bernstein energy drivers of decline rates in mature hydrocarbon

TRANSCRIPT

BernsteinResearch.com European/Russian Oil & Gas – April 2012

Bernstein EnergyDrivers of Decline Rates in Mature Hydrocarbon Basins & The Need for Enhanced Oil Recovery

April 2012

See Disclosure Appendix of this publication for important disclosures and analyst certifications

Oswald Clint PhD, ACASenior Research Analyst

[email protected]+44 20 7959 5089

Iain Pyle, CFA, ACASenior Research Associate

[email protected]+44 20 7170 0564

Rob WestResearch Associate

[email protected]+44 20 7170 0589

Oswald Clint PhD, ACASenior Research Analyst

European Oil & Gas

+ (44) 20 7170 5089

Rob WestResearch Associate

European Oil & Gas

+ (44) 20 7170 0589

BernsteinResearch.com European/Russian Oil & Gas – April 2012

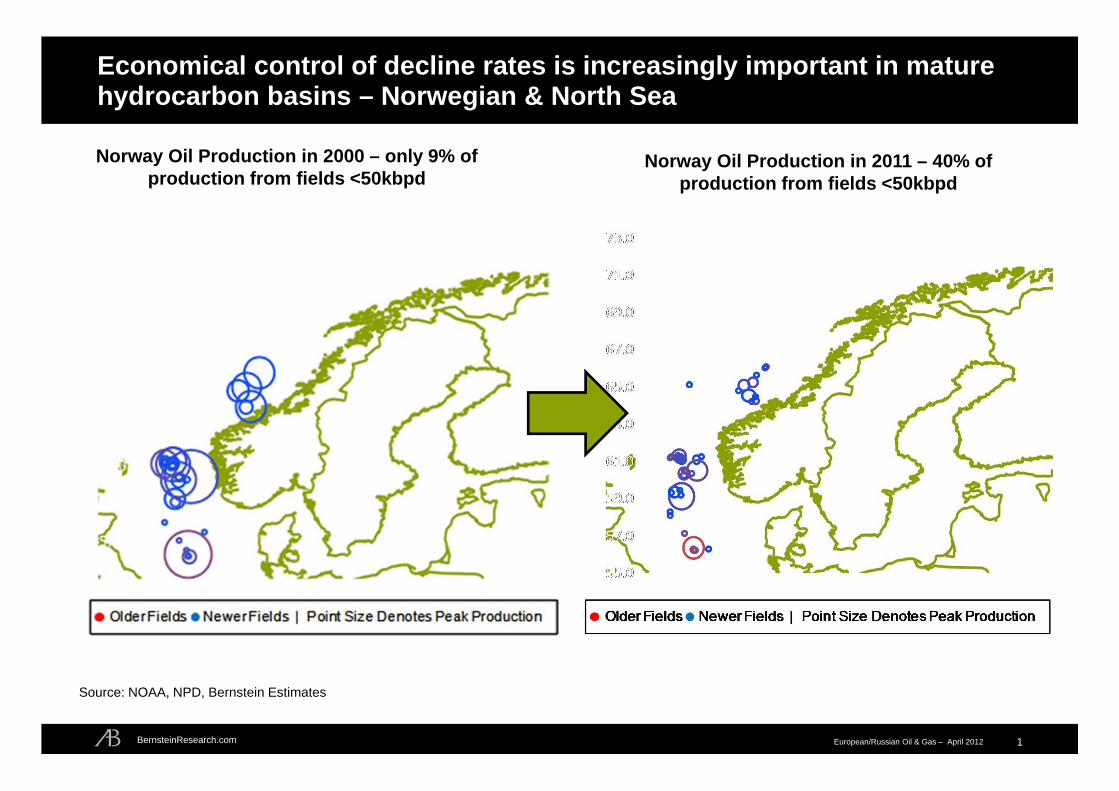

Economical control of decline rates is increasingly important in mature hydrocarbon basins – Norwegian & North Sea

1

Norway Oil Production in 2000 – only 9% of production from fields <50kbpd

Norway Oil Production in 2011 – 40% of production from fields <50kbpd

Source: NOAA, NPD, Bernstein Estimates

BernsteinResearch.com European/Russian Oil & Gas – April 2012

Economical control of decline rates is increasingly important in mature hydrocarbon basins – U.K. North Sea

2

UK North Sea Oil Production in 1995 – only 11% of production from fields <5kbpd

UK North Sea Oil Production in 2011 – 42% of production from fields <5kbpd

Source: NOAA, DECC, Bernstein Estimates

BernsteinResearch.com European/Russian Oil & Gas – April 2012

Median y-o-y changes in production have averaged -12.2% and -9.3% in the UK and Norway, with -21.7% average natural declines in both basins

3

2.4%

-7.6%-12.2%

-24.6%

-12.2%

-20.1%-21.7%

-29.7%

-40%

-30%

-20%

-10%

0%

10%

20%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

y-o-

y C

hang

e in

Fie

ld P

rodu

ctio

n (%

)

Percentile

All Data All Declining Fields with No New Wells Drilled Quartiles Mean Average

Benefits arising from field ramp‐up, infrastructure ramp‐up, EOR, reservoir management and new well completions

3.9%

-4.6%-9.3%

-20.4%

-11.0%

-20.4%-21.7% -30.6%

-40%

-30%

-20%

-10%

0%

10%

20%

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

y-o-

y C

hang

e in

Fie

ld P

rodu

ctio

n (%

)

PercentileAll Data All Declining Fields with No New Wells Drilled Quartiles Mean Average

Benefits arising from field ramp‐up, infrastructure ramp‐up, EOR, reservoir management and new well completions

UK North Sea

•240 oil fields• Monthly production data since first oil in the basin•Median y-o-y change in production = -12.2% • Mean Average Natural decline rates of -21.7%

Norwegian Offshore Sector

•83 oil fields• 3700 development wellbores• Monthly production data since first oil in the basin•Median y-o-y change in production = -9.3% • Mean Average Natural decline rates of -21.7%

Source: NPD, DECC, Bernstein Estimates

UK

Norway

BernsteinResearch.com European/Russian Oil & Gas – April 2012

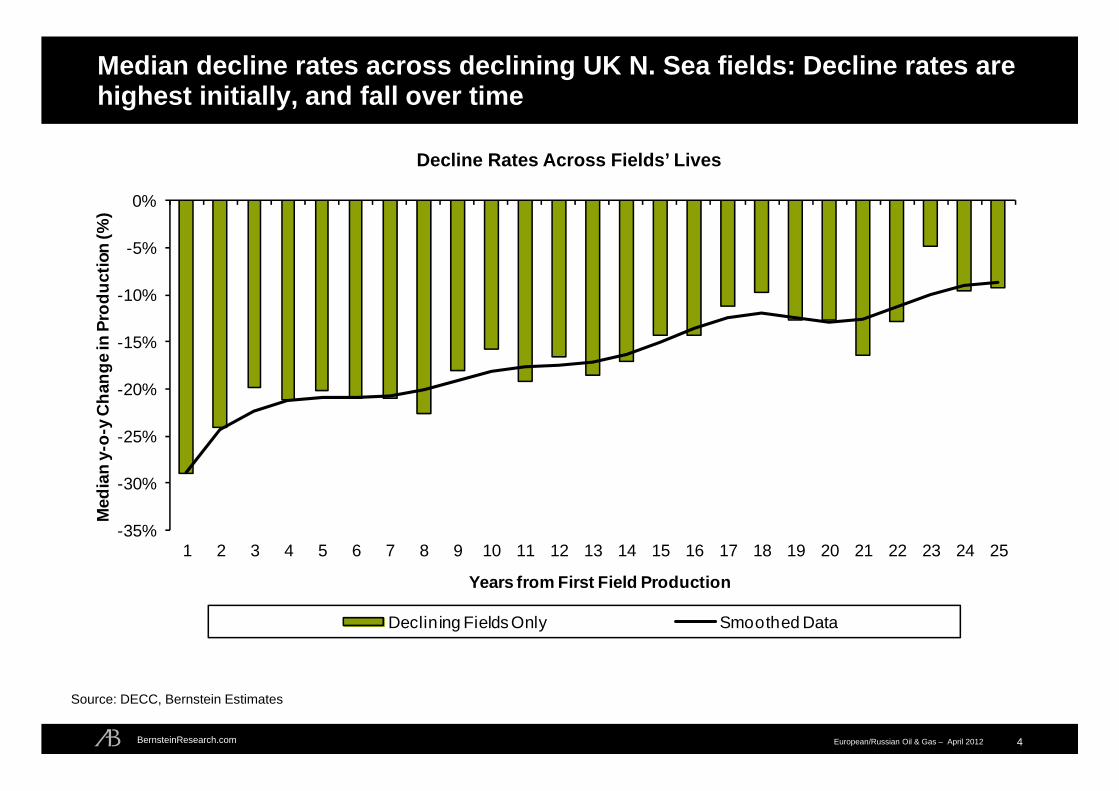

Median decline rates across declining UK N. Sea fields: Decline rates are highest initially, and fall over time

4

Source: DECC, Bernstein Estimates

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25

Med

ian

y-o-

y C

hang

e in

Pro

duct

ion

(%)

Years from First Field Production

Declining Fields Only Smoothed Data

Decline Rates Across Fields’ Lives

BernsteinResearch.com European/Russian Oil & Gas – April 2012

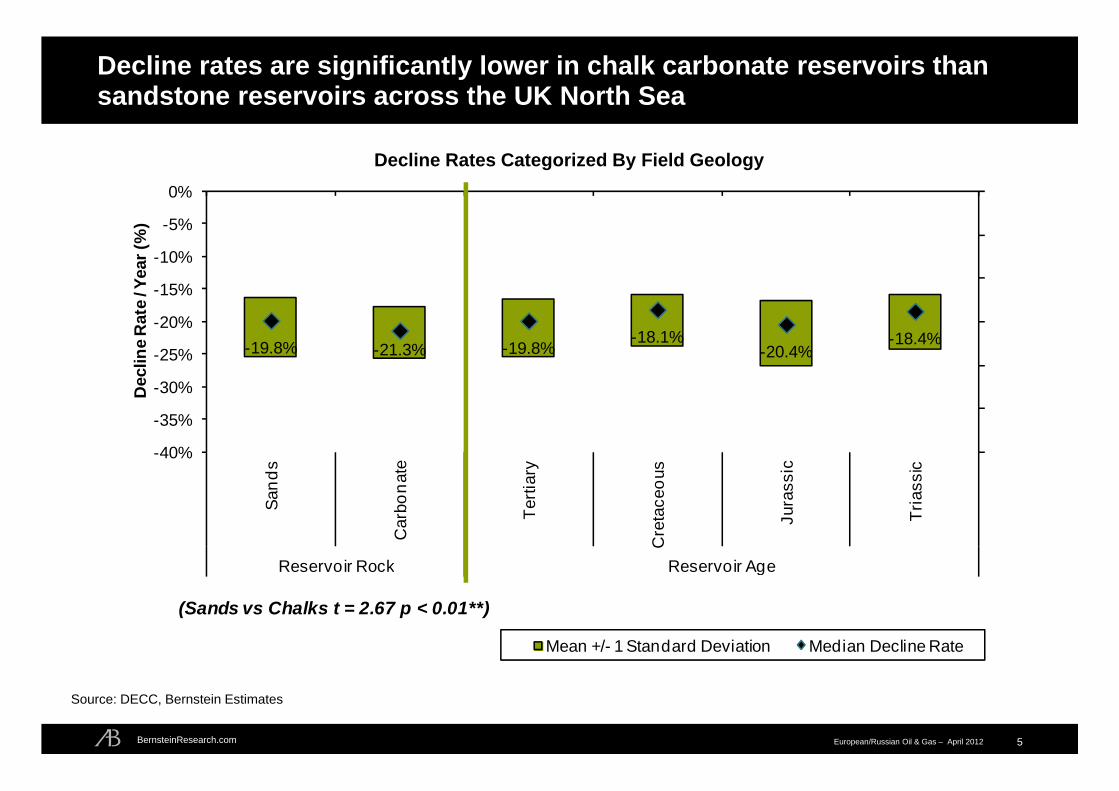

Decline rates are significantly lower in chalk carbonate reservoirs than sandstone reservoirs across the UK North Sea

5

Source: DECC, Bernstein Estimates

-19.8% -21.3% -19.8%-18.1%

-20.4%-18.4%

50%

60%

70%

80%

90%

100%

110%

-40%

-35%

-30%

-25%

-20%

-15%

-10%

-5%

0%

Sand

s

Car

bona

te

Terti

ary

Cre

tace

ous

Jura

ssic

Tria

ssic

Reservoir Rock Reservoir Age

Dec

line

Rat

e / Y

ear (

%)

Mean +/- 1 Standard Deviation Median Decline Rate

(Sands vs Chalks t = 2.67 p < 0.01**)

Decline Rates Categorized By Field Geology

BernsteinResearch.com European/Russian Oil & Gas – April 2012

“Just drill more wells” – the simplest approach to slowing decline rates

6

-15%

-10%

-5%

0%

5%

10%

15%

0 1 2 3 4 5+A

vera

ge O

il P

rodu

ctio

n (A

ll fie

lds,

y-

o-y

%)

New Wells Completed In Calendar Year

-15%

-10%

-5%

0%

5%

10%

15%

0 1 2 3 4 5+

Ave

rage

Cha

nge

in O

il P

rodu

ctio

n

(All

Fiel

ds y

-o-y

%)

New Wells Completed In Calendar YearSource: NPD, DECC, Bernstein Estimates

0

10

20

30

40

50

60

70

80

1985

1987

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

Cum

ulat

ive

Dev

elop

men

t Wel

ls D

rille

d Pe

r Fie

ld

Norway (All Fields)UK (Oil Fields)

Wells Per Field in Norway & the UK y-o-y production -vs- the number of new production wells completed

UK

Norway

BernsteinResearch.com European/Russian Oil & Gas – April 2012

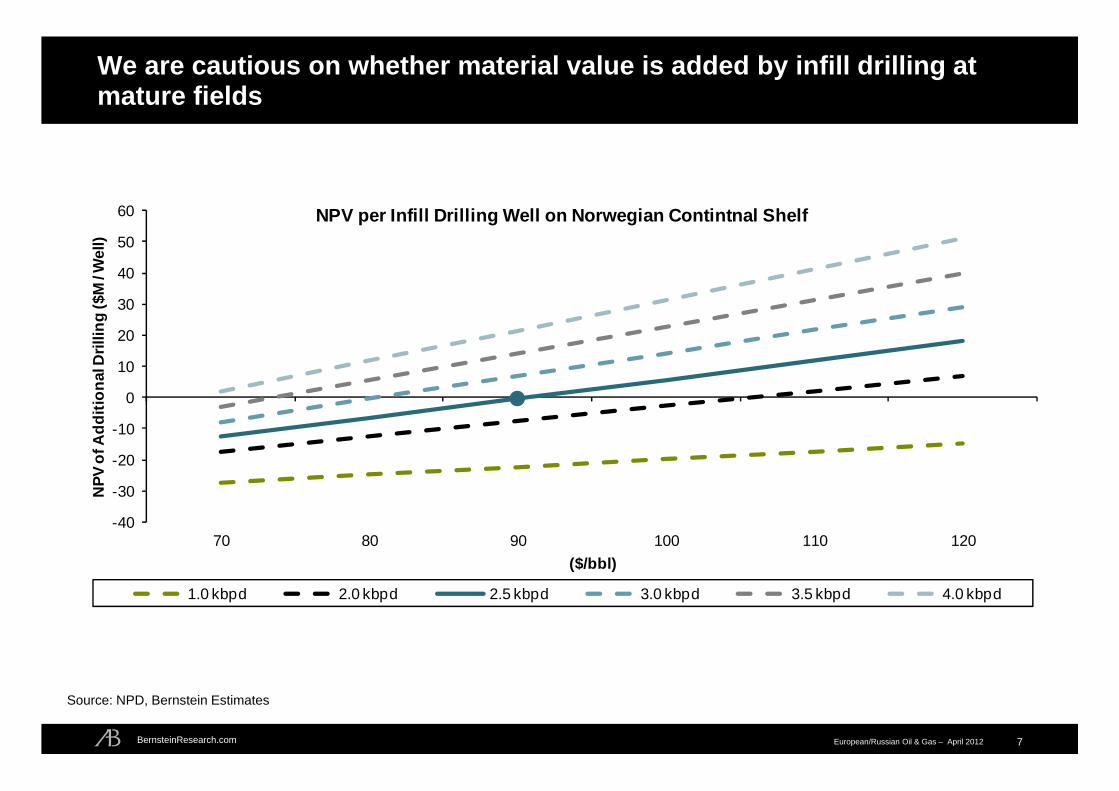

We are cautious on whether material value is added by infill drilling at mature fields

7

-40

-30

-20

-10

0

10

20

30

40

50

60

70 80 90 100 110 120

NPV

of A

dditi

onal

Dril

ling

($M

/ Wel

l)

($/bbl)

NPV per Infill Drilling Well on Norwegian Contintnal Shelf

1.0 kbpd 2.0 kbpd 2.5 kbpd 3.0 kbpd 3.5 kbpd 4.0 kbpd

Source: NPD, Bernstein Estimates

BernsteinResearch.com European/Russian Oil & Gas – April 2012

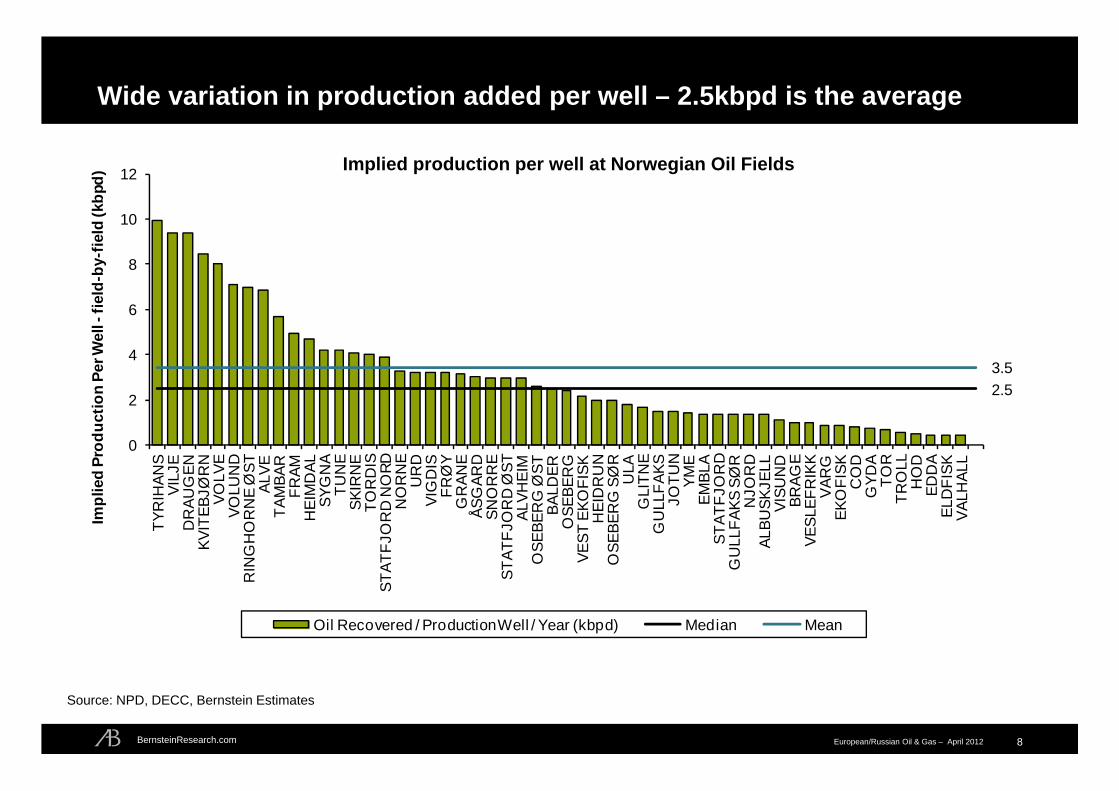

Wide variation in production added per well – 2.5kbpd is the average

8

2.53.5

0

2

4

6

8

10

12TY

RIH

ANS

VILJ

ED

RAU

GEN

KVIT

EBJØ

RN

VOLV

EVO

LUN

DR

ING

HO

RN

E Ø

STAL

VETA

MBA

RFR

AMH

EIM

DAL

SYG

NA

TUN

ESK

IRN

ETO

RD

ISST

ATFJ

OR

D N

ORD

NO

RN

EU

RD

VIG

DIS

FRØ

YG

RAN

EÅS

GAR

DSN

OR

RE

STAT

FJO

RD

ØST

ALVH

EIM

OSE

BER

G Ø

STBA

LDER

OSE

BER

GVE

ST E

KOFI

SKH

EID

RU

NO

SEBE

RG

SØ

RU

LAG

LITN

EG

ULL

FAKS

JOTU

NYM

EEM

BLA

STAT

FJO

RD

GU

LLFA

KS S

ØR

NJO

RD

ALBU

SKJE

LLVI

SUN

DBR

AGE

VESL

EFR

IKK

VAR

GEK

OFI

SKC

OD

GYD

ATO

RTR

OLL

HO

DED

DA

ELD

FISK

VALH

ALL

Impl

ied

Prod

uctio

n Pe

r Wel

l -fie

ld-b

y-fie

ld (k

bpd)

Oil Recovered / Production Well / Year (kbpd) Median Mean

Source: NPD, DECC, Bernstein Estimates

Implied production per well at Norwegian Oil Fields

BernsteinResearch.com European/Russian Oil & Gas – April 2012

The past five years have seen an acceleration in production from smaller fields – how does this change the economics of infill drilling?

9

0%

10%

20%

30%

40%

50%

60%

Jan-85 May-87 Sep-89 Jan-92 May-94 Sep-96 Jan-99 May-01 Sep-03 Jan-06 May-08 Sep-10

Prop

ortio

n of

Pro

duct

ion

From

Fie

lds

Belo

w

Each

Thr

esho

ld

Proportion of Fields Producing Below Threshold Values

60kbpd 50kbpd 40kbpd 30kbpd 20kbpd 10kbpdThreshold:

Source: NPD, Bernstein Estimates

BernsteinResearch.com European/Russian Oil & Gas – April 2012

Reliance on infill drilling increases vulnerability to rising rig rates

10

0

50

100

150

200

250

300

350

400

450

500

0

50

100

150

200

250

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Nor

th S

ea R

ig R

ate

(Tho

usan

ds D

olla

rs / D

ay)

Nor

way

-N

umbe

r of D

evel

opm

ent W

ells

Dril

led

Norway Development Wells Drilled Y-o-Y Change in Rig Rate

Norway – New Development Wells Drilled versus Rig Rates

Source: DECC, ODS-Petrodata, Bernstein Estimates

BernsteinResearch.com European/Russian Oil & Gas – April 2012

The difficulty of economical EOR is exacerbated by the UK higher supplementary tax rate - Are Operators Just Shutting Down?

11

0

2

4

6

8

10

12

14

16

18

20

0

2

4

6

8

10

12

14

Jan-96 Oct-97 Jul-99 Apr-01 Jan-03 Oct-04 Jul-06 Apr-08 Jan-10

NB

P G

as P

rice

($/m

cf)

Shut

In +

Shu

t Dow

n C

apac

ity (T

TM, B

cfd)

Capacity Shut Iin Capacity Shut Down Production UK NPNatural Gas Prices ($/mcf)

Source: DECC, Bernstein Estimates

UK North Sea Gas Production, Shut Ins and Shut Downs -vs- the NBP Gas Price

BernsteinResearch.com European/Russian Oil & Gas – April 2012

Injection wells reduce the decline rates at UK and Norwegian fields, with effects well beyond the years they are initially drilled

12

Effect of Injection Wells on Field Decline Rates

-12.5%

-10.8%

-6.3%

-8.6%

-14.0%

-12.0%

-10.0%

-8.0%

-6.0%

-4.0%

-2.0%

0.0%

Norway UK (Water Injection Only)

Med

ian

y-o-

y C

hang

e in

Fie

ld P

rodu

ctio

n (%

)

Fields With No Injection Fields With Injection Wells

Source: NPD, DECC, Bernstein Estimates

BernsteinResearch.com European/Russian Oil & Gas – April 2012

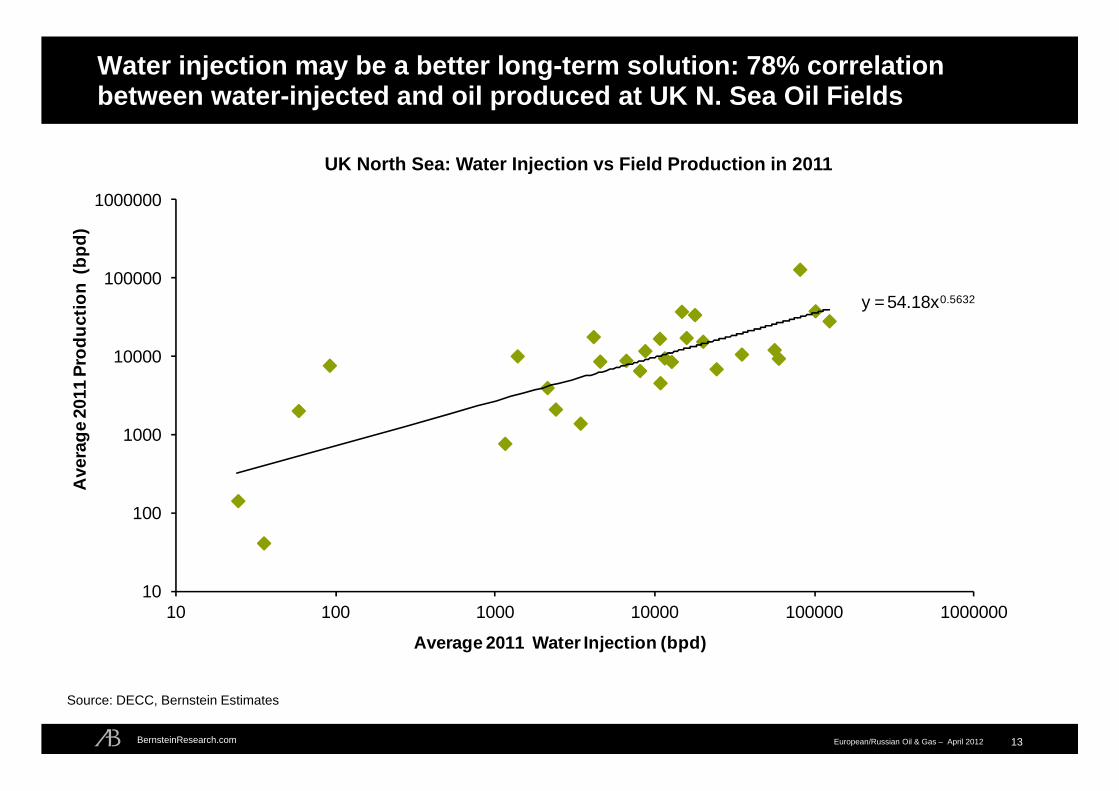

Water injection may be a better long-term solution: 78% correlation between water-injected and oil produced at UK N. Sea Oil Fields

13

y = 54.18x0.5632

10

100

1000

10000

100000

1000000

10 100 1000 10000 100000 1000000

Ave

rage

201

1 Pr

oduc

tion

(bpd

)

Average 2011 Water Injection (bpd)

UK North Sea: Water Injection vs Field Production in 2011

Source: DECC, Bernstein Estimates

BernsteinResearch.com European/Russian Oil & Gas – April 2012

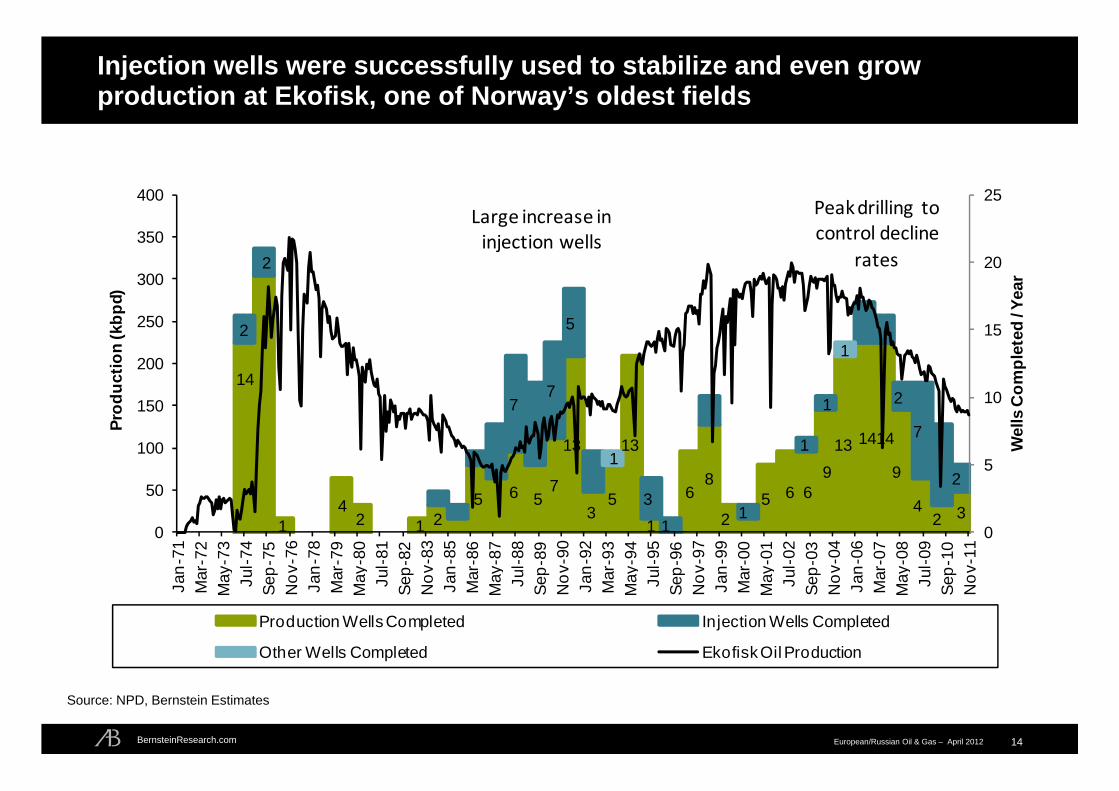

Injection wells were successfully used to stabilize and even grow production at Ekofisk, one of Norway’s oldest fields

14

14

14

2 1 25 6 5

7

13

35

13

1

68

25 6 6

913 1414

9

42 3

2

2

77

5

31

1

1

1 2

7

21

1

0

5

10

15

20

25

0

50

100

150

200

250

300

350

400Ja

n-71

Mar

-72

Ma y

-73

Jul-7

4Se

p-75

Nov

-76

Jan-

78M

ar-7

9M

a y-8

0Ju

l-81

Sep-

82N

ov-8

3Ja

n-85

Mar

-86

Ma y

-87

Jul-8

8Se

p-89

Nov

-90

Jan-

92M

ar-9

3M

a y-9

4Ju

l-95

Sep-

96N

ov-9

7Ja

n-99

Mar

-00

Ma y

-01

Jul-0

2Se

p-03

Nov

-04

Jan-

06M

ar-0

7M

a y-0

8Ju

l-09

Sep-

10N

ov-1

1

Wel

ls C

ompl

eted

/ Yea

r

Prod

uctio

n (k

bpd)

Production Wells Completed Injection Wells Completed

Other Wells Completed Ekofisk Oil Production

Large increase in injection wells

Peak drilling to control decline

rates

Source: NPD, Bernstein Estimates

BernsteinResearch.com European/Russian Oil & Gas – April 2012

We expect faster oil production declines out to 2016, based on our analysis of decline rates

15

-1,000

-500

0

500

1,000

1,500

2,000

2,500

3,000

3,500

2011 2012 2013 2014 2015 2016 2017 2018

UK

+ N

orw

ay N

orth

Se\

a Pr

oduc

tion

(kbp

d)

New Project Growth Existing Project GrowthNatural Declines SCBIEA DECC + NPDWood Mackenzie (includes Condensate)

UK + Norway Total Oil Production (kbpd)

Source: NPD, IEA, DECC, Company Reports, Wood MacKenzie, Bernstein Estimates

BernsteinResearch.com European/Russian Oil & Gas – April 2012 16

Disclosure Appendix

SRO REQUIRED DISCLOSURES

References to "Bernstein" relate to Sanford C. Bernstein & Co., LLC, Sanford C. Bernstein Limited, and Sanford C. Bernstein, a unit of AllianceBernstein Hong Kong Limited, collectively.

Bernstein analysts are compensated based on aggregate contributions to the research franchise as measured by account penetration, productivity and proactivity of investment ideas. No analysts are compensated based on performance in, or contributions to, generating investment banking revenues.

Bernstein rates stocks based on forecasts of relative performance for the next 6-12 months versus the S&P 500 for stocks listed on the U.S. and Canadian exchanges, versus the MSCI Pan Europe Index for stocks listed on the European exchanges (except for Russian companies), versus the MSCI Emerging Markets Index for Russian companies and stocks listed on emerging markets exchanges outside of the Asia Pacific region, and versus the MSCI Asia Pacific ex-Japan Index for stocks listed on the Asian (ex-Japan) exchanges - unless otherwise specified. We have three categories of ratings:

Outperform: Stock will outpace the market index by more than 15 pp in the year ahead.

Market-Perform: Stock will perform in line with the market index to within +/-15 pp in the year ahead.

Underperform: Stock will trail the performance of the market index by more than 15 pp in the year ahead.

Not Rated: The stock Rating, Target Price and estimates (if any) have been suspended temporarily.

As of 02/03/2011, Bernstein's ratings were distributed as follows: Outperform - 42.9% (1.6% banking clients) ; Market-Perform - 49.4% (1.4% banking clients); Underperform - 7.7% (0.0% banking clients); Not Rated - 0.0% (0.0% banking clients). The numbers in parentheses represent the percentage of companies in each category to whom Bernstein provided investment banking services within the last twelve (12) months.

David Vos maintains a long position in Cadaogan Petroleum (CAD.LN)

Accounts over which Bernstein and/or their affiliates exercise investment discretion own more than 1% of the outstanding common stock of the following companies BG/.LN / BG Group PLC, PMO.LN / Premier Oil PLC, TLW.LN / Tullow Oil PLC, BP / BP PLC, BP/.LN / BP PLC, FP.FP / TotalFinaElf SA, TOT / Total SA, RDS/A / Royal Dutch Shell PLC, RDS/B / Royal Dutch Shell PLC, RDSA.LN / Royal Dutch Shell PLC, RDSA.NA / Royal Dutch Shell PLC, RDSB.LN / Royal Dutch Shell PLC, RDSB.NA / Royal Dutch Shell PLC.

The following companies are or during the past twelve (12) months were clients of Bernstein, which provided non-investment banking-securities related services and received compensation for such services BG/.LN / BG Group PLC, BP / BP PLC, BP/.LN / BP PLC, FP.FP / TotalFinaElf SA, TOT / Total SA.

In the next three (3) months, Bernstein or an affiliate expects to receive or intends to seek compensation for investment banking services from OGZD.LI / Gazprom OAO, LKOD.LI / LUKOIL, ROSN.LI / Rosneft Oil Co, NVTK.LI / NovaTek OAO, SGGD.LI / Surgutneftegaz, BG/.LN / BG Group PLC, CNE.LN / Cairn Energy PLC, GALP.PL / Galp Energia SGPS SA, PMO.LN / Premier Oil PLC, TLW.LN / Tullow Oil PLC, BP / BP PLC, BP/.LN / BP PLC, E / ENI SpA, EAD.FP / European Aeronautic Defense, ENI.IM / ENI SpA, FP.FP / TotalFinaElf SA, TOT / Total SA, RDS/A / Royal Dutch Shell PLC, RDS/B / Royal Dutch Shell PLC, RDSA.LN / Royal Dutch Shell PLC, RDSA.NA / Royal Dutch Shell PLC, RDSB.LN / Royal Dutch Shell PLC, RDSB.NA / Royal Dutch Shell PLC.

This research publication covers six or more companies. For price chart disclosures, please visit www.bernsteinresearch.com, you can also write to either: Sanford C. Bernstein & Co. LLC, Director of Compliance, 1345 Avenue of the Americas, New York, N.Y. 10105 or Sanford C. Bernstein Limited, Director of Compliance, Devonshire House, One Mayfair Place, London W1J 8SB, United Kingdom; or Sanford C. Bernstein, a unit of AllianceBernstein Hong Kong Limited, Director of Compliance, Suite 3401, 34th Floor, One IFC, One Harbour View Street, Central, Hong Kong.

BernsteinResearch.com European/Russian Oil & Gas – April 2012 17

12-Month Rating History as of 02/06/2011

Ticker Rating Changes BG/.LN O (IC) 01/22/09 BP M (IC) 08/03/10 O (DC) 08/02/10 O (RC) 05/10/10 M (RC) 03/03/09 BP/.LN M (IC) 08/03/10 O (DC) 08/02/10 O (RC) 05/10/10 M (RC) 03/03/09 CNE.LN O (IC) 01/22/09 E O (IC) 08/03/10 O (DC) 08/02/10 O (RC) 11/21/08 EAD.FP O (RC) 12/17/09 ENI.IM O (IC) 08/03/10 O (DC) 08/02/10 O (RC) 11/21/08 FP.FP O (IC) 08/03/10 M (DC) 08/02/10 M (RC) 02/16/10 O (IC) 05/30/03 GALP.PL O (RC) 05/26/10 M (IC) 01/22/09 LKOD.LI U (IC) 01/15/09 NVTK.LI O (IC) 01/15/09 OGZD.LI O (RC) 07/16/09 PMO.LN O (RC) 02/19/10 M (IC) 01/22/09 RDS/A O (IC) 08/03/10 O (DC) 08/02/10 O (RC) 02/16/10 M (RC) 03/16/09 RDS/B O (IC) 08/03/10 O (DC) 08/02/10 O (RC) 02/16/10 M (RC) 03/16/09 RDSA.LN O (IC) 08/03/10 O (DC) 08/02/10 O (RC) 02/16/10 M (RC) 03/16/09 RDSA.NA O (IC) 08/03/10 O (DC) 08/02/10 O (RC) 02/16/10 M (RC) 03/16/09 RDSB.LN O (IC) 08/03/10 O (DC) 08/02/10 O (RC) 02/16/10 M (RC) 03/16/09 RDSB.NA O (IC) 08/03/10 O (DC) 08/02/10 O (RC) 02/16/10 M (RC) 03/16/09 ROSN.LI U (IC) 01/15/09 SGGD.LI U (IC) 01/15/09 STL.NO M (IC) 01/22/09 TLW.LN O (IC) 01/22/09 TOT O (IC) 08/03/10 M (DC) 08/02/10 M (RC) 02/16/10 O (IC) 05/30/03 Rating Guide: O - Outperform, M - Market-Perform, U - Underperform, N - Not Rated Rating Actions: IC - Initiated Coverage, DC - Dropped Coverage, RC - Rating Change

OTHER DISCLOSURES

A price movement of a security which may be temporary will not necessarily trigger a recommendation change. Bernstein will advise as and when coverage of securities commences and ceases. Bernstein has no policy or standard as to the frequency of any updates or changes to its coverage policies. Although the definition and application of these methods are based on generally accepted industry practices and models, please note that there is a range of reasonable variations within these models. The application of models typically depends on forecasts of a range of economic variables, which may include, but not limited to, interest rates, exchange rates, earnings, cash flows and risk factors that are subject to uncertainty and also may change over time. Any valuation is dependent upon the subjective opinion of the analysts carrying out this valuation.

This document may not be passed on to any person in the United Kingdom (i) who is a retail client (ii) unless that person or entity qualifies as an authorised person or exempt person within the meaning of section 19 of the UK Financial Services and Markets Act 2000 (the "Act"), or qualifies as a person to whom the financial promotion restriction imposed by the Act does not apply by virtue of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005, or is a person classified as an "professional client" for the purposes of the Conduct of Business Rules of the Financial Services Authority.

To our readers in the United States: Sanford C. Bernstein & Co., LLC is distributing this publication in the United States and accepts responsibility for its contents. Any U.S. person receiving this publication

BernsteinResearch.com European/Russian Oil & Gas – April 2012

and wishing to effect securities transactions in any security discussed herein should do so only through Sanford C. Bernstein & Co., LLC.

To our readers in the United Kingdom: This publication has been issued or approved for issue in the United Kingdom by Sanford C. Bernstein Limited, authorised and regulated by the Financial Services Authority and located at Devonshire House, 1 Mayfair Place, London W1J 8SB, +44 (0)20-7170-5000.

To our readers in member states of the EEA: This publication is being distributed in the EEA by Sanford C. Bernstein Limited, which is authorised and regulated in the United Kingdom by the Financial Services Authority and holds a passport under the Investment Services Directive.

To our readers in Hong Kong: This publication is being issued in Hong Kong by Sanford C. Bernstein, a unit of AllianceBernstein Hong Kong Limited. AllianceBernstein Hong Kong Limited is regulated by the Hong Kong Securities and Futures Commission.

To our readers in Australia: Sanford C. Bernstein & Co., LLC and Sanford C. Bernstein Limited are exempt from the requirement to hold an Australian financial services licence under the Corporations Act 2001 in respect of the provision of the following financial services to wholesale clients: providing financial product advice; dealing in a financial product; making a market for a financial product; and providing a custodial or depository service.

Sanford C. Bernstein & Co., LLC, Sanford C. Bernstein Limited and AllianceBernstein Hong Kong Limited are regulated by, respectively, the Securities and Exchange Commission under U.S. laws, by the Financial Services Authority under U.K. laws, and by the Hong Kong Securities and Futures Commission under Hong Kong laws, all of which differ from Australian laws.

One or more of the officers, directors, or employees of Sanford C. Bernstein & Co., LLC, Sanford C. Bernstein Limited, Sanford C. Bernstein, a unit of AllianceBernstein Hong Kong Limited, and/or their affiliates may at any time hold, increase or decrease positions in securities of any company mentioned herein.

Bernstein or its affiliates may provide investment management or other services to the pension or profit sharing plans, or employees of any company mentioned herein, and may give advice to others as to investments in such companies. These entities may effect transactions that are similar to or different from those recommended herein.

Bernstein Research Publications are disseminated to our customers through posting on the firm's password protected website, www.bernsteinresearch.com. Additionally, Bernstein Research Publications are available through email, postal mail and commercial research portals. If you wish to alter your current distribution method, please contact your salesperson for details.

Bernstein and/or its affiliates do and seek to do business with companies covered in its research publications. As a result, investors should be aware that Bernstein and/or its affiliates may have a conflict of interest that could affect the objectivity of this publication. Investors should consider this publication as only a single factor in making their investment decisions.

This publication has been published and distributed in accordance with Bernstein's policy for management of conflicts of interest in investment research, a copy of which is available from Sanford C. Bernstein & Co., LLC, Director of Compliance, 1345 Avenue of the Americas, New York, N.Y. 10105, Sanford C. Bernstein Limited, Director of Compliance, Devonshire House, One Mayfair Place, LondonW1J 8SB, United Kingdom, or Sanford C. Bernstein, a unit of AllianceBernstein Hong Kong Limited, Director of Compliance, Suite 3401, 34th Floor, One IFC, One Harbour View Street, Central, Hong Kong.

CERTIFICATIONS

I/(we), Oswald Clint, Ph.D., ACA, Senior Analyst(s)/Analyst(s), certify that all of the views expressed in this publication accurately reflect my/(our) personal views about any and all of the subject securities or issuers and that no part of my/(our) compensation was, is, or will be, directly or indirectly, related to the specific recommendations or views in this publication.

Copyright 2011, Sanford C. Bernstein & Co., LLC, Sanford C. Bernstein Limited, and AllianceBernstein Hong Kong Limited, subsidiaries of AllianceBernstein L.P. ~ 1345 Avenue of the Americas ~ NY, NY 10105 ~ 212/756-4400. All rights reserved.

This publication is not directed to, or intended for distribution to or use by, any person or entity who is a citizen or resident of, or located in any locality, state, country or other jurisdiction where such distribution, publication, availability or use would be contrary to law or regulation or which would subject Bernstein or any of their subsidiaries or affiliates to any registration or licensing requirement within such jurisdiction. This publication is based upon public sources we believe to be reliable, but no representation is made by us that the publication is accurate or complete. We do not undertake to advise you of any change in the reported information or in the opinions herein. This publication was prepared and issued by Bernstein for distribution to eligible counterparties or professional clients. This publication is not an offer to buy or sell any security, and it does not constitute investment, legal or tax advice. The investments referred to herein may not be suitable for you. Investors must make their own investment decisions in consultation with their professional advisors in light of their specific circumstances. The value of investments may fluctuate, and investments that are denominated in foreign currencies may fluctuate in value as a result of exposure to exchange rate movements. Information about past performance of an investment is not necessarily a guide to, indicator of, or assurance of, future performance.