automobile sector

DESCRIPTION

analysing the sector with reference to tata motorsTRANSCRIPT

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 1/33

Automobile

sector(India)Done by

Priya Upadhyay

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 2/33

• Mainly engaged in manufacturing motorvehicles or motor vehicle engines.

• Primary activities are:

o Motor cars manufacturing

o Motor vehicle engine manufacturing

• Major products and services:

o Passenger motor vehicles

o Commercial vehicles

o

Two wheelers & three wheelers

Introduction to automobile sector

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 3/33

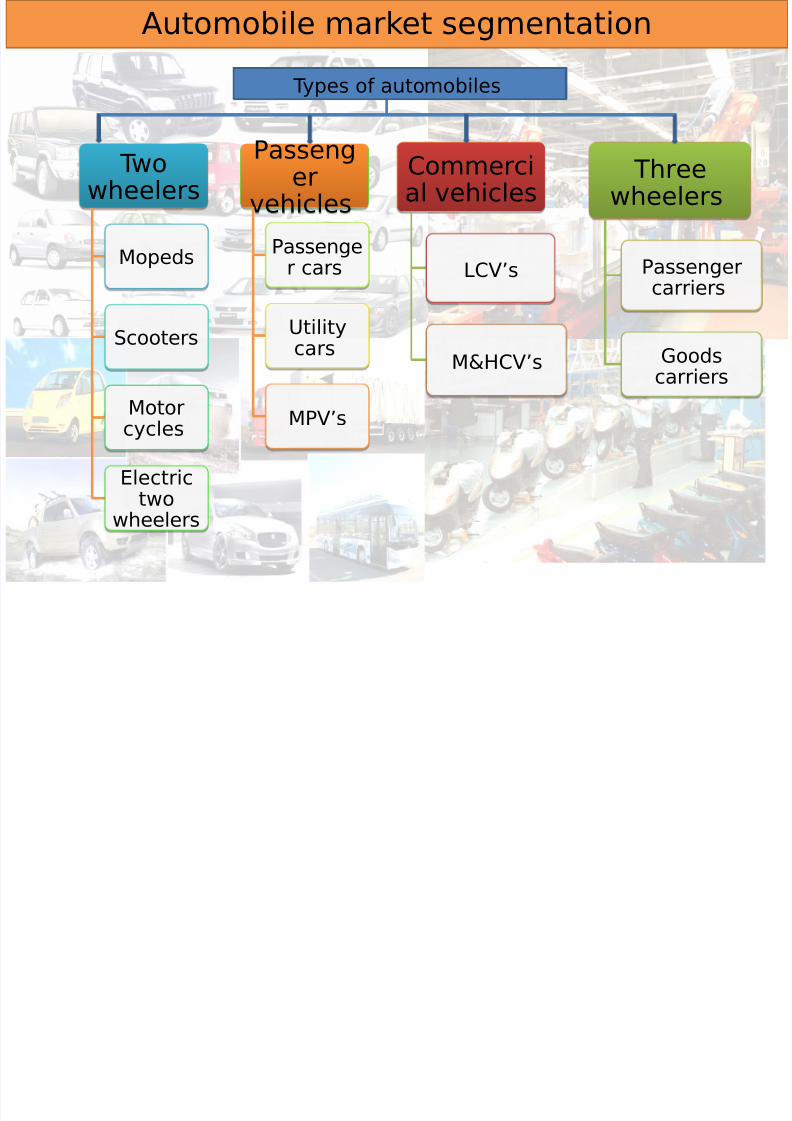

Automobile market segmentation

Twowheelers

Mopeds

Scooters

Motorcycles

Electrictwo

wheelers

Passenger

vehicles

Passenge

r cars

Utilitycars

MPVs

!ommercial vehicles

"!Vs

M#$!Vs

Threewheelers

Passengercarriers

%oodscarriers

Types o& automobiles

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 4/33

!ontributes about ' per cent in(ndias %DP

) percent in (ndia*s industrialproduction

%enerated about +,) lakh o& directemployment

About - crore o& indirect employment

Establishment o& competitive auto

ancillary industry. automobile testingand /#D centers

Introduction continued…Source:- SIAM

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 5/33

Automotive

ecosystem

u o n us ry s con r u onto the economy

Generategovernmentrevenue

Create

economicdevelopment

Encouragepeople

development

R&D and innovation

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 6/33

• Manufacturing over 11 million vehicles

and exporting about 1.5 million every

year

• 91% of the vehicles sold by

households, 9% for commercial

purposes

• Two wheelers with a maret share of

!".#9%, passenger cars with 15.9"5,

About the industry

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 7/33

Position o& automobile industry in (ndia0th largestautomobile

industry

1nd largesttwo wheeler

market

--th largestpassenger

cars

producers

+th largest in

heavy trucks

1nd largest

tractormanu&acturer

Annualproduction o&

over 1,2

million units

Monthly

sales o&passenger

cars in (ndiae3ceeds-44.444

units,

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 8/33

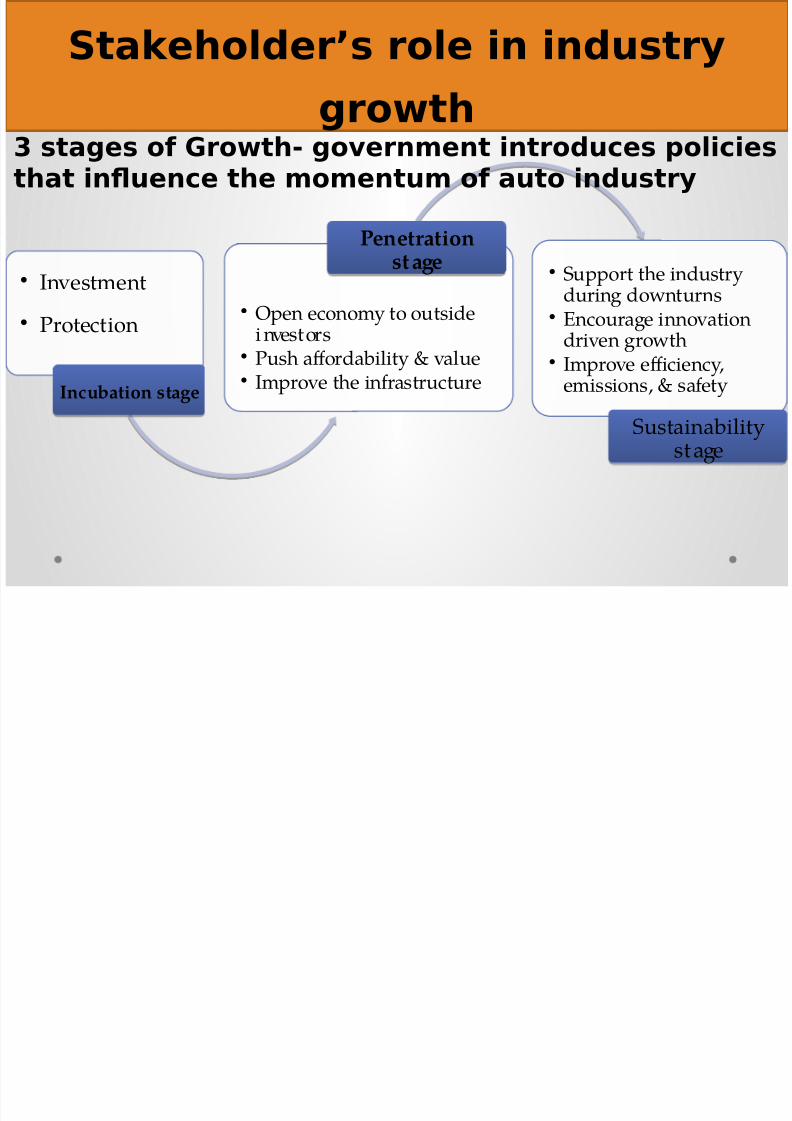

• Investment

• Protection

Incubation stage

• Open economy to outsideinvestors

• Push affordability & value• Improve the infrastructure

Penetrationstage

•Support the industryduring downturns

• Encourage innovationdriven growth

• Improve efficiency,emissions, & safety

Sustainabilitystage

Staeholder’s role in industry

gro!th" stages of #ro!th$ government introduces policiesthat in%uence the momentum of auto industry

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 9/33

&uele'ciency

(missionreduction

Safety )durability

*oste+ectivene

ss

Innovative

features

&o

cu

sArea

s

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 10/33

Key drivers for growth

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 11/33

Market dominance in each category

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 12/33

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 13/33

Automotive companies in (ndia

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 14/33

• &ero &onda and 'a(a( )uto are dominant players in

the two*wheelers space.

• Maruti +uui, Tata Motors, Mahindra $ Mahindra,

)sho -eyland rule the four wheelers space.

• )n original euipment manufacturer, or /0M,

manufactures products or components which are purchased by a second company and retailed under

the second companys brand name.

• Tata Motors, Mahindra $ Mahindra are famous/0M across the world.

n order to mae ndia a power to recon with in

the automotive sector, the government launched the

)utomotive Mission 2lan 3)M24 66"*61".

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 15/33

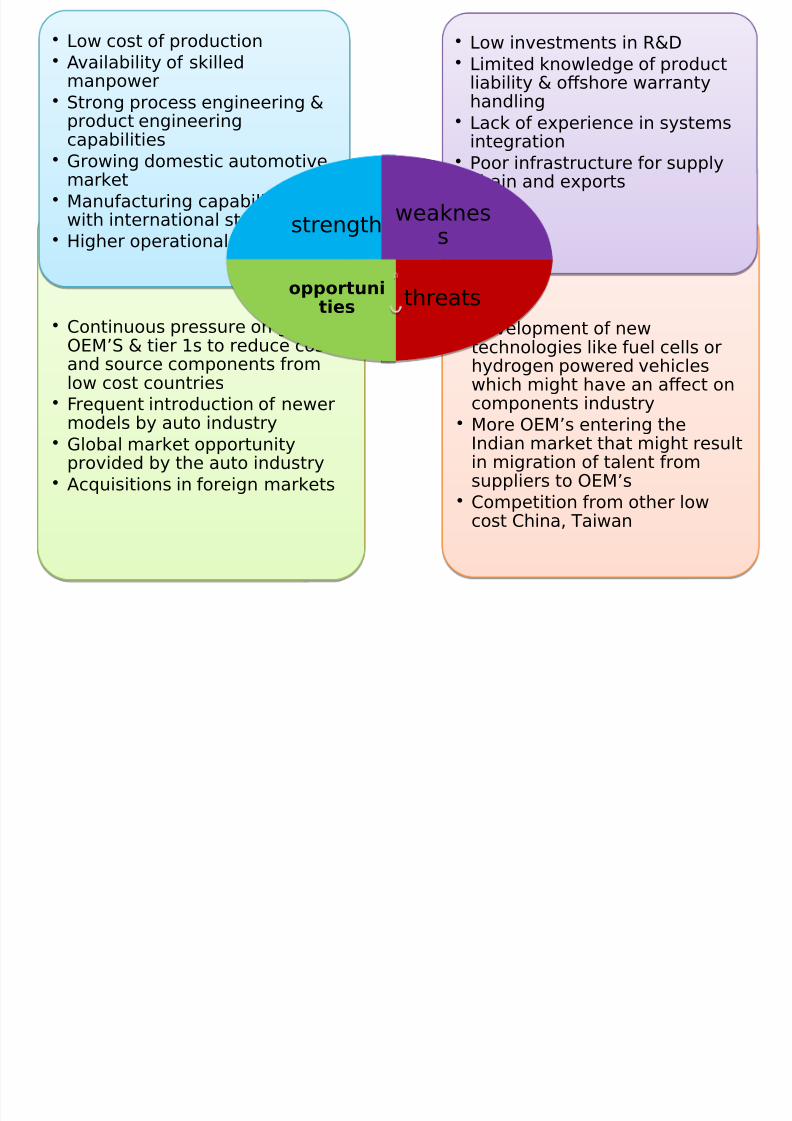

• Development o& newtechnologies like &uel cells orhydrogen powered vehicleswhich might have an a5ect oncomponents industry

• More 6EMs entering the(ndian market that might resultin migration o& talent &romsuppliers to 6EMs

• !ompetition &rom other lowcost !hina. Taiwan

• !ontinuous pressure on global6EMS # tier -s to reduce costand source components &romlow cost countries

• 7re8uent introduction o& newermodels by auto industry

• %lobal market opportunityprovided by the auto industry

• Ac8uisitions in &oreign markets

• "ow investments in /#D• "imited knowledge o& product

liability # o5shore warrantyhandling

• "ack o& e3perience in systems

integration• Poor in&rastructure &or supply

chain and e3ports

• "ow cost o& production• Availability o& skilled

manpower• Strong process engineering #

product engineering

capabilities• %rowing domestic automotive

market• Manu&acturing capabilities

with international standards• $igher operational e9ciency

strengthweaknes

s

threatsopportuni

ties

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 16/33

UTURE

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 17/33

Third largestautomobile

industry by 1414E

:orlds secondlargest two

wheelermanu&acturer

Passenger vehiclesales to nearlytriple by 1414E

Passenger vehicleto increase &rom

2,1 million in7;14-2 to 0,4

million in 7;1414E

Two wheeler sales

to rise &rom -),0million in 7;14-2to 10,- million by

7;1414E

<y 1414. (ndiasshare in the globalpassenger vehiclemarket to double

to => &rom +>over 14-4?--

14-4 1414+,44> =,44>

(ndia*s share in global

passenger vehicle market

7;-2 7;14-),04 10,-4

T:6 :$EE"E/S@M(""(6U(TSB

!A%/0>

7;-2 7;142,14 0,44

passenger vehicles @millionunitsB

!A%/-C>

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 18/33

The market isbubbling with

activity and the rateo& new launches can

be averaged toalmost -,)?1 newmodels a week

(ndia is one o& themost pricecompetitive

markets globally

The need &orsa&er and cleaner

vehicles is theneed o& the hour

Managing gro!th

dynamics

fh ld f bl

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 19/33

One of the main leading company of automobile

industry in India

Tata motors

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 20/33

*,-,/(

accountability.customer #

product &ocus.e3cellence.

speed

0 I SI 1 2 most ad mi r e d by c ust ome r s. e mpl oy e e s. busi ne ss par t ne r s # shar e hol d e r s & o

r t he e 3 pe r i e nc e # v al ue t he y e n D oy

Mission 0ision )*ulture

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 21/33

(t is a leader in!ommercial

Vehicles in eachsegment. andamong the top

players inPassenger

Vehicles withwinning products

in the compact.midsie car andutility vehiclesegments,

Presence across-') countries.

Tata cars. busesand trucks aremarketed in

several countriesin Europe. A&rica.the Middle East.

South Asia. South

East Asia. SouthAmerica. !(S and

/ussia,

The !ompanysmanu&acturingbase in (ndia is

spread across Famshedpur@FharkhandB. Pune

@MaharashtraB."ucknow @Uttar

PradeshB.Pantnagar

@UttarakhandB.Sanand @%uaratB

and Dharwad@GarnatakaB,

Throughsubsidiaries and

associatecompanies. Tata

Motors hasoperations in theUG. South Gorea. Thailand. South

A&rica and

(ndonesia, Amongthem is Faguar"and /over.

ac8uired in 144=,

Tata motors at a glance

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 22/33

The business segments are :-

(i) automotive operations (ii) all other operations

Revenue (INR crore)

2014 2013*oreoperations 12-C4-,=

-='C12,0-

1theroperations 1)-=,00 11C),01

Source:- Annual Report 2013-14

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 23/33

HORIZONEXT

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 24/33

Key Performance Indicators (2013-14)3345666 crores

Market !apitaliation

@as on March 2-.14-+B

345478 crores

!onsolidated ProHt<e&ore Ta3

75799

Sales and servicetouch

points. globally

37.3

E<(TDA Margin

;""577; crores Total /evenue

Source:- Annual Report 2013-14

M i & t 5 ti

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 25/33

Macro?economic &actors a5ectingTata MotorsI

India’s #<P gro!th continues to remain !ea5 at =.6 in &> ;93"$3=?advance estimates@ after gro!ing at =. in &> ;93;$3".

Mining output registered a negative of 3.3B manufacturingoutput registered a negative of 9.6 during the same period.

&> ;93"$3= !itnessed a decline in investments in ne! projectsin line !ith slo!do!n in overall gro!th.

&> ;93"$3= !as mared by the challenge to the #overnment tocontain the Cscal deCcit5 and the #overnment eDpenditure on

infrastructure and other ey sectors su+ered.Across the Mediterranean the pattern !as more disappointing5!ith Italy5 Spain5 Portugal and #reece all enduring a year of risingunemployment

<ue to announcement by the ,S federal reserve of reducing itsmonthly asset purchases ?so$called EtaperingF@5 caused currencies to

depreciate and borro!ing costs to rise. *ountries !ith large currentaccount and Cscal deCcits !ere !orst a+ected.

SourceI? Annual /eport 14-2?-+

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 26/33

Mar *-+ Mar *-2 Mar *-1 Mar *-- Mar *-44

)4.444

-44.444

-)4.444

144.444

1)4.444

121.=2+ -==.=-= -C).C)+ -11.-1= 0-.'44

2et Sales

Mar *-+ Mar *-2 Mar *-1 Mar *-- Mar *-44

).444

-4.444

-).444

14.444

1).444

24.444

2).444

+4.444

"=5743

;=567;;53=3

365=64

395"63

-=.=C0

-2.C22 -2.)2+

-4.+2'

2.)C=

-+.-4+

0.=C1

-2.)'+ 0.11- 1.)-'

(GI<A5 PG5 PA

E<(TDA

P<T

PAT

Mar *-+ Mar *-2 Mar *-1 Mar *-- Mar *-44

).444

-4.444

-).444

14.444

1).444

24.444

2).444

+4.444

2+.=2=

1+.)+'11.2--

-C.=-'

C.=-C

1perating ProCt

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 27/33

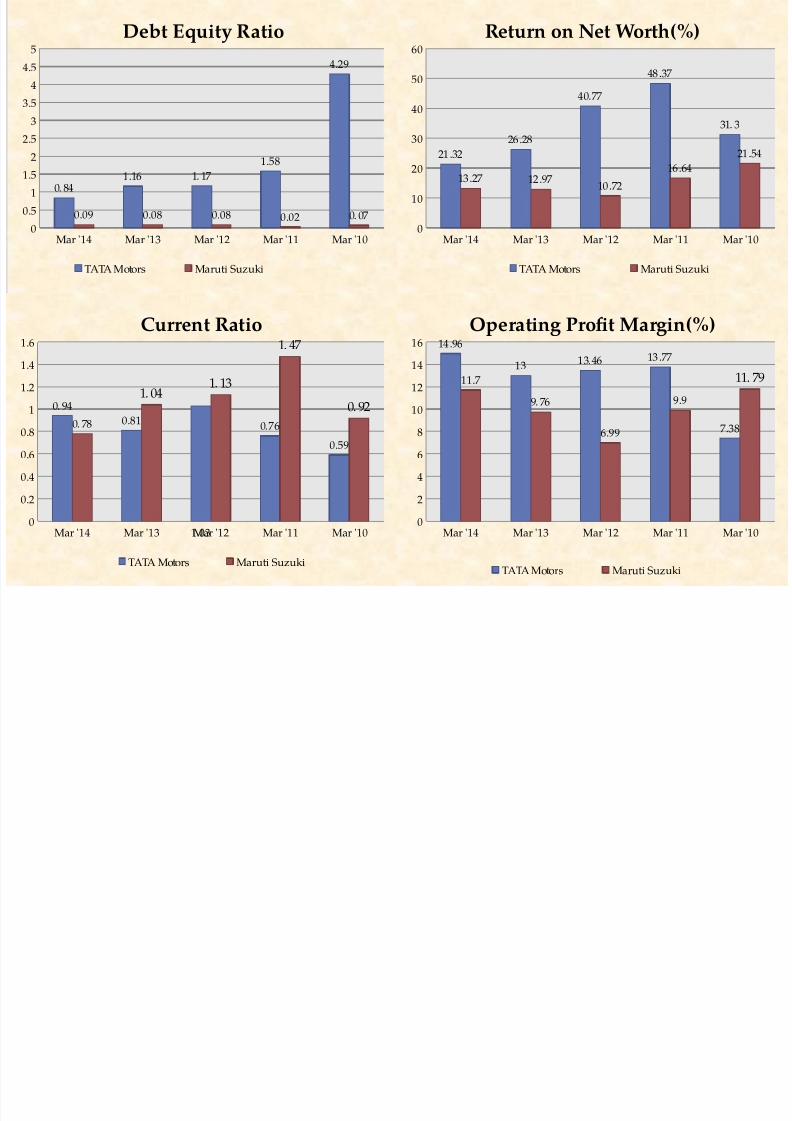

Mar '14 Mar '13 Mar '12 Mar '11 Mar '100

0.5

1

1.5

22.5

3

3.5

4

4.5

5

0.841.16 1.17

1.58

4.29

0.09 0.08 0.08 0.02 0.07

Debt Equity Ratio

TATA Motors Maruti Suzuki

Mar '14 Mar '13 Mar '12 Mar '11 Mar '100

0.2

0.4

0.6

0.81

1.2

1.4

1.6

0.94

0.81

1.03

0.76

0.59

0.78

1.041.13

1.47

0.92

Current Ratio

TATA Motors Maruti Suzuki

Mar '14 Mar '13 Mar '12 Mar '11 Mar '100

10

20

30

40

50

60

21.3226.28

40.77

48.37

31.3

13.27 12.9710.72

16.64

21.54

Return on Net Worth(%)

TATA Motors Maruti Suzuki

Mar '14 Mar '13 Mar '12 Mar '11 Mar '100

2

4

6

810

12

14

16 14.96

13 13.46 13.77

7.38

11.7

9.76

6.99

9.9

11.79

Operating Profit Margin(%)

TATA Motors Maruti Suzuki

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 28/33

Mar '14 Mar '13 Mar '12 Mar '11 Mar '100

0.5

1

1.5

2

2.5

3

3.5

2.44 2.512.34

2.06

1.721.96

2.242.44

3.13

2.78

Fixed Assets Turnover Ratio

TATA Motors Maruti Suzuki

Mar '14 Mar '13 Mar '12 Mar '11 Mar '100

2

4

6

8

5.19 5.015.82

5.28

1.91

Interest Coverage ratio

P)- summary

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 29/33

P)- summary?in crores@ &orecast

Sales *A#/38.= ;939 ;93" ;93= ;93

Sales0C.4'1,C

= -=0.C4=,1=1.22.CC

1,1);5685398.7

4,0' 4,12 9.38

*ost of goodsold

)+.-4),)+ --2.=)-,2+

-.2).))4,4+

;5375449.97

*ost of goodsoldJsales 4,C4 4,)= 9.79

S#)A )=.)+0,2C'+.)40,

+C87547;

."9S#)AJsales 4,2- 4,21 9."9

InteresteDpense 2.)C4,1)

+.'22,'=

=54;4.=7

4,41 4,41 9.9;

PG -2.C+',22-=.=C=,

0'65=93

.9=+.'C+,' 3=5"9

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 30/33

Highlights• The demand for *ommercial vehicles

remained depressed throughout the year, 7or7; 14-2?-+ the !ommercial vehicle industryvolumes at C0=.04' reKect a decline o& 11,+>over 7; 14-1?-2,

• The Medium and Keavy *ommercial0ehicles ?M)K*0@ segment recorded a&urther negative o& 1),1> on the back o&

12,2> decline in the last Hscal,• The ban on mining5 %eet underutiliLation5

fall in resale value and low economicactivities contributed to the &all,

• 6ver the last &ew months. the decline has

• M- <istribution *ompany -td ?<*-@ acts as a dedicated

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 31/33

M- <istribution *ompany -td ?<*-@. acts as a dedicateddistribution and logistics management company to support thesales and distribution operations o& vehicles in (ndia, TD!" helpsus improve planning. inventory management. transportmanagement

• The Tata Motors %roup fund its short$term !oring capitalreuirements with cash generated &rom operations. overdra&t&acilities with banks. short and medium term borrowings &rom

lending institutions. banks and commercial paper, The maturitieso& these short and medium term borrowings and debentures aregenerally matched to particular cash Kow re8uirements

• The %overnment o& (ndia had proposed a comprehensive

national goods and services taD5 or #S. regime that willcombine ta3es and levies by the central and state %overnmentsinto one uniHed rate structure, :hile both the %overnment o&(ndia and other state %overnments o& (ndia have publiclyannounced that all committed incentives will be protected

&ollowing the implementation o& the %ST

• The bus segment also witnessed reversal in market share

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 32/33

The bus segment also witnessed reversal in market sharethrough intensive sales e5orts coupled with launch o& buseswith mechanical 7uel (nection Pump @7(PB. introduction o&Starbus Ultra in Stage carriage. marketing initiatives such as

**$umare <us Gi <aat $ain** and **Dream it to win it**program

• The !arranty for M)K*0 buses and trucs wereincreased to three years and &our years respectively.symboliLing improvement in uality, The Tata Alert**service. to return a vehicle back on road within += hours.has been e3panded across all national highways,

• Safety and Kealth (nvironment ?SK(@ !ouncils havebeen &ormed &or both !ommercia Vehicle business andPassenger Vehicle business, The !ompany has come up withSa&ety Manual &or 7ully <uilt Vehicle @7<VB ApplicationVendors, The -ost ime Injury ®uency /ate ?-I&/@&or this year is 4,20>. a reduction o& ++> over 7; 14-1?-2,

7/17/2019 automobile sector

http://slidepdf.com/reader/full/automobile-sector-5691276b91166 33/33

han you