australia, corruption to good governance

TRANSCRIPT

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 1/70

From Corruption to

Good Governance

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 2/70

From Corruption to

Good GovernanceMarch 2008

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 3/70

This paper by the Justice and International Mission (JIM) Unit, Uniting Church in

Australia, Synod of Victoria and Tasmania contributes to the current debate about

increasing overseas aid to developing countries. The JIM Unit is a member of the

Micah Challenge campaign

Authors:

Dr Mark Zirnsak, Director, Justice and International Mission Unit

Ms Kerryn Clarke, Social Justice Ofcer

Ms Annie Feith, Social Justice Ofcer

Editors

Bessy Andriotis, UnitingCare Victoria and Tasmania

Cath James, Environment Project Ofcer

Typesetting and design

Jesse Cain

AcknowledgementThe Justice and International Mission Unit would like to thank Ben Thurley of

TEAR Australia for examples of good governance at the local level in developing

countries and to Amanda Jackson of Micah Challenge for providing comments on

the draft of the report.

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 4/70

Executive Summary 6Why should Australia be active in curbing corruption?The role of wealthy countries in corruptionDenitionsThe role of human rights in good governanceModels of successWhat attempts are being made internationally to deal with these problems?Conclusion

Summary 8

Why should Australia be active in curbing corruption?The role of international aidStructure of the reportThe role of human rights in good governanceModels of success Australian Catholic Bishops ConferenceThe role of wealthy countries in corruptionWhat attempts are being made internationally to deal with these problems?How does Australia perform in dealing with corruption?OECD assessment of AustraliaSummary of Australia’s performanceConclusion

Recommendations on what Australia could do to combat corruption globally 18

Introduction 20

Good governance and corruption 222.1 Participation, equality and inclusion2.2. Rule of law2.3. Transparency and accountability2.4. Efciency and effectiveness2.5. Dening corruption

Theology of Corruption and Good Governance 24

Models of transition from corruption to good governance 264.1 Fighting corruption needs funding4.2 Need to build demand for good governance4.3 Integrating traditional governance with liberal democratic methods of governance4.4 Good governance and respect for human rights4.5 One size does not t all4.6 Examples of successful good governance projects and actions4.7 Conclusion

Aspects of the global nancial system that encourage corruption in developing

countries 335.1 Wealthy country bodies paying bribes5.2 Tax havens and tax competition5.3 Recovering looted funds from western nation bank accounts5.4 Corruption in lending5.5 Beneting from products obtained with the involvement of corruption

Table of Contents

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 5/70

5.6 Corruption and multilateral development bank loans5.7 Asian Development Bank: accountability and transparency?

What attempts are being made to deal with corruption? 436.1 UN Convention Against Corruption6.2 OECD Anti-bribery Convention6.3 Partnering Against Corruption Principles for Countering Bribery (PACI) Principles6.4 Extractive Industries Transparency Initiative6.5 The Equator Principles6.6 Publish What You Pay and Publish What You Lend6.7 The APEC Code of Conduct for Business6.8 Actions against tax injustice6.9 Stolen Asset Recovery (StAR) Initiative6.10 International collaboration to deal with money laundering

How does Australia perform in dealing with corruption? 487.1 The Financial Action Task Force’s assessment of Australia7.2 OECD assessment of Australia7.3 Australian Wheat Board bribery scandal7.4 Recovery of funds stolen through corruption7.5 Australian efforts to deal with tax havens and tax avoidance and evasion7.6 Corruption under the occupation forces in Iraq

7.7 Allegations of Australian bodies beneting from corruption7.8 Operation Wickenby7.9 Australia leading by example7.10 Dealing with imports produced with the involvement of corruption7.11 AusAID’s approach to good governance7.12 Tackling corruption for growth and development policy7.13 Building Demand for Better Governance program

Conclusion 60

References 63

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 6/70

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 7/70

Why should Australia be active incurbing corruption?

Corruption hurts countries, communities and

individuals. It is a threat to the economic stability and

security of countries whose resources have been

stolen or diverted. When a country’s health budget

is stolen, clinics are left without the medications they

need, hospitals are left without equipment, doctors

are left unpaid, and babies are not immunised. Inthe words of Australia’s former Minister for Foreign

Affairs, The Hon. Alexander Downer, “It is the poor

who suffer if funds are diverted through corruption”.

The role of wealthy countries incorruption

The relationship between aid and development

is complex and corruption and poverty are key

factors. Some have tried to argue that governments

in developing countries are corrupt and thereforeoverseas aid is wasted or used to prop up such

governments.

One of the key factors often missing from the debate

is the role of wealthy countries. Some wealthy

countries can be seen to actively foster corruption,

reward it and seek to benet from it. They do this

through:

providing tax havens to allow corrupt companies

and individuals to avoid paying their fair share oftax;

allowing a whole industry of accountants, lawyers

and bankers to operate to assist rich companies

and individuals in avoiding paying their fair share

of tax;

lax banking laws that allow for money laundering

of funds stolen through corruption;

failing to assist developing countries in recovering

funds stolen through corruption that are thendeposited into investments in wealthy countries;

the failure of laws to deal severely enough

with bribery and, in some cases, even allowing

companies to claim bribes as tax deductions; and

1.

2.

3.

4.

5.

making loans to corrupt governments for

unproductive purposes, saddling developing

country communities with the repayments of

debts from which they have had no benet.

Denitions

Anti-corruption organisation Transparency

International has dened corruption as ‘the misuse of

entrusted power for private benet’.

The Tax Justice Network has suggested that a

possible broader denition for corruption would be

“an activity which undermines public condence in

the integrity of the rules, systems and institutions that

govern society is corrupt.”

The role of human rights in goodgovernance

Effective promotion of ‘good governance’ and

challenging corruption requires respect for basic

human rights. Corruption often ourishes in an

environment where basic human rights are violated.

The Australian Government’s support for the

promotion and protection of human rights globally has

been mixed.

Models of success

Whilst there is no one model that will t all

circumstances, there are some universally applicable

conditions that offer a society protection from

corruption - political and economic stability, strong

social infrastructures, respected institutions,

functioning systems of accountability and

transparency, and a relatively narrow equality gap.

Currently, donor funds for good governance programs

are largely directed to strengthening law and order

institutions, building national security, reforming

public sector administration and economic capacity

building. The majority of good governance projects

are not directed at the community level.

However, for a culture of good governance to

develop, there is a need to build demand for it within

the general community. Good governance requires

6.Executive Summary

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 8/70

and fosters participation by the whole community

in decision making processes, especially the

disenfranchised and marginalised.

What attempts are being madeinternationally to deal with theseproblems?

There are a number of concrete initiatives being taken

internationally to shift cultures of corruption to those

of good governance.

These include:

UN Convention against Corruption (2003);

OECD Anti-bribery Convention (1997);

Asian Development Bank – OECD Action Plan

for Asia-Pacic;

The Partnering Against Corruption Principles

for Countering Bribery (PACI Principles), aninitiative of the World Economic Forum in

partnership with Transparency International

and the Basel Institute on Governance;

Extractive Industries Transparency Initiative

(EITI) (2002);

The Equator Principles;

Publish What You Pay and Publish What You

Lend; and

The APEC Code of Conduct for Business.

There are bodies that assist government agencies incombating money laundering. The Financial Action

Task Force, the Egmont Group and the Asia Pacic

Group on Money Laundering are three that Australia is

a member of.

In September 2007, the World Bank and the UN

Ofce of Drugs and Crime launched a new effort to

assist developing countries in recovering billions of

dollars of looted funds, known as the Stolen Asset

Recovery Initiative.

Conclusion

While lecturing developing countries about

corruption, wealthy countries often play a role in

fostering, rewarding and beneting from corruption in

developing countries. Eliminating corruption globally

will require signicant effort by all countries. It will

not be assisted by withholding aid from developing

countries. In fact withholding aid is likely to increase

corruption. Instead, aid needs to targeted in ways

that does not assist corruption and supports parts ofsociety that are seeking to tackle corruption.

The effort to eliminate corruption will need to include:

Building a global culture to respect basic human

•

•

•

•

•

•

•

•

•

rights;

A global effort to address tax competition, tax

havens and tax evasion;

Wealthy countries being willing to return funds

looted from developing countries;

Wealthy countries being willing to punish

bribery by companies and citizens that

operate from their country;Governments of wealthy countries introducing

measures to prevent the importation of goods

produced through corruption, such as illegally

logged timber; and

A willingness to cancel odious debts, to

discourage those that would make corrupt

loans.

The Australian Government has made signicant

efforts to assist in addressing corruption in developing

countries, including tackling the role that companiesfrom developed countries can play in fostering and

beneting from corruption in these countries. The

Australian Government has made commendable

efforts to tighten up domestic law to prevent money

laundering and nancing of terrorism.

However, it remains to be seen in practice if the

steps taken are sufcient to prevent Australians from

participating in and beneting from corruption in

developing countries and then being able to keep

their ill-gotten gains in Australia.

Australia’s aid program also contains a number of

positive and well-thought through elements to combat

corruption and promote good governance in countries

that receive aid from Australia.

Regrettably, there are black marks on Australia’s

commitment to dealing with corruption, with Iraq

being the most prominent recent example. The

Australian Government appears to have largely looked

the other way with regard to many cases of alleged

human rights abuse in Iraq committed by US-led

forces. It also failed to take much action as Iraqis

were cheated out of billions of dollars of oil revenue

by mismanagement and corruption within the US-led

Coalition Provisional Authority.

Australia could also be doing more at the global level

to address tax competition, tax havens, tax evasion,

odious debts, and the promotion of international

standards to combat corruption and promote good

governance.

•

•

•

•

•

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 9/70

SummaryWhy should Australia be active incurbing corruption?

Corruption hurts countries, communities and

individuals. It is a threat to the economic stability and

security of countries whose resources have been

stolen or diverted. When a country’s health budget

is stolen, clinics are left without the medications they

need, hospitals are left without equipment, doctors

are left unpaid, and babies are not immunised. Inthe words of Australia’s former Minister for Foreign

Affairs, The Hon. Alexander Downer, “It is the poor

who suffer if funds are diverted through corruption”.

Curbing corruption is part of the means to creating a

more accountable, efcient and effective government.

It also allows for development that assists those in

poverty. Anti-corruption measures should focus on a

fairer distribution of resources for all in society.

Donor countries, including Australia, cannot expectsignicant change in the short term. A long term

approach is needed.

The role of international aid

The relationship between aid and development

is complex and corruption and poverty are key

factors. Some have tried to argue that governments

in developing countries are corrupt and therefore

overseas aid is wasted or used to prop up such

governments.

In reality, without sufcient aid, poverty increases.

Poverty then encourages corruption and corruption

in turn undermines efforts to address poverty. This

cycle is not broken by withholding nancial assistance

to impoverished communities. Instead, breaking the

cycle requires a more sophisticated approach to shift

a culture of corruption to one of ‘good governance’.

One of the key factors often missing from the debate

is the role of wealthy countries. Some wealthy

countries can be seen to actively foster corruption,

reward it and seek to benet from it. They do this

through:

providing tax havens to allow corrupt companies1.

and individuals to avoid paying their fair share of

tax;

allowing a whole industry of accountants, lawyers

and bankers to operate to assist rich companies

and individuals in avoiding paying their fair share

of tax;

lax banking laws that allow for money laundering

of funds stolen through corruption;

failing to assist developing countries in recovering

funds stolen through corruption that are then

deposited into investments in wealthy countries;

the failure of laws to deal severely enough

with bribery and, in some cases, even allowing

companies to claim bribes as tax deductions; and

making loans to corrupt governments for

unproductive purposes, saddling developing

country communities with the repayments ofdebts from which they have had no benet.

Structure of the report

The report is organised into sections that examine:

Denitions around good governance and

corruption;

Lessons about what is needed to change a

society from one where corruption ourishes

to one in which good governance exists andthe opportunities for corruption are minimised.

This section also provides examples of where

corruption has been dealt with successfully and

good governance systems have been installed.

The ways that wealthy countries can foster,

reward and benet from corruption.

International measures being pursued to address

corruption as a global problem.

Australia’s performance in relation to corruption.This section looks at how Australia rates in

dealing with corruption; ways it seeks to address

corruption globally, and what inadequacies exist

and where is further improvement needed?

2.

3.

4.

5.

6.

1.

2.

3.

4.

5.

The needs of the poor are more

the freedom of the dominated is more

enabling marginalised groups to participate

which

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 10/70

important than the wants of the rich;

important than the liberty of the powerful, and;

is more important than retaining a system

excludes them. Australian Catholic Bishops Conference

Denitions

Good Governance is dened by the United Nations

Economic and Social Commission for Asia and the

Pacic as:

participatory, consensus oriented, accountable,

transparent, responsive, effective and efcient,

equitable and inclusive and follows the rule of

law. It assures that corruption is minimized,

the views of minorities are taken into account

and that the voices of the most vulnerable in

society are heard in decision-making. It is also

responsive to the present and future needs of

society.

Anti-corruption organisation Transparency

International has dened corruption as ‘the misuse of

entrusted power for private benet’.

The Tax Justice Network has suggested that a

possible broader denition for corruption would be

“an activity which undermines public condence in

the integrity of the rules, systems and institutions that

govern society is corrupt.”

The role of human rights in goodgovernance

Effective promotion of ‘good governance’ and

challenging corruption requires respect for basic

human rights. Corruption often ourishes in an

environment where basic human rights are violated.

The Australian Government’s support for the

promotion and protection of human rights globally has

been mixed. For example, the Australian Government

has pressured the Government of the Philippines

over murders of human rights defenders, church

members, trade unionists, journalists, lawyers and

anti-corruption campaigners.

In contrast, with regard to the case of an Iraqiallegedly tortured to death by US-led forces in Iraq,

the Department of Foreign Affairs and Trade has

stated that Government policy is, “not to comment

on the actions of other countries in relation to matters

in which Australia has no involvement.” In the latter

case, such a policy seems at odds with promoting an

environment which respects human rights and good

governance. This stance sets a very poor example

to the Iraqi authorities and the Iraqi people. Further,

such a policy is likely to undermine the commendable

programs the Australian Government has run to

promote human rights and good governance in Iraq.

Models of success

Whilst there is no one model that will t all

circumstances, there are some universally applicable

conditions that offer a society protection from

corruption - political and economic stability, strong

social infrastructures, respected institutions,

functioning systems of accountability and

transparency, and a relatively narrow equality gap.

Currently, donor funds for good governance programs

are largely directed to strengthening law and orderinstitutions, building national security, reforming

public sector administration and economic capacity

building. The majority of good governance projects

are not directed at the community level.

However, for a culture of good governance to

develop, there is a need to build demand for it within

the general community. Good governance requires

and fosters participation by the whole community

in decision making processes, especially the

disenfranchised and marginalised.

Combating corruption requires being exible and

adaptive to local contexts. For example, the use of

standard competitive tendering for demining projects

in Bosnia resulted in contracts being awarded to

commercial companies that cut corners on safety.

This resulted in an accident rate three times higher

than for non-commercial, non-government demining

organisations.

It also needs to be recognised that in weak states

in post-conict situations, effective systems of

governance are rarely established, and rules can be

bypassed through extra-legal mechanisms such as

bribery and favouritism.

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 11/70

0

Local communities should be involved in the planning,

implementing and monitoring of aid projects, to

minimise the risks of corruption. Citizens need to be

empowered to hold their governments to account

– especially for the delivery of basic and essential

services. There is a need to empower those people

who have the greatest needs and make sure they

have the ability to hold authorities to account. Donor

countries, such as Australia, have an important role toplay in facilitating this engagement in the aid projects

they fund.

Progress toward good governance will be most

effective using incremental approaches which respect

local social and political constraints, rather than

attempts at comprehensive reform.

The role of wealthy countries incorruption

Corporations, individuals, and governments in

wealthy countries sometimes facilitate and benet

from corruption in developing countries. In the words

of the World Bank and the UN Ofce on Drugs and

Crime1:

“While the traditional focus of the international

development community has been on

addressing corruption and weak governance

within the developing countries themselves,

this approach ignores the “other side of the

equation”: stolen assets are often hidden in the

nancial centres of developed countries; bribes

to public ofcials from developing countries

often originate from multinational corporations;

and the intermediary services provided by

lawyers, accountants, and company formation

agents, which could be used to launder or

hide the proceeds of asset theft by developing

country rulers, are often located in developed country nancial centres.”

Bodies in wealthy country paying bribes

The World Bank estimates that US$1 trillion is paid in

bribes each year globally. Transparency International

is concerned that corruption in developing countries

is in fact sustained by bribes paid by Western

countries. A 1997 estimate of bribes paid by

international companies to do business in developing

countries put the gure at US$80 billion per year,more than the total overseas aid to these countries.

UN Ofce on Drugs and Crime and the World Bank, ‘Stolen

Asset Recovery (StAR) Initiative: Challenges, Opportunities and

Action Plan’, The World Bank, June 2007, p. 1.

In some cases, wealthy countries have been slow

or reluctant to act on issues of bribery in developing

countries. For example, the OECD has criticised the

UK Government for taking into consideration the

possible impact on the UK economy, or its relations

with other states, before being willing to take forward

a bribery case. In fact, there has not been a single

prosecution of a UK company in the UK for bribery of

a public ofcial in a developing country.

Tax havens and tax competition

Over the last two decades, tax competition has led to

a ‘race to the bottom’ in corporate tax rates in many

developing countries that now have signicantly lower

tax rates than OECD countries. In trying to attract

foreign investors, there has been a dramatic decrease

in tax rates for foreign owned subsidiaries and

afliates of trans-national companies.

Oxfam estimates that developing countries could

be losing annual tax revenues of at least US$50

billion as a result of tax competition and the use of

tax havens. The recovery of some of this revenue, if

used effectively, could have an enormous impact on

alleviating extreme poverty in developing countries.

Alex Cobham at the Oxford Council on Good

Governance has shown that poorer countries forego

US$385 billion in revenues per year as a result of tax

avoidance and tax evasion, nearly four times what

they get in foreign aid.

The Tax Justice Network estimated in March 2005

that there was US$11,500 billion held by individuals

in approximately 73 tax havens around the world. The

worldwide tax revenue lost as a result was estimated

at US$255 billion per year. With so much revenue

lost due to international tax evasion and avoidance

by large companies and wealthy individuals,

governments are forced to either reduce public

spending and/or increase taxation on less mobile

small companies or poorer individuals.

Banking secrecy and trust services provided by global

nancial institutions operating offshore provide a

secure cover for laundering the proceeds of political

corruption, fraud, embezzlement, illicit arms trading

and the global drug trade. The lack of transparency

in international nancial markets contributes to the

spread of globalised crime, terrorism, bribery of

under-paid ofcials by western businesses, and the

plunder of resources by business and political elites.

Corruption clearly threatens development, and itis tax havens that facilitate the money laundering

of the proceeds of corruption and all types of illicit

commercial transactions.

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 12/70

Tax havens create an illusion. Through the use of

nominees and trust arrangements, tax haven activity

can appear to take place nowhere, which means

it is accountable to no government, pays no tax to

anyone, and has no duty to report anything because it

can deny it is anywhere.

In combination, tax competition, aggressive tax

avoidance, tax evasion and the associated illicit

capital ight to offshore nance centres imposes

a massive cost on developing countries. This cost

usually far outweighs the amount of aid received.

Recovering stolen funds from western bank

accounts

Developing country governments often have

difculties recovering funds stolen through corruption

by past regimes, when such stolen funds have been

placed in the banks of wealthy developed countries.

A report by the Paris-based Comité Catholique contre

le Faim et pour le Développement in March 2007

estimated that the value of wealth stolen by the most

prominent dictators over recent decades amounted to

US$100–180 billion. The report found that only US$4

billion has been repatriated from wealthy countries

and a further US$2.7 billion has been frozen.

However, the UN Convention Against Corruption

contains detailed asset recovery provisions which

are now in force, but still need to be implemented bycountries that have ratied the Convention.

Corruption in lending

Leaders of developing countries may take out loans

for corrupt purposes. The resulting debts can saddle

future governments, and the people of the country,

with the burden of paying interest on the loans as

well as repaying the principal borrowed. In effect,

nancial markets may enable corrupt governments to

steal from the future. Another way nancial marketsfacilitate this kind of corruption is to provide loans

against secured assets. Valuable assets can be

converted into cash today without ever being publicly

sold. Future governments and tax payers are left with

repayment.

Governments of developed countries have largely

refused to recognise the concept of ‘odious debt’

being applied to the debts of developing countries.

Odious debt is applied when:

loans are made to illegitimate authorities, such as

undemocratic governments;

the loans are not used for the benet of the

people under that authority; and

1.

2.

the lender should have reasonably known of the

rst two conditions.

In such cases the concept of ‘odious debt’ is

applied and the loans are deemed to be illegitimate

and unenforceable. The Australian Government

has refused to accept that odious debts should be

cancelled.

Loans made for corrupt purposes increase a country’sdebt level while doing nothing to increase a country’s

capacity to make repayments.

Beneting from products obtained through

corruption

One of the ways that wealthy countries benet

from corruption in the developing world is through

the receipt of goods obtained through corruption.

Products obtained through corruption are often

cheaper than if the products had been producedthrough legal or legitimate means. Developing

countries are then cheated out of revenues they

would have otherwise received if the products had

been produced and sold legitimately.

Timber and wood products obtained from illegal

logging are an example of the types of products

that developed countries receive cheaply as a result

of corruption in the developing world. The World

Bank estimates that the global annual market value

of losses from illegal logging at over US$10 billion,which is more than eight times the foreign aid

provided for sustainable management of forests.

Multilateral Development Banks dealing with

corruption

The World Bank has investigated 2000 cases of

corruption since 999, and sanctioned over 300 rms

and individuals. However, the World Bank has not

always assisted developing countries in their attempts

to combat corruption.

Meanwhile the Asian Development Bank (ADB) has

not published the list of companies blacklisted for

corruption in ADB funded projects.

The lack of transparency of the ADB in dealing with

corruption needs to be of signicant concern to

Australians given that the Australian Government

White Paper Australian Aid: Promoting Growth and

Stability indicates that the Australian Government will

work with the ADB in areas of mutual interest.

3.

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 13/70

What attempts are being madeinternationally to deal with theseproblems?

There are a number of concrete initiatives being taken

internationally to shift cultures of corruption to those

of good governance.

These include:

UN Convention against Corruption (2003);

OECD Anti-bribery Convention (1997);

Asian Development Bank – OECD Action Plan

for Asia-Pacic;

The Partnering Against Corruption Principles

for Countering Bribery (PACI Principles), an

initiative of the World Economic Forum in

partnership with Transparency International

and the Basel Institute on Governance;

Extractive Industries Transparency Initiative(EITI) (2002);

The Equator Principles;

Publish What You Pay and Publish What You

Lend; and

The APEC Code of Conduct for Business.

In addition, the OECD issued a report in 1998 on

Harmful Tax Competition, which identied harmful

tax practices, many of which are associated with tax

havens. The OECD approach has been to eliminate

harmful practices by obtaining mutual undertakings

between all parties. The OECD has only been partially

successful in its efforts largely because of conicts

between the tax havens it targeted, and the inability of

the OECD to stop countries within the OECD pursuing

the very practices the report identied as harmful.

There are bodies that assist government agencies in

combating money laundering. The Financial Action

Task Force, the Egmont Group and the Asia Pacic

Group on Money Laundering are three that Australia is

a member of.

In September 2007, the World Bank and the UN

Ofce of Drugs and Crime launched a new effort to

assist developing countries in recovering billions of

dollars of looted funds, known as the Stolen Asset

Recovery Initiative.

How does Australia perform indealing with corruption?

Financial Action Task Force Assessment of Australia (FATF)

The FATF is an intergovernmental body which sets

standards and develops policies to combat money

laundering and terrorist nancing. Its Third Mutual

•

•

•

•

•

•

•

•

Evaluation Report on Anti-Money Laundering and

Combating the Financing of Terrorism, released in

October 2005, assessed Australia’s performance.

The report found:

That while Australia’s legal regime for dealing

with money laundering appeared to be

comprehensive, dissuasive and proportional,

it was not being effectively applied. In caseswhere it has been applied, sentences appear

low.

There were no legislative or other enforceable

obligations regarding the identication and

verication of foreign government ofcials

who deposit money with Australian nancial

institutions and who have the greatest ability

to engage in large scale corruption.

There are no specic obligations for nancial

institutions to monitor complex, unusuallylarge transactions or transactions with no

visible economic purposes, or to further

examine these situations and set out the

ndings in writing.

That, although the Financial Transactions

Reports Act 1988 extends to overseas

branches of nancial institutions, Australian

banks indicated that they would rst apply

the local laws. In several cases, local laws

prohibited full implementation of the Australian

standards due to local secrecy provisions.

The International Monetary Fund also conducted an

assessment of Australia’s nancial sector, releasing

their report in October 2006. The assessment

examined Australia’s implementation of the Basel

Core Principles for Effective Banking Supervision. The

assessment found that Australia was “Materially non-

compliant” with Principle 15 dealing with prevention

of use of the banks by criminal elements.

In response to the FATF ndings, the AustralianGovernment stated that it had enhanced the ability

of the Australian Federal Police to investigate and

pursue money laundering. The Government has

also introduced comprehensive new anti-money

laundering and counter-terrorism nancing legislation.

The legislation includes the following measures:

Financial institutions are prohibited from

entering into correspondent banking

relationships with shell banks or other nancial

institutions that allow shell banks to holdaccounts with them.

All foreign and overseas branches and

subsidiaries have to comply with the

principles of Australian anti-money laundering

•

•

•

•

•

•

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 14/70

requirements.

Financial institutions are required to assess

the risk they are exposed to, the threat of

money laundering and terrorism nancing and

then must take steps they deem appropriate

to address the risks.

Penalties for non-compliance with the regulatory

obligations by a company are as high as $11

million (100,000 penalty units, where a penalty unit

is currently $110) and $2.2 million for individuals.

Individuals that commit criminal offences under the

legislation will face up to 10 years imprisonment.

OECD assessment of Australia

According to an OECD report released in January

2006, Australian authorities demonstrated a strong

commitment to combating foreign bribery. However,

the report concluded that Australia needs to toughen

its stand on companies paying bribes or ‘facilitation

payments’ to foreign governments.

The report stated that the Australian Tax Ofce (ATO)

should implement better systems for detecting foreign

bribery transactions when conducting tax audits. The

OECD’s bribery group urged that corporate nes for

bribery be increased from the current maximum of

$330,000, and that sanctions such as disqualifying for

government contracts, be brought against companies

found to have bribed foreign ofcials. It recommended

that the Australian government change whistleblower

legislation to protect public servants who, “report

suspicions of foreign bribery” and that it consider

introducing “stronger whistleblower protections for

private sector employees”.

The Australian Government is due to respond to the

OECD report in early 2008.

In December 2006 the Australian Taxation Ofce

issued guidelines for its auditors to detect bribes in

payments companies make in developing countries.The guidelines are based on OECD standards and will

require companies to record information such as the

amount paid, the identity of the foreign public ofcial

who was paid, and details of what they were paying

for.

On 3 May 2007, the then Attorney General announced

that the government will tighten up the rules for being

able to claim facilitation payments to foreign ofcials

as tax deductions and reduce the defences that can

be mounted against a charge of foreign bribery underthe Criminal Code.

•

Recovery of funds stolen through corruption

The Proceeds of Crime Act 2002 was introduced

by the Australian Government to be able to trace,

restrain and conscate the proceeds of crime against

Australian law. In combination with the Mutual

Assistance in Criminal Matters Act 1987 it allows the

Australian Government to register and enforce legal

efforts by foreign countries to recover money stolen

through corruption.

Australian efforts to deal with Tax Havens and Tax

Avoidance and Evasion

The Australian Taxation Ofce (ATO) has expanded

its relationships with tax authorities in other countries

to address the misuse of tax havens. Australia is

a member of the OECD’s Forum on Harmful Tax

Practices which aims to eliminate harmful tax

practices from both OECD member countries and

non-member jurisdictions, including tax havens.

In 2005-2006, the ATO provided over 1.5 million

income records under the automatic exchange of

information program (regarding dividends, interest

and unit trust distributions) to 42 treaty partners

aiding in efforts to prevent international tax avoidance

and evasion.

Australia is also a member of the OECD’s Committee

on Fiscal Affairs, which was established to bring

together senior tax ofcials from all OECD membergovernments. Australia is part of a working party

established by the committee to monitor all matters

covering tax avoidance and evasion.

Corruption in Iraq

The Australian Government appears to have done

little to address signicant levels of corruption under

the US-led administration of Iraq after the 2003

invasion of Iraq that overthrew the brutal regime of

Saddam Hussein. Billions of dollars went missingafter the US-led Coalition Provisional Authority was

installed, after the overthrow of Saddam Hussein’s

regime. Favourable contracts were then awarded to

companies close to the Bush Administration. The

result was that the Iraqi people were cheated of oil

revenue that was theirs and have subsequently been

deprived of vital services, such as healthcare clinics.

As of April 2006, the US Special Inspector General

for Iraq Reconstruction was investigating 72 cases of

alleged fraud, theft, bribery and corruption in Iraq.

There are no allegations of any corruption relating to

Australia’s direct aid program to Iraq.

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 15/70

Operation Wickenby

The Australian Government has been conducting

Operation Wickenby to investigate internationally

promoted tax evasion and large scale money

laundering. The Operation has resulted in charges

against three Gold Coast businessmen and $17.9

million in extra tax being paid. The Australian Crime

Commission and the Australian Taxation Ofce

have conrmed more than 500 people are being

investigated for participation in illegal arrangements

such as offshore tax havens. The investigation initially

focussed on Swiss accountant Philip Egglishaw, but

has since widened to cover more than 100 promoters

of international tax-evasion schemes.

Leading by example

If Australia wishes to urge developing countries to

address corruption, then it needs to lead by example

domestically. The new Federal Rudd Government

has promised to establish a Freedom of Information

Commissioner, to end the ability of Ministers to

be able to refuse freedom of information requests

through the use of unchallengeable conclusive

certicates, improve whistleblower protection for

government employees, and not seeking to prosecute

journalists who publish material that is merely

embarrassing to government.

At the same time, the South Australian and

Victorian Governments are the only mainland state

governments that have refused to set up independent

anti-corruption commissions.

Tackling Corruption for Growth and Development

Policy

The Australian Government has developed a ‘Anti-

Corruption for Development’ policy to guide the

development and implementation of all Australian aid

program activities aimed at countering corruption in

the region.

Launched on 30 March 2007 under the title ‘Tackling

corruption for growth and development. A Policy

for Australian Development Assistance on Anti-

Corruption’ it outlines three elements to combat

corruption in the region: building constituencies

for anti-corruption reform; reducing opportunities

for corruption and changing incentives for corrupt

behaviour. Positively, the Australian Government

recognises that due to the complexity and political

sensitivity of corruption, the strategy will have a long-term focus and will include some exploratory and

experimental elements as well as ongoing research.

The policy commits Australia to supporting efforts

to develop anti-corruption policies and plans in

countries that do not have them.

In terms of building constituencies for anti-corruption

reform, the policy recognises the need for large-scale

and sustained commitment to formal and informal

education of young men and women who will be

society’s future politicians, judges, prosecutors, police

ofcers, civil servants, regulators, entrepreneurs, and

labour and community leaders. The policy also states

that supporting gender equity in leadership positions

will contribute to a more just society and lower

tolerance for corruption.

AusAID will report on progress in implementing its

anti-corruption initiatives through the Annual Review

of Development Effectiveness, to be prepared by the

Ofce of Development Effectiveness.

In the 2006-2007 nancial year, the Australian

Government spent approximately $645 million from

the aid budget on anti-corruption and governancemeasures in the Asia-Pacic region.

Building demand for better governance program

The Australian Government has recognised in its

White Paper on Australia’s overseas aid program

that “insufcient demand for better performance or

reform is one of the most important obstacles to

institutional development in poor countries.” The

Building Demand for Better Governance program

will support strategic partnerships to help augmentdomestic demand for reform and accountability in

the Asia-Pacic region. Australian aid has supported

the PNG Church Partnership Program and ‘War

Against Corruption’ campaigns, support for national

human rights institutions, and partnerships with

Transparency International. Such support is planned

to be expanded with a particular focus on supporting

women’s groups and building capacity in developing

countries for independent analysis of government

policy.

Summary of Australia’sperformance

The table below summaries Australia’s performance

in tackling and deterring corruption in developing

countries and preventing Australians and Australian

companies from engaging in corruption in developing

countries and beneting from it.

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 16/70

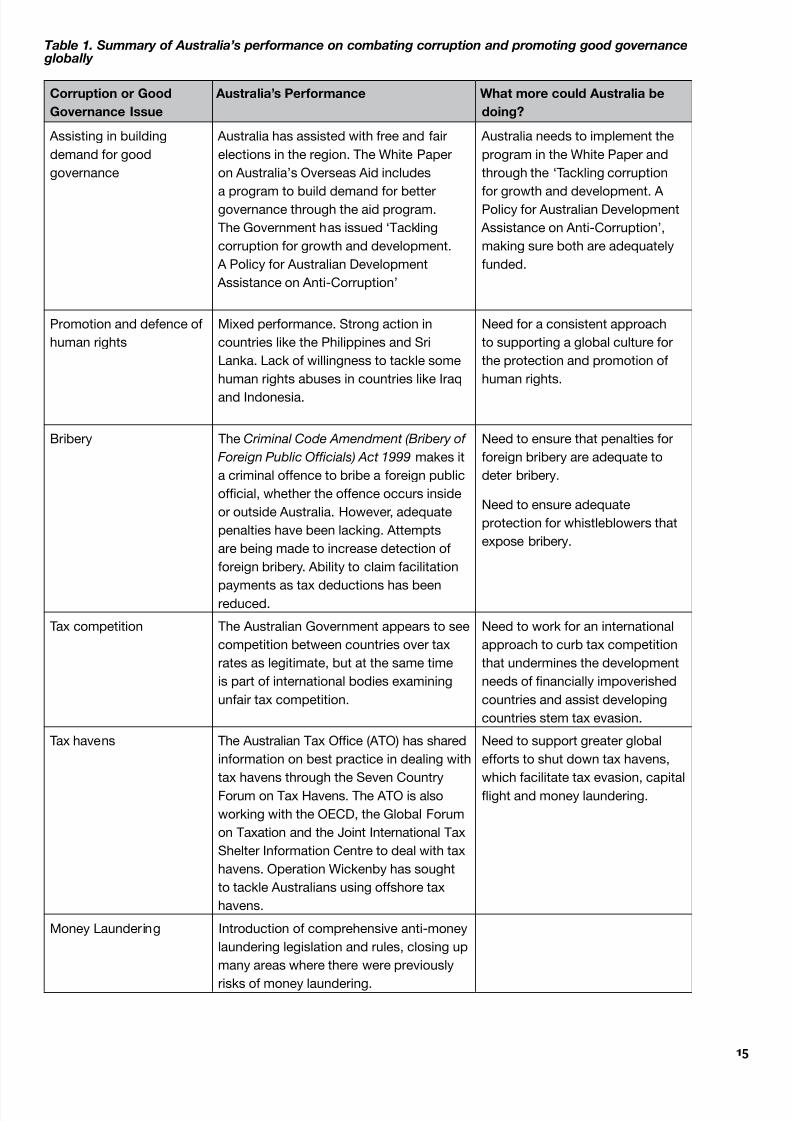

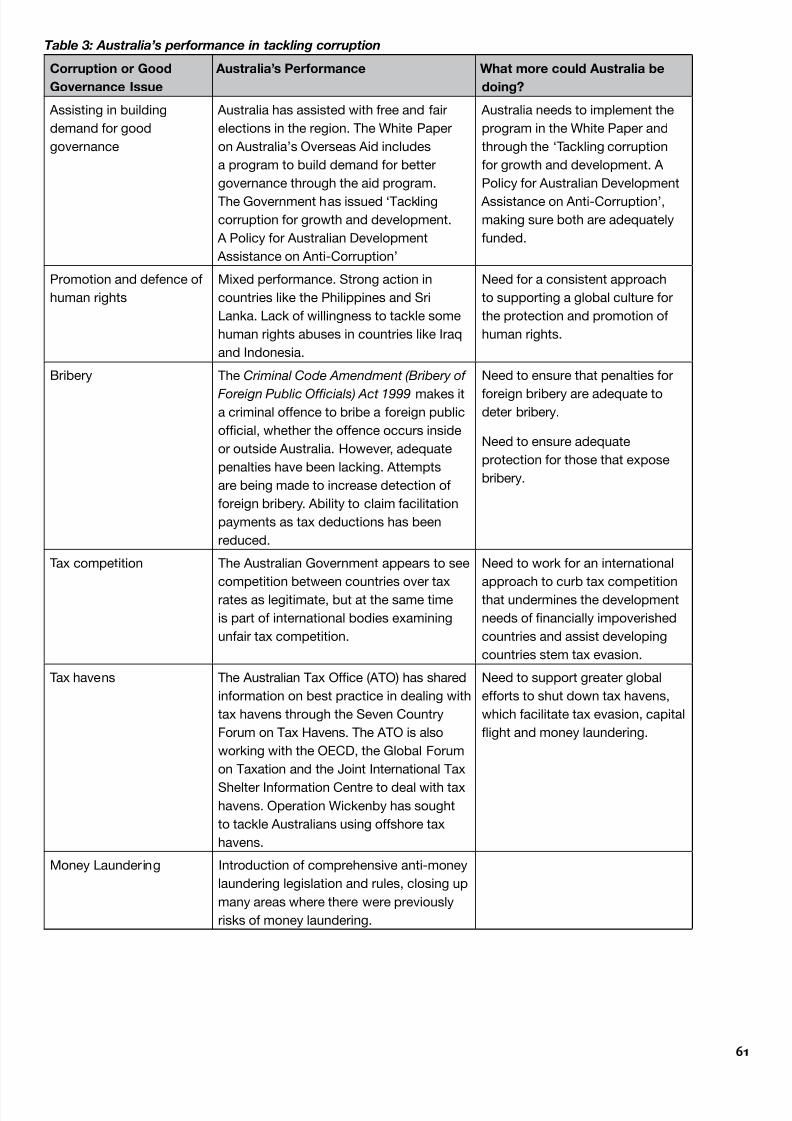

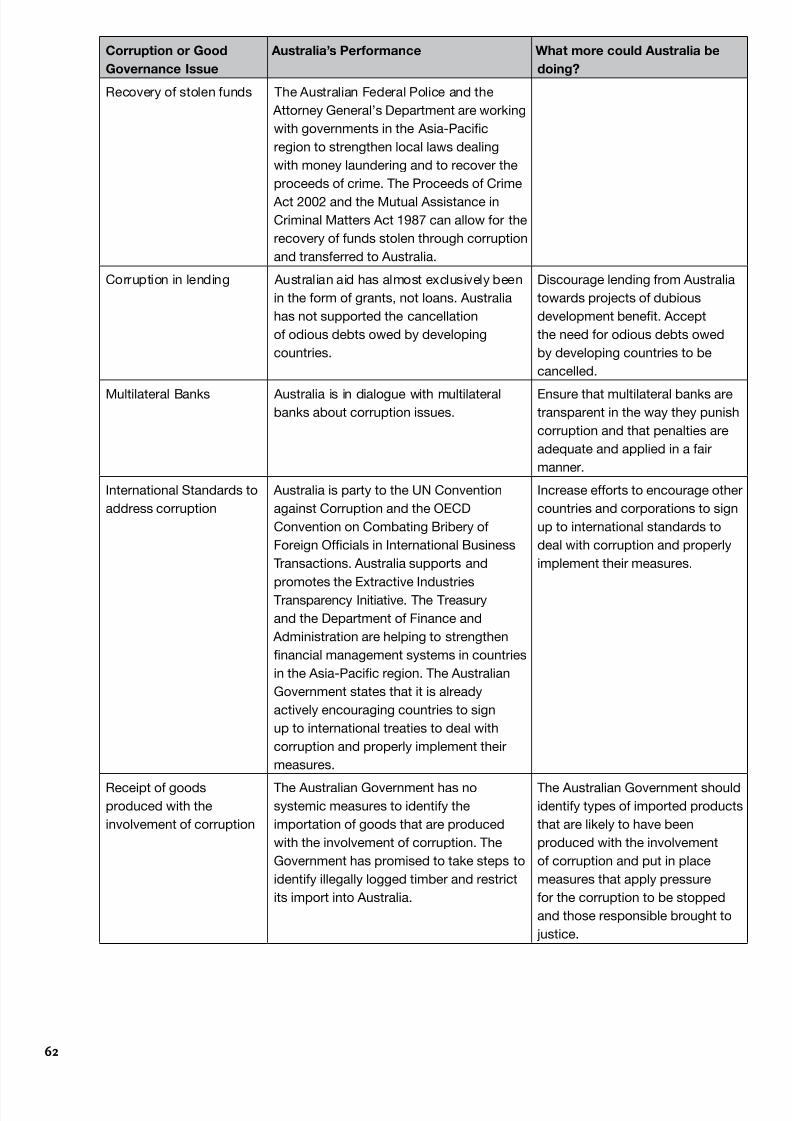

Table 1. Summary of Australia’s performance on combating corruption and promoting good governance globally

Corruption or Good

Governance Issue

Australia’s Performance What more could Australia be

doing?

Assisting in building

demand for good

governance

Australia has assisted with free and fair

elections in the region. The White Paper

on Australia’s Overseas Aid includes

a program to build demand for bettergovernance through the aid program.

The Government has issued ‘Tackling

corruption for growth and development.

A Policy for Australian Development

Assistance on Anti-Corruption’

Australia needs to implement the

program in the White Paper and

through the ‘Tackling corruption

for growth and development. A Policy for Australian Development

Assistance on Anti-Corruption’,

making sure both are adequately

funded.

Promotion and defence of

human rights

Mixed performance. Strong action in

countries like the Philippines and Sri

Lanka. Lack of willingness to tackle some

human rights abuses in countries like Iraq

and Indonesia.

Need for a consistent approach

to supporting a global culture for

the protection and promotion of

human rights.

Bribery The Criminal Code Amendment (Bribery of

Foreign Public Ofcials) Act 1999 makes it

a criminal offence to bribe a foreign public

ofcial, whether the offence occurs inside

or outside Australia. However, adequate

penalties have been lacking. Attempts

are being made to increase detection of

foreign bribery. Ability to claim facilitation

payments as tax deductions has beenreduced.

Need to ensure that penalties for

foreign bribery are adequate to

deter bribery.

Need to ensure adequate

protection for whistleblowers that

expose bribery.

Tax competition The Australian Government appears to see

competition between countries over tax

rates as legitimate, but at the same time

is part of international bodies examining

unfair tax competition.

Need to work for an international

approach to curb tax competition

that undermines the development

needs of nancially impoverished

countries and assist developing

countries stem tax evasion.

Tax havens The Australian Tax Ofce (ATO) has shared

information on best practice in dealing with

tax havens through the Seven CountryForum on Tax Havens. The ATO is also

working with the OECD, the Global Forum

on Taxation and the Joint International Tax

Shelter Information Centre to deal with tax

havens. Operation Wickenby has sought

to tackle Australians using offshore tax

havens.

Need to support greater global

efforts to shut down tax havens,

which facilitate tax evasion, capitalight and money laundering.

Money Laundering Introduction of comprehensive anti-money

laundering legislation and rules, closing up

many areas where there were previouslyrisks of money laundering.

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 17/70

Corruption or Good

Governance Issue

Australia’s Performance What more could Australia be

doing?

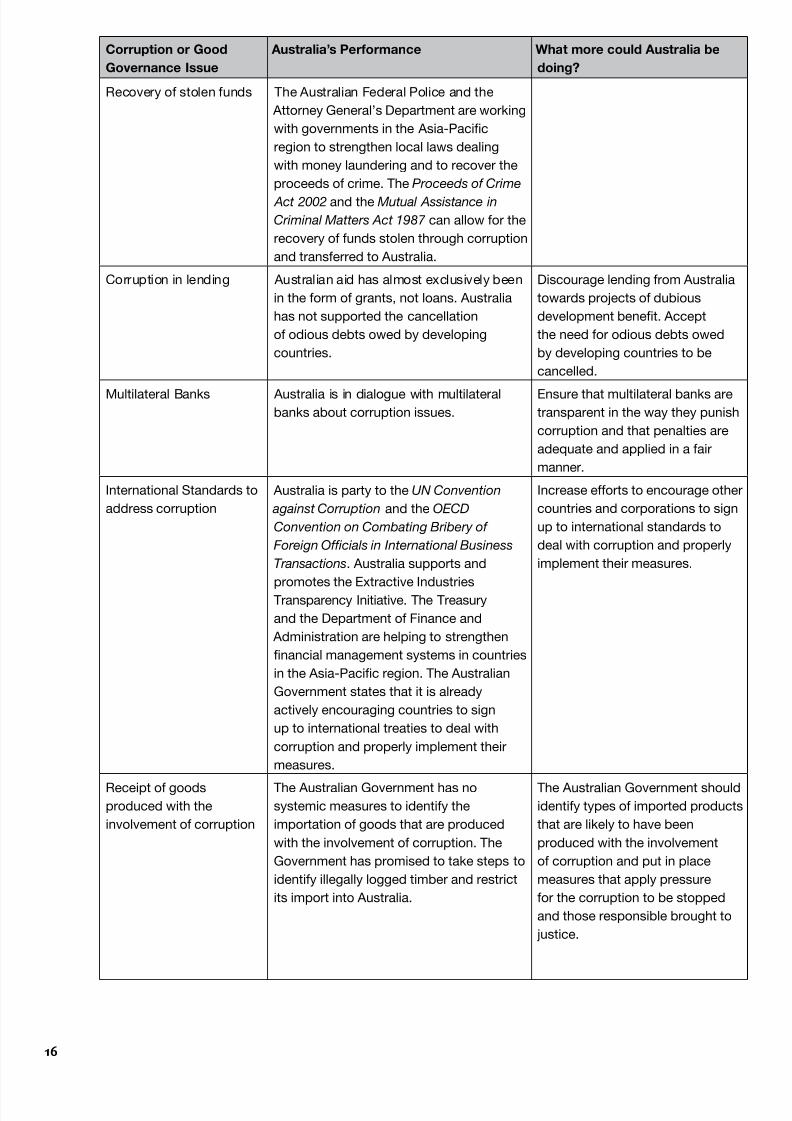

Recovery of stolen funds The Australian Federal Police and the

Attorney General’s Department are working

with governments in the Asia-Pacic

region to strengthen local laws dealing

with money laundering and to recover the

proceeds of crime. The Proceeds of Crime

Act 2002 and the Mutual Assistance in

Criminal Matters Act 1987 can allow for the

recovery of funds stolen through corruption

and transferred to Australia.

Corruption in lending Australian aid has almost exclusively been

in the form of grants, not loans. Australia

has not supported the cancellation

of odious debts owed by developing

countries.

Discourage lending from Australia

towards projects of dubious

development benet. Accept

the need for odious debts owed

by developing countries to be

cancelled.

Multilateral Banks Australia is in dialogue with multilateral

banks about corruption issues.

Ensure that multilateral banks are

transparent in the way they punish

corruption and that penalties are

adequate and applied in a fair

manner.

International Standards to

address corruption

Australia is party to the UN Convention

against Corruption and the OECD

Convention on Combating Bribery of

Foreign Ofcials in International Business

Transactions. Australia supports and

promotes the Extractive IndustriesTransparency Initiative. The Treasury

and the Department of Finance and

Administration are helping to strengthen

nancial management systems in countries

in the Asia-Pacic region. The Australian

Government states that it is already

actively encouraging countries to sign

up to international treaties to deal with

corruption and properly implement their

measures.

Increase efforts to encourage other

countries and corporations to sign

up to international standards to

deal with corruption and properly

implement their measures.

Receipt of goods

produced with the

involvement of corruption

The Australian Government has no

systemic measures to identify the

importation of goods that are produced

with the involvement of corruption. The

Government has promised to take steps to

identify illegally logged timber and restrict

its import into Australia.

The Australian Government should

identify types of imported products

that are likely to have been

produced with the involvement

of corruption and put in place

measures that apply pressure

for the corruption to be stopped

and those responsible brought to

justice.

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 18/70

Conclusion

While lecturing developing countries about

corruption, wealthy countries often play a role in

fostering, rewarding and beneting from corruption in

developing countries. Eliminating corruption globally

will require signicant effort by all countries. It will

not be assisted by withholding aid from developing

countries. In fact withholding aid is likely to increasecorruption. Instead, aid needs to targeted in ways

that does not assist corruption and supports parts of

society that are seeking to tackle corruption.

The effort to eliminate corruption will need to include:

Building a global culture to respect basic

human rights;

A global effort to address tax competition, tax

havens and tax evasion;

Wealthy countries being willing to return fundslooted from developing countries;

Wealthy countries being willing to punish

bribery by companies and citizens that

operate from their country;

Governments of wealthy countries introducing

measures to prevent the importation of goods

produced through corruption, such as illegally

logged timber; and

A willingness to cancel odious debts, to

discourage those that would make corruptloans.

The Australian Government has made signicant

efforts to assist in addressing corruption in developing

countries, including tackling the role that companies

from developed countries can play in fostering and

beneting from corruption in these countries. The

Australian Government has made commendable

efforts to tighten up domestic law to prevent money

laundering and nancing of terrorism.

However, it remains to be seen in practice if thesteps taken are sufcient to prevent Australians from

participating in and beneting from corruption in

developing countries and then being able to keep

their ill-gotten gains in Australia.

Australia’s aid program also contains a number of

positive and well-thought through elements to combat

corruption and promote good governance in countries

that receive aid from Australia.

Regrettably, there are black marks on Australia’s

commitment to dealing with corruption, with Iraq

being the most prominent recent example. The

Australian Government appears to have largely looked

the other way with regard to many cases of alleged

human rights abuse in Iraq committed by US-led

•

•

•

•

•

•

forces. It also failed to take much action as Iraqis

were cheated out of billions of dollars of oil revenue

by mismanagement and corruption within the US-led

Coalition Provisional Authority.

Australia could also be doing more at the global level

to address tax competition, tax havens, tax evasion,

odious debts, and the promotion of international

standards to combat corruption and promote good

governance.

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 19/70

The Australian Government has a moral and ethical

obligation to do as much as it can to combat

domestic and global corruption.

The Australia Government can do more to combat

corruption and promote good governance by:

Continuing to fund anti-corruption and good

governance projects within developing countries

in the Asia-Pacic region, including support for

anti-corruption campaigners.

Make sure that aid assists in the payment

of adequate salaries, as insufcient income

increases the risk of corrupt behaviour.

When Australia provides aid in the form of

‘services in kind’ the Australian Auditor-General

and/or the Commonwealth Joint Committee

of Public Accounts and Audit should audit the

effectiveness of the aid.

International Anti-Corruption Standards

Encouraging more countries and corporations to

sign up to appropriate multilateral agreements to

combat corruption such as:

The UN Convention against Corruption (2003);

The OECD Anti-Bribery Convention (1997);

The Asian Development Bank – OECD Action

Plan for Asia-Pacic;

The Partnering Against Corruption Principlesfor Countering Bribery (PACI Principles), an

initiative of the World Economic Forum in

partnership with Transparency International

and the Basel Institute on Governance;

The Extractive Industries Transparency

Initiative (EITI) (2002); and

The Equator Principles.

The Australian Government should encourage

those that have signed up to these agreements to

fully comply with their provisions.

Taxation reform

Supporting an international approach to taxation,

corruption and nancial stability. For taxation

1.

2.

3.

4.

•

•

•

•

•

•

5.

6.

this means a framework that balances the need

to curb tax competition with a respect for the

ability of democratic governments to set generally

applicable tax rates and which empower poorer

countries to stem tax evasion.

Supporting an international agreement to share

information on tax administration and income

paid to citizens of one country who reside in

another to help poorer countries to stem taxevasion1.

Providing assistance to developing countries to

ensure they can establish:

sound taxation systems;

rigorous procedures that require international

companies to account for what they do;

international enforcement procedures that

ensure international corporations pay what

they owe; andsound career paths for key tax administration

personnel so that they stay in their jobs for

longer and are not lured away.

Whistleblower protection

Supporting programs which enhance the

protection of journalists and whistleblowers in

developing countries.

Strengthening whistleblower legislation to protect

public servants who report suspicions of briberyin relation to foreign contracts and introduce

stronger whistleblower protections for private

sector employees that reveal corruption.

Dealing with bribery

Increasing penalties 30-fold for Australian

companies and individuals found guilty of bribing

foreign governments and ofcials and ensure that

those found guilty are denied access to public

contracting opportunities (particularly through Australia’s aid program).

Oxfam UK, ‘Tax Havens: Releasing the Hidden Billions forPoverty Eradication’, 2000, http://www.attac.org/fra/toil/doc/ oxfam2.htm and Richard Murphy, John Christensen and JennyKimmis, ‘Tax us if you can’, Tax Justice Network, September 2005,p. 48.

7.

8.

•

•

•

•

9.

10.

11.

Recommendations on what Australia could do to

combat corruption globally

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 20/70

Ensuring that all cases of foreign bribery be

referred to the Australian Federal Police by

Commonwealth agencies.

Changing processes to ensure that politically

sensitive cases of foreign bribery are not

potentially delayed in being referred to the

Australian Federal Police by the notication to the

Minister of Justice and Customs.

Requiring an external auditor who discovers

indications of a possible illegal act of bribery

to report the discovery to management and, as

appropriate, to corporate monitoring bodies, and

the competent authorities2.

Ensuring that members of the Australian Public

Service, including AusAID ofcials, who come into

contact with companies involved in international

business understand that the Australian Public

Service Code of Conduct requires them to reportto the Australian Federal Police credible evidence

of foreign bribery offences that they uncover in

the course of performing their duties3.

Introducing formal rules on the imposing of

civil or administrative penalties upon bodies

and individuals convicted of foreign bribery,

so that public subsidies, licences, government

procurement contracts and export credits can be

denied or terminated as penalty for foreign bribery

in appropriate cases4.

Establishing a policy for denying access to

contracting opportunities with public agencies,

such as the Export Finance and Insurance

Corporation (EFIC) and AusAID, as well as

provisions for the termination of such contracts

in appropriate cases where contractors are

convicted of foreign bribery after entering the

contract5.2 Based on the recommendation under the section numbered179 in OECD, Directorate for Financial and Enterprise Affairs,‘Australia: Phase 2. Report on the Application of the Conventionon Combating Bribery of Foreign Public Ofcials in InternationalBusiness Transactions and the 1997 Recommendation onCombating Bribery in International Business Transactions’, 4January 2006.3 Based on the recommendation under the section numbered179 in OECD, Directorate for Financial and Enterprise Affairs,‘Australia: Phase 2. Report on the Application of the Conventionon Combating Bribery of Foreign Public Ofcials in InternationalBusiness Transactions and the 1997 Recommendation onCombating Bribery in International Business Transactions’, 4January 2006.4 Based on the recommendation under the section numbered181 in OECD, Directorate for Financial and Enterprise Affairs,‘Australia: Phase 2. Report on the Application of the Convention

on Combating Bribery of Foreign Public Ofcials in InternationalBusiness Transactions and the 1997 Recommendation onCombating Bribery in International Business Transactions’, 4January 2006.5 Based on the recommendation under the section numbered181 in OECD, Directorate for Financial and Enterprise Affairs,‘Australia: Phase 2. Report on the Application of the Conventionon Combating Bribery of Foreign Public Ofcials in International

12.

13.

14.

15.

16.

17.

Fully implementing the Action Statement on

Bribery and Ofcially Supported Export Credits

agreed by the OECD.

Dealing with lending as corruption

Australia should accept the principle that those

debts that meet the criteria of being ‘odious’

should be cancelled.

Australia should commit to the principle of

creditor co-responsibility and ensure the

responsibility of any future bilateral and

multilateral lending involving Australia by:

Introducing guidelines that discourage lending

(or insurance of lending by EFIC, Australia’s

Export Credit Agency) towards projects

where there is dubious development benet,

where there is an unacceptable risk of non-

repayment or where there are not adequatehuman rights or environmental safeguards.

Advocating for the adoption of similar

guidelines at by the multilateral development

banks at which Australia is represented,

particular the Asian Development Bank.

Supporting local initiatives

Supporting the promotion of a global culture of

respect for basic human rights, so that those

seeking to tackle corruption are not subjected to

human rights abuses.

Providing assistance to communities to tackle

corruption and build good governance that build

a strong sense of local ownership and genuine

partnership.

Multilateral Development Bank Reform

Advocating for reforms of the World Bank and

International Monetary Fund (IMF) that enhance

democratic representation and transparency,including elections by Board of Governors to all

board seats, publication of meeting transcripts

and a democratic, transparent and merit-based

process for selecting the World Bank President

and IMF Managing Director

Pressuring the World Bank, IMF and the Asian

Development Bank to deal promptly with

companies found to have engaged in corruption,

and with sufcient penalties to deter other

companies from engaging in corruption.

Business Transactions and the 1997 Recommendation onCombating Bribery in International Business Transactions’, 4January 2006.

18.

19.

20.

•

•

21.

22.

23.

24.

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 21/70

0

1The following paper has been prepared by the Justice

and International Mission Unit of the Uniting Church

in Australia, Synod of Victoria and Tasmania as a

contribution to the current debate about increasing

overseas aid.

Corruption hurts local communities and individuals.

Corruption is a threat to the economic stability and

security of countries whose resources have been

stolen or diverted.

When a country’s health budget is stolen, clinics are

left without the medications they need, hospitals are

left without equipment, doctors are left unpaid and

babies are not immunised. In the words of Australia’s

former Minister for Foreign Affairs, The Hon.

Alexander Downer, “It is the poor who suffer if funds

are diverted through corruption.”1

Those opposed to increasing nancial assistance to

developing countries in reducing poverty often rely

on the argument that the governments of developing

countries are corrupt and that aid placed into those

developing countries will be wasted.

The Unit acknowledges that corruption is a

signicant problem in some developing countries,

but certainly not all. Further, there is a cycle in which

poverty encourages corruption and corruption then

undermines attempts to reduce the poverty. This

cycle is not broken by withholding nancial support

to impoverished communities, but requires a more

sophisticated approach to shift a culture of corruption

to one of good governance.

Further, wealthy countries can foster corruption

and reward it as they benet from the corruption

themselves. Countries with lax banking laws may in

effect allow money stolen through corruption to be

laundered through their banking system. They may

also fail to assist developing countries in the recovery

of funds stolen through corruption. A number of

wealthy countries do not have adequate laws to

prevent companies based in their country from paying

bribes to ofcials in developing countries where

the company may also be operating. Tax havens,

AusAID, ‘Tackling corruption for growth and development. A Policy for Australian Development Assistance on Anti-Corruption’,Canberra, March 2007, p. iii.

often in wealthy countries, have a whole industry

of accountants, lawyers and bankers dedicated

to assisting rich companies and individuals in the

corrupt avoidance of paying their fair share of tax.

The Royal African Society in London has stated that

Africa loses as much as US$148 billion a year in

corruption, a gure that is accepted by the UN and

the World Bank, and which represents 25% of the

Gross Domestic Product of African countries. Theyclaim this money is rarely invested in Africa, but nds

its way into the international banking system and

often into western banks.

Australia needs to ensure that the Australian banking

system is not a recipient of money taken in corruption

and that any such money must be repatriated to the

country of origin. The Australian Government also

has a role to play in encouraging other developed

countries to reform their banking sectors not to

accept money taken in corruption and to return stolenassets.

Developed countries put staff and resources into

investigating funds related to drugs and terrorism

because these activities are seen to have adverse

effects on people. However, the same effort does

not appear to have been made with regard to money

connected to corruption. Yet, corruption may actually

kill or adversely effect more people than both drugs

and terrorism.

Transparency International has concluded that

corruption is undermining progress towards the UN

Millennium Development Goals, in particular the three

related directly to health: reduced child mortality;

improved maternal health; and the ght against

HIV/AIDS, malaria and other diseases. In their view,

“With the target date for achieving the goals just nine

years away, the global community is already off target

to meet them – and corruption is one of the primary

causes.”2

Curbing corruption is part of the means to creating a

more accountable, efcient and effective government.

It also allows for development that assists those in

2 Transparency International, ‘Theft, bribery and extortion robmillions of proper healthcare, says Global Corruption Report 2006’Media Release, 1 February 2006.

Introduction

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 22/70

poverty. Anti-corruption measures should focus on

a fairer distribution of resources for all in society. A

long term approach is needed where donors cannot

expect signicant change in the short term.

In Section 2 of the report, denitions around good

governance and corruption are explored. Section

3 provides a brief theological consideration of

Christianity’s support for anti-corruption activities

and supporting good governance. Section 4 dealswith what general lessons exist about what is needed

to change a society from one where corruption

ourishes to one in which good governance exists

and the opportunities for corruption are minimised.

This section also provides some examples of

where corruption has been dealt with successfully

and good governance systems installed. Section

5 deals with the ways that wealthy countries can

foster, reward and benet from corruption. Section

6 deals with international measures being pursued

to address corruption as a global problem, looking

at the development of international treaties,

agreements and programs to address corruption

and promote good governance. Section 6 does

not consider the multitude of local initiatives that

exist around the world to address corruption and

develop good governance, with a number of these

having already been addressed in Section 4. Finally,

Section 7 examines how Australia rates in dealing

with corruption. In what ways does Australia seek

to address corruption globally, but also whatinadequacies exist and where is further improvement

needed?

Most of the examples in the report are from the Asia

– Pacic region, but other global examples are used,

especially from Africa.

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 23/70

2Good governance and corruptionworking defnitions

The concept of governance is widely understood as

‘the process of decision-making and the process

by which decisions are implemented (or not

implemented).’ The World Bank and International

Monetary Fund (IMF) dene governance as “the

manner in which public ofcials and institutions

acquire and exercise authority to shape public policy

and provide public goods and services1.”

‘Good governance’ is dened by the United NationsEconomic and Social Commission for Asia and the

Pacic as:

participatory, consensus oriented, accountable,

transparent, responsive, effective and efcient,

equitable and inclusive and follows the rule of

law. It assures that corruption is minimized,

the views of minorities are taken into account

and that the voices of the most vulnerable in

society are heard in decision-making. It is also responsive to the present and future needs of

society 2.

2.1 Participation, equality andinclusion

Participation in civil society includes the decision-

making processes of both men and women, across

race, religion, ethnicity and disability allowing the

concerns of the most vulnerable in society to be

heard and addressed. This would mean ensuring thedevelopment of an organised civil society, as well as

freedom of association and expression.

2.2. Rule of law

Rule of law refers to the impartial enforcement of a

law by an independent judiciary and an incorruptible

and unbiased police force, both upholding the

protection of the human rights of all members of

society.

Development Committee, ‘Strengthening Bank GroupEngagement on Governance and Anticorruption’, World Bank andInternational Monetary Fund, 8 September 2006, p. i.2 United Nations Economic and Social Commission for Asia andthe Pacic http://www.unescap.org/huset/gg/governance.htm

2.3. Transparency andaccountability

Transparency and accountability are inextricably

linked with each other and the rule of law.

Transparency and accountability are achieved when

rules and regulations are followed in an open and

traceable manner. In general, decision-makers and

implementers are accountable to those who are

affected by their decisions and actions.

The international non-government organisation

Transparency International (TI), founded in 1993

to campaign against corruption, has dened

transparency as, “a principle that allows those

affected by administrative decisions, business

transactions or charitable work to know not only the

basic facts and gures, but also the mechanisms

and processes. It is the duty of civil servants,

managers and trustees to act visibly, predictably and

understandably.”

2.4. Efciency and effectiveness

Good governance must involve meeting the needs

of society through making best use of the resources

available, including development assistance as

a substantial resource for some countries. This

includes attention to the sustainable use of resources

and the protection of the environment.

One Christian perspective on ethical governanceargues that:

The needs of the poor are more important

than the wants of the rich; the freedom of the

dominated is more important than the liberty of

the powerful, and; enabling marginalised groups

to participate is more important than retaining a

system which excludes them.

2.5. Dening corruptionTransparency International (TI) initially dened

corruption as, ‘the use of public ofce for private

3 Australian Catholic Bishops’ Conference, Common Wealth forthe Common Good: A Statement on the Distribution of Wealth in

Australia, Melbourne, Collins Dove, 1992.

8/3/2019 Australia, Corruption to Good Governance

http://slidepdf.com/reader/full/australia-corruption-to-good-governance 24/70

gain’. Its founders were motivated by what they saw

as a silence on the part of the World Bank over the

problem of corruption. TI later expanded its denition

to, ‘the misuse of entrusted power for private benet’.

This was seen as necessary in light of the privatisation

of public services such as water and electricity

where private companies were subsequently able to

monopolise the supply of these essential services4.

The German Federal Ministry of EconomicCooperation and Development has dened corruption

as the “behaviour of people who are entrusted with

public or private tasks and who, by failing to respect

their obligations, acquire unjustied advantages.”5

The Tax Justice Network has pointed out that the