blue square re n.v. - aegon · pdf fileb.3 risk management system including the own risk and...

TRANSCRIPT

Blue Square Re N.V.

Solvency and Financial Condition Report

2016

1

Table of contents Scope of the report ...................................................................................................................... 6

Summary ..................................................................................................................................... 7

A. Business and Performance ........................................................................................................ 8

A.1 Business ......................................................................................................................................... 8

A.1.1 Overview ................................................................................................................................ 8

A.1.2 Regulators and auditor ........................................................................................................... 8

A.1.3 Solvency II key figures ............................................................................................................ 9

A.1.4 Holders of qualifying holdings ................................................................................................ 9

A.1.6 List of principal subsidiaries, joint ventures and investments in associates ........................ 10

A.1.7 Related party transactions ................................................................................................... 11

A.1.8 Material lines of business and material geographical areas. ............................................... 12

A.2 Underwriting performance ......................................................................................................... 13

A.2.1 Premium Income .................................................................................................................. 13

A.2.2 Policyholder claims and benefits ......................................................................................... 14

A.3 Investment performance ............................................................................................................ 14

A.3.1 Investment income and expenses ....................................................................................... 14

A.3.2 Results from financial transactions ...................................................................................... 14

A.3.3 Projections of expected investment performance .............................................................. 15

A.3.4 Investments in securitisation ............................................................................................... 15

A.4 Performance of other activities .................................................................................................. 15

A.4.1 Other activities income and expenses ................................................................................. 15

A.4.2 Material leasing arrangements ............................................................................................ 16

A.5 Any other information ................................................................................................................ 16

B. System of Governance ............................................................................................................ 17

B.1 General information on the System of Governance ................................................................... 17

B.1.1 Corporate governance ......................................................................................................... 17

B.1.2 Remuneration policy ............................................................................................................ 21

B.1.3 Organizational Structure ...................................................................................................... 28

B.2 Fit and proper requirements ....................................................................................................... 28

B.2.1 Requirements ....................................................................................................................... 28

B.2.2 Process for assessment ........................................................................................................ 30

B.3 Risk management system including the Own Risk and Solvency Assessment ............................ 31

B.3.1 Risk management system .................................................................................................... 31

2

B.3.2 Own Risk and Solvency Assessment ..................................................................................... 42

B.4 Internal Control system ............................................................................................................... 46

B.4.1 Key procedures ..................................................................................................................... 46

B.4.2 Compliance activities and policy .......................................................................................... 50

B.5 Internal Audit function ................................................................................................................ 52

B.5.1 Internal Audit function ......................................................................................................... 52

B.5.2 Independence and objectivity of the Internal Audit function.............................................. 53

B.5.3 Internal Audits performed ................................................................................................... 53

B.6 Actuarial function ........................................................................................................................ 54

B.7 Outsourcing ................................................................................................................................. 56

B.7.1 External outsourcing arrangements ..................................................................................... 56

B.7.2 Intra-group outsourcing arrangements ............................................................................... 57

B.8 Any other information ................................................................................................................. 57

B.8.1 Assessment of adequacy ...................................................................................................... 57

B.8.2 Other material information .................................................................................................. 57

C. Risk Profile ............................................................................................................................. 58

General .......................................................................................................................................... 58

Prudent Person Principle ............................................................................................................... 59

Off-balance positions and Special Purpose Vehicles ..................................................................... 60

C.1 Underwriting risk ......................................................................................................................... 60

C.1.1 Underwriting risk description ............................................................................................... 60

C.1.2 Underwriting risk assessment .............................................................................................. 61

C.1.3 Underwriting risk concentration .......................................................................................... 63

C.1.4 Underwriting risk mitigation ................................................................................................ 63

C.1.5 Underwriting risk sensitivity ................................................................................................. 64

C.1.6 Underwriting risk data .......................................................................................................... 66

C.2 Market risk .................................................................................................................................. 66

C.2.1 Market risk description ........................................................................................................ 66

C.2.2 Market risk assessment ........................................................................................................ 67

C.2.3 Market risk concentration .................................................................................................... 67

C.2.4 Market risk mitigation .......................................................................................................... 68

C.2.5 Market risk sensitivity .......................................................................................................... 68

C.2.6 Market risk data ................................................................................................................... 69

C.3 Credit risk .................................................................................................................................... 69

3

C.3.1 Credit risk description .......................................................................................................... 69

C.3.2 Credit risk assessment .......................................................................................................... 71

C.3.3 Credit risk concentration ...................................................................................................... 71

C.3.4 Credit risk mitigation ............................................................................................................ 72

C.3.5 Credit risk sensitivity ............................................................................................................ 73

C.3.6 Credit risk data ..................................................................................................................... 73

C.4 Liquidity risk ................................................................................................................................ 73

C.4.1 Liquidity risk description ...................................................................................................... 73

C.4.2 Liquidity risk assessment ...................................................................................................... 73

C.4.3 Liquidity risk concentration .................................................................................................. 74

C.4.4 Liquidity risk mitigation ........................................................................................................ 74

C.4.5 Liquidity risk sensitivity ........................................................................................................ 74

C.4.6 Liquidity risk data ................................................................................................................. 74

C.4.7 Expected profit included in future premiums ...................................................................... 75

C.5 Operational risk ........................................................................................................................... 75

C.5.1 Operational risk description ................................................................................................. 75

C.5.2 Operational risk assessment ................................................................................................ 75

C.5.3 Operational risk concentration ............................................................................................ 76

C.5.4 Operational risk mitigation .................................................................................................. 77

C.5.5 Operational risk sensitivity ................................................................................................... 78

C.5.6 Operational risk data ............................................................................................................ 78

C.6 Other material risk ...................................................................................................................... 78

D. Valuation for Solvency Purposes ............................................................................................. 80

Approach towards IFRS to Solvency II balance sheet reconciliation ............................................. 80

Balance sheet reconciliation overview .......................................................................................... 81

D.1 Assets .......................................................................................................................................... 82

D.1.1 Goodwill ............................................................................................................................... 82

D.1.2 Deferred acquisition costs ................................................................................................... 82

D.1.3 Intangible assets .................................................................................................................. 82

D.1.4 Deferred tax assets .............................................................................................................. 83

D.1.5 Pension benefit surplus........................................................................................................ 84

D.1.6 Property, plant & equipment held for own use ................................................................... 84

D.1.7 Investments (other than assets held for index- and unit-linked funds) .............................. 84

D.1.8 Assets held for index- and unit-linked funds ....................................................................... 87

4

D.1.9 Loans and mortgages ........................................................................................................... 87

D.1.10 Reinsurance recoverables .................................................................................................. 87

D.1.11 Deposits to cedants ............................................................................................................ 88

D.1.12 Insurance and intermediaries receivables ......................................................................... 88

D.1.13 Reinsurance receivables .................................................................................................... 90

D.1.14 Receivables (trade, not insurance) .................................................................................... 90

D.1.15 Own shares ........................................................................................................................ 91

D.1.16 Cash and cash equivalents ................................................................................................. 91

D.1.17 Any other assets ................................................................................................................. 92

D.2 Technical provisions .................................................................................................................... 92

Data Quality ................................................................................................................................... 96

Model governance ......................................................................................................................... 97

Movements of technical provision ................................................................................................ 98

D.2.1 Technical provisions – non-life ............................................................................................ 99

D.2.2 Technical provisions – life (excluding index-linked and unit-linked) and health ............... 101

D.2.3 Technical provisions – index-linked and unit-linked .......................................................... 103

D.2.4 Matching adjustment ......................................................................................................... 103

D.2.5 Volatility adjustment .......................................................................................................... 103

D.2.6 Transitional risk-free interest rate-term structure ............................................................ 103

D.2.7 Transitional deduction ....................................................................................................... 104

D.2.8 Recoverables from reinsurance contracts and Special Purpose Vehicles ......................... 104

D.2.9 Material changes in assumptions made in calculations of technical provisions ............... 104

D.3 Other liabilities .......................................................................................................................... 105

D.3.1 Contingent liabilities .......................................................................................................... 105

D.3.2 Provisions other than technical provisions ........................................................................ 105

D.3.3 Pension benefit obligations ............................................................................................... 105

D.3.4 Deposits from reinsurers ................................................................................................... 105

D.3.5 Deferred tax liabilities ........................................................................................................ 105

D.3.6 Derivatives ......................................................................................................................... 105

D.3.7 Debts owed to credit institutions ...................................................................................... 106

D.3.8 Financial liabilities other than debts owed to credit institutions ...................................... 107

D.3.9 Insurance & intermediaries payables ................................................................................ 107

D.3.10 Reinsurance payables ...................................................................................................... 108

D.3.11 Payables (trade, not insurance) ....................................................................................... 108

5

D.3.12 Subordinated liabilities .................................................................................................... 109

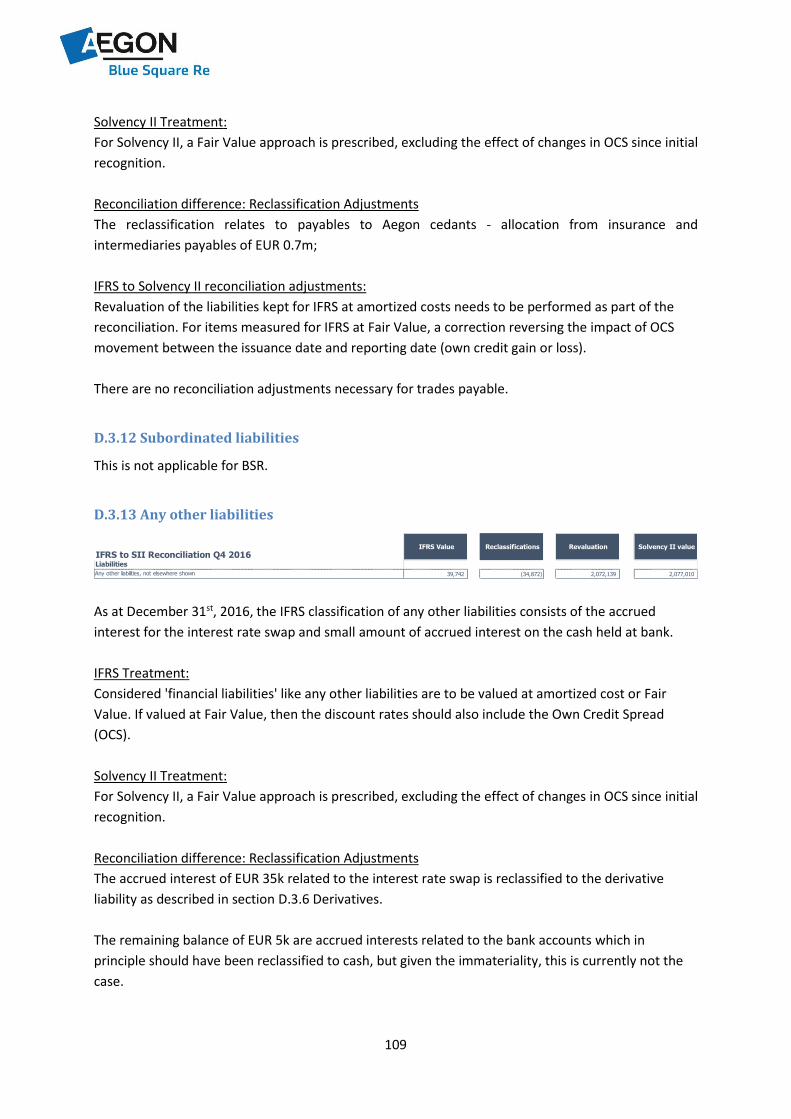

D.3.13 Any other liabilities .......................................................................................................... 109

D.4 Alternative methods for valuation ............................................................................................ 110

D.5 Any other information .............................................................................................................. 110

Management actions ................................................................................................................... 110

Policyholder behaviors ................................................................................................................ 111

E. Capital Management ............................................................................................................. 112

General ........................................................................................................................................ 112

Capital Management policy ......................................................................................................... 112

Capital quality .............................................................................................................................. 113

Managing our leverage ................................................................................................................ 114

E.1 Own Funds ................................................................................................................................. 114

E.1.1 Aggregation methods ......................................................................................................... 114

E.1.2 Tiering of Own Funds .......................................................................................................... 114

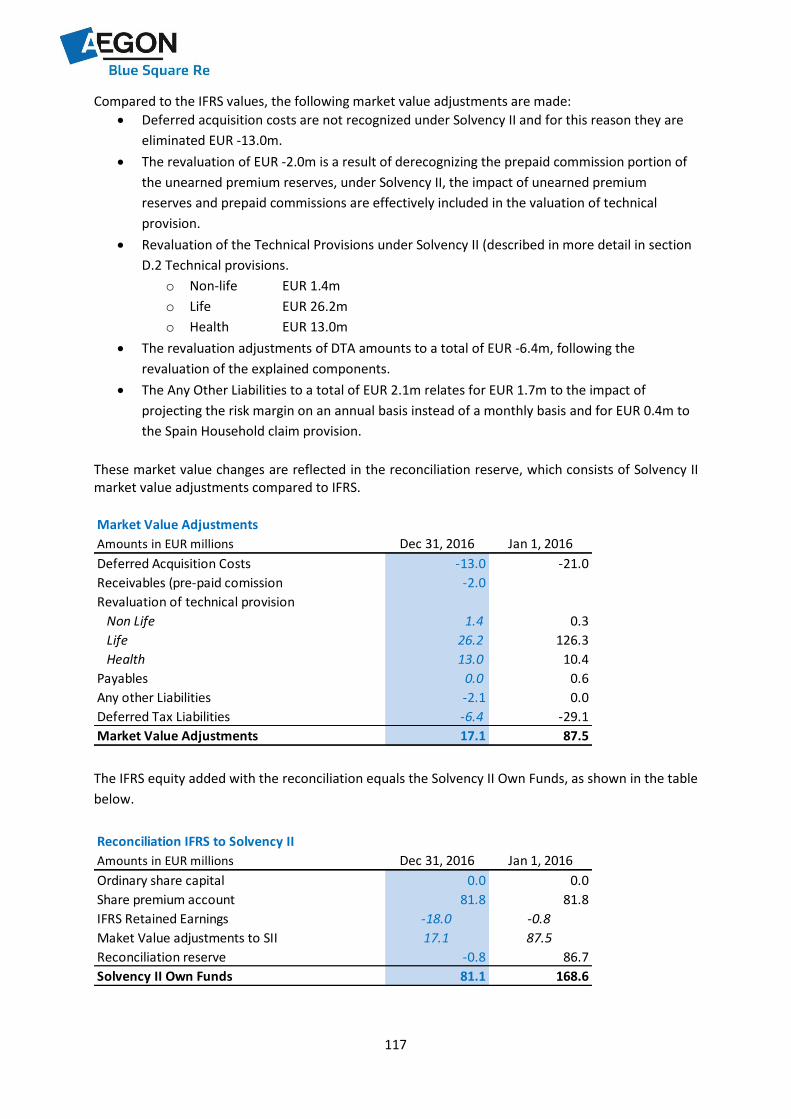

E.1.3 Difference between Solvency Own Funds and IFRS Shareholders Equity .......................... 118

E.1.4 Transitional arrangements ................................................................................................. 118

E.1.5 Ancillary own funds ............................................................................................................ 118

E.1.6 Description of items deducted from Own Funds ............................................................... 118

E.1.7 Significant changes to Own Funds over the reporting period ............................................ 118

E.2 Solvency Capital Requirement and Minimum Capital Requirement ......................................... 119

E.2.1 Solvency Capital Requirement ............................................................................................ 119

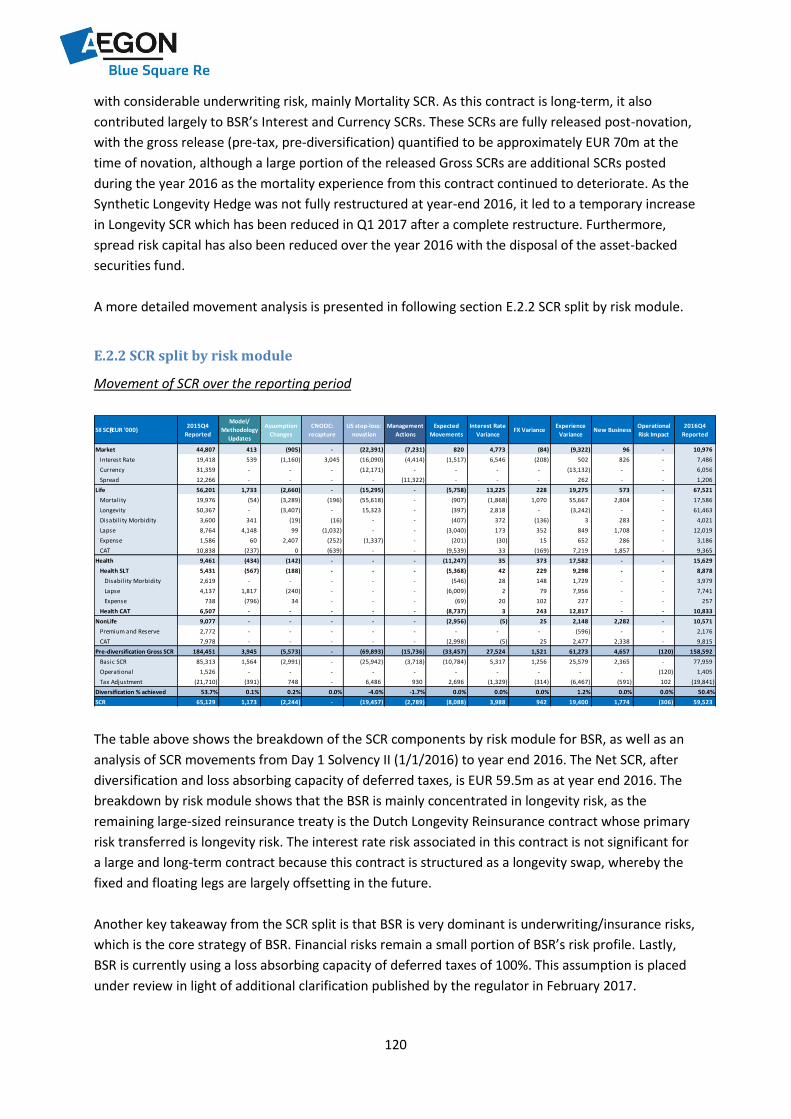

E.2.2 SCR split by risk module ..................................................................................................... 120

E.2.3 Simplified calculations ........................................................................................................ 123

E.2.4 Undertaking- specific parameters (Article 104(7) of Directive 2009/138/EC) ................... 123

E.2.5 Article 51(2) of Directive 2009/138/EC .............................................................................. 123

E.2.6 Minimum Capital Requirement .......................................................................................... 123

E.3 Use of the duration-based equity risk sum-module .................................................................. 123

E.4 Differences between standard formula and partially internal model used .............................. 124

E.5 Non-compliance with capital requirements .............................................................................. 124

E.6 Any other information ............................................................................................................... 124

BSR Annual Report is available upon request through the website: www.bluesquarere.com

6

Scope of the report

This report is Blue Square Re N.V.’s Solvency and Financial Condition Report (SFCR) for the year

ended December 31st, 2016. This report informs Blue Square Re N.V.’s stakeholders about Blue

Square Re N.V.’s:

A. Business and Performance;

B. System of Governance;

C. Risk Profile;

D. Valuation for Solvency Purposes; and

E. Capital Management.

This report is prepared in accordance with the requirements of Solvency II Directive and Delegated

and relevant EIOPA Guidelines, in particular ‘Guidelines on reporting and public disclosure’ (EIOPA-

BoS-15/109) as issued by the European Insurance and Occupational Pensions Authority (EIOPA).

Blue Square Re N.V. is referred to in this document as ‘Blue Square Re’, ‘BSR’, or ‘the Company’, and

the parent company, Aegon N.V. together with its member companies are referred to as ‘Aegon

Group’ or simply ‘Aegon’.

While the information contained in this report is purported to be true and accurate to the best of

BSR’s knowledge, this is nonetheless an unaudited report.

7

Summary Blue Square Re N.V. (BSR) FY 2016 Own Funds and SCR are as follows:

The Own Funds dropped substantially over the last year due to the novation of the US stop-loss

mortality contract in Q4, and mitigated by a partial restructure of the Synthetic Longevity Hedge

contract. The novation led to the derecognition of Own Funds represented by future premiums

under this contract, but it also released the SCRs associated with this treaty.

In Q3, BSR updated mortality and morbidity assumptions related to the key contracts, resulting in the

overall strengthening of reserves, especially for the Dutch Longevity Reinsurance contract. The

overall impact is also a reduction in Own Funds, with marginal change in the SCR.

Within the company, BSR had grown the number of full-time employees over the year. A Research &

Development unit is created to spearhead innovative projects and ideas. The previously Pricing &

Modelling unit is restructured and renamed to Business Development to strengthen the focus on

client relationship management, account planning and general business development initiatives. The

modelling function is moved into the Valuation & Capital unit.

The systems of governance do not see material changes other than the appointment of a new

Management Board and a new Supervisory Board member respectively to replace the outgoing

members of the respective board.

With the novation of the US stop-loss mortality contract in Q4, the risk profile of BSR is tipped

towards longevity risk. The nonlife block continues to grow as BSR continues to strengthen the

participation in nonlife reinsurance across the Group. As of Q1 2017, the longevity risk profile is

substantially reduced with the complete restructure of the Synthetic Longevity Hedge, which was a

management action undertaken since Q4 2016.

Over the year, BSR had also significantly improved and streamlined the internal processes, which

collectively mitigated the operational risk elements. Models were reviewed and migrated into a

standardized modelling approach while BSR continues to improve the modelling standards. A data

management project was undertaken to build an integrated data platform for the validation, storage

and management of data. A significant milestone related to data management is expected to be

accomplished in 2017 when a platform is rolled out for use. A Solvency II financial reporting system

was rolled out across the Group for the production of QRTs in the required format.

BSR completes an Own Risk and Solvency Assessment (ORSA) annually culminating in an ORSA report

that is shared with the regulator. The most recent ORSA was dated Q4 2016.

Solvency II key figures

Amounts in EUR millions Dec 31, 2016 Jan 1, 2016 %

Own Funds 81.1 168.6 -52%

SCR 59.5 65.1 -9%

Solvency II ratio 136% 259%

8

A. Business and Performance

A.1 Business

A.1.1 Overview

Blue Square Re N.V. is a public limited liability company with its statutory seat and head office in The

Hague, the Netherlands.

A.1.2 Regulators and auditor

The authority responsible for Solvency II supervision on Blue Square Re N.V. is:

De Nederlandsche Bank (DNB), the Dutch Central Bank;

Address : Westeinde 1, 1017 ZN, Amsterdam

Telephone : +31 (0) 20 524 91 11

The external auditor of Blue Square Re N.V. is:

PricewaterhouseCoopers Accountants N.V.

Thomas R. Malthusstraat 5

1066 JR Amsterdam

Postbus 90357

1006 BJ Amsterdam

The Netherlands

Telephone: + 31(0)88-7920020

The external auditor’s mandate does not cover an audit on the information disclosed in this SFCR.

9

A.1.3 Solvency II key figures

In the following table, the Solvency II key figures for BSR are presented:

The year-end 2016 Solvency II ratio of 136% (January 1, 2016: 259%) is based on the Solvency Capital

Requirement (SCR) calculated under Standard Formula. The Own Funds dropped substantially over

the last year due to the novation of the US stop-loss mortality contract in Q4, and mitigated by a

partial restructure of the Synthetic Longevity Hedge contract. The novation led to the derecognition

of Own Funds represented by future premiums under this contract, but it also releases the SCRs

associated with this treaty.

BSR updated mortality and morbidity assumptions related to the key contracts, resulting in the

overall strengthening of reserves, especially for the Dutch Longevity Reinsurance contract. The

overall impact is also a reduction in Own Funds, with marginal change in the SCR.

Other significantly business developments over the past year are described concisely in the Summary

section.

The composition of the Own Funds and the SCR are discussed more in detail in respectively section

E.2 Solvency Capital Requirement and Minimum Capital Requirement and section E.1 Own Funds.

The material differences between the financial statements based on IFRS and the Solvency II figures

are discussed in more detail in section D. Valuation for Solvency Purposes.

A.1.4 Holders of qualifying holdings

Blue Square Re N.V. is wholly owned by Aegon N.V., a Dutch multinational insurer domiciled in The

Netherlands and regulated by the DNB.

On December 31, 2016, Aegon N.V. held a total of 45 common shares out of a total of 225 authorized

shares. The remaining 180 shares remain unissued.

Blue Square Re is part of the Aegon N.V. Group The following picture illustrates the simplified

structure of the Aegon group, to show the legal position of Blue Square Re in the group.

Solvency II key figures

Amounts in EUR millions Dec 31, 2016 Jan 1, 2016 %

Own Funds 81.1 168.6 -52%

SCR 59.5 65.1 -9%

Solvency II ratio 136% 259%

10

Organizational structure of the significant entities of Aegon Group

A.1.5 BSR’s corporate structure

Blue Square Re N.V., incorporated and domiciled in the Netherlands, is a private limited liability

company organized under Dutch law and recorded in the Commercial Register of The Hague under its

registered address at Aegonplein 50, 2591 TV, The Hague, the Netherlands.

Blue Square Re N.V. is a wholly owned subsidiary of Aegon N.V. BSR’s website address is

www.aegonbluesquare.com.

Aegon N.V., incorporated and domiciled in the Netherlands, is the ultimate parent of the Aegon

Group and publishes consolidated financial statements that have been prepared in accordance with

International Financial Reporting Standards as adopted by the European Union and with Part 9 of

Book 2 of the Dutch Civil Code. Aegon N.V.’s consolidated financial statements are available on its

website (www.aegon.com).

BSR received its reinsurance license from De Nederlandsche Bank (DNB) on February 22, 2011 and

with that it undertakes its principal activity of a reinsurer for specified life and non-life insurance

risks. BSR does not employ any employees.

A.1.6 List of principal subsidiaries, joint ventures and investments in associates

BSR does not have any subsidiaries nor any material related undertakings.

Aegon N.V.

Aegon Asset Management

Aegon International

N.V.

Aegon Americas

Aegon Asia

Aegon Europe N.V,.

Aegon Netherlands

Aegon UK

Aegon CEE

Corporate Center B.V.

Blue Square Re N.V.

11

A.1.7 Related party transactions

BSR provides reinsurance services to other entities within the Aegon Group. For the year 2016, the

premium received from Aegon entities amounts to EUR 20,282k (with the total premium being EUR

42,233k).

The breakdown per legal entity is as follows (amounts in EUR ‘000):

In 2016, the Company provided expertise to Aegon Levensverzekering N.V. in order to assist in

entering into a possible transaction for an amount of EUR 180k. Aegon Levensverzekering N.V. also

pays an amount of EUR 50k to the Company for managing the collateral process, which is classified as

Commission and Fee income in the Annual Report.

Over 2016, the Company paid claims on the transactions entered into with Aegon Group companies

for the amount EUR 3,403k of which EUR 2,236k relates to the transaction with Scottish Equitable plc

and EUR 1,167k relates to the transaction with Aegon Emeklilik ve Hayat A.S..

The Company has entered into a service level agreement with Aegon N.V. As a result Aegon N.V. will

provide amongst others administrative, asset management services and conducting management.

Over 2016, Aegon N.V. charged the Company an amount of EUR 2,001k (2015: EUR 1,651k) for these

services.

The Company has entered into a service level agreement with Aegon Insights (previously Aegon

Direct Affinity Marketing Services) Regional Office (hereafter: AI RO). As a result AI RO will provide

pricing, modelling and actuarial services. Over 2016, AI RO charged the Company for an amount of

USD 200k for these services.

In June 2014, the Company entered into an investment mandate with Aegon Asset Management.

Over 2016 Aegon Asset Management charged an investment management fee of EUR 44k (2015: EUR

94k).

Over 2016, the Company paid EUR 4,259k (2015: EUR 5,318k) to Aegon Insights Japan as commission

for the acquisition of reinsurance contracts. The commission over November and December for the

amount of EUR 402k is not paid before December 31, 2016 and is therefore included as a payable to

a group company.

The receivables from group companies of EUR 3,456k (2015: EUR 3,476k) consist of receivables under

the reinsurance contracts. The main receivables are on Aegon Levensverzekering N.V. (EUR 730k),

Legal entity 2016 2015

Aegon Levensverzekering N.V. 3,115 3,191

Aegon Schadeverzekering N.V. 584 850

Aegon Magyarország Általános Biztositó Zrt 3,933 5,228

Aegon Emeklilik ve Hayat A.S. 3,355 2,687

Scottish Equitable plc 2,353 2,349

Transamerica Life Bermuda 2,363 775

Monumental Life Insurance Company 4,578 4,638

Total premium 20,282 19,718

12

Monumental Life Insurance Company (EUR 1,185k), Aegon Msagyarország Általános Biztositó Zrt

(EUR 912k), Transamerica Life Bermuda (EUR 603k) and Aegon Emeklilik ve Hayat (EUR 912k).

The payables to group companies of EUR 1,742k (2015: EUR 6,835k) mainly consist of a payable to

Aegon N.V. with respect to services charged to the Company and invoices paid by Aegon N.V. on

behalf of the Company (EUR 1,066k) and a payable to Aegon Insights Japan relating to the November

and December commission for the acquisition of reinsurance contracts (EUR 402k).

BSR is wholly owned by Aegon N.V., and as such none of the members of the BSR Management or

Supervisory Board has any direct interest in BSR’s shares.

A.1.8 Material lines of business and material geographical areas.

The reinsurance contracts ceded to BSR can be grouped into three major lines of business:

1. Life

2. Health

3. Non-life

The Life line of business is the most material line, and within it, is currently highly skewed towards a

single large longevity reinsurance contract (Dutch Longevity Reinsurance). As such, this contract will

contribute significantly to the performance and volatility of BSR’s result in comparison to the other

ceded businesses. The major risk underlying this segment is the risk of participants in the reinsured

portfolio living longer than expected. The Life line of business encompasses reinsured products

offering protection against mortality (both the risk of people dying and the risk of people living

longer) and morbidity (mainly critical illness and total and permanent disability).

The Health similar-to-life includes reinsured products offering protection against supplemental

health, critical illness and cancer treatment, and accidental death and dismemberment.

Lastly, the Non-life line of business includes household reinsurance and fire damages, as well as

natural catastrophe reinsurance programs.

Given the current business model of BSR where business is ceded from all geographical segments

over the world as shown in the list above, but the underlying insurance risks are directly assumed on

BSR’s own balance sheet, which is domiciled in The Netherlands, BSR does not yet split the business

into geographical areas based on ceding company’s risk location.

It is also important to note that BSR, as a young company, continues to grow the balance sheet in the

coming years especially as envisioned in the business plan. As the balance sheet and risk profile of

BSR continue to evolve in the future, the categories for the lines of business and geographical

segmentation may consequently change in the future.

13

The company did not employ employees in 2016 and 2015. Personnel is legally employed by Aegon

group entities. At the end of 2016, 13.8 fulltime equivalent employees were dedicated to Blue

Square Re.

A.2 Underwriting performance

A.2.1 Premium Income

The premium income is specified in the table below by material lines of business – life and non-life –

as per the Financial Statements.

(amounts shown in EUR ‘000s)

The decrease in life premium income is mainly a result of the unwinding of the China Modified

Coinsurance transaction which was included in the figures of 2015 for EUR 11.6m, this is partly offset

by the new Brazil Life and the Spain Life reinsurance treaties.

The increase of non-life premium can be explained by the growth of the portfolio with regard to the

Spain JV non-life transaction and the Mitsumi Sumitomo transaction. This block of business is

classified as non-life in the BSR Financial Statements, but reclassified as Health (similar-to-life) on the

Solvency II balance sheet.

The premium to reinsurers of EUR 4.9m (2015: EUR 5.9m) relates to the Turkey Life Reinsurance

contract (EUR 1.1m) and the Aegon Hungary transaction (EUR 3.7m).

Gross Reinsurance

2016

Total Life 21,265 1,112

Non-Life

Property & Casualty 10,765 3,746

Accident & Health 5,790 -

Total Non-Life 16,555 3,746

Total Life & Non-Life 37,820 4,859

Gross Reinsurance

2015

Total Life 27,891 704

Non-Life

Property & Casualty 7,849 5,228

Accident & Health 3,555 -

Total Non-Life 11,404 5,228

Total Life & Non-Life 39,295 5,932

14

A.2.2 Policyholder claims and benefits

(amounts shown in EUR ‘000s)

The decrease in the policyholder claims and benefits is mainly the result of unwinding of the China

Modified Coinsurance transaction in Q1 2016 offset by higher claims for the UK Individual Protection

and the Brazil Life reinsurance treaties.

The increase in the change in valuation of liabilities for reinsurance contracts is mainly driven by the

mortality assumption updates, especially for the Dutch Longevity Reinsurance contract.

A.3 Investment performance

A.3.1 Investment income and expenses

This section provides an overview of the investment performance. The investment performance is

specified by income only as the investment income is shown net of investment management fees.

Investment income

(amounts shown in EUR ‘000s)

The interest income mainly relates to the deposit that was held by the cedant with regard to the

modified coinsurance transaction that was unwound in Q1 2016.

The dividend income relates to the dividend received on the investment funds.

A.3.2 Results from financial transactions

(amounts shown in EUR ‘000s)

2016 2015

Claims and benefits paid to policyholders 10,023 11,781

Change in valuation of liabilities for reinsurance contracts 23,061 16,379

Total 33,084 28,160

2016 2015

Interest income 1,206 3,410

Dividend income 179 -

Total 1,385 3,410

Results from financial transactions comprise: 2016 2015

Net fair value change of shares at fair value through profit or loss (2,738) (196)

Net fair value change of free standing derivatives 11,866 9,588

Net fair value change of financial liabilities 58 (86)

Net foreign currency gains and (losses) 498 (1,807)

Total 9,684 7,499

15

The net fair value gains of shares relate to the unrealized fair value movements (minus transaction

expenses) relating to the investments in Aegon Asset Management Investment Funds and Insurance

Linked Securities (“ILS”).

The net fair value loss of free standing derivatives relate to the longevity index derivative the

Company entered into in 2013 as well as the net fair value change of interest rate swaps the

Company entered into to hedge the interest rate sensitivity of the longevity index derivative. As a

result of unwinding the MLIC transaction an amount of EUR 9m is paid for unwinding the longevity

index derivative for the mortality leg. The change in comparison to prior year includes fair value

movements and assumption and model updates.

The net foreign currency gains mainly relate to the foreign currency results on the Deferred

Acquisitions Costs for reinsurance contracts and the results on the FX forwards.

A.3.3 Projections of expected investment performance

The investment performance is expected to perform normally over 2017. As the underlying securities

in BSR’s investment funds are of highly-rated and of short-term nature, we expect a return of 0 - 1%

on the Investment funds and a return of around 6 - 8% on the Insurance Linked Securities. At this

moment there are no plans to rebalance the investment portfolio, as the current liability duration of

BSR is negative, the expected liability is more than funded by expected future premiums.

In addition, the investment in insurance-linked securities is exposed to random natural catastrophe

events and as such, a normal year is expected to give good return, except in the unpredictable event

that a major catastrophe occurs. As most of BSR’s funds have been invested in highly-rated and

short-term instruments and since liability duration is negative, this fund is complementary to the risk

profile of other investments as it delivers a higher expected yield. The benefit of this fund choice is

that it offers diversification to BSR’s balance sheet in terms of risk exposure, and consequently, offers

a very attractive return on risk capital.

A.3.4 Investments in securitisation

BSR does not hold any investments through portfolio securitization. BSR had invested in some asset-

backed securities (ABS) through an ABS fund managed by Aegon Asset Management, and had fully

liquidated the position by year end 2016.

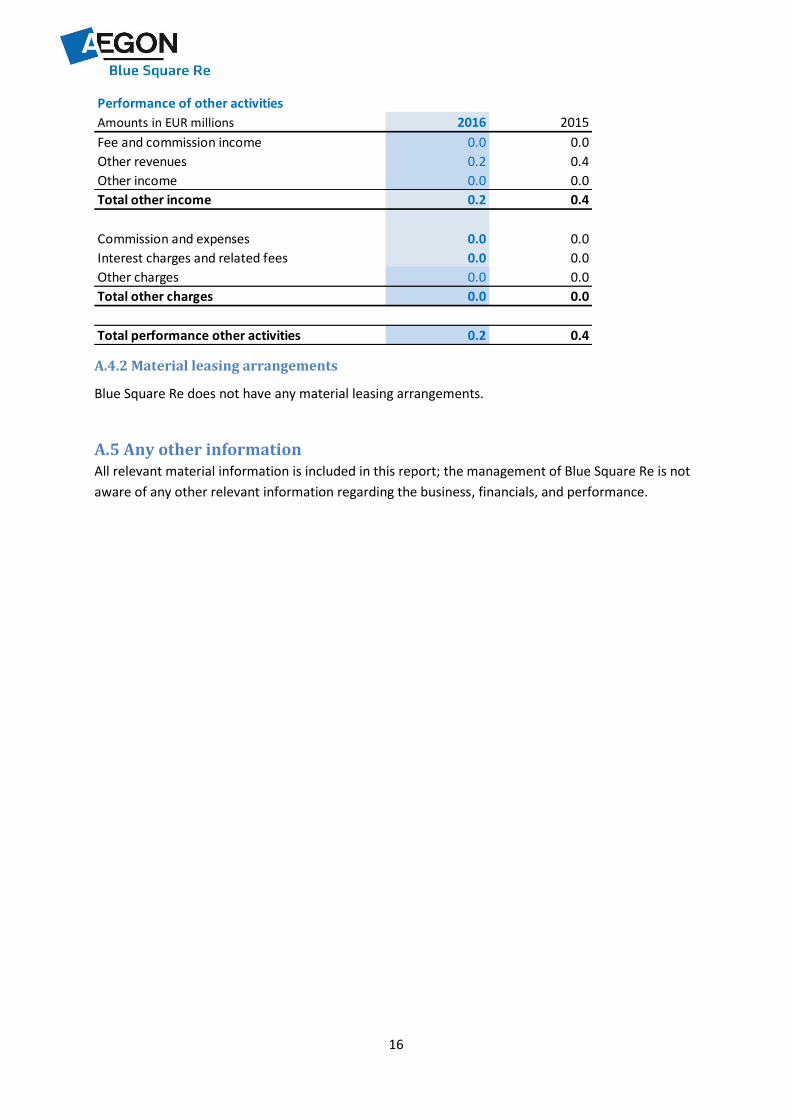

A.4 Performance of other activities

A.4.1 Other activities income and expenses

This section provides an overview of the performance of other activities – other than underwriting or

investment income and expenses.

With regard to other activities not related to underwriting or investment income and expenses, Blue

Square Re provides services to Aegon the Netherlands with regard to support on collateral processes

and consultancy services on longevity transactions for a total amount of EUR 230k.

16

A.4.2 Material leasing arrangements

Blue Square Re does not have any material leasing arrangements.

A.5 Any other information All relevant material information is included in this report; the management of Blue Square Re is not

aware of any other relevant information regarding the business, financials, and performance.

Performance of other activities

Amounts in EUR millions 2016 2015

Fee and commission income 0.0 0.0

Other revenues 0.2 0.4

Other income 0.0 0.0

Total other income 0.2 0.4

Commission and expenses 0.0 0.0

Interest charges and related fees 0.0 0.0

Other charges 0.0 0.0

Total other charges 0.0 0.0

Total performance other activities 0.2 0.4

17

B. System of Governance

B.1 General information on the System of Governance

B.1.1 Corporate governance

Blue Square Re N.V. is a public limited liability company incorporated and based in the Netherlands.

As a company established in the Netherlands, Blue Square Re must comply with Dutch law and

subscribes voluntarily to suitable parts of the Dutch Corporate Governance Code.

The company has a two-tier board system, with a Supervisory Board and a Management Board.

B.1.1.1 General Meeting of Shareholders

A General Meeting of Shareholders is held at least once a year and, if deemed necessary, the

Supervisory or Management Board of the Company has the authority to convene an Extraordinary

General Meeting of Shareholders. The main function of the General Meeting of Shareholders is to

decide on matters such as the adoption of annual accounts, amendment of the articles of

association, the approval of the remuneration of the Management Board and the Supervisory Board,

dividend payments and (re)appointments to the Supervisory Board and Management Board of Blue

Square Re.

B.1.1.2 The Supervisory Board and its committees

Blue Square Re Supervisory Board oversees the Management Board and the general course of affairs

of Blue Square Re in relation to the Company's business and corporate strategy. The Supervisory

Board must take into account the interests of all Blue Square Re stakeholders. The Supervisory Board

operates according to the principles of collective responsibility and accountability.

Composition of the Supervisory Board

Members of the Supervisory Board are appointed by the General Meeting of Shareholders. BSR aims

to ensure that the composition of the Company's Supervisory Board is well balanced in terms of

professional background, geography and gender. A profile has been established that outlines the

required qualifications of its members. The profile is tailored to the Company’s nature, size and

complexity and also incorporates the competences of the in DNB’s Suitability Matrix for Supervisory

Boards.

The Supervisory Board has drawn up a Succession Planning of the Blue Square Re Supervisory Board.

The Succession Planning will be reviewed, and updated if necessary, annually. Remuneration of the

Supervisory Board members is determined by the General Meeting of Shareholders.

The Supervisory Board currently consists of four members. The Company and the Supervisory Board

believe this number is appropriate to the nature, size and complexity of the Company. The

Supervisory Board is diverse in terms of gender and professional background of its members. The

diversity of its members ensures the complementary profile of the Supervisory Board. The

Supervisory Board does not have a risk and or audit sub-committee. Audit, risk and remuneration

related topics are discussed by the Supervisory Board in full.

18

The main role and responsibilities of the Supervisory Board are to fulfil its oversight responsibilities

regarding:

The achievement of Blue Square Re’s objectives;

The corporate strategy and the risks inherent in the business activities;

The integrity of the financial statements and financial reporting processes;

Internal control systems and the effectiveness of the internal audit process;

The performance of the external auditors and the effectiveness of the external audit process,

including monitoring the independence and objectivity of PwC;

Risk strategy, risk tolerance, risk monitoring and risk governance;

Regulatory compliance;

Overseeing the remuneration of the Management Board and Control functions;

Board member succession planning;

Reviewing and updating board profile and charters for the Supervisory and Management

Board;

Overseeing the corporate governance structure of the Company;

Any other applicable corporate governance legislation and regulations.

The Supervisory Board advises on the activities of the Management Board, identifying any matters

about which it considers action or improvements are needed, and making recommendations as to

the steps to be taken. Furthermore, the Supervisory Board regularly reviews risk exposures as they

relate to capital, earnings and compliance with risk policies. The Company's risk management is an

important topic for the Supervisory Board.

Composition of the Supervisory Board

According to the articles of association the Supervisory Board should consist of at least three

members. The Supervisory Board is composed of Independent Supervisory Directors and Aegon

Supervisory Directors. The majority of the members of the Supervisory Board must qualify as

independent.

The Board member is independent when there is no employment relationship between the person

and any company within the Aegon Group for the last five years.

The Supervisory Board currently consist of four members:

Wolf Becke, who is the Chairman and an independent board member;

Annette Sadolin, who is the Vice-Chairman and is an independent board member;

Patrick Peugeot, who is an independent board member;

Michiel van Katwijk, who is an Aegon Supervisory Director.

Key Functions

A description of the main roles and responsibilities of key functions, how they have necessary and

operational independence is disclosed in section B.2 Fit and proper requirements.

19

B.1.1.3 The Management Board

Blue Square Re's Management Board is responsible for the overall management of the Company and

is therefore responsible for achieving Blue Square Re's business objectives, developing the strategy

and its associated risk profile, taking into account the interests of all Blue Square Re stakeholders and

the development of the Company's earnings. Each member has duties related to his or her specific

area of expertise and for the management of the company as a whole.

Blue Square Re's Articles of Association determine that for certain decisions the Management Board

must seek prior approval from the General Meeting of Shareholders. In addition, the approval policy

of Blue Square Re determines that the Management Board must seek prior approval for certain

decisions from the Supervisory Board, and for certain decisions approval from the Executive Board of

Aegon N.V. prior to the Management Board approval.

Composition of the Management Board

The Management Board consists of a minimum of two Managing Directors, as described in the

articles of association. Members of the Management Board are only appointed by the General

Meeting of Shareholders after the Regulator has declared that it does not object to the intended

appointment.

The Management Board of Blue Square Re consists of:

Chris Madsen, who is Chief Executive Officer (CEO) and Chairman;

Martine Ammerlaan, appointed as Chief Financial Officer (CFO) and responsible for

Operations;

Pat Curtin, appointed as Chief Risk Officer (CRO, stepped down per April 30th, 2017);

Barry White member of the Management Board.

The number of Management Board members and their terms of employment are determined by the

General Meeting of Shareholders. The Supervisory Board prepares a profile for the size and

composition of the Management Board, taking into account the requirements regarding the

suitability and reliability as required under the provisions of the Act on Financial Supervision (Wet

financieel toezicht). Management Board members are appointed by the General Meeting of

Shareholders, following nomination by the Supervisory Board.

Role of the Management Board

The Management Board is entrusted with the overall strategic direction of the Company, more in

particular with respect to:

Setting, implementing and achieving the Company’s business objectives and strategy as well

as ensuring the delivery of results;

Establishing, monitoring and, where necessary, adjusting overall risk management of BSR.

Ensuring proper embedding of the risk strategy, the risk tolerance, risk monitoring and risk

governance;

Responsible for the set up and the proper functioning of the governance of new products or

services (business acceptance process);

The compliance with all relevant laws and regulations;

20

Assessing adequate functioning of the internal control framework by setting up and

periodically reviewing a system of monitoring and reporting;

Analysing risks with regard to Blue Square Re’s operational and financial objectives;

Adopting, discussing and sponsoring Blue Square Re’s policies;

Establish and periodically review effective systems of governance, which includes an

adequate transparent organisational structure with a clear allocation and appropriate

segregation of responsibilities;

Establishing and maintaining internal procedures that ensure that all major financial

information is known;

Responsible for the quality and completeness of (publicly) disclosed financial reports;

Ensuring that the External Auditor can properly perform his audit work;

Ensuring that effective processes and procedures are in place to prevent conflicts of interest

and identifying any potential sources of conflicts of interest;

An effective system for ensuring the transmission of relevant information.

Each individual Management Board member is accountable for the operations and management of

the role that the member is responsible for, in line with the Company’s policies, values and principles

and compliance standards. Management Board members are collectively responsible for managing

the company as a whole.

The Management Board shall have full information rights vis-à-vis all departments and processes

within the Company. The Management Board shall, in performing their duties, have access to the

expertise of and support and services from all BSR’s departments.

In the performance of their responsibilities, the Management Board shall act in accordance with the

interests of the Company and the business connected with it, taking into consideration the interests

of the Company’s stakeholders. The members of the Management Board shall externally express

concurring views with respect to important affairs, matters of principle and matters of general

interest in accordance with the final decision taken, with due observance of each member’s

individual responsibilities.

A description of how the risk management and internal control systems and reporting procedures

are implemented consistently, reference is made to section B.4 Internal Control system. Information

on any material intra-group outsourcing arrangements is described in section B.7 Outsourcing.

B.1.1.5 Material changes in the system of governance.

On April 30th, 2016 Ronald de Leeuw stepped down from the Management Board. On June 14th, 2016

Martine Ammerlaan was appointed as CFO and member of the Management Board. As per April 30th,

2017 Pat Curtin stepped down from the Management Board.

On June 1st, 2016 Karen Wright stepped down as Supervisory Director. On December 1st, 2016

Michiel van Katwijk took up office as a Supervisory Director.

21

B.1.2 Remuneration policy

Remuneration Principles

There were no employees employed by Blue Square Re N.V. in either 2016 or 2015. All employees,

including the Management Board are employed by Aegon Nederland N.V. or an Aegon Group

company. BSR has adopted the Aegon Group Global Remuneration Principles as laid down in the

Aegon Group Global Remuneration Framework (AGGRF) as a result whereof all employees working

for BSR are exposed to these principles

The Aegon Group Global Remuneration Principles (AGRF) provide the foundation for remuneration

policies and practices throughout the Aegon Group. The AGRF defines specific terms and conditions

for the employment of various groups of staff. In addition, all steps in the remuneration process, in

addition to the involvement of Human Resources, Risk Management, Compliance and Audit, are

governed by the AGRF and its underlying policies.

These Global Remuneration Principles are applied and implemented locally by BSR. The key pillars of

the Aegon Group Global Remuneration Principles are as follows:

Aegon remuneration is employee-oriented by: fostering a sense of value and appreciation in

each individual employee; promoting the short- and long-term interests and well-being of all

Aegon staff via fair compensation, pension and/or other benefits; supporting employees’

career development; and supporting the (international) mobility of its staff;

Aegon remuneration is performance-related by: establishing a clear link between pay and

performance by aligning objectives and target setting with performance evaluation and

remuneration; reflecting individual as well as collective performance in line with Aegon's

long-term interests; enhancing the transparency and simplicity of Aegon Group

remuneration, consistent with the principle of pay for performance; avoiding any pay for

non-performance;

Aegon remuneration is fairness-driven by: promoting fairness and consistency in Aegon’s

remuneration policies and practices, with remuneration packages that are well-balanced

across the different echelons within Aegon and its business units; avoiding any discrimination

in Aegon’s remuneration structures, including, among others, discrimination based on

nationality, race, gender, religion, sexual orientation, and/or cultural beliefs; creating global

alignment in the total compensation of all Identified Staff; aiming at controlled market

competitive remuneration, by providing total compensation packages in line with an

appropriately established peer group at a regional unit, country and/or functional level; and

Aegon remuneration is risk-prudent by: aligning business objectives with risk management

requirements in the target setting practices throughout the Aegon Group; giving an incentive

to appropriate risk-taking behavior while discouraging the taking of excessive risks;

protecting the risk alignment effects embedded in the remuneration arrangements of

individual staff against any personal strategies or insurance to counter them.

The AGRF, contains the guiding principles to support sound and effective remuneration policies and

practices by ensuring consistency throughout the Aegon Group. The framework is designed in

accordance with relevant rules, guidelines and interpretations, for instance the Decree on Sound

Remuneration Policy (Regeling beheerst beloningsbeleid (Rbb) Wft 2014) from DNB (the Dutch

22

Central Bank), and the 2015 Act on the Remuneration Policy of Financial Undertakings (Wet

beloningsbeleid financiële ondernemingen, Wbfo 2015 stb 2015, 45).

The regulations concern, among other things, a cap on variable compensation of twenty percent

(20%) of the fixed compensation and require at least fifty percent of the performance indicators used

for determining variable compensation to be of a non-financial nature. In addition the regulations

limit the use of financial retention and severance arrangements. The Wbfo has a provision that

makes it possible to apply an average variable compensation maximum of twenty percent (20%) for

employees whose employment conditions are not primarily determined by a Collective Labour

Agreement. As a result employees may receive a higher maximum as long as the average variable

compensation for this category of employees is twenty percent (20%) of the total fixed income of

that group of employees. Since the employment conditions of the BSR board members are not

primarily determined by a Collective Labour Agreement, Blue Square Re has offered the

Management Board a maximum variable compensation opportunity in line with the Wbfo exemption

of an average of twenty percent (20%) of variable compensation as referred to hereinbefore.

Role of Risk Management and Compliance

Variable compensation may have an impact on risk-taking behaviors and, as such, may undermine

effective risk management. This can lead to excessive risk taking, which can have a material impact

on the Company's financial soundness. To avoid such undesired effects, both the Aegon Group Risk

Management and Aegon Group Compliance functions are involved in the design and execution of

remuneration policies and practices. Given the size and complexity of BSR, the Risk Management and

Compliance functions for remuneration policies and practices are performed by the Aegon Group

Risk Management and Aegon Group Compliance functions.

The AGRF includes separate remuneration policies for specific groups of employees. This is in

recognition of the fact that these employees' roles and responsibilities require specific risk mitigating

measures and governance processes. These remuneration policies are for material risk takers

(Identified Staff) and Control Staff. Given the rationale for having a separate policy for material risk

takers and the risk mitigating measures that are applied to the remuneration of these individuals,

Risk Management is involved in deciding which positions are deemed 'Identified Staff'. Regarding the

form and timing of payments, the regulation requires a portion of the variable remuneration paid to

Identified Staff (i.e. members of the BSR Management Board) to be deferred and partially paid in

shares. Furthermore, where exceptions to the policies are requested to reflect local practices or

regulations, Risk Management and Compliance are involved in order to ensure such exceptions do

not undermine effective risk management and that sufficient mitigating measures are undertaken.

In addition, the Risk Management and Compliance functions, together with the Aegon Group Human

Resources and Aegon Group Finance functions, are responsible for the execution of the various

measures that ensure the AGRF and associated practices are aligned with the defined risk tolerances

and behaviors. The risk mitigating measures are taken prior to the pay-out of compensation to

individual employees (regardless of whether the compensation is deferred) as well as after pay-outs,

or allocated but deferred payments (before vesting of these payments) to ensure sustainability of

performance, are considered ex-post measures.

23

The risk management process is aimed to find an appropriate balance of ex-ante and ex-post

assessments to ensure effectiveness in both the short- and long-term risk taking behavior of

employees.

General compensation practices

The Aegon Group Global Remuneration Principles are based on a pay philosophy of total

compensation total compensation. This means that the aim is for total remuneration for experienced

and competent employees to be consistent with the market in which Blue Square Re operates and

competes for employees. Total compensation typically consists of base salaries and - where in line

with local market practices - variable compensation. Market survey information from reputable

sources is used to provide information on competitive compensation levels and practices.

Variable compensation, if any, is capped at an appropriate level as a percentage of base pay. Variable

compensation for senior management is usually paid out in cash and shares in Aegon NV over

multiple years, and is subject to further conditions being fulfilled. There is an additional holding

period for one year. Variable compensation already paid out may also be retrieved under certain

circumstances ('Claw-back').

Pension arrangements are offered in line with market practice.

In the following sections more detailed information is provided on the compensation practice for the

Supervisory Board and the Management Board of Blue Square Re.

Supervisory Board Remuneration

Independent Supervisory Directors are entitled to a base fee for membership of the Supervisory

Board. No separate attendance fees are paid to members for attendance at the regular Supervisory

Board meetings. The external members of the Supervisory Board receive an annual remuneration of

EUR 40k for the chairman and EUR 25k for the other members (excluding VAT).

The fee is a fixed amount. Independent Supervisory Directors do not receive any performance or

equity-related compensation, and Independent Supervisory Directors do not accrue pension rights

with Blue Square Re. These measures are designed to ensure the independence of Independent

Supervisory Board members and to strengthen the overall effectiveness of Blue Square Re's

corporate governance.

The Internal Supervisory Directors do not receive remuneration from Blue Square Re.

The remuneration of an internal member of the Blue Square Re’s Supervisory Board is based on the

AGRF and the therewith connected – for that specific function and employer applicable – Reward

Policy, as may be amended from time to time.

Management Board remuneration

Blue Square Re's Management Board is remunerated on the basis of the principles described in the

AGRF.

24

The remuneration for Management Board members charged to the Company in the financial year

pursuant to Section 383:1 of Book 2 of the Netherlands Civil Code is set out below (amounts in

thousands of euros).

The members of the Management Board are not employed by the Company. For the year 2016,

expenses for the members are either included in employee expenses (for members fully dedicated to

the Company) or are included in the cost charge from Aegon N.V.

During 2015 and 2016, a few Management Board members received Long Term Incentive and

Variable compensation. These Management Board Members have been identified as material risk

takers and control function holders at Aegon group level.

Below an overview is provided of the number of shares in Aegon NV resulting from the active plans

for Long Term Incentive and Variable Compensation for the Management Board members.

*) included on the basis of "on target" performance. Actual performance is established after 31 December of the performance period

Role of the Aegon NV’s Remuneration Committee

The Remuneration Committee of Aegon's Supervisory Board has overall responsibility for the Aegon

Group's Remuneration Policies. Members of the Committee are drawn from the Aegon N.V.

Supervisory Board.

Each year, Aegon's Remuneration Committee reviews Aegon's remuneration policies to ensure they

remain in line with prevailing international standards. This review is based partly on information

provided by Aegon's external advisor, Willis Towers Watson.

The Aegon Remuneration Committee may recommend changes to the policies to the Aegon

Supervisory Board. Given the size and complexity of Blue Square Re and the fact that the Company

only performs its activities for Aegon group entities it has no separate remuneration committee.

2016 2015

Current Management Board Members

Gross salary and social security contributions 352 385

Pension Premium 26 31

Other benefits * 325 232

Total 703 649

* Within the other benefits short term incentive plans are included.

25

Since the board members of Blue Square Re who receive variable compensation have been identified

as material risk taker and control function holder at group level, Aegon’s Remuneration Committee is

supervising the remuneration of these board members.

Fixed compensation

The fixed compensation of the members of the BSR Management Board is based on their

qualifications, experience and expertise.

Variable compensation

The Aegon Global Remuneration Principles are based on the belief that variable compensation

strengthens the commitment of the Management Board of Blue Square Re to the Company's

objectives, business strategy, risk tolerance and long-term performance. Variable compensation is

based on a number of individual and company performance indicators that are linked to these items.

The indicators are regularly evaluated by experts in the Aegon Groups Finance, Risk Management,

Business Control, Audit, Human Resources and Compliance departments to ensure the alignment

remains strong.

Performance is assessed by Aegon's Remuneration Committee and validated by the full Supervisory

Board. Each year, a one-year target is set for each performance indicator. By paying half of the

variable compensation in cash and the other half in shares, together with adding deferral and

additional holding periods to the variable compensation that is allocated, the long-term interests of

Management Board members are aligned with the interests of BSR and its stakeholders.

All variable compensation is conditionally granted at the beginning of each performance period. The

number of conditionally granted shares is calculated using the value of one Aegon share at the

beginning of this period. This value is equal to the average price on the Euronext Amsterdam stock

exchange for the period December 15 to January 15. After the performance year, the Company

assesses the realized performance against the performance indicators and compares the minimum,

target and maximum levels of the performance indicators with the realized performance. The

amount of conditional variable compensation that can be allocated is then established. Variable

compensation is allocated once the accounts for the financial year are prepared and after an ex-ante

assessment.

The allocated variable compensation consists of equal parts of cash and shares, of which 60% is paid

out (or vests) in the year following the performance year, and 40% is deferred to later years. This

deferred portion remains conditional until it vests.

The deferred parts vest in equal tranches after a one-year holding period. After an ex-post

assessment, which may lower the vesting portion, these two individual parts are paid 50% in cash

and 50% in shares. The shares are restricted for a further period of one year (with the exception of

shares withheld to cover for the payment of any applicable taxes, social security premiums and

possible other deductions by the government due for which the company holds a withholding

obligation in connection with the vesting of the shares).

26

The variable compensation pay-out can be illustrated by the following example and the table below.

For every 1,000 variable compensation that is allocated following the performance period, 600 is

paid out/vested in the year following that performance year (N in the following table). This part will

be paid 50% in cash (=300) and 50% in shares vesting immediately (=300 /5.128 = 49 shares). The

remaining 400 is deferred and vests according to a pre-defined schedule.

Risk adjustment methodology (ex-ante)

At the end of the performance period, but prior to allocation of variable compensation, the

Remuneration Committee Board assesses whether (downward) modifications are needed. For this

purpose, quantitative and qualitative measures at group, regional unit and individual level are taken

into account, such as:

Breaches of laws and regulations;

Breaches of internal risk policies (including compliance);

Significant deficiencies or material weaknesses relating to the Sarbanes-Oxley Act; and

Reputation damage due to risk events.

Ex-post assessment and discretionary adjustments

The Remuneration Committee uses its judgment in the assessment of the outcome of

strategic/personal targets to ensure that, taken together, they represent a fair reflection of the

overall performance of the Management Board member over the performance period.

In addition, the Remuneration Committee applies an ex-post risk assessment to deferred payouts of

variable compensation to determine whether allocated (that is, unvested) variable compensation

should become unconditional (meaning it vests) or should be adjusted. This ex-post assessment is

based on informed judgment by the Remuneration Committee, taking into account significant and

exceptional circumstances that are not (sufficiently) reflected in the initially applied performance

indicators.

Performance N N+1 N+2 N+3 N+4

Year

c

60% upfront s h h h

c c

c s h h h

40% Deferred c c

s s h h h

s c

s s h h

c Cash s Shares h Holding period

1/3

1/3

1/3

27

Implementation of this authority is on the basis of criteria such as:

The outcome of a re-assessment of the performance against the original financial

performance indicators;

A significant downturn in the Company’s financial performance;

Evidence of misbehavior or serious error by the participant;

A significant failure in risk management; and

Significant changes in the Company’s economic or regulatory capital base.

The Supervisory Board of Aegon asks the Remuneration Committee to review these criteria in detail

prior to each vesting and to document its findings. Based on this analysis, the Committee may then

put forward a proposal to the Supervisory Board of Aegon to adjust unvested variable compensation.

Deferred variable compensation may only be adjusted downwards. Ex-post, risk-based assessments

concern deferred variable compensation, not fixed compensation.

Circuit breaker

For each performance indicator, variable compensation is only paid if the threshold level set for that

performance indicator is reached

Claw-back provision

Where required based on the regulations that apply from time to time, where variable compensation

is based on incorrect data (including non-achievement of performance indicators in hindsight), or in

the event of material financial restatements or individual gross misconduct, Blue Square Re's

Supervisory Board is obliged to claim back variable compensation that has already been paid out or

vested.

Pension scheme

Members of Blue Square Re's Management Board are offered an Aegon group pension scheme.

Benefits offered are consistent with the local Aegon pension agreements, there are no specific early

retirement schemes.

The principal features of the pension scheme were as follows in 2016:

Average pay pension plan

Retirement age: 67 years

Accrual rate for old-age pension: 1.875% for all salary groups

Employee contribution: 5.45% of pensionable earnings

Pensionable salary: fixed annual salary on 1 April of any year (capped at EUR 101,519 gross)

Partner’s pension: 70% of projected old-age pension

Orphan’s pension: 14% of projected old-age pension

Flexible elements: early retirement, deferred retirement, exchange, high/low, part-time

No allowance for discretionary pensions

28

Loans

Blue Square Re does not grant Management Board members personal loans, guarantees or other

such arrangements, unless in the normal course of business and on terms applicable to all Aegon

employees.

Employment contracts

Members of the Management Board of Blue Square Re have a contract of employment with an

Aegon group entity, no severance payments were paid to Management Board members during the

year.

Other than intragroup reinsurance transactions as part of the business model for BSR as an internal

reinsurer (described in section A.1.7 Related party transactions) and the Aegon Corporate Center

cost charges (find ref), there are no other material transactions with the shareholder Aegon NV, with

persons who exercise a significant influence on the undertaking, and with members of the

Management Board or Supervisory Board.

B.1.3 Organizational Structure

In section B.2.1 Requirements, a list of the persons that are responsible for key functions within Blue Square Re is provided. Besides the members of the Management Board and Supervisory Board, Colin Selfridge, Alexander MacLean and Ruurd van den Berg are Solvency II key function holders.

B.2 Fit and proper requirements

B.2.1 Requirements

Aside from the General Meeting of Shareholders, as a public limited liability company under Dutch

law, Blue Square Re is governed by a two-tier board system, the Supervisory Board and the

Management Board. Blue Square Re’s Management Board is responsible for the day to day

management and the implementation of Blue Square Re’s strategy.

B.2.1.1 Supervisory Board

Blue Square Re’s Supervisory Board oversees the management of the Management Board, in

addition to the Company’s business and corporate strategy. The Supervisory Board must take into

account the interests of all Blue Square Re’s stakeholders. The Supervisory Board operates according

to the principles of collective responsibility and accountability.

All members of Blue Square Re’s Supervisory Board have been tested by the Dutch supervisory