automotive china production outlook - cdn.ihs.comcdn.ihs.com/www/pdf/20170228-eng-tao.pdf · china...

TRANSCRIPT

© 2017 IHS Markit© 2017 IHS Markit. All Rights Reserved.

China Production OutlookNew normal: The slowdown and stimulus in China

AUTOMOTIVE

Gao Tao, Manager, Great China Light Vehicle Production, 0086-21-2422 9116, [email protected]

28 February 2017 | Tokyo, Japan

Contents

© 2017 IHS Markit

Agenda 3

Regional economic outlook 4

GDP development Disposable income Exchange rate Urbanization Demographic structure

Fluctuation in 2015–18 10

Inventory pressure Turbulence in financial market Engine displacement development

Long-term development 15

Entering adjustment phase NEV development OEM growth distribution Module platform Brand expansion & Multi-brand Domestic capacity expansion COEM R&D development Sharing economy COEM milestone of autonomy

China Production Outlook / February 2016

2

© 2017 IHS Markit 3

Economic outlook

Presentation Name / Month 2016

© 2017 IHS Markit 4

China’s long-term GDPGDP growth decelerates smoothly in coming decadesChina GDP growth

0

2

4

6

8

10

12

14

16

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

Gro

wth

rate

(%)

World GDP2016: 2.5%2017: 2.8%2018: 3.1%

China GDP growth2016: 6.7%2017: 6.4%2018: 6.2%2019: 6.1%6.0

4.0

2017 Spring Automotive Conference | 8 March 2017

© 2017 IHS Markit 5

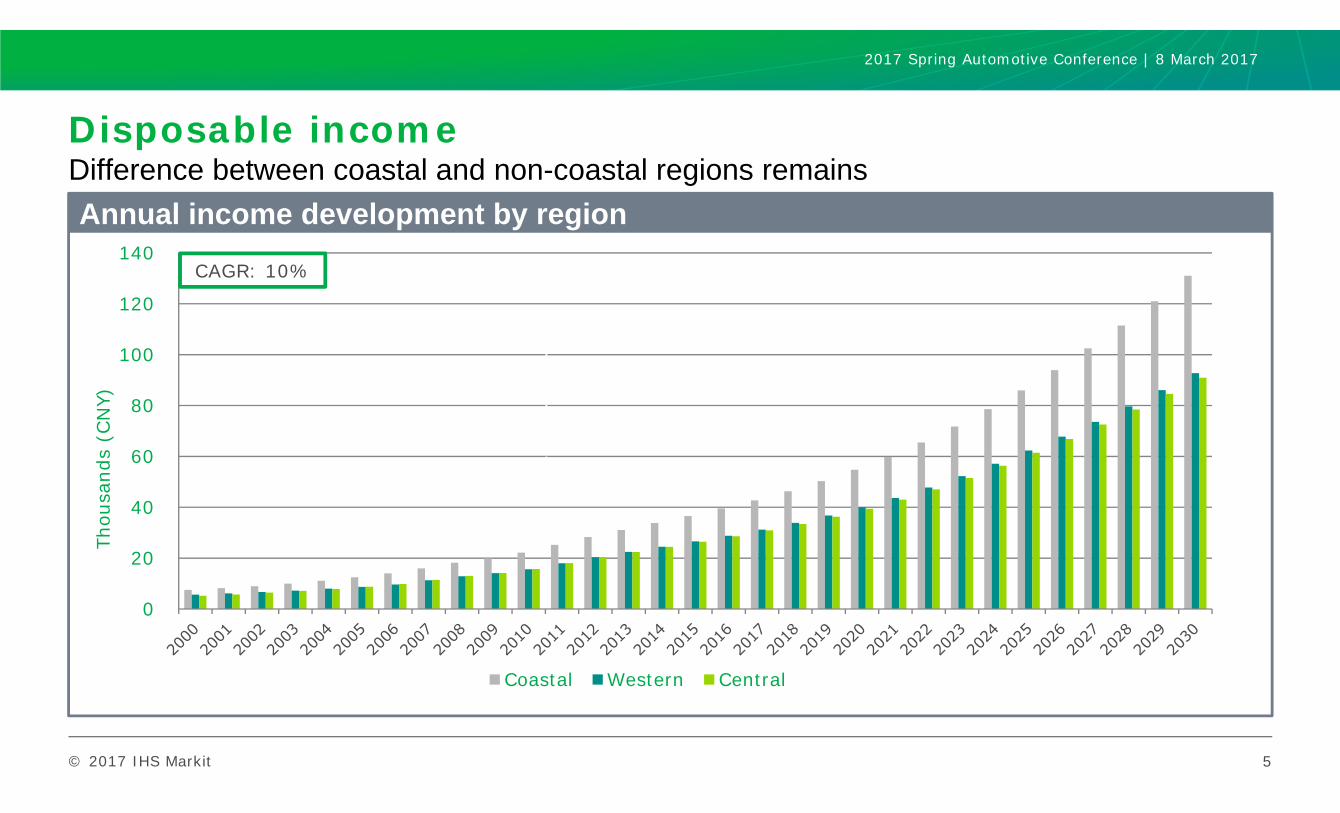

Disposable incomeDifference between coastal and non-coastal regions remainsgrowing rapidly generally; but slow down graduallyAnnual income development by region

0

20

40

60

80

100

120

140

Thou

sand

s (C

NY)

Coastal Western Central

CAGR: 10%

2017 Spring Automotive Conference | 8 March 2017

© 2017 IHS Markit

0.00

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

0.09

0

1

2

3

4

5

6

7

8

9

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

CNY vs USD CNY vs JPY

Easy period for US & EU import-sourced models is overYuan is in new phase, making premium imports more expensive

6

CNY per currency unit

2017 Spring Automotive Conference | 8 March 2017

© 2017 IHS Markit 7

UrbanizationDeviation seen among different regions, with moderate growth expected to slowUrbanization rate

0%

1%

2%

3%

4%

5%

6%

7%

0

200

400

600

800

1,000

1,200

1,400

1,600

Urban population Rural population Urban popul. growth

Urbanization rate: 50%

Mill

ions

2017 Spring Automotive Conference | 8 March 2017

© 2017 IHS Markit 8

China’s demographic structureAmount of potential vehicle consumers is shrinking Share of demographic by age

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 2020 2025 2030

0-19 20-59 60 up

Peak population in 2028: 1,416.4 million

61%

2017 Spring Automotive Conference | 8 March 2017

© 2017 IHS Markit 9

Fluctuation in 2015–18Recovery from recession by stimuli

Presentation Name / Month 2016

© 2017 IHS Markit

Inventory pressure since 2014

10

0

0.5

1

1.5

2

2.5

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2013 2014 2015

87%

7%2%4%

Sales structure

New vehicle After sales

Financial service Others

55%40%

5%

Margin structure

New vehicle After sales

Others

Mon

th

High inventory from Q4 2014 Pressure relief

Tax-cut policy started

Vehicle inventory level

Source: CADA Source: Gasgoo

Business structure of dealer

2017 Spring Automotive Conference | 8 March 2017

© 2017 IHS Markit

0

1000

2000

3000

4000

5000

6000

7000

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Shanghai Shenzhen

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

50%

Prod growth rate

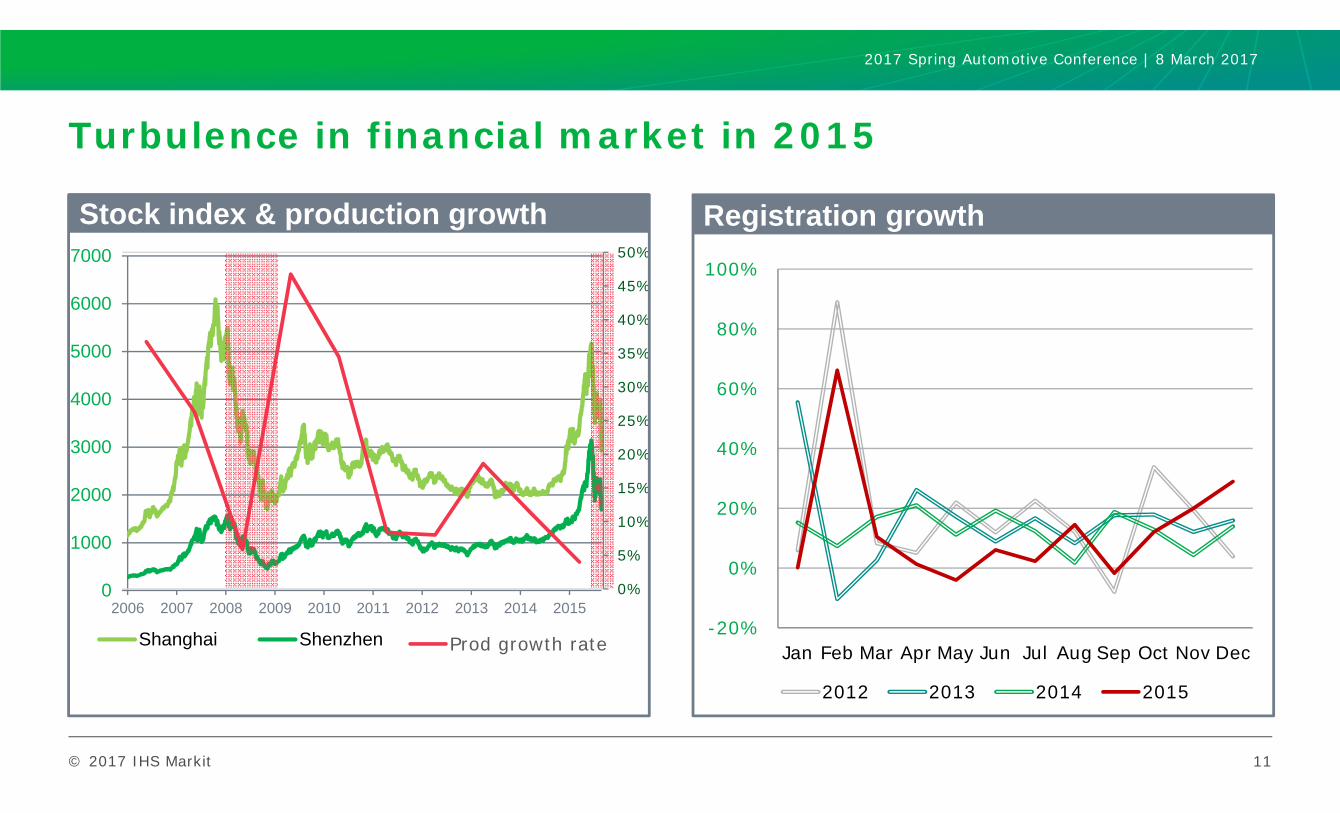

Turbulence in financial market in 2015

11

Stock index & production growth Registration growth

-20%

0%

20%

40%

60%

80%

100%

Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec

2012 2013 2014 2015

2017 Spring Automotive Conference | 8 March 2017

© 2017 IHS Markit 12

Production development 2000–20Significant impacts by tax-cut stimulus policyAnnual volume and growth rate

0%

10%

20%

30%

40%

50%

60%

0

5

10

15

20

25

30

35

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Mill

ions

PC LCV Growth rate y/y

6%

Tax-cut policy as main driver

49%31%

3%

13%

3%0%

2017 Spring Automotive Conference | 8 March 2017

© 2017 IHS Markit

0

5

10

15

20

25

30

35

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Mill

ions

Engine share in policy stimulation periods

Europe 2017 production change, by type of shipmentsVolume trend and engine ratio

0

5

10

15

20

25

30

35

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Mill

ions

Ideal volume trend Actual volume trend

55%

Ratio of engine <=1.6 in passenger car sector

63% 62%

64%68%

70%

2017 Spring Automotive Conference | 8 March 2017

© 2017 IHS Markit 14

Long-term developmentWays to reach mature market

Presentation Name / Month 2016

© 2017 IHS Markit 15

China market enters adjustment phaseSlowing down gradually after 2019, a decline still not expectedProduction volume development

Growth phase Mature phaseAdjustment phase

0%

10%

20%

30%

40%

50%

60%

0

5

10

15

20

25

30

35

40

Mill

ion

s

PV LCV Growth rate y/y

6 million

2017 Spring Automotive Conference | 8 March 2017

© 2017 IHS Markit

OEM growth distribution 2016 to 2025 by body type

16

SUV

Sedan/Hatch

MPV

Rest of body type

General Motors+0.6 million+3.0% p.a.

Toyota+0.5 million+4.1% p.a.

Volkswagen+0.7 million+1.9% p.a.*

* p.a. = per annum

Geely+0.6 million+6.2% p.a.

Chery+0.3 million+5.2% p.a.

Renault-Nissan+0.3 million+2.7% p.a.

PSA+0.3 million+4.6% p.a.

Hyundai+0.3 million+1.6% p.a.

BAIC+0.3 million+4.1% p.a.

6.0+M

Rest of OEMs+2.1 million+2.2% p.a.

SUV still the strongest driver in the next decade. China’s main local OEMs will remain in over-average growth.

2017 Spring Automotive Conference | 8 March 2017

© 2017 IHS Markit

- 1 2 3 4 5 6 7 8 9

10 11 12 13

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

Electric Plug-in hybrid Full hybrid Mild hybrid

Units: Million

+China-defined NEVs

xEVs=

China-defined NEVs

xEVs

Whole PVs

5 years CAGR 140%

131%

11%

2010~2015

49%

71%

5%

2015~2020

16%

30%

2%

2020~2025

17

NEV development

2017 Spring Automotive Conference | 8 March 2017

© 2017 IHS Markit

Modular platform of China brandsLocal OEMs are developing own modular platforms

Local brand ownedJoint venture & local cooperation

>30%

2017 Spring Automotive Conference | 8 March 2017

© 2017 IHS Markit

Brand expansion by joint venture and China brandsBrand diversification by local OEMs; further localization by joint venture OEMs PV Brand number

0

20

40

60

80

100

120

CY 2005 CY 2015 CY 2025Local brand JV non-Premium Premium brand

52

79

104

>20%

Production CAGR of premium brand

BAIC

Geely

GreatWall

Chery

Brilliance

Return of multi-brand strategy?

Production in 2025

Number of brands

9

5

3

4

5

SOP Nov2016

SOP June 2017

SOP April 2017

“Huarui”SOP April 2017

“Chery+Tata”SOP 2018

2017 Spring Automotive Conference | 8 March 2017

© 2017 IHS Markit

Domestic capacity expansion by China brandsMarket new entrants and NEV facilities as large contributors

20

1.3M

Harbin

Wuhan

Changzhou

ShangraoHangzhou

Ruili

Chongqing

Huanghua

BaojiZhenjiang

Miyun

Yangzhou

Urumqi

In 2016BAIC: Huanghua, Ruili, Zhenjiang, Miyun, ChongqingChangan: HarbinFDG: HangzhouHanteng: ShangraoJoylong: YangzhouDongfeng: Changzhou

Suzhou

DeqingGuiyang

Zhangjiakou

Huaian

Tianjin

Xushui

After 2016CH Auto: SuzhouDongfeng: Wuhan IIIFaraday: DeqingGAC: Urumqi, HangzhouGeely: Baoji, Zhangjiakou, GuiyangMinan: HuaianNEVS: TianjinWangxiang: HangzhouGreatwall: XushuiJAC: Wuhan

1.1M

NEV2016 Post 2016

2017 Spring Automotive Conference | 8 March 2017

© 2017 IHS Markit

R&D establishment by China brands overseasEstablishing new plants and R&D centres reflect COEMs’ ambitions

Production

R&D

BAIC

NEXTEV

BYD

Volvo

SAIC

GWM

ChanganJACVolvo

JAC

Changhe

SAICGWM Lifan

JACHaima

FotonSAIC

SAICChery

Foton

R&D spending in 2015

0

1

2

3

4

5

6

7

8

9

Bill

ion

EURO

Growth2015 vs 2011

40%31%

300%

60%

186%

2017 Spring Automotive Conference | 8 March 2017

© 2017 IHS Markit

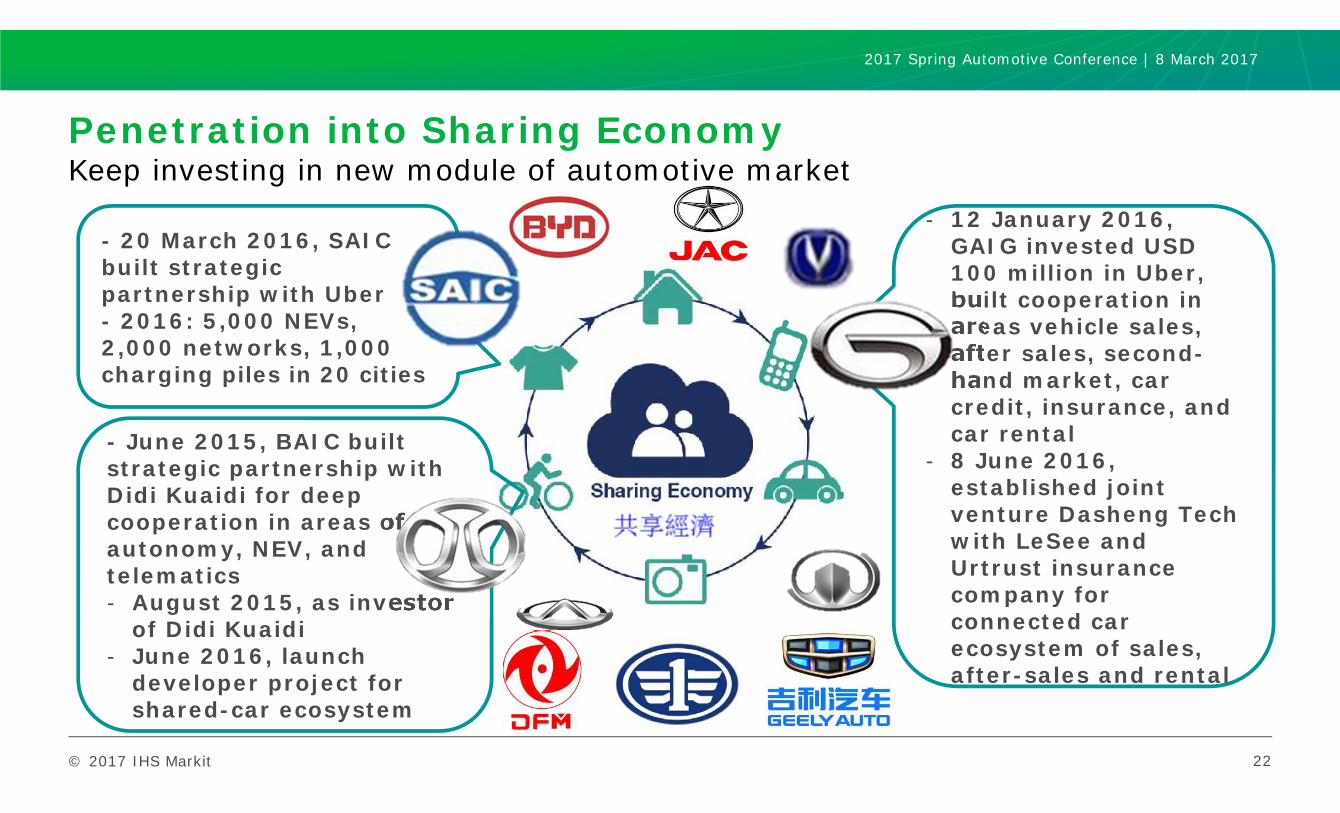

Penetration into Sharing EconomyKeep investing in new module of automotive market

22

- 20 March 2016, SAIC built strategicpartnership with Uber- 2016: 5,000 NEVs, 2,000 networks, 1,000 charging piles in 20 cities

- June 2015, BAIC built strategic partnership with Didi Kuaidi for deep cooperation in areas of autonomy, NEV, and telematics- August 2015, as investor

of Didi Kuaidi- June 2016, launch

developer project for shared-car ecosystem

- 12 January 2016, GAIG invested USD 100 million in Uber, built cooperation in areas vehicle sales, after sales, second-hand market, car credit, insurance, and car rental

- 8 June 2016, established joint venture Dasheng Tech with LeSee and Urtrust insurance company for connected car ecosystem of sales, after-sales and rental

2017 Spring Automotive Conference | 8 March 2017

© 2017 IHS Markit

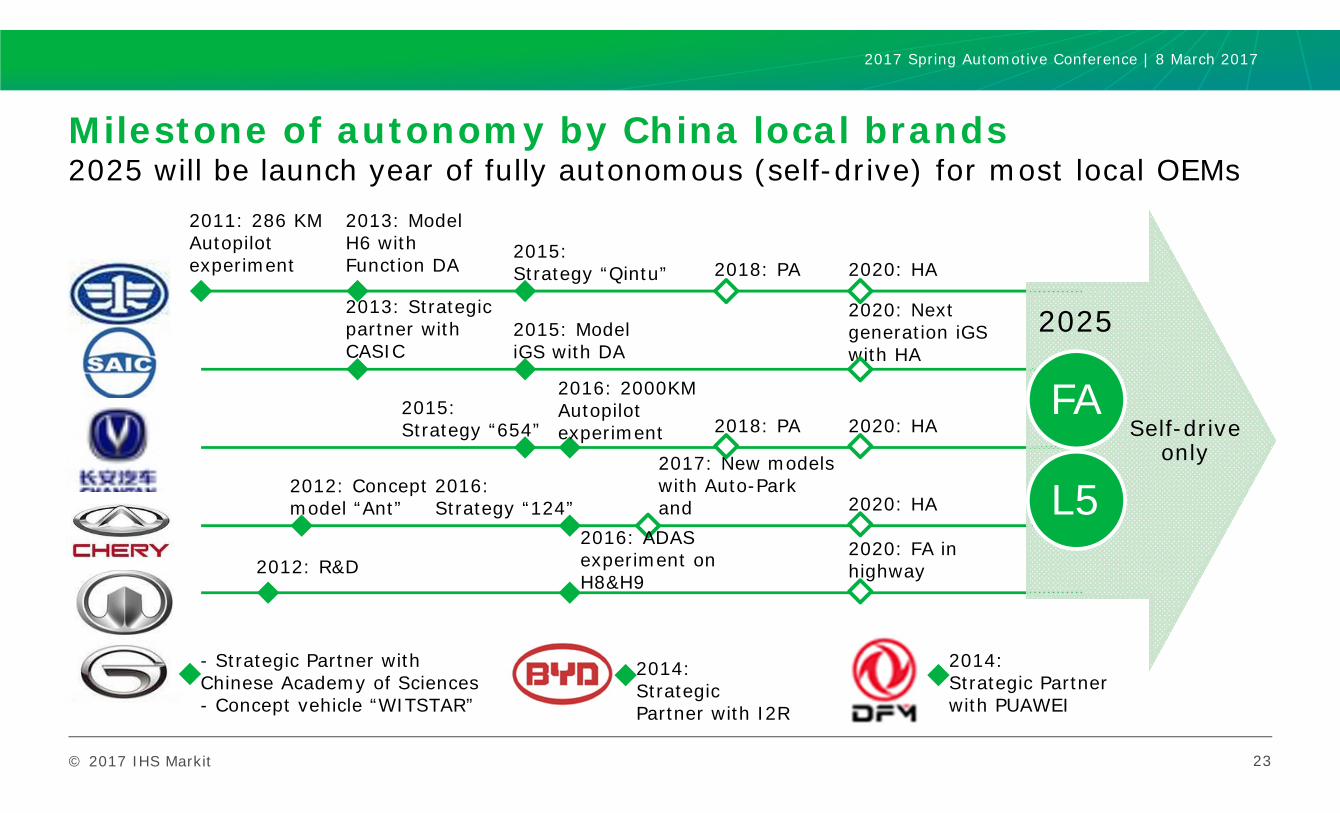

Milestone of autonomy by China local brands2025 will be launch year of fully autonomous (self-drive) for most local OEMs

23

2011: 286 KM Autopilot experiment

2013: Model H6 with Function DA 2018: PA 2020: HA

2015: Model iGS with DA

2020: Next generation iGS with HA

2016: 2000KM Autopilot experiment 2018: PA 2020: HA

2013: Strategic partner with CASIC

2015:Strategy “Qintu”

2015:Strategy “654”

2020: HA

2014:Strategic Partner with I2R

2014:Strategic Partner with PUAWEI

2017: New models with Auto-Park and

2020: FA in highway2012: R&D

- Strategic Partner with Chinese Academy of Sciences- Concept vehicle “WITSTAR”

2012: Concept model “Ant”

2016: ADAS experiment on H8&H9

2016:Strategy “124”

Self-drive only

FA

L5

2025

2017 Spring Automotive Conference | 8 March 2017

IHS MarkitTM COPYRIGHT NOTICE AND DISCLAIMER © 2017 IHS Markit.

No portion of this presentation may be reproduced, reused, or otherwise distributed in any form without prior written consent of IHS Markit. Content reproduced or redistributed with IHS Markit permission must display IHS Markit legal notices and attributions of authorship. The information contained herein is from sources considered reliable, but its accuracy and completeness are not warranted, nor are the opinions and analyses that are based upon it, and to the extent permitted by law, IHS Markit shall not be liable for any errors or omissions or any loss, damage, or expense incurred by reliance on information or any statement contained herein. In particular, please note that no representation or warranty is given as to the achievement or reasonableness of, and no reliance should be placed on, any projections, forecasts, estimates, or assumptions, and, due to various risks and uncertainties, actual events and results may differ materially from forecasts and statements of belief noted herein. This presentation is not to be construed as legal or financial advice, and use of or reliance on any information in this publication is entirely at your own risk. IHS Markit and the IHS Markit logo are trademarks of IHS Markit.

IHS Markit Customer Care:[email protected]: +1 800 IHS CARE (+1 800 447 2273)Europe, Middle East, and Africa: +44 (0) 1344 328 300Asia and the Pacific Rim: +604 291 3600

Thank you

Presentation Name / Month 2016