australia economics update - anz...economic expansion • fuel prices in australia are low relative...

TRANSCRIPT

1

Australia Economics update

Australia and New Zealand Banking Group Limited

August 2008

2

-1

0

1

2

3

4

5

6

7

8

9

70 75 80 85 90 95 00 05 10

WorldG7Emerging Economies

Real % change from year earlierGlobal economic growth

Global growth is slowing to the weakest in 5 years.......but keep it in perspective

Note: GDP is measured in US$ at purchasing power parities

Sources: IMF and Economics @ ANZ

3

Developing Asian growth will remain strong even as developed country growth slows – US not (yet) in recession

2007 2008 2009 2010

United states 2.2 0.7 0.8 2.3

Eurozone 2.7 1.8 1.4 2.2

United Kingdom 3.1 1.5 1.2 2.4

Japan 2.0 1.3 1.0 2.0

China 11.6 9.9 9.3 9.9

East Asia ex Japan & China

5.9 4.8 4.3 5.4

India 9.0 8.0 8.0 8.5

World 4.8 3.6 3.4 4.4

Sources: Economics @ ANZ

4

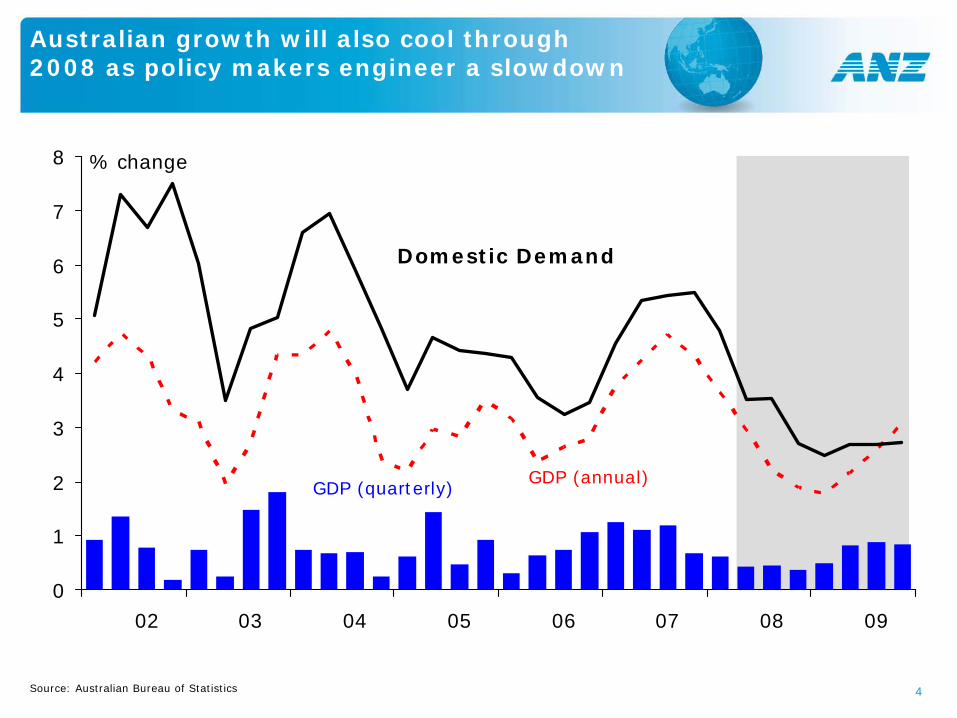

0

1

2

3

4

5

6

7

8

02 03 04 05 06 07 08 09

% change

GDP (quarterly)GDP (annual)

Domestic Demand

Source: Australian Bureau of Statistics

Australian growth will also cool through 2008 as policy makers engineer a slowdown

5

0.0

0.5

1.0

04 05 06 07 08

80

90

100

110

120

130

140% change (trend)

consumer confidence annualised monthly

retail sales monthly % change

Retail sales and consumer sentiment

Economic momentum slowing from higher interest rates, petrol prices and drop in confidence

Business credit

0

5

10

15

20

25

00 01 02 03 04 05 06 07 08

% change from year earlier

0

1

2

3

4

5

6

7

8

NSW SA VIC TAS ACT QLD WA NT

2006-07 (e)2007-08 (f)2008-09

%

Real Gross State Product

Sources: Australian Bureau of Statistics and Economics@ANZ & WBC

6

0

1

2

3

4

5

6

7

8

9

90 94 98 02 06

% change from year earlier

Developed Economies

Total World

Global inflation

Global inflation has spiked in 2008 to the highest since 1999 …and developed countries highest since 1991!

Note: Inflation is GDP weighted

Sources: IMF and Economics @ ANZ

5.3%

3.5%

7

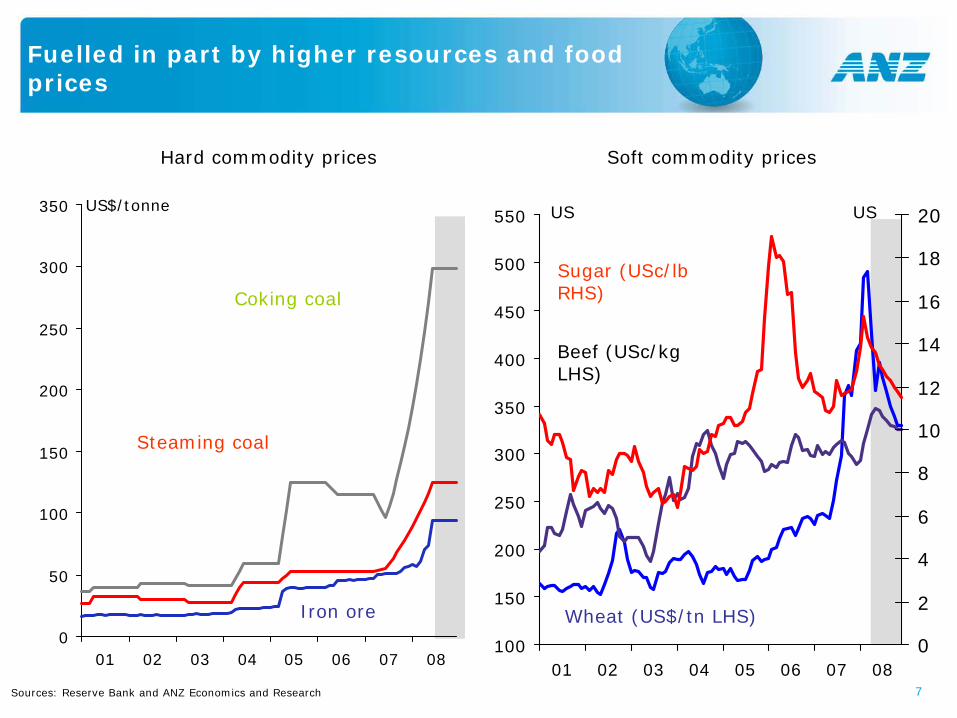

0

50

100

150

200

250

300

350

01 02 03 04 05 06 07 08

US$/tonne

100

150

200

250

300

350

400

450

500

550

01 02 03 04 05 06 07 080

2

4

6

8

10

12

14

16

18

20US US

Hard commodity prices Soft commodity prices

Coking coal

Steaming coal

Iron ore

Sources: Reserve Bank and ANZ Economics and Research

Wheat (US$/tn LHS)

Beef (USc/kgLHS)

Sugar (USc/lbRHS)

Fuelled in part by higher resources and food prices

8

0

1

2

3

4

5

97 99 01 03 05 07

annual % change

Targetband

Core inflation

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

02 03 04 05 06 07

annual % change

Tradeables and non-tradeables

Source: Australian Bureau of Statistics

Non tradeables

Tradeables

In Australia core inflation is at decade highs and much of it is home grown

9

65

70

75

80

85

90

95

100

105

110

115

120

2-Apr 14-May

25-Jun

6-Aug 17-Sep

29-Oct

10-Dec

21-Jan

3-Mar 14-Apr

26-May

7-Jul

Index, 2 April=100

Japan

UK

Australia

USA

Global equity markets are still taking a hammering and Australia has not been immune

International equity market comparisons

Source: Bloomberg

10

-80-40

04080

120160200

94 96 98 00 02 04 06 08

Australia’s housing market has also softened, but is unlikely to become as dire as US

-20-15-10-505

101520

01 02 03 04 05 06 07 08

% change from year earlier

Australia

US

House prices

* 90 days or more past due. For Australia, securitized mortgages only. Sources: ABS; US Commerce Department; S&P; Mortgage Bankers’ Association of America, Economics@ANZ

Mortgage delinquency rates*

0

1

2

3

4

5

01 02 03 04 05 06 07 08

% of total loans outstanding

Australia

US

0.0

0.5

1.0

1.5

2.0

01 02 03 04 05 06 07 08

% change from year earlierAustralia

US

Population growth

Housing market balance

Underlying Requirement

Completions

Forecast

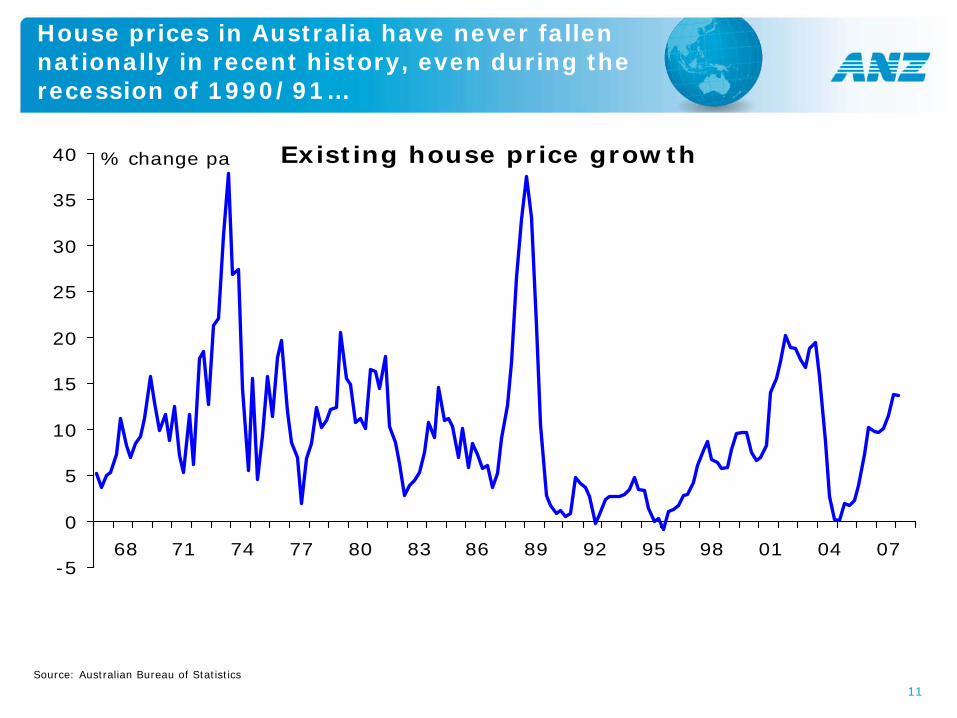

11

-5

0

5

10

15

20

25

30

35

40

68 71 74 77 80 83 86 89 92 95 98 01 04 07

% change pa Existing house price growth

Source: Australian Bureau of Statistics

House prices in Australia have never fallen nationally in recent history, even during the recession of 1990/91…

12

Existing house prices

…although individual markets have at times gone south with Sydney the most recent example

Sources: Australian Bureau of Statistics and Economics@ANZ

100

150

200

250

300

350

400

450

500

550

02 03 04 05 06 07

$'000Sydney

Perth

Hobart

Canberra

Melbourne

Brisbane

Adelaide

Darwin

13

0

3

6

9

97 98 99 00 01 02 03 04 05 06 07 08 09

%

Australia

USA

UK

Europe

NZ

Japan

Global cash rates

Global cash rate moves have been desynchronised

Sources: Bloomberg and Economics @ ANZ

14

0

20

40

60

80

100

120

140

160

86 90 94 98 02 0660

80

100

120

140

160

180US$bbl

Crude (LHS)

Aust Petrol (RHS)

Ac litreGlobal oil and Australian petrol prices

Third oil price shock - record price highs for global oil and Australian petrol

Sources: BP Review and Economics @ ANZ

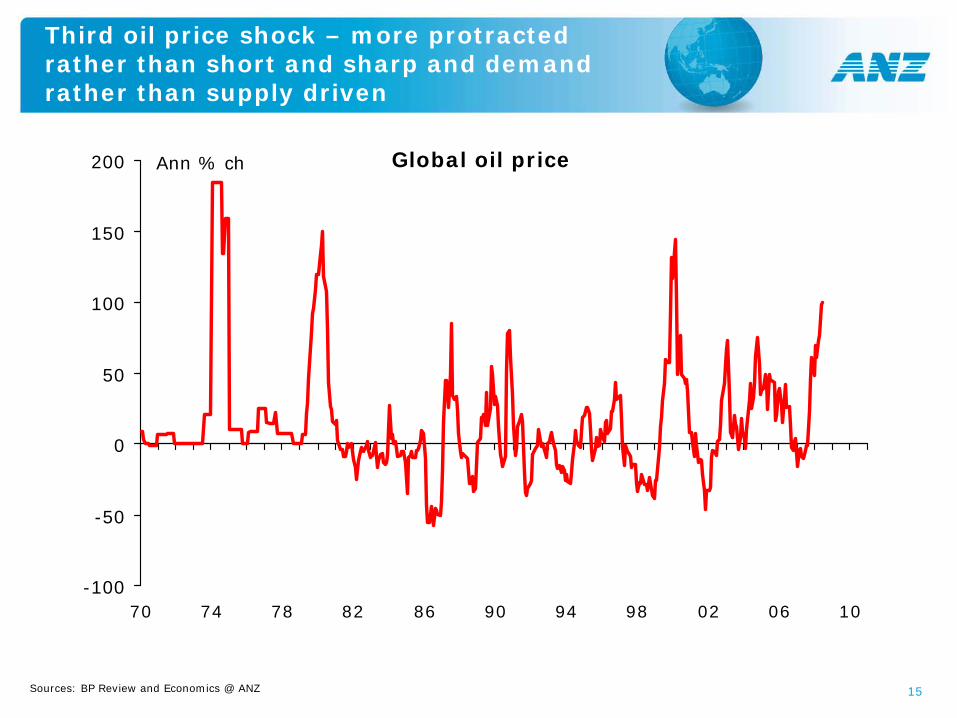

15

-100

-50

0

50

100

150

200

70 74 78 82 86 90 94 98 02 06 10

Ann % ch Global oil price

Third oil price shock – more protracted rather than short and sharp and demand rather than supply driven

Sources: BP Review and Economics @ ANZ

16

200

400

600

800

1000

1200

1400

80 85 90 95 00 05

Thousand million barrels

“Proven” oil reserves may be plateauing – and most reserves are in OPEC hands – although production expected to keep rising for now, so globally not yet at “peak oil”

Sources: BP Statistical Review

60

65

70

75

80

85

90

90 95 00 05 10

Mn barrels a day

World oil production

Total Reserves

OPEC Reserves

World Reserves

17

0

5

10

15

20

25

30

90 95 00 05 10

% global consumption

USA

China

US still biggest oil consumer – but it is the growth of China which is driving the big increase in demand

Sources: BP World Energy Review

Consumption of oil

18

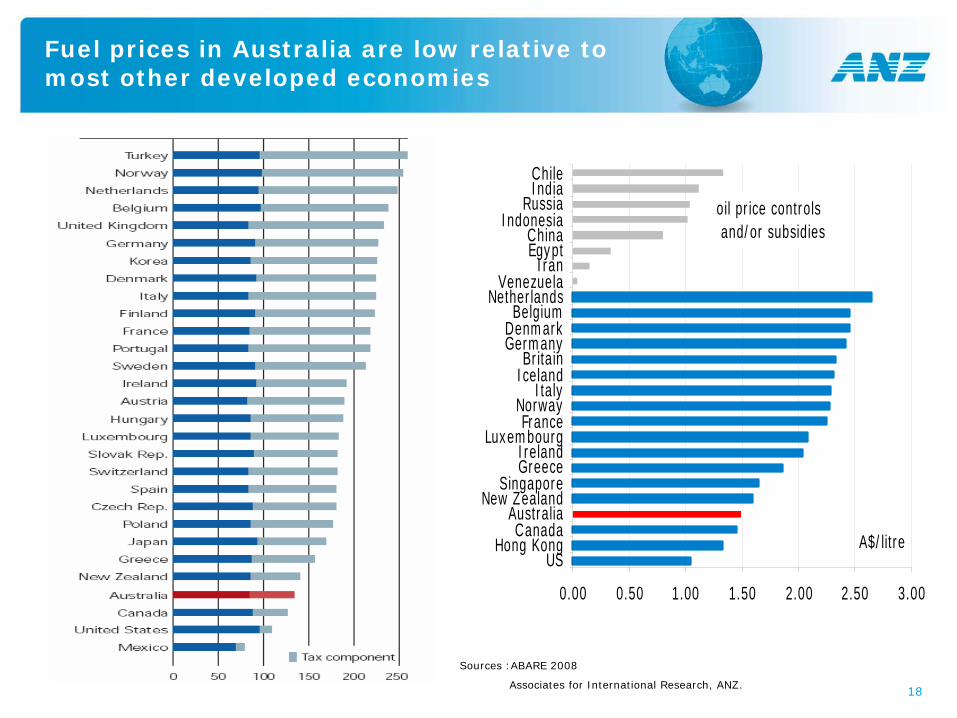

Fuel prices in Australia are low relative to most other developed economies

oil price controls and/or subsidies

0.00 0.50 1.00 1.50 2.00 2.50 3.00

USHong Kong

CanadaAustralia

New ZealandSingapore

GreeceIreland

LuxembourgFrance

NorwayItaly

IcelandBritain

GermanyDenmarkBelgium

NetherlandsVenezuela

IranEgyptChina

IndonesiaRussia

IndiaChile

A$/litre

Sources :ABARE 2008

Associates for International Research, ANZ.

19

Impacts of higher fuel costs

• For households, fuel is a smaller component of spending than commonly believed at under 3% total household spending.

• Nevertheless, if petrol price increases were at the expense of other retail spending, then each 10c increase would reduce retail spending by 0.5%.

• Average household purchases 35 litres petrol and 2.6 litres diesel weekly. At $1.50 litre that amounts to $56.40. Note that 10% households have no car so for those that do cost could be $62.65.

20

0

100

200

300

400

500

600

700

800

900

1000

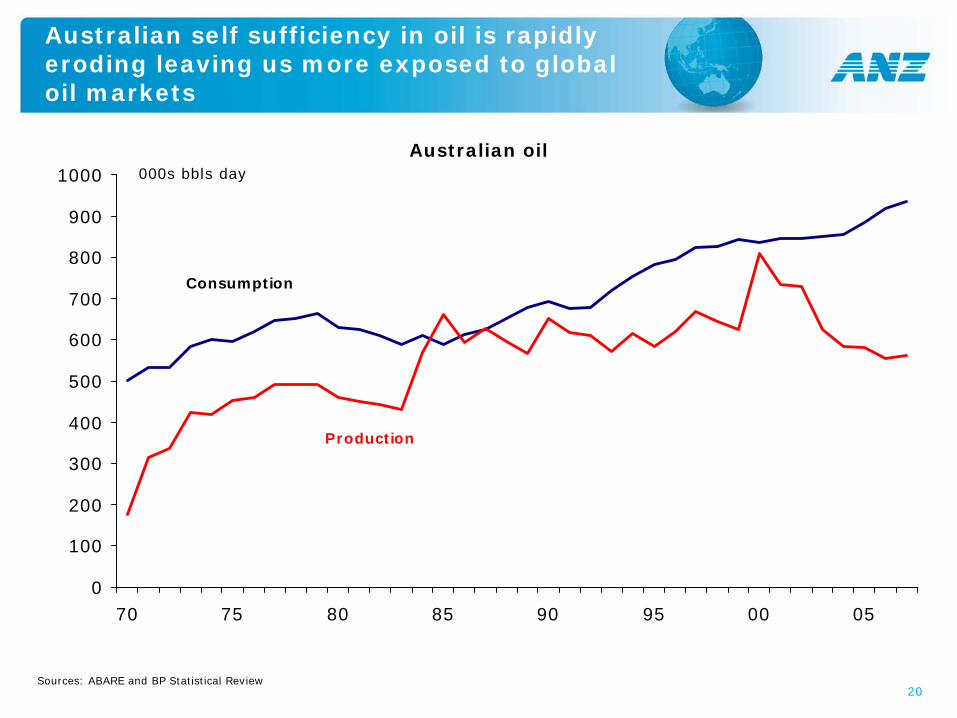

70 75 80 85 90 95 00 05

000s bbls day

Consumption

Production

Australian oil

Australian self sufficiency in oil is rapidly eroding leaving us more exposed to global oil markets

Sources: ABARE and BP Statistical Review

21

Oil shortages – Are biofuels the answer?

• First generation biofuels essentially use food – grains and sugar and vegetable oils – to make synthetic petrol and diesel

• World Bank reports that biofuels have increased global food prices by up to 75% since 2002. More than a third of US corn now used for ethanol and half of vegetable oils in EU used for biodiesel

• Higher energy and fertiliser costs have accounted for 15% of higher food prices

• Income growth in developing nations has not been a major factor

• Biofuels derived from sugar cane have not had such a dramatic effect

• The answer might lie in “second generation” biofuels which use plant waste like sugar bagasse, stalks and wood waste

22

First Garnaut – and now the Carbon Pollution Reduction Scheme Green Paper

Reducing carbon emissions means reducing use of carbon releasing fossil fuels like oil, gas and coal, and also reducing clearing of carbon sequestering trees

The primary mechanism for reducing use of carbon is to increase its price, which will be achieved via a cap and trade emissions trading scheme

– Commencing in 1 July 2010

– Covers 1000 significant-emitting companies, responsible for around 75% of Australia’s total GHG emissions – other companies should not panic

– Agriculture, which is responsible for around 16% of GHG emissions, will be excluded till at least 2015

– Petrol will be included in the scheme, but price effect will be offset by equivalent reduction in fuel excise

– Money raised from the scheme will be used to compensate households and business. For example, emissions intensive trade exposed industries will receive free permits equivalent to up to 90% of estimated permit requirement

An emissions trading system will:

– result in higher prices for energy (+16% for electricity and +9% for gas), fuel and food

– increase inflation (+0.9%) and reduce growth

– potentially have a big impact on coal, electricity generation, transport, agriculture

Crucial details of the scheme are still to be released (such as the short-term targets and who qualifies for concessions), and the final design is still open to discussion. But it is worth keeping in mind the overall effect of the ETS must hurt to be effective and to change behaviour!

Climate Change – Adapt or Perish!

23

0

5

10

15

20

25

30

Australia USA EU UK Japan China India World

Carbon dioxide equivalents Mt pa

Greenhouse Gas Emissions per capita

Source: Stern Review

Climate change – Australia is one of the world’s biggest carbon emitters per capita

24

0

50

100

150

200

250

300

350

Electricity Industry Agriculture Methanefrom

landfill

Land use Transport FugitiveEmissions

Carbon dioxide equivalents Mt pa

Australia’s Greenhouse Gas Emissions 2006

Source: Department of Climate Change. Greenhouse gases include carbon dioxide, methane, nitrous oxide, hydrofluorocarbons, perfluorocarbons, sulphur hexafluoride

Climate change – Power generation is Australia’s biggest greenhouse gas emitter

25

Climate Change – See the opportunities, not the costs

Massive investment required in

• Water saving infrastructure

• Low carbon fuels “clean coal”

• Energy saving technology for households and business

• Alternative energy (wind, thermal, hydro, solar)

• Forestry and other carbon sequestration

• Many initiatives will be government supported and in part government funded

26

Australia – Still the lucky country despite the challenges ahead

• Although global growth is slowing, the international environment relevant to Australia will remain buoyant

• Further massive rises in commodity prices will boost income flows into Australia

• Australia has moved early to combat inflation – rates may have peaked – RBA will restore low inflation environment to underpin continued economic expansion

• Fuel prices in Australia are low relative to most other developed economies

• Climate change is a big challenge – Australia has a lot to lose from inaction but costs of mitigation will not be trivial – nevertheless presents opportunities to be a world leader

• Overall still the lucky country, still a great time to be Australian

27

0

5

10

15

20

25

00 01 02 03 04 05 06 07 08

% change from year earlier

Credit growth slowing sharply across all sectors

Sources: RBA; Economics@ANZ

Housing credit Personal credit

Business credit Total credit

0

5

10

15

20

00 01 02 03 04 05 06 07 08

% change from year earlier

0

5

10

15

20

25

00 01 02 03 04 05 06 07 08

% change from year earlier

0

5

10

15

20

00 01 02 03 04 05 06 07 08

% change from year earlier

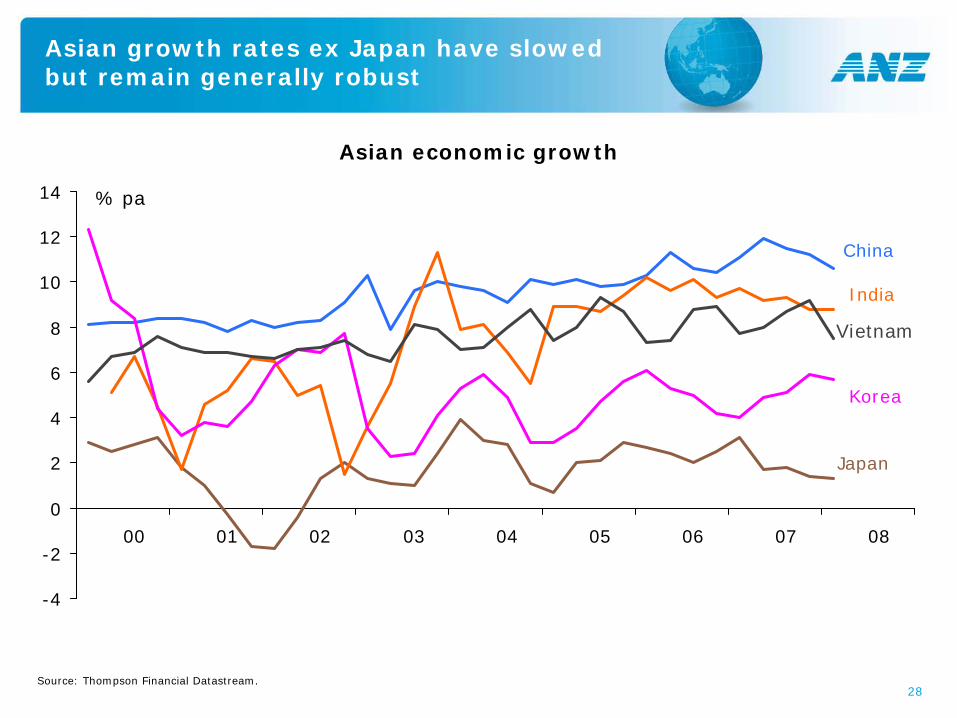

28

-4

-2

0

2

4

6

8

10

12

14

00 01 02 03 04 05 06 07 08

% pa

China

India

Japan

Korea

Vietnam

Asian growth rates ex Japan have slowed but remain generally robust

Source: Thompson Financial Datastream.

Asian economic growth

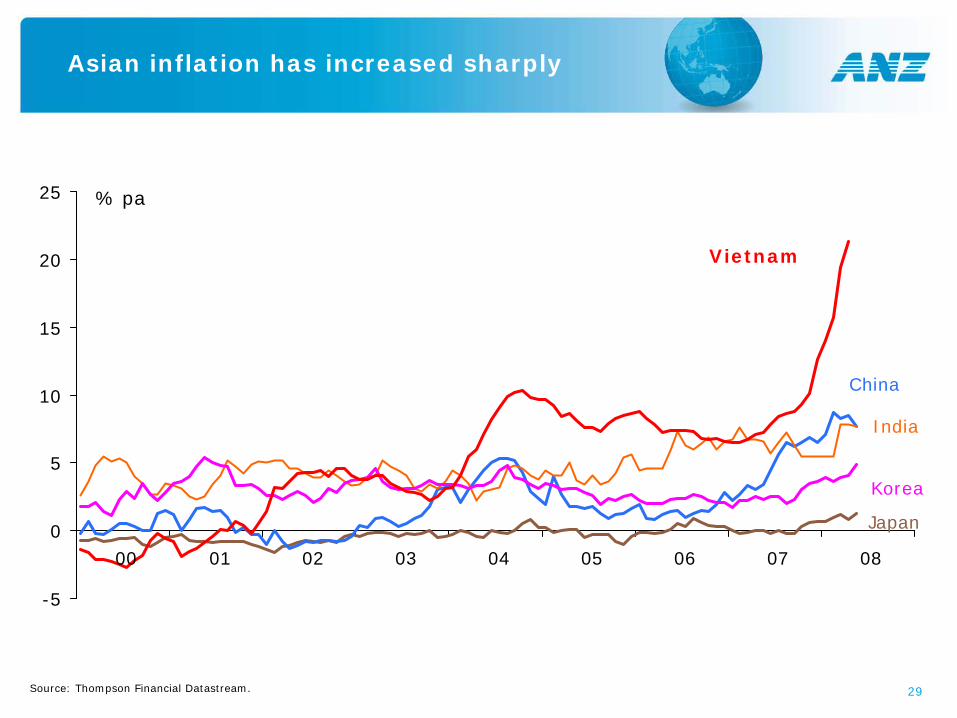

29

-5

0

5

10

15

20

25

00 01 02 03 04 05 06 07 08

% pa

China

India

Japan

Korea

Vietnam

Asian inflation has increased sharply

Source: Thompson Financial Datastream.

30

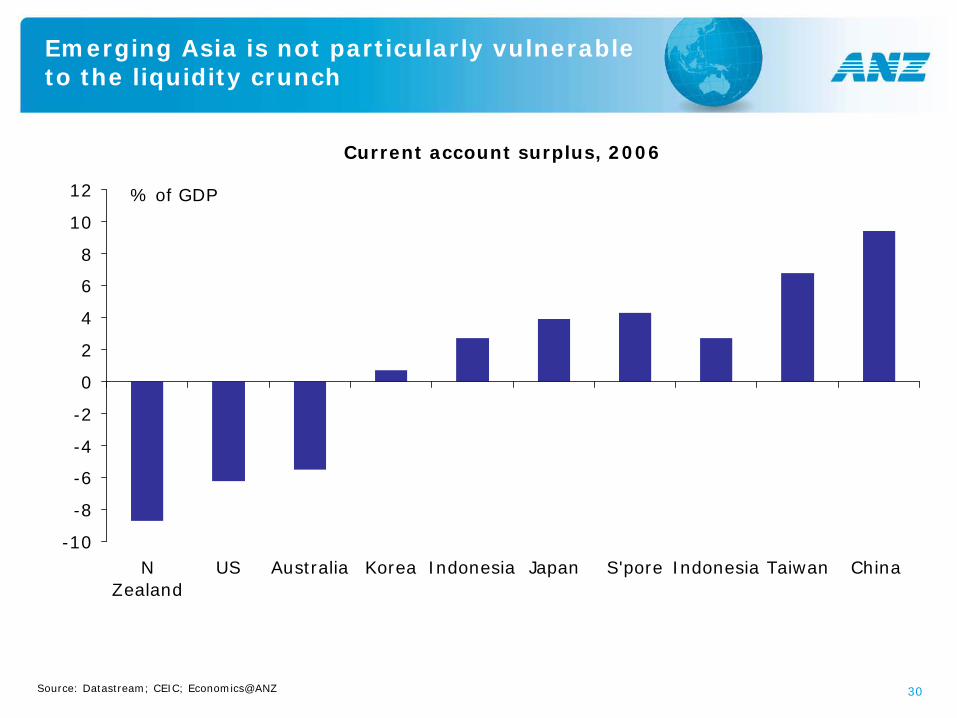

Emerging Asia is not particularly vulnerable to the liquidity crunch

-10

-8

-6

-4

-2

0

2

4

6

8

10

12

NZealand

US Australia Korea Indonesia Japan S'pore Indonesia Taiwan China

% of GDP

Current account surplus, 2006

Source: Datastream; CEIC; Economics@ANZ

31

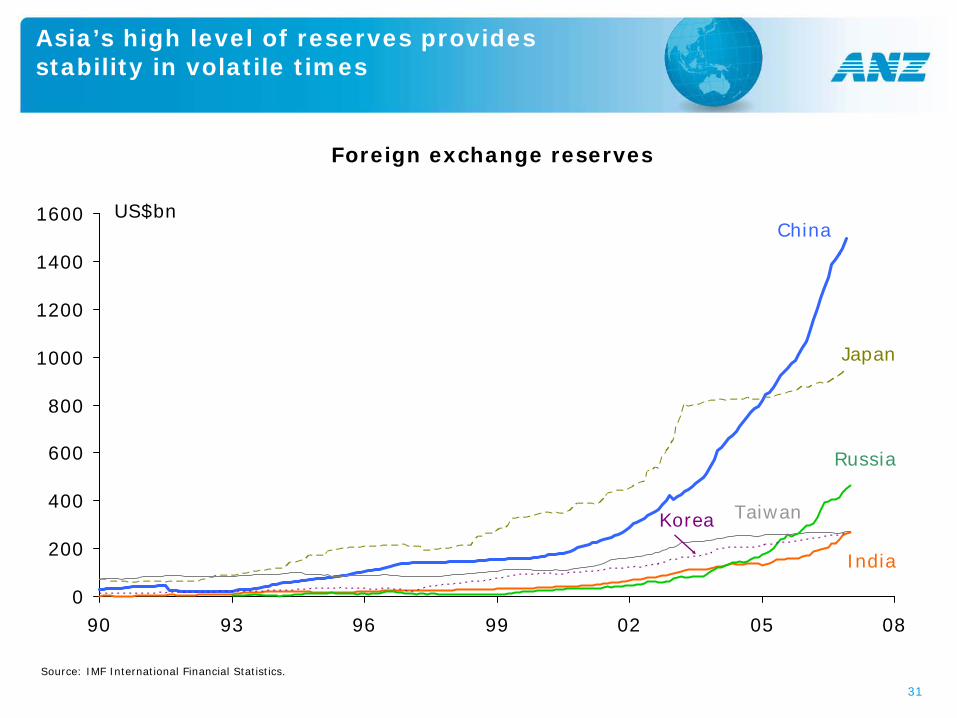

0

200

400

600

800

1000

1200

1400

1600

90 93 96 99 02 05 08

US$bn

Japan

Russia

India

China

TaiwanKorea

Asia’s high level of reserves provides stability in volatile times

Source: IMF International Financial Statistics.

Foreign exchange reserves

32

Disclaimer

• This document (“document”) is distributed to you in Australia and the United Kingdom by Australia and New Zealand Banking Group Limited ABN 11 005 357 522 (“ANZ”) and in New Zealand by ANZ National Bank Limited (“ANZ NZ”). ANZ holds an Australian Financial Services licence no. 234527 and is authorised in the UK by the Financial Services Authority (“FSA”).

• This document is being distributed in the United States by ANZ Securities, Inc. (“ANZ S”) (an affiliated company of ANZ), which accepts responsibility for its content. Further information on any securities referred to herein may be obtained from ANZ S upon request. Any US person(s) receiving this document and wishing to effect transactions in any securities referred to herein should contact ANZ S, not its affiliates.

• This document is being distributed in the United Kingdom by ANZ for the information of its market counterparties and intermediate customers only. It is not intended for and must not be distributed to private customers. In the UK, ANZ is regulated by the FSA. Nothing here excludes or restricts any duty or liability to a customer which ANZ may have under the UK Financial Services and Markets Act 2000 or under the regulatory system as defined in the Rules of the FSA.

• This document is issued on the basis that it is only for the information of the particular person to whom it is provided. This document may not be reproduced, distributed or published by any recipient for any purpose. This document does not take into account your personal needs and financial circumstances. Under no circumstances is this document to be used or considered as an offer to sell, or a solicitation of an offer to buy.

• In addition, from time to time ANZ, ANZ NZ, ANZ S, their affiliated companies, or their respective associates and employees may have an interest in any financial products (as defined by the Australian Corporations Act 2001), securities or other investments, directly or indirectly the subject of this document (and may receive commissions or other remuneration in relation to the sale of such financial products, securities or other investments), or may perform services for, or solicit business from, any company the subject of this document. If you have been referred to ANZ, ANZ NZ, ANZ S or their affiliated companies by any person, that person may receive a benefit in respect of any transactions effected on your behalf, details of which will be available upon request.

• The information herein has been obtained from, and any opinions herein are based upon, sources believed reliable. The views expressed in this document accurately reflect the author’s personal views, including those about any and all of the securities and issuers referred to herein. The author however makes no representation as to its accuracy or completeness and the information should not be relied upon as such. All opinions and estimates herein reflect the author’s judgement on the date of this document and are subject to change without notice. No part of the author's compensation was, is or will directly or indirectly relate to specific recommendations or views expressed about any securities or issuers in this document. ANZ, ANZ NZ, ANZ S, their affiliated companies, their respective directors, officers, and employees disclaim any responsibility, and shall not be liable, for any loss, damage, claim, liability, proceedings, cost or expense (“Liability”) arising directly or indirectly (and whether in tort (including negligence), contract, equity or otherwise) out of or in connection with the contents of and/or any omissions from this communication except where a Liability is made non-excludable by legislation.

• Where the recipient of this publication conducts a business, the provisions of the Consumer Guarantees Act 1993 (NZ) shall not apply..

Important NoticeAustralia and New Zealand Banking Group Limited is represented in:AUSTRALIA by:Australia and New Zealand Banking Group Limited ABN 11 005 357 52210th Floor 100 Queen Street, Melbourne 3000, AustraliaTelephone +61 3 9273 6224 Fax +61 3 9273 5711UNITED KINGDOM by:Australia and New Zealand Banking Group LimitedABN 11 005 357 52240 Bank Street, Canary Wharf, London, E14 5EJ, United KingdomTelephone +44 20 3229 2121 Fax +44 20 7378 2378

UNITED STATES OF AMERICA by:ANZ Securities, Inc. (Member of NASD and SIPC)6th Floor 1177 Avenue of the AmericasNew York, NY 10036, United States of AmericaTel: +1 212 801 9160 Fax: +1 212 801 9163NEW ZEALAND by:ANZ National Bank LimitedLevel 7, 1-9 Victoria Street, Wellington, New ZealandTelephone +64 4 802 2000

33

The material in this presentation is general background information about the Bank’s activities current at the date of the presentation. It is information given in summary

form and does not purport to be complete. It is not intended to be relied upon as advice to investors or potential investors and does not take into account the investment

objectives, financial situation or needs of any particular investor. These should be considered, with or without professional advice when deciding if an investment is

appropriate.

For further information visit

www.anz.comor contact

Jill CraigHead of Investor Relations

ph: (613) 9273 4185 fax: (613) 9273 4091 e-mail: [email protected]