banned 1q13 results - il sole 24 ore · 1q13 results table of contents ... base and attract net new...

TRANSCRIPT

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

1Q13 Results

Milan, 9th May 2013

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

2

1Q13 Results Table of contents

1Q13 Highlights

Asset Management

Distribution

1Q13 Financials

Summary & Outlook

About Azimut

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

3

1Q13 Results

1Q13 Highlights

Asset Management

Distribution

1Q13 Financials

Summary & Outlook

About Azimut

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

4

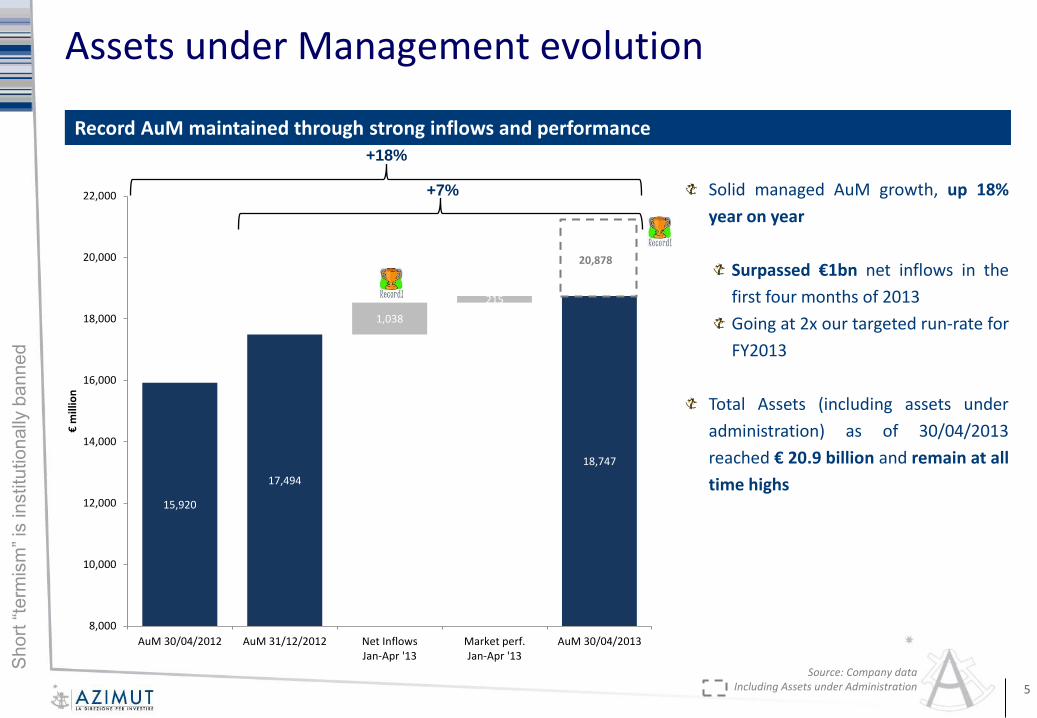

Growth path continues, delivered solid results in a volatile 1Q

Source: Company data

1Q13 Highlights

Financials:

Total revenues €112.2 million (vs. €136.0 million in 1Q12)

Rising recurring fees (€76.2 million vs. €73.8 million)

Variable fees in-line with past few quarters (€26.0 million), compared to an extraordinary 1Q12 (€54.4

million)

Net profit €41.4 million (vs. €63.3 million in 1Q12)

Net Financial Position €314.5 million (vs. €278.2 million as of FY2012 and €166.3 million at 1Q12)

Assets under Management & Inflows:

Total Assets at 1Q13: € 20.6 billion (+14% vs. 1Q12), of which € 18.4 billion AuM (+15% vs. 1Q12)

Total Inflows in 1Q13: €744 million (+27% vs. 1Q12)

At the end of April 2013, net inflows surpassed €1 billion, already achieving 67% of the FY 2013 target of

€1.5bn

GROWTH CONTINUES IN A CHALLENGING ENVIRONMENT, CONSIDERING 1Q12 WAS A RECORD QUARTER WITH EXTRAORDINARY VARIABLE FEES

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

15,920

17,494

18,532 18,747

1,038

215

8,000

10,000

12,000

14,000

16,000

18,000

20,000

22,000

AuM 30/04/2012 AuM 31/12/2012 Net InflowsJan-Apr '13

Market perf.Jan-Apr '13

AuM 30/04/2013

€m

illio

n

5

Record AuM maintained through strong inflows and performance

Source: Company data Including Assets under Administration

Solid managed AuM growth, up 18%

year on year

Surpassed €1bn net inflows in the

first four months of 2013

Going at 2x our targeted run-rate for

FY2013

Total Assets (including assets under

administration) as of 30/04/2013

reached € 20.9 billion and remain at all

time highs

Assets under Management evolution

+7%

+18%

20,878

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

6

1Q13 Results

1Q13 Highlights

Asset Management

Distribution

1Q13 Financials

Summary & Outlook

About Azimut

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

7

Source: Bloomberg Risk free: MTSIBOTR Index (net of 12,5% withholding tax)

Italian industry index: FIDMGEND Index

+3.1

+1.9

2013 YTD weighted average performance of our funds ahead of Italian industry and risk free: +2.9%

Asset Management - Performance

99

100

101

102

103

Ita. Industry Risk free AZM WAP

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

Source: Company data

Fund of Funds are quite entirely for asset classes not managed in house

Asset Management – Breakdown by type

8

31,2%30,6%30,3%29,9%28,9%28,6%27,1%27,2%27,1%26,3%27,1%26,5%25,5%26,1%26,6%26,2%26,2%26,0%27,1%27,3%27,2%26,8%26,9%26,8%27,2%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

FOFS IN HOUSE - LUX IN HOUSE - ITA

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

Source: Company data at 31/03/2013

Fund of funds have the same margin as in house funds

Luxembourg Funds breakdown

9

TARGET

FORMULA TARGET 2014, FORMULA TARGET 2015, INSTITUTIONAL TARGET, BOND TARGET 2015, BOND

TARGET GIUGNO 2016, INTERNATIONAL BOND TARGET GIUGNO 2016, BOND TARGET SETT. 2016, BOND TARGET DICEMBRE 2016, BOND TARGET EQUITY OPTIONS 2016

0-30% EQUITY F1 CONSERVATIVE, CORPORATE PREMIUM , CGM

OPPORTUNISTIC CORPORATE, CGM OPPORTUNISTIC GOVERNMENT, SOLIDITY

0-70% EQUITY EUROPEAN DYNAMIC, DIVIDEND PREMIUM, STRATEGIC

TREND

0-100% EQUITY

F1 ABSOLUTE, TREND, ITALIAN TREND, PACIFIC TREND, AMERICAN TREND, EUROPEAN TREND, LONG TERM

VALUE, CGM OPPORTUNISTIC EUROPEAN, CGM OPPORTUNISTIC GLOBAL, GLOBAL GROWTH SELECTOR

MARKET NEUTRAL F1 ALPHA PLUS, MARKET NEUTRAL

QUANT QBOND, QPROTECTION, QTREND, QINTERNATIONAL

MACRO MACRO DYNAMIC TRADING, GLOBAL MACRO

COMMODITIES COMMODITY TRADING

EQUITY LONG/SHORT ACTIVE SELECTION, CORE BRANDS

MULTI ACTIVE STRATEGY

CASH MANAGEMENT CASH OVERNIGHT, CASH 12 MONTH

OTHER OTHER SINGLE MANAGER (RMB OPP., CAT BOND, MACRO

VOLATILITY, GLOBAL CURRENCIES & RATES, ETC.)

FOFs MULTIMANAGER FOFs

0-30% EQ5.9% 0-70% EQ

2.3%

0-100% EQ14.5%

MKT NEU5.1%

QUANT.2.2%

MACRO1.4%

COMMOD.0.4%

EQ. L/S1.0%

MULTI0.1%

CASH MGMT5.2%

OTHER19.9%

FOFs28.9%

TARGET12.9%

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

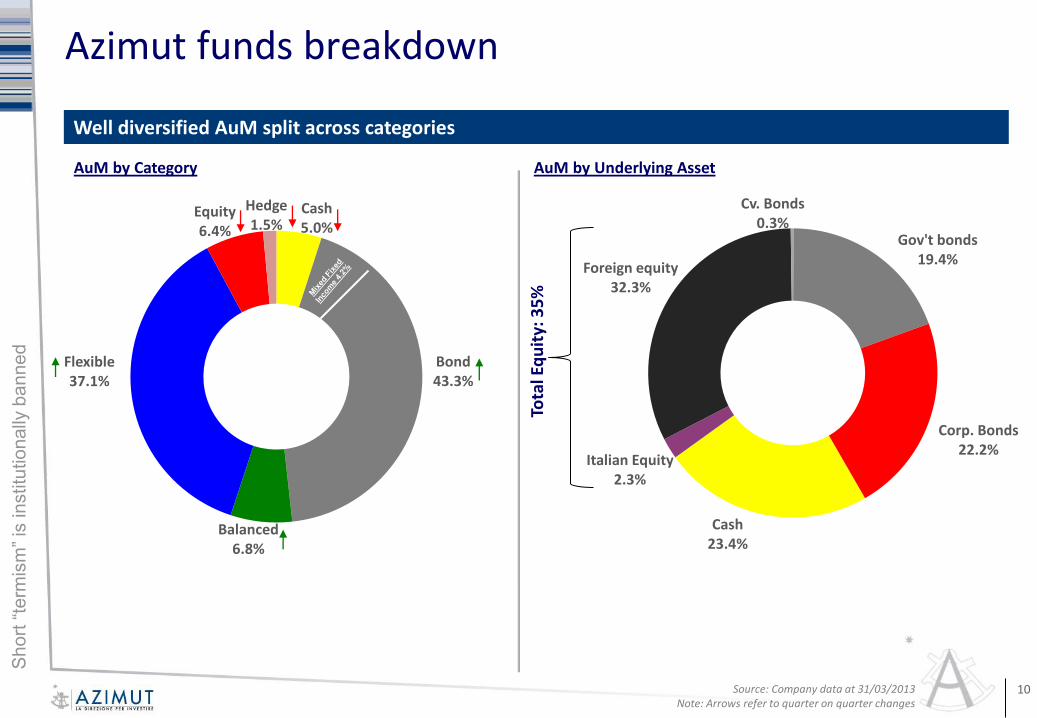

Cash5.0%

Bond43.3%

Balanced6.8%

Flexible37.1%

Equity6.4%

Hedge1.5%

Cash23.4%

Italian Equity2.3%

Foreign equity32.3%

Cv. Bonds0.3%

Gov't bonds19.4%

Corp. Bonds22.2%

Well diversified AuM split across categories

Source: Company data at 31/03/2013 Note: Arrows refer to quarter on quarter changes

AuM by Category

Azimut funds breakdown

10

AuM by Underlying Asset

Tota

l Eq

uit

y: 3

5%

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

Gov't €30.3%

Gov't extra €1.0%

Gov't USD4.5%

Other Gov't10.8%

Corp. BDS53.4%

Europe €42.9%

Other Europe5.3%

UK7.9%

USA25.7%

ASPAC11.1%

Other7.1%

Well diversified AuM split across categories

Source: Company data at 31/03/2013

Azimut funds breakdown

11

Equities Fixed Income

Austria, Belgium, Finland, France, Germany, Italy,

Netherlands

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

Share of new products launched since 2011

Despite a volatile market environment, new products have helped to defend the existing client base and attract net new money from existing and new customers

Innovation has and will be one of Azimuts’ key success factors

Share of new products launched since 2008

Product innovation: Azimut success story

12 Source: Company data at 31/03/2013

New products26,8%

Existing products73,2%

New products46,0%

Existing products54,0%

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

13

1Q13 Results

1Q13 Highlights

Asset Management

Distribution

1Q13 Financials

Summary & Outlook

About Azimut

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

14

Azimut Italian Funds’ Industry

Source: Company out of Assogestioni monthly figures Note *: CGM acquisition

2006 – 13 Funds’ net inflows as a % of total managed assets

Distribution - Funds

*

-5,0%

-4,0%

-3,0%

-2,0%

-1,0%

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

-5,0%

-4,0%

-3,0%

-2,0%

-1,0%

0,0%

1,0%

2,0%

3,0%

4,0%

5,0%

6,0%

Jan

-06

Mar

-06

May

-06

Jul-

06

Sep

-06

No

v-0

6

Jan

-07

Mar

-07

May

-07

Jul-

07

Sep

-07

No

v-0

7

Jan

-08

Mar

-08

May

-08

Jul-

08

Sep

-08

No

v-0

8

Jan

-09

Mar

-09

May

-09

Jul-

09

Sep

-09

No

v-0

9

Jan

-10

Mar

-10

May

-10

Jul-

10

Sep

-10

No

v-1

0

Jan

-11

Mar

-11

May

-11

Jul-

11

Sep

-11

No

v-1

1

Jan

-12

Mar

-12

May

-12

Jul-

12

Sep

-12

No

v-1

2

Jan

-13

Mar

-13

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

Launched in November 2009, the WM division is an important reality for Azimut:

135 Wealth Managers

8 external WMs, coming from top tier Italian and International Global Banks, added in 2013 alone (43 since the launch)

Successfully added teams of WMs with on average 2-3 people managing on average € 100 million

Target to reach €5.0bn AuM by the end of 2015

Continue to work to develop a broad product offering in order to meet wealth management requirements from a Personal, Family and Business perspective

Completed the first 3 years of activity reaching total AuM of €3.3 billion as of 1Q13

Distribution – Wealth Management Division

Source: Company data 15

FUND MANAGEMENT

INSURANCE PRODUCTS

DISCRETIONARY ACCOUNTS

BANKING SERVICES

WEALTH PLANNING

PORTFOLIO ANALYSIS

VENTURE CAPITAL

CHINA DESK

CORPORATE & INVESTMENT BANKING

CORPORATE ANALYSIS

TRUST

SUCCESSION PLANNING

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

16

Maintaining a high quality clientele to alleviate impact of the European sovereign debt crisis

Distribution – Clientele breakdown

Source: Company data as of 31/03/2013

Customers segmentation based on Assets

under Management volumes:

Smaller Wealth: below € 12,500

Medium Wealth: from € 12,500 to €

125,000

Affluent: from € 125,000 to € 500,000

High Net Worth Individuals: above €

500,000

Smaller Wealth

1.2% Medium Wealth16.7%

Affluent32.8%

HNWI49.3%

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

31/12/12* In Churn 31/03/2013

1,084 23 -1.2% 1,094

208 10 -1.2% 215

104 10 -2.9% 111

TOTAL 1,396 43 -1.4% 1,420

17

Note*: Already net of intercompany transfers. Churn includes retired FAs

Azimut continues to recruit top quality financial advisors from competition

Distribution – Recruitment of FAs

Source: Company data

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

1 3 5 7 9 11 13 15 17

1 3 5 7 9 11 13 15 17

18

Fly to quality: Top 3 by total inflows, notwithstanding significant differences in network size …

Distribution – 1Q13 Net Inflows in Italy

Source: Assoreti 31/03/2013 Note: network size is based on average Jan-Mar figures

Network size

Total inflows (€mln)

2337

831

4271

730

1408

682 645

4972

620 513 234 -13

1457 1843

1541

699

Banca Generali

Banca Fideuram

Fineco

Finanza & Futuro

Mediolanum

Allianz

UBI

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

100

150

200

250

300

350

400

450

500

0 500 1,000 1,500 2,000 2,500 3,000 3,500 4,000 4,500 5,000

1Q

13

In

flo

ws

pe

r FA

(€

'00

0)

1Q13 Avg n. of FA

19

… yet number 1 in FA productivity, almost doubling the industry average

Distribution – 1Q13 Net Inflows in Italy (cont’d)

Banca Generali

Banca Fideuram

Fineco

Finanza & Futuro Mediolanum

Allianz

Source: Assoreti 31/03/2013

INDUSTRY AVERAGE

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

20

1Q13 Results

1Q13 Highlights

Asset Management

Distribution

1Q13 Financials

Summary & Outlook

About Azimut

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

21

Consolidated reclassified Income Statement IAS/IFRS Compliant

Source: Company data

Income Statement

€/000 1Q13 1Q12 2012FY

Entry commission income 2,286 1,916 7,637Recurring fees 76,232 73,769 281,934Variable fees 26,049 54,444 119,714Other income 1,433 1,375 6,174Insurance revenues 6,190 4,484 18,114Total revenues 112,190 135,988 433,573Distribution costs (49,815) (42,545) (173,259)Commission on no load products (2,147) (4,668) (13,787)Personnell and SG&A (17,362) (15,597) (62,664)Depreciation, amort./provisions (989) (1,802) (6,704)Operating costs (70,313) (64,612) (256,414)Operating profits 41,877 71,376 177,159Interest income 3,348 2,628 10,508Net non operating costs (232) (127) (1,508)Interest expenses (794) (1,329) (4,488)Profit before tax 44,199 72,548 181,671Income tax (2,030) (8,260) (21,522)Deferred tax (673) (982) 162Net profit 41,496 63,306 160,311

Minorities 72 - (325)

Consolidated Net Profit 41,424 63,306 160,636

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

22

Treasury shares are not booked within the NFP

NFP at the end of March does not include:

€73mln dividends (May 23rd 2013)

Cash and Total debt at the end of March do not include :

€17.7mln subordinated bond partial repayment (July 1st 2013)

€30mln Senior loan partial repayment (June 30th 2013)

Consolidated reclassified Balance Sheet IAS/IFRS Compliant

Source: Company data

Balance Sheet

€/000 31/03/2013 31/12/2012 31/03/2012

Amounts due to banks: (86,694) (86,646) (100,161) Senior Loan (80,282) (80,301) (90,592)

Trademark lease-back (6,412) (6,345) (9,569)

Securities issued: (36,086) (35,664) (53,521)

Azimut 09-16 subordinated bond 4.0% (35,259) (34,823) (52,663)

Azimut 11-16 senior 2.5% (827) (841) (858)

TOTAL DEBT (122,780) (122,310) (153,682)

CASH AND CASH EQUIVALENTS 437,289 400,466 320,030

NET FINANCIAL POSITION 314,509 278,156 166,348

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

23

1Q13 Results

1Q13 Highlights

Asset Management

Distribution

1Q13 Financials

Summary & Outlook

About Azimut

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

24

On track to deliver our long term targets while remaining focused on profitability

Summary & Outlook

FINANCIAL RESULTS

Completed a solid 1Q13 notwithstanding uncertainties:

Growing recurring fees

Variable fees in-line with past quarters

Robust cash flow generation

Preserve profitability across asset classes

Continue generating strong cash flow to be returned to shareholders or used for potential M&A deals

Conserve a healthy balance sheet

PRODUCTION

Solid performance YTD of +2.9%

Launched successful new products (e.g. Bond Target Equity Options), gradually increasing the exposure to equity

Remain focused on product innovation

Gradual re-introduction of more equity-like products

Keep on delivering good performance in any market condition

DISTRIBUTION

Total Assets remains at all time highs

Record inflows in 4 months of activity 67% of FY2013 target already achieved

Assuming current market conditions, well ahead of our €1.5bn net inflow target for FY 2013

Confirm our €27bn AuM target by end-2014

Focus on network quality

INTERNATIONAL EXPANSION

Increased stake in Chinese partnership

Good progress in other countries

Evaluating opportunities in South-East Asia

South America remains a priority

What’s done Outlook

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

25

1Q13 Results

1Q13 Highlights

Asset Management

Distribution

1Q13 Financials

Outlook

About Azimut

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

26

Azimut Group structure

Source: Company data as at 30/04/2013 Note *: Under regulatory approval

100%

AZ IM (2011)

Azimut CM (2004)

Azimut Cons. (1988)

AZ Investimenti (2005)

AZ CM (2007)

Azimut Holding (Listed: AZM.IM)

Azimut Sgr (1986)

AZ Fund (1999)

AZ Life (2003)

Ass

et

Man

age

men

t

Life

in

sura

nce

s D

istr

ibu

tio

n

Azimut Fiduc. (2007)

Tru

ste

e

Apogeo Cons. (2008)

An Zhong (AZ) IM HK (2011)

An Zhong (AZ) IM (2011)

AZ International Holdings (2010)

100%

100%

100% 100%

100% 100%

100%

100% 100% 100%

100%

100%

AZ Global (2011)

5%+5%*

60%

Global Securities (2011)

CGM (2011)

51%

Katarsis CA (2011)

75%

Eskatos CM (2011)

100%

CGM SIM (2011)

100%

AZ Swiss (2012)

90%

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

Acquisition of Turkey’s Global Asset Management and Global Securities.

Acquisition of CGM, a Monaco-based independent asset management company.

Acquisition of Swiss company Katarsis Capital Advisors and its Luxembourg subsidiary Eskatos Capital Management. Eskatos is one of the 3/5 companies managing ILS (Insurance Linked Securities) funds domiciled in the EU.

Azimut and Siqurgest launch an asset management and distribution partnership in Switzerland targeting HNWI and Institutional clients.

Azimut and CMT launch An Zhong Investment Management in Hong Kong and Shanghai specializing in asset management and investment advisory

27

Azimut current presence

Azimut potential expansion

Aiming at covering all 3 macro areas (Americas, EMEA, Asia-Pacific) and time zones while offering a worldwide service to our clients

Where we are and where we want to be: 10% of AuM outside Italy by 2014

Going International

Azimut launches AZ Swiss joint venture with a team of portfolio managers in Switzerland focusing on macro strategies.

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

28

Azimut’s partnership philosophy has been

implemented also in China by involving local partners,

aligning the interests of all stakeholders.

An Zhong (AZ) Investment Management in Hong

Kong is the Holding company controlling two

operating subsidiaries. Azimut, through the Holding

company, oversees them and relocated three Senior

PMs from Luxembourg.

Through the operating subsidiaries Azimut aims at

creating a regional hub and developing local

production and distribution of asset management

products and investment advisory services with a

focus on qualified investors.

An Zhong (AZ) IM (2011)

AZ International Holdings

(2010)

100%

100%

AZ Investment Management (2011)

An Zhong (AZ) IM HK (2011)

100%

2010: Definition of a frame agreement with local entrepreneurs/partners

International expansion – China / HK

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

29

Global Securities (Trading + Distribution)

60%

Global Yatirim

Holding

40%

5%+5%*

AZ Global (Asset management)

75%

On 14th March 2011 AZ International Holdings S.A.

(“AIH”) signed a binding frame agreement with Global

Yatirim Holding and Global Portfoy Yonetimi (“GAM”) to

implement a partnership in the AM and distribution

business in Turkey.

In particular, AIH has purchased 5% of the distribution

company’s share capital (Global Menkul Değerler)

during its IPO on the Istanbul Stock Exchange while

Global Yatirim Holding holds around 75% of the capital.

Subsequently on 28th February 2012, through a capital

increase, Azimut has completed the acquisition of 60%

of the asset management company’s share capital,

Global Portföy, and on 17th January 2013 it increased its

stake in the distribution company from 5% to 10%*.

Through a team of dedicated Azimut people, Global

and Azimut are re-structuring the product range and

creating a sales force focused on the distribution of

mutual funds in order to attract new clients and AuM.

AZ International Holdings

(2010)

2011: Definition of a frame agreement with local entrepreneurs/partners (Global Investment Holdings)

International expansion – Turkey

Note *: Under regulatory approval

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

30

51% CGM

(Asset management)

On 10th May 2011 Azimut through its subsidiary AZ

International Holdings S.A. (“AIH”) signed a binding

frame agreement with CGM (Compagnie de Gestion

privée Monegasque); the acquisition of a 51% stake

has been completed on 30th December 2011

AuC of CGM stood at nearly €800m (o/w more than

€600m AuM) – consideration of ~€ 15m (including

shareholders’ equity) paid entirely with treasury

shares

The partnership adds new competences to Azimut

Group targeting UHNWI also thanks to CGM’s

operating subsidiary in Italy

Current CGM management entered Azimut’s

shareholders’ agreement

CGM Italia SIM

100%

AZ International Holdings

(2010)

2011: Agreement for a 51% stake acquisition

International expansion – Monaco

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

31

1988: Azimut is established by Akros Finanziaria

1990-1992: Pietro Giuliani and the most of the current top management join the company and start the recruitment of top level professionals for the distribution network (organised in 6 regional companies) and the fund managers team.

1998: Bipop-Carire acquires Azimut, which continues to operate independently.

December 2001: as a result of the Bipop restructuring, Azimut’s management buys out the business backed up by Apax Partners. Approximately 700 people invested in the MBO, completed in June 2002.

December 2002: the 6 regional distribution companies merged into Azimut Consulenza SIM.

July 2004: Azimut’s Initial Public Offering (AZM.IM)

20+ years of growth and evolution

Azimut pre-IPO history

Promotori

Azimut Holding

Azimut Piemonte

Azimut Centro-sud

Azimut Liguria-Toscana

Azimut Adriatica

Azimut Triveneto

Azimut Lombardia

20%

80%

Management and Promotori

Azimut Consulenza SIM

Azimut Holding

100%

35% 65%

Apax Partners

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

TIMONE25.0%

FREE FLOAT75.0%

32

Total shares issued: 143.3m

Source: Consob, May 2013

Free float breakdown

Timone Fiduciaria represents the shares of around 1,200 individual shareholders (Promotori, employees, managers working for Azimut), tied up in a strong shareholders’ agreement.

Treasury shares: in excess of 7.5% of share capital

Azimut’s shareholder base

2.9%2.4%

2.1%

2.1%

2.1%

7.5%

HARRIS ASSOC.

JPMORGAN AM

ALLIANZ

BANCO POPOLARE

AVIVA

WILLIAM BLAIR & CO.

CANTILLON CAP.

TREASURY SH.

OTHER

2.3%

2.0%

52%

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

33

A strong agreement for a long term commitment

Participants Promotori, employees and management organised in separate areas

Duration 3 years automatically renewed unless the absolute majority of the voting rights refuses. Already renewed in 2010 and 2013

Share lock-up 66%-75% of each participant’s shares are locked until retirement, regardless of the tenure within the Group

The residual 25%-34% can be sold at any time but subject to pre-emption right amongst other participants.

The price for this transfer is a 30 days rolling average.

Governance A share trust includes 100% of the voting rights of the participants.

A committee is responsible for managing and monitoring the participants’ obligations and rights under the agreement

Timone – the Shareholders agreement

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

34

Source: Company data as of 31/12/2012

Continuous growth throughout the decade, notwithstanding turbolent years

Main growth trend - Clients, FAs and AuM

0

4,000

8,000

12,000

16,000

20,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Total AuM (€m)

0

4,000

8,000

12,000

16,000

20,000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Managed AuM (€m)

60

80

100

120

140

160

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Clients ('000)

0

200

400

600

800

1000

1200

1400

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

FAs

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

35

Net inflows Performance

Note: Data in million € Includes managed assets only

AuM, Net Inflows and Performance

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

7,0018,221

11,052

13,281

14,897

12,147

13,881

14,61314,621

17,494

€m

illio

n

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

36 Source: Company data as of 31/03/2013

2008-2013 A beta stock with a strong P&L

Solid financial performance (€mln)

-70

-50

-30

-10

10

30

50

70

90

110

130

1Q082Q083Q084Q081Q092Q093Q094Q091Q102Q103Q104Q101Q112Q113Q114Q111Q122Q123Q124Q121Q13

REC. FEES VF SG&A OTHER COST

0

5

10

15

20

25

30

35

40

45

50

55

60

65

70

75

1Q082Q083Q084Q081Q092Q093Q094Q091Q102Q103Q104Q101Q112Q113Q114Q111Q122Q123Q124Q121Q13

REC. MARGIN VF

0

10

20

30

40

50

60

70

80

1Q082Q083Q084Q081Q092Q093Q094Q091Q102Q103Q104Q101Q112Q113Q114Q111Q122Q123Q124Q121Q13

OPERATING PROFIT

0

10

20

30

40

50

60

70

1Q082Q083Q084Q081Q092Q093Q094Q091Q102Q103Q104Q101Q112Q113Q114Q111Q122Q123Q124Q121Q13

NET PROFIT

Sh

ort

“te

rmis

m”

is in

stitu

tio

nally

ba

nn

ed

37

Disclaimer – Safe harbour statement

This document has been issued by Azimut Holding just for information purposes. No reliance may be placed for any purposes whatsoever on the information contained in this document, or on its completeness, accuracy or fairness. Although care has been taken to ensure that the facts stated in this presentation are accurate, and that the opinions expressed are fair and reasonable, the contents of this presentation have not been verified by independent auditors, or other third parties.

Accordingly, no representation or warranty, express or implied, is made or given by or on behalf of the Company, or any of its members, directors, officers or employees or any other person. The Company and its subsidiaries, or any of their respective members, directors, officers or employees nor any other person acting on behalf of the Company accepts any liability whatsoever for any loss howsoever arising from any use of this presentation or its contents or otherwise arising in connection therewith.

The information in this document might include forward-looking statements which are based on current expectations and projections about future events. These forward-looking statements are subject to risks, uncertainties and assumptions about the Company and its subsidiaries and investments, including, among other things, the development of its business, trends in its operating industry, and future capital expenditures and acquisitions. In light of these risks, uncertainties and assumptions, the events in the forward-looking statements may not occur. No one undertakes to publicly update or revise any such forward-looking statement.

The information and opinions contained in this presentation are provided as at the date of this presentation and are subject to change without notice.

Any forward-looking information contained herein has been prepared on the basis of a number of assumptions which may prove to be incorrect and, accordingly, actual results may vary. This document does not constitute an offer or invitation to purchase or subscribe for any shares and/or investment products mentioned and no part of it shall form the basis of or be relied upon in connection with any contract or commitment whatsoever.

The information herein may not be reproduced or published in whole or in part, for any purpose, or distributed to any other party. By accepting this document you agree to be bound by the foregoing limitations.

Vittorio Pracca tel. +39.02.8898.5853

Gabriele Blei tel. +39.02.8898.5849

Email [email protected]

IR Website www.azfund.com

IR Contacts Upcoming events

25 July 2013: Board of Directors approval of 1H 2013 results

7 November 2013: Board of Directors approval of 9M 2013 results

Contacts & Corporate calendar