avm investor presentation september 2012 …...- automated cyanide dosing avocet mining investor...

TRANSCRIPT

Page 1Page 1

December 2011

Avocet Mining Investor PresentationSeptember 2012

Page 2

OPERATIONSIntroduction

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 3

DISCLAIMER

This Presentation is for information purposes in connection with Avocet Mining PLC’s (the “Company’s”) investor presentation only. While the information contained herein has been prepared in good faith, neither the Company nor any of its shareholders, directors, officers, agents, employees, consultants or advisers give, have given or have authority to give, any representations or warranties (express or implied) as to, or in relation to, the accuracy, reliability, completeness or suitability of the information in this Presentation, or any revision thereof, or of any other written or oral information made or to be made available to any interested party or its advisers (all such information being referred to as "Information") and liability therefore is expressly disclaimed.Accordingly, neither the Company nor any of its shareholders, directors, officers, agents, employees, consultants or advisers take any responsibility for, or will accept any liability whether direct or indirect, express or implied, contractual, tortious, statutory or otherwise, in respect of the accuracy or completeness of the Information or for any of the opinions contained herein or for any errors, omissions or misstatements or for any loss, howsoever arising or out of or in connection with the use of this Presentation. Each party to whom this Presentation is made available must make its own independent assessment of the Company and the Presentation after making such investigations and taking such advice as may be deemed necessary. Any reliance placed on the Presentation is strictly at the risk of such person relying on such Presentation. This Presentation may contain forward-looking statements regarding the Company and its subsidiaries. These statements are based on various assumptions made by the Company. Such assumptions are subject to factors which are beyond our control and which involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performances or achievements expressed or implied by the forward-looking statements. Forward-looking statements may in some cases be identified by terminology such as “may”, “will”, “could”, “should”, “expect”, “plan”, “intend”, “anticipate”, “believe”, “estimate”, “predict”, “potential” or “continue”, the negative of such terms or other comparable terminology. These forward looking statements are only predictions. Actual events or results may differ materially, and a number of factors may cause our actual results to differ materially from any such statement. Such factors include among others general market conditions, demand for our products, development in reserves and resources, unpredictable changes in regulations affecting our markets, market acceptance of products and such other factors that may be relevant from time to time. Although we believe that the expectations and assumptions reflected in the statements are reasonable, any person relying on such Information and Presentation are cautioned that we cannot guarantee future results, levels of activity, performance or achievement. In preparing this Presentation and except as required by law, we do not undertake or agree to any obligation or responsibility to provide the recipient with access to any additional information or to update this Presentation or Information or to correct any inaccuracies in, or omission from this Presentation or to update publicly any forward-looking statements for any reason after the date of this Presentation to conform these statements to actual results or to changes in our expectations. You are advised, however, to consult any further public disclosures made by us, such as filings made with the London Stock Exchanges, Oslo Stock Exchange or press releases.This Presentation does not constitute an offer or invitation to sell, or any solicitation of any offer to subscribe for or purchase any securities and nothing contained herein shall form the basis of any contract or commitment whatsoever. Copies of this Presentation should not be distributed to any affiliates, third parties or indirect recipients in any manner whatsoever. The distribution of this Presentation in or to persons subject to other jurisdiction may be restricted by law and persons into whose possession this Presentation comes should inform themselves about, and observe any such restrictions. Any failure to comply with these restrictions may constitute a violation of the laws of the relevant jurisdictions.United Kingdom: This Presentation has not been approved by an authorised person in accordance with Section 21 of the Financial Services and Markets Act 2000 and therefore it is being delivered for information purposes only to a very limited number of persons and companies who are persons who have professional experience in matters relating to investments and who fall within the category of person set out in Article 19 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 (the "Order") or are high net worth companies within the meaning set out in Article 49 of the Order or are otherwise permitted to receive it. Any person who receives this Presentation who does not fall within the category of person set out in Article 19 and Article 49 of the Order should not rely or act upon it. By accepting this Presentation, the recipient represents and warrants that they are a person who falls within the above description of persons entitled to receive the Presentation.

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 4

H1 2012 STRATEGIC & OPERATIONAL HIGHLIGHTS

• Gold production of 71,213 oz. (H2 2011: 79,358 oz.)

• Full year guidance revised to 135,000 – 140,000 oz. at cash cost of US$1,000 – 1,050 per oz.

• Measures taken to improve operational performance, including strengthening of on-site management team

• Inata expansion scoping study delayed due to ongoing metallurgical test work

• Resource development in Burkina Faso progressing ahead of schedule

• No dividend to be paid in respect of the 2012 financial year

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 5

H1 2012 FINANCIAL HIGHLIGHTS

• Cash costs US$922 per oz. (H2 2011: US$788 per oz.)

• Average realised gold price of US$1,494 per oz. (H2 2011: US$1,449 per oz.)

• EBITDA of US$36.8 million (H2 2011: US$42.1 million)

• Net cash generated by operating activities of US$34.6 million(H2 2011: US$13.0 million)

• Cash of US$80.4 million, with external debt reduced to US$17.0 million

• Discussions ongoing to replace current financing facility that will be repaid in Q1 2013

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 6

• Complete scoping study on Inata expansion x

• Finalise metallurgical modelling of deposit at Inata ~• Advance cost control and operating efficiency initiatives x

• Finish commissioning of gravity circuit at Inata plant

• Complete geo-chemical drilling of near term exploration targets in Bélahouro

• Commence infill drilling programme at Souma

2012 YEAR TO DATE EVALUATION

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 7

H1 2012 OPERATIONAL CHALLENGES

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

• Ongoing poor availabilities of excavators in both Q1 and Q2 2012

• Inadequate stripping, as a result of limited earthmoving capacity, restricted access to ore

- Grade and recoveries impacted in turn

• Minor pit wall slip in Q1 2012 restricted access to high grade ore

• Presence of preg-robbing ore kept recoveries at below 90%

• Lack of continuity of on-site management

Page 8

Operations

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 9

BURKINA FASO

• Stable mining friendly jurisdiction

• Rapidly expanding mining sector- Only one gold mine in 2007- Seven gold mines operational

by end 2012- Gold production rose by 32% in

2011

• Over 30 listed gold producers and explorersin country

• Gold constitutes 47% of export revenues

• Third biggest gold exploration and fourth biggest gold producing country in Africa

• Candidate country for EITI

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Source: Mining Journal

Page 10

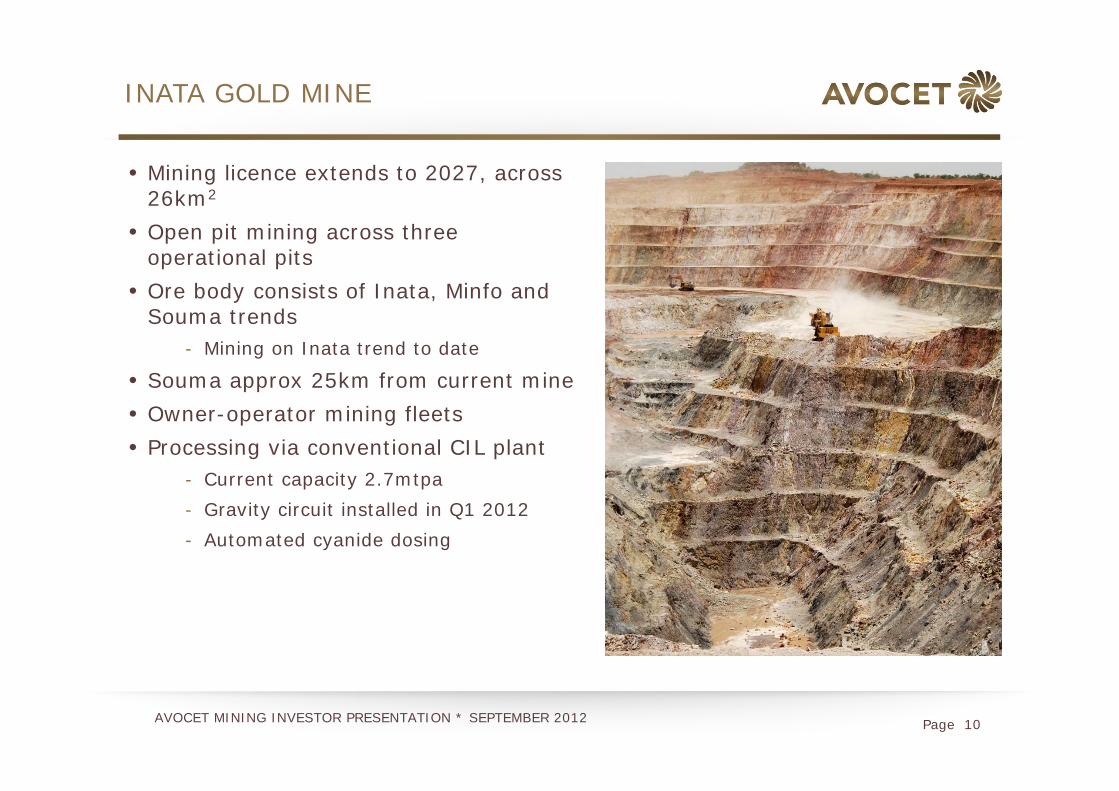

INATA GOLD MINE

• Mining licence extends to 2027, across 26km2

• Open pit mining across three operational pits

• Ore body consists of Inata, Minfo and Souma trends

- Mining on Inata trend to date

• Souma approx 25km from current mine• Owner-operator mining fleets• Processing via conventional CIL plant

- Current capacity 2.7mtpa- Gravity circuit installed in Q1 2012- Automated cyanide dosing

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 11

INATA – H1 2012 OPERATING PERFORMANCE

• Q2 2012 LTI free, year to date one LTI• 15.1mt mined (H2 2011: 15.5mt) due to low

excavator availabilities• Strip ratio 11.7:1• 1.26mt processed (H2 2011: 1.24mt) • Production of 71,213 oz. (H2 2011: 79,358 oz.)

- Average recoveries of 86% (H2 2011:91%)- Average head grade of 2.1 g/t Au

(H2 2011: 2.3 g/t Au)

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 12

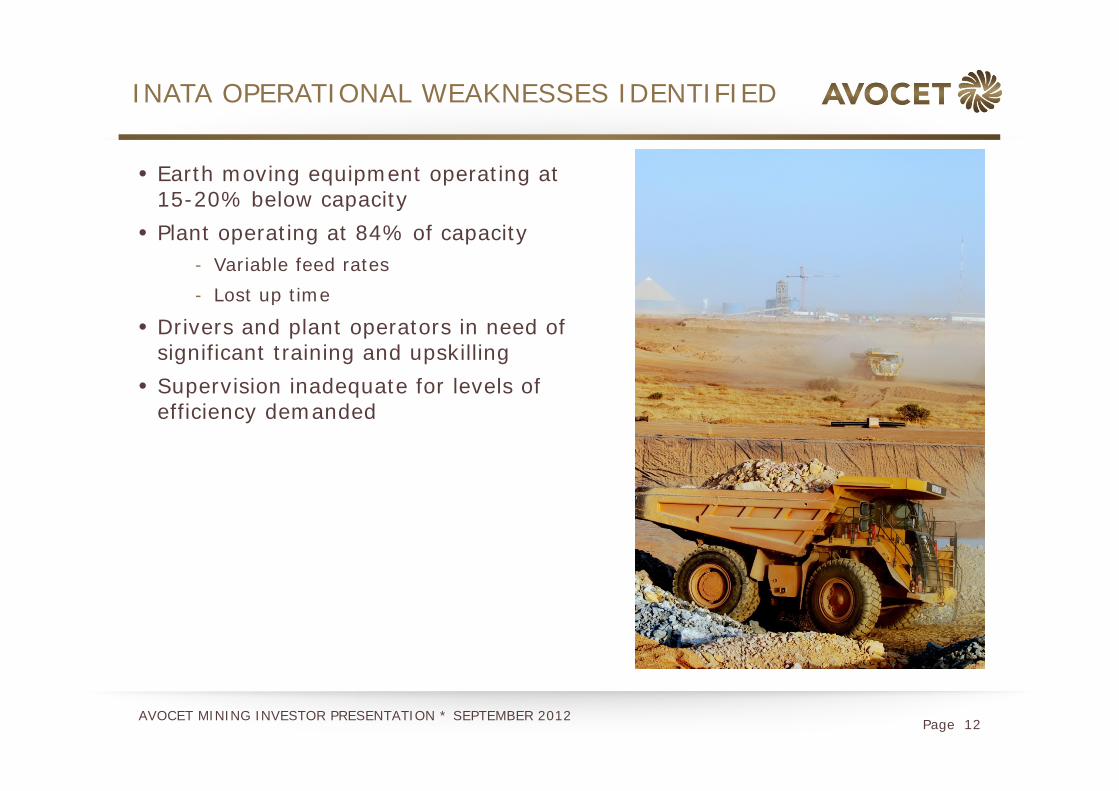

INATA OPERATIONAL WEAKNESSES IDENTIFIED

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

• Earth moving equipment operating at 15-20% below capacity

• Plant operating at 84% of capacity- Variable feed rates- Lost up time

• Drivers and plant operators in need of significant training and upskilling

• Supervision inadequate for levels of efficiency demanded

Page 13

INATA - ADDRESSING CHALLENGES

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

• Mining consultants Alexander Proudfoot engaged• Initial 3 week diagnostic evaluation undertaken• 27 week implementation plan now underway, full benefit end Q1 2013• Implementation plan initally focused on mining:

- Excavator “hot seating” is easiest win- Shift transition process changed to reduce down time- Staggered shift starts improve labour efficiency- Truck loads increased with numerous small optimisation efforts- “Go line” moved to reduce haulage distance- Truck refuelling moved to lunch breaks, reducing down time

• Second workstream will focus on processing efficiency• Changes to standard operating procedures to be supported by:

- Implementation of management control systems for both mining and processing- Behavioural coaching across all management and supervisors

Page 14

INATA - ADDRESSING CHALLENGES CONT’D

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

• AMS fleet contracted to assist with earth moving

- Capacity of 15,000 tpd- Arrived on site early September 2012

• Enhancements to existing fleet capacity- Hungry boards fitted to dump trucks,

increasing load factor by 10 tonnes- New wheeled loader procured and now

on site

• Operational management team expanded

Page 15

NEW OPERATIONAL TEAM

David Cather

CEO

• Mining engineer, Imperial College

• Over 30 years experience

• Ex Anglo American and De Beers

• Operational positions held in UK, Brazil,Continental Europe, Colombia, Philippines, Nicaragua, DRC

• Recently COO of European Goldfields

• Appointed July 2012

John McNair

GENERAL MANAGER

• Engineer by training

• Over 30 years experience

• Over five years experience at General Manager level

• Managed operations in West Papua, Philippines, Australia

• Joined August 2012

Andy Mortimore

PROCESS MANAGER

• Camborne School of Mines

• Over 30 years experience in processing in both copper and gold

• Operational positions held in UK, Zambia, Zimbabwe, Canada, DRC and Kyrgyzstan

• Ex Centerra Gold

• Joined August 2011

Karel Jordaan

MINE MANAGER

• Over 20 years experience in mining across Africa

• Ex Anglogold Ashanti

• Joining October 2012

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 16

INATA – 2012, 2013 MINE PLAN

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

• Ore sources primarily from oxide material for until mid 2013

• Average strip ratio of 12.5:1 over 18 months

• Ore processed over next 18 months of 4 mt

• Average head grade of 2.0 g/t over next 18 months

• Average recoveries of 89%• 64,000 - 69,000 oz. of production

for remainder of FY12- Highest production in Q4 2012

• 150,000-160,000 oz. of production in 2013

- High grade Inata North pit scheduled for Q3 2013

Page 17

INATA - SCOPING STUDY UPDATE

• Rationale remains to optimise the processing capacity to maximise return from enlarged ore body

• Optimal processing methodology, suitable for ore sources across Bélahouro, remains to be determined:

1. Metallurgical testing of composite samples, to determine the appropriate ore processing, has been completed

2. Next step is to analyse the sample performance under selected processing route

3. Engineering and cost study to follow- Estimate recoveries and operating costs - Estimate capital cost

• Parallel process of metallurgical testing on Souma ores• Full update planned for November 2012

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 18

Exploration

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 19

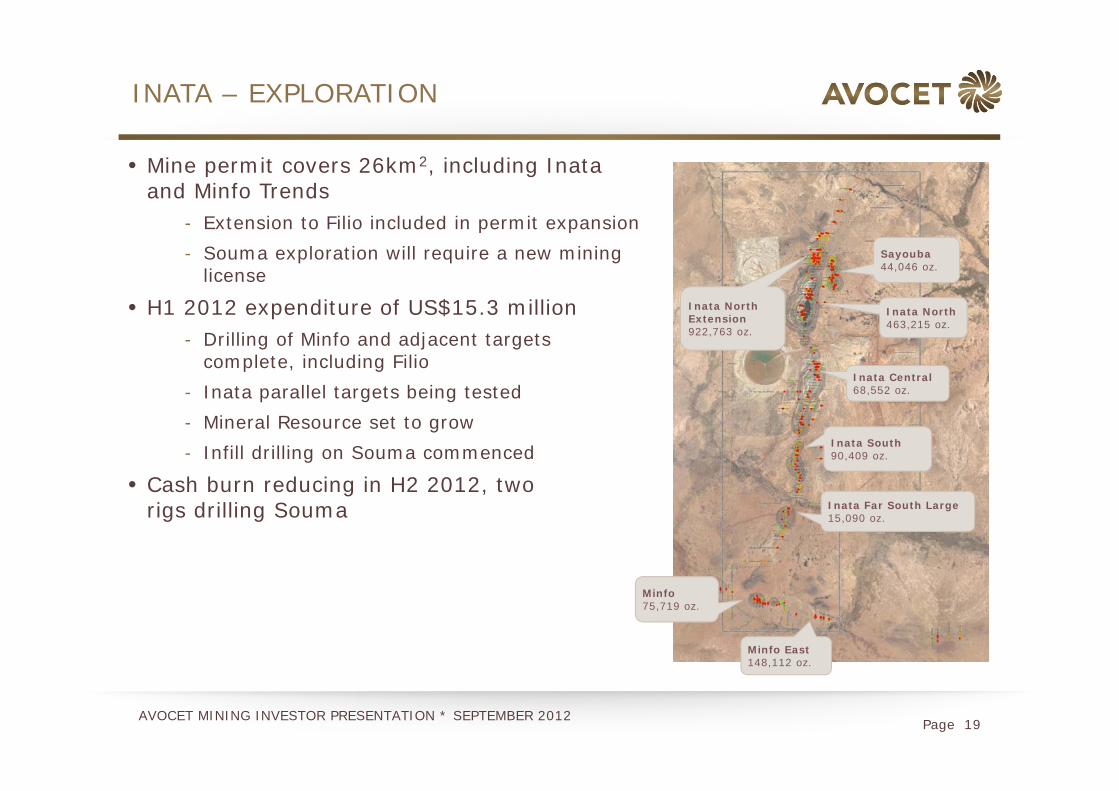

INATA – EXPLORATION

• Mine permit covers 26km2, including Inata and Minfo Trends

- Extension to Filio included in permit expansion- Souma exploration will require a new mining

license

• H1 2012 expenditure of US$15.3 million- Drilling of Minfo and adjacent targets

complete, including Filio- Inata parallel targets being tested- Mineral Resource set to grow- Infill drilling on Souma commenced

• Cash burn reducing in H2 2012, two rigs drilling Souma

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Minfo75,719 oz.

Inata North Extension922,763 oz.

Inata North463,215 oz.

Inata Central68,552 oz.

Inata South90,409 oz.

Inata Far South Large15,090 oz.

Minfo East148,112 oz.

Sayouba44,046 oz.

Page 20

INATA – EXPANDED RESOURCE MODELLING

• Over 5,000 pulps from across Inataanalysed

- Organic carbon, total carbon, preg-robbing index (PRI)

- Sulphide sulphur, total sulphur- Quick leach test (QLT)- Ag and XRF multielements (As, Fe, Ca, Ba)

• Initial metallurgical models show variable character of fresh and transition ore

• Metallurgical test work results, expected in Q3 2012, will allow generation of an accurate recovery model

• Final model will determine Mineral Reserves and optimal LOM plan due Q4 2012

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 21

INATA

Dynamite

Miilam

GasselGarafo

FeteKole

Pali

Kourfadie

Damba

Oka Gakinde

GomdeBarrage

OuzemiFilioMinfo

Priority drilling target

INATA TREND

SOUMA TREND

MINFO TREND

N

5km

BÉLAHOURO – EXPLORATION

• Geochemical auger drilling over 80% of VTEM targets now complete- Awaiting gold assays and XRF analysis

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 22

GUINEA

• Untapped mineral potential- Two +5M oz. and three ~1M oz. Au

deposits- Extensive under-explored Birimian

geology

• Three producing mines• Government embracing EITI• New Mining Code gazetted in

January 2012• Established Commission of Mines

- Oversees all aspects of mining industry

- Grants new mining licences, permits and conventions

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 23

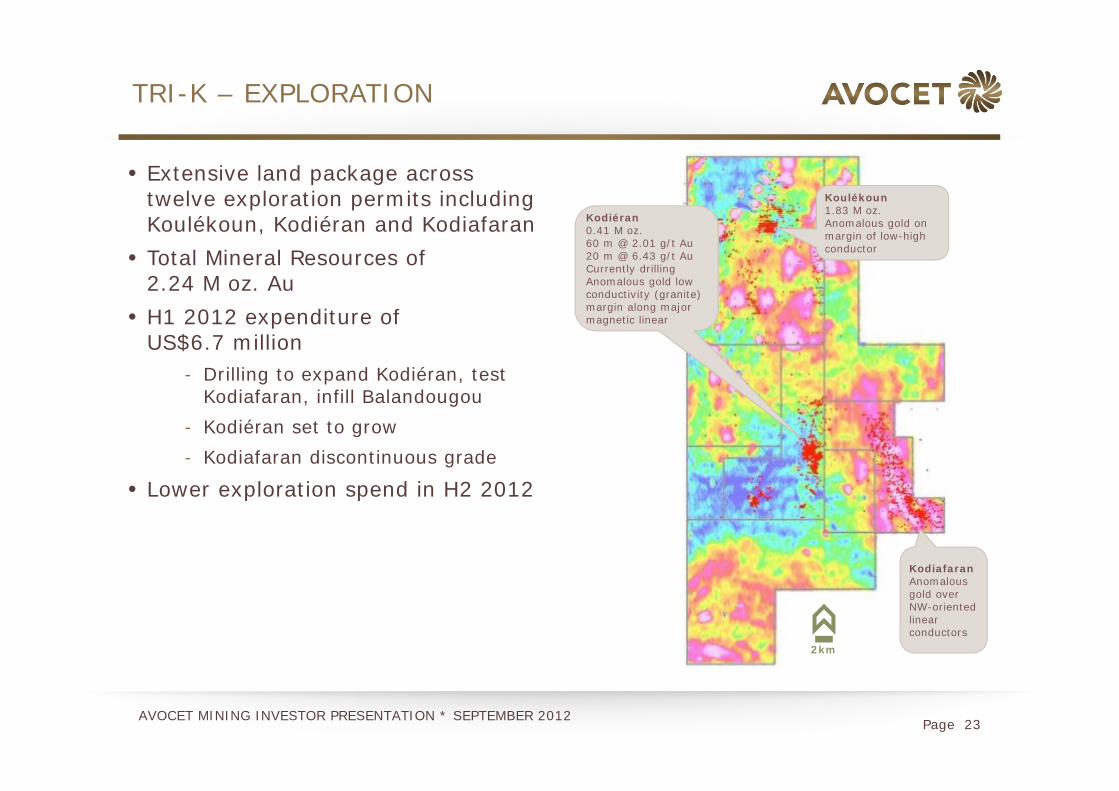

TRI-K – EXPLORATION

• Extensive land package across twelve exploration permits including Koulékoun, Kodiéran and Kodiafaran

• Total Mineral Resources of 2.24 M oz. Au

• H1 2012 expenditure of US$6.7 million

- Drilling to expand Kodiéran, test Kodiafaran, infill Balandougou

- Kodiéran set to grow- Kodiafaran discontinuous grade

• Lower exploration spend in H2 2012

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

KodiafaranAnomalous gold over NW-oriented linear conductors

Koulékoun1.83 M oz. Anomalous gold on margin of low-high conductor

2km

Kodiéran0.41 M oz. 60 m @ 2.01 g/t Au20 m @ 6.43 g/t AuCurrently drillingAnomalous gold low conductivity (granite) margin along major magnetic linear

Page 24

TRI-K – WAY FORWARD

• Metallurgical test work in process for Koulékoun

- Initial results of oxidised and fresh ore grade samples positive for simple CIL

- Will expand to include the deeply weathered Kodiéran prospect

• Updated Mineral Resource estimates due Q4 2012

- Targeting +2.5M oz. Au mainly through Kodiéran growth

• Drilling now halted in favour of scoping study- PEA due Q4 2012- IRR rather than ounce based - prioritising

grade over production

• Exploration permits to be extended to October 2013

- Feasibility study complete by this date

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 25

Financial Performance

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 26

INCOME STATEMENT- H1 2012

H1 2012 H2 2011

US$ million

Revenue 109.5 112.9

Cash costs (65.7) (63.2)

Inventory 5.1 2.1

Other cost of sales (5.8) (3.4)

Admin and share based payments (6.4) (9.2)

Depreciation (12.4) (18.6)

Exceptional items (39.8)

Profit before taxation 23.3 (21.0)

Taxation (7.5) (2.7)

Profit for the period 15.8 (23.7)

EPS (basic) 7.14 10.96

EBITDA 36.8 42.1

• Revenue down due to lower ounces sold

• Total cash costs stable but costs per oz. up 20%

• Inventory changes reflect timing of gold sales and stockpile movements

• Lower depreciation in line with fewer ounces produced

• Reduced EBITDA and EPS reflect variances in revenue and inventory change

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 27

CASH FLOW – H1 2012

H1 2012 H2 2011

US$ million

EBITDA 36.8 42.1

Working capital and interest (4.1) (29.2)

Provision/other non-cash 1.9 0.2

Operating cash flow 34.6 13.1

Capex (13.7) (25.7)

Exploration (22.0) (12.6)

Loan repayment (12.0) (12.0)

Dividend (13.2) (6.5)

Disposal of investments and operations 2.0 16.3

Restructure of hedge - (39.8)

Net cash flow (24.9) (74.1)

Opening cash 105.24 179.3

Closing cash 80.4 105.2

• Improved working capital, including more regular VAT refunds

• Operating cash flow of US$34.6m, up from US$13.1m despite lower production

• Higher exploration reflects seasonality of field spend

• Significant cash balance of US$80.4m at the end of June

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 28

CASH COSTS – H1 2012

• Lower head grade accounted for US$44 increase in costs • Lower recoveries associated with lower grade, accounting for US$24

increase in costs• Higher fuel and explosives prices increased mining costs

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

0

200

400

600

800

1,000

H2 2011Actual

Tonnestreated

Grade Recovery From/tocircuit

Miningcosts

Mill costs Admin Royalty H1 2012

US$

797 (32) 13 922559242444(11)

H1 2012 vs H2 2011 cash costs

Page 29

TOTAL CASH COSTS PER OUNCE – H1 2012

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Mining US$

Processing US$

AdminUS$

RoyaltiesUS$

TotalUS$

Fuel 122 97 13 - 232

Maintenance 93 73 11 - 179

Labour 42 23 62 - 128

Other 35 21 18 - 74

Royalties - - - 120 120

Reagents - 91 - - 91

Explosives 48 - - - 48

Contractors/ Consultants 23 - 16 - 40

Insurance - - 13 - 13

Total per oz. 364 305 133 120 922

Total US$ millions 25.9 21.7 9.5 8.5 65.7

25%

19%

14%

8%

13%

10%

5%4% 1%

Fuel Maintenance

Labour Other

Royalties Reagents

Explosives Contractors/consultants

Insurance

Page 30

Way Forward

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 31

H2 2012 WORKSTREAMS

• Complete metallurgical test work on Inata ore body and scoping study on Inata expansion

• Improve mining capacity to allow for higher rate of stripping

• Implement recommendations from operational review by consultantsAlexander Proudfoot

• Complete infill drilling at Souma

• Undertake scoping study at Koulékoun to produce PEA

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 32

Avocet Mining – a leading West African gold mining and exploration company

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 33

MINERAL RESOURCES AND RESERVES: INATA

Gross Net attributable (90%)

Tonnes(Mt)

Grade(g/t)

Containedounces

Tonnes(Mt)

Grade(g/t)

Containedounces

Mineral Reserves

Proven 16,091,000 1.72 888,000 14,482,000 1.72 799,000

Probable 17,234,000 1.70 940,000 15,510,000 1.70 846,000

ROM Stockpiles 497,000 1.25 20,000 447,000 1.25 18,000

Reserves total 33,822,000 1.70 1,848,000 30,440,000 1.70 1,663,000

Mineral ResourcesMeasured 17,881,000 1.68 963,800 16,093,000 1.68 868,000

Indicated 39,446,000 1.35 1,712,000 35,501,000 1.35 1,541,000

Measured + Indicated 57,327,000 1.45 2,676,000 51,594,000 1.45 2,409,000

Inferred 17,846,000 1.36 779,000 16,061,000 1.36 701,000

Resources total 75,173,000 1.43 3,455,000 67,655,000 1.43 3,110,000

Mineral Reserves and Mineral Resources as at 31 December 2011

1. Mineral Resources are inclusive of Mineral Reserves and reported above 0.5g/t Au cut off and below the 31 December 2011 topographic surface. The Mineral Resources were estimated by Mr David Williams (MAusIMM, MAIG) and Mr Sam Beckett (MAIG), both of whom are consultants employed by CSA Global Pty Ltd. Both Mr Williams and Mr Beckett have the experience relevant to the style of mineralisation and type of deposit under consideration to qualify as a Competent Persons as defined by the Australasian JORC Code (2004) for the reporting of Exploration Results, Mineral Resources and Ore Reserves and as Qualified Persons as defined by the Canadian National Instrument 43-101 for the reporting of Exploration Results, Mineral Resources and Mineral Reserves (NI 43-101). Mr Williams and Mr Beckett have consented to the inclusion of the technical information in this report in the form and context in which it occurs.

2. The Mineral Reserves were estimated by Mr Clayton Reeves (MSAIIM), who at the time is the compilation of this statement was the Principal Mining Consultant, CSA Global (UK). Mr Reeves is a Competent Person as defined by the JORC Code and a Qualified Person as defined by NI-43-101. Mr Reeves has consented to the inclusion of the technical information in this report in the form and context in which it occurs.

3. Avocet owns 90% of Société des Mines de Bélahouro SA, owner of the Inata Gold Mine.4. Rounding errors may occur.

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 34

MINERAL RESOURCES AND RESERVES: SOUMA

Gross Net attributable (100%)

Tonnes(Mt)

Grade(g/t)

Containedounces

Tonnes(Mt)

Grade(g/t)

Containedounces

Mineral ReservesProven ‐ ‐ ‐ ‐ ‐ ‐

Probable ‐ ‐ ‐ ‐ ‐ ‐

ROM Stockpiles ‐ ‐ ‐ ‐ ‐ ‐

Reserves total - - - - - -

Mineral ResourcesMeasured ‐ ‐ ‐ ‐ ‐ ‐

Indicated 324,000 1.44 15,000 324,000 1.44 15,000

Measured + Indicated 324,000 1.44 15,000 324,000 1.44 15,000

Inferred 10,376,000 1.64 546,000 10,376,000 1.64 546,000

Resources total 10,700,000 1.63 561,000 10,700,000 1.63 561,000

Mineral resource estimate as at 31 October 2010

1. Mineral Resources are reported above 0.5g/t Au cut off. The Mineral Resources were estimated by Mr David Williams (MAusIMM, MAIG), a consultant employed by CSA Global Pty Ltd. Mr Williams has the experience relevant to the style of mineralisation and type of deposit under consideration to qualify as a Competent Person as defined by the Australasian JORC Code (2004) for the reporting of Exploration Results, Mineral Resources and Ore Reserves and as a Qualified Person as defined by the Canadian National Instrument 43-101 for the reporting of Exploration Results, Mineral Resources and Mineral Reserves (NI 43-101). Mr Williams consents to the inclusion of the technical information in this report in the form and context in which it occurs.

2. Avocet owns 100% of the Souma property through its wholly-owned subsidiary, Goldbelt Resources (West Africa) SARL.3. Rounding errors may occur.

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012

Page 35

MINERAL RESOURCES AND RESERVES: TRI-K

Gross Net attributable (100%)

Tonnes(Mt)

Grade(g/t)

Containedounces

Tonnes(Mt)

Grade(g/t)

Containedounces

Mineral ReservesProven ‐ ‐ ‐ ‐ ‐ ‐

Probable ‐ ‐ ‐ ‐ ‐ ‐

ROM Stockpiles ‐ ‐ ‐ ‐ ‐ ‐

Reserves total - - - - - -

Mineral ResourcesKoulékoun

Measured ‐ ‐ ‐ ‐ ‐ ‐

Indicated 21,610,000 1.44 1,001,000 21,610,000 1.44 1,001,000

Measured + Indicated 21,610,000 1.44 1,001,000 21,610,000 1.44 1,001,000

Inferred 22,600,000 1.15 832,000 22,600,000 1.15 832,000

KodiéranInferred 7,260,000 1.76 411,000 7,260,000 1.76 411,000

Resources total 51,470,000 1.36 2,244,000 51,470,000 1.36 2,244,000

Mineral Resources as at 20 December 2011

1. Mineral Resources are reported above 0.5g/t Au cut off. The Company owns 100% of Wega Mining Guinée SA, owner of the Tri-K gold project. The Mineral Resources were estimated by Mr David Williams (MAusIMM, MAIG), a consultant employed by CSA Global Pty Ltd. Mr Williams has the experience relevant to the style of mineralisation and type of deposit under consideration to qualify as a Competent Person as defined by the Australasian JORC Code (2004) for the reporting of Exploration Results, Mineral Resources and Ore Reserves and as a Qualified Person as defined by the Canadian National Instrument 43-101 for the reporting of Exploration Results, Mineral Resources and Mineral Reserves (NI 43-101). Mr Williams consents to the inclusion of the technical information in this report in the form and context in which it occurs.

2. Note: rounding errors may occur.

AVOCET MINING INVESTOR PRESENTATION * SEPTEMBER 2012