attitude of students toward credit card

TRANSCRIPT

Attitudes of students towards credit cardsukessays.com /essays/marketing/attitudes-of-students-towards-credit-cards-marketing-essay.php

1.0 Introduction

The attitudes of students towards credit cards is quite complex subject, one that when measuredneeds to combine both demographic and attitudinal data to provide a complete picture of the topic.Before we go further, here are briefly discussed about credit card scenario in Malaysia.

According to a newspaper report in 2008, total bankrupted of individuals because credit card debt inlast year is 1,873 people. Credit card holder in this country fail to settled loan debts which hitRM21.6 billion until last September 2008. Of the number, as much as RM591 million was NonPerforming Loan (NPL). Apparently trend of use the credit card among present youth has alreadybecame a priority to show standard and modern lifestyle without realize them would bebecome 'slave' lifelong debt. This is due to fail manage the usage nicely and well-mannered. Creditcard usage has its advantages and disadvantages. As long the owner of credit card can control itsusage according to smart financial plan, then, it will return some valuable to the owners.

2.0 Rationale for using e-mail survey

Electronic mail or e-mail has revolutionized communication process by allowing users to transmit andreceived information from virtually all around the world when the users connected online. The usersinstantly get the email message and relatively low cost compare to conventional mail.

Email is one of the types of self-administered survey questionnaire that is filled in by respondent inelectronic environment. In this way, respondent will more convenience to fill up the questionnaire interm of anonymity and time controlling to complete the survey.

Email survey research is the systematic data collection of information on a specific topic usingquestionnaires delivered to an online sample or population. The respondents will receive, complete,and return their questionnaires answer via email. With the growth of online networks around the world,it is feasible to see an increase in the use of email in survey research.

3.0 Research methodology

Research issue

There are several issues in this overall report regarding to design questionnaire and collecting datathrough email survey. To design the questionnaire, the questions were divided into two parts which areparts A is for respondents who has a credit card and Part B for without credit cards. These are toensure clear and precise data gathering from both categories. The collecting data from respondents isa major problem as well. Reluctance to gain feedback or reply from respondents is quite high. Toovercome this problem, some techniques have been practiced such as call back through telephone lineto respondents and send email reminder. There are some questionnaire email was undelivered torespondents and need to send to secondary respondent email address. Another issue is the questiongiven in questionnaire was incomplete filled and need to ask again from several respondentsanswered.

Research goal

In completing this survey and resulting analysis, the following research goals were first defined:

Discover through the use of seven questions of demographic characteristic of who are have or not have

a credit card especially relating in income group.

Measure students’ attitudes to using credit cards to feel better about themselves, specifically more incontrol of their lives and feeling more important or privileged when they get a credit card.

Measure students’ attitude towards credit cards to feel about themselves for those is not using a creditcard.

Methodology

Approximately about 10 students were send the questionnaire by using OUM email address and thesampling focused on 5 male students and 5 female students to avoid bias. The method of sendingemail is randomly send according to email features which is the list of email recipients name willautomatically display when I fill the first alphabet. It means that, for example when we press ‘A’ at the‘to’ column, then OUM email will shows the list of the names which are start with ‘a’ such as ‘ahmadrasky’, ahmad saiful’, etc. About two weeks after the questionnaire has sent to all, 10 replies hassuccessfully collected. Nevertheless, the samplings are about 7 male and 3 female. This is due to timelimitation of waiting reply from target respondents. The anonymity of respondents was assured bywhere they are from. The questionnaire itself includes 7 demographic questions.

Good questionnaire have to be as simple as it can, and the method of answering must within short timeas well. To do that way, the question given is quite simple, short and the way to reply answers is moreconvenience to respondents where they are only required to reply with draft email and only need tounderline the answers given and send. Below are the lists of original design question where had beensend to target respondents:

This is simple and easy step to reply. Just click 'reply' with draft,underline the answers and send..

SURVEY ON STUDENT’S ATTITUDE TOWARD CREDIT CARDS

Demographic Characteristics:

Kindly underline at the answer chosen:

1. Age:

a. <25

b. 26-40

c. 41-55

d. 56 and above

2. Gender:

a. Male

b. Female

3. Race:

a. Malay

b. Chinese

c. India

d. Others

4. Marital Status:

a. Single

b. Married

c. Divorce

5. Course undertaking/current Level:

a. Diploma

b. Degree

c. Master

d. PhD

e. Others

6. Work position:

a. Private sector

b. Government sector

c. Others

7. Monthly net Income:

a. < RM 1000

b. RM1000-RM1999

c. RM 2000-RM2999

d. >RM3000

10 questions in Part A has been designed, which are respondents who have a credit card and 10questions in Part B which is to respondents who do not have credit card. Each of these questions wereresponded to on a five-point scale comprised of 1) Strongly disagree, 2) Disagree, 3) Neutral, 4) Agreeand 5) Strongly agree. The following attitudinal statements were responded to in the questionnaire:

Student’s Attitude Toward Credit Cards:

Did you have a credit card?

a. Yes (if ‘yes’, answer part (A) only)

b. No (Proceed to questions on part (B) and ignore the part (A) questions )

Part (A)

By using the scale given, please indicate your reason of using credit cards.Kindly underline at thenumber that best describes your reason:

Scale indicator: 1. Strongly disagree 2. Disagree 3. Neutral 4. Agree 5. StronglyAgree

(a) Credit card used for medical expenses

and family related emergencies 1 2 3 4 5

(b) Credit card used for making travel

arrangements and reservations 1 2 3 4 5

(c) Credit card used as a method of payment

for shopping by internet 1 2 3 4 5

(d) Credit card used to pay for education-

related expenses such as fees and books. 1 2 3 4 5

(e) Credit card offers added security over

carrying cash 1 2 3 4 5

(f) It is easy to overspend with a credit card 1 2 3 4 5

(g) I can take the cash advances on my credit

cards 1 2 3 4 5

(h) Credit card used to cover living expenses 1 2 3 4 5

(i) Credit card used to cover the expenses of

a vacation 1 2 3 4 5

(j) I becomes more desire when shopping with

credit cards 1 2 3 4 5

Part (B) By using the scale given, kindly indicate your reason of NOT using credit cards by underline atthe number that best describes your reason:

Scale indicator: 1. Strongly disagree 2. Disagree 3. Neutral 4. Agree 5. StronglyAgree

(k) Uncontrolled spending can result in

bad financial situation. 1 2 3 4 5

(l) Credit cards will costing me more

than I think. 1 2 3 4 5

(m) I dislike all credit cards. 1 2 3 4 5

(n) I fear the consequences of overspending of

credit card. 1 2 3 4 5

(o) It is easier to control expenditure when

I pay by cash. 1 2 3 4 5

(p) Paying by credit card encourages me

to buy things beyond my budget 1 2 3 4 5

(q) Using a credit cards can only bring the

financial confusion to me 1 2 3 4 5

(r) Paying by cash can help me to avoid debt 1 2 3 4 5

(s) I worry on how I will pay my credit cards

debt. 1 2 3 4 5

(t) I am less concerned with price of a product

when I use a credit card 1 2 3 4 5

--------------------------------------END QUESTION..THANK YOU FOR YOUR KIND COOPERATION------

4.0 The qualitative report on the responses received.

4.1 Analysis of Results

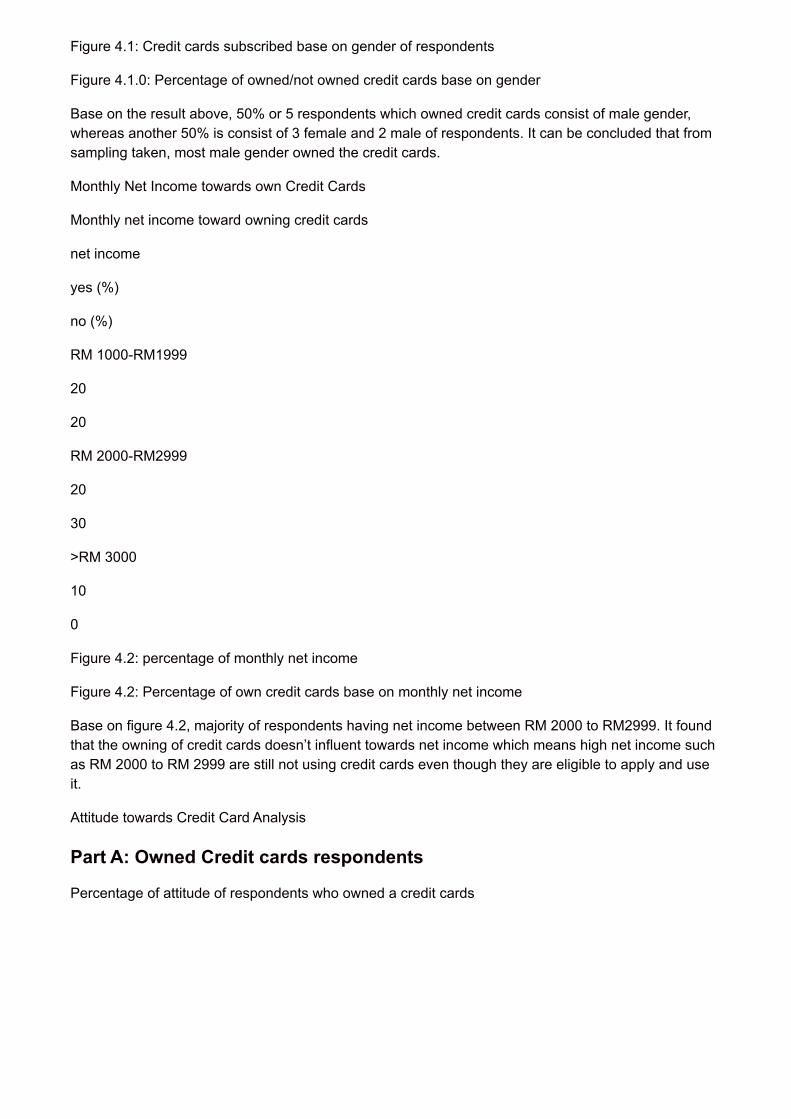

Starting with the research design, the first criteria has been measured was 5 respondents have a creditcard and another 5 respondents don’t have a credit cards, these constant is to ensure that the analysisis fairly acceptable as illustrated in Figure 4.1 below.

Percentage of credit card subscriber

gender

yes (%)

no (%)

male

50

20

female

0

30

Figure 4.1: Credit cards subscribed base on gender of respondents

Figure 4.1.0: Percentage of owned/not owned credit cards base on gender

Base on the result above, 50% or 5 respondents which owned credit cards consist of male gender,whereas another 50% is consist of 3 female and 2 male of respondents. It can be concluded that fromsampling taken, most male gender owned the credit cards.

Monthly Net Income towards own Credit Cards

Monthly net income toward owning credit cards

net income

yes (%)

no (%)

RM 1000-RM1999

20

20

RM 2000-RM2999

20

30

>RM 3000

10

0

Figure 4.2: percentage of monthly net income

Figure 4.2: Percentage of own credit cards base on monthly net income

Base on figure 4.2, majority of respondents having net income between RM 2000 to RM2999. It foundthat the owning of credit cards doesn’t influent towards net income which means high net income suchas RM 2000 to RM 2999 are still not using credit cards even though they are eligible to apply and useit.

Attitude towards Credit Card Analysis

Part A: Owned Credit cards respondents

Percentage of attitude of respondents who owned a credit cards

attitude\scale

strongly disagree

disagree

neutral

agree

strongly agree

a) use for medical expenses, emergency

0

20

0

20

60

b) travel arrangement, reservation

0

0

0

80

20

c) shopping by internet

0

0

20

60

20

d) pay education matter

0

20

40

20

20

e) security over carrying cash

0

20

20

60

0

f) easy to overspend

0

20

20

0

60

g) withdraw advance cash

20

20

20

40

0

h) cover living expenses

20

80

0

0

0

i) vacation expenses

20

60

0

20

0

j) more shopping desired

20

20

0

40

20

Figure 4.3a: Percentage of scale about determined attitude of using credit cards (a – e)

Credit cards used for Travel arrangement and reservation

According to figure 4.3a, it is concluded that 100% (80% agree + 20% strongly agree) or equivalenceto all 5 respondents agreed that credit cards is used for travel arrangement and reservation.

Credit cards used for Shopping by Internet

Base on figure 4.3a, almost all respondents agreed that shopping by internet are the choice of theowner of credit cards.

Security of credit cards over carrying cash

The result shown above has concluded that 60% respondents agreed that use credit cards is moresecured rather that carrying cash, 20% disagreed and 20% are neutral.

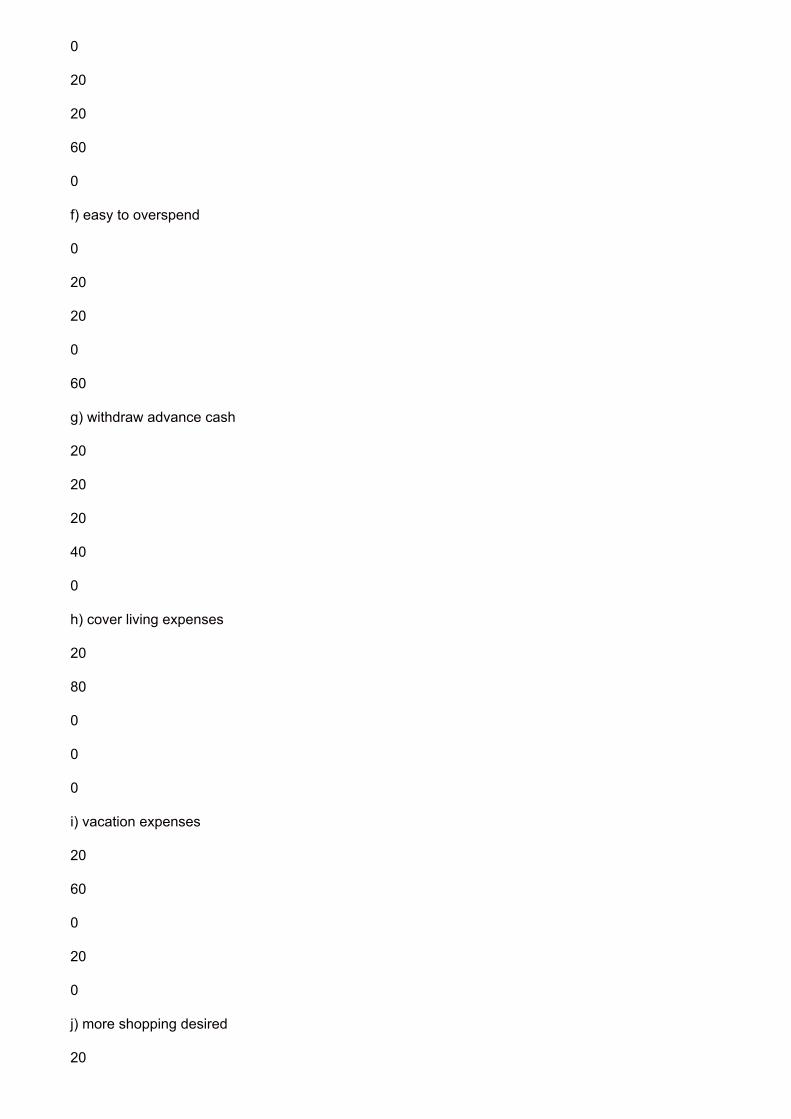

Figure 4.3b: percentage of scale about determined attitude of using credit cards (f to j)

Attitude of cover living expenses by using credit cards.

Base on figure 4.3b, it found that 100% or all 5 respondents are disagreed for the above statement. Itmeans the owner of credit cards respondents are not practiced that method for cover daily livingexpenses.

Credit cards encourage to owner withdraw advance cash

Base on figure 4.3b, 40% of respondents are agreed,40% (20% strongly disagree+20% disagree) and20% are neutral. The result shows balances between agree and disagree.

Attitude of easy to overspend

The result shows almost respondents or 60% are strongly agreed for the above statement. The used ofcredit cards will encourage the owner to overspend to buy unnecessary things. The disagreed aboutthis statement is about 20% and the rest 20% choose neutral.

Attitude of vacation expenses by using credit cards.

Base on figure 4.3b, the result surprisingly shows that 80% (20% strongly disagree+60% disagree)respondents are disagreed about vacation expenses is covered by using credit cards which meansthey preferred another method instead of credit cards whereas 20% are agreed for this statement.

Part B: Non credit cards respondents

According to the data collected, 5 respondents out of 10 have not been using credit cards. Part B willdeliberate the attitudes of non credit cards respondents towards credit cards. The result of analysis hasshown below:

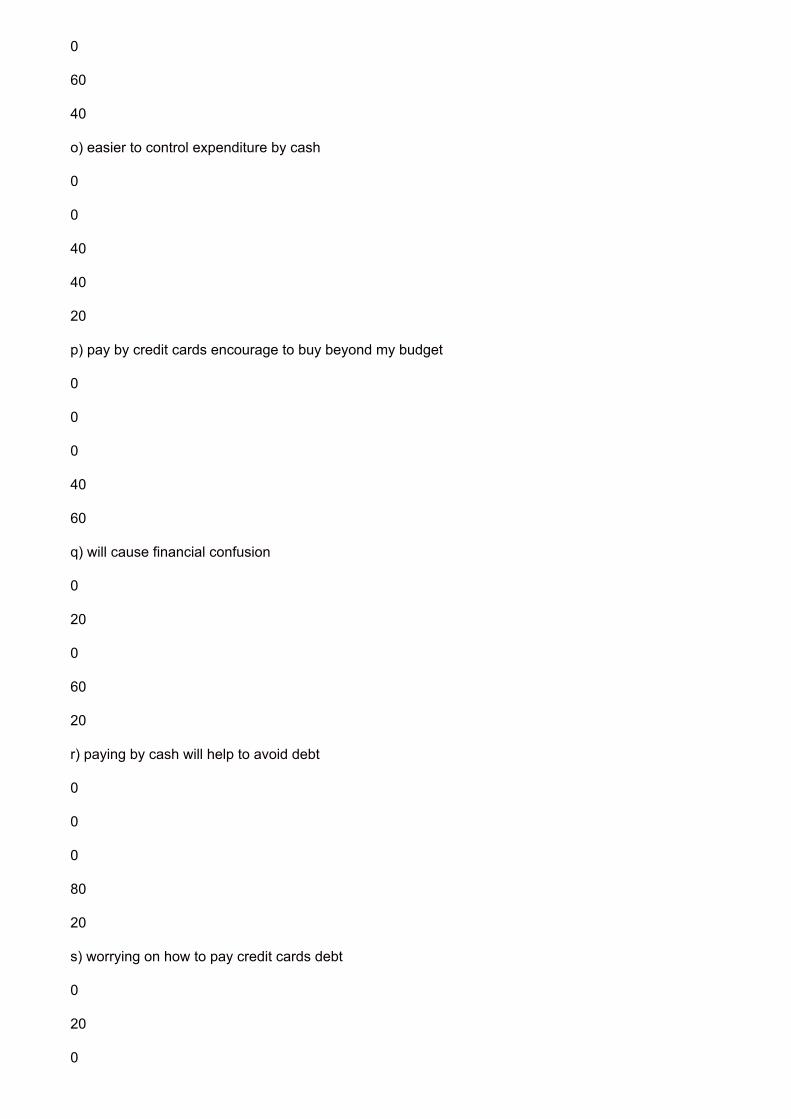

Percentage of attitude of respondents who are non credit cards

attitude\scale

strongly disagree

disagree

neutral

agree

strongly agree

k) uncontrolled spend will caused bad financial situation

0

0

0

20

80

l) will costing me more than I think

0

0

0

40

60

m) I dislike all the credit cards

20

0

40

40

0

n) fear the consequences of overspending

0

0

0

60

40

o) easier to control expenditure by cash

0

0

40

40

20

p) pay by credit cards encourage to buy beyond my budget

0

0

0

40

60

q) will cause financial confusion

0

20

0

60

20

r) paying by cash will help to avoid debt

0

0

0

80

20

s) worrying on how to pay credit cards debt

0

20

0

20

60

t) less concerned with price of product by using credit cards

0

20

20

20

40

Figure 4.4a: Percentage of attitude of respondents who are none credit cards ((k) to (o))

Figure 4.4b: Percentage of attitude of respondents who are none credit cards ((p) to (t))

Will costing me more than I think

With reference on result in figure 4.4a, 100% or 5 out of 5 respondents are agreed about by usingcredit card will charge more cost instead of cash usage. Respondents perceived that credit card willcaused carrying financial burden.

Attitude about fear the consequences of overspending.

Figure 4.4a has shows about 100% respondents are agreed of this statement which means therespondents avoid to having credit card due to this reason. It is also related to variable (p) – ‘pay bycredit card encouraged to buy beyond my budget’ which is also shows that 100% has agreed for thisstatement.

Attitude of easier to control expenditure by cash instead of credit card

Figure 4.4a has shows that 60% respondents are agreed and 40% are neutral, which means majorityof respondents perceived when using cash, the expenditure will be more in controlled rather than creditcards. The resulted was related to variable r) – ‘paying by cash will help to avoid debt’ which resulted100% respondents are agreed for this statement. With strong justification of 2 dependent variablewhich are (o) and (r), it concluded that respondents are trying hard to avoid debt. Thus, this scenarioencourages the respondents to decline credit card usage.

5.0 Conclusion

The student attitude towards credit card in this research report has come out with several results whichare not expected that we had imagined before. The conclusions are summarised as below:

10 respondents are consists of 7 male and 3 female. The result shows that all the 3 femalerespondents do not used or have credit card whereas 5 out of 7 male having credit card. It can beconcluded, male are more influence to have or use credit card compare to female.

It has concluded that credit card is acceptable and practically to use nowadays. This is because whenwe look at the result of variable (m) – ‘I dislike all credit cards’, there’s only 2 respondents out of 10 orequivalence to 20% are dislike of all credit cards. The balanced 80% are chose disagree and neutral.Thus, it concluded that, whether respondents having or not having credit cards, majority of themaccepting credit cards usage and noticed about beneficial of credit cards.

References

Assoc Prof Dr Ahmad Shuib (2010). BBYN4103 Business Research Method. (March version). MeteorDoc. Sdn. Bhd. Selangor Darul Ehsan.

Alan Bryman, Emma Bell. (2003). Business Research Method. Oxford University Press

Roman L. Weil and Michael W. Maher. (2005). Handbook of Cost Management, Second Edition. JohnWiley & Sons.

Wan Marzuki Wan Ramli. (2008). Usah ghairah berhutang dengan kad kredit. Retrieved July 18, 2010,from

http://www.utusan.com.my/utusan/info.asp?y=2008&dt=0702&pub=Utusan_Malaysia&sec=Rencana&pg=re_05.htm

Share This Essay

To share this essay on Reddit, Facebook, Twitter, or Google+ just click on the buttons below:

Request Removal

If you are the original writer of this essay and no longer wish to have the essay published on the UKEssays website then please click on the link below to request removal:

Request the removal of this essay.

More from UK Essays