bci – industrial battery forecastc.ymcdn.com/sites/batterycouncil.org/resource/collection/...na...

TRANSCRIPT

Presented at the 127th Convention of Battery Council International May 3-5, 2015

North American Industrial Battery Forecast 2015-2017

Mitch Bregman Division President Energy and Industrial Systems

Thank You Industry Experts

• Sean Blayloch - Exide

• Doug Bouquard – East Penn

• Bruce Cole – Exide

• Taylor Frederickson - Exide

• John Gagge – EnerSys

• Jim Garcia – Exide

• Gary Gray – EnXergy

• Vincent Halma – Kion

• Jerry Hoffman – NorthStar

• Sam Jaffe – Cairn ERA

• Mark Jesko – Exide

• Scott Johnson – Clark

• Mark Kelley – Crown Battery

• John Kleba – Midtronics

• Manfred Kleinert – Exide Europe

• François Linck – Saft

• Jeff Long – EnerSys

• Saeed Mahramnia – Schneider Electric

• Jim Marshall – Emerson

• Chuck Mathias – East Penn

• Mike Nispel – C&D Tech

• Jay Northey – GS Battery

• Doug Pierce –Yuasa

• Chad Uplinger – EnerSys

• Steve Vechy – EnerSys

• Mark Wels – East Penn

• Brett Wood – Toyota

• John Wood - Ecoult

1

Data Collection Methodology

• Sales data include lead-acid battery sales of reporting BCI members

• Imports from non-reporting companies are not included

• Stationary products include batteries 25Ah and above

• Lead prices assumed to be stable during forecast period

• Stationary 2013 market segment data corrected, total market remains unchanged

• 3-Year industry forecast is an accumulation of the forecast from individual reporting members

2

Macro Industrial Battery Market Drivers

Source: Industry Experts 3

Environmental Awareness

Global Economy

Alternative Technologies

Motive Power

4

NA Motive Power Battery Market 2014

$700

$750

$800

$850

$900

$950

$1,000

$1,050

$1,100

2013 2014

Sale

s $

MM

Industrial Truck Railroad Mining

Segment 2014

Actual Growth

Last Year BCI Fcst

Ind. Truck 9.5% 4.2%

Railroad 22.1% 4.8%

Mining -20.7% 2.1%

TOTAL 9.4% 4.2%

2014 Motive Power Sales Grew 9.4% with Strong Economy Industrial Truck is 95% of Motive Power Market

Drivers

North America Economy

User Productivity / Solution Selling

Source: BCI, Industry Experts

$949

$1,038

5

Quick Word On Rail and Mining Segments

Government Environmental Regulations are Driving Market Changes

Source: BCI, Industry Experts, EPA 6

Railroad Starting Mining

Traffic & Idling/Emissions Regulations

Coal vs Natural Gas

$0

$10

$20

$30

$40

2008 2009 2010 2011 2012 2013 2014

Sale

s $

MM

Railroad Battery Sales

$0

$10

$20

$30

$40

2008 2009 2010 2011 2012 2013 2014

Sale

s $

MM

Mining Battery Sales

+22% 2014 -20% 2014

NA Motive Power Battery Market 2008-2014

$0

$200

$400

$600

$800

$1,000

$1,200

2008 2009 2010 2011 2012 2013 2014

Sale

s $

MM

Industrial Truck Railroad Mining

CAGR ‘08-’14

Ind. Truck 5.5%

Railroad 6.5%

Mining -12.8%

TOTAL 5.2%

Motive Power Shows Steady Growth

Source: BCI 7

NA OEM Lift Truck Sales 2003-2014

0

50

100

150

200

Nu

mb

er

of

Lift

Tru

cks

(00

0)

Electric Internal Combustion

CAGR ‘03-’14

Electric 3.3%

IC 1.5%

TOTAL 2.5%

Total Lift Truck Sales Approaching 2006 Historical Peak Electric Lift Truck Sales at Record Levels

Source: Industrial Truck Association 8

‘13-’14 Growth

Electric 4.1%

IC 12.8%

TOTAL 7.5%

NA OEM Electric Lift Truck Market Share

40%

45%

50%

55%

60%

65%

70%

% E

lect

ric

Tru

cks

Sold

Drivers

Environmental Awareness

North America Economy

Improved Truck Technology – Narrowing Performance Gap with IC Trucks

Experts Expect Electric Lift Trucks to be 60-65% of the Market

Source: Industrial Truck Association, Industry Experts 9

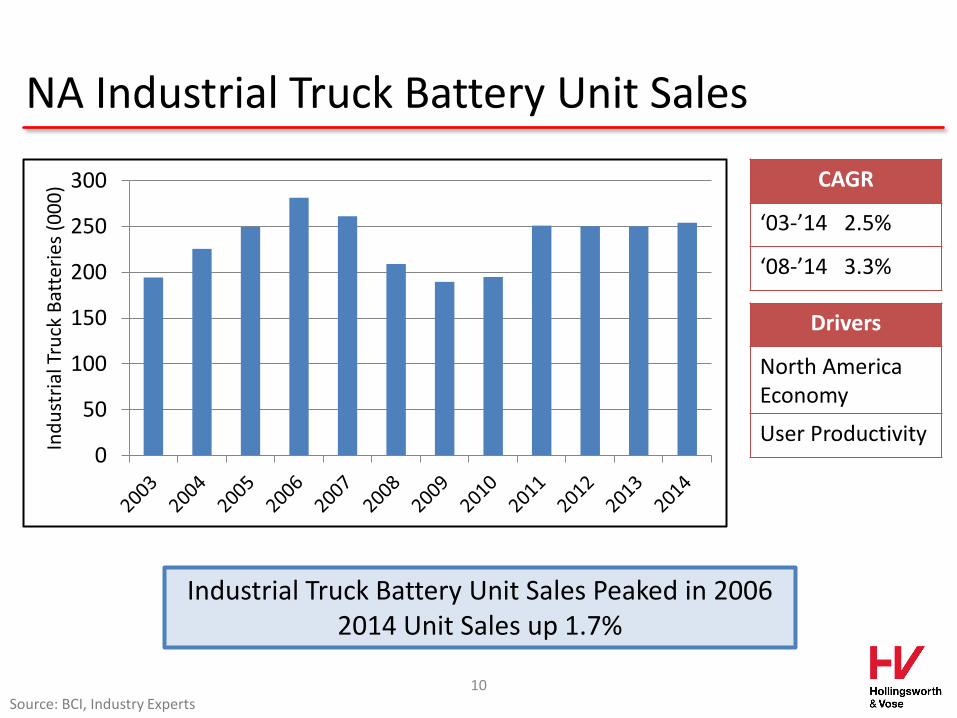

Recession

CAGR

‘03-’14 2.5%

‘08-’14 3.3%

NA Industrial Truck Battery Unit Sales

0

50

100

150

200

250

300

Ind

ust

rial

Tru

ck B

atte

ries

(0

00

)

Industrial Truck Battery Unit Sales Peaked in 2006 2014 Unit Sales up 1.7%

Source: BCI, Industry Experts 10

Drivers

North America Economy

User Productivity

NA Industrial Truck Battery Mix Change

User Productivity Driving Improved Product Mix - Premium Batteries (Tubular & Flat Plate High Capacity) - Opportunity Charging Requires Larger, More Expensive Batteries

Source: BCI, Industry Experts 11

866 905

991

$0

$200

$400

$600

$800

$1,000

$1,200

2012 2013 2014

Ind

ust

rial

Tru

ck B

atte

ry S

ales

$M

M

NA Industrial Truck Battery Sales

0

50

100

150

200

250

300

2012 2013 2014In

du

stri

al T

ruck

Un

it V

ol (

00

0)

Industrial Truck Battery Unit Mix

250 250

12-Cell

18-Cell

24-Cell

Other

254

-1.3%

+1.1%

+5.2%

+0.5%

+3.0%

+1.4%

+4.5%

+9.5%

US Industrial Capacity Utilization

Source: Federal Reserve, BCI, ITA

Change in Capacity Utilization & OEM Lift Truck Sales R²=0.85

12

R² = 0.8474

-60%

-40%

-20%

0%

20%

40%

60%

-15.0% -10.0% -5.0% 0.0% 5.0% 10.0%

Ch

ange

in O

EM L

ift

Tru

ck U

nit

Sal

es

Change in US Industrial Capacity Utilization

Lift Truck Units vs. US Industrial Capacity Utilization

2014

US Industrial Capacity Utilization

Source: Federal Reserve, BCI, ITA

60

65

70

75

80

85

0

50

100

150

200

250

300

US

Ind

ust

rial

% C

apac

ity

Uti

lizat

ion

MP

Bat

tery

an

d O

EM L

ift

Tru

ck U

nit

s (0

00

)

US Industrial Capacity Utilization & Lift Truck/Battery Sales

Motive Battery Units OEM Lift Truck Sales Industrial Capacity Utilization

US Industrial Production Capacity Utilization is Below the Long-Run Average, Indicating Headroom for Growth

13

Long-Run Ind. Cap. Util. Avg 80.1 (1972-2014)

NA Motive Power Sales Forecast 2015-2017

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

Sale

s $

MM

Industrial Truck Railroad Mining

‘14-’17 CAGR

Ind Truck 4.8%

Railroad 5.0%

Mining 7.3%

TOTAL 4.8%

BCI Forecast MP Sales Growth at 4.8% per Year vs. Historical 5.2%

Yearly Forecast

2015 5.0%

2016 4.8%

2017 4.6%

Source: BCI 14

Forecast

Stationary

15

NA Stationary Market 2014

$0

$200

$400

$600

$800

$1,000

$1,200

2013 2014

Sale

s $

MM

Communications Control & Switchgear

UPS Misc Standby*

Segment 2014

Actual Growth

Last Year BCI

Forecast

Comm. -9.6% 8.0%

Ctrl & S/G 7.8% -2.2%

UPS -15.3% 13.0%

Misc Standby -6.0% 1.7%

TOTAL -9.4% 8.1%

Stationary Market Down -9.4% in 2014 Driven by Reduced Telecom & UPS Capital Spending

Source: BCI, Industry Experts

$980 $888

*Misc Standby Includes: Emergency Lighting, Security, Railroad Signaling, Photovoltaic, Diesel Generator Starting, etc

16

NA Stationary Market 2008-2014

$0

$200

$400

$600

$800

$1,000

$1,200

2008 2009 2010 2011 2012 2013 2014

Sale

s $

MM

Communications Control & Switchgear

UPS Misc Standby*

CAGR ‘08-’14

Comm. 1.1%

Ctrl & S/G 2.9%

UPS -1.2%

Misc Standby

17.6%

TOTAL 1.9%

After Several Years of Steady Growth, Stationary Market Declined in 2014

Source: BCI, Industry Experts 17

*Misc Standby Includes: Emergency Lighting, Security, Railroad Signaling, Photovoltaic, Diesel Generator Starting, etc

NA Stationary Product Sales 2008-2014

$0

$200

$400

$600

$800

$1,000

$1,200

2008 2009 2010 2011 2012 2013 2014

Sale

s $

MM

Flooded 2-Volt VRLA VRLA Monobloc

CAGR ‘08-’14

Flooded -6.1%

2-Volt VRLA 3.5%

Monobloc 5.6%

TOTAL 1.9%

Market Continues to Mix Towards VRLA Monobloc Flooded Decline Accelerated in 2014

Source: BCI 18

‘13-’14 Growth

Flooded -16.5%

2-Volt VRLA -1.1%

Monobloc -10.1%

TOTAL -9.4%

44%

23%

33%

54%

26%

20%

Percent Share

Communications Market Growth & Trends

$0

$100

$200

$300

$400

$500

2008 2009 2010 2011 2012 2013 2014

Sale

s $

MM

Flooded 2-Volt VRLA VRLA Monobloc

Segment ‘08-’14 CAGR

2014 Growth

Flooded -4.8% -0.5%

2-Volt VRLA 2.1% -2.3%

Monobloc 2.4% -16.7%

TOTAL 1.1% -9.6%

Telecom Market Uncertainty and Evolution Impacting Battery Sales

Drivers

Telecom Capex Spending

Regulatory Environment

Carrier System Architecture Changes

Source: BCI, Industry Experts 19

Why Mobile Data Didn’t Drive Battery Sales

20 Source: Industry Experts, AT&T/Verizon Annual Reports

Keep Engaged in the Market During Uncertainty and Change

Uncertainty Changing Industry

Dynamics

AT&T Spending Spree Network Build-Out Changing

Acquisition Paralysis Software vs Hardware (AT&T Domain 2.0)

‘Net Neutrality’ Increasing Competition (Incumbents & Disrupters)

Communications Quarterly Sales 2011-2014

Communications Sales Remain Soft, Five Straight Quarters of Year/Year Quarterly Sales Decline

Source: BCI, Industry Experts 21

Drivers

Large Telecoms Influencing Market

Capital Spending Mix Change

Uncertainty

-30%

-20%

-10%

0%

10%

20%

30%

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2012/2011 2013/2012 2014/2013

Telecom Year/Year Quarterly Sales Change

NA UPS Market Growth & Trends

$0

$50

$100

$150

$200

$250

$300

$350

2008 2009 2010 2011 2012 2013 2014

Sale

s $

MM

Flooded 2-Volt VRLA VRLA Monobloc

Segment ‘08-’14 CAGR

2014 Growth

Flooded -12.7% -41.7%

2-Volt VRLA 1.3% -8.0%

Monobloc 4.9% -3.7%

TOTAL -1.2% -15.3%

Evolution from Enterprise to Cloud Data Storage Driving Market

Source: BCI

Drivers

Co-Location Data Center Capacity

Storage Efficiency Changing Backup Requirements

Mix Change = Lower $/Watt

Source: BCI, Industry Experts 22

NA UPS Quarterly Sales 2011-2014

UPS Sales Recovering, Three Straight Quarters of Sales Growth After Declines Starting 2Q13

Source: BCI, Industry Experts, fastcompany.com 23

$50

$55

$60

$65

$70

$75

$80

$85

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4

2011 2012 2013 2014

Sale

s $

MM

UPS Quarterly Sales $MM Drivers

Near-Term Data Center Overcapacity

Long-Term Data Storage Demand Growth

“Since last summer, the number of videos watched on Facebook has tripled, now totaling over 4 billion per day.” - John Titlow, April 2015

Control & Switchgear Market Growth & Trends

$0

$20

$40

$60

$80

$100

$120

2008 2009 2010 2011 2012 2013 2014

Sale

s $

MM

Flooded 2-Volt VRLA VRLA Monobloc

Segment ‘08-’14 CAGR

2014 Growth

Flooded 0.9% 6.4%

2-Volt VRLA 11.3% 8.8%

Monobloc 5.9% 16.3%

TOTAL 2.9% 7.8%

Control & Switchgear Market Remains Stable Flooded Batteries Approximately 70% of the Market

Source: BCI, Industry Experts 24

Drivers

Aging Power Infrastructure

Increasing Power Demand

NA Misc. Standby Market Growth & Trends

$0

$20

$40

$60

$80

$100

$120

$140

2008 2009 2010 2011 2012 2013 2014

Sale

s $

MM

Flooded 2-Volt VRLA VRLA Monobloc

Segment ‘08-’14 CAGR

2014 Growth

Flooded -1.2% -30.4%

2-Volt VRLA 12.2% 7.9%

Monobloc 21.7% -8.2%

TOTAL 17.6% -6.0%

Many Applications, Mix Driving Market Sales

Drivers

Renewable Energy Demand

Rail-Positive Train Control

Source: BCI, Industry Experts

*Misc Standby Includes: Emergency Lighting, Security, Railroad Signaling, Photovoltaic, Diesel Generator Starting, etc

25

NA Stationary Sales Forecast 2015-2017

$0

$200

$400

$600

$800

$1,000

$1,200

Sale

s $

MM

Communications Control & Switchgear

UPS Misc Standby

‘14-’17 CAGR

Comm. 4.4%

Ctrl & S/G 6.0%

UPS 2.4%

Misc Standby

4.0%

TOTAL 4.0%

BCI Forecast Stationary Growth at 4.0% per Year

Yearly Forecast

2015 4.9%

2016 3.7%

2017 3.3%

Source: BCI 26

Forecast

Industrial Battery Market Summary

• 2014 NA Market $1.93 Billion

– Motive Power $1.04 Billion

– Stationary $888 Million

• Market Flat in 2014

– Motive Power 9.4%

– Stationary -9.4%

• Forecasted Growth 4.5% CAGR 2014-2017

– Motive Power 4.8% to $1.20 Billion

– Stationary 4.0% to $1.00 Billion

Source: BCI 27

NA Energy Storage Systems BCI Forecast

$4 $2 $3

$18

$36

$86

$0

$20

$40

$60

$80

$100

2012 2013 2014 2015 2016 2017

Sale

s $

MM

Market Moving Out of Demonstration Stage Confidence Increasing, BCI Forecasting Strong Growth

Constraints

Project Economics & Capital Cost

Unproven Technology

Drivers

Increasing Renewable Energy Generation / Energy Conservation

Government Regulation & Funding

Overtaxed Infrastructure

Source: BCI, Industry Experts 28

Forecast

Grid Energy Storage is Real in New York City

29 Source: Demand-Energy.com, NYSERDA, Con Edison, greentechmedia.com

NYSERDA & Con Edison 125MW Peak Reduction Program

Offset Potential Closing of Indian Point Nuclear Facility 44MW for Energy Storage for Behind-the-Meter Distributed Energy Storage First 1MW of Projects Approved •Glenwood Management Luxury

Apartments •Proven Lead-Acid Technology •Demand Response and Peak Shaving

Brooklyn/Queens 52MW Demand Management Program

Target to defer $1 Billion substation investment for 10 years 11MW for Utility-Side Battery Energy Storage required in place by 2018

Two Opportunities Valued at $50MM in NYC

Source: Industry Experts , worditout.com 30

What Keeps You Up At Night?

Fuel Cell Lithium

Lithium NiCd

Fly Wheels

Alternative Technologies

Source: Industry Experts, datacenterjournal.com, BYD 31

• Customers want smaller, lighter, maintenance-free, longer-lasting batteries: lowest cost of ownership

• Lead-Acid batteries can’t meet all the needs, all the time

• Alternative technologies will win select applications

Lead-Acid is a Low-Cost, Trusted Solution Technology Advances Critical for Sustained Growth

Mo

tive

St

atio

nar

y

Presented at the 127th Convention of Battery Council International May 3-5, 2015

North American Industrial Battery Forecast 2015-2017

Mitch Bregman Division President Energy and Industrial Systems