bd0804 air travel in africa

TRANSCRIPT

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 1/29

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 2/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

1

Wings over Africa?

Trends and Models for African Air Travel

Greg Mills and Larry Swantner1

AIR TRAVEL WORLD-WIDE is a fast-changing business. A number of events in Marchand April 2008 illustrate the scale of the changes in and challenges faced by thishyper cost-sensitive and technology-dependent industry.

Heathrow’s Terminal Five was opened on 27 March, an edifice taking 19 years todesign, 20,000 workers to build and costing £4.3 billion. It has been said that withthis new terminal, travel will never be the same.2 But when London Airport wasopened in 1955, it was believed that what has become today’s Terminal Two atHeathrow would meet all air transport needs until the end of the 20 th century. Forwhen the first 747 flights occurred in 1970, the 400 passengers of the giant Boeingturned such arithmetic of air travel on its head. With a projected usage of 30 millionpassengers annually, thus raising Heathrow’s total to 90 million, Terminal Five is a

far cry, initial baggage handling problems apart, from the village of tents that wasHeathrow in 1947 or, slightly further afield, Gatwick’s 1933 flying club. Even theplanners of airports seem not to know the trends in their business that well. As weshall see, the manufacturers of aircraft, too, are making bets on the future that may,or may not, prove correct.

EOS Airlines filed for a Chapter 11 bankruptcy at the end of April 2008, leavinghundreds of executive stranded in New York. Coming just four months after its mainrival, Maxjet, went bust, EOS’ problems called into question the strategy of business-class-only airlines, or for those such as Singapore Airlines and British Airways considering business-class-only routes. EOS was reported to have lost US$37 millionin the first nine months of 2007 on sales of just US$35 million.3

On 15 April 2008, a Hewa Bora Airways DC-9 crashed after aborting its takeoff fromGoma, in the far east of the Democratic Republic of Congo (DRC). At least 40 peoplewere killed with more than 50 others seriously injured.

The mooted merger between loss-making US giants Continental and United appearedto have collapsed by the end of April 2008, with the talk moving to the prospect of aUnited deal with US Airways and a Continental three-way alliance with AmericanAirlines and British Airways. The Continental-United merger discussions weredropped after United’s parent, UAL, announced worse-than-expected earnings, whichsent its shares falling. The mooted deal indicated further the musical chairs gamebeing played in the US airline industry shortly after the merger announcement byDelta Air Lines and Northwest Airlines. The point was – the US airline business was in

ill-health and in need of rapid overhaul.

1 DR MILLS heads the Johannesburg-based Brenthurst Foundation, and during 2008 is on secondment to theGovernment of Rwanda as ‘strategic adviser to the President’; COLONEL (rtd.) SWANTNER is a US-basedconsultant with 40 years of experience of flying and administrating military and commercial long-haul aircraft.This paper has partly been compiled from a range of interviews of senior aviation sector personnel in the UnitedStates, Europe and Africa.

© The Brenthurst Foundation, May 2008

2 ‘Plane genius’, 5: British Airways, 2008.

3 The Daily Telegraph Business, 28 April 2008.

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 3/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

2

The South African-based low-fare carrier Nationwide ceased operations on 29 April2008, having failed to recover from the loss in revenue flowing from the temporaryrevoking of its licence to operate in 2007 as a result of safety concerns.4

African Airline Safety,5 2005

Finally, the price of oil went through the US$130 per barrel mark, with the upperlimit price still uncertain. With jet fuel at US$145 per barrel, fuel as a percentage of operating expenses jumped in non-African operations from 15% budgeted to over55% and in some cases over 65% in day-to-day operations. This has raisedquestions about fuel saving methods – from changes in flight profiles to single-

engine taxiing, the removal of non-essential equipment from aircraft, the grafting of efficiency-generating winglets on older aircraft, and more efficient models.

The five airlines (Aloha, ATA, Business Jet, Midwest Express and Spirit) that haveceased operations in the US in late 2007 and early 2008 have all ostensibly beenlow-cost, point-to-point operators rather than the more expensive hub-and-spokeoperations. Fuel costs for the industry world-wide are estimated at US$136 billion in2007, a 22.5% increase over 2006.

*

4 A note on the Nationwide website read: ‘On the 7th November 2007, Nationwide Airlines experienced an

engine separation from a Boeing 737-200 on departure from Cape Town. Subsequent to this a protractedgrounding of our fleet was mandated by the South African Civil Aviation Authority. In the months of Decemberand January we resumed operations and attained a gradual recovery of the business however in the months of March and April we faced a 30% increase in fuel costs coupled with a decrease in passenger load factors.Throughout this period we continued to work towards securing investment by a black empowerment consortiumwhich unfortunately has not come to fruition. Our cash-flow has become critical and as a result have decided tovoluntarily cease all flight operations until further notice. The company was placed under Provisional Winding-Up Order on the 29th April 2008 and in the hands of the Master of the High Court, Johannesburg. A provisionalliquidator, Tshwane Trust Company has since been appointed, who will take charge of Nationwide Airlines… .’ Athttp://www.flynationwide.co.za/

5 From: Charles Schlumberger, Case Study Exercise: Insight for Transport Task Managers, The World Bank, 11March 2005.

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 4/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

3

African air travel may, in the eyes of many, be at the other end of the scale. There isno continent with the same number of crashes per frequency of flights6 – six timesworse than the world average – or with the extent of unregulated airspace. Eventhough Africa accounts for just five% of the world’s aviation traffic, 2007’s ‘hull lossrate’ for the continent, which measures the frequency of accidents, stood at four,compared to 0.7 globally. The skies remain unregulated and dangerous, with therelative absence of essential services, especially competent radar-guided air trafficcontrol, and given aircraft safety standards. For example, the Geneva-based AircraftCrashes Record Office reported eight air accidents in the DRC alone in 2007.7

Yet the frequency of more thanfifty flights a day into Goma inthe eastern DRC, the city wherethe DRC’s most recent airdisaster occurred on 15 April2008, is an indication of at leasttwo things. Firstly, since most of these flights are carrying

unrefined ore (rocks), this isevidence of the absence of roadinfrastructure in that cavernousterritory. There is a need for airlinks to transport cargo andpeople alike. Secondly, there isthe need for air travel as a sine

qua non for international exchanges of trade, finance, technology and skills – inessence, for development and prosperity.

The last two decades have nonetheless been a time of great upheaval for Africa’snational air carriers. Many have gone bust, including a few notables such as Ghana,Nigeria and Zambia Airways. There are very few even partially state-owned airlines

operating in Africa today: South African Airways (SAA), Air Namibia, Angola, LAM(Mozambique), Air Zimbabwe, Air Senegal and Royal Air Maroc among them. And afew loss-making ones, seemingly focused on staff welfare and governmentpatronage rather than service considerations, should probably also be allowed to go

6 A recent chronology of African air disasters includes: January 8, 1996 - At least 350 people died when aRussian-built Antonov-32 cargo plane crashed into a crowded market in central Kinshasa, capital of Zaire (nowDRC). November 23 - One hundred and twenty-five of 175 passengers and crew are killed when a hijackedEthiopian Airlines Boeing 767 crashed into the sea off the Comoros Islands; January 30, 2000 - A KenyaAirways Airbus A-310 crashed into the sea shortly after takeoff from Abidjan in Ivory Coast, killing 169 of the179 passengers and crew; May 4, 2002 - A Nigerian EAS Airlines BAC1-11-500 crashed in the north Nigeriancity of Kano, with at least 148 fatalities, 75 on the plane and 73 on the ground; March 6, 2003 - An Algerian Boeing 737-200 crashed shortly after takeoff from Tamanrasset airport, killing 103 passengers and crew; May 8- Cargo door opens in mid-flight on an Ilyushin 76 transport plane in the DRC, sending at least 70 passengersplummeting to their deaths; July 8 - A Sudan Airways Boeing 737 crashed shortly after takeoff near Port

Sudan, killing 104 passengers and the crew of 11. One child survives; December 25 - A Boeing 727 bound forBeirut clips a building after takeoff in Benin and plunges into the Atlantic Ocean, killing 111 passengers andcrew. Twenty-two survive; October 22, 2005 - A Nigerian Bellview Airlines Boeing 737-200 airliner with 111passengers and six crew crashed north of Lagos, shortly after takeoff. All aboard are killed; December 10 - ANigerian Sosoliso Airlines DC-9 flight from Abuja carrying 110 passengers and crew crashed on landing. Fourpeople survive; May 5, 2007 - All 114 people on board a Kenya Airways Boeing 737 are killed when the planecrashed in torrential rain after takeoff from Douala in Cameroon en route to Nairobi; April 15, 2008 - A Hewa

Bora Airways McDonnell Douglas DC-9 crashed after aborting its takeoff from Goma in the DRC. Sourced fromhttp://www.alertnet.org/thenews/newsdesk/L16864928.htm.

7 IATA Director-General Giovanni Bisignani said about Africa’s air safety record during a visit to Nigeria in 2008, ‘This cannot go on ... When you have a continent that is six times worse than the world average,embarrassment is the only word to explain it.’ Reuters, 10 April 2008 at http://www.globalgoodnews.com.

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 5/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

4

bust. African airlines lost approximately US$400 million in 2006-7, and profits arenot expected to accelerate until Africa’s safety record improves, though losses areexpected to ease slightly to US$300 million in 2008. This is partly a result of theinternational traffic increase of 8% in 2007, in turn reflecting market liberalisationand robust economic growth in parts of the continent.8

In their place have sprung up an increasing number of private regional carriers. Aview of the ramp of Nairobi airports gives some idea of this proliferation in EastAfrica alone, this in a venue where the national carrier is dominant: Fly 504, EastAfrica Airways, Air Uganda, Jetlink, Aero Kenya, Imatogo Airlines, Lakevik Aviation and Executive Turbine are all private airlines. There are 50 licensed airlines in Kenyatoday, of which around 30 are operational. As a result of this growth, thehumanitarian aid delivery business and private charters, Nairobi’s Wilson Airport issaid to be the busiest in Africa when measured by air movements. (If the UnitedNations were to leave the region, it is calculated that there would be a 50% drop intraffic.) Such growth has stressed airport functioning to breaking point and is despite

the tough current times for African carriers, withincreasing fuel costs and, in Kenya’s case, theimpact of recent bad politics on its tourism

industry.

9

But as the saying goes, the best way to make asmall fortune from airlines is to start with a largeone. In the nearly one hundred years of commercial air travel, few have made money. Itis a difficult business by nature of the intensityof its competitiveness, uncontrollable costs(especially fuel) and heavy capital expenditure.

It has been said that managing an airline is a bit like trying to solve a Rubic’s Cubewith uncontrollable inputs. Just when you think you have the puzzle solved, an inputbeyond your control (fuel price, extreme weather, unexpected governmentinterference, labour unrest and terrorist activity) makes two or three quick spins of

your cube, and your planned ‘solution’ is again in complete disarray. Save SingaporeAirlines and Emirates, there are no state-owned national airlines that are todaymaking money. And few countries with successful services and tourist economiesrequire national carriers to grow that side of their economies. Is there a model thatAfrican airlines should best follow to maintain profits and offer a competitive service?What is the current best practice thinking in this regard? And are there specialconsiderations that must be borne in mind in Africa?

This Discussion Paper examines these questions against a backdrop of currentthinking in international airline strategic thinking and management.

*

8 Ana McAhron-Schulz, IFALPA Industrial Advisor, Airline Industry Overview, April 2008.

9 The Kenyan tourism industry recorded a 61 percent drop in the first quarter of 2008 when compared to thesame period in 2007, posting KSh8 billion in income compared to the projected figure of KSh21 billion. Some274,000 tourists arrived in Kenya compared to 500,000 in the period in 2007. See ‘Tourism earnings fall by 61per cent’, Saturday Nation (Nairobi), 3 May 2008. For example, the number of airlines plying the Nairobi-Kisumu route in Kenya has increased to eight from just two three years ago. The annual number of passengershas increased from 70,000 in 2005 to 240,000 in 2007. The Kisumu facilities, from the terminal to the runway,is now deemed unsuitable for this increase in traffic. See ‘Kisumu airport in need of expansion’, Saturday Nation (Nairobi), 3 May 2008.

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 6/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

5

The Global and African Air Picture

Air traffic globally has increased at around 5% annually on average since the 1970s.Globally, the air transport industry enjoyed an estimated turnover of more thanUS$1,800 billion and created more than 28 million direct or indirect jobs in 2005.However, Africa’s share in the global air transport industry remains insignificant. Outof more than two billion passengers carried in 2006 by the 190 member states of theInternational Civil Aviation Organization (ICAO), Africa accounts for just five percentof all traffic. And two-thirds of that five percent was handled by airlines that are notmembers of the African Airlines Association (AFRAA).

World Bank Aviation Data for Low- and Middle-Income Countries (‘000 passengers)

0

100,000

200,000

300,000

400,000

500,000

600,000

700,000

800,000

1996 2001 2002 2003 2004 2005 2006

Asia Pacific

Eastern Europe &Central Asia

Latin America &Caribbean

Middle East & NorthAfrica

South Asia

Sub-Saharan Africa

Africa has, however, rapidly increased passenger loads since the end of the ColdWar, albeit from a very low base. According to the International Air TravelAssociation(IATA), in 2005 Africa air traffic had a growth rate higher than the worldaverage: 11% as against 8.3% for passengers; 8% as against 3% for freight. This is

corroborated by Boeing forecasts, which predict an African air transport growth of 4.8% for passengers and 6.4% for freight in the 2000-19 period. Similarly, Airbuspredicts a 6.3% increase in the passenger traffic for the period 2004-2013 and 3.9%for the period 2014-33, as well as a 7% increase in freight traffic for the period

2005-23 (see above andleft).

In 2004, 42 members of AFRAA carried 36 millionpassengers, representinga 12% increase comparedto 2003, while Europeanairlines (Air France, KLM,

British Airways, Alitalia,Iberia, Lufthansa, SNBrussels and Swiss Air)transported from and toAfrica 72 million

passengers, i.e two-thirds of the total air traffic (108 million passengers).10 AFRAAmembers moved 656,000 tons of freight in 2004, a 12% increase over 2003.11

10 The top ten South African inter-continental country-routes alone accounted for 5.75 million passengers in2007.

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 7/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

6

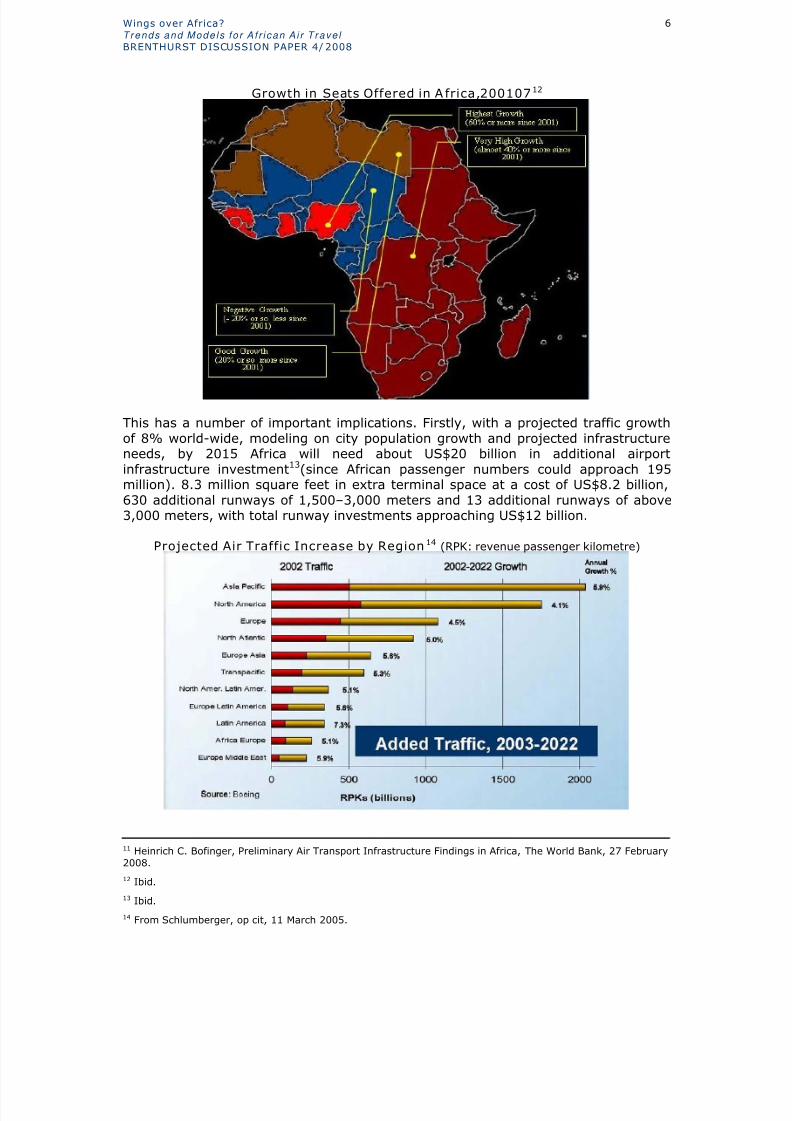

Growth in Seats Offered in A frica,20010712

This has a number of important implications. Firstly, with a projected traffic growthof 8% world-wide, modeling on city population growth and projected infrastructureneeds, by 2015 Africa will need about US$20 billion in additional airportinfrastructure investment13(since African passenger numbers could approach 195million). 8.3 million square feet in extra terminal space at a cost of US$8.2 billion,630 additional runways of 1,500–3,000 meters and 13 additional runways of above3,000 meters, with total runway investments approaching US$12 billion.

Projected Air Traffic Increase by Region14 (RPK: revenue passenger kilometre)

11 Heinrich C. Bofinger, Preliminary Air Transport Infrastructure Findings in Africa, The World Bank, 27 February2008.

12 Ibid.

13 Ibid.

14 From Schlumberger, op cit, 11 March 2005.

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 8/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

7

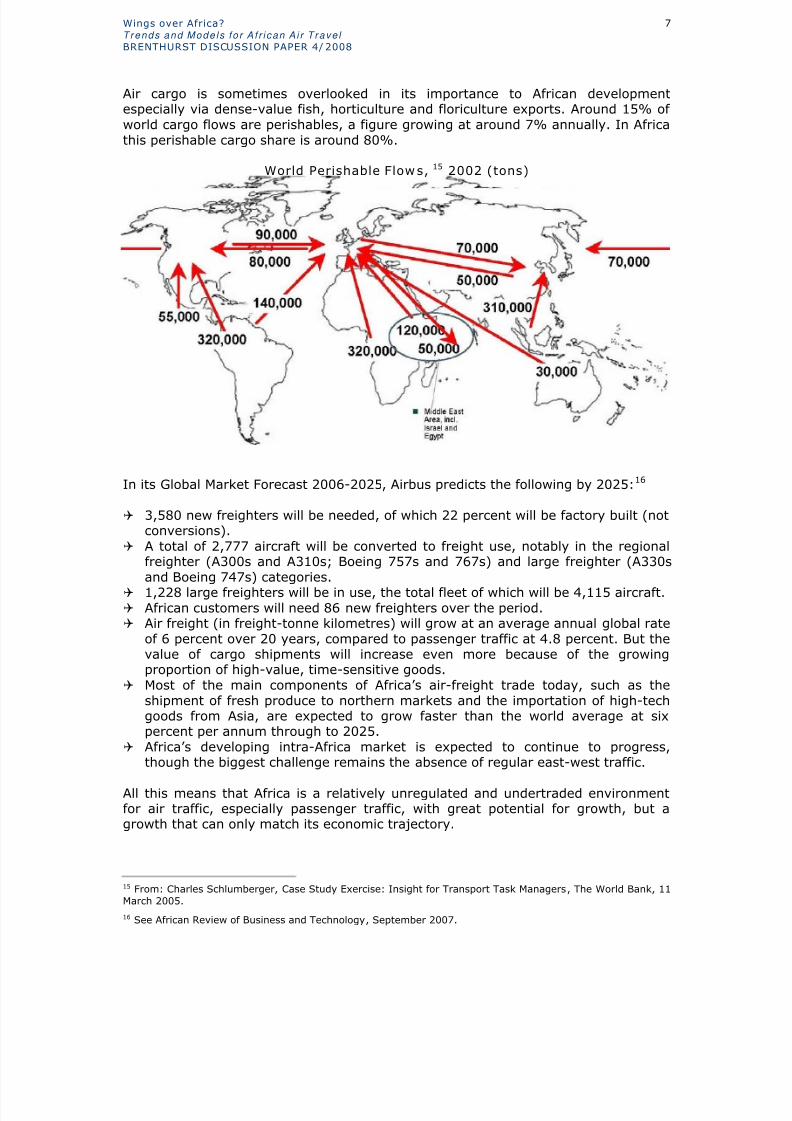

Air cargo is sometimes overlooked in its importance to African developmentespecially via dense-value fish, horticulture and floriculture exports. Around 15% of world cargo flows are perishables, a figure growing at around 7% annually. In Africathis perishable cargo share is around 80%.

World Perishable Flows, 15 2002 (tons)

In its Global Market Forecast 2006-2025, Airbus predicts the following by 2025:16

3,580 new freighters will be needed, of which 22 percent will be factory built (notconversions).

A total of 2,777 aircraft will be converted to freight use, notably in the regionalfreighter (A300s and A310s; Boeing 757s and 767s) and large freighter (A330sand Boeing 747s) categories.

1,228 large freighters will be in use, the total fleet of which will be 4,115 aircraft. African customers will need 86 new freighters over the period. Air freight (in freight-tonne kilometres) will grow at an average annual global rate

of 6 percent over 20 years, compared to passenger traffic at 4.8 percent. But thevalue of cargo shipments will increase even more because of the growingproportion of high-value, time-sensitive goods.

Most of the main components of Africa’s air-freight trade today, such as theshipment of fresh produce to northern markets and the importation of high-techgoods from Asia, are expected to grow faster than the world average at sixpercent per annum through to 2025.

Africa’s developing intra-Africa market is expected to continue to progress,though the biggest challenge remains the absence of regular east-west traffic.

All this means that Africa is a relatively unregulated and undertraded environmentfor air traffic, especially passenger traffic, with great potential for growth, but agrowth that can only match its economic trajectory.

15 From: Charles Schlumberger, Case Study Exercise: Insight for Transport Task Managers, The World Bank, 11March 2005.

16 See African Review of Business and Technology, September 2007.

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 9/29

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 10/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

9

delay and cost. And because the route network is no longer interconnected, delaystend not to spread around the system. Not only does this improve customersatisfaction, it also allows for more efficient utilisation of expensive aircraft.

But this debate is not over. Indeed, the two major offerings by the two major aircraftmanufacturers, the Airbus A380 and Boeing 787 ‘Dreamliner’, are precisely aimed ateach of these models: the 600-seater Airbus at the hub-and-spoke distributionsystem, the smaller Boeing the latter.

An African Example: One – The Kenyan Model

Kenya Airways has captured a large slice of the African market, opening up routesacross East, Central and West Africa. It has done so largely because no-one else didor could, and because it is respected as having a good business model. This is builton the SkyTeam alliance (around KLM and Air France), ensuring that this aspect of international connectivity provides it with a passenger advantage none of its(private) competitors currently enjoys.

Kenya Airways traces its history back to 1946, with the formation of the East AfricanAirways Corporation (EAA). Initially, EAA had a good reputation for service andreliability. With the formation of the East African Community, EAA passed into the

joint ownership of the governments of Kenya, Tanzania and Uganda. Shortly afterthe collapse of the East African Community in 1976, EAA was placed in liquidation.Kenya Airways was incorporated in January 1977 as a company wholly owned by theKenyan government until April 1996.

In 1992, Kenya Airways was given priority among national companies in Kenya to beprivatised. In 1993/4, the airline produced its first profit since the start of commercialisation. With assistance from the World Bank’s International FinanceCorporation (IFC), in 1995, Kenya Airways restructured its debts, while KLM

purchased 26% of its shares, thereby becoming the largest shareholder. In the same

year the airline started trading on the Nairobi Stock Exchange; and in October 2004on the Dar es Salaam bourse. In April 2004, the company reintroduced KenyaAirways Cargo as a brand and in July 2004, the company’s domestic subsidiaryFlamingo Airlines was reabsorbed.

The airline is today owned by individual Kenyan shareholders (32.5%), KLM (now Air

France-KLM) (26%), the Kenyan government (22%), Kenyan institutional investors(15.7%), foreign institutional investors (4.36%) and individual foreign investors(0.07%). Today it has 2,862 employees. Kenya Airways also owns 49% of Precision

Air in Tanzania.

Precision Air was established in 1993 as a private air charter company operating afive-seater Piper Aztec aircraft flying to tourist destinations. A growing demand for

air transport services led to Precision operating scheduled flights and maintainingArusha town as its base. The first flights were scheduled using a small Cessnas untilthe mid-1990s when the bigger ATR-42 fleet was introduced. Total passengerscarried increased from 268,580 in the 2004/5 financial year to 340,000 in 2005/6. In2003, Kenya Airways acquired a 49% shareholding, with the majority retained in thehands of the founder (coffee-farmer Michael Ngaleku Shirima). This has enabled theairline to increase frequencies and to build its fleet, now comprising eight aircraft,with connections to major towns in Tanzania, as well as regional destinations to

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 11/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

10

Malawi and Kenya. Precision operates as a Tanzanian and regional connector for KQinto Nairobi.

From 2004, much of Kenya Airways’ success has been attributed to the KTAP (KenyaAirways Turn Around Project) overhauling the airline’s revenue management, coststructures, and route and fleet planning. In the 2005/6 financial year, after-taxprofits nearly tripled over 2003/4 to US$50 million, with over two million passengers

carried. Again, in2005/6, after-tax profitsincreased to aroundUS$65 million.Passenger numbers in2006/7 were 2.6million.

Kenya Airways’ inter-African routes reputedlycomprise up to 40percent of its profits.

KQ’s break-even loadfactors are apparentlyin the 65-70 percentmargin, where they arecurrently operating atthe 75 percent level.Kenya’s use of the hub-

and-spoke model has been enabled through the correct scheduling and acquisition of the proper aircraft type for these routes, and the connectivity and code-sharingoffered by its KLM-AF alliance. Its success has spurred greater domesticcompetitiveness domestically, with the emergence of private airlines.

Overall, the experience of Kenya Airways and the concomitant rise of its domestic

competitors suggest that:

Cheaper fares are not the critical competitiveness factor. Consistency, reliability,frequency and location of the airport are at least equally as important.

The introduction of new airlines has led to a price war on internal routes, whichmay lead to a shake-out of domestic players. Four Kenya-based airlines today flythe Juba (South Sudan) route, with fares reducing from US$700 to underUS$200, a level at which operations are unsustainable.

There is a growing domestic and regional commuter market feeding the Nairobihub. While greater loads follow greater frequency – the airline equivalent of the

‘build and they will come’ logic – it, however, takes time to build up a route.Currently there are large gaps between capacity and usage, suggesting thatsupply has been growing faster than demand, and creating problems within the

industry around profitability and potentially safety. This may lead to a new roundof mergers between competitors.

If there is to be a single East African regional hub, Nairobi is best positioned to fillthis role.

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 12/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

11

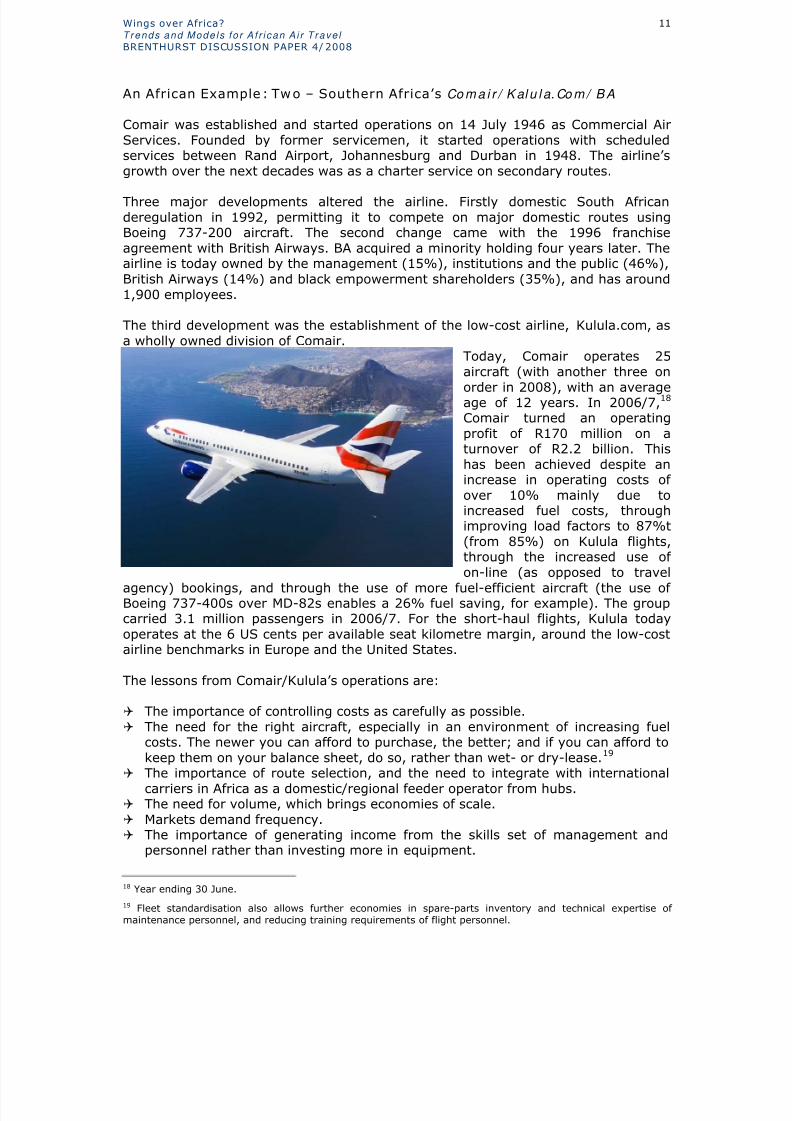

An African Example: Two – Southern Africa’s Co m a i r / K al u l a. Co m / B A

Comair was established and started operations on 14 July 1946 as Commercial AirServices. Founded by former servicemen, it started operations with scheduledservices between Rand Airport, Johannesburg and Durban in 1948. The airline’sgrowth over the next decades was as a charter service on secondary routes.

Three major developments altered the airline. Firstly domestic South Africanderegulation in 1992, permitting it to compete on major domestic routes usingBoeing 737-200 aircraft. The second change came with the 1996 franchiseagreement with British Airways. BA acquired a minority holding four years later. Theairline is today owned by the management (15%), institutions and the public (46%),British Airways (14%) and black empowerment shareholders (35%), and has around1,900 employees.

The third development was the establishment of the low-cost airline, Kulula.com, asa wholly owned division of Comair.

Today, Comair operates 25aircraft (with another three on

order in 2008), with an averageage of 12 years. In 2006/7,18 Comair turned an operatingprofit of R170 million on aturnover of R2.2 billion. Thishas been achieved despite anincrease in operating costs of over 10% mainly due toincreased fuel costs, throughimproving load factors to 87%t(from 85%) on Kulula flights,through the increased use of on-line (as opposed to travel

agency) bookings, and through the use of more fuel-efficient aircraft (the use of Boeing 737-400s over MD-82s enables a 26% fuel saving, for example). The groupcarried 3.1 million passengers in 2006/7. For the short-haul flights, Kulula todayoperates at the 6 US cents per available seat kilometre margin, around the low-costairline benchmarks in Europe and the United States.

The lessons from Comair/Kulula’s operations are:

The importance of controlling costs as carefully as possible. The need for the right aircraft, especially in an environment of increasing fuel

costs. The newer you can afford to purchase, the better; and if you can afford tokeep them on your balance sheet, do so, rather than wet- or dry-lease.19

The importance of route selection, and the need to integrate with international

carriers in Africa as a domestic/regional feeder operator from hubs. The need for volume, which brings economies of scale. Markets demand frequency. The importance of generating income from the skills set of management and

personnel rather than investing more in equipment.

18 Year ending 30 June.

19 Fleet standardisation also allows further economies in spare-parts inventory and technical expertise of maintenance personnel, and reducing training requirements of flight personnel.

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 13/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

12

Making safety a priority. Building strong brands that customers trust. Recruiting and retaining high-quality management and staff.

An International Example: easyJet 20

Based at Luton Airport just north of London, easyJet is one of the largest low-fareairlines in Europe. It operates domestic and international scheduled services on 387routes between 104 European and North African destinations. Established on 18October 1995, easyJet was launched by (now Sir) Stelios Haji-Ioannou with two wet-leased Boeing 737-200s, initially operating two routes: London-Luton to Glasgow andEdinburgh.

Similar to its largest rival, Ryanair, easyJet has seen rapid expansion throughacquisitions and base openings, both of which have been fuelled by consumerdemand for low-cost air travel.

Ray Webster, the former easyJet CEO, and its founder, Haji-Ioannou, were drawn to

such an architecture by a number of insights. The first was that the European Unionhad agreed to deregulate travel within Europe, thus breaking the stranglehold of thenational carriers. The second was that the smaller, efficient, jets, originally designedfor feeder flights would make excellent point-to-point platforms. Finally, theyrealised that demand for air travel was extremely sensitive to price and that a lower-priced product could attract a whole new range of customers rather than justcompeting with existing offerings.

In so doing, easyJet, like Ryanair, borrows its business model from the American aircarrier Southwest. Both airlines have adapted this model for the European marketthrough further cost-cutting measures, including not selling connecting flights orproviding complimentary snacks on board. The key points of this business model arehigh aircraft utilisation, quick turnaround times, charging for extras (such as priority

boarding, hold baggage and food) and keeping operating costs low.

easyJet’s early marketing strategy was based on ‘making flying as affordable as apair of jeans’ and urged travellers to ‘cut out the travel agent’. Its early advertisingconsisted of little more than the airline’s telephone booking number painted in brightorange on the side of its aircraft. Styling itself as ‘the web’s favourite airline’, easyJet played on the British Airways’ slogan ‘the world’s favourite airline’.

Though it was not the first no-frills carrier or the first large one in Europe, easyJet’s success arguably paved the way for the boom in cheap air travel in the late 1990sand early 2000s. Along with other low-cost providers such as Jet Blue and Ryanair,easyJet was among the first in Europe to move away from a hub-and-spoke towardsa point-to-point architecture.

Onboard sales are an important part of the airline’s ancillary revenue. easyJet alsosells gifts such as fragrances, cosmetics and easyJet-branded items onboard, as wellas tickets for airport transfer services. It offers only limited in-flight entertainment,and a charge is made for movies on longer flights.

20 This is drawn partly from http://radar.oreilly.com/archives/2006/12/a-startup-airline.html.

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 14/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

13

In March 1998, easyJet purchased a 40% stake in Swiss charter airline TEA Basle.On 16 May 2002, easyJet purchased rival airline, London Stansted-based Go for£374 million, in so doing inheriting three new bases from Go at Bristol InternationalAirport, East Midlands and London Stansted. In 2001, easyJet opened its base atLondon Gatwick Airport; and between 2003-2007, new bases were created inGermany, France, Italy and Spain. On 25 October 2007, easyJet purchased GBAirways Ltd for £103.5 million, using this to expand easyJet operations at LondonGatwick Airport and establish a base at Manchester Airport. The deal expandedeasyJet’s operations to existing destinations in Spain, Portugal, Austria and theCanary Islands, and to new destinations in the north of Africa, Malta, France, theGreek islands and Gibraltar.

The airline now operates 137 aircraft from 17 bases across Europe. Listed on theLondon Stock Exchange, it has 4,859 employees. From 6 million passengers in 2000and £22m profit, in 2005/6 it flew 33 million passengers with £130m profit, and 37.2million and £200m profit in 2006/7.

Apart from the initial pair of 737-200s leased from GB Airways and some 737-300s

inherited from Go, the airline has only ever operated new aircraft, either 737-300s,737-700s or Airbus A319s. The newer aircraft are advertised to produce loweremissions and be more environmentally friendly. The easyJet fleet consists of 173aircraft (at April 2008), including 128 Airbus A319-100s, the average age of theaircraft being 3.1 years.

Like others, easyJet has voiced concerns recently over the impact of rising fuel costs,which it sees as ‘going to put enormous pressure on all airlines.’ It sees airlines

‘having to ‘restructure, merge, shrink or disappear’. The airline views profit growthcoming from new capacity and higher margins, with an aim to increase capacity byabout 15% in 2008.21

Africa’s Aviation Picture

In 2003, Africa had a fleet of 1,165 commercial aircraft, 605 jets and 400 turbo-props.22 Then the average age was 20 years, compared to 12 years in North America,nine in Europe, and seven years in Southeast Asia. Put differently, Africa hasproportionately more aircraft that are noisy, expensive to run in terms of fuel andmaintenance, and most dangerous for air safety.

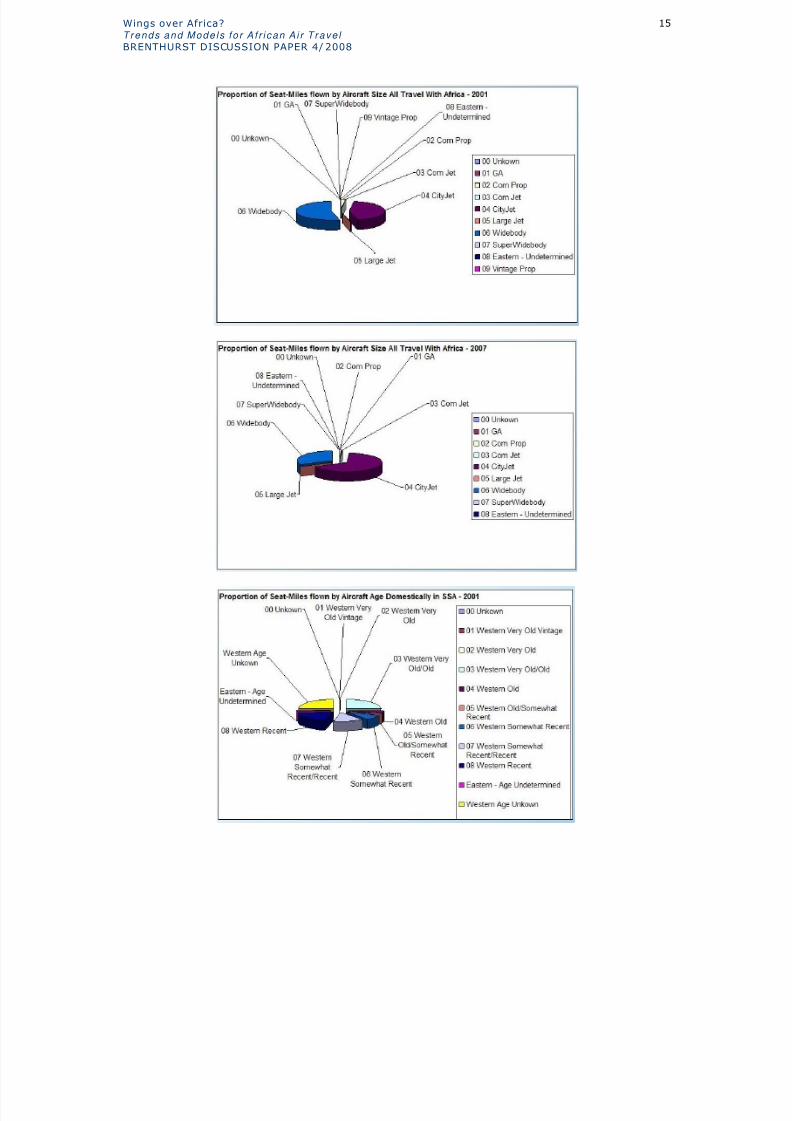

South Africa is the epicentre of aircraft registrations in Africa, reflecting the health of its general aviation sector, with over 10,000 aircraft of all types, though Kenya hastoday around 750 aircraft on the national registry. More important than numbers inthe commercial world are, however, types and age profiles of aircraft. The figuresbelow indicate how this is changing in Africa, illustrating the following patterns over

the 2001-2007 period:23

21 Aviation News, May 2008, p.15.

22 The world total of commercial aircraft operated in 2003 was 13,612 in 2003, made up of 5,535 in America,3,368 in Europe, 2,418 in Asia, 539 in the Middle-East, 272 in the Pacific. Strategy for Air Transport

Development in Africa, African Development Bank, May 2006.

23 Western Very Old Vintage: DC 3, etc.; Western Very Old: 1960s-1970s, include 727s, 737-100’s, etc.;Western Old: 1970s to 1980s; Western Somewhat Recent: 1980s to the 1990s, such as the Boeing 757;Western Recent: Group of the newest aircraft, generally from the mid 1990s onwards; Eastern Built: Notbroken down by age, though they do not play a large role in scheduled passenger travel in Africa. FromBofinger, op cit, 27 February 2008.

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 15/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

14

The age of aircraft predominantly in passenger service in Africa has moved from

Western ‘somewhat recent’ (1980s-90s) category to Western ‘recent’ (1990s).The latter category has dramatically increased its share of seat miles flown.

The type24 of aircraft has shifted, too, from ‘wide-body’ (Boeing 747, DC10) to ‘city jet’ (Boeing 737 type). As one illustration, the 737-200 model accounted, in2007, for 91 percent of the old Western aircraft types in operation in Africa.

The increasing use of modern aircraft has an impact, as is highlighted below, onincreasing fuel efficiency, especially important in an environment of rising fuel costs.Increased fuel efficiency saved the industry an estimated US$2.1 billion in 2007,Since 2001, fuel efficiency has increased about 16.5 percent, with every one percentin industry fuel efficiency reducing annual fuel costs by about US$700 million. TheBoeing 787 and Airbus A320 target a fuel efficiency of three litres per 100 passengerkm, which is better than a compact car.25

24 GA: Up to around a Beechcraft King Air, Twin Otter not included; Commuter Propeller: ATR, Dash-8’s,Fokker, etc., Twin Otter included; Commuter Jet: Embraer type, Fokker 100, Canadair, etc; CityJet: Boeing737-type category; Big Jet: Larger, but not wide body. Boeing 757, 707s and DC-8s; Widebody: 747, A310,DC10 (MD11), etc.; Super Widebody: A380 (none in Africa yet); Eastern Built: Not further broken down bysize. From Bofinger, op cit, 27 February 2008.

25 Ana McAhron-Schulz, op cit, April 2008.

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 16/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

15

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 17/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

16

Airline Competitiveness

Airline competitiveness depends both on strategic (which model) and operational(which aircraft, which routes, what frequency) considerations.

In simple terms, the choice of aircraft has to be matched to routes and passengerloads. This is based both on historical data and marketing projections. These can beinfluenced by political developments, notably open skies, and economic growth (or,conversely, contraction).

A typical low-cost (and profit-making) carrier would have the following costbreakdown (in percentages):

Fuel: 40 (possibly more at 2008 oil prices) Aircraft capital costs: 10 Labour: 15 Maintenance: 15 Handling: 10 Overheads, including marketing and catering: 10

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 18/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

17

The above breakdown can be altered by using very old planes (bringing down thecapital figure to around 5%, but at the cost of rising fuel and maintenance costs). In

the 1920s, the cost of transporting apassenger by aircraft 1.600km wasapproximately US$1 per kilometre; in the21st century this has fallen thirty-fold.Today’s 747 fuel per available seatkilometre (ASK) costs show an 85%improvement over a four-engined DC4,for example. Outside of Africa, low-costcarriers work on a cost ratio of around 6US cents per ASK on short-haul (underthree hours) routes. Africa’s low-costcarriers operate at around that margin;the unprofitable carriers about twice asmuch. Profitability is also a factor of load:

during 2007, international load factors reached an industry record of 77%, up from76% t in 2006.

IATA Industry P rofits, 1998-200826 (forecast)

There is also a balance between getting away with paying lower staff costs(especially for pilots, who can make up over 50% of the salary bill in airlines) andstaff retention of maintenance personnel and pilots. This is especially a problem inAfrica, given that such skills are highly mobile, easily affected by political whims andeconomic troubles, and slow to be replaced.

A further complicating factor is code-share agreements. Essentially this refers to the

practice where a flight operated by an airline is jointly marketed as a flight for one ormore other airlines. This enables passengers to book through one airline on routesnot necessarily serviced by them, and offers airlines both exposure and the ability togain market share on routes through others through payment schemes.

What does this mean?

26 Ana McAhron-Schulz, op cit, April 2008.

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 19/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

18

Cost controls are especially important, as is the right infrastructure and rightequipment in finding a balance between older aircraft with higher fuel andmaintenance costs and newer, more expensive, cheaper-to-run versions. As ageneral rule, the newer aircraft that the airline can afford to fly, the better it is. Asecond general rule is, if you can afford to hold it on the balance sheet, buy ratherthan lease it. But few African airlines bar a few (SAA and Kenya, for example) areable to afford to buy aircraft en masse in the sort of numbers that enable largediscounts from the manufacturer – a practice that Ryanair has reputedly perfected.

Aircraft Operating Costs27

Regional Jets and Turbo-Props

The example of regional jets (RJs) in the United States is a case in point of howdifferent solutions are preferred to solve perceived air needs and how, too, thesechange rapidly over time.

Currently, moves are afoot to US regional jet capacity, there being over 1,600 RJs inoperation. It is anticipated that there will be around half of this number in US skiesin future. Thus there are likely to be a glut of 50-seat RJs (such as BombardierCRJ200s, Embraer ERJ-145s and Avro 146s) on the leasing and sale market in thenear future as the major airlines, including Continental and Delta, begin culling such

fleets.28

RJs became popular as part of the hub-and-spoke concept as replacement for turbo-prop aircraft. High fuel costs have forced this change of direction, placing pressureon this already mature US market and highlighting the need for replacing the less-economical and relatively under-utilised RJs with larger capacity aircraft – in the

27 From Schlumberger, op cit, 11 March 2005.

28 See Flight International, 29 April-5 May 2008.

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 20/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

19

100-seat range – especially at feeder carriers. This also reflects the preferencechange from hub-and-spoke to point-to-point operations. The bottom line is that inthe US market there are just too many 50-seaters currently. And although they areless expensive to operate per hour, their low passenger and very low cargo capacityresults in a higher cost per seat. Additionally, as skies and runways in the US havebecome more congested, the proliferation of RJs has contributed significantly to in-flight and airport delays.

It is suggested that the use of RJs might be a way for smaller African airlines to go.However, one must remember that this depends on loads: as stated, an RJ’s costshave to be divided by the seat loading. If a 50-seat capacity is what the market willsupport, then the RJ might be the best aircraft for the route. RJs still have amongthe highest seat-per-kilometre costs. A larger aircraft of the same generation, at thesame load factor (proportion of seats filled relative to capacity), with far greatercargo capacity, could prove to be cheaper to operate.

Turbo-props are slower and noisier, but considerably cheaper to run and topurchase. With the high fuel price, their 30% saving on fuel per seat kilometre is anattractive option. Such aircraft generally also perform better on short and rough

fields.

Liberalisation and Open Skies

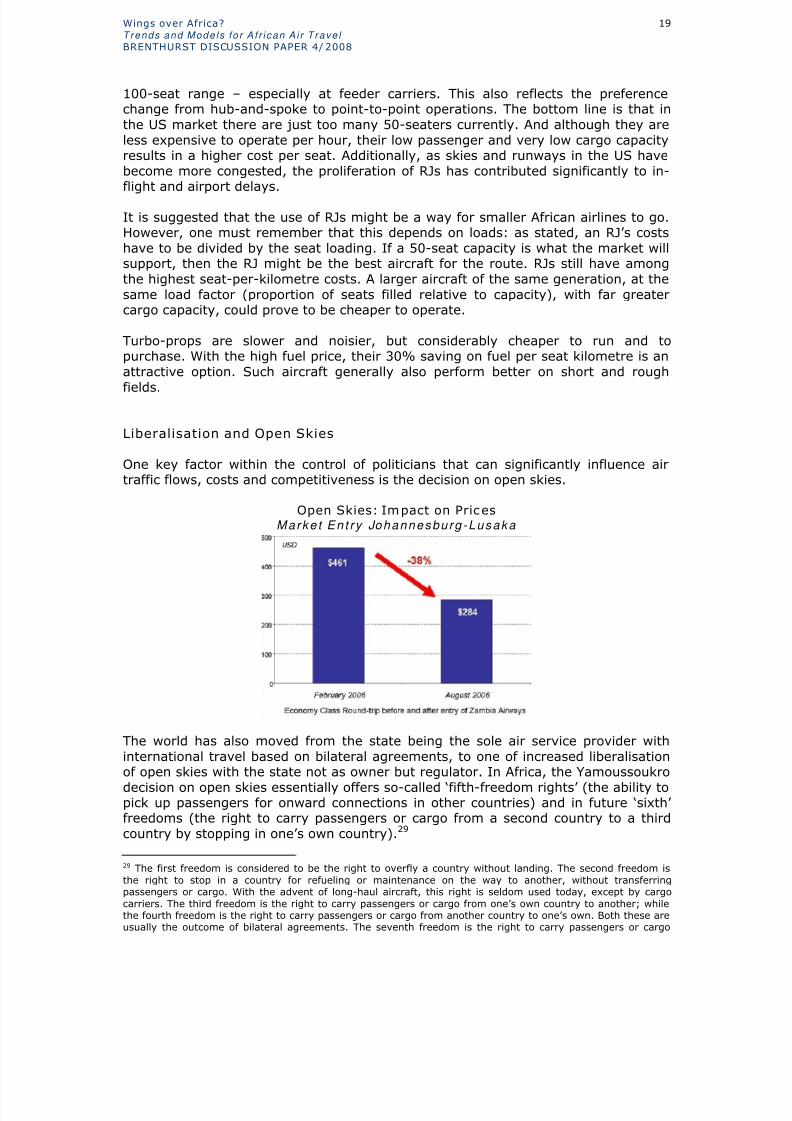

One key factor within the control of politicians that can significantly influence airtraffic flows, costs and competitiveness is the decision on open skies.

Open Skies: Impact on Prices

Marke t En t ry Johannesbu rg -Lusaka

The world has also moved from the state being the sole air service provider withinternational travel based on bilateral agreements, to one of increased liberalisationof open skies with the state not as owner but regulator. In Africa, the Yamoussoukro

decision on open skies essentially offers so-called ‘fifth-freedom rights’ (the ability topick up passengers for onward connections in other countries) and in future ‘sixth’ freedoms (the right to carry passengers or cargo from a second country to a thirdcountry by stopping in one’s own country).29

29 The first freedom is considered to be the right to overfly a country without landing. The second freedom isthe right to stop in a country for refueling or maintenance on the way to another, without transferringpassengers or cargo. With the advent of long-haul aircraft, this right is seldom used today, except by cargocarriers. The third freedom is the right to carry passengers or cargo from one’s own country to another; whilethe fourth freedom is the right to carry passengers or cargo from another country to one’s own. Both these areusually the outcome of bilateral agreements. The seventh freedom is the right to carry passengers or cargo

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 21/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

20

The Price of P rotection

Key Mozam b ique Rou tes Com pared to Sim i la r

Open skies means, in effect, removing constraints on a given route in terms of thenumber of air carriers, frequency of flights and seats per flight. As such, it offersmajor advantages and not just for the cost of tickets and frequency of flights, as

detailed by the figures above and below.30 However, open skies has been slow to beadopted, given protectionist instincts. An absence of liberalisation has implicationsbeyond just the price of tickets to include the expenditure available for the upgradingof services, including air traffic control and airports. There have been just tenprivatisation/concession processes with African airports since 1996: Cameroon, Côted’Ivoire, Kenya, Madagascar (a 15-year concession ended in 2006), Mauritius, SouthAfrica (Airports Company, Rand, Mpumalanga and Kruger Park) and Tanzania.

Open Skies: Impact on Volumes

Johannesbu rg -Na i rob i

between two foreign countries without continuing service to one’s own country. The United Kingdom andSingapore have agreed, from 30 March 2008, to allow unlimited seventh freedom rights. The eighth freedom isthe right to carry passengers or cargo within a foreign country with continuing service to or from one’s owncountry. The ninth freedom is the right to carry passengers or cargo within a foreign country without continuingservice to or from one’s own country.

30 These tables were prepared by Genesis Analytics for The Brenthurst Foundation in preparation for thePresidential International Advisory Board of the Government of Mozambique in November 2007.

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 22/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

21

Open Skies: Impact of Discount Airlines

London -Ba rce lona

While the benefits of the opening of the skies are beyond doubt, the when, how andimmediate impacts are a more difficult calculation, since it may lead to a

proliferation of smaller carriers and, initially, considerable market volatility.

None of the above should understate the importance of airport infrastructure inbuilding African airlines. This is not only essential in terms of safety and passengercomforts, but for the growth envisaged by African countries in terms of their use as

‘clearing houses’ for high-value agriculture exports. Storage and distribution facilitiesare crucial for perishables. This helps to explain why those countries in need of financing, management and technology to modernise their airports have looked toprivatise them. This applies equally to the operational (air traffic, policing,maintenance, meteorology, services), handling (cleaning, customs, baggage, fuel,etc.) and commercial (duty-free shops, banks, bars, restaurants, parking, etc.)aspects.

Airport Public-Private-Investment Models31

31 Schlumberger, op cit, 11 March 2005.

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 23/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

22

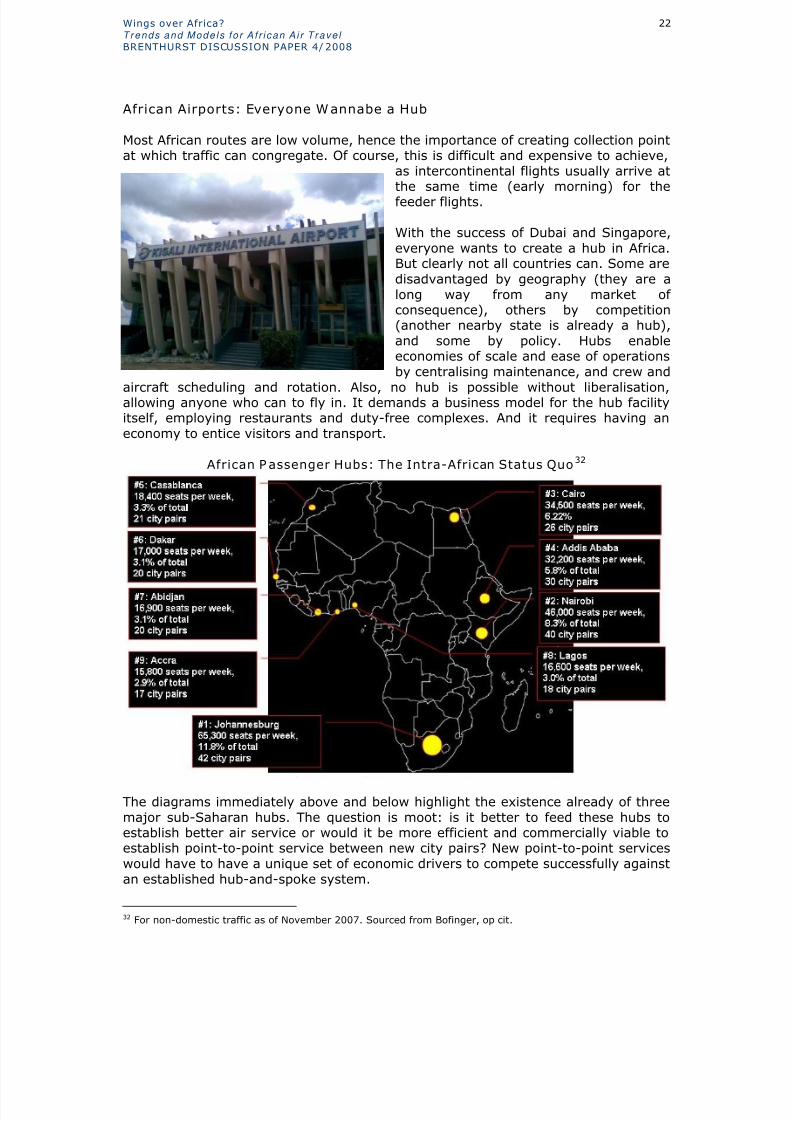

African Airports: Everyone Wannabe a Hub

Most African routes are low volume, hence the importance of creating collection pointat which traffic can congregate. Of course, this is difficult and expensive to achieve,

as intercontinental flights usually arrive atthe same time (early morning) for thefeeder flights.

With the success of Dubai and Singapore,everyone wants to create a hub in Africa.But clearly not all countries can. Some aredisadvantaged by geography (they are along way from any market of consequence), others by competition(another nearby state is already a hub),and some by policy. Hubs enableeconomies of scale and ease of operationsby centralising maintenance, and crew and

aircraft scheduling and rotation. Also, no hub is possible without liberalisation,allowing anyone who can to fly in. It demands a business model for the hub facilityitself, employing restaurants and duty-free complexes. And it requires having aneconomy to entice visitors and transport.

African Passenger Hubs: The Intra-African Status Quo32

The diagrams immediately above and below highlight the existence already of threemajor sub-Saharan hubs. The question is moot: is it better to feed these hubs toestablish better air service or would it be more efficient and commercially viable toestablish point-to-point service between new city pairs? New point-to-point serviceswould have to have a unique set of economic drivers to compete successfully againstan established hub-and-spoke system.

32 For non-domestic traffic as of November 2007. Sourced from Bofinger, op cit.

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 24/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

23

Passenger Hubs: The In tercontinental African Status Quo33

With all of the above in mind, what might an African model look like?

An African Model: A ‘Third Way’?

Tourism is touted as an African niche in globalisation. After all, it is difficult to seehow most African countries can compete in low-end manufacturing against China andother Asian work forces. Here airlines have a crucial role to play in accessing Africanmarkets.

Global and African Tourism Flows34

1990 1995 2000 2006 Africa 15,200 20,311 28,184 40,900 (3.4%)

World 455,900 539,565 686,738 842,000

Overall, if Africa is to be more prosperous, it is generally accepted it must be a placethat is:

more accessible; cost-competitive; open for business; and offers a decent standard of living, health, and education for all of its citizens.

How might this be achieved with respect to air traffic?

Comparing point-to-point with a hub-and-spoke model is difficult because by theirvery nature they do not compete directly on the same city pairs. It would always bemore desirable to fly directly from Beira to Lusaka, but the traffic would have tosupport it. Point-to-point has enjoyed a great success in Europe because of a fairlywell developed infrastructure and enough city pairs with high numbers of origin and

33 As of November 2007. Sourced from Bofinger, ibid.

34 Source: World Tourism Organisation.

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 25/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

24

destination (so-called O&D) traffic that were able and inclined to pay the low faresoffered. (When Southwest first got started it claimed it was not competing with otherairlines. It said it was competing with the bus lines.) One study35 of the AfricanDevelopment Bank shows, for example, that of the 276 city pairs in West Africa lessthan 5% generates more than 150 passengers per day. But 85% of the city pairsgenerate less than 70 passengers per day. Thus getting the proper fleet mix androute structure in any regional airline is the key component of any airline strategy.

For some African markets there may be a ‘third way’ in the hub-and-spoke versuspoint-to-point model debate, and that would be taking a bit of both (perhaps a ‘hub-to-point’ service). For point-to-point to work there must be sufficient O&D in the citypairs, and the aircraft should be matched to the route. However point-to-pointservice breaks down after connecting the more recognised city pairs. Chicago-Pariswork but Nashville-Budapest or Beira-Lusaka does not. So there must be a gatheringof like-minded people for the long-haul portion of the flight.

Longer turnaround times for hub-and-spoke aircraft are acceptable if they havecompleted long-haul flights; so even though it may take longer to turn it out again,they has been utilized for a considerable amount of productive time (known as the

daily ‘ute’ rate) The turnaround time for smaller aircraft that have been out collectinglike-minded people can be acceptable if managed properly and some separatefacilities at the airport are available. The pros and cons of this debate are manifest inthe strategic difference between the Airbus A380 and the Boeing 787.

While this is interesting, its application for a regional African airline is doubtful –other than defining the outside aviation world with which it has to connect.

For Africa, the imperative for a major code-share partner is essential: i.e, a long haulfrom Europe, United States, Asia and other places to the international arrival airportwith regional distribution of passengers from there. But with recent ICOA, IATA, FAAand other restrictions of code-shares and liability exposure, the local carrier wouldhave to pass an international audit. Fortunately there are many programmes

developed by the above mentioned organizations as well as the World Bank andother trade associations.36

Thus the factors that influence the African airline model are:

Liberalisation and competition: The extent of open skies will have a significantbearing on flight frequencies and costs. The deregulation imperative – gettinggovernment out of the business of airlines and airports – will not only assistcompetitiveness and reduce government burdens, but will enable governmentagencies to concentrate on the aspects which they do best: regulation, oversightand policy setting.

35

ADB, op cit.36 The World Bank Group through its various components (International Development Association, InternationalFinance Corporation, International Bank for Reconstruction and Development, and Multilateral InvestmentGuarantee Agency) has made available more than US$1 billion to support aviation development throughout theworld. Additionally The International Civil Aviation Organization (ICAO) has set up several programs specificallyto promote safety and help train aviation specialist in Africa. The International Air Transport Association, IATA,has developed a program of Operation Safety Audits to assist airlines in achieving compliance with ICOA rulesand regulations. IATA also has set up a working group ASET, Aviation Safety Enhancement Team, for theexpress purpose of reducing Africa’s unacceptable accident rate. The FAA in the US conducts its annualInternational Aviation Training Symposium which many African countries participate. The Air Transport ActionGroup is also very active in not only promoting aviation safety but it also to promote best practices in aviationmanagement.

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 26/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

25

Drivers: Passengers need reasons (tourism, business, visiting friends andrelatives, etc.) to travel. The more reasons, the greater the passenger loads.

Location: Proximity to a regional hub will assist improve connectivity withinternational traffic.

Attraction of strategic airlines: This is especially essential for those countrieswithout absent frequently serviced intercontinental routes by their domesticairline, and dependent on tourism income. Being serviced by a reliable and

‘branded’ airline is a critical component in building a tourism market. The reverseis also true: having a bad nationally branded one can do a lot of damage.

Routes, Planes, and Fuel: The viability of airlines is a calculation based on fuel,routes and load factors. If governments, where there is partial state ownership,demand the servicing of politically important routes, this may not becommercially viable.

Access to experienced management: Airlines and airports are complexbusinesses best left to professionals. Even if government does not wish torelinquish entirely, for strategic or business reasons, its stakes in this sector, itshould contract the management of entities to specialists.

And the competitiveness (or not) of African airlines relates to: 37

the use of modern technology from aircraft to e-tickets, billing and collection; membership of world air alliance enabling connectivity and feeder routes; political interference from governments that fail to put profitability first; under-capitalisation and a shortage of financing and skilled personnel; low incomes of populations, leading to small markets in which it is difficult to

generate sufficient returns on investment;38 poor management and ignorance by the private sector; and the proliferation of smaller, often short-lived carriers, which increases market

volatility even though it might lead, temporarily, to a consumer boom.

These are some of the basics to fix if African countries are to compete in one sectorwhere there is great promise for growth and economic reward beyond the sector.

Conclusion: Towards a Virtuous Cycle

Air routes and traffic are essential components of development, especially for land-locked nations. But what are the factors that go into devising an air-traffic growthstrategy?

Although it might be the catalyst for reform, this is not fundamentally aboutreforming loss-making national airlines. Indeed, the national airline should be asecondary consideration in this process. A number of much more important andcentral factors have to be considered in developing a strategy:

The first is the overall economic environment that the air sector will service and intowhich it will integrate.

37 ADB, op cit, p.40.

38 According to the ADB report, it has been proven, however, that during stable periods the average growthrate of air traffic is double that of GDP; for example, the growth in world traffic is double that of world GDPincreases over the past three decades.

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 27/29

Wings over Africa?

Trends and Mode ls f o r A f r ican A i r T rave l BRENTHURST DISCUSSION PAPER 4/ 2008

26

The second factor is that making countries a good place for people and things to flyin and out of is far more important than having a healthy national airline or airport.In this there are many things than can be done more easily than others, whichdemands setting priorities. This includes everything from developing adventuretourism experiences to easing the visa restrictions on visitors and opening the skiesto competition. Indeed, the critical first consideration in reforming (and growing) airtraffic is liberalisation: nothing much can be achieved without opening the skies, andnot just rhetorically.

The Virtuous Air Traffic-Economic Growth Circle

So a lot of this is about policy, setting priorities and making things happen. Thefuture of the national airline may be one answer to another, more importantquestion: What is required to get more people to fly to a destination? And this is onlyone dimension to the imperative of getting more people and goods to and fromAfrica cheaper, easier and with a much greater degree of safety.

With the above in mind, there are a number of things that countries can do toencourage air traffic:

Open Skies and Commercialisation - There is no option but to liberalise toincrease the flow and volume of air traffic arrivals to and from a destination. Thisdemands liberalisation and openness, and attention to the details on the drivers fromtourism to shopping that will bring people. A national airline should not be protectedat the expense of openness.

Get CAAs out of Business and into Regulation – The commercialisationimperative extends to airports: every effort must be made to get Civil AviationAuthorities out of business and into regulatory roles, and also to find ways toincrease investment in airport facilities and management. The easiest wayinternationally to achieve this has been through concessioning or privatisation,

Air Traffi c

Safety & Security

EfficiencyEase of Transit

Hotels

EconomicDrivers:Tourists

Business- Visitors

Shoppers

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 28/29

8/6/2019 BD0804 Air Travel in Africa

http://slidepdf.com/reader/full/bd0804-air-travel-in-africa 29/29