australia roadmap v45 - 3d printing expo australia may...

TRANSCRIPT

Additive Manufacturing

Technology Roadmap

for Australia

AustraliaCoverFinal_Layout 1 6/13/11 1:45 PM Page 1

Additive ManufacturingTechnology Roadmap

for Australia

Created by

Wohlers Associates, Inc.OakRidge Business Park1511 River Oak Drive

Fort Collins, Colorado 80525 USA970-225-0086

Fax 970-225-2027wohlersassociates.com

March 2011

AustraliaCoverFinal_Layout 1 2/10/11 11:52 AM Page 2

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 3 Wohlers Associates, Inc.

Table of Contents

BACKGROUND.............................................................................................................................................. 5

EXECUTIVE SUMMARY ................................................................................................................................ 6

1.0 INTRODUCTION ..................................................................................................................................... 8

1.1 FACTORY OF THE FUTURE ....................................................................................................................... 8 1.2 BRIEF HISTORY OF AM IN AUSTRALIA ....................................................................................................... 9 1.3 AUSTRALIA’S MANUFACTURING INDUSTRY................................................................................................. 9

2.0 GROWTH OF ADDITIVE MANUFACTURING .......................................................................................10

2.1 WORLDWIDE REVENUES.........................................................................................................................11 2.2 WORLDWIDE UNIT SALES .......................................................................................................................11 2.3 GROWTH OF PRODUCTION APPLICATIONS ................................................................................................13

3.0 STRENGTHS AND LIMITATIONS OF THE TECHNOLOGY.................................................................14

3.1 MATERIAL PROPERTIES..........................................................................................................................14 3.2 COST CONSIDERATIONS.........................................................................................................................16 3.3 PART FEATURES AND FINISH...................................................................................................................17 3.4 THE NEED FOR ANCHORS.......................................................................................................................18 3.5 INDUSTRY STANDARDS...........................................................................................................................19

4.0 NEW OPPORTUNITIES .........................................................................................................................19

4.1 FLEXIBILITY OF DESIGN AND MANUFACTURING..........................................................................................20 4.2 DESIGN FREEDOM .................................................................................................................................20 4.3 INCREASED FUNCTIONALITY....................................................................................................................21 4.4 REDUCED MATERIAL AND ENERGY CONSUMPTION ....................................................................................21

5.0 PART PRODUCTION APPLICATIONS..................................................................................................21

5.1 AEROSPACE..........................................................................................................................................22 5.2 MEDICINE .............................................................................................................................................24 5.3 NEW BUSINESSES AND BUSINESS MODELS ..............................................................................................26 5.4 PRODUCTION VOLUMES SUITABLE FOR AM..............................................................................................28

6.0 ENVIRONMENTAL CONCERNS ...........................................................................................................28

6.1 ATKINS PROJECT...................................................................................................................................29 6.2 LIGHTWEIGHT STRUCTURES....................................................................................................................30

7.0 PRODUCTION OF METAL PARTS .......................................................................................................30

7.1 POWDER-BED SYSTEMS ........................................................................................................................31 7.2 POWDER AND WIRE DEPOSITION SYSTEMS ..............................................................................................32 7.3 OTHER METAL-BASED SYSTEMS.............................................................................................................33 7.4 COSTS AND OTHER CONSIDERATIONS .....................................................................................................33

8.0 TITANIUM...............................................................................................................................................34

8.1 PRODUCING THE METAL .........................................................................................................................34 8.2 TITANIUM AND ITS ALLOYS......................................................................................................................35 8.3 APPLICATIONS.......................................................................................................................................36 8.4 TITANIUM IN AUSTRALIA..........................................................................................................................36

9.0 ALUMINIUM ...........................................................................................................................................37

10.0 FUTURE OPPORTUNITIES AND FORECASTS .................................................................................38

10.1 MID TERM (2015)................................................................................................................................38 10.2 LONG TERM (2015–2025) ...................................................................................................................41 10.3 ADOPTION OF AM FOR PART PRODUCTION ............................................................................................43

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 4 Wohlers Associates, Inc.

11.0 RECOMMENDATIONS.........................................................................................................................44

11.1 APPLICATIONS RESEARCH AND EDUCATION............................................................................................45 11.2 CENTRES OF EXCELLENCE ...................................................................................................................45 11.3 COMPANY INCUBATION.........................................................................................................................46 11.4 TECHNOLOGY ADOPTION......................................................................................................................46 11.5 REMOTE MANUFACTURING FACILITIES ...................................................................................................47 11.6 INSTRUCTOR TRAINING.........................................................................................................................47 11.7 CONFERENCE SERIES ..........................................................................................................................48 11.8 MATERIALS RESEARCH AND DEVELOPMENT ...........................................................................................48 11.9 DOMESTIC PROCESSING OF MINERALS ..................................................................................................49 11.10 INDUSTRY STANDARDS DEVELOPMENT ................................................................................................49 11.11 GLOBALISM.......................................................................................................................................50

SUMMARY ....................................................................................................................................................50

APPENDIX A: EXTERNAL REVIEWERS .....................................................................................................52

A.1 AEROSPACE AND DEFENCE ....................................................................................................................52 A.2 BIOMEDICAL AND DENTAL.......................................................................................................................53 A.3 AUTOMOTIVE AND MOTOR SPORTS .........................................................................................................53 A.4 CONSUMER PRODUCTS AND SPORTING GOODS .......................................................................................53 A.5 LEADING INTERNATIONAL TECHNOLOGY/SERVICE PROVIDERS ...................................................................54 A.6 LEADING PUBLIC RESEARCH PROVIDERS AND CENTRES OF EXCELLENCE ...................................................54 A.7 LEADING INDUSTRY BODIES AND CONSULTANTS.......................................................................................55

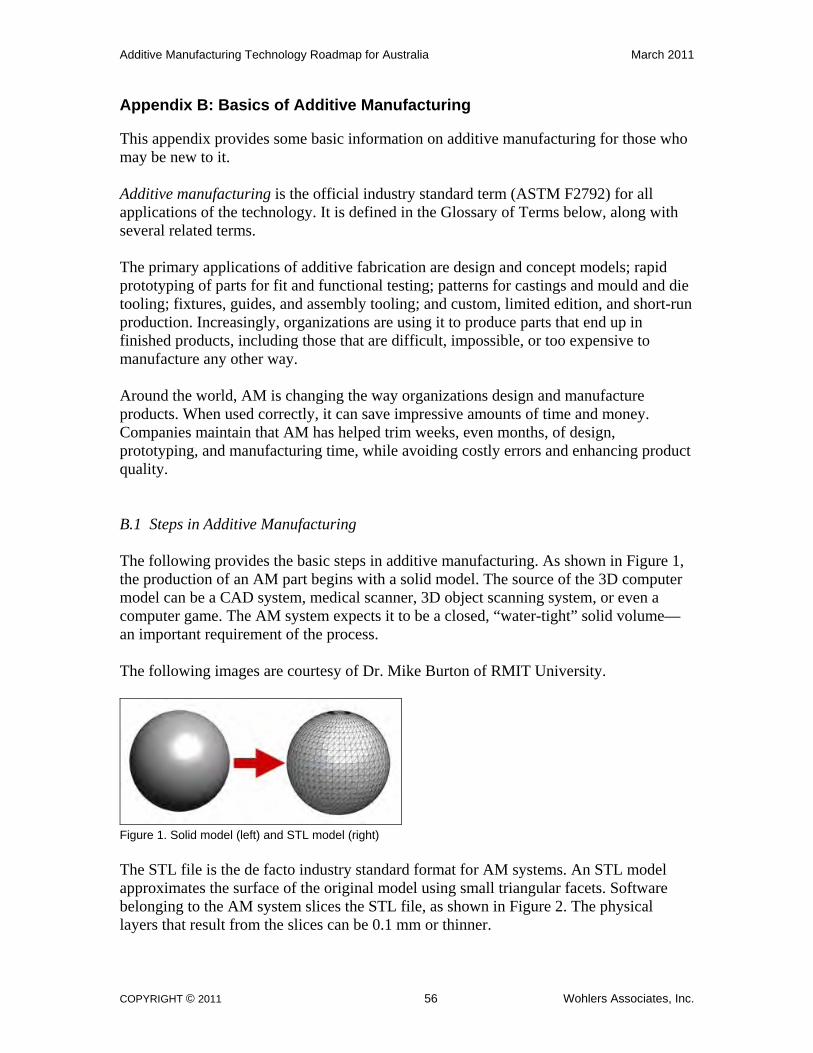

APPENDIX B: BASICS OF ADDITIVE MANUFACTURING.........................................................................56

B.1 STEPS IN ADDITIVE MANUFACTURING ......................................................................................................56 B.2 GLOSSARY OF TERMS............................................................................................................................58

APPENDIX C: HISTORY OF ADDITIVE MANUFACTURING IN AUSTRALIA ............................................60

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 5 Wohlers Associates, Inc.

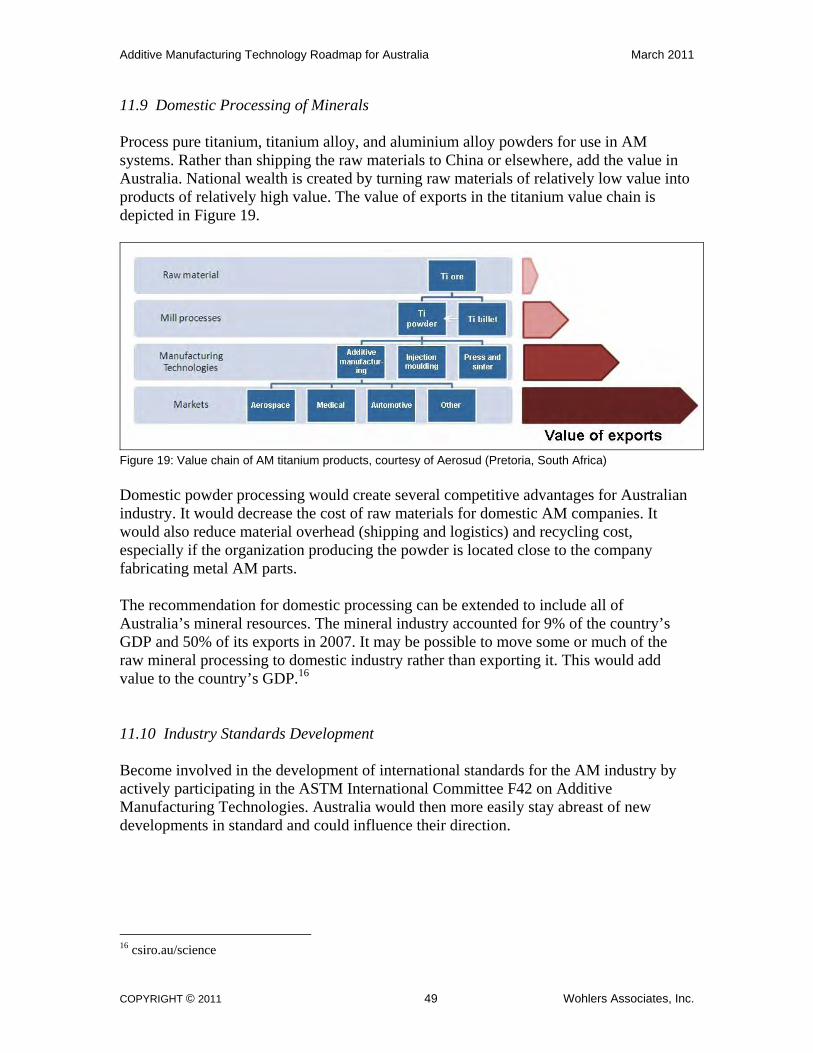

Background In September 2010, Wohlers Associates was commissioned by CSIRO to create an industry-aligned additive manufacturing (AM) technology roadmap for Australia. Its focus was to be on metals with a particular emphasis on titanium. The following lists the primary outcomes of the project. 1) Identify the market, technology, and other drivers associated with the development of

additive manufacturing technologies worldwide.

2) Identify current, emerging, and likely future market opportunities for additive manufacturing in Australia, particularly for metals and especially titanium and titanium alloys.

3) Identify future technology needs and associated enablers for Australian industry to take advantage of these opportunities.

4) Forecast technology development trends and opportunities in the targeted areas.

5) Offer a framework to assist with planning, coordination, and uptake of technology development by industry.

6) Identify critical technologies, enablers, and gaps. Technology road mapping often begins with input from a spectrum of individuals and organizations. This input is then used to form the basis of the roadmap. Wohlers Associates instead used its collective knowledge and experience to create a rough draft version of the roadmap. It then shared the early draft with many industry experts from around the world. It is believed that this approach reduced the time required to complete the work and led to a higher quality and more useful final product. Wohlers Associates was fortunate to have received in-depth ideas, opinions, and suggestions from 30 top experts and opinion leaders in design, new product development, additive manufacturing, and/or materials science. Among them were individuals from CSIR (South Africa), Chrysler (USA), Formero (Australia), Northrop Grumman (USA), Procter & Gamble (USA), Renault F1 (England), RMIT University (Australia), and Walter Reed Army Medical Center (USA). Many of their ideas and suggestions were further developed and integrated into this roadmap document.

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 6 Wohlers Associates, Inc.

Executive Summary Additive manufacturing (AM) technology is having an impact on product development and manufacturing around the world. Companies such as Airbus, Audi, BMW, Boeing, Cochlear, Ford, General Electric, Hewlett-Packard, Nike, ResMed, and Sunbeam as well as countless small and medium-sized organizations, use the technology extensively. Parts produced by AM are going into aircraft, race cars, home and office products, and human beings. The demand for products and services from AM technology has been strong over its 22-year history. The compound annual growth rate (CAGR) of revenues produced by all products and services over this period is 26.4%. Due to the Great Recession, the CAGR slowed to 3.3% during the period 2007–2009. The future for additive manufacturing is bright. The overall economic impact of the technology is believed to be in the billions of dollars worldwide. It is impossible to estimate the benefit precisely because the total savings of avoiding costly design errors at so many companies around the world is unknown. AM helps to reduce mistakes and delays to a minimum and produce winning products. Australia is presented with the opportunity to embrace AM technology to help stimulate and streamline product development and manufacturing. Also, AM provides Australia the prospect of creating new types of products, businesses, business models, and jobs. With its vast mineral resources, Australia is in a position to produce materials, such as titanium, and use them to create high-value products that are sold domestically and internationally. The following provides a set of specific recommendations for Australia. They are presented in more detail in Section 11 of this document. Applications Research and Education: Consider projects that evaluate the feasibility of using additive manufacturing for production applications. Centres of Excellence: Launch national and/or regional centres of excellence in Australia. Their purpose would be to conduct applications research, and offer courses and workshops on additive manufacturing. Company Incubation: Create incubator programmes at educational institutions in Australia to help those with ideas for a new product or service. Technology Adoption: Encourage companies in Australia to adopt additive manufacturing technology for advanced prototyping, tooling, and part production applications. Remote Manufacturing Facilities: Due to Australia’s relative isolation and large distances between its own population centres, establish AM facilities to overcome the logistic issues of supplying parts or products.

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 7 Wohlers Associates, Inc.

Instructor Training: Conduct instructor training for the faculty and staff of high schools, vocational schools, colleges, and universities in Australia. Conference Series: Support annual series of conferences on additive manufacturing to bring new ideas from around the world to Australia. Material Research and Development: Sponsor or co-sponsor metals-based research and development programmes in Australia. Domestic Processing of Minerals: Process pure titanium, titanium alloy, and aluminium alloy powders for use in AM systems. Industry Standards Development: Become involved in the development of international standards for the AM industry. Globalism: Encourage globalism in industry, academia, and government throughout the country to promote an international outlook and overcome market isolation. This roadmap focuses on the needs of Australia and includes contributions from customers and suppliers of additive manufacturing, government, and the public research sector. The roadmap emphasizes metals, with a particular focus on titanium, and addresses Australia’s opportunity to process titanium inside the country rather than exporting raw materials to other countries for processing. This document also considers the importance of using additive manufacturing technology to reduce cost, lead time, and damage to our environment.

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 8 Wohlers Associates, Inc.

1.0 Introduction The purpose of this document is to provide the Australian government and industry with direction and guidelines on additive manufacturing (AM) technology and its possible acceptance on a national scale. ASTM International Committee F42 on Additive Manufacturing Technologies defines additive manufacturing as the process of joining materials to make objects from 3D model data, usually layer upon layer, as opposed to subtractive manufacturing methodologies. Synonyms are additive fabrication, additive processes, additive techniques, additive layer manufacturing, layer manufacturing, and freeform fabrication. Wohlers Associates fully supports this definition and encourages others around the world to adopt it. This roadmap considers the wealth of new developments and opportunities that AM technology presents. Among them are new types of products that would be difficult or impractical to manufacture by traditional methods. AM is also creating innovative businesses, business models, and supply chains, and so this document takes them into account. It considers exciting possibilities in high-value custom and limited edition products, replacement part manufacturing, short-run production, and series production in aerospace, defence, medical, transportation, and other industrial sectors. 1.1 Factory of the Future In June 2010, Australia served as host to the “Factory of the Future” series of conferences, workshops, and company presentations. All of them focused on the use of additive manufacturing for part production applications. About 600 engineering and manufacturing professionals from across the country attended the events, which were held in Melbourne, Adelaide, Sydney, and Brisbane. Organizers and participants of the series found that companies in Australia have used AM technology for prototyping applications for many years. In fact, an estimated 390 AM systems were installed in Australia through the end of 2010, according to research conducted by Wohlers Associates. However, few companies in the country have applied it to part production applications. This is where many of the most interesting and exciting opportunities lie, especially in metals. The event series also revealed a sense of urgency in Australia to fully understand how additive manufacturing can reduce lead time, cost, and waste—and how it can help position manufacturers to better compete globally. In part, it is believed that the June 2010 series of events established the basis for this roadmap. The people of Australia are not only interested in AM technology, but they are genuinely excited about what it can bring to them, to their organizations, and to the country as a whole. The “light bulb” has switched on, and it is now clear that Australia is ready to take additive manufacturing to a new level.

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 9 Wohlers Associates, Inc.

1.2 Brief History of AM in Australia Additive manufacturing was introduced to Australia by Vipac Engineering when it installed an SLA 250 stereolithography machine from 3D Systems in its Melbourne premises in 1990. Its intention was to demonstrate the new technology and sell machines, materials, and services. No machines were sold. The equipment and agency were acquired, moved to Brisbane, and set up as a technology diffusion and transfer operation about one year later at the newly formed Queensland Manufacturing Institute (QMI). In the early 1990s, the South Australian Centre for Manufacturing (SACFM) came into being in Adelaide. Its aims and objectives were similar to that of QMI. It adopted the laser-sintering process in 1993 and laminated object manufacturing (LOM) in 1995. A high degree of cooperation developed between SACFM and QMI in their joint efforts to demonstrate AM’s capabilities to industry and encourage the uptake of 3D CAD and AM, then referred to as rapid prototyping. It was not until the early 2000s that AM technologies, which then included less expensive 3D printing systems, were sufficiently understood and adopted by industry. At around this time, both QMI and SACFM withdrew from its AM activities. Since then, many new AM systems have been installed throughout Australia, with significant growth in fused deposition modelling (FDM) technology, and most recently, PolyJet from Objet Geometries. Service providers, such as Formero (previously Silhouette and then ARRK ANZ) in Melbourne and Solid Concepts in Perth, were early adopters and pioneers in the use of AM. They have been instrumental in bringing the technology to where it is today. In 2002, 3D Systems announced that it had partnered with the University of Queensland and UniQuest (both of Queensland) to develop an aluminium powder for its laser-sintering (LS) process. The work continued for many years, but the material was never commercialized. A longer version of Australia’s history of additive manufacturing is found in Appendix C. 1.3 Australia’s Manufacturing Industry Manufacturing’s contribution to Australia’s gross domestic product peaked in the 1960s at 25%, and has dropped slowly and steadily since. Manufacturing revenues have barely kept pace with inflation, growing at an average of 3% over the past two decades. Despite the health of the country’s mining and agricultural sectors, export growth has remained flat compared to strong import growth. The economy has been affected by the global economic crisis and increased competition from foreign suppliers.1 Australia has a large immigrant population from China, Indonesia, and other Asian countries. The manual labour force is thus fairly large and wages are relatively low,

1 wikipedia.com, csiro.au/science

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 10 Wohlers Associates, Inc.

which may impede the growth of additive manufacturing. Australia also outsources much of its manufacturing to nearby countries where labour costs are very low. The manufacturing industry, however, is very important to Australia. More than one million people are employed in manufacturing and the industry accounts for over half of total exported goods. Large manufacturers produce automobiles, including Ford Australia, GM Holden, and Toyota. In the aerospace industry, Boeing Australia is the company’s largest operation outside the U.S., employing 3,500 in 2009. Other key manufacturing sectors include machinery, chemical production, transport equipment, food processing, and steel production.2 In a speech given in May 2009, CSIRO chief executive Dr. Megan Clarke said, “It has long been recognized that Australia must focus on making products at the high-value end of the global market—knowledge rich products. Manufacturing enterprises of the future will be small to medium and export oriented.” The key challenge is to produce finished parts for export instead of exporting raw materials. In the words of Innovation, Industry, Science, and Research minister Kim Carr, “We can win only in industries in which we can add value, ideally covering the entire value chain from raw materials to the finished product.” 3 Additive manufacturing is an enabling technology that can help the Australian manufacturing industry achieve this goal. 2.0 Growth of Additive Manufacturing The demand for products and services from additive manufacturing technology has been strong in Australia and other parts of the world. The compound annual growth rate (CAGR) of revenues produced by all products and services worldwide over a period of 22 years is 26.4%, according to Wohlers Report 2010. The CAGR slowed to 3.3% during the years 2007–2009, with 2009 being the slowest. Data for 2010 is not yet available, although anecdotal information suggests that strong growth returned in late 2010. Several indicators point to solid growth in 2011. Additive manufacturing is a growing technology for several reasons. AM plays a role in reducing cost in manufacturing. Examples are highlighted in later sections of this document. Another reason is a cultural development: there is a trend toward more custom products. The “one size fits all” model does not work as well as it once did. AM is a tool that allows designers to create unique products that can be manufactured at low volumes in an economical way. Another driver of AM technology is its environmental and ecological promise. AM technologies have the potential to reduce the carbon footprint of manufacturing by using

2 wikipedia.com, csiro.au/science, boeing.com.au, nationsencyclopedia.com/economies 3 csiro.au/science

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 11 Wohlers Associates, Inc.

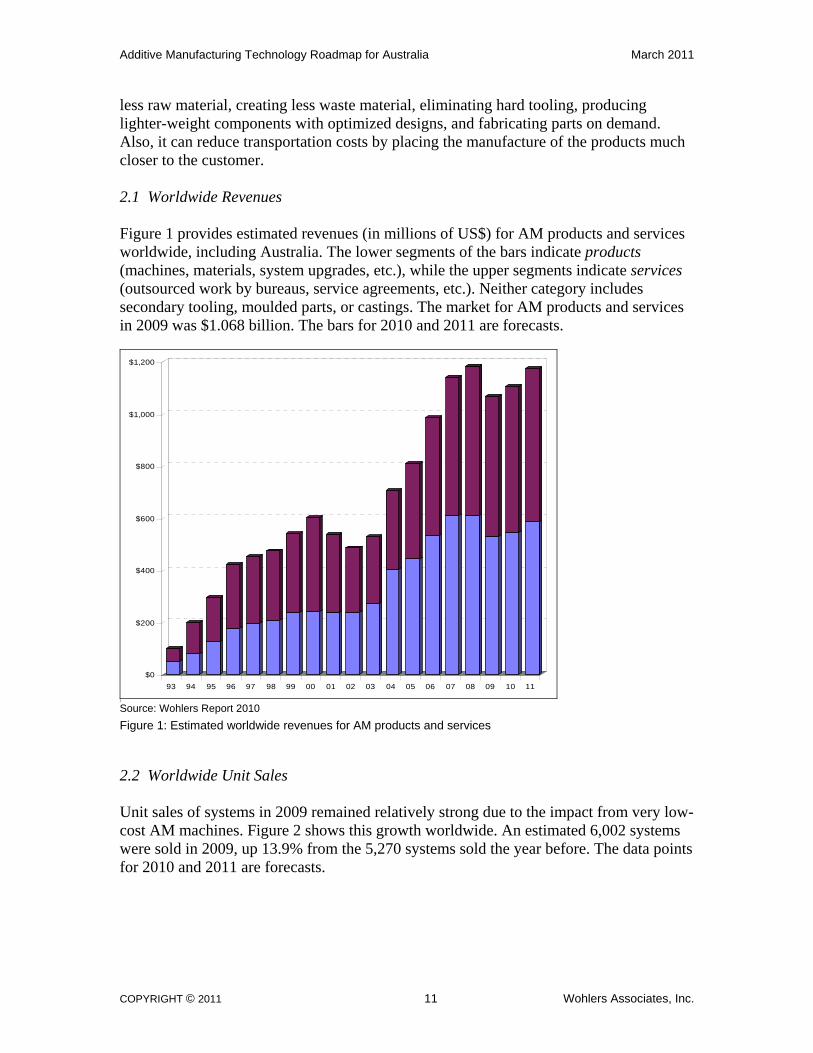

less raw material, creating less waste material, eliminating hard tooling, producing lighter-weight components with optimized designs, and fabricating parts on demand. Also, it can reduce transportation costs by placing the manufacture of the products much closer to the customer. 2.1 Worldwide Revenues Figure 1 provides estimated revenues (in millions of US$) for AM products and services worldwide, including Australia. The lower segments of the bars indicate products (machines, materials, system upgrades, etc.), while the upper segments indicate services (outsourced work by bureaus, service agreements, etc.). Neither category includes secondary tooling, moulded parts, or castings. The market for AM products and services in 2009 was $1.068 billion. The bars for 2010 and 2011 are forecasts.

$0

$200

$400

$600

$800

$1,000

$1,200

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11

2

Source: Wohlers Report 2010

Figure 1: Estimated worldwide revenues for AM products and services 2.2 Worldwide Unit Sales Unit sales of systems in 2009 remained relatively strong due to the impact from very low-cost AM machines. Figure 2 shows this growth worldwide. An estimated 6,002 systems were sold in 2009, up 13.9% from the 5,270 systems sold the year before. The data points for 2010 and 2011 are forecasts.

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 12 Wohlers Associates, Inc.

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11

Source: Wohlers Report 2010

Figure 2: Unit sales of AM systems worldwide The lengths of the bars in Figure 3 indicate the AM systems sold in 2009. The units along the horizontal axis are arbitrary values and do not reflect the exact number of systems sold. The chart shows where Australia stands in relation to other countries around the world. It is somewhat surprising, even puzzling, that Australia would trail smaller countries such as Turkey and Taiwan. The “Other” segment includes countries with a relatively small number of AM systems, although some are expanding their installations quickly.

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 13 Wohlers Associates, Inc.

0 200 400 600 800 1000 1200 1400 1600

U.S.

China

Germany

Japan

UK

Italy

France

Korea

Canada

Russia

Turkey

Taiwan

Australia

Sweden

Brazil

Spain

Thailand

India

Switzerland

Poland

Israel

South Africa

Other

Source: Wohlers Report 2010

Figure 3: AM system sales in 2009

Growth is expected to continue, especially with the relatively new low-cost AM systems that are becoming available. Today, an individual, school, or company can purchase a non-industrial AM system for A$3,000. Even lower cost systems are available as a kit that the purchaser assembles. These systems are appealing to cost-conscience buyers and will introduce the fundamental technology to many people in Australia and around the world. 2.3 Growth of Production Applications One of the fastest growing applications of additive manufacturing is the production of end-use products. This segment grew by 22.8% in 2009, compared to 19.9% the year before. This is according to 71 service providers and system manufacturers from around the world that responded to a survey on the subject. Three of the service providers are located in Australia. Together, the 71 companies represent more than an estimated 5,000 users and customers of AM technology.

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 14 Wohlers Associates, Inc.

3.0 Strengths and Limitations of the Technology Additive manufacturing technology is used broadly for design, product development, and manufacturing. Among the applications are concept modelling, design validation, prototyping for fit and functional testing, patterns for castings, parts for mould and die tooling; fixtures, guides, and assembly tooling; and custom, limited edition, and short-run production. AM has been used for many of these applications for more than two decades. AM is well understood for modelling and prototyping in Australia and most developed countries around the world. Organizations can easily rationalize its use for models and prototypes because the cost and time benefits are clear. The technology has matured to the point where many companies no longer need to create a written justification for having AM prototypes built. This is similar to how companies no longer need to justify the use of CAD. Both CAD and AM (for prototyping) have become industry standard methods for new product development around the world. Mike Naylon, a former QMI employee and now a consultant in additive manufacturing, pointed out that in 1925—20 years after Bakelite was patented—very few plastic materials were available. At the time, they were expensive, difficult to process, and had poor and variable properties. Even in the 1960s, many products made in plastic were considered substandard. Naylon explained that additive manufacturing materials and processes of today are far more advanced than the plastics were back then, and they are continually improving. This gives us some indication of where AM materials could go in the future. 3.1 Material Properties The material properties of parts made on an AM system are a consideration. Plastic parts from additive manufacturing do not typically match the properties of injection-moulded parts made from the same material. The high packing pressure of injection moulding forces the material to completely fill the mould, which minimizes shrink and produces fully dense parts. This is not true for thermoplastic-based AM systems, such as LS and FDM. For these processes, it is difficult to build fully dense parts because there is no analogous “packing pressure” as there is in injection moulding. LS, for example, is said to produce parts that are 97–98% dense, although density could be in the range of 90–92%, depending on the build parameters set by the machine operator. Also, the bond between layers can impact the strength of an AM part. This is not to suggest that plastic parts from AM systems are not strong enough for many part production applications; it only states that they do not match the properties of the same material that is injection moulded. Several AM users report that they have built fully dense thermoplastic-based parts in their AM systems, though they concede it can take work and iteration to achieve. Most additive manufacturing systems that build metal parts melt the materials and approach 100% density. While not all are fully dense, the result is usually a part that is

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 15 Wohlers Associates, Inc.

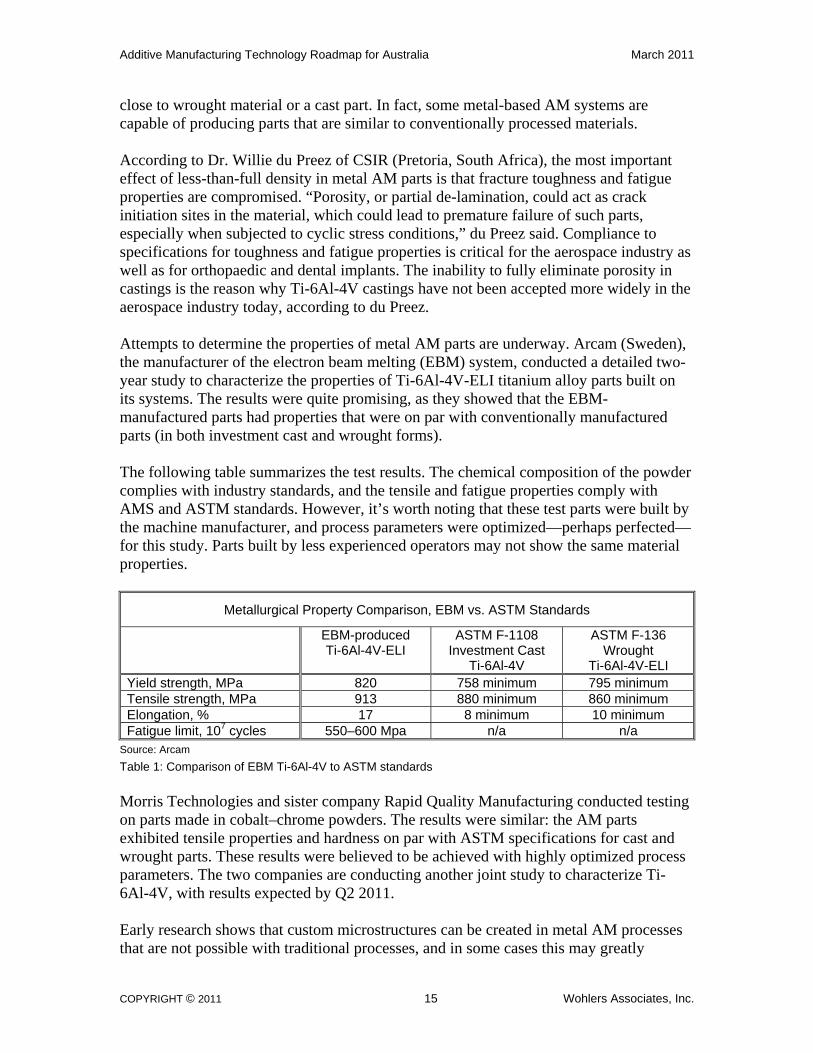

close to wrought material or a cast part. In fact, some metal-based AM systems are capable of producing parts that are similar to conventionally processed materials. According to Dr. Willie du Preez of CSIR (Pretoria, South Africa), the most important effect of less-than-full density in metal AM parts is that fracture toughness and fatigue properties are compromised. “Porosity, or partial de-lamination, could act as crack initiation sites in the material, which could lead to premature failure of such parts, especially when subjected to cyclic stress conditions,” du Preez said. Compliance to specifications for toughness and fatigue properties is critical for the aerospace industry as well as for orthopaedic and dental implants. The inability to fully eliminate porosity in castings is the reason why Ti-6Al-4V castings have not been accepted more widely in the aerospace industry today, according to du Preez. Attempts to determine the properties of metal AM parts are underway. Arcam (Sweden), the manufacturer of the electron beam melting (EBM) system, conducted a detailed two-year study to characterize the properties of Ti-6Al-4V-ELI titanium alloy parts built on its systems. The results were quite promising, as they showed that the EBM-manufactured parts had properties that were on par with conventionally manufactured parts (in both investment cast and wrought forms). The following table summarizes the test results. The chemical composition of the powder complies with industry standards, and the tensile and fatigue properties comply with AMS and ASTM standards. However, it’s worth noting that these test parts were built by the machine manufacturer, and process parameters were optimized—perhaps perfected—for this study. Parts built by less experienced operators may not show the same material properties.

Metallurgical Property Comparison, EBM vs. ASTM Standards

EBM-produced Ti-6Al-4V-ELI

ASTM F-1108 Investment Cast

Ti-6Al-4V

ASTM F-136 Wrought

Ti-6Al-4V-ELI Yield strength, MPa 820 758 minimum 795 minimum Tensile strength, MPa 913 880 minimum 860 minimum Elongation, % 17 8 minimum 10 minimum Fatigue limit, 107 cycles 550–600 Mpa n/a n/a

Source: Arcam

Table 1: Comparison of EBM Ti-6Al-4V to ASTM standards

Morris Technologies and sister company Rapid Quality Manufacturing conducted testing on parts made in cobalt–chrome powders. The results were similar: the AM parts exhibited tensile properties and hardness on par with ASTM specifications for cast and wrought parts. These results were believed to be achieved with highly optimized process parameters. The two companies are conducting another joint study to characterize Ti-6Al-4V, with results expected by Q2 2011. Early research shows that custom microstructures can be created in metal AM processes that are not possible with traditional processes, and in some cases this may greatly

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 16 Wohlers Associates, Inc.

improve the properties of the part. Dr. Ola Harrysson of North Carolina State University explained that with casting, solidification of the metal starts at the mould surface, since it is coolest, and results in a refined microstructure at the surface. The grains continue to form and grow toward the centre of the casting as it cools, oriented toward the middle point. The speed of solidification slows, so the grains tend to be larger, with reduced material properties. Harrysson went on to explain that when casting metal alloys, the alloy with the highest melting point will start to solidify first, and as the casting cools from the surface toward the middle, the grains will have different concentrations of the alloying elements. Thus, the concentration of alloys will vary throughout the part; the material properties will not be isotropic and the grains will form in specific orientations. “Direct metal additive manufacturing processes melt a very small amount of material at a time,” Harrysson said. “Rapid solidification will take place, resulting in a more uniform microstructure through the part.” For metal alloys, some segregation of the alloying elements takes place, but on a much smaller scale. The chemical composition is more uniform throughout the part, resulting in better material properties, he explained. This is why direct metal AM parts can have material properties that exceed the properties of cast parts and approach the properties of forged parts. Harrysson said some studies have shown that the scanning pattern of the energy beam can create microstructures that have never been seen before, and that it is possible to customize the microstructure by controlling the scanning pattern and modifying the orientation of the part. It is worth noting that switching from one metal powder to another in the same machine can be problematic. Contamination of the build environment could occur, compromising the integrity of the material used in manufacturing applications. 3.2 Cost Considerations One of additive manufacturing’s considerations is the cost of machines and materials. New machines are being sold for less than A$20,000, but demanding industrial applications can require machines that cost A$200,000–400,000 or more. Even if you outsource the building of parts, the cost of the machine can impact the cost of the parts. Every part built on the system shares a piece of the original equipment cost, as well as maintenance and other costs associated with operating the machine. Systems that produce parts in metal can cost from A$390,000 to more than A$1 million. At the same time, metal AM parts have a much higher value than their plastic counterparts. Even though the metal machines are more expensive, they have the potential to generate much higher revenues with the same amount of machine time. Materials for AM are typically priced many times higher than equivalent materials used in conventional manufacturing processes. Generally, they range from about A$65 to A$450 for 1 kg. Most AM plastics—both thermoplastics and photopolymers—are priced in the A$175 to A$250 per kg range. For FDM from Stratasys, this translates to about

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 17 Wohlers Associates, Inc.

A$4.44 per 16.4 cm3 for both model and support material. For machines from Z Corp., the material cost is A$2 to A$3 per 16.4 cm3, which includes the powder, binder, infiltrant, and print head. While these prices are widely accepted for modelling and prototyping applications, they may be high for manufacturing quantities. By comparison, injection moulding plastics are priced from about A$2.40 to A$3.30 per kg, meaning that AM plastics are 53 to 104 times more expensive. For injection moulding, you need to also consider mould costs, lead times, and other factors such as part complexity. As one might expect, metal powders are more expensive than their plastic counterparts. Ti-6Al-4V for direct metal laser sintering from EOS (Germany) is about A$680 per kg. Cobalt-chrome for the same process is A$420 per kg. Meanwhile, Ti-6Al-4V and dental-grade cobalt-chrome from SLM Solutions (Germany) lists for about A$900 and A$290, respectively. Aluminium (AlSi12) is A$84, 316L stainless steel is A$126, and H13 tool steel is A$126. These prices exclude shipping costs and applicable taxes. As demand grows and volumes increase, prices will decline, but for now, they are expensive. A growing number of materials are becoming available for AM, but it’s still a small fraction compared to materials that are available for conventional methods of manufacturing. One might argue that the final part cost is more important than the system or material price. When calculating the cost of AM parts, it important to consider all costs, including machine depreciation, maintenance, labour, material, and overhead. Including machine depreciation means that every part built includes a small fraction of the original cost of the machine. AM machines are typically depreciated over a period of 5 to 7 years in Australia. This cost can be significant if the machine purchase price is high. That’s why the cost of a part built on an inexpensive machine can be significantly lower than the same part build on an expensive machine, even if other costs are the same. At some companies, the cost of materials is about 15 to 20% of the cost of a part, although this can vary depending on the size of the part and the level of finish required. A high level of finish requires skilled labour, and this portion of the overall cost can be significant. The shape of the part has an impact on material cost and the amount of support material needed. Some machines use more support material than others. Also, waste comes from processes, such as plastic laser sintering (LS), which cannot recycle much of the unused powder. About 30 to 40% of all loose powder in the build chamber becomes scrap after the parts are built. 3.3 Part Features and Finish The surface finish of metal parts produced in AM systems is often relatively poor compared to plastic parts from AM systems. As a result, a considerable amount of time and money can be required to post-process parts. This post-processing can defeat the purpose of using AM technologies in the first place, because a fixture and CNC machining may be required. Parts with many freeform surfaces can be difficult to fixture

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 18 Wohlers Associates, Inc.

during machining setup. And parts with internal surfaces can be very difficult or impossible to finish. “At the moment there is a gap between the AM technologies and the finishing technologies,” said Dr. Harrysson. He believes the total production process, including post-processing, needs to be perfected to fabricate metal components at an economical level and at a truly rapid rate. Best in Class (Switzerland) is one example of a company that has developed a finishing technology for metal AM parts. Their proprietary Micro Machining Process produces impressive, high-quality surface finishes for metal parts. Another limitation to consider is parts with small features or internal structures, such as meshes. When using powder-based AM processes, it can be quite difficult to remove the powder from the mesh after the build because some of the unmelted powder may become partially sintered during the build process. 3.4 The Need for Anchors AM systems that build metal parts require anchors to secure the parts and their features to the build plate, and to reduce distortion due to high thermal stresses. According to Tim Gornet of the University of Louisville, these stresses exist due to the large thermal differences between the molten layer and the underlying cooler layer. There is a much larger temperature difference between the melt area and the unmelted powder surrounding it with metal powders, so thermal stress and distortion is a bigger issue. For most metal powder bed systems, a secondary thermal process is needed to relieve these thermal stresses. The requirement for anchors is a limitation that is important to understand. Both laser and electron beam systems use anchors when building parts, although the laser systems require them to a much greater degree. The anchors require time to build and they use material that becomes scrap. Worse, they can be difficult or impossible to remove when they are located in internal cavities, holes, or channels. After removal, unwanted artefacts are sometimes left behind that scar the surface of the part. The design may be altered to reduce the need for anchors, but customers usually do not want to make design changes due to the need for anchors. Sometimes, the orientation of the part in the build chamber can be changed to reduce the need for anchors. However, other build parameters may then be adversely affected, such as increasing the z-height, which lengthens the build time. Even with this limitation, laser-based AM systems are being used for part production. For example, laser-based machines are being used to manufacture dental copings. A dental coping is the main structural body of a crown or bridge. Copings are typically coated with a thin layer of porcelain to produce a more realistic looking tooth. An experienced dental technician can produce about 8–10 crowns per day. One AM machine is capable of producing up to 400 copings in cobalt–chrome in about 20 hours. As of mid-2010, an estimated 6,000 copings were being manufactured daily using laser-based AM systems

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 19 Wohlers Associates, Inc.

from EOS, MTT Technologies Group (England), SLM Solutions, Concept Laser (Germany), Phenix Systems (France), and ReaLizer (Germany). 3.5 Industry Standards Industry standards have been lacking for years in the additive manufacturing industry. In 2009, ASTM International Committee F42 on Additive Manufacturing Technologies was formed. It consists of representatives that span four continents and includes companies such as Arcam, Boeing, DePuy Spine, EOS, General Electric, Goodrich, Honeywell, Lockheed Martin, Materialise, Objet Geometries, Raytheon, Stratasys, the U.S. Army, and Z Corp. The purpose of the committee is to develop industry standards for terminology, testing, materials, processes, and design, which includes file formats. The first industry standard from the group—a terminology standard—was published in Q4 2009. As of October 2010, no individuals or organizations from Australia had contributed to this ASTM effort. For AM to advance to a wider range of production applications, the development of industry standards is important. Few industries develop fully without them. Also, the cost of machines and materials must improve, and almost certainly will, as demand and production volumes increase and industry standards emerge. 4.0 New Opportunities

Systems for additive manufacturing are mature for prototyping in Australia and other parts of the world, but not for production applications. Even so, many organizations are applying AM to the production of end-use products. An impressive range of industrial examples are found in aerospace, defence, motor sports, medicine, dentistry, automotive, video games, lighting designs, furniture, jewellery, and other consumer products. Innovative individuals and organizations are creating new businesses, business models, and supply chains that were unthinkable in the past. Inventory consists of 3D models stored on a server and products that are manufactured on demand. This makes it easier for manufacturing to occur closer to the customer and reduces inventory, shipping costs, and lead time. A reduction of excess inventory can have a significant effect. The costs of manufacturing and storing products until they are needed, coupled with the cost of associated inventory taxes, can be greatly diminished by producing small batches and parts on demand.

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 20 Wohlers Associates, Inc.

4.1 Flexibility of Design and Manufacturing Additive manufacturing is attractive for the production of parts because it eliminates the need for tooling. Moulds and dies are expensive, require weeks or months of lead time, and lock you into a design. With AM, companies and individuals are given much more freedom to experiment with and manufacture new designs without making a large commitment. This dramatically reduces risk and allows the commercialization of new products to see whether a market appetite exists for them. With additive manufacturing, part quantities can be as low as a few or even one without major negative consequences. This permits the production of affordable custom and limited edition products, as well as replacement parts. Additive manufacturing provides unprecedented levels of flexibility in production and redefines reconfigurable manufacturing. It is possible for a company to manufacture metal parts for an aircraft engine, orthopaedic implants, and dental copings in cobalt chrome—all in a single build. The following day, the company can be producing a mix of similar or different parts in a titanium alloy. 4.2 Design Freedom AM also offers freedom of design and creation. Some would argue that it is the most powerful benefit of the technology. As Tim Gornet of the University of Louisville puts it, “AM allows for one to manufacture for design instead of design for manufacture.” When using moulds, dies, CNC machines, and other conventional methods of manufacturing, designers are faced with constraints, such as die-lock conditions. For example, if it is impossible to remove a part from an injection mould, the design cannot be manufactured without making changes. These changes could result in a substandard design or the need to produce it in two or more parts, which creates the need for additional tooling. The freedom to design without the constraints of tooling allows designers to compensate for the slightly inferior properties of AM materials. A plastic part built on an AM system may not deliver the properties of an injection-moulded part, but the part could be designed to have the same structural integrity—a design that may not have been possible before due to tooling constraints. With additive manufacturing, it is possible to manufacture nearly anything that can be modelled as a 3D volume on a computer. This includes parts with multiple undercuts, highly complex and convoluted features, and shapes that would be impossible to produce any other way. Consider that a complete human skull, with all internal features, can be manufactured in its entirety in a single piece on an AM system. With additive manufacturing’s freeform capabilities, it will be important for Australia’s design community to fully understand what AM brings to them and their organizations. Young and veteran designers alike will need to learn when AM is an option and when it is not and how a design can change when AM is used for part production.

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 21 Wohlers Associates, Inc.

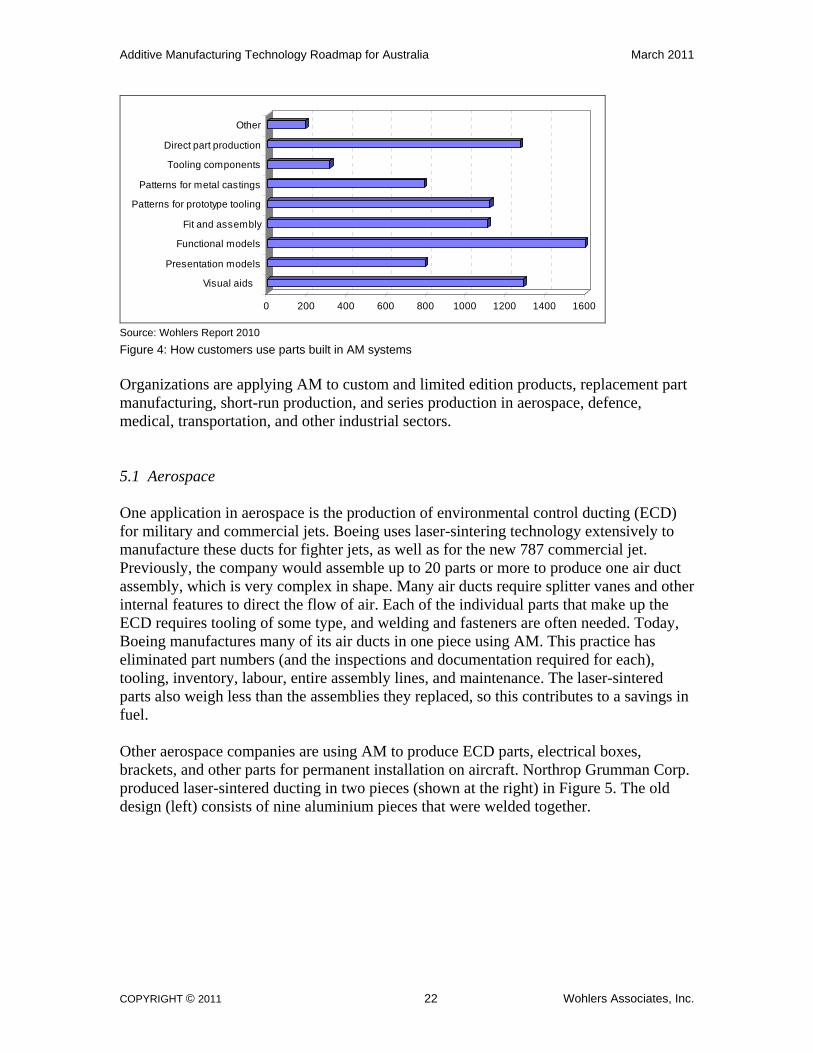

4.3 Increased Functionality AM technology allows designers to create parts that include complex functions and capabilities. An assembly that comprises multiple parts can be fabricated in one build, eliminating fasteners and assembly labour. More importantly, when the parts that go into that assembly are no longer needed, the costs of designing, fabricating, inspecting, documenting, and certifying them are also eliminated. The amount of paperwork and engineering controls required to carry a single part in a design/manufacturing system can be significant and expensive. Other examples of increased functionality include integration of heating or cooling channels in moulds, integration of internal structures, such as internal fluid transport channels, and a reduction in weight. 4.4 Reduced Material and Energy Consumption Another benefit of additive manufacturing is a reduction in the amount of raw material needed to manufacture a part. Conventional machining can be material and energy intensive, with a large amount of the original metal ending up as scrap on the shop floor after hours of machining. It’s not always cost effective to recycle this material, so it becomes waste. “From a full product life cycle assessment point of view, the environmental impact of such waste, added to the energy cost associated with extensive machining, becomes quite significant,” said Dr. Willie du Preez of CSIR. Contrast that with AM technology, which produces net-shape or near-net-shape parts and metal powder systems that produce very little waste. “This is of particular importance when expensive materials, such as titanium alloys, are used for part production,” du Preez said. 5.0 Part Production Applications In a short few years, part production has grown from almost nothing to become one of the most popular applications of AM technology, as shown in Figure 4. This information came from a survey question “How do your customers use the parts built on AM systems?” that was sent to AM system manufacturers and service providers worldwide, including companies in Australia. The length of each bar in the chart reflects the numerical responses received from the survey.

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 22 Wohlers Associates, Inc.

0 200 400 600 800 1000 1200 1400 1600

Visual aids

Presentation models

Functional models

Fit and assembly

Patterns for prototype tooling

Patterns for metal castings

Tooling components

Direct part production

Other

Source: Wohlers Report 2010

Figure 4: How customers use parts built in AM systems

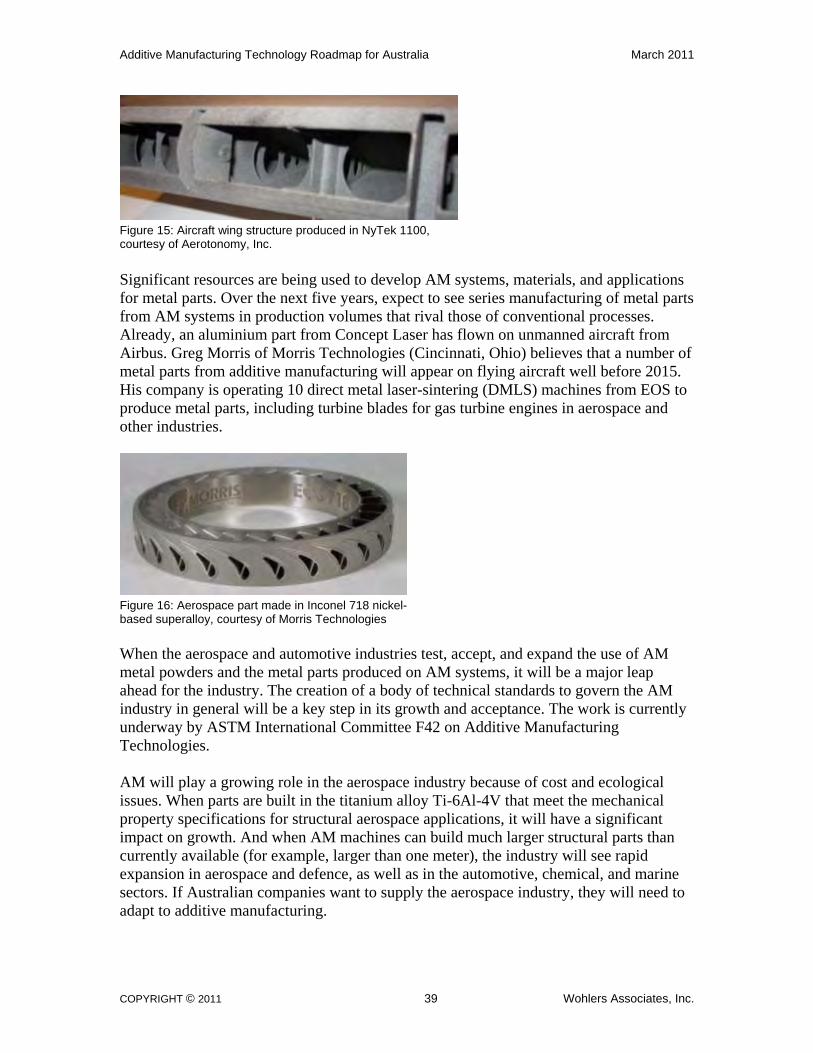

Organizations are applying AM to custom and limited edition products, replacement part manufacturing, short-run production, and series production in aerospace, defence, medical, transportation, and other industrial sectors. 5.1 Aerospace One application in aerospace is the production of environmental control ducting (ECD) for military and commercial jets. Boeing uses laser-sintering technology extensively to manufacture these ducts for fighter jets, as well as for the new 787 commercial jet. Previously, the company would assemble up to 20 parts or more to produce one air duct assembly, which is very complex in shape. Many air ducts require splitter vanes and other internal features to direct the flow of air. Each of the individual parts that make up the ECD requires tooling of some type, and welding and fasteners are often needed. Today, Boeing manufactures many of its air ducts in one piece using AM. This practice has eliminated part numbers (and the inspections and documentation required for each), tooling, inventory, labour, entire assembly lines, and maintenance. The laser-sintered parts also weigh less than the assemblies they replaced, so this contributes to a savings in fuel. Other aerospace companies are using AM to produce ECD parts, electrical boxes, brackets, and other parts for permanent installation on aircraft. Northrop Grumman Corp. produced laser-sintered ducting in two pieces (shown at the right) in Figure 5. The old design (left) consists of nine aluminium pieces that were welded together.

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 23 Wohlers Associates, Inc.

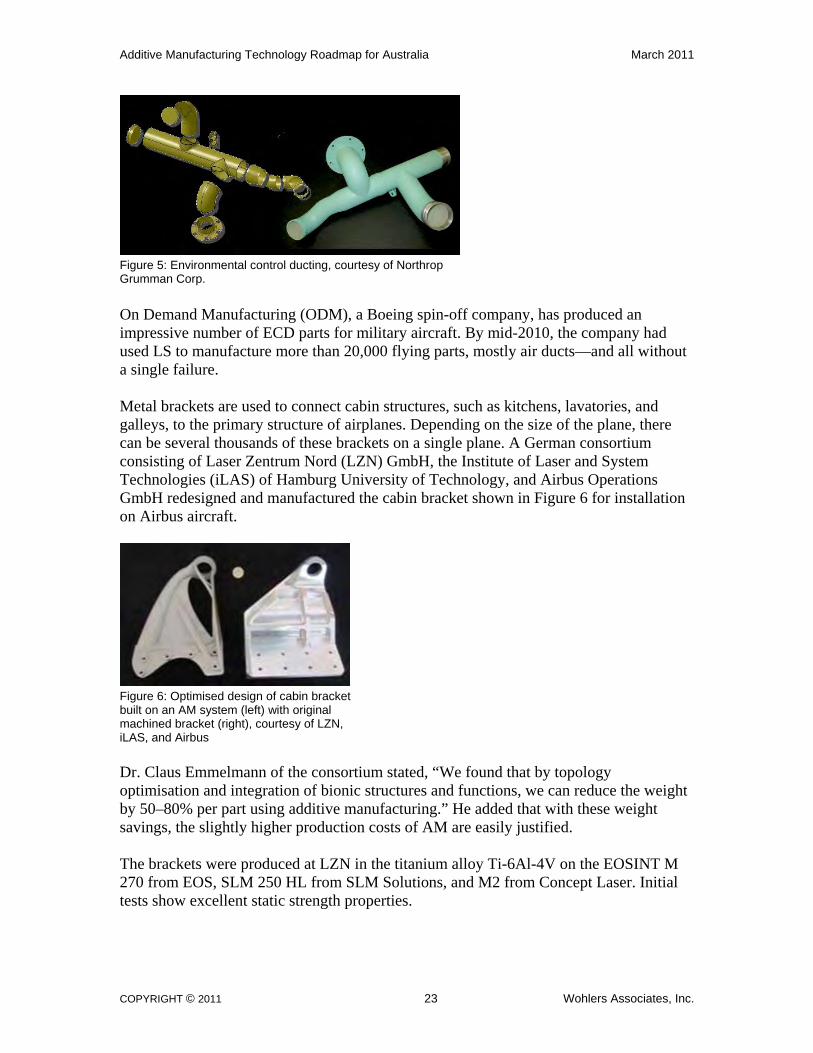

Figure 5: Environmental control ducting, courtesy of Northrop Grumman Corp.

On Demand Manufacturing (ODM), a Boeing spin-off company, has produced an impressive number of ECD parts for military aircraft. By mid-2010, the company had used LS to manufacture more than 20,000 flying parts, mostly air ducts—and all without a single failure. Metal brackets are used to connect cabin structures, such as kitchens, lavatories, and galleys, to the primary structure of airplanes. Depending on the size of the plane, there can be several thousands of these brackets on a single plane. A German consortium consisting of Laser Zentrum Nord (LZN) GmbH, the Institute of Laser and System Technologies (iLAS) of Hamburg University of Technology, and Airbus Operations GmbH redesigned and manufactured the cabin bracket shown in Figure 6 for installation on Airbus aircraft.

Figure 6: Optimised design of cabin bracket built on an AM system (left) with original machined bracket (right), courtesy of LZN, iLAS, and Airbus

Dr. Claus Emmelmann of the consortium stated, “We found that by topology optimisation and integration of bionic structures and functions, we can reduce the weight by 50–80% per part using additive manufacturing.” He added that with these weight savings, the slightly higher production costs of AM are easily justified. The brackets were produced at LZN in the titanium alloy Ti-6Al-4V on the EOSINT M 270 from EOS, SLM 250 HL from SLM Solutions, and M2 from Concept Laser. Initial tests show excellent static strength properties.

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 24 Wohlers Associates, Inc.

5.2 Medicine Additive manufacturing technology and computed tomography (CT) scanning are giving orthopaedic doctors new and exciting surgical capabilities. One example is the repair of severely damaged hip joints. Repairing the ball-and-socket joint of the hip with a titanium implant is a complicated procedure, especially with extensive damage or bone degeneration. Royal Perth Hospital, in collaboration with University of Western Australia, created custom acetabular (hip socket) implants in titanium alloy. First, the patient’s bone structure was captured with CT scanning, which is now relatively inexpensive and widely available. A 3D model of the bone was created, and a custom acetabular cage was designed to fit, according to Robert Day of Royal Perth Hospital. The location and size of the screws that anchor the implant were also optimally designed for the bone structure of the patient. The Ti-6Al-7Nb titanium alloy implant was built on a selective laser melting machine from SLM Solutions GmbH. Post-production heat treatment was required to improve the alloy’s fatigue strength.

Figure 7: Custom acetabular socket fitted to model of patient’s hip, courtesy of Biomedical Engineering, Royal Perth Hospital

Custom acetabular prostheses have several advantages. Foremost is the superior fit and secure fastening. Day explained that the implant acts as a drill guide for screw placement, ensuring that the screws are located correctly. This reduces the risk of damage to nearby organs and blood vessels. Off-the-shelf implants, by their very nature, do not fit perfectly, which increases the chance of additional surgery in the patient’s future. The custom implant also reduces surgery time, since sizing, fitting, and anchoring have been predetermined. Custom implants are not limited to hip replacement surgery. Figures 8 and 9 illustrate how medical scan data and the additive manufacture of a titanium implant were used to repair a patient’s skull. Cranio-maxillofacial surgery is a specialized area of orthopaedics where scanning and AM technologies are being used more frequently.

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 25 Wohlers Associates, Inc.

Figure 8: CAD model of custom titanium implant, courtesy of Dr. Jules Poukens, University Hasselt (Belgium)

Figure 9: The white model of the patient’s skull was produced on an AM system, as was the custom titanium part, which is about to be implanted, courtesy of Dr. Jules Poukens, University Hasselt (Belgium)

Dr. Stephen Rouse of Walter Reed Army Medical Center has been instrumental in the production of many custom cranio-maxillofacial implants. He has used EBM to produce more than 40 of them in Ti-6Al-4V. Meanwhile, the Rapid Manufacturing Group at The University of Western Australia (UWA) is working on two Australian Research Council (ARC) projects on SLM. The university has secured ARC Linkage Infrastructure, Equipment and Facilities (LIEF) funding to purchase the latest generation SLM machine. The first project is a collaborative effort between UWA and a team of mathematicians from The University of Queensland. The aim of the project, according to Dr. Tim Sercombe of UWA, is to design and manufacture new-generation bone implants that could potentially reduce

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 26 Wohlers Associates, Inc.

surgery and rehabilitation times. Also, the project hopes to provide a solution for patients for whom current orthopaedic implants are not suitable, Sercombe explained. The project uses a mathematical approach called “topology optimization,” a method that optimizes the layout of a material within a particular design space. The team has developed a prototype of a 3D scaffold that closely matches the modulus of human bone, while maintaining the necessary pore structure. This ensures transport of essential nutrients through the implant. These complex structures are manufactured from a new generation of low modulus, biocompatible beta titanium alloy using SLM. The use of low modulus titanium alloys facilitates the production of a scaffold with stiffness that matches bone, while retaining a relatively low level of in-built porosity, which maximises strength. The second project is aimed at developing an aluminium alloy specifically for the SLM process. The composition of the alloy is being judiciously designed with consideration to break up of the oxide layer, optimizing the properties of the molten track, and enhancing absorption of the incident laser energy. Unlike most work in the field, this project will not be constrained by conventional alloys. Instead, the alloy will be designed specifically for selective laser melting. 5.3 New Businesses and Business Models New types of products are becoming available because companies and individuals are able to introduce them so easily. Also, new types of businesses are emerging for this and other reasons. An example is Freedom of Creation (FOC,Netherlands), which offers a wide range of consumer products. FOC started with impressive, high-end lighting designs and continues to design and commercialize them today. These and other products, mostly furniture and home and office accessories, are manufactured entirely using additive manufacturing. Most of the products could not be manufactured any other way because of their extreme complexity. This company would not be in business, at least not in its current form, without additive manufacturing. Materialise .MGX (Belgium) is another company that is offering an impressive collection of lights, furniture, and accessories—all by additive manufacturing. It operates machines in-house, whereas FOC outsources all of its production.

Figure 10: Collapsible chair built by laser sintering, courtesy of the .MGX division of Materialise

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 27 Wohlers Associates, Inc.

Shapeways is another company that has emerged as a result of additive manufacturing technology. This relatively young company was a part of an incubator programme at consumer products giant Philips Electronics (Netherlands). The web-based company was launched in 2008 and today offers an estimated 150,000 products—all on-demand by additive manufacturing. It is selling 2,500–3,000 of its AM-produced products each week, according to Peter Weijmarshausen, CEO of the company. Nearly all of them are custom or limited edition products. Product pricing varies widely, but many are only A$10–50 and some are available in metal, such as the examples in Figure 11.

Figure 11: BMW gearshift handle with custom metal insert priced at US$40, courtesy of Shapeways

The company allows anyone to set up a “Shapeways Shop” to sell designs such as jewellery, sculptures, puzzles, and a wide range of other products. Shapeways handles the marketing, sales, transaction, manufacturing (which is outsourced to companies in Europe and the U.S.), and shipping. More than 1,200 Shapeways Shops have been established. Many of the products available at Shapeways would be difficult, very expensive, or impossible to manufacture using conventional methods. For these reasons, a new range of products is becoming available for the first time. Online tools at shapeways.com are available to customers that allow them to create custom products from more than 650 designs. In September 2010, Shapeways received US$5 million in venture capital. In December 2010, the company moved its headquarters from Eindhoven, Netherlands to New York, USA. As of January 2011, the company had 16 employees in Eindhoven and nine in New York. FigurePrints is also targeting the consumer with its products. The company, headed by former Microsoft vice president Ed Fries, manufactures custom characters from the wildly popular World of Warcraft video game. Within 10 months of announcing the manufacturing service in late 2007, FigurePrints was producing more than 1,500 custom products monthly at US$130 (plus shipping) for U.S. customers and €130 (plus shipping) for European customers. The elaborate characters are manufactured on 3D colour printers from Z Corp.

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 28 Wohlers Associates, Inc.

Figure 12: Manufactured characters from World of Warcraft game data, courtesy of FigurePrints

5.4 Production Volumes Suitable for AM Production numbers can range from one to thousands. The size of the part, especially the build height, influences the build speed and cost more than anything else. Loughborough University (England) conducted a study to determine the breakeven point of producing plastic parts by AM versus injection moulding. It found that the breakeven point of a part measuring 77 x 48 x 32 mm is at around 7,700 pieces when using laser sintering. In other words, if the quantity is below 7,700 units of this part, it would be less expensive to use laser sintering. If it is above this number, injection moulding is less expensive. Many other factors besides cost enter into the decision process, including the physical properties of the part, surface finish, dimensional accuracy, design flexibility, and delivery. When manufacturing a part measuring 140 x 190 x 155 mm, the breakeven point drops to about 180 pieces. These numbers can change dramatically from process to process. AM systems are becoming faster at building parts, so the numbers should improve in favour of additive manufacturing in the future. Tom Mueller of Express Pattern said that part complexity can have a significant effect on the breakeven point. He defines part complexity as the presence of features that increase the difficulty of manufacture, which includes undercuts, thin walls, disparate wall thickness, a very smooth surface finish, and tight tolerances. If there are part features that require a complex mould (e.g., slides or pulls), the breakeven point improves in favour of AM because of the additional tooling cost. However, Mueller pointed out that there may not be a choice in some cases because accuracy, surface finish, or volume requirements rule out additive manufacturing as an option. 6.0 Environmental Concerns Aerospace, transportation, and other industries in Australia and around the world continue to face issues associated with materials, weight, transportation cost, and each product’s carbon footprint on the environment. It is believed that additive manufacturing, especially metal-based systems, can dramatically reduce the amount of material used in

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 29 Wohlers Associates, Inc.

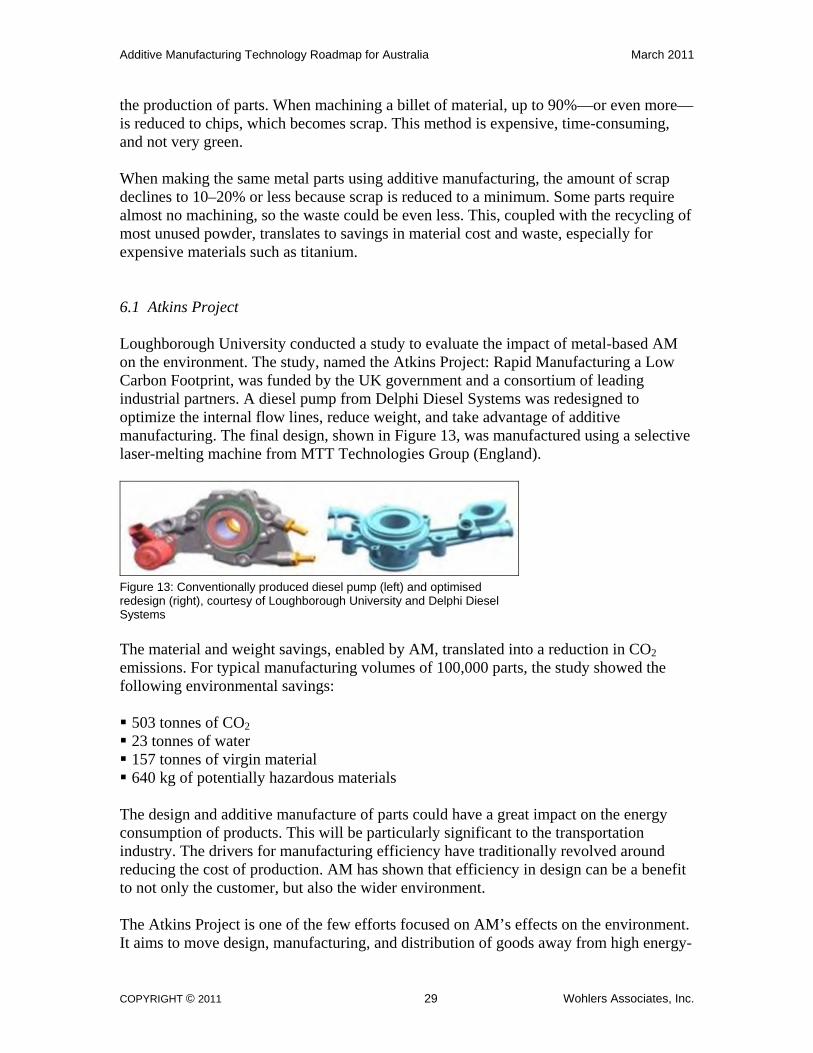

the production of parts. When machining a billet of material, up to 90%—or even more— is reduced to chips, which becomes scrap. This method is expensive, time-consuming, and not very green. When making the same metal parts using additive manufacturing, the amount of scrap declines to 10–20% or less because scrap is reduced to a minimum. Some parts require almost no machining, so the waste could be even less. This, coupled with the recycling of most unused powder, translates to savings in material cost and waste, especially for expensive materials such as titanium. 6.1 Atkins Project Loughborough University conducted a study to evaluate the impact of metal-based AM on the environment. The study, named the Atkins Project: Rapid Manufacturing a Low Carbon Footprint, was funded by the UK government and a consortium of leading industrial partners. A diesel pump from Delphi Diesel Systems was redesigned to optimize the internal flow lines, reduce weight, and take advantage of additive manufacturing. The final design, shown in Figure 13, was manufactured using a selective laser-melting machine from MTT Technologies Group (England).

Figure 13: Conventionally produced diesel pump (left) and optimised redesign (right), courtesy of Loughborough University and Delphi Diesel Systems

The material and weight savings, enabled by AM, translated into a reduction in CO2 emissions. For typical manufacturing volumes of 100,000 parts, the study showed the following environmental savings: 503 tonnes of CO2 23 tonnes of water 157 tonnes of virgin material 640 kg of potentially hazardous materials The design and additive manufacture of parts could have a great impact on the energy consumption of products. This will be particularly significant to the transportation industry. The drivers for manufacturing efficiency have traditionally revolved around reducing the cost of production. AM has shown that efficiency in design can be a benefit to not only the customer, but also the wider environment. The Atkins Project is one of the few efforts focused on AM’s effects on the environment. It aims to move design, manufacturing, and distribution of goods away from high energy-

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 30 Wohlers Associates, Inc.

intensive methods to more sustainable methods. Additive manufacturing could support this goal by reducing raw material consumption and waste, compared to machining from solid stock. Also, it could reduce the size of the supply chain through digital supply chains and distributed services, minimizing transportation costs and waste material disposal or recycling. Australia is a country focused on the environment. Government programmes, such as those delivered through AusIndustry, are helping small and medium-sized Australian manufacturers through grants of A$10,000 to A$500,000. This programme, titled Re-tooling for Climate Change, was aimed at reducing the carbon footprint among manufacturing companies by improving energy and/or water efficiency of their production processes. 6.2 Lightweight Structures Additive manufacturing makes it possible to create lightweight but strong parts using an internal lattice-style build structure. A wide range of configurations has been tried, and some engineered to optimize the ratio of strength to weight. Parts that would otherwise be solid and heavy are semi-hollow with internal structural members that make the parts incredibly light, but impressively strong.

Figure 14: Metal structures (left and right), courtesy of Arcam and netfabb, respectively, and plastic laser-sintered parts (middle), courtesy of the Katholieke Universiteit Leuven

In addition to the reduction of weight, building parts in this way come with other important benefits. One is the reduction of material, which reduces cost. Another is build speed because less material is processed. Yet another benefit is the design of special properties and functions into parts; something that is difficult or impossible to achieve with conventional methods of manufacturing. For example, one could make one region of a part rigid and another region soft or flexible. 7.0 Production of Metal Parts Impressive machines and materials for additive manufacturing have become available over the past 10 years for the production of metal parts. The technology is being used to help develop products in aerospace, medical, dental, and other industries. A growing number of the machines and materials are being targeted for end-use production applications, especially in the medical and dental industries.

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 31 Wohlers Associates, Inc.

The development of plastic parts from additive manufacturing had a head start of about 10 years, yet metal parts from AM are exhibiting excellent mechanical properties. In fact, the progress in metals is as good as or better than that of plastics. The metals are processed differently than the plastics and this largely accounts for the difference. As mentioned previously, fully dense thermoplastic parts made by additive manufacturing can be difficult to achieve, and usually have some porosity. Building fully dense metal parts can also be difficult, yet many users have reported success in producing full density, or near full density, metal parts. This positive result has come at a much earlier phase in the development of metal AM parts than it did in the development of thermoplastic AM parts. Put another way, if one compares the properties of metal AM parts to the properties of parts produced with traditional manufacturing, then compares the properties of thermoplastic AM parts to those produced by traditional manufacturing, the gap is smaller for metals. 7.1 Powder-Bed Systems AM systems that produce metals parts can be divided into three broad groups. The first group includes systems that use a laser or electron beam to heat powder to melt and form parts. An estimated cumulative total of 552 of these systems were installed worldwide at the beginning of 2010. All of the systems in this group produce parts in a powder bed, meaning that the parts being fabricated are entirely inside the powder when the build process is complete. These systems have become the most popular, by far, and four were in operation in Australia as of October 2010. These systems can process a range of materials including stainless steel, tool steel, aluminium, Inconel, gold alloys, cobalt–chrome, titanium, and titanium alloys, including Ti-6Al-4V. Over the past couple of years, the most popular metals for additive manufacturing have been stainless steel, titanium, titanium alloys, and cobalt–chrome for medical, dental, and aerospace applications. One of the strengths of the laser-based systems is the fine feature detail that can be achieved. Also, these systems are capable of producing a surface finish that is as good as or better than a sand-cast finish. With shot-peening or bead-blasting, the surface quality is impressive, although not as good as a machined part. Mating surfaces and features that require high dimensional accuracy may require post-processing such as CNC machining or grinding. AM systems that use an electron beam to melt powder metal are somewhat more expensive than laser-based systems, but are many times faster. The surface finish and feature detail of electron beam systems have improved significantly in recent years, but they are not as good as what can be achieved with laser systems. Parts built on electron beam systems typically have superior mechanical properties. Also, the build process

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 32 Wohlers Associates, Inc.

produces less residual stress in the part, so distortion is lower. Arcam is the primary manufacturer of electron beam melting systems. With EBM systems, the need for anchors is not a significant problem according to users of the process. Even so, reducing or eliminating them would improve the quality of down-facing surfaces. EBM parts that require anchors often use them as a heat sink down to the build plate. Orthopaedic implant manufacturers are embracing the use of EBM systems from Arcam. In the second half of 2007, Ala Ortho (Italy) launched its first range of orthopaedic implant products using the Arcam process. The implants are being produced in Ti-6Al-4V titanium alloy. Ala Ortho and other manufacturers of orthopaedic products have used EBM to produce an estimated 30,000 metal hip implants (acetabular cups). As of December 2010, about 15,000 of them had been implanted into patients. 7.2 Powder and Wire Deposition Systems The second group of metal-based AM systems consists of those that combine a laser heat source with a powder deposition head to deposit the metal powder. Most use a 4- or 5-axis motion system to position the head, and some even employ a robot to deliver this motion. Unlike the powder-bed systems, these machines can be used for the repair of existing parts and tooling. However, they are generally more expensive, more complex to program, and require an operator skilled in CNC machining. Their acceptance in industry has been limited, with a relatively high percentage of the systems sold going into academic and research facilities. Optomec Inc. (Albuquerque, New Mexico) was first to offer a commercially available system of this type. The company’s laser-engineered, net-shaping (LENS) process injects metal powder into a pool of molten metal created by a focused laser beam. The LENS system supports many types of metals including 316 and 304 stainless steels; nickel-based superalloys such as Inconel 625, 690, and 718; H13 tool steel; cobalt–chrome; and Ti-6Al-4V titanium alloy. The LENS method is said to produce fully dense metal and creates near-net-shape parts or repaired surfaces that require finish machining or some other type of finishing. According to Optomec, the LENS system is capable of producing parts with material properties that exceed traditional processes, due to its unique material-processing environment that improves the material microstructure. LENS-deposited 316 stainless steel, for instance, typically has a cellular spacing of a few microns. This leads to yield strengths that are nearly twice that of conventionally processed 316 stainless steel, according to Optomec. POM (Auburn Hills, Michigan) offers a process called direct metal deposition (DMD). The process uses a laser and powder feed system to deposit thin layers of metallic coatings and creates parts using powdered metal and laser-cladding techniques. DMD is

Additive Manufacturing Technology Roadmap for Australia March 2011

COPYRIGHT © 2011 33 Wohlers Associates, Inc.