bayernlb group investor presentation

TRANSCRIPT

BayernLB Group Investor Presentation

Munich, January 2021

2

The German banking system stands on 3 pillars

Private banks Public banks Co-operative banks

› DZ Bank (central institution)

› Credit co-operatives (878)

› Building and loan associations (1)

› Mortgage banks (2)

› Landesbanks (6) including BayernLB

› DekaBank

› Savings banks (386)

› Building and loan associations (8)

› Mortgage banks (2)

› Big banks (4)

› Deutsche Bank› DB Privat- und

Firmenkundenbank› Commerzbank› UniCredit Bank

› Regional and other banks (159)

› Branches of foreign banks (119)

› Building and loan associations (11)

› Mortgage banks (7)

Source: Bundesbank, Statistische Beihefte Bankenstatistik, p. 104; f igures as of 2018 adjusted by BayernLB Research excluding development banks

3

Strong owners

1 A body established under public law w hich is a legally dependent part of BayernLB

BAYERNLB HOLDING AG

~ 25% ~ 75 %

100%

Free State of Bavaria

1

100%

Institution established under public law

100% state

guarantee from the Free

State of Bavaria

Association of Bavarian Savings Banks

4

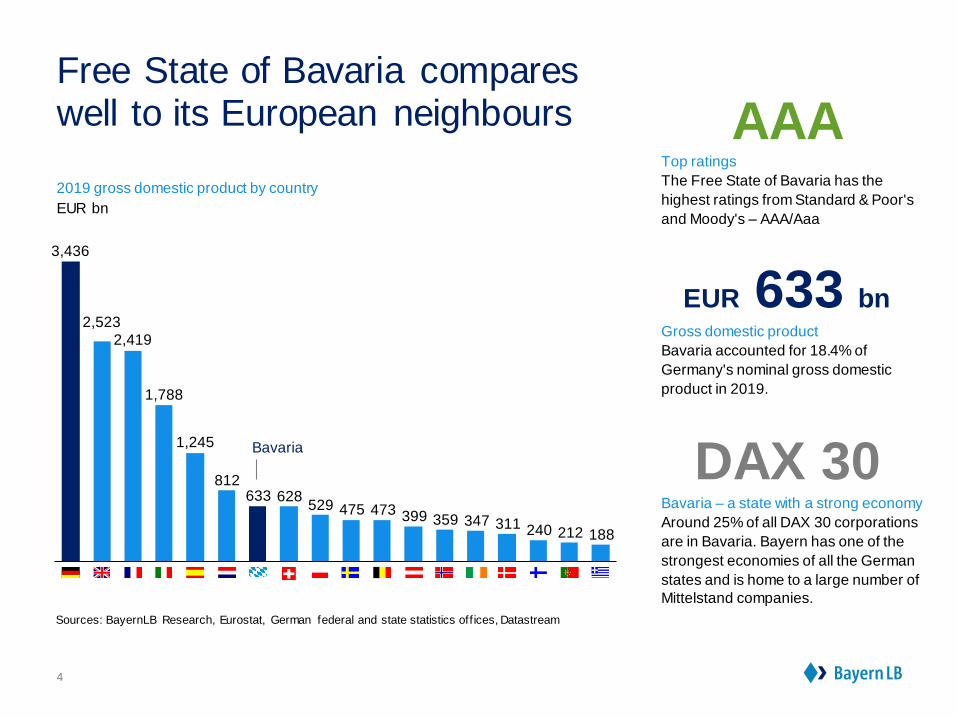

Free State of Bavaria compares well to its European neighbours

Sources: BayernLB Research, Eurostat, German federal and state statistics off ices, Datastream

2019 gross domestic product by country

EUR bn

AAATop ratings

The Free State of Bavaria has the

highest ratings from Standard & Poor's

and Moody's – AAA/Aaa

EUR 633 bnGross domestic product

Bavaria accounted for 18.4% of

Germany's nominal gross domestic

product in 2019.

DAX 30Bavaria – a state with a strong economy

Around 25% of all DAX 30 corporations

are in Bavaria. Bayern has one of the

strongest economies of all the German

states and is home to a large number of

Mittelstand companies.

812633 628

529 475 473 399 359 347 311 240 212 188

2,523

2,419

1,245

1,788

3,436

Bavaria

5

Savings banks – major customers and sales partners

Savings banks are the top financial

services providers throughout Bavaria

› 64 savings banks

› EUR 222.7 bn in total assets

› EUR 142.3 bn credit volume

› EUR 175.0 bn in customer deposits

› 36,621 employees and trainees

› 2,748 branches (incl. self service)

› 14.9 m savings, current and securities

accounts

As at: 31 December 2019

1. As a streamlined, specialised bank we are the reliable innovation

partner for companies in high-growth business sectors of the

future in particular in Bavaria and Germany, and support our

corporate customers sustainably and for the long term with in-depth

expertise

2. In real estate financing, we use our specialist knowledge and

network to support our customers throughout the entire value chain

in Germany and other selected markets

3. We are the central bank for the Bavarian savings banks and the

main bank for the Free State of Bavaria

4. As a tech bank, DKB provides its customers with an excellent client

experience and outstanding digital solutions

5. Our asset management companies Real I.S. and BayernInvest

enable our customers to choose from a wide variety of sustainable

investments

Our value proposition as the BayernLB bank of the future:

6

Our structure:three strong segments

Corporates & Markets DKBReal Estate /

Savings Banks & FI

› Special lender with in-depth

expertise in sectors of the

future

› Advanced structuring

expertise in financing:

structured asset finance and

debt capital markets (DCM)

› Streamlined offering of

Financial Markets’ risk

management products

› Reliable real estate lender with

special consulting expertise

in Germany and selected

foreign markets

› Central bank of the Bavarian

savings banks and a strong

partner to the public sector and

financial institutions

› Innovative tech bank,

which inspires its customers as

a digital companion and

sustainable partner

(#geldverbesserer)

› Strong earnings growth

through its target to double

customer numbers to 8 million

7

Support for your international activities thanks to around

1,100 correspondent banks in 100 countries

We are there for youat home in Bavaria and abroad

Representative office

Moscow

German Centres

Shanghai

Taicang

Germany

Munich

Nuremberg

Stuttgart

Frankfurt

Dusseldorf

Hamburg

Berlin

Leipzig

Foreign

branches:

London

Milan

Paris

New York

8

Munich head office

9

DKB –retail pillar of the BayernLB Group

DKB – Das kann Bank

Our products and services lead the market and are renowned

for their fair prices.

We provide an intelligent banking experience based on the

latest technology. Our retail customers carry out their daily

banking transactions conveniently and securely online. Our

business customers are served personally on location by our

sector experts.

› Approx. 4.5 m retail customers

› Germany’s second largest online bank

› The most sustainable of Germany’s top 20 banks (e.g. social

bond for retail customers, sustainability funds and the crowd

investing platform DKB-Crowd)

› In business with corporate and infrastructure customers, the

focus is on sectors with long-term growth potential in

Germany

› Financing partner for more than 4,000 municipalities,

administrative districts and municipal associations

DKB Group IFRS financial statements 30 June 2020

Total assets EUR 97.7 bn

Equity EUR 3.7 bn

Liabilities to customers EUR 65.4 bn

Net interest income EUR 477.6 m

Profit/loss before taxes EUR 118.0 m

RoE 7.4%

Convenient and secure –

DKB’s internet banking

DKB business customers –

personal service

10

BayernLabo –development bank of the BayernLB Group

Subsidised housing and municipal lending for Bavaria

BayernLabo has the legal mandate to promote social housing

and municipal construction in Bavaria. In addition, BayernLabo

issues government and municipal loans in Bavaria.

› The Free State of Bavaria is liable for all the liabilities assumed

by BayernLabo

› BayernLabo has a Aaa rating from Moody’s

› Solva 0 status

› LCR status level 1

› No bail-in risk

31 December 2019

Total assets EUR 18.0 bn

Own funds EUR 2.8 bn

CIR 48%

Employees 219 FTE

AaaBayernLabo’s rating

from Moody’s

BayernLabo –

a sustainably good company

› Stable operating performance: net interest income on par with year-

before period, net commission income higher

› Risk provisions raised to EUR 175 m to cover potential risks from the

coronavirus pandemic

› Strategic investments, particularly in IT infrastructure, cause rise in

administrative expenses

› Transformation continues on schedule despite operational challenges

from the coronavirus pandemic

› Solid capital base: CET1 ratio at 15.6%

BayernLB posts earnings before taxes of EUR 276 m

HIGHLIGHTS

11

12

Operating profit was stable

433

276

9M 2019 9M 2020

Profit/loss before taxesEUR m

Consolidated profit/lossEUR m

CIRIn %

RoEIn %

394

179

9M 2019 9M 2020

65.3

9M 2019 9M 2020

65.4 6.0

3.7

9M 2019 9M 2020

13

Capital base still sound

Total assetsEUR bn

RWAsEUR bn

CET1 capital EUR bn

CET1 capital ratio in %

Dec 2019 Sep 2020

226.0265.6

Dec 2019 Sep 2020

64.6 65.0

Dec 2019 Sep 2020

10.110.1 15.6

Dec 2019 Sep 2020

15.6

14

Net interest and net commission income up slightly on 9M 2019 at approx. EUR 1.5 bn

› Net interest income unchanged on the year-before

period despite the difficult climate

› Increase of approx. 9% on 9M 2019, due in

particular to new business

Net interest incomeEUR m

Net commission incomeEUR m

1,292

9M 2019 9M 2020

1,324 205 224

9M 2019 9M 2020

15

Risk provisions for expected charges from the coronavirus pandemic

› Earnings higher, boosted mainly by precious metals

business

Gains or losses on fair value measurementEUR m

(29)

73

9M 2019 9M 2020

› Risk provisions increased, in particular to cover

potential risks from the coronavirus pandemic

(post model adjustment)

› Year-before period buoyed by high releases and

recoveries on written down receivables

› Average NPL ratio remains low: 0.6%

Risk provisionsEUR m

(8) (175)

9M 2019 9M 2020

16

Increased administrative expenses due to investment, higher contribution to bank levy and deposit guarantee scheme

› Strategic investment, especially in modernisation of

IT at BayernLB and DKB

› Initial reductions in operating costs, mainly at

BayernLB core Bank

Administrative expensesEUR m

(1,135)(1,078)

9M 2019 9M 2020

› Expenses for the bank levy EUR 67 m

(9M 2019: EUR 56 m)

› Expenses for the deposit guarantee scheme

approx. EUR 83 m (9M 2019: EUR 68 m), mainly

due to higher secured deposits at DKB

Expenses for the bank levy and deposit guarantee schemeEUR m

(123) (150)

9M 20209M 2019

17

Segment results marked by positive earnings trend and risk provisions

DKB

241 234

› Expected drop in earnings at DKB resulting from

strategic investments in sales and digitalisation was

moderate, as it was softened by net positive risk

provisions and gains on measurement of equity

investments.

› Earnings in Central Areas & Others impacted

considerably by low one-off income, additional costs

to resolve the last legacy issues and higher

contributions to the bank levy and deposit guarantee

scheme.

› Increase in earnings in Real Estate & Savings

Banks/FI due to pleasing new business performance

in real estate and very good business with precious

metals. Earnings in the previous year were favoured

by releases of risk provisions.

› Positive earnings trend and savings in administrative

expenses in Corporates & Markets overshadowed by

risk provisions to cover potential risks arising from

the coronavirus pandemic.

Real Estate & Savings

Banks/Financial Institutions

19 (70)

Corporates &

Markets

165140

Central Areas &

Others

10 (28)

Profit before taxes by segmentEUR m

Note: the previous year’s figures in all segments apart from DKB have been changed following the BayernLB Group’s strategic realignment

9M 20209M 2019

18

CET1 ratio well above SREP minimum ratios

15,6

4,5

2,0

2,5

9,5

Sep 2020

CET1 ratio

0,5

2020

CET1 SREP requirement

› CET1 ratio of 15.6% on 30 September 2020 was

well above the SREP minimum ratio for 2020 of

9.5%

› The minimum CET1 ratio set by the CRR (Pillar 1

requirement) is 4.5%

› On top of that is an individual premium (Pillar 2

requirement) of 2.0% for 2020

› Additional capital buffers:

Capital conservation buffer: 2.5%: may be

temporarily undershot due to the corona crisis

Buffer for national, systemically important

institutions: 0.5%1

Buffer for national systemic relevance

Pillar 2 requirement

Pillar 1 requirement

Capital conservation buffer

1 Reduction of 0.5 percentage pointsfrom 1 December 2020

19

MREL requirement is significantly exceeded

MREL holdingsIn % of RWAs

› MREL holdings as at 30 Sep 2020 take account of

changes resulting from the banking package (e.g.

senior preferred and other MREL are no longer

eligible)

› Supervisory authority’s MREL requirement is 7.75%

of TLOF (equates to 25.34% of RWAs)

› MREL holdings as at 30 Sep 2020 stood at 14.38%

of TLOF (equates to 56.72% of RWAs), which far

exceeds the supervisory authorities’ requirements

› Large portfolio of subordinated eligible liabilities

(senior non-preferred) not only effectively protects

the superior senior preferred category from losses,

but also offers broad protection within the senior

non-preferred category

MREL holdings

30 Sep 2020

38.78

17.93

56.72

Senior non-preferred

Regulatory capital

Transformation process and outlook

Outlook

As it currently stands, BayernLB expects profit before taxes to be positive for

financial year 2020 – nevertheless the coronavirus pandemic and the related

challenges are the source of exceptionally high uncertainty. The negative

impact on global economic output will be considerable and will be greater the

longer the pandemic continues.

20

Progress with the transformation

Despite operational challenges posed by the coronavirus pandemic, the

BayernLB Group is forging ahead as planned with its extensive, multi-year

transformation programme Fokus 2024 launched in January 2020. BayernLB

has achieved key project milestones in the past few months and, for example,

launched various IT modernisation projects in the core Bank and DKB. In

addition, it has taken initial measures to improve earnings and profitability in

the Group’s business areas and implemented the first efficiency initiatives in all

units of the Bank, including, for example, redesigning the credit process and

optimising trading and transaction processes. The core Bank is on schedule

with reducing its operating costs.

21

We will continue to be a reliable

partner to our customers in

Bavaria and Germany.

We will remain the principal bank

to the Free State of Bavaria and

strong partner to the public

sector.

We will still be the central bank of

the Bavarian savings banks, firmly

rooted in the S-Finanzgruppe.

We will invest in infrastructure

and IT at the core Bank and DKB

and will set ourselves up as

modern and secure.

At the same time we will

considerably reduce our cost

base, especially in the core Bank.

We will increase the efficiency of

the platform in Munich and thereby

also support the ongoing growth of

our subsidiary, DKB.

We will further expand our position

in real estate finance and

structured asset finance.

We will focus on profitable and

future-oriented sectors in our

corporates and capital market

business.

We will double our customer base

in DKB’s retail business.

We will focus our business more

closely on sustainability.

How we will achieve sustainable success on our own terms in future

We are focusing on our

STRENGTHS

We are improving our

EFFICIENCY

We are a strong

PARTNER

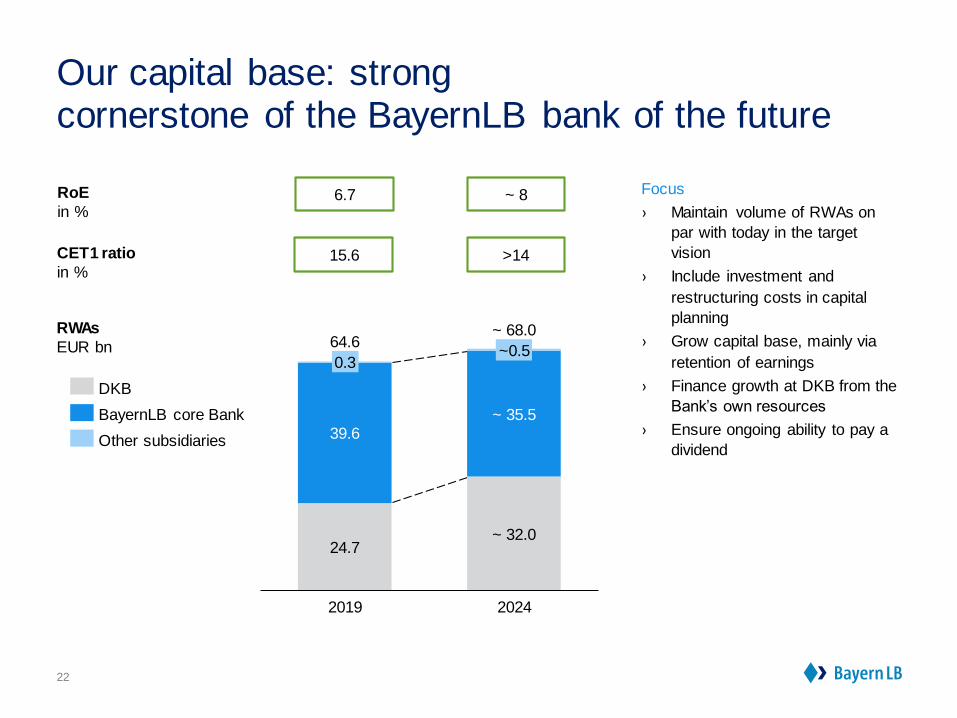

Our capital base: strongcornerstone of the BayernLB bank of the future

2019

~ 35.5

0.3

~ 68.0

~ 32.0

~0.5

2024

64.6

24.7

39.6

RWAs

EUR bn

15.6 >14CET1 ratio

in %

Focus

› Maintain volume of RWAs on

par with today in the target

vision

› Include investment and

restructuring costs in capital

planning

› Grow capital base, mainly via

retention of earnings

› Finance growth at DKB from the

Bank’s own resources

› Ensure ongoing ability to pay a

dividend

DKB

Other subsidiaries

BayernLB core Bank

6.7 ~ 8RoE

in %

22

Major investment in the future...

› Core Bank: Invest in further increasing sector expertise in

business with corporate, real estate and special

customers; in addition, invest a triple-digit million

sum in infrastructure and IT to significantly

increase the efficiency of the platform in Munich

› DKB: Invest EUR 400 m in growth and in the future over

the next five years, both to modernise and

upgrade the IT systems and to achieve

considerable growth in retail and business

customers

Considerably reduce costs in the core Bank by 2024

› Streamline activities in the capital market and

corporate lending business, incl. reducing the range

of products and complexity in the trading and credit

processes

› Generate savings in the central areas and in IT costs

by significantly simplifying the IT landscape

› In addition to the 400 job cuts agreed at the end of

2019, further socially responsible job cuts of a similar

scope are planned. However, the Bank has ruled out

redundancies until autumn 2022.

INVESTMENT COSTS

…and efficiency improvements

23

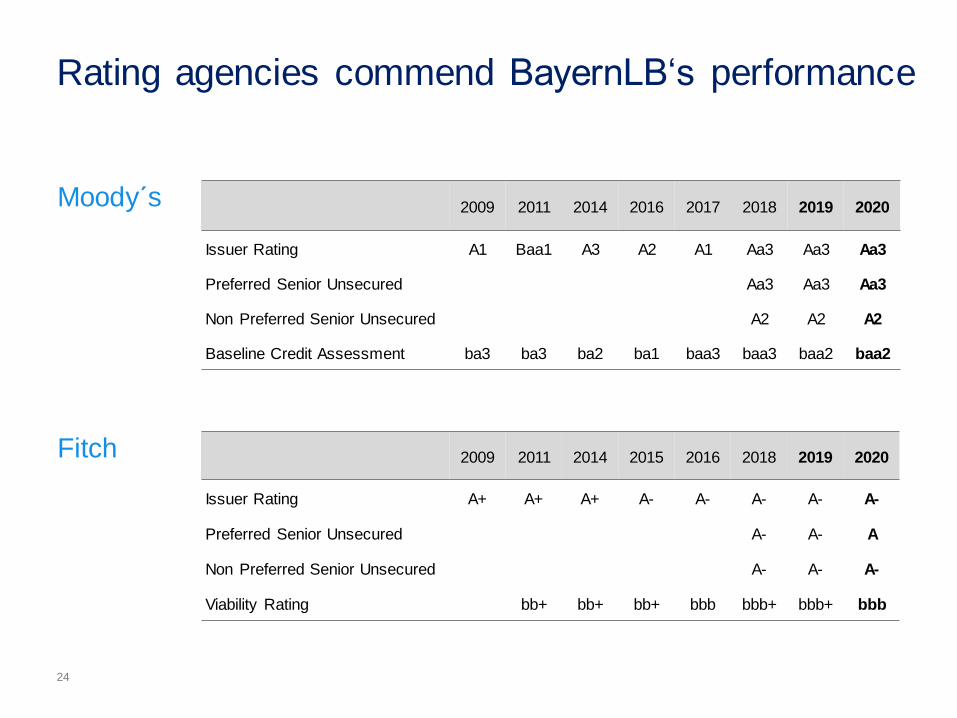

Rating agencies commend BayernLB‘s performance

Moody´s 2009 2011 2014 2016 2017 2018 2019 2020

Issuer Rating A1 Baa1 A3 A2 A1 Aa3 Aa3 Aa3

Preferred Senior Unsecured Aa3 Aa3 Aa3

Non Preferred Senior Unsecured A2 A2 A2

Baseline Credit Assessment ba3 ba3 ba2 ba1 baa3 baa3 baa2 baa2

Fitch 2009 2011 2014 2015 2016 2018 2019 2020

Issuer Rating A+ A+ A+ A- A- A- A- A-

Preferred Senior Unsecured A- A- A

Non Preferred Senior Unsecured A- A- A-

Viability Rating bb+ bb+ bb+ bbb bbb+ bbb+ bbb

24

25

Excellent asset quality

280 307

Dec 2019 Jun 2020

Gross credit volume

EUR bn

Credit portfolio

› Growth in lending in part due to participation in

the ECB tender (TLTRO III)

› Portfolio quality very high

› Impact of coronavirus pandemic still low

NPL ratio

In %

Dec 2019 Jun 2020

0.70.6

Rising quality

› NPL ratio and NPL portfolio shrank slightly in the

first half of the year and remain low

› Slight drop to 0.6% is the result of reducing

individual exposures

› Cover ratio stable at 42% without collateral

26

Well diversified credit portfolio

Gross credit volume by region

In %

› Germany EUR +26.7 bn

› Western Europe EUR +0.7 bn

81%11%

5%

Eastern Europe

Western Europe

Germany

North America 1%

Middle East

(EUR 1.5 bn, <1%)

Latin America/Caribbean

(EUR 0.6 bn, <1%)

Asia/Australia/Oceania

(EUR 1.7 bn, <1%)

Supranational orgs

(EUR 2.7 bn, <1%)

CIS

(EUR 1.0 bn, <1%)

Africa

(EUR 0.2 bn, <1%)

24%

18%

19%

11%

28%

Retail/Other

Corporates

Financial Institutions

Commercial Real Estate

Countries/Public Sector/

Non-Profit Orgs.

Gross credit volume by sub-portfolio

In %

› Countries/Pub. Sec.

/Non-Prof. Org.1 EUR +20.6 bn

› Financial Institutions EUR +3.2 bn

› Commercial Real Estate EUR +2.2 bn1 Growth in part due to participation in the ECB tender (TLTRO III)

27

Very high investment grade share

Gross credit volume by rating category

EUR bn / %

MR 0 - 7 MR 12-14MR 8-11

178.3

MR 15-18

201.2

MR 19-21 MR 22-24

7.0

65.2

1.3

68.9

25.8 26.47.6 1.4 2.0 1.9

Dec 2019: Total EUR 279.7 bn

Jun 2020: Total EUR 307.3 bn

87.9%investment grade

Investment grade Non-investment grade Default categories

28

Highly granular

Net credit volume

EUR bn / %

EUR 1 bn to

EUR 2.5 bn

3.2

> EUR 2.5 bn EUR 250 m to

EUR 500 m

57.5

EUR 50 m to

EUR 100 m

EUR 500 m

to EUR 1 bn

EUR 100 m to

EUR 250 m

EUR 5 m to

EUR 50 m

Up to EUR 5 m

37.2

19.1

38.2

16.3

3.3

17.220.8

26.9

36.0

24.8 21.7

54.4

35.3 35.4

Jun 2020: Total EUR 235.2 bn

Dec 2019: Total EUR 212.2 bn

76% up to EUR 500 m

› Considerable growth posted in the “> EUR 2.5 bn” size category, as balances held with central banks

were increased at Deutsche Bundesbank

› The portfolio remains highly granular and a very high volume of EUR 151 bn still falls under the size

categories up to EUR 0.25 bn

29

Diversified corporate customer portfolio which maintains a high investment grade share

Corporates by sector

EUR bn

› Business volume grew by EUR 760 m

› Investment grade share remains very high at 74.9% and is only down slightly due to the coronavirus

pandemic

Chemicals,

pharmaceuticals & healthcare

Raw

materials, oil & gas

8.5

Utilities Consumer

goods, tourism,

wholesale & retail

Logistics

& aviation

Mechanical

engineering, aerospace

& defence

Telecoms,

media & technology

Automotive Construction

23.7 24.2

8.4 7.9 8.2 7.5 7.4 6.7 5.55.46.5 5.6 5.7 5.3 5.23.5 3.8

Dec 2019: Total EUR 74.1 bn

Jun 2020: Total EUR 74.9 bn

30

Commercial real estate finance

Gross credit volume by asset class/unit

EUR bn/Jan 2020

Highlights

› Portfolio was expanded as planned by EUR 5.2 bn

to EUR 55.5 bn

› Granular portfolio with 88% share in Germany

› Residential asset category includes around EUR

21.5 bn (previous year: EUR 19.0 bn) of low-risk

business due to local authority/government

ownership or guarantees and housing associations

› 85% investment grade share

› 70% of the cash flow generating gross exposure

(GEX) has a debt service capacity of > 8% p.a.

› Expected loss at 5 bp; stable trend

› Low average NPL ratio of 0.4%

Outlook

› Pursue a clearly defined, well considered growth path

in Germany and abroad with increasing risk

diversification within the real estate portfolio

› Realise growth in foreign business by using existing

infrastructure via foreign branches and local networks

while maintaining the current portfolio and risk profile

› Breakdown of asset classes in the target portfolio will

remain almost unchanged

6.4

Residential

25.4

Office

2.5

RetailManaged

real estate

34.4

6.5

9.7

2.9

3.54.4

BayernLB BayernLaboDKB

31

Private residential construction term loans

Gross credit volume by unit

EUR bn/Dec 2019

Distribution in Germany

Granular portfolio with focus on Bavaria, mainly due

to BayernLabo

Outlook for DKB

Credit volume will increase from 2020. New business

will be managed in a targeted manner to improve

efficiency through higher loan amounts per

application

2018

0.4

20192017

14.0

0.3

14.7

0.2

13.7

3.5

10.8

3.3

10.4

3.2

10.3

BayernLB DKB BayernLabo

Highlights of the DKB portfolio

› Average ticket size (entire portfolio): EUR 144 k

› Average ticket size (new business): EUR 223 k

0.3

1.5

0.7

0.40.5

0.5

0.70.7

0.90.8

Volume (EUR bn)

0.5

1.04.8

0.1

0.1

32

Comfortable liquidity levels

Capital market funding

EUR bn/BayernLB core Bank not incl. BayernLabo

Funding strategy

› Lower funding needs in 2020 are the result of the

streamlining of BayernLB core Bank and the

related reduction in requirements

› Slight uptick in funding volumes in 2021 due to

planned new business

› Focus on unsecured funding at BayernLB level

using diversified sources of funding, especially

via the savings banks, institutional investors,

retail and the international DIP scheme

› Maintain capital market presence by regularly

issuing secured benchmark bonds

› EUR 27bn participation in TLTRO III ECB tender

(BayernLB and DKB)

› Liquidity coverage ratio (LCR): 233% as at Sep

2020

Issued Planned

2018

6.14.2

5.14.0

0.0

3.5

2019

4.5

2020

3.8

2.3

2021e

8.2 8.6

4.5

Secured Unsecured

33

Investor-friendly structure on the liabilities side

Liabilities structure

EUR bn/Jun 2020

71.6

1.7

112.1

43.3

17.7 11.6

balance

sheet total

258.0

Securitised liabilities

Liabilities to customers

Liabilties to banks Other liabilities

Subordinated capital

Equity

Of which

Pfandbriefs

Of which

unsecured debt

instruments under Section

46 f KWG

4.6

Of which

structured debt

instruments under Section

46 f KWG

29.430.2

Funding via Pfandbriefs

› BayernLB uses a total of four funding

programmes based on the German Pfandbrief

Act (PfandBG) as a low-cost, long-term source of

funding, two each at BayernLB and DKB AG

Broad base of unsecured liabilities

› BayernLB has an investor-friendly structure on

the liabilities side with sufficient unsecured bonds

in relation to total assets. The Bank actively

monitors and plans the proportion of unsecured

bonds in accordance with Moody’s Loss Given

Failure-Analysis

34

BayernLB Pfandbriefs

Public Pfandbriefs

The majority of the cover (>90%) consists of German

municipal finance and receivables guaranteed by

German states with a focus on Bavaria. Tap issues

and jumbolinos are issued on a regular basis to

maintain a liquid Pfandbrief curve.

Mortgage Pfandbriefs

Cover mainly includes commercial real estate,

primarily residential, office and retail with a focus on

Germany. The high overcollateralization provides

freedom to launch issues across all maturity bands.

Key figures for Q3 2020

Outstanding volume EUR 3.9 bn

Moody’s rating Aaa

Excess cover 140.6%

Cover pool Germany EUR 6.1 bn

Cover pool abroad EUR 3.0 bn

Key figures for Q3 2020

Outstanding volume EUR 17.9 bn

Moody’s/Fitch rating Aaa/AAA

Excess cover 28.3%

Cover pool Germany EUR 21.2 bn

Cover pool abroad EUR 1.3 bn

A Group with a strong sustainability background

35

Legally dependent institution

established under public law w ithin

BayernLB

~ 25 % ~ 75 %

Free State of Bavaria

100 %

Institution established under public law

100 % state

guarantee from the Free

State of Bavaria

Association of Bavarian Savings Banks

Focus areas of the

Bavarian Sustainability

Strategy

› Climate change

› Sustainable energy

› Natural resources

› Sustainable mobility

› Social cohesion

› Education and research

› Sustainable economy

and consumption

› Nutrition, health, care

› State and administration

› Sustainable financial

policy

› Global responsibility

BayernLB has a mandate geared towards sustainability based on the approach of the Free State of Bavaria and the

EU Taxonomy. To this end, all issuing entities have established a green and/or social framework

36

› BayernLB has been actively engaged in the promotion of sustainability for

25 years, achieving numerous milestones along the way

› Signing UNEP-Finance Initiative ("Environmental Banks") in 1995,

commitment to World Bank standards in 2004, regular and detailed

sustainability reporting since 2007, signing of UN Principles for

Responsible Investment (PRI) by BayernInvest in 2011, first DKB

Green Bond in 2016, BayernLabo Social Bond in 2017, first DKB

Social Bond in 2019 and BayernLB Sustainable Finance Framework

in 2020 (formerly “Green Bond Framework”) with subsequent Green

Bond issues for retail customers

› In 2019 the bank cemented sustainability as a core building block of its

new strategy, further strengthening its commitment to a sustainable future

› The bank is already one of the largest financiers of renewable energies in

Germany and has extensive expertise and market knowledge in European

and non-European markets

› The leading ESG rating agencies confirm BayernLB's commitment to

sustainable development, which is well above the industry average

› BayernLB’s subsidiary DKB also shows top performance. It has been rated

separately since 2015 and is currently rated "B-", the best rating in its

industry and thus the "Industry Leader". The development bank

BayernLabo also receives a separate rating and qualifies for prime status

Position of BayernLBPromoting sustainability

BayernLB, DKB and BayernLabo

are ranked among the leading,

sustainable banks in their sectors

Industry Leader

Awarded by ISS ESG (formerly

ISS Oekom) and held by

BayernLB since 2006 (first

sustainability rating in 2000)

Prime Status

D- D D+ C- C B-C+

Prime

37

Overview Details

Assessment and selection of

projects lead by Sustainability

Working Group

Sustainable Loan Pool

(currently 2.45 EURbn)

Annual impact and

allocation reporting

Plain/structured

bonds/Schuldschein

loans

Commercial paper

BayernLB’s Sustainable Financing Framework

Use of Proceeds

› In the first phase, only renewable energy projects are included in

the Sustainable Loan Pool. In the second phase, mass public

transportation as well as green real estate will be added

› All assets in the pool contribute significantly to the UN Sustainable

Development Goals

Process for Project Evaluation and Selection

› Assets are assessed in a two-step process with credit departments

proposing a project/loan and the Sustainability Working Group

deciding on its merit

Management of Proceeds

› Proceeds from sustainable issuances are managed by Group

Treasury within the general liquidity pool while ensuring that the

sustainable asset pool surpasses all outstanding sustainable

funding in volume (i.e. portfolio approach)

Reporting

› BayernLB will publish an annual impact and allocation reporting

containing details of the asset pool (volume, geographical/

technological split, capacity installed, CO2 avoided) and details of

the issued sustainable securities

Significant contribution!

Framew ork and second party opinion are available on our Investor-Relations-Homepage

38

Overall Sustainable Loan Portfolio Technological split (in EURm)

Geographical split

Renewable Energy Portfolio

6%

31%

18%

27%

18%Germany

Italy

UnitedStatesUK

Others

11%

20%

22%19%

22%

6% Germany

United States

Turkey

UK

Canada

Others

Solar Wind

97%

3%

Photovoltaik

87%

13%

On-Shore

Off-Shore

› The renewable energies portfolio of

BayernLB (without DKB) comprises 1.6

EURbn in wind energy projects as well

as 860 EURm in solar power plants

› Clear focus on Western and Northern

Europe but also significant exposure in

the United States and Canada

Comments

1,610 EURm

860 EURm

Solar Wind

Information based on data provided for the second party opinion.

39

Sustainability Ratings of the Group

ISS ESG Sustainalytics imug MSCI ISS ESG imug ISS ESG

Rating C+ 68 Points 48,69 % AA B- 43,61% C+

Ranking /

Investment Status

„Prime“

(Rank 7 out of 252

Banks)

77 out of 340

Unsecured

bonds "neutral" (CCC)

Public Pfandbriefs

"positive" (BBB) Mortgage

Pfandbriefs "positive" (BB)

Above

industryaverage

„Prime“

Public

Pfandbriefs „very

positive" (A) Mortgage

Pfandbriefs "positive"

(BBB)

„Prime“

Industry

averageD 60 Points 50,99 % A D 21,45% n/a

Range A+ to D- 0 - 100 Points 0% - 100 % AAA to CCC A+ to D--100 % -

100 %A+ to D-

Benchmark

252

„Financials/ Public &

Regional Banks"

340 „Banks“24 „Savings

Banks“

MSCI ACWI

Index constituents,

Banks, n=200

281

„Financials/ Public &

Regional Banks"

57 Banks

„Financials/

Mortgage & Public Sector

Finance"

Date 01 / 2020 06 / 2019 03 / 2020 10 / 2020 01 / 2020 03 / 2019 12 / 2019

› Projects and all related goods and services for mining or extracting nuclear fuels and constructing new nuclear

power plants are excluded from financing, while companies that generate their sales exclusively from products

and services employed in the excluded areas are excluded from general corporate financing

40

Selected BayernLB policies for critical sectorsN

ucle

ar

Weapons

Fossil

Fuels

Food

› Excluded from financing in particular are projects that are harmful to the climate or the environment. For

example, financing is not provided for the construction of new coal-fired power plants or to extract natural gas

or crude oil through fracking or extraction from tar sands. Companies that generate their sales exclusively from

products and services employed in areas excluded from financing by the financing guidelines are excluded

from corporate financing

› BayernLB Group does not engage in speculative transactions in staple foods. In this vein the Group does not

invest directly in staple foods, nor indirectly in derivatives which replicate or speculate on the price performance

and/or shortages of staple foods. Furthermore, the bank does not offer any investment products which replicate

or speculate on the price performance and/or shortages of staple foods

› BayernLB recognizes the right of a state to defend itself. On this basis, offering services to arms companies or

individual financial transactions for weapons and armaments is in principle possible within the framework of

existing laws. We require that the financing is approved following an mandatory case-specific examination

› With BayernLB’s new strategic focus defense ceased to be a focus sector at the end of 2019 and will be

scaled down over the long term

BayernLB observes the World Bank’s environmental and social standards in all relevant financing transactions. These

are based on the performance standards of the World Bank Group’s International Finance Corporation (IFC) and the

World Bank's Environmental, Health, and Safety (EHS) Guidelines.

More details are available in our 2019 Annual Report (link to f inancial reports)

Disclaimer

42

The information in this presentation constitutes neither an offer nor an invitation to subscribe to or purchase securities or a

recommendation to buy. It is solely intended for informational purposes and does not serve as a basis for any kind of obligat ion,

contractual or otherwise.

Rounding differences may occur in the presentation.