bigdata@sns: air traffic & financial markets fabrizio lillo scuola normale superiore di pisa

TRANSCRIPT

BigData@SNS: Air traffic & Financial Markets

Fabrizio LilloScuola Normale Superiore di Pisa

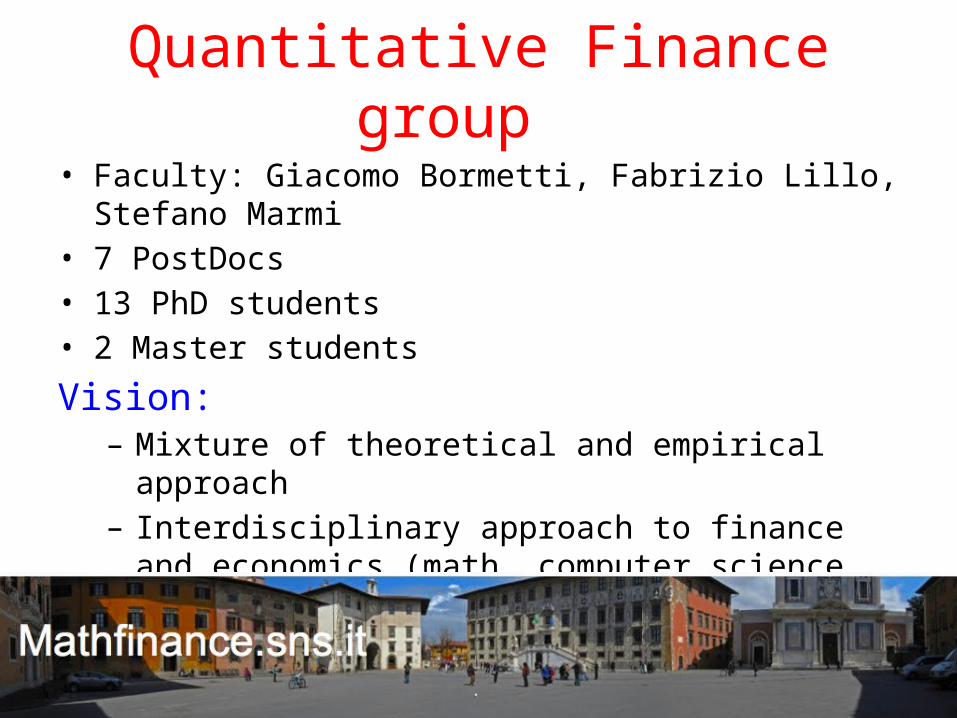

Quantitative Finance group • Faculty: Giacomo Bormetti, Fabrizio Lillo, Stefano Marmi• 7 PostDocs• 13 PhD students • 2 Master students

Vision: – Mixture of theoretical and empirical approach– Interdisciplinary approach to finance and economics

(math, computer science, physics) – Big data

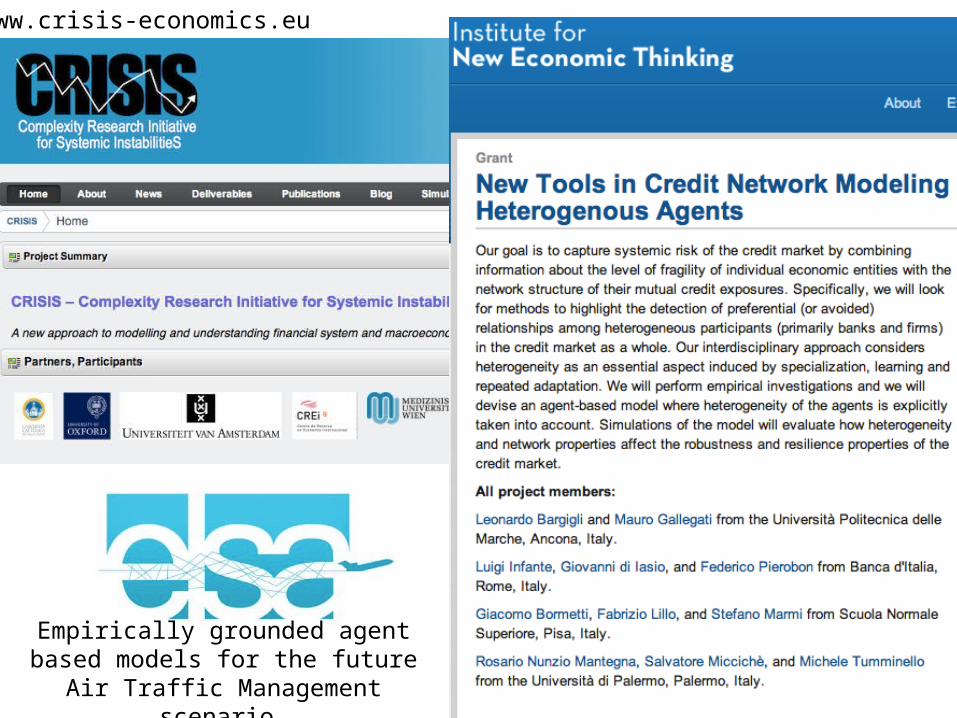

www.crisis-economics.eu

Empirically grounded agent based models for the future Air Traffic

Management scenario

Collaborations

• Oxford, Ecole Polytechnique, Princeton, ETH, CUNY, Central European University Budapest, Perm State University,…

• S. Anna, Bologna, IMT, Venezia, Palermo, Ancona,…

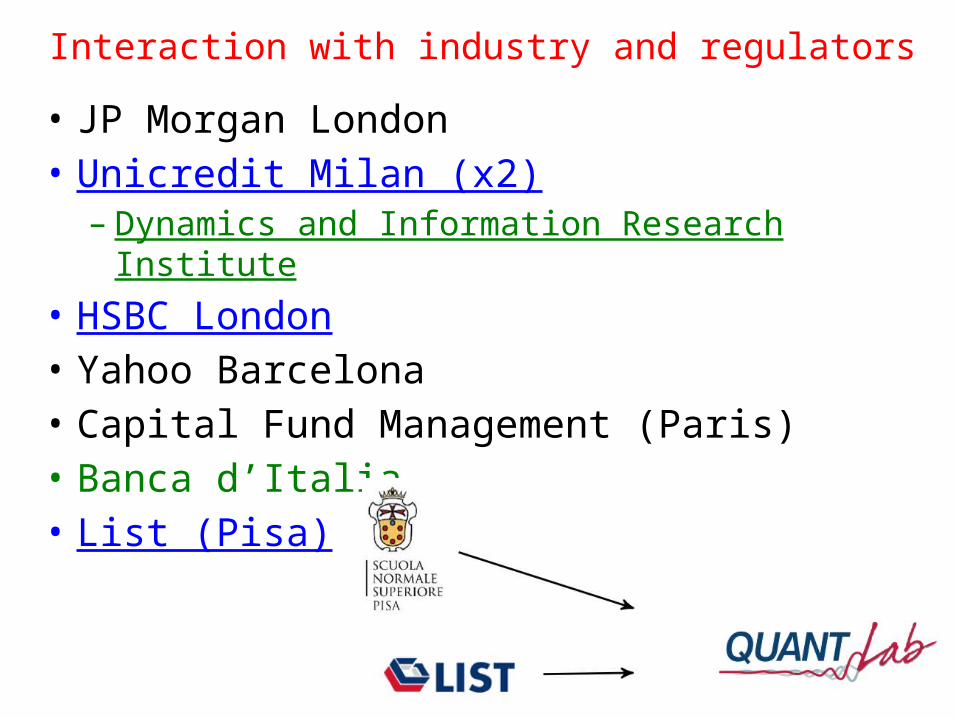

Interaction with industry and regulators• JP Morgan London• Unicredit Milan (x2)– Dynamics and Information Research Institute

• HSBC London• Yahoo Barcelona• Capital Fund Management (Paris)• Banca d’Italia• List (Pisa)

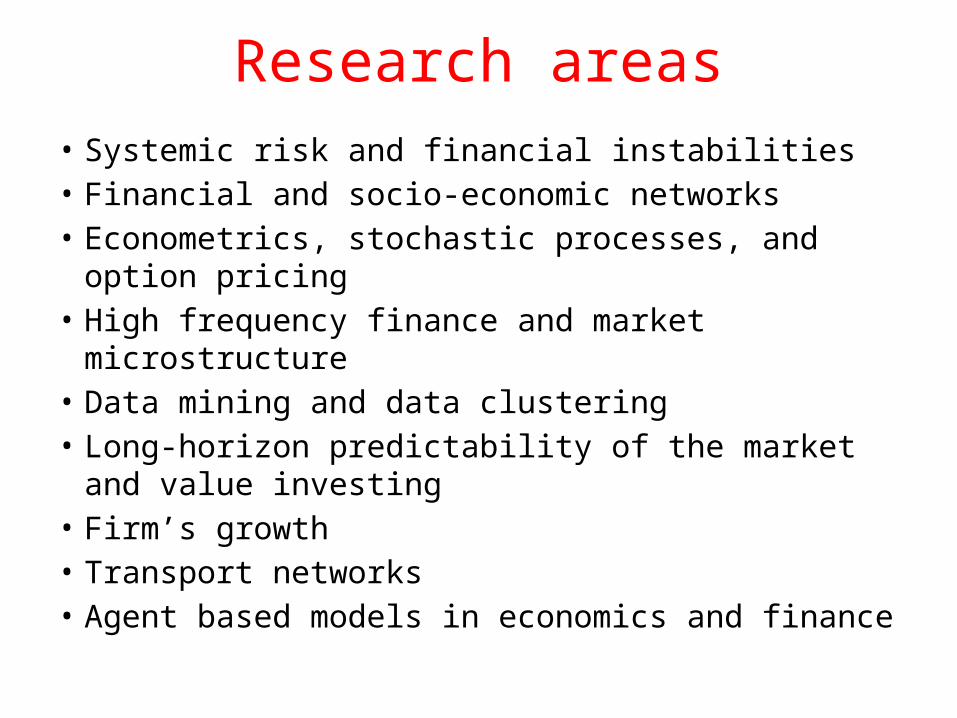

Research areas• Systemic risk and financial instabilities• Financial and socio-economic networks• Econometrics, stochastic processes, and option

pricing• High frequency finance and market microstructure• Data mining and data clustering• Long-horizon predictability of the market and value

investing• Firm’s growth• Transport networks• Agent based models in economics and finance

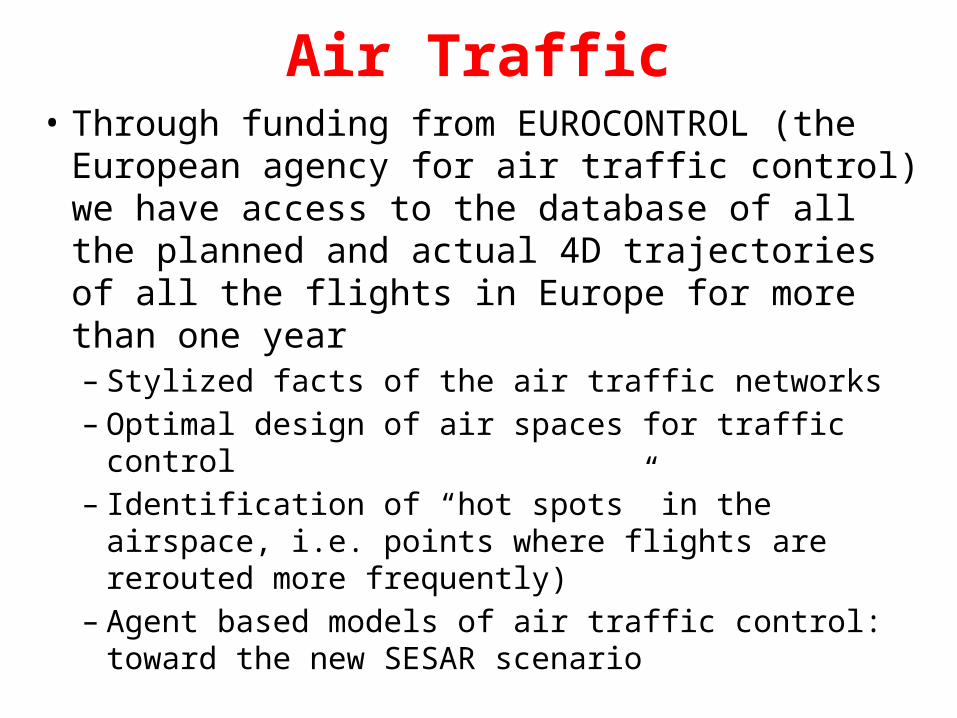

Air Traffic• Through funding from EUROCONTROL (the

European agency for air traffic control) we have access to the database of all the planned and actual 4D trajectories of all the flights in Europe for more than one year– Stylized facts of the air traffic networks– Optimal design of air spaces for traffic control– Identification of “hot spots” in the airspace, i.e.

points where flights are rerouted more frequently)– Agent based models of air traffic control: toward the

new SESAR scenario

Air Traffic Management and networksFrom traffic data to design of air traffic control by using community detection in networksWhole European air traffic over more than one year

Design of sectors from traffic data

Design of airspace from traffic between sectors

Multiresolution community detection

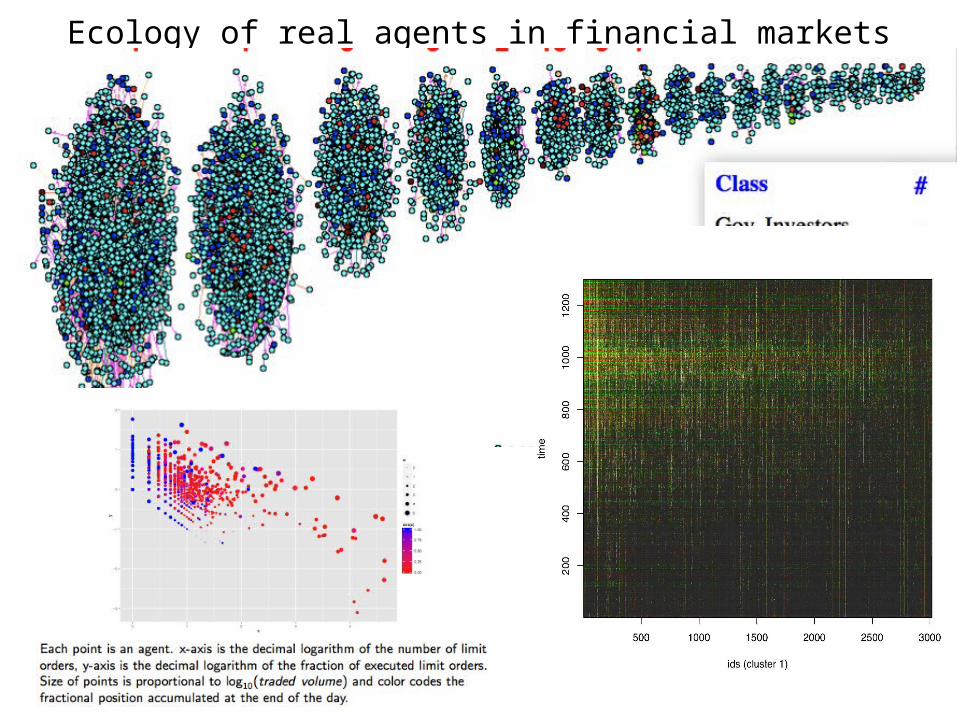

Ecology of real agents in financial markets

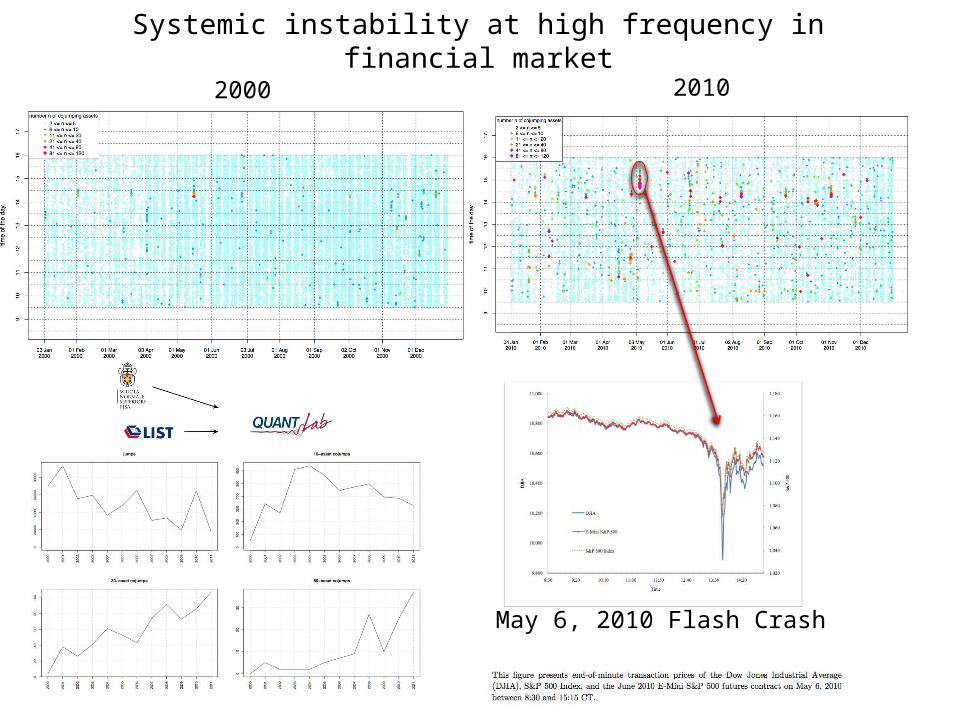

Systemic instability at high frequency in financial market2000 2010

May 6, 2010 Flash Crash

News, sentiment, and finance

Users clicking data for measuring the importance of a news

• In financial markets, news should help predicting stock prices• Sentiment analysis typically performs badly• Access to clicking data of Yahoo Finance• We claim this is due to very heterogeneous importance of news • # of clicks to weight impor-tance• Granger causality

• Coupling news sentiment with web browsing data predicts intra-day stock prices

Systemic risk in the interbank market

• Multiplex representation of the interbank network• What are the most “systemically important” financial institution?• Statistical models for the interbank networks: Maximum Entropy approach

Statistical inference of high dimensional data (Maximum Entropy, Belief Propagation)