bonanza potential in wyoming investor package november, 2014 1

TRANSCRIPT

1

Bonanza Potential in Wyoming

Investor Package

November, 2014

2

The information contained herein, together with any amendments or supplements and any other information that may be furnished by the company, includes forward-looking information. Such information is based on assumptions as to future events that are inherently uncertain and subjective. The company makes no representation or warranty as to the attainability of such assumptions, including the completion of a financing or as to whether future results will occur as projected.

Forward Looking Statements

Note this is not a technical presentation – additional technical informationis available upon request

Highlights

• Current Shares Outstanding 73,600,000• Fully Diluted 73,600,000• Stock Range $.01-$.09• Current Price $.02• Symbol OTCPK: FCEN• Focus Wyoming E&P• Principal Project Rocky Ford & Phosphoria• Financing Up to $250,000 Senior Convertible 10% NotesSpecial Opportunity: A shareholder friendly to management has acquired approximately $570,000 worth of debt in the company for $150,000. The shareholder will provide the company the ability to allocate half of the debt, $285,000 in return for a new $75,000 note.

3

Summary

4

Balance SheetCurrent Assets

Cash $1,344

Notes Receivable , net of allowance of $878,354 -

Total Current Assets $1,344

Oil and Natural Gas, Unproved $210,000

Total Assets $211,344

Liabilities and Stockholders Deficit

Current Liabilities

Bank Overdraft $19

Notes payable (current portion) $750,097

Related Party Payables $870,578

Interest Payable $319,515

Accrued Expense and other liabilities $159,550

Total Current Liabilities $2,099,759

Total Liabilities $2,099,759

Stockholder Deficit

Common Stock $26,100

Additional Paid In Capital $347,900

Deficit accumulated during the development stage ($2,262,415)

Total Stockholder deficit ($1,888,415)

1. The Note Receivable while written off for accounting purposes will we believe see a recovery of about 50% of value over next year.

2. The Note Payable current is with large shareholders who we have advised would only receive payout of future revenue or convert as the company grows at the companies option. Over half is not expected to ever be paid given holder recoveries from other security but we have been unable to reach other parties since 2008. In seven years it can come off book.

3. Related Parties were previous management or directors they have been advised would only receive payout of future revenue or convert as the company grows at the companies option.

4. Accrued Liabilities is almost totally a payable under review to former CEO. He has been advised would only receive payout of future revenue or convert as the company grows at the companies option.

5

Proposed Convertible Debt Deal

• Shareholder has four parties it will share its portion of debt with. This is done to stay under 4.9% ownership an avoid insider status.• Shareholder owner of debt would keep half debt and trade half for a

$75,000 current note from company. Providing company ability to give new note holder(s) a combination of past debt which can be converted and new debt.• Company would agree to convert 30% of debt over now @$0.015

and agree to convert another 35% over at 50% of market in three and six months from date of investment.

Our Target- Wyoming

6

7

Why Wyoming-Macro

• Prolific Oil and Gas Production• 3rd Largest Producer of Natural Gas in USA• 8th Largest producer of Oil• Oil Production in 1980 was 130,000 BOPD - 63,000 MBPD in 2012 • Pipeline, Heavy Oil Refineries, Production Infrastructure in place• Well educated labor force

8

Why Wyoming - Micro

• Joint Venture with experienced successful Evergreen Petroleum team. Principals

George Wulf Joe Banks Forest Twiford

40+ Years In Wyoming E&PWell site Geo on 451 Minnelusa wellsDiscovered 6 New Minnelusa FieldsExcellent local reputation

40+ Years in Wyoming E&PDrilled and or Operated 1522 wellsMud engineer Gillette based Established & Respected

40+ Years Global E&PEngineer, Geologist, Research GeophysicistTexaco, Mobil, Pan American + 202 VenturesDiscovered Edgemnot Minnelusa field &Burnt Hollow (Sun Oil)

9

Evergreen Proprietary Research Study• Began January 2008 – Ongoing- Investment of over $2,000,000• Includes all 319 known Minnelusa Fields - 1909 to present

Geological, Geophysical, and Engineering• Reference Information Wyoming Oil & Gas Commission Database Published Papers, especially Wyoming Geological Society Purchase Proprietary Data, Retained Consultants Corporate Information Files

10

Minnelusa Formation• Permian Age Sandstone; 220 Million years ago• Major producer of oil Wyoming• Total production end 2011- 1.2 Billion bbls• Est. Discovered oil in place – 3.5 billion bbls• Open Federal, State and Fee Lands• Reasonable land costs- $50-$200 acre• Shallow depth – 500-7000 feet• Est. undiscovered reserves – 8.5 billion bbls Source Proprietary Evergreen Research Study

11

Minnelusa Reservoirs• Dune Sandstones• 300-400 acres per original dune• Thickness 30-100 feet• Porosity 10-40%; permeability very high• Black sour crude oil• API 15-41 degrees• Solution Gas Drive initially; later water injection• 4-5 million recoverable per dune. Many wells produce over 1 million bbls/well• One of the World’s best reservoirs Source Proprietary Evergreen Research Study

12

Location Map Crook County

13

Regional Activity- Prospect Overlay

14

Potential of Minnelusa Heavy Oil Production

Play Area - @500,000 Fee acres in Crook County, WyomingDepth to pay - 100-2000 feet (average 500 feet)Potential Reserves - 5 Billion BOAPI Gravity - 7 to 24 API degrees @ 60°F surfaceRock Temperature 100 to 140°F @ BHThree Types of Prospects

ROCKY FORD Depth - 180 feet; Core -- 2000 md, 25% par, 82% oil, 24.5 API, reservoir temp 115 degrees F (?)Near 1909 cable tool well with 15.6 API; swabbed oilEstimated 30 mm bo in buried sand dune

BURNT HOLLOW Depth -670 feet; Log - 1000 md, 26% par, 68% oil av, 9 API at surface, reservoir temp 135 degrees F (?)Flowed water and low gravity oil through perfsSteam injected and recovered 25 boEstimated 126 mm bo in sand dunes

ZIMMERSCHIED 19-T53N, R66W (P&A 1967)Depth - 1600 feet; Core - 500 to 1000 md, 25-30% par, 60 to 80% oil, 7 API at surface, reservoir temp 140 degrees FWell 0.5 mi to east, 5 ft of tight sand with light oil stn & flecks heavy oil

Opportunity is to test Rocky Ford. Sizeableland package current and considerable upsideto add additional land at Rocky Ford and analogousprospects Burnt Hollow & Zimmerschied

15

Rocky Ford Prospect

16

Rocky Ford AnalogiesRocky Point & Brennan Fields

Characteristic Rocky Ford Rocky PointAPI 15 – 25 API 16 – 19 APIPermeability 27 md – 1900 md 500 md averagePorosity 12 – 27% 20%Net Pay 5 ft – 40 ft 76 ftAcres 300 acres 880 acresPrimary Recovery 10,500,000 bbls

Characteristic Rocky Ford BrennanAPI 15 – 25 API 23 APIPermeability 27 md – 1900

md585 md average, 1.8 md – 2850 md range

Porosity 12 – 27% 16% Average, 30% MaxNet Pay 5 ft – 40 ft 72 ftAcres 300 acres 320 acresPrimary Recovery

723,898 bbls (15.5% recovery)

Secondary Recovery

2,444,651 bbls (52.6% recovery)

OOIP 4,648,000 bbls

Rocky Ford Initial Production Expectations

• Main analogy fields Rocky Point & Brennan • Brennan Initial Production : 362 barrels of oil / day• Rocky Point Initial Production : 480 barrels of oil / day

• Rocky Ford Economic Expectation• Low Case : Initial Production 50 barrels of oil / day• Average Case : Initial Production 150 barrels of oil / day• High Case : Initial Production 400 barrels of oil / day

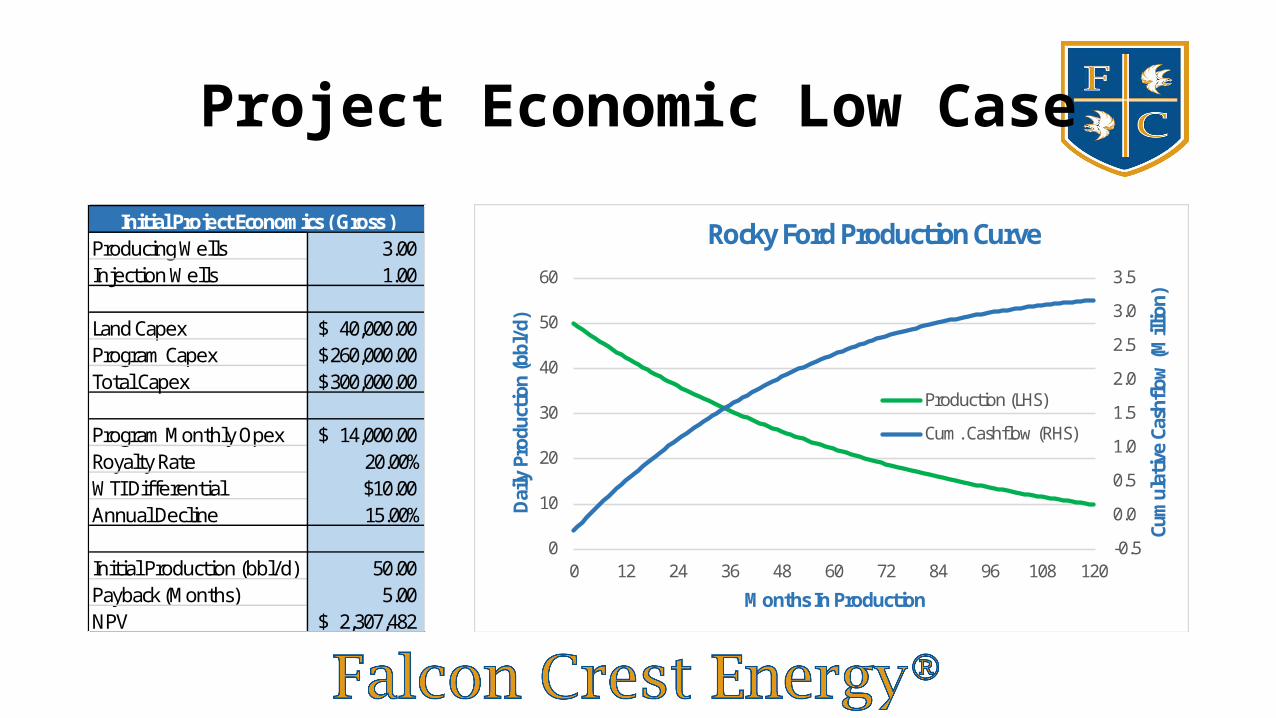

Project Economic Low Case

Producing Wells 3.00 Injection Wells 1.00

Land Capex 40,000.00$ Program Capex 260,000.00$ Total Capex 300,000.00$

Program Monthly Opex 14,000.00$ Royalty Rate 20.00%WTI Differential $10.00Annual Decline 15.00%

Initial Production (bbl/d) 50.00 Payback (Months) 5.00 NPV 2,307,482$

Initial Project Economics ( Gross )

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

0

10

20

30

40

50

60

0 12 24 36 48 60 72 84 96 108 120

Cum

ulati

ve C

ashfl

ow (M

illio

n)

Dai

ly P

rodu

ction

(bbl

/d)

Months In Production

Rocky Ford Production Curve

Production (LHS)

Cum. Cashflow (RHS)

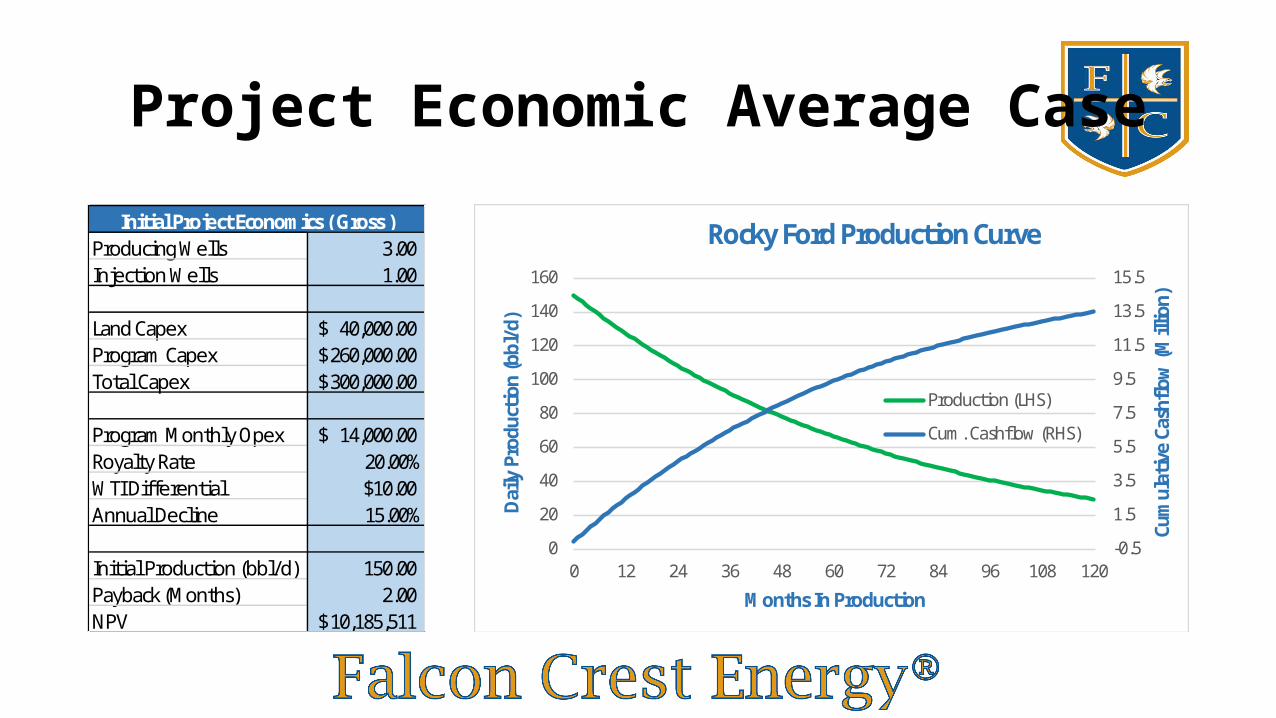

Project Economic Average Case

Producing Wells 3.00 Injection Wells 1.00

Land Capex 40,000.00$ Program Capex 260,000.00$ Total Capex 300,000.00$

Program Monthly Opex 14,000.00$ Royalty Rate 20.00%WTI Differential $10.00Annual Decline 15.00%

Initial Production (bbl/d) 150.00 Payback (Months) 2.00 NPV 10,185,511$

Initial Project Economics ( Gross )

-0.5

1.5

3.5

5.5

7.5

9.5

11.5

13.5

15.5

0

20

40

60

80

100

120

140

160

0 12 24 36 48 60 72 84 96 108 120

Cum

ulati

ve C

ashfl

ow (M

illio

n)

Dai

ly P

rodu

ction

(bbl

/d)

Months In Production

Rocky Ford Production Curve

Production (LHS)

Cum. Cashflow (RHS)

Project Economic High Case

Producing Wells 3.00 Injection Wells 1.00

Land Capex 40,000.00$ Program Capex 260,000.00$ Total Capex 300,000.00$

Program Monthly Opex 14,000.00$ Royalty Rate 20.00%WTI Differential $10.00Annual Decline 15.00%

Initial Production (bbl/d) 400.00 Payback (Months) 1.00 NPV 29,880,583$

Initial Project Economics ( Gross )

-0.5

4.5

9.5

14.5

19.5

24.5

29.5

34.5

39.5

44.5

0

50

100

150

200

250

300

350

400

450

0 12 24 36 48 60 72 84 96 108 120

Cum

ulati

ve C

ashfl

ow (M

illio

n)

Dai

ly P

rodu

ction

(bbl

/d)

Months In Production

Rocky Ford Production Curve

Production (LHS)

Cum. Cashflow (RHS)

21

Sections Currently Owned

22

Rocky Ford Prospect

Two Initial Sand Dune Targets

23

Blue Sky

• Multiple wells per Sand Dune• Sand Dunes range from 4-5 Million Barrels Recoverable• Two Initial Sand Dunes well supported• Multiple Sand Dunes in larger package• Only $100,000 USD to Test including land• Theory supports existence of up to 5 Billion Barrels

24

Davis Family -Phosphoria Project – 30,000 Acres

25

Davis Family Investments Deal• Convey 10% of common stock for rights to land package• Have two years to commence drilling• Control 30,000 acres in productive oil producing region• 80/20 deal on drilling• Study on land package by credible engineering firm concluded there

was 700 MBO in Place and over 300 MBO producible• Needs seismic and geological study to advance to drilling stage• DFI to provide IR/PR support as part of deal

26

Next Steps 2014

1. Acquire Equity Conversion and New Financing - November2. Announce Davis Trust Drilling Deal - November3. Acquire additional acreage around Rocky Ford - November4. Announce drilling plans for Rocky Ford - December5. Drill Rocky Ford - January6. If Rocky Ford is successful we will acquire as much acreage as possible around Rocky Ford, Burnt Hollow and Zimmerschied7. Raise $1-3 Million to conduct seismic on Davis land and advance Rocky Ford8. Move to AMEX

Terry Lynch - Chairman Patrick Johnson - CEO

Co-Founder Pacific Tiger Energy CEO Victura Construction CEO Chilean Metals Super Bowl Champ

Management Team & Advisors

Mike Cvetanovic Denis Clement Scott Davis Peter KentAdvisor O&G Hedge Fund Fmr Pres. CGX Energy R D Davis Partner LLBExploration Geologist $1 Billion Raised 1,000,000 acres Multiple M&A

27

28

100 KING STREET WEST SUITE 5600

TORONTO, ONTARIO M5X-1C9

O/F (888) 570.3698

WWW.falconcrestenergy.COM

Contact: [email protected]

777 MAIN STREET SUITE 615 FORT WORTH, TEXAS 76102O/F (888) 570.3698WWW.falconcrestenergy.COM

Bonanza Potential in Wyoming