest. Interest qualifies for tax deduction in determining tax liability.

Therefore the effective cost of debt is less than the actual interest payment made by the firm.

The Net Cash Outflows in terms of Amount of Periodic interest Payment and Repayment of Principal in Installments or in lump-sum on Maturity.

RAHUL GUPTA, MBAHCS (2ND SEM), SUNJECT CODE-MB0029, SET-2 Page 5

ASSIGNMENT ON FINANCIAL MANAGEMENT

The Interest Payment made by the firm on Debt Issues qualifies for tax deduction in determining the net taxable income.

Therefore, the effective cash outflow is less than the actual payment of Interest made by the firm to the debt holders by the amount of tax shield on Interest Payment.

The debt can either be Perpetual/Irredeemable or Redeemable.

Q.4: Why capital budgeting decision very crucial for finance managers?

Answer:

There are many reasons that make the Capital budgeting decisions the most crucial for finance Managers:

1. These decisions involve large outlay of funds now in anticipation of cash flows in future. For example, investment in plant and machinery. The economic life of such assets has long periods. The projections of cash flows anticipated involve forecasts of many financial variables. The most crucial variable is the sales forecast.

a. For example, Metal Box spent large sums of money on expansion of its production facilities based on its own sales forecast. During this period, huge investments in R & D in

RAHUL GUPTA, MBAHCS (2ND SEM), SUNJECT CODE-MB0029, SET-2 Page 6

ASSIGNMENT ON FINANCIAL MANAGEMENT

packaging industry brought about new packaging medium totally replacing metal as an important component of packing boxes. At the end of the expansion Metal Box Ltd found itself that the market for its metal boxes had declined drastically. The end result is that Metal Box became a sick company from the position it enjoyed earlier prior to the execution of expansion as a blue chip. Employees lost their jobs. It affected the standard of lining and cash flow position of its employees. This highlights the element of risk involved in these type of decisions.

b. Equally we have empirical evidence of companies which took decisions on expansion through the addition of new products and adoption of the latest technology creating wealth for shareholders. The best example is the Reliance group.

c. Any serious error in forecasting Sales and hence the amount of capital expenditure can significantly affect the firm. An upward bias may lead to a situation of the firm creating idle capacity, laying the path for the cancer of sickness.

d. Any downward bias in forecasting may lead the firm to a situation of losing its market to its competitors. Both are risky fraught with grave consequences.

2. A long term investment of funds some times may change the risk profile of the firm. A FMCG company with its core competencies in the business decided to enter into a new business of power generation. This decision will totally alter the risk profile of the business of the company. Investor’s perception of risk of the new business to be taken up by the company will change his required rate of return to invest in the company. In this connection it is to be noted that the power pricing is a politically sensitive area affecting the profitability of the organization. Therefore, Capital budgeting decisions change the risk dimensions of the company and hence the required rate of return that the investors want.

3. Most of the Capital budgeting decisions involve huge outlay. The funds requirements during the phase of execution must be synchronized with the flow of funds. Failure to achieve the required coordination between the inflow and outflow may cause time over run and cost over run. These two problems of time over run and cost over run have to be prevented from occurring in the beginning of execution of the project. Quite a lot empirical examples are there

RAHUL GUPTA, MBAHCS (2ND SEM), SUNJECT CODE-MB0029, SET-2 Page 7

ASSIGNMENT ON FINANCIAL MANAGEMENT

in public sector in India in support of this argument that cost over run and time over run can make a company’s operations unproductive. But the major challenge that the management of a firm faces in managing the uncertain future cash inflows and out flows associated with the plan and execution of Capital budgeting decisions.

4. Capital budgeting decisions involve assessment of market for company’s products and services, deciding on the scale of operations, selection of relevant technology and finally procurement of costly equipment. If a firm were to realize after committing itself considerable sums of money in the process of implementing the Capital budgeting decisions taken that the decision to diversify or expand would become a wealth destroyer to the company, then the firm would have experienced a situation of inability to sell the equipments bought. Loss incurred by the firm on account of this would be heavy if the firm were to scrap the equipments bought specifically for implementing the decision taken. Sometimes these equipments will be specialized costly equipments. Therefore, Capital budgeting decisions are irreversible.

5. The most difficult aspect of Capital budgeting decisions is the influence of time. A firm incurs Capital expenditure to build up capacity in anticipation of the expected boom in the demand for its products. The timing of the Capital expenditure decision must match with the expected boom in demand for company’s products. If it plans in advance it may effectively manage the timing and the quality of asset acquisition. But many firms suffer from its inability to forecast the future operations and formulate strategic decision to acquire the required assets in advance at the competitive rates.

6. All Capital budgeting decisions have three strategic elements. These three elements are cost, quality and timing. Decisions must be taken at the right time which would enable the firm to procure the assets at the least cost for producing the products of required quality for customer. Any lapse on the part of the firm in understanding the effect of these elements on

RAHUL GUPTA, MBAHCS (2ND SEM), SUNJECT CODE-MB0029, SET-2 Page 8

ASSIGNMENT ON FINANCIAL MANAGEMENT

implementation of Capital expenditure decision taken will strategically affect the firm’s profitability.

7. Liberalization and globalization gave birth to economic institutions like World Trade organization. General Electrical can expand its market into India snatching the share already enjoyed by firms like Bajaj Electricals or Kirloskar Electric Company. Ability of G E to sell its products in India at a rate less than the rate at which Indian Companies sell cannot be ignored. Therefore, the growth and survival of any firm in today’s business environment demands a firm to be proactive. Proactive firms cannot avoid the risk of taking challenging Capital budgeting decisions for growth. Therefore, Capital budgeting decisions for growth have become an essential characteristics of successful firms today.

8. The social, political, economic and technological forces generate high level of uncertainty in future cash flows streams associated with Capital budgeting decisions. These factors make these decisions highly complex.

9. Capital expenditure decisions are very expensive. To implement these decisions firm’s will have to tap the Capital market for funds. The composition of debt and equity must be optimal keeping in view the expectation of investors and risk profile of the selected project.

Q.5: A road project require an initial investment of Rs.10,00,000. It is expected to generate the following cash flow in the form of toll tax recovery.

Year Cash Inflows1 4,50,0002 4,25,0003 3,00,0004 3,50,000

What is the IRR of the project?

RAHUL GUPTA, MBAHCS (2ND SEM), SUNJECT CODE-MB0029, SET-2 Page 9

ASSIGNMENT ON FINANCIAL MANAGEMENT

Ans.

To calculate Internal Rate of Return (IRR):

Step I: Compute the average of annual cash inflows

Year Cash Inflow in Rs.

1 4,50,000

2 4,25,000

3 3,00,000

4 3,50,000

Total 15,25,000

Average = 15,00,000 / 4 = Rs. 3,81,250

Step II: Divide the initial investment by the average of annual cash inflows:

=10,00,000 / 3,81,250

=2.622

Step III: From the PVIFA table for 4 years, the annuity factor very near to 2.622 is 20%. Therefore

the first initial rate is 20%

Year Cash flows PV factor at 20% PV of Cash

1 4,50,000 0.833 3,74,850

2 4,25,000 0.694 2,94,950

3 3,00,000 0.579 1,73,700

4 3,50,000 0.482 1,68,700

Total 10,12,200

RAHUL GUPTA, MBAHCS (2ND SEM), SUNJECT CODE-MB0029, SET-2 Page 10

ASSIGNMENT ON FINANCIAL MANAGEMENT

Since the initial investment of Rs.10,00,000 is less than the computed value at 20% of

Rs. 10,12,200 then next trial rate is 22%.

Year Cash flows PV factor at 22% PV of Cash

1 4,50,000 0.82 3,69,000

2 4,25,000 0.672 2,85,600

3 3,00,000 0.551 1,65,300

4 3,50,000 0.451 1,57,850

Total 9,77,750

Since initial investment of Rs.10,00,000 lies between 9,77,750 (22%) and 10,12,200 (20%), the IRR by interpolation is,

IRR = 20 + ((10,12,200-10,00,000) / (10,12,200-9,77,750))*2

= 20 + 0.3541 *2

= 20.70%

Q.6: What is sensitivity analysis? Mention the steps involved in it.

Answer:

Sensitivity Analysis:1. There are many variables like sales, cost of sales, investments, tax rates etc which affect

the NPV and IRR of a project.

2. Analysing the change in the project’s NPV or IRR on account of a given change in one of the variables is called Sensitivity Analysis.

RAHUL GUPTA, MBAHCS (2ND SEM), SUNJECT CODE-MB0029, SET-2 Page 11

ASSIGNMENT ON FINANCIAL MANAGEMENT

3. It is a technique that shows the change in NPV given a change in one of the variables that determine cash flows of a project.

4. It measures the sensitivity of NPV of a project in respect to a change in one of the input variables of NPV.

5. The reliability of the NPV depends on the reliability of cash flows.

6. If forecasts go wrong on account of changes in assumed economic environments, reliability of NPV & IRR is lost.

7. Therefore, forecasts are made under different economic conditions viz pessimistic, expected and optimistic. NPV is arrived at for all the three assumptions.

Steps involved in Sensitivity analysis:

1. Identification of variables that influence the NPV & IRR of the project.

2. Examining and defining the mathematical relationship between the variables.

3. Analysis of the effect of the change in each of the variables on the NPV of the project.

RAHUL GUPTA, MBAHCS (2ND SEM), SUNJECT CODE-MB0029, SET-2 Page 12