awareness of financial products among rural households …apjor.com/downloads/2812201411.pdf ·...

TRANSCRIPT

Asia Pacific Journal of Research Vol: I Issue XX, December 2014

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 85

AWARENESS OF FINANCIAL PRODUCTS AMONG RURAL HOUSEHOLDS IN SRIKAKULAM

DISTRICT, ANDHRA PRADESH

Dr. T.V.V. Phani Kumar

Associate Professor,

Department of Finance,

GITAM Institute of Management,

GITAM University,

Rushikonda, Visakhapatnam - 530045

ABSTRACT

The emerging economies like India where more than 60% of the population lives in the rural areas, should

ensure adequate access to the financial products and services to all the individuals in the country.The growth

of financial system depends on the penetration of the financial products into the rural markets in the

country.Lack of awareness about the different financial products among the rural households not only affects

the growth of financial system in the country but also the overall quality of life of rural households. The

present study focuses on the awareness of various financial products among the rural households in the

Srikakulam district of Andhra Pradesh.

Key Words :Rural Households, Awareness of Financial Products, Financial Literacy, Awareness of Capital

Market Instruments

1.1 INTRODUCTION

The emerging economies like India where more than 60% of the population lives in the rural areas, should

ensure adequate access to the financial products and services to all the individuals in the country. According to

the annual MasterCard’s index for financial literacy 2013, India is in 15th place among 16 countries in Asia

Pacific region in terms of overall financial literacy. The report states that for Indians, “the lack of ability to

keep up with bills, set money aside for big item purchases and to pay off credit cards fully could be due to a

lack of surplus cash, resulting from the fact that income levels are not high enough to cover expenses”. The

condition is still worse in rural India where the levels of financial literacy are very low. The Reserve Bank of

India in March 2005 initiated financial inclusion as a major policy objective to extend banking services to the

entire population without any discrimination. The Financial Stability and Development Council (FSDC),

Asia Pacific Journal of Research Vol: I Issue XX, December 2014

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 86

headed by the Finance Minister, is mandated to focus on financial inclusion and financial literacy. All financial

sector regulators, RBI, SEBI and IRDA are committed to the mission to “create a financially aware and

empowered India”.

The growth of financial system depends on the penetration of the financial products into the rural markets in

the country. The wider participation of rural households in financial markets will lead to increased financial

deepening in Indian Economy. Lack of awareness about the different financial products among the rural

households not only affects the growth of financial system in the country but also the overall quality of life of

rural households. The present study focuses on the awareness of various financial products among the rural

households in the Srikakulam district of Andhra Pradesh. The results of the study will help the government,the

policy makers to further strengthen the financial system in rural India and improve the financial literacy among

the rural households.

1.2 REVIEW OF LITERATURE

AnnamariaLusbrdi(2005)1analyzed the effects of financial education on saving and investment behaviour of

African-Americans and Hispanics Households. The study revealed that seminars have some effect on savings,

particularly for those at the bottom of the wealth distribution, and those with low education.

C Thilakam (2012)2opined that the knowledge of rural households is limited to the traditionally known

savings and investment avenues like bank saving, holding insurance policy, investment in gold or in

land/building. The sample population’s knowledge on the modern and market sophisticated investment

avenues is very much limited.

FurqanQamar (2003)3analyzed the savings behaviour and investment preferences among average urban

middle class of Delhi. The following are the relevant findings of the study :

a. Despite financial sector reforms and entry of private, domestic and foreign banks into the country, the

nationalized commercial banks seem to be the favorite choice of an average household.

b. Capital market imperfections and associated risk have not been a deterrent for many households as they

were found investing in debentures and shares either directly or indirectly.

c. The saving behaviour and investment preferences of average urban household seem to be significantly

influenced by the level of educational attainments and income of the respondents.

Amu Manasseh Edison Komla (2012)4concluded that demo-graphic factors influence the rural household

savings of rural households. The study found that the age of the head of the household, the size of family has a

major bearing on the saving and investment behaviour of rural households in the study area. Family size and

knowledge in saving and in-vestment by household heads had no significant relationship with savings and

investment of the rural households in the Ho Municipality.

SEBI – NCAER Survey (2012)5was carried out to prepare a comprehensive profile of savings and investment

behaviour in the context of income and consumption patterns and to obtain the risk profile of the households

and relate this to savings and investment behaviour. Some of the relevant findings of the study are :

i) The percentage of investors is nearly 20 per cent in urban areas while it is much lower (6 per cent) in

rural India.

ii) There is a significant degree of non-investment by rural households because of: a)

inadequateinformation, and b) lack of adequate skills.

iii) Only 6 per cent of all households, whose primary occupation is agriculture, allocate a part of their

savings to pension plans.

Srikakulam District formerly known as Chicacole is one backward district among the nine coastal districts of

Andhra Pradesh.The current study focuses on analyzing the awareness of different financial products among

the rural households in relation to the different socio-economic indicators.

Asia Pacific Journal of Research Vol: I Issue XX, December 2014

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 87

1.3 OBJECTIVES OF THE STUDY

The main objective of the study is to analyze the awareness of financial products among the rural households

in relation to the different socio economic indicators.

1.4 METHODOLOGY OF THE STUDY

Selection of Sample :

The data needed for the study is collected from the select rural households in the Srikakulam District.

Data Collection :

The data needed for the study will be collected from both primary and secondary sources. The secondary

sources include Census 2011 reports, various journals and books in the area of financial literacy, savings and

investment behaviour of individuals.

Sampling Design :

The stratified random sampling technique will be used to collect information from the target respondents. The

population from which the sample is drawn is divided into different stratasbased on gender, income levels,

marital status, levels of education, age and occupation.

Sample Size :

The sample size is 225 rural households in Srikakulam District.

Statistical Tools

The entire data collected will be coded and computerized in Excel sheets and Bi- Variate analysis is applied.

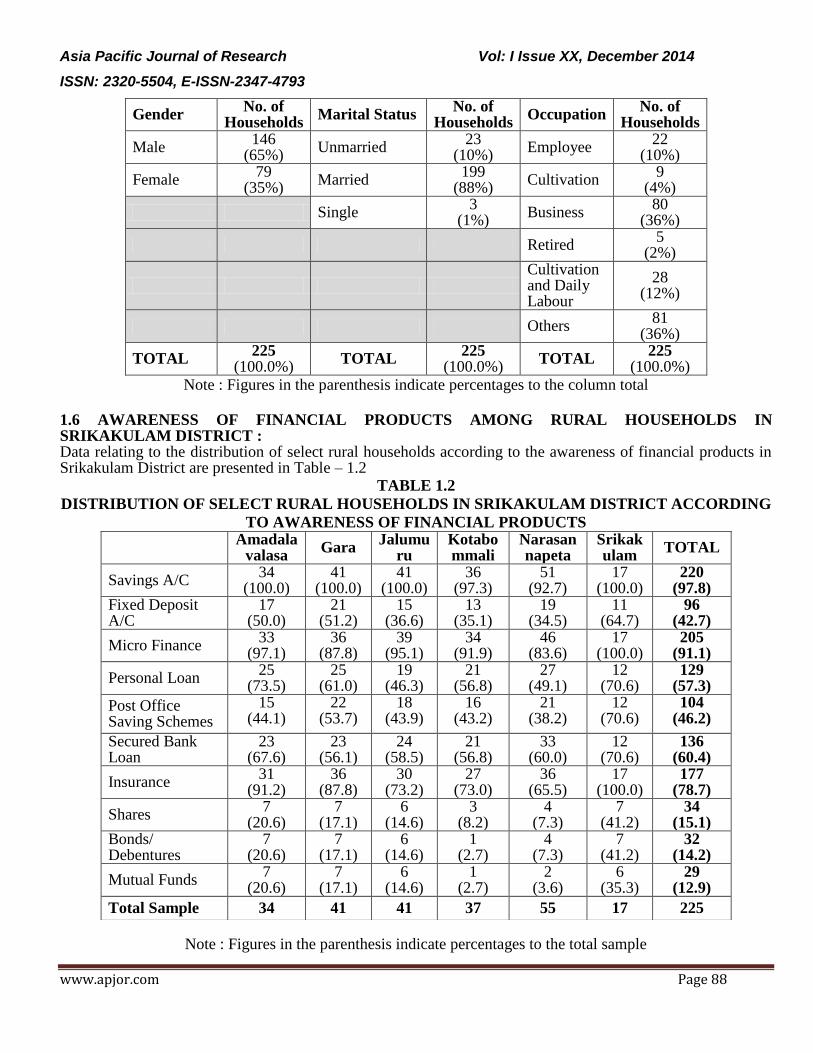

1.5 PROFILE OF THE SELECT SAMPLE OF RURAL HOUSEHOLDS IN THE STUDY AREA :

A brief profile of the select sample of the rural households in the study area is presented in the Table 1.1

TABLE 1.1

PROFILE OF THE SELECT SAMPLE OF RURAL HOUSEHOLDS

Age No. of

Households Education

No. of

Households

Income Level

(per month in Rs.)

No. of

Households

Below 30 Years 86

(38%) Uneducated

101

(45%) Less than 5,000

154

(68%)

31-40 Years 66

(29%)

Under

Graduate

102

(45%) 5001 - 10,000

52

(23%)

41-50 Years 39

(17%) Graduate

17

(8%) 10,001 - 15,000

14

(6%)

51-60 Years 25

(11%)

Post

Graduate

2

(1%) More than 15,000

5

(2%)

Above 60 Years 9

(4%) Others

3

(1%)

TOTAL 225

(100.0%) TOTAL

225 (100.0%)

TOTAL 225

(100.0%)

Note : Figures in the parenthesis indicate percentages to the column total

Asia Pacific Journal of Research Vol: I Issue XX, December 2014

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 88

Gender No. of

Households Marital Status

No. of Households

Occupation No. of

Households

Male 146

(65%) Unmarried

23 (10%)

Employee 22

(10%)

Female 79

(35%) Married

199 (88%)

Cultivation 9

(4%)

Single 3

(1%) Business

80 (36%)

Retired 5

(2%)

Cultivation and Daily Labour

28 (12%)

Others 81

(36%)

TOTAL 225

(100.0%) TOTAL

225 (100.0%)

TOTAL 225

(100.0%)

Note : Figures in the parenthesis indicate percentages to the column total

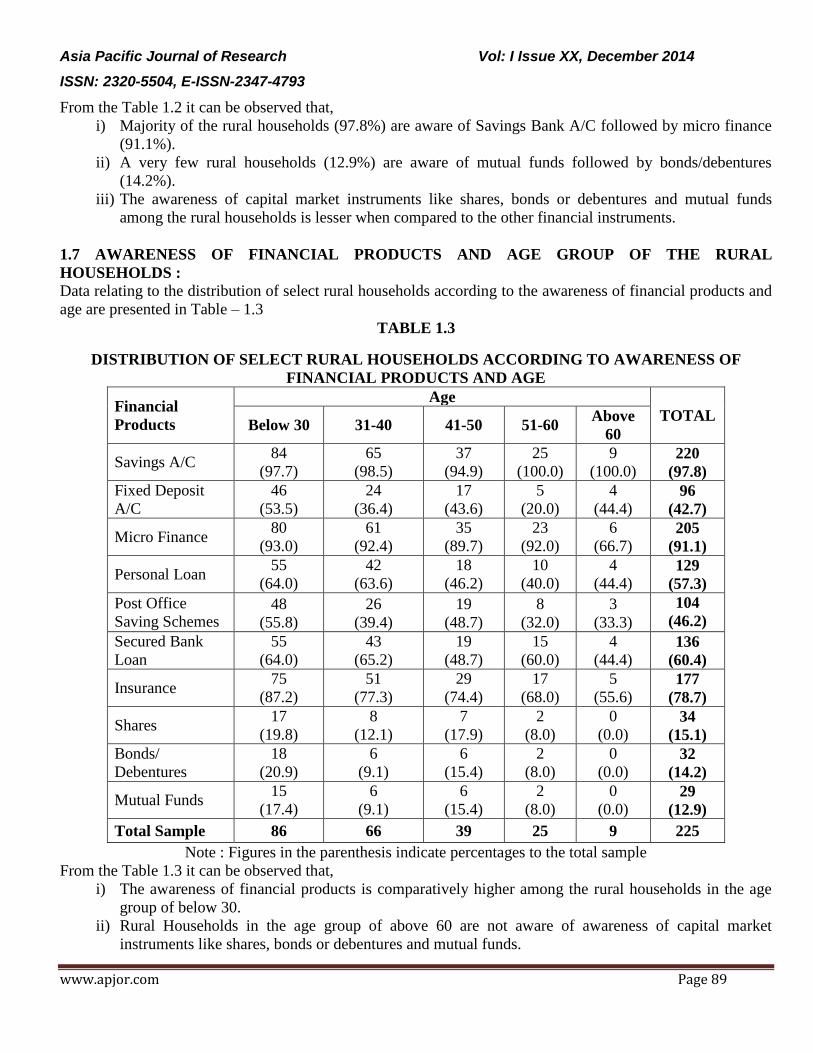

1.6 AWARENESS OF FINANCIAL PRODUCTS AMONG RURAL HOUSEHOLDS IN SRIKAKULAM DISTRICT : Data relating to the distribution of select rural households according to the awareness of financial products in Srikakulam District are presented in Table – 1.2

TABLE 1.2

DISTRIBUTION OF SELECT RURAL HOUSEHOLDS IN SRIKAKULAM DISTRICT ACCORDING

TO AWARENESS OF FINANCIAL PRODUCTS

Note : Figures in the parenthesis indicate percentages to the total sample

Amadala

valasa Gara

Jalumuru

Kotabommali

Narasannapeta

Srikakulam

TOTAL

Savings A/C 34

(100.0) 41

(100.0) 41

(100.0) 36

(97.3) 51

(92.7) 17

(100.0) 220

(97.8) Fixed Deposit A/C

17 (50.0)

21 (51.2)

15 (36.6)

13 (35.1)

19 (34.5)

11 (64.7)

96 (42.7)

Micro Finance 33

(97.1) 36

(87.8) 39

(95.1) 34

(91.9) 46

(83.6) 17

(100.0) 205

(91.1)

Personal Loan 25

(73.5) 25

(61.0) 19

(46.3) 21

(56.8) 27

(49.1) 12

(70.6) 129

(57.3)

Post Office Saving Schemes

15 (44.1)

22 (53.7)

18 (43.9)

16 (43.2)

21 (38.2)

12 (70.6)

104 (46.2)

Secured Bank Loan

23 (67.6)

23 (56.1)

24 (58.5)

21 (56.8)

33 (60.0)

12 (70.6)

136 (60.4)

Insurance 31

(91.2) 36

(87.8) 30

(73.2) 27

(73.0) 36

(65.5) 17

(100.0) 177

(78.7)

Shares 7

(20.6) 7

(17.1) 6

(14.6) 3

(8.2) 4

(7.3) 7

(41.2) 34

(15.1) Bonds/ Debentures

7 (20.6)

7 (17.1)

6 (14.6)

1 (2.7)

4 (7.3)

7 (41.2)

32 (14.2)

Mutual Funds 7

(20.6) 7

(17.1) 6

(14.6) 1

(2.7) 2

(3.6) 6

(35.3) 29

(12.9)

Total Sample 34 41 41 37 55 17 225

Asia Pacific Journal of Research Vol: I Issue XX, December 2014

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 89

From the Table 1.2 it can be observed that,

i) Majority of the rural households (97.8%) are aware of Savings Bank A/C followed by micro finance

(91.1%).

ii) A very few rural households (12.9%) are aware of mutual funds followed by bonds/debentures

(14.2%).

iii) The awareness of capital market instruments like shares, bonds or debentures and mutual funds

among the rural households is lesser when compared to the other financial instruments.

1.7 AWARENESS OF FINANCIAL PRODUCTS AND AGE GROUP OF THE RURAL

HOUSEHOLDS :

Data relating to the distribution of select rural households according to the awareness of financial products and

age are presented in Table – 1.3

TABLE 1.3

DISTRIBUTION OF SELECT RURAL HOUSEHOLDS ACCORDING TO AWARENESS OF

FINANCIAL PRODUCTS AND AGE

Financial

Products

Age

TOTAL Below 30 31-40 41-50 51-60

Above

60

Savings A/C 84

(97.7)

65

(98.5)

37

(94.9)

25

(100.0)

9

(100.0) 220

(97.8)

Fixed Deposit

A/C

46

(53.5)

24

(36.4)

17

(43.6)

5

(20.0)

4

(44.4) 96

(42.7)

Micro Finance 80

(93.0)

61

(92.4)

35

(89.7)

23

(92.0)

6

(66.7) 205

(91.1)

Personal Loan 55

(64.0)

42

(63.6)

18

(46.2)

10

(40.0)

4

(44.4) 129

(57.3)

Post Office

Saving Schemes 48

(55.8)

26

(39.4)

19

(48.7)

8

(32.0)

3

(33.3)

104

(46.2)

Secured Bank

Loan

55

(64.0)

43

(65.2)

19

(48.7)

15

(60.0)

4

(44.4) 136

(60.4)

Insurance 75

(87.2)

51

(77.3)

29

(74.4)

17

(68.0)

5

(55.6) 177

(78.7)

Shares 17

(19.8)

8

(12.1)

7

(17.9)

2

(8.0)

0

(0.0) 34

(15.1)

Bonds/

Debentures

18

(20.9)

6

(9.1)

6

(15.4)

2

(8.0)

0

(0.0) 32

(14.2)

Mutual Funds 15

(17.4)

6

(9.1)

6

(15.4)

2

(8.0)

0

(0.0) 29

(12.9)

Total Sample 86 66 39 25 9 225

Note : Figures in the parenthesis indicate percentages to the total sample

From the Table 1.3 it can be observed that,

i) The awareness of financial products is comparatively higher among the rural households in the age

group of below 30.

ii) Rural Households in the age group of above 60 are not aware of awareness of capital market

instruments like shares, bonds or debentures and mutual funds.

Asia Pacific Journal of Research Vol: I Issue XX, December 2014

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 90

1.8 AWARENESS OF FINANCIAL PRODUCTS AND EDUCATION OF THE RURAL

HOUSEHOLDS :

Data relating to the distribution of select rural households according to the awareness of financial products and

education are presented in Table – 1.4

TABLE 1.4

DISTRIBUTION OF SELECT RURAL HOUSEHOLDS ACCORDING TO AWARENESS OF

FINANCIAL PRODUCTS AND EDUCATION

Financial

Products

Education

TOTAL Uneducated

Under

Graduate Graduate Post Graduate Others

Savings A/C 99

(98.0)

99

(97.1)

17

(100.0)

2

(100.0)

3

(100.0) 220

(97.8)

Fixed Deposit

A/C

18

(17.8)

58

(56.9)

16

(94.1)

2

(100.0)

2

(66.7) 96

(42.7)

Micro Finance 91

(90.1)

95

(93.1)

15

(88.2)

2

(100.0)

2

(66.7) 205

(91.1)

Personal Loan 39

(38.6)

70

(68.6)

16

(94.1)

2

(100.0)

2

(66.7) 129

(57.3)

Post Office

Saving Schemes

26

(25.7)

60

(58.8)

15

(88.2)

1

(50.0)

2

(66.7) 104

(46.2)

Secured Bank

Loan

45

(44.6)

71

(69.6)

16

(94.1)

2

(100.0)

2

(66.7) 136

(60.4)

Insurance 64

(63.4)

92

(90.2)

16

(94.1)

2

(100.0)

3

(100.0) 177

(78.7)

Shares 2

(2.0)

19

(18.6)

12

(70.6)

1

(50.0)

0

(0.0) 34

(15.1)

Bonds/

Debentures

2

(2.0)

18

(17.6)

10

(58.8)

2

(100.0)

0

(0.0) 32

(14.2)

Mutual Funds 1

(1.0)

17

(16.7)

10

(58.8)

1

(50.0)

0

(0.0) 29

(12.9)

Total Sample 101 102 17 2 3 225

Note : Figures in the parenthesis indicate percentages to the total sample

From the Table 1.3 it can be observed that,

i) The awareness of financial products is considerably increasing with the level of education.

ii) The awareness of capital market instruments like shares, bonds or debentures and mutual funds

among the rural households is increasing significantly with the increase in the level of education.

1.9 AWARENESS OF FINANCIAL PRODUCTS AND INCOME OF THE RURAL HOUSEHOLDS :

Data relating to the distribution of select rural households according to the awareness of financial products and

income are presented in Table – 1.5

Asia Pacific Journal of Research Vol: I Issue XX, December 2014

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 91

TABLE 1.5

DISTRIBUTION OF SELECT RURAL HOUSEHOLDS ACCORDING TO AWARENESS OF

FINANCIAL PRODUCTS AND INCOME

Financial

Products

Income per month

TOTAL Less than

5,000

5001 -

10,000

10,001 -

15,000

More than

15,000

Savings A/C 149

(96.8)

52

(100.0)

14

(100.0)

5

(100.00) 220

(97.8)

Fixed Deposit

A/C

46

(29.9)

35

(67.0)

11

(79.0)

4

(80.0) 96

(42.7)

Recurring

Deposit A/C

12

(7.8)

8

(15.0)

6

(43.0)

2

(40.0) 28

(12.4)

Micro Finance 140

(90.0)

48

(92.0)

12

(86.0)

5

(100.0) 205

(91.1)

Personal Loan 78

(50.6)

36

(69.0)

10

(71.0)

5

(100.0) 129

(57.3)

Post Office

Saving Schemes

52

(33.8) 37

(71.0)

11

(79.0)

4

(80.0) 104

(46.2)

Secured Bank

Loan

78

(50.6)

42

(81.0)

11

(79.0)

5

(100.0) 136

(60.4)

Insurance 114

(74.0)

46

(88.0)

12

(86.0)

5

(100.0) 177

(78.7)

Shares 13

(8.4)

11

(21.0)

7

(50.0)

3

(60.0) 34

(15.1)

Bonds/

Debentures

13

(8.4)

10

(19.0)

6

(43.0)

3

(60.0) 32

(14.2)

Mutual Funds 10

(6.5)

10

(19.0)

6

(43.0)

3

(60.0) 29

(12.9)

Total Sample 154 52 14 5 225

Note : Figures in the parenthesis indicate percentages to the total sample

From the Table 1.5 it can be observed that,

i) The awareness of financial products among the rural households has increased considerably with

increase in the income levels. This signifies that the rural households with higher income are

considering financial products for investments and also for raising funds when needed.

ii) The awareness of capital market instruments like shares, bonds/debentures and mutual funds is more

among the rural households in the higher income group.

1.10 AWARENESS OF FINANCIAL PRODUCTS AND GENDER OF THE RURAL HOUSEHOLDS :

Data relating to the distribution of select rural households according to the awareness of financial products and

gender are presented in Table – 1.6

TABLE 1.6

Asia Pacific Journal of Research Vol: I Issue XX, December 2014

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 92

DISTRIBUTION OF SELECT RURAL HOUSEHOLDS ACCORDING TO AWARENESS OF

FINANCIAL PRODUCTS AND GENDER

Financial

Products

Gender TOTAL

Male Female

Savings A/C 141

(96.6)

79

(100.0) 220

(97.8)

Fixed Deposit

A/C

71

(48.6)

25

(31.6) 96

(42.7)

Recurring

Deposit A/C

22

(15.1)

6

(7.6) 28

(12.4)

Micro Finance 131

(89.7)

74

(93.7) 205

(91.1)

Personal Loan 91

(62.3)

38

(48.1) 129

(57.3)

Post Office

Saving Schemes

75

(51.4)

29

(36.7) 104

(46.2)

Secured Bank

Loan

96

(65.8)

40

(50.6) 136

(60.4)

Insurance 117

(80.1)

60

(75.9) 177

(78.7)

Shares 26

(17.8)

8

(10.1) 34

(15.1)

Bonds/

Debentures

26

(17.8)

6

(7.6) 32

(14.2)

Mutual Funds 24

(16.4)

5

(6.3) 29

(12.9)

Total Sample 146 79 225

Note : Figures in the parenthesis indicate percentages to the total sample

From the Table 1.6 it can be observed that,

i) The awareness of financial products among the male rural households is higher compared to the

female rural households.

ii) The awareness of capital market instruments like shares, bonds/debentures and mutual funds is more

among the male rural households.

1.11 AWARENESS OF FINANCIAL PRODUCTS AND MARITAL STATUS OF THE RURAL

HOUSEHOLDS :

Data relating to the distribution of select rural households according to the awareness of financial products and

marital status are presented in Table – 1.7

Asia Pacific Journal of Research Vol: I Issue XX, December 2014

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 93

TABLE 1.7

DISTRIBUTION OF SELECT RURAL HOUSEHOLDS ACCORDING TO AWARENESS OF

FINANCIAL PRODUCTS AND MARITAL STATUS

Note : Figures in the parenthesis indicate percentages to the total sample

From the Table 1.7 it can be observed that,

i) Majority of the households (97.8%) in different marital statuses are aware of saving bank account

followed by micro finance (91.1%).

ii) The awareness of capital market instruments like shares, bonds/debentures and mutual funds is higher

among the rural households who are unmarried.

1.12 AWARENESS OF FINANCIAL PRODUCTS AND OCCUPATION OF THE RURAL

HOUSEHOLDS :

Data relating to the distribution of select rural households according to the awareness of financial products and

occupation are presented in Table – 1.8

Financial

Products

Marital Status TOTAL

Unmarried Married Single

Savings A/C 22

(95.7)

195

(98.0)

3

(100.0) 220

(97.8)

Fixed Deposit

A/C

11

(47.8)

84

(42.2)

1

(33.3) 96

(42.7)

Recurring

Deposit A/C

4

(17.4)

23

(11.6)

1

(33.3) 28

(12.4)

Micro Finance 19

(82.6)

184

(92.5)

2

(66.7) 205

(91.1)

Personal Loan 10

(43.5)

118

(59.3)

1

(33.3) 129

(57.3)

Post Office

Saving Schemes

13

(56.5)

90

(45.2)

1

(33.3) 104

(46.2)

Secured Bank

Loan

11

(47.8)

124

(62.3)

1

(33.3) 136

(60.4)

Insurance 18

(78.3)

158

(79.4)

1

(33.3) 177

(78.7)

Shares 6

(26.1)

28

(14.1)

0

(0.0) 34

(15.1)

Bonds/

Debentures

8

(34.8)

24

(12.1)

0

(0.0) 32

(14.2)

Mutual Funds 6

(26.1)

23

(11.6)

0

(0.0) 29

(12.9)

Total Sample 23 199 3 225

Asia Pacific Journal of Research Vol: I Issue XX, December 2014

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 94

TABLE 1.8

DISTRIBUTION OF SELECT RURAL HOUSEHOLDS ACCORDING TO AWARENESS OF

FINANCIAL PRODUCTS AND OCCUPATION

Note : Figures in the parenthesis indicate percentages to the total sample

From the Table 1.8 it can be observed that,

i) The awareness of financial products is higher among rural households who are employed than the

rural households in other occupations. This signifies that the employed rural households are

considering financial products for investments and also for raising funds when needed.

ii) The awareness of capital market instruments like shares, bonds/debentures and mutual funds is higher

among the rural households who are employed.

Financial

Products

Occupation

TOTAL Employee Cultivation Business Retired

Cultivation

and Daily

Labour

Others

Savings A/C 21

(95.5)

8

(88.9)

79

(98.8)

4

(80.0)

28

(100.0)

80

(98.8) 220

(97.8)

Fixed Deposit

A/C

16

(72.7)

3

(33.3)

52

(65.0)

1

(20.0)

7

(25.0)

17

(21.0) 96

(42.7)

Recurring

Deposit A/C

7

(31.8)

0

(0.0)

15

(18.8)

0

(0.0)

3

(10.7)

3

(3.7) 28

(12.4)

Micro Finance 18

(81.8)

7

(77.8)

76

(95.0)

5

(100.0)

27

(96.4)

72

(88.9) 205

(91.1)

Personal Loan 19

(86.4)

4

(44.4)

61

(76.3)

1

(20.0)

13

(46.4)

31

(38.3) 129

(57.3)

Post Office

Saving Schemes

17

(77.3)

2

(22.2)

56

(70.0)

1

(20.0)

9

(32.1)

19

(23.5) 104

(46.2)

Secured Bank

Loan

17

(77.3)

4

(44.4)

64

(80.0)

1

(20.0)

18

(64.3)

32

(39.5) 136

(60.4)

Insurance 20

(90.0)

6

(66.7)

73

(91.3)

3

(60.0)

23

(82.1)

52

(64.2) 177

(78.7)

Shares 7

(31.8)

1

(11.1)

22

(27.5)

0

(0.0)

2

(7.1)

2

(2.5) 34

(15.1)

Bonds/

Debentures

6

(27.3)

1

(11.1)

21

(26.3)

0

(0.0)

1

(3.6)

3

(3.7) 32

(14.2)

Mutual Funds 6

(27.3)

1

(11.1)

20

(25.0)

0

(0.0)

1

(3.6)

1

(1.2) 29

(12.9)

Total Sample 22 9 80 5 28 81 225

Asia Pacific Journal of Research Vol: I Issue XX, December 2014

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 95

1.13 FINDINGS OF THE STUDY :

The major findings from the study of the major challenges of retail investors are summarized below :

i) Majority of the rural households (97.8%) are aware of Savings Bank A/C followed by micro finance

(91.1%).

ii) The awareness of capital market instruments like shares, bonds or debentures and mutual funds among the

rural households is lesser when compared to the other financial instruments.

iii) The awareness of financial products is comparatively higher among the rural households in the age group

of below 30.

iv) The awareness of capital market instruments like shares, bonds or debentures and mutual funds among the

rural households is increasing significantly with the increase in the level of education.

v) The awareness of financial products among the rural households has increased considerably with increase

in the income levels. This signifies that the rural households with higher income are considering financial

products for investments and also for raising funds when needed.

vi) The awareness of capital market instruments like shares, bonds/debentures and mutual funds is higher

among the rural households who are unmarried.

vii) The awareness of financial products is higher among rural households who are employed than the rural

households in other occupations

1.14 SUGGESTIONS :

From the findings presented above the following suggestions are offered to the government, the policy makers

to further strengthen the financial system in rural India.

1. Improving Awareness of Financial Products among Rural Households : The Government should

take necessary initiatives to further strengthen the awareness of financial products among rural

households in the country. The Government should involve all the public sector banks, post offices,

Insurance Companies and Capital Market Institutions for conducting Investor Awareness Programs in

Rural India.

2. Basic Financial Education in Adult Education Programs:The adult education programs conducted

by the Government authorities should also include the basic financial education. These programs

should impart the required knowledge for effective financial planning in the future.

3. Role of FLCCs in improving Financial Awareness :The Financial Literacy and Credit

CounsellingCentres (FLCCs) sponsored by the commercial banks set up in the rural areas should be

instructed by the Reserve Bank of India to conduct Financial Awareness regularly in the rural areas of

India aiming at improving financial literacy.

1.15 CONCLUSION

The improvement of awareness of financial products among the rural hoouseholds in India will growth of

financial system depends on the penetration of the financial products into the rural markets in the country. The

wider participation of rural households in financial markets will lead to increased financial deepening in Indian

Economy. The success of the “National Mission on Financial Inclusion”initiated by Sri NarendraModi,The

Prime Minister of India not just depends on the number of bank accounts that were opened in Prime Minister

Jan DhanYojana (PMJDY) scheme but on the government’s ability in enhancing the awareness of the various

financial products among rural households in the country.

Asia Pacific Journal of Research Vol: I Issue XX, December 2014

ISSN: 2320-5504, E-ISSN-2347-4793

www.apjor.com Page 96

BIBLIOGRAPHY 1Annamaria Lusardi(2005), “Financial Education and the Savings Behaviour of African-American and

Hispanics Households”, U.S. Department of labour, Employee Benefits Security Administration.

2C Thilakam(2012), “Financial Literacy among rural masses in India”, paper presented in the 2012

International Conference on Business and Management, 6 – 7 September 2012, Phuket – Thailand.

3FurqanQamar (2003), “Saving Behaviour and Investment Preferences among Average Urban Household”,

The Indian Journal of Commerce, Vol.56, No.1, January-March 2003, p. 36-49.

4FurqanQamar (2003), “Demographic Influences on Rural Households’ Saving and Investment: A Study of

Rural Households in the Ho Municipality of Ghana”, The International Journal of Applied Psychology, 2(4),

p. 41-46.

5SEBI – NCAER (2000), “How Households Save and Invest –Evidence from NCAER Household Survey ”,

SEBI, Mumbai.