b416 the evolution of global economies lecture 10 recent global economic crisis part 2

TRANSCRIPT

B416: The Evolution of Global Economies

Lecture 10: Recent Global Economic Crisis Part 2

Learning OutcomesBy the end of this lecture, you should understand the following:• Analyzes the origins, extent, and duration of the Global

Economic Crisis, which started in 2008 and took the world virtually by complete surprise, for different parts of the world in terms of collapsing trade flows and production levels, declining market value, and government response.

• Analyze various sources of the Global Economic Crisis and how global connections transferred problems from one part of the world to another.

• Analyze the response of governments to the Global Economic Crisis at the initial stages and the problems this created, particularly within Europe, at later stages.

2

Page 3

Overview of financial crises• We discussed the Global Economic Crisis starting in 2008/9 in

Lecture 9; this lecture focuses on crises more generally• The world economy is regularly confronted with financial crises

(e.g. Argentina 2002, Turkey 2001, Asia 1997)• This lecture explains what a financial crisis is and describes its

characteristics• It analysis two models of currency crises highlighting the role of

bad economic fundamentals and investors’ expectations • Furthermore, we look at the frequency, sequencing and costs of

currency and banking crises• Finally, it looks at a third generation model of financial crises that

integrates all views and characteristics into one coherent framework

Page 4

What is a currency crisis?• A currency crisis occurs if investors lose confidence in the

value of a currency such that they sell their investments denominated in that currency

• The typical currency crisis unfolds like the 1997 Asian crisisFirst there is mounting pressure on the exchange rate to

depreciate as investors sell their assets in the currencyThe monetary authorities try to prevent depreciation by raising

interest rates or through interventions (by selling their foreign exchange reserves for local currency)

Eventually, the monetary authorities have to give in and the currency depreciates steeply

Such a speculative attack can be largely self-fulfilling because the actions investors undertake, in the end vindicate their own doubts that started the attack

Page 5

Thai Baht example Thai Baht - US dollar xrate, inverted scale

10

20

30

40

50

1985 1990 1995 2000 year

exchange r

ate

July 1997

Page 6

What is a currency crisis?

• There can also be unsuccessful speculative attacks on a currency, when the monetary authorities overcome the pressure on the exchange rate

• Unsuccessful attacks can also be seen as a currency crisis given the costs involved in preventing a depreciation

• It can sometimes be puzzling why in seemingly identical cases, one country succumbs to a speculative attack, while the other country manages to escape a devaluation

• Capital mobility is a crucial requirement for a currency crisis to occur• If investors cannot switch between currencies or only at high transaction

costs, a currency crisis is virtually impossible• A currency crisis typically brings about a reversal of capital flows,

particularly in the case of emerging market economies• Typically there are large capital inflows preceding the crisis, following a

rapid reversal of capital flows as investors withdraw all their money at once

Page 7

Asian crisis example I

a. Current account balance (% of GDP)

-15

-10

-5

0

5

10

15

20

1990 1995 2000 2005 2010

Thailand

Malaysia

Indonesia

Page 8

Asian crisis example II

b. GDP per capita (PPP, constant 2005 international $)

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

1990 1995 2000 2005 2010

Malaysia

Thailand

Indonesia

1997 2002 2005

2003

Page 9

First generation models (1)

• In analysing currency crises we look at the following players:Private portfolio investorsMonetary authorities

• We assume that the monetary authorities want to maintain a fixed exchange rate and that economic decisions have been made under the assumption that this fixed rate is maintained in the future

• Models on currency crisis have two main defining dimensions:– Do investors merely react to a changed outlook of the

currency or do they themselves determine what this outlook looks like?

– Is the currency crisis due to inherent flaws of the economic fundamentals, or are currency crises purely speculative?

Page 10

First generation models (2)

• Foreign exchange reserves of the central bank are limited and with unchanged fiscal policy, a budget deficit financed this way will inevitably cause a currency depreciation

• Rational investors will not wait for this moment to happen as they can see what is coming when reserves run down

• They therefore ‘attack’ well before reserves are depleted by selling the domestic currency, further depleting the foreign exchange reserves of the central bank

• The crises occurs then, at some point in between the start of the budget deficit and the moment of reserves depletion

• Here, the investors simply bring forward in time an inevitable devaluation given the unsustainable fiscal and monetary policy of a country

Page 11

Some remarks on first generation models

• Currency crises do indeed tend to be the result of bad fundamentals (unsustainable policies)

• Speculative attacks are not random, they always occur with currencies that have doubtful fundamentalsEmpirical research shows that in the eighteen months up

to the crisis there is a significant fall in foreign exchange reserves

• The model explains why a crisis can occur quite suddenly and at a time when the authorities still seem able to maintain their fixed rate in the short run Investors lose faith that fiscal policy will ever be adjusted,

thereby triggering the crisis• The abruptness of a currency crisis in the model implies a

sudden reversal of capital flows, as we see empirically

Page 12

Second generation models (1)

• In the second-generation models, currency crises depend not only on economic fundamentals, but also on the behaviour and expectations of investors

• It is based on three core assumptions:Policy makers have a reason to give up the fixed

exchange rate (e.g. boost exports, reduce debt burden)Policy makers have a reason to stick to the fixed exchange

rate (e.g. benefits of pegging to a ‘hard’ currency)The costs of maintaining a fixed exchange rate increase if

a devaluation is expected (e.g. investors demand a higher interest rate to hold a currency)

Page 13

Second generation models (2)

• The first two assumptions imply the trade-off for the policy maker, there are costs and benefits to sticking to a fixed exchange rate

• The third assumption implies that investors determine where the policy maker is positioned on this trade-off.

• If investors have doubts on the sustainability of a fixed exchange rate, they will push the policy maker away from it by demanding a higher interest rate, which makes it more likely that the fixed exchange rate will be suspended

• These effects can be summarized in a social loss function H• The policy maker will attempt to minimize this function

Page 14

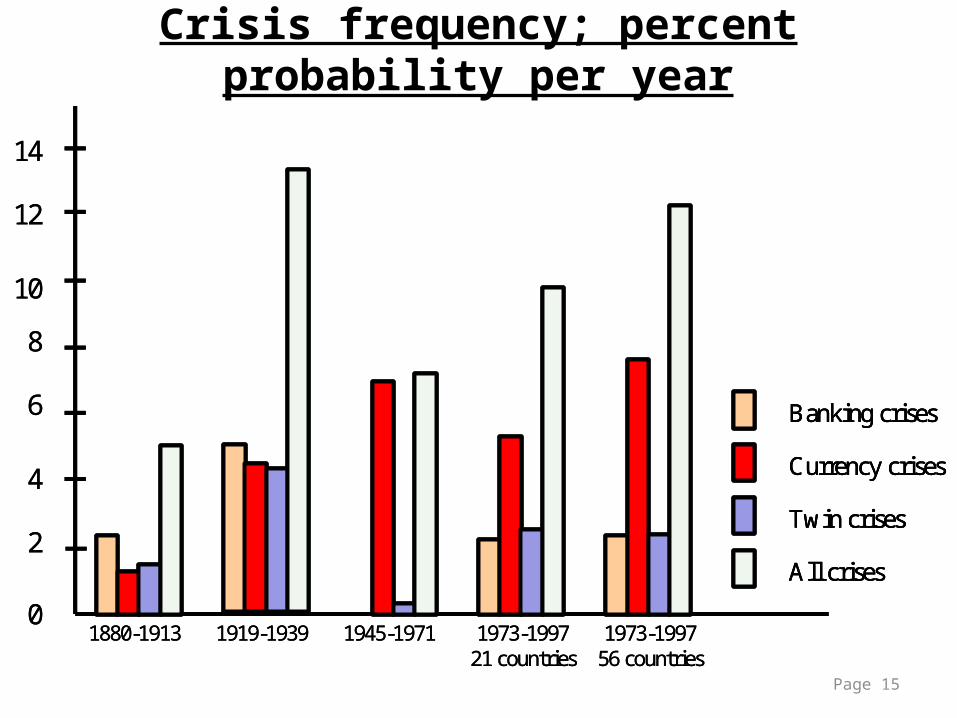

Frequency and measurement

• To identify a currency crisis, Eichengreen et al. have developed a widely used currency crisis indicator based on changes in the exchange rate, short-term interest rates and official foreign exchange reserves

• Based on this indicator, Bordo et al. show that currency crises have become more frequent in the free floating era. The increase in capital mobility surely plays a role here

• The bulk of empirical research concludes that currency crisis can be attributed to economic fundamentals being at odds with a fixed exchange rate (e.g. falling reserves, excessive money growth, high current account deficit)

• Contagion also plays a role in currency crises. If there is a crisis elsewhere, the probability of a crisis at home increases significantly, as investors expectations and behaviour change

Page 15

Crisis frequency; percent probability per year

0

4

8

12

1880-1913 1919-1939 1945-1971 1973-199721 countries

1973-199756 countries

Banking crises

Currency crises

Twin crises

All crises

14

6

2

10

0

4

8

12

1880-1913 1919-1939 1945-1971 1973-199721 countries

1973-199756 countries

Banking crises

Currency crises

Twin crises

All crises

Banking crises

Currency crises

Twin crises

All crises

14

6

2

10

Page 16

Contagion

Table 30.3 The incidence of global contagion, 1970-1998

probabilities (%) Other countries with

crises (share, %) unconditional (A) conditional (B) difference: (B) - (A)

0-25 29.0 20.0 -9.0

25-50 29.0 33.0 4.0

50 and above 29.0 54.7 27.7

Page 17

The costs of financial crises and sequencing• A currency crisis is a disruption in the currency market,

which leads to devaluation, a loss of reserves, higher interest rates and capital outflow

• Its domestic equivalent is a banking crisis, where the government has to step in to recapitalise insolvent banks

• It is customary to refer to a twin crisis if both a currency and a banking crisis occur at the same time (as they often do)

• Most crises occur in emerging markets, costing up to 20 percent of GDP. Typically, the costs increase from currency crises to banking crises to twin crises

• A discussion rages on the sequencing of crises. Do currency crises trigger banking crises or is it the other way around?

Page 18

Sequencing Stage I Banking crisis

Domestic financial fragility due to ill-devised financial liberalisation; under-regulated and over-guaranteed banks.

Large capital inflows; bank lending boom, but poor quality of bank loans. Banking sector increasingly vulnerable, possible bank runs.

1) Deterioration of firms and bank balance sheets.2) Drop in asset prices.3) Increase in uncertainty.1) + 2) + 3): Problems of asymmetric information increase.

Stage II Currency crisis

Loss of confidence (foreign) investors; pressure on the exchange rate.

Currency crisis and reversal of capital flows;4) Debt-deflation (debt in foreign currency).5) Interest rate increase.4) + 5): Further increase in problems of asymmetric information.

Stage I Banking crisis

Domestic financial fragility due to ill-devised financial liberalisation; under-regulated and over-guaranteed banks.

Large capital inflows; bank lending boom, but poor quality of bank loans. Banking sector increasingly vulnerable, possible bank runs.

1) Deterioration of firms and bank balance sheets.2) Drop in asset prices.3) Increase in uncertainty.1) + 2) + 3): Problems of asymmetric information increase.

Stage II Currency crisis

Loss of confidence (foreign) investors; pressure on the exchange rate.

Currency crisis and reversal of capital flows;4) Debt-deflation (debt in foreign currency).5) Interest rate increase.4) + 5): Further increase in problems of asymmetric information.

Page 19

Third generation models• In the debate on the root cause of currency crises,

fundamentals or self-fulfilling expectations, the third generation models offer a synthesis

• Aspects of both views are reconciled in a vicious circle

• Both views are right depending on where you start in this circle. Once you are in this vicious circle, the dynamics are the same

Loss of confidence

Domestic balance sheet problems

Currency depreciation

Page 20

Third generation models• It does matter where you start on the circle though, as the

policy implications are different• If self-fulfilling expectations are to blame (for example due

to contagion), capital markets are the main culprits, providing a possible rationale for restricting capital mobility

• If you start with domestic balance sheet problems, policies that would remedy weaknesses in the financial sector and stricter macro policies would be your recommendation

• The main improvements of the third generation models are: A larger and more direct role for self-fulfilling expectations An explicit analysis of the interaction between the domestic

financial sector and the exchange rate, necessary for analysing twin crises

Page 21

Conclusions• Currency crises have increased over time due to increased

capital mobility and possibly contagion• First generation models explain why a speculative attack

occurs even before the central bank runs out of reserves• Second generation models highlight the trade-off policy

makers face in possibly abandoning their fixed exchange rate, and the effect of investors’ expectations on this trade-off

• The economic costs of twin crises (currency and banking crises in tandem) are very high. Does a banking crisis cause a currency crisis or is it the other way around?

• Third generation models offer a synthesis of two views, showing the cause can be either weak fundamentals or self-fulfilling expectations. They are particularly well-suited to analyzing twin crises

Page 22

Euro area problems in the Global Economic Crisis

Selected Euro area countries; unemployment and inflation (%), 2010

-2

-1

0

1

2

3

4

5

6

0 5 10 15 20 25

unemployment

infla

tion

Netherlands

Luxembourg

Austria

Ireland

Greece

Spain

Drastically different unemployment and inflation developments

Page 23

Euro area problems in the Global Economic CrisisDrastically different government debts and deficits

Debt and deficit criteria and EU countries, 2010

0

3

6

9

12

0 30 60 90 120 150

Public debt (% of GDP)

Go

ve

rnm

en

t d

eficit (

% o

f G

DP

)

Euro area other EU countries max deficit max debt

Luxembourg

Finland

Sweden

Denmark

Greece

Italy

Portugal

UK

Belgium

France

Ireland

Page 24

Euro area problems in the Global Economic CrisisECB government bond purchases ; total balance, bn euro

0

100

M J J A S O N D J F M A M J J A

2010 2011

Greek crisis

Irish crisis

Portuguse crisis

Spain and Italy

0

100

M J J A S O N D J F M A M J J A

2010 2011

Greek crisis

Irish crisis

Portuguse crisis

Spain and Italy

Page 25

Government bond yields (%); selected countries, 1990 - 2011

0

5

10

15

20

25

1990 1995 2000 2005 2010

Germany

Italy

Germany

Greece

Spain

Greece

Euro area problems; benefits and credibility

benefits

credibility

Page 26

Conclusions

• Seventeen European countries have embarked on a unique process of monetary integration, culminating in the introduction of the euro currency

• We reviewed the process of monetary integration, the Maastricht criteria and the Stability and growth pact

• Of particular relevance for monetary integration is the theory of optimal currency areas, focusing on the ability of countries to weather asymmetric shocks or avoid these altogether

• We also looked at the benefits of a common currency, such as avoiding transaction costs and reducing uncertainty

• Finally, we discussed the workings of the Eurosystem and looked at the issues of extending the euro area and the credibility problems arising during the Global Economic Crisis

And Now…Work Outside the LecturePreparation

ForPadagogic

StylePreparation Time Budget

Individual Task

Group Task Output Week 10 Preparation Activity

Read Chapters 30 & 31 from International Econimics - 2nd Edition by Charles Van

Marrewijk, Oxford, ISBN 978-0-19-956709-6

Seminar 10 30 Minutes Read above Material + Seminar material

Workshop 10 1 HourOnline Collaboration Activities relating Final

Assignment

2 HourLecture 10

End of presentation

© Pearson College 2013