brighton & hove connected and partnerships & partnership... · brighton & hove...

TRANSCRIPT

Simon Newell, Head of Partnerships & External

Relations, Brighton & Hove Connected

Brighton & Hove Connected and

Partnerships

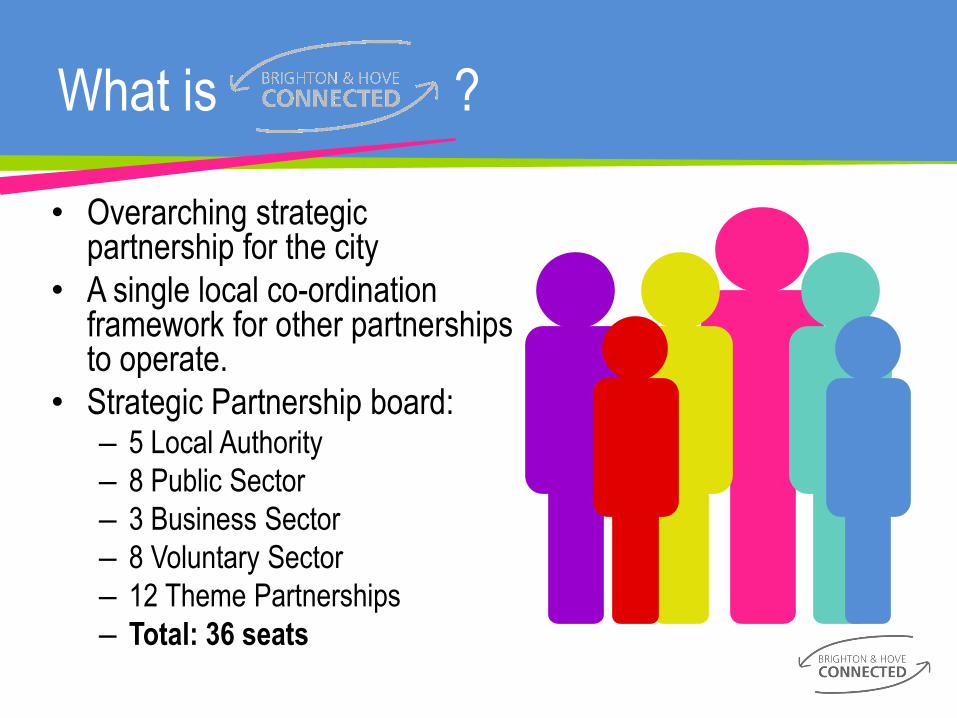

What is ?

• Overarching strategic partnership for the city

• A single local co-ordination framework for other partnerships to operate.

• Strategic Partnership board: – 5 Local Authority

– 8 Public Sector

– 3 Business Sector

– 8 Voluntary Sector

– 12 Theme Partnerships

– Total: 36 seats

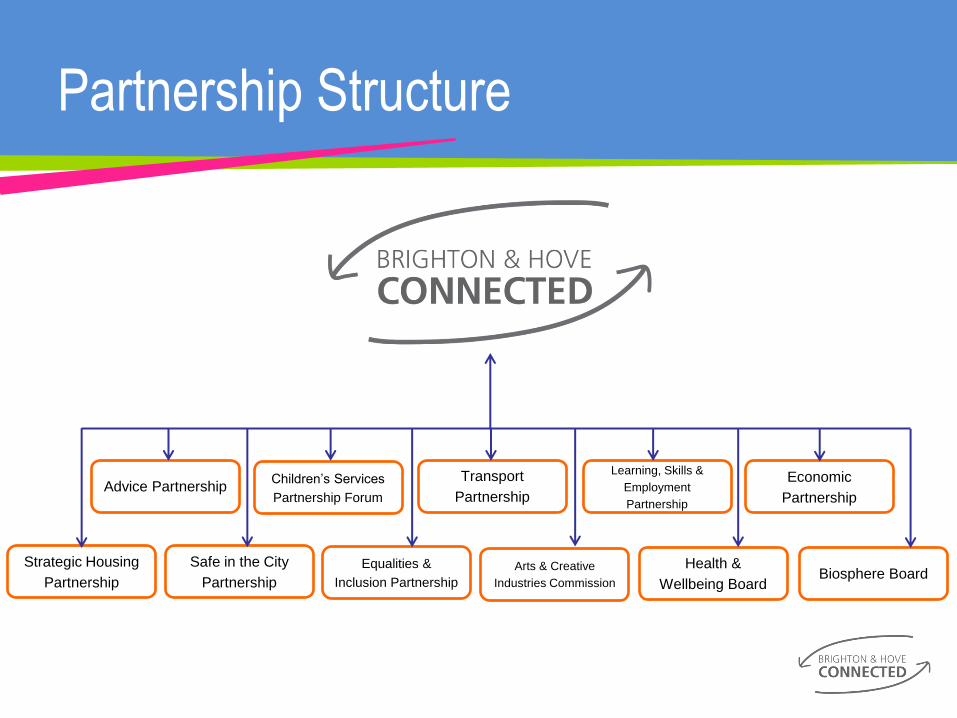

Partnership Structure

Children’s Services

Partnership Forum

Strategic Housing

Partnership

Safe in the City

Partnership

Equalities &

Inclusion Partnership

Arts & Creative

Industries Commission

Transport

Partnership

Health &

Wellbeing Board

Economic

Partnership

Learning, Skills &

Employment

Partnership

Advice Partnership

Biosphere Board

Sustainable Community Strategy

The Sustainable Community

Strategy (SCS) is the

overarching strategic

document for the city.

Brighton & Hove Connected

oversees the development

and implementation of this

strategy

SCS Partnership Approaches

ECONOMY

• Sarah Springford

Director, Brighton & Hove Chamber of Commerce

Business Sector Rep.

• Dean Orgill

Chairman, Mayo Wynne Baxter LLP

Chair, Economic Partnership

• Gavin Stewart

Executive Director, Economic Partnership

Housing

• Julie Frith

Director, Mishon Mackay Land and New Homes

Strategic Housing Partnership Rep.

• Martin Reid

Head of Housing Strategy, Brighton & Hove City

Council

Housing in Brighton and Hove

Martin Reid Head of Housing Strategy, Development & Private Sector Housing

t: +44 (0)1273 293321

Brighton and Hove

• 280,000 people in 130,000 homes

• High property prices and low incomes

• Small social rented sector, large private rented sector

• Non-decent housing across all tenures, primarily affecting the vulnerable

• 25% of households in the city contain a member with a long term health problem or disability

• High levels of mental health, physical disability, drug use

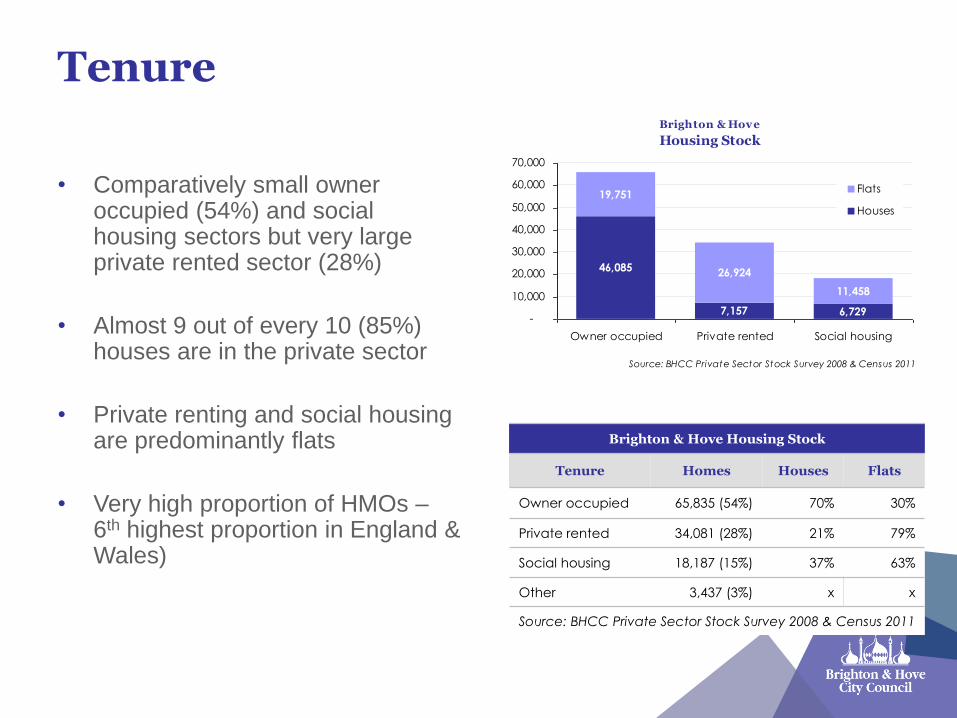

Tenure

• Comparatively small owner occupied (54%) and social housing sectors but very large private rented sector (28%)

• Almost 9 out of every 10 (85%) houses are in the private sector

• Private renting and social housing are predominantly flats

• Very high proportion of HMOs – 6th highest proportion in England & Wales)

Brighton & Hove Housing Stock

Tenure Homes Houses Flats

Owner occupied 65,835 (54%) 70% 30%

Private rented 34,081 (28%) 21% 79%

Social housing 18,187 (15%) 37% 63%

Other 3,437 (3%) x x

Source: BHCC Private Sector Stock Survey 2008 & Census 2011

Brighton & Hove

Housing Stock

46,085

7,157 6,729

19,751

26,924

11,458

-

10,000

20,000

30,000

40,000

50,000

60,000

70,000

Owner occupied Private rented Social housing

Flats

Houses

Source: BHCC Private Sector Stock Survey 2008 & Census 2011

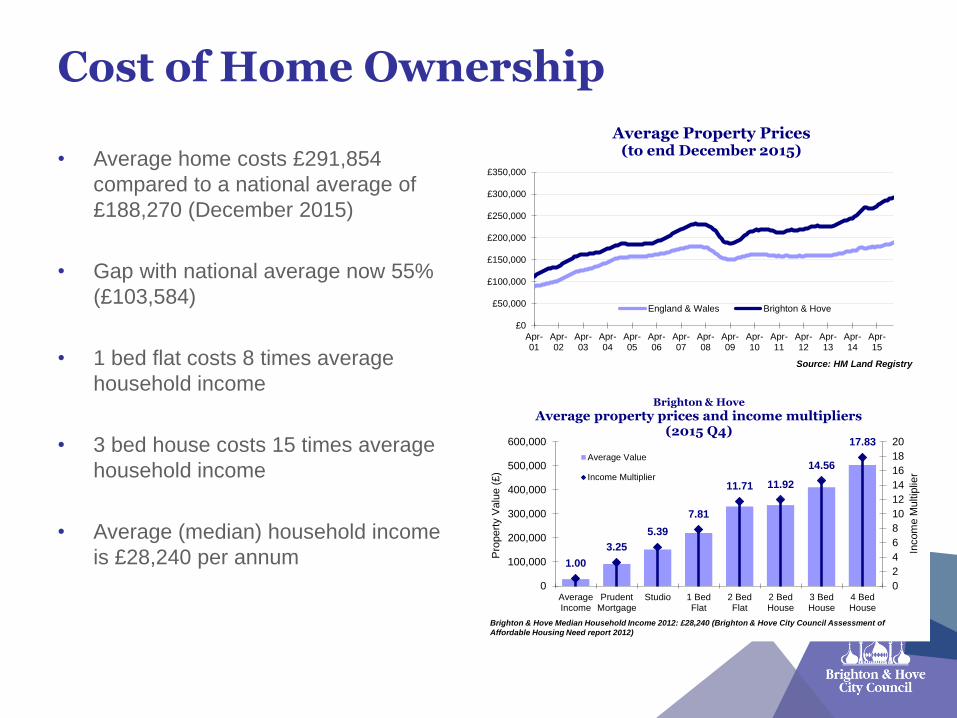

Cost of Home Ownership

• Average home costs £291,854

compared to a national average of

£188,270 (December 2015)

• Gap with national average now 55%

(£103,584)

• 1 bed flat costs 8 times average

household income

• 3 bed house costs 15 times average

household income

• Average (median) household income

is £28,240 per annum

£0

£50,000

£100,000

£150,000

£200,000

£250,000

£300,000

£350,000

Apr-01

Apr-02

Apr-03

Apr-04

Apr-05

Apr-06

Apr-07

Apr-08

Apr-09

Apr-10

Apr-11

Apr-12

Apr-13

Apr-14

Apr-15

Average Property Prices (to end December 2015)

England & Wales Brighton & Hove

Source: HM Land Registry

1.00

3.25

5.39

7.81

11.71 11.92

14.56

17.83

0

2

4

6

8

10

12

14

16

18

20

0

100,000

200,000

300,000

400,000

500,000

600,000

AverageIncome

PrudentMortgage

Studio 1 BedFlat

2 BedFlat

2 BedHouse

3 BedHouse

4 BedHouse

Incom

e M

ultip

lier

Pro

pert

y V

alu

e (

£)

Brighton & Hove

Average property prices and income multipliers (2015 Q4)

Average Value

Income Multiplier

Brighton & Hove Median Household Income 2012: £28,240 (Brighton & Hove City Council Assessment of

Affordable Housing Need report 2012)

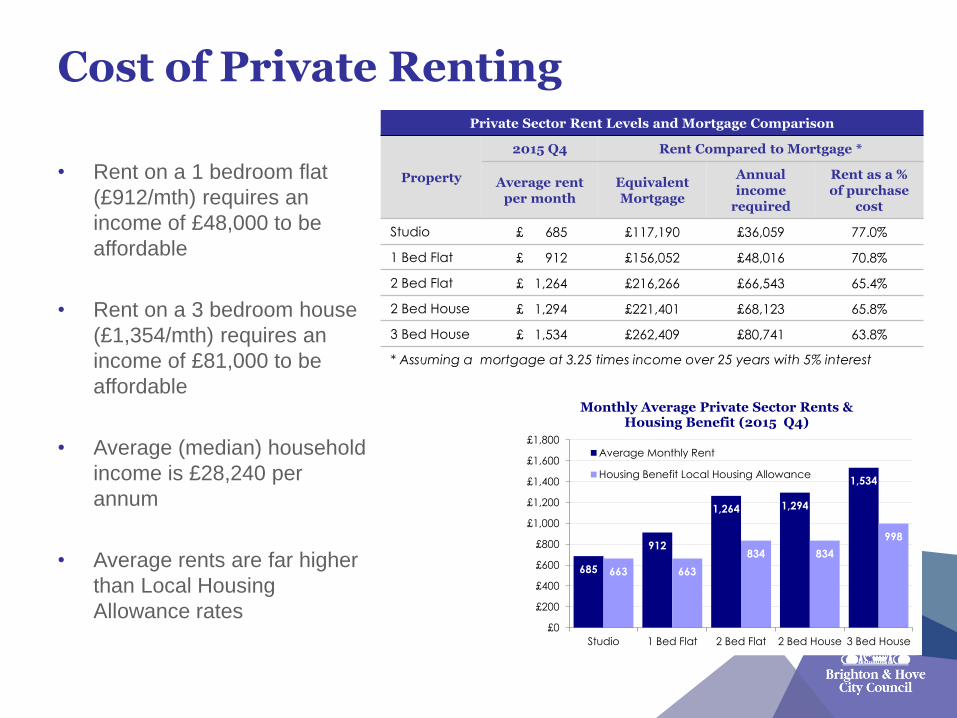

Cost of Private Renting

• Rent on a 1 bedroom flat

(£912/mth) requires an

income of £48,000 to be

affordable

• Rent on a 3 bedroom house

(£1,354/mth) requires an

income of £81,000 to be

affordable

• Average (median) household

income is £28,240 per

annum

• Average rents are far higher

than Local Housing

Allowance rates

Private Sector Rent Levels and Mortgage Comparison

Property

2015 Q4 Rent Compared to Mortgage *

Average rent per month

Equivalent Mortgage

Annual income

required

Rent as a % of purchase

cost

Studio £ 685 £117,190 £36,059 77.0%

1 Bed Flat £ 912 £156,052 £48,016 70.8%

2 Bed Flat £ 1,264 £216,266 £66,543 65.4%

2 Bed House £ 1,294 £221,401 £68,123 65.8%

3 Bed House £ 1,534 £262,409 £80,741 63.8%

* Assuming a mortgage at 3.25 times income over 25 years with 5% interest

685

912

1,264 1,294

1,534

663 663

834 834

998

£0

£200

£400

£600

£800

£1,000

£1,200

£1,400

£1,600

£1,800

Studio 1 Bed Flat 2 Bed Flat 2 Bed House 3 Bed House

Monthly Average Private Sector Rents & Housing Benefit (2015 Q4)

Average Monthly Rent

Housing Benefit Local Housing Allowance

Housing Affordability

• Minimum household income required to afford market housing without subsidy is £42,000 per annum (average income £28,240)

• 87,945 households (72%) can not afford market housing without spending a disproportionate level of their income on housing costs or some form of subsidy

• Without using housing benefit, social rent is the only tenure affordable to the majority of those in need:

– 8.5% Intermediate Rent

– 32.5% Affordable Rent

– 59% Social Rent

Brighton & Hove Assessment of Affordable Housing Need Report 2012

Brighton & Hove (2012 Q4 Oct-Dec)

Average Monthly Housing Cost Comparison

£293

£332

£386

£402£

622

£903 £

1,1

59

£778

£1,1

29

£1,4

49

£753

£1,1

20 £

1,3

91

£650 £800 £950

£348

£294

£0

£200

£400

£600

£800

£1,000

£1,200

£1,400

£1,600

1 Bed 2 Bed 3 Bed

Local Authority (Social Rent)

Registered Prov ider (Social Rent)

Affordable Rent (80% Market)

Priv ate Rented

Owner (75% Mortgage)

Local Housing Allowance

Notes: The average rent for Registered Providers is based on 2011 figures and for the Local Authority is based on 2012/13 figures.

Average cost to buy based on a 25% deposit, 25 year mortgage at 5% interest

The city has a strong housing market which helps investment and reflects confidence in

Brighton & Hove, however

Homelessness

• 2,000+ households have their homelessness prevented each year through detailed casework

• Homelessness is decreasing (21% in last 2 years)

• Over 2/3 of all homeless cases involve households with either children or a pregnant family member

• Proportion of homelessness due to physical disability or mental illness is generally double the national average

754 825

978

1,108

1,348 1,284

1,107

368 426

496 506 510 420 402

0

200

400

600

800

1,000

1,200

1,400

2009/10 2010/11 2011/12 2012/13 2013/14 2014/15 2015/16

Hou

se

ho

lds

Brighton & Hove

Homeless Decisions & Acceptances

Homelessness Decisions

Homeless Acceptances

Source: P1E

487 692 594

1,436 1,543 1,010

1,812

2,059 1,858

1,545 1,441

1,528

0

500

1,000

1,500

2,000

2,500

3,000

2009/10 2010/11 2011/12 2012/13 2013/14 2014/15

Hou

se

ho

lds

Brighton & Hove City Council Prevention Casework Outcomes

Sustained Accommodation Alternative Accommodation

Rough Sleeping

• Rough sleeping has been increasing in recent years:

– Estimate 78 people sleeping rough (Nov 2015)

– Brighton & Hove has third highest number after Westminster and Bristol

– 1,129 cases involving 776 people (2014/15)

– Approximately 4 in 10 have a local B&H connection, 4 in 10 are from the rest of UK, 2 in 10 are international

– Average of more than 2 new people every day seen by services

– Almost 300 hostel beds full with around 200 on the waiting list

– Nationally, the average age of death of someone sleeping rough is 47 compared to 77 for population as a whole

• New Rough Sleeping Strategy in development

– Final strategy expected to be recommended to B&H Connected for approval on 5 July 2016

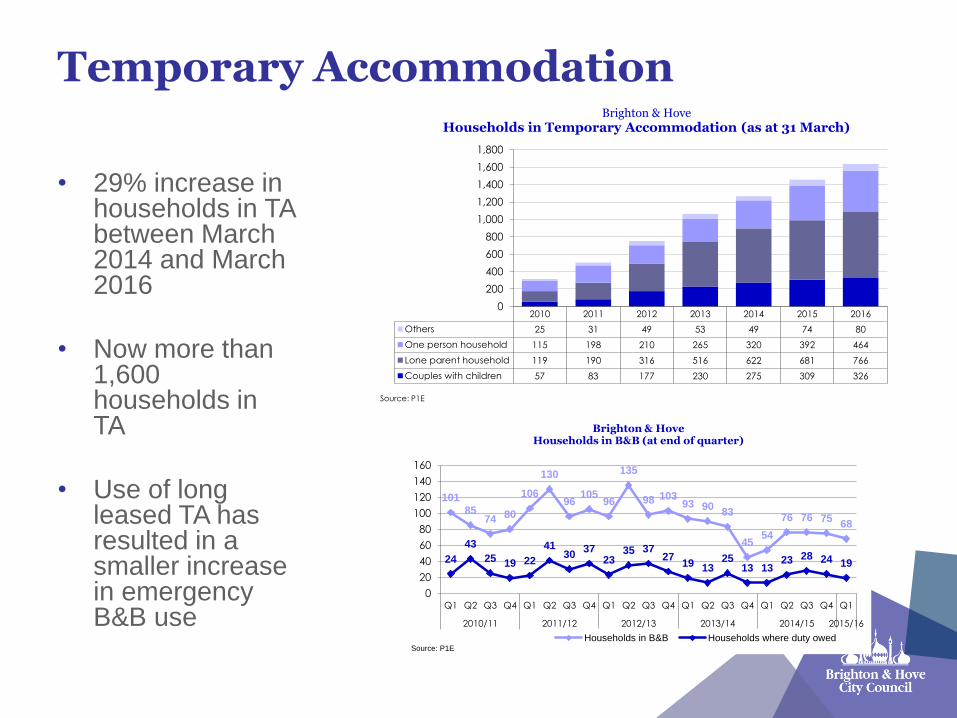

Temporary Accommodation

• 29% increase in households in TA between March 2014 and March 2016

• Now more than 1,600 households in TA

• Use of long leased TA has resulted in a smaller increase in emergency B&B use

2010 2011 2012 2013 2014 2015 2016

Others 25 31 49 53 49 74 80

One person household 115 198 210 265 320 392 464

Lone parent household 119 190 316 516 622 681 766

Couples with children 57 83 177 230 275 309 326

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Brighton & Hove

Households in Temporary Accommodation (as at 31 March)

Source: P1E

101

85 74 80

106

130

96 105

96

135

98 103 93 90

83

45 54

76 76 75 68

24

43

25 19 22

41 30

37 23

35 37 27

19 13 25

13 13 23 28 24 19

0

20

40

60

80

100

120

140

160

Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1 Q2 Q3 Q4 Q1

2010/11 2011/12 2012/13 2013/14 2014/15 2015/16

Brighton & Hove Households in B&B (at end of quarter)

Households in B&B Households where duty owedSource: P1E

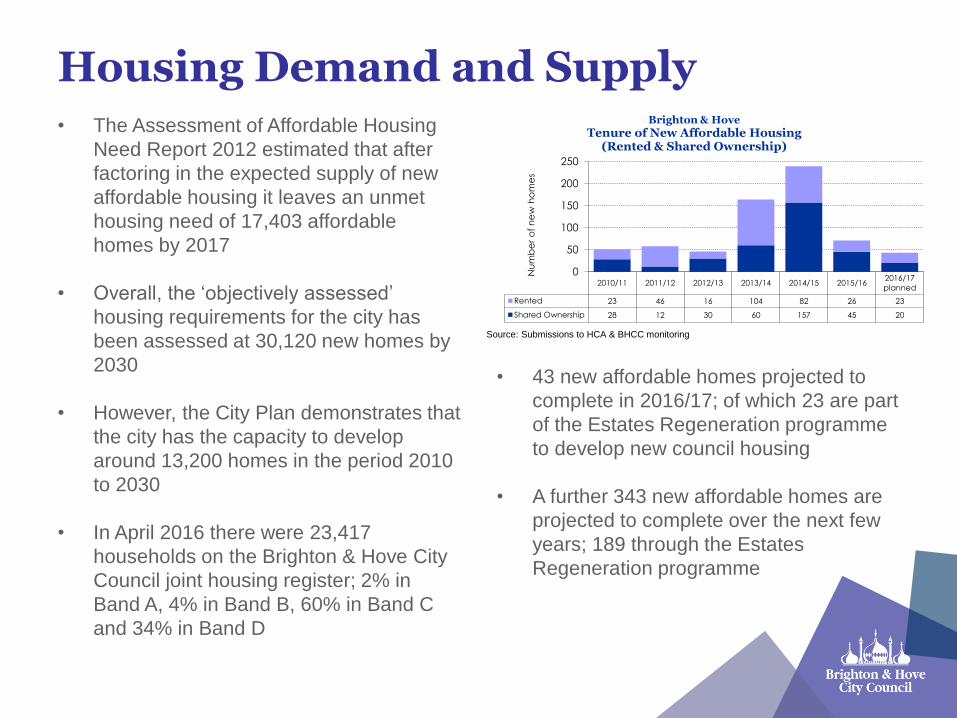

Housing Demand and Supply • The Assessment of Affordable Housing

Need Report 2012 estimated that after

factoring in the expected supply of new

affordable housing it leaves an unmet

housing need of 17,403 affordable

homes by 2017

• Overall, the ‘objectively assessed’

housing requirements for the city has

been assessed at 30,120 new homes by

2030

• However, the City Plan demonstrates that

the city has the capacity to develop

around 13,200 homes in the period 2010

to 2030

• In April 2016 there were 23,417

households on the Brighton & Hove City

Council joint housing register; 2% in

Band A, 4% in Band B, 60% in Band C

and 34% in Band D

• 43 new affordable homes projected to

complete in 2016/17; of which 23 are part

of the Estates Regeneration programme

to develop new council housing

• A further 343 new affordable homes are

projected to complete over the next few

years; 189 through the Estates

Regeneration programme

2010/11 2011/12 2012/13 2013/14 2014/15 2015/162016/17

planned

Rented 23 46 16 104 82 26 23

Shared Ownership 28 12 30 60 157 45 20

0

50

100

150

200

250

Nu

mb

er

of

ne

w h

om

es

Brighton & Hove

Tenure of New Affordable Housing (Rented & Shared Ownership)

Source: Submissions to HCA & BHCC monitoring

Non-Decent Housing

• Poor quality housing has a direct impact on resident’s quality of life and a subsequent impact on the public purse due to illness and being out of work

• Almost a third of the city’s housing stock (up to 37,000 homes) is considered to be non-decent (99.9% in the private sector)

• More than 4 in 10 of the city’s LSOAs (Lower Super Output Areas) are in the bottom 20% nationally for housing quality

• 11.9% of households (15,500) are in fuel poverty

Figure 3: 39% of Brighton & Hove Lower Super Output Areas are in the lowest 20% nationally on the Indoor Living Environment sub domain (Index of Multiple Deprivation 2015)

Ma

p ©

20

15

Go

og

le

Student Housing

• Increasing student numbers – currently 33,360

• By 2014/15 University of Brighton predict that 6,347 students will reside off campus in private rented accommodation

• Has directly led to a loss of family homes, through concentrations of HMOs – particularly around the Lewes Road corridor

• Student Housing Strategy – actions to address include HMO additional licensing, Article 4 Planning directive and increasing purpose built accommodation

Supporting Independence

• The Council funds housing support to more than 3,500 residents to maintain their independence

• Our programme (approximately £8m) is estimated to save the wider public sector an additional £33m after allowing for our costs

• Targeted services such as hostels for

rough sleepers, the domestic violence

refuge and special projects working

with a range of groups such as those

with learning disabilities or mental

health problems

• Every £1 spent saves an additional £4.10 in care, health, police and housing costs

• 25% of households in the city contain a member with a long term health problem or disability (Census 2011)

• The proportion of homelessness acceptances that are related to a physical disability are around double the national average

• Spending £2,000-£20,000 on adaptations to support an older person at home can save £6,000 per year in care costs

• During 2014/15 we completed 179 Disabled Facilities Grant assisted major adaptations to support private sector households plus 238 major and 655 minor adaptations to council properties worth £2.6m

Delivering our Housing Strategy

• Improving housing supply:

– Building new council housing with more than 250 homes in the pipeline

– Exploring the potential for a joint venture company to develop new affordable housing (looking at options such as modern off-site manufacture, living wage rents and mortgages)

– Helping owners bring more than 150 empty homes back into use each year

• Improving housing quality:

– Expanding additional licensing of houses in multiple occupation into the city centre wards

– Exploring the evidence to support or reject the need for licensing across those whole private rented sector (citywide or in certain locations)

– Continuing to invest in council homes

• Improving housing support:

– Improving the provision of adaptations and disabled facilities grants to support residents to be independent at home

– Working with partners on early interventions to sustain tenancies and tackle, prevent and reduce homelessness

– Providing a comprehensive home options service for those seeking homes as a first point of contact with the council, including sustaining tenancies and early interventions with hospitals and GPs to prevent homelessness

– Developing a new Rough Sleeping Strategy to make sure no one in Brighton & Hove has the need to sleep rough by 2020 (for B&H Connected approval on 5 July 2016)

LEARNING, SKILLS AND EMPLOYMENT

Learning, Skills & Employment

Partnership

Update for Brighton & Hove Connected

Marcelo Staricoff Headteacher of Balfour Primary and

representing the Learning, Skills and

Employment Partnership

Learning • Brighton & Hove residents are well educated compared to the

South East and England.

• 16% of people have no qualifications in Brighton & Hove

compared with 22% across England

• Test and exam results improved in all key stages in

2014/2015, making Brighton & Hove in the top quartile for

attainment

• The achievement of vulnerable groups remains a priority. The

gap between their outcomes and those of ‘other’ pupils

nationally is too wide

• We are developing a schools supporting schools partnership

model

Skills and Employment

• There has been a focus this year on the City Employment and Skills Plan.

• Emerging priorities include:

- Assisting people back into the labour market

- Increase and make systematic the number of Apprenticeships

- Review and improve Careers and IAG offer

- Consider work readiness

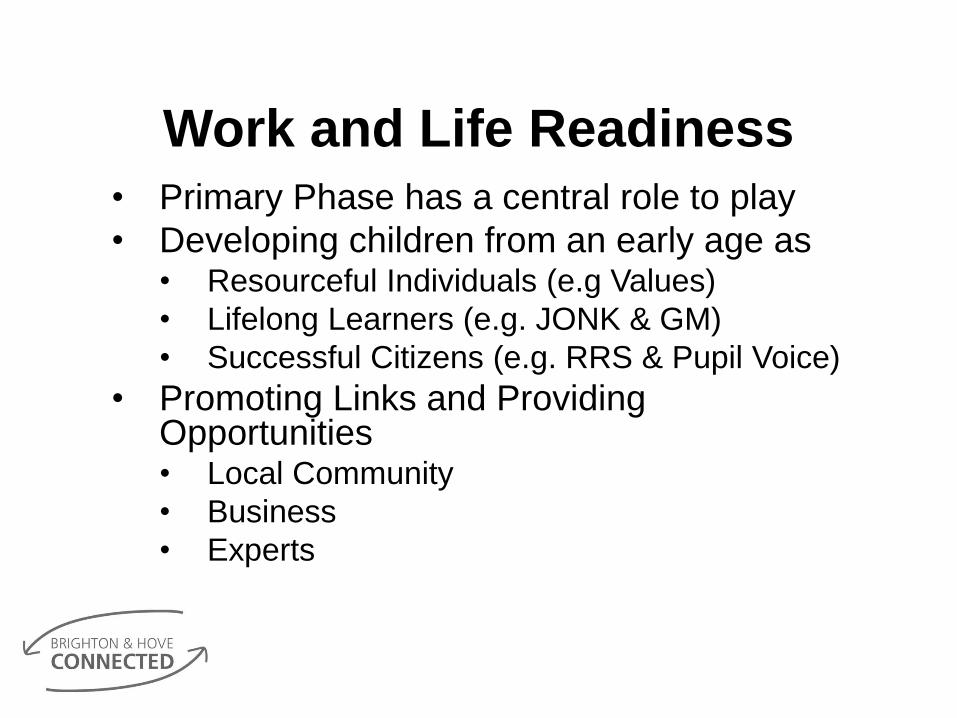

Work and Life Readiness

• Primary Phase has a central role to play

• Developing children from an early age as • Resourceful Individuals (e.g Values)

• Lifelong Learners (e.g. JONK & GM)

• Successful Citizens (e.g. RRS & Pupil Voice)

• Promoting Links and Providing Opportunities • Local Community

• Business

• Experts

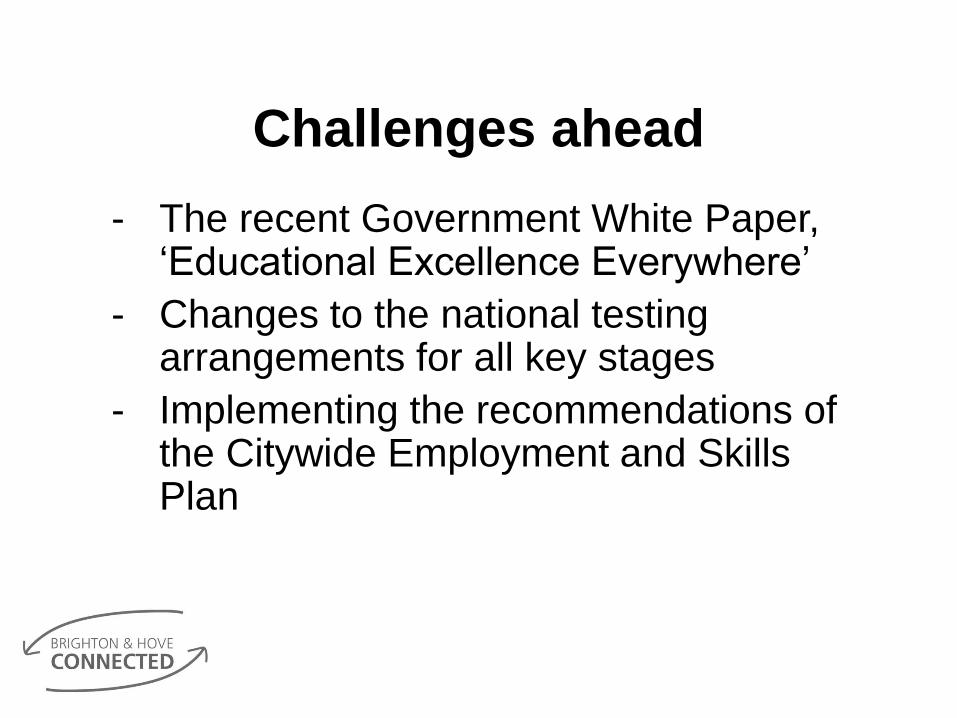

Challenges ahead

- The recent Government White Paper, ‘Educational Excellence Everywhere’

- Changes to the national testing arrangements for all key stages

- Implementing the recommendations of the Citywide Employment and Skills Plan

LEARNING, SKILLS AND EMPLOYMENT

Children’s Services Partnership Forum

Update for Brighton & Hove Connected

Pinaki Ghoshal Executive Director, Children's Services

Brighton & Hove City Council

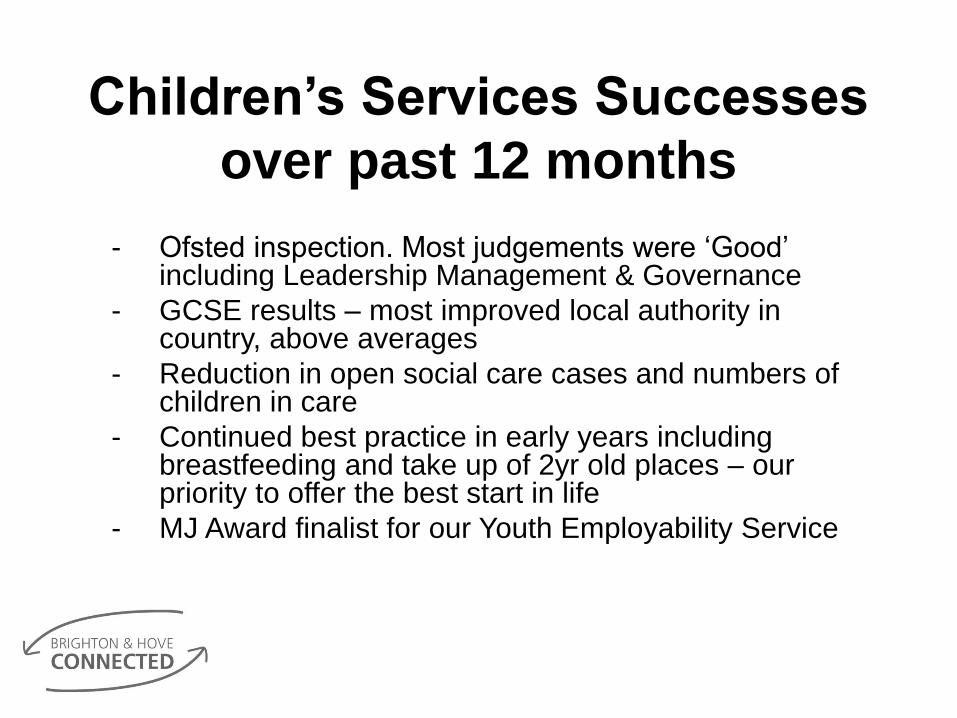

Children’s Services Successes

over past 12 months

- Ofsted inspection. Most judgements were ‘Good’ including Leadership Management & Governance

- GCSE results – most improved local authority in country, above averages

- Reduction in open social care cases and numbers of children in care

- Continued best practice in early years including breastfeeding and take up of 2yr old places – our priority to offer the best start in life

- MJ Award finalist for our Youth Employability Service

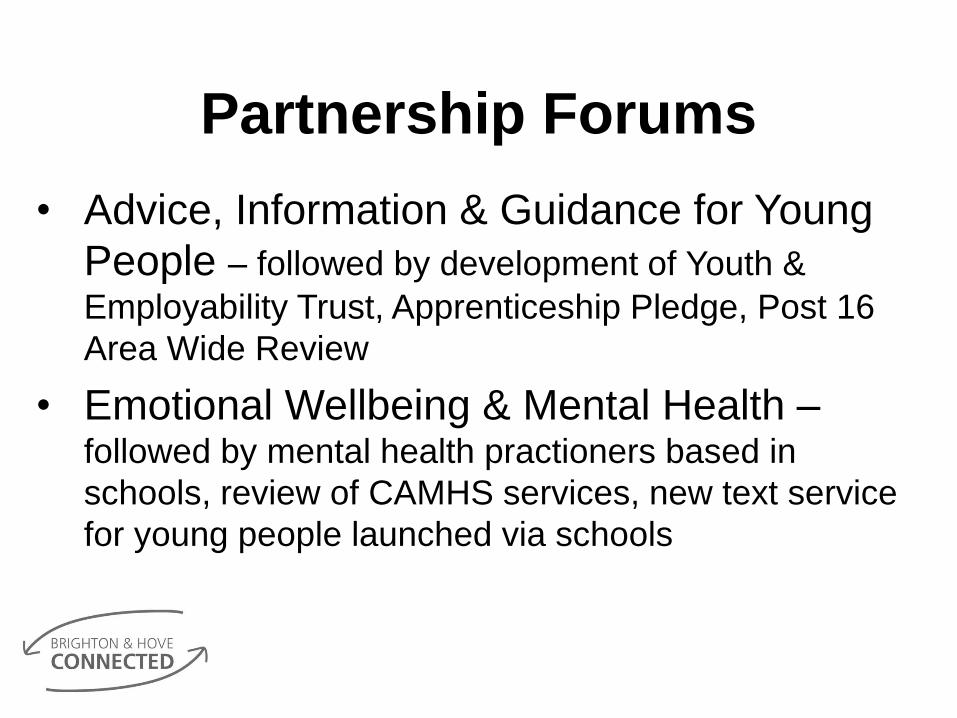

Partnership Forums

• Advice, Information & Guidance for Young

People – followed by development of Youth &

Employability Trust, Apprenticeship Pledge, Post 16

Area Wide Review

• Emotional Wellbeing & Mental Health – followed by mental health practioners based in

schools, review of CAMHS services, new text service

for young people launched via schools

Challenges ahead

- More inspections. Two new challenging frameworks for multi-agency safeguarding and services for SEND

- Significant amount of change and restructures underway

- Continued challenge of managing budget in context of fluctuating demand

- Income streams such as Stronger Families Programme under increasing pressure to deliver more for reduced financial offer

A future with greater

partnership working

- It takes a city to raise a child – join our discussions on 21st June on creating a child centred city

- Maintain the focus on tackling the causes of poverty

- How can we do more to ensure there is greater coordination on both preventative and more intensive early help?

COMMUNITIES AND EQUALITIES

• Sally Polanski

Chief Executive, Brighton & Hove Community Works

Community Works Rep.

• Geraldine Des Moulins

Chief Officer, The Fed Centre for Independent Living

Equalities & Inclusion Partnership Rep.

• Emma McDermott

Head of Communities & Equality, Brighton & Hove City

Council

Communities: recent successes

• Community collaboration and asset building

• Targeted work: BME, LGBT, disability, faith

• Employment engagement (BME/disability)

• NCE and EQUIP

• Fairness Commission

• Power of Volunteering

Power of Volunteering Vision & Commitments

Brighton & Hove, a city which champions volunteering:

valuing the contribution that volunteers make; striving to

ensure positive volunteering experiences; and recognising

the impact of volunteering on the economic, social,

cultural, leisure and environmental life of the city.

Communities: challenges

• Neighbourhood hubs

• Service redesign involving residents and providers

• Commissioning

• Social Value Framework

• Third Sector Investment Programme

• Need and capacity

Communities: further collaboration needed

• Power of Volunteering: implementing the pledge

• Equalities: embedded approach within BHC

partnerships

• Local Giving: strategies to increase it

• Health inequalities: community resilience in the

context of changing primary care

HEALTH AND WELLBEING

• Simon Newell

Head of Partnerships & External Relations, Brighton

& Hove Connected

Independent Secretariat

Brighton and Hove CCG Achievements and Challenges

John Child

April 2016

The recent successes over the last 12 months

•Primary Care:

•Developed clusters of general practice working

together to deliver new proactive models of care

tailored to the needs of those individuals most at

risk of losing their independence

•Piloted new model of care and support for

homeless

•Children’s Services:

•Implemented Paediatric Liaison Service at Royal

Alex Children’s Hospital

The recent successes over the last 12 months

•Communications and engagement:

•National accolades for DOM Joly’s ‘not QUITE

an emergency’ campaign

•Online GP guide for supporting Trans patients

•Bespoke website for general practice

•Partnership working with community and

voluntary sector

•Hospital Services:

•Reduction in the number of patients attending

hospital as an emergency

•

The recent successes over the last 12 months

•Medicines Management:

•Reduction in prescribing costs

•Pharmacists supporting clusters of general

practice

•Care home medication reviews

• Mental Health:

•Crisis care concordat – reduction in the number

of people detained under Section 136 who go to

custody

•Increased dementia diagnosis rate by 20%

The challenges for the next year

• Health & Well Being: life limiting illness, social

isolation, mental health & substance misuse,

homelessness

• Care & Quality Gap: NHS Constitutional targets-

A&E performance, referral to treatment, cancer

outcomes & care home admission targets, need

to sustain and develop primary care

• Finance & efficiency gap: CCG achieved a

surplus for 15/16, provider deficit for 15/16 &

financial challenges within City Council

Areas that you think could benefit from further collaboration or input from other partners.

•Integrated commissioning and provision

•Working collaboratively to tackle:

•Homelessness

•Substances misuse

•Social Isolation

•Workforce

•Housing

•Ensuring that:

•every child has a good start in life

•People are supported to improve their health and

wellbeing

ADVICE AND WELFARE

• Jackie Grigg

Chief Executive, Money Advice Plus

• Emily Ballantyne

Moneyworks Co-ordinator, Brighton & Hove

Citizen's Advice Bureau

Brighton and Hove Advice Partnership –

working together to help residents with debt,

benefits, housing, social care and employment

problems

Emily Ballantyne – Citizens Advice

Jackie Grigg – Money Advice Plus

Brighton and Hove Advice Partnership

Working in partnership to make Brighton & Hove a

fairer place

What does the Advice sector do?

We provide free, confidential and impartial advice, and give evidence to

policy makers about the big issues affecting people’s lives.

Our goal is to help everyone find a way forward, whatever problems

they face. We help people from all walks of life cope with life events

such as job loss, relationship breakdown, moving home and dealing

with ill health.

People come to us with all sorts of issues, mainly about benefits, debt,

housing and employment.

Last year the CAB and Money Advice Plus alone advised over 10,000

individual residents

Quality Assured Services

Expert advice:

• Debt and money

management

• Welfare Benefits

• Housing

Impact on residents and the city

The Advice Sector

• Keeps people in employment or helps them back to work

• Prevents housing evictions and statutory homelessness

• Reduces the demand for mental health and GP services

• Improves residents’ wellbeing and family relationships

• Benefits the local economy by increasing people’s income

• Mr G had to leave his job due to a back injury. He had a mortgage and

outstanding loans. He was able to claim Job Seekers Allowance but was

only entitled to 6 months of payments at £73.10 a week because his partner

was working.

• Mr G’s mental health deteriorated due to stress. He was seen by an adviser

whilst a patient at Millview Hospital. By this time his mortgage was in

arrears and his home was at risk, he had used all of the family’s savings to

pay bills and his credit cards were over their limits.

• An adviser helped him claim Employment and Support Allowance (ESA)

with Support for Mortgage Interest and arranged a mortgage holiday with

the lender for 39 weeks. He was also helped to claim Personal

Independence Payments (PIP). The adviser negotiated with the credit

cards on his behalf and arranged affordable repayments with a freeze on

interest and charges.

• Once his financial situation was stabilised and he understood how to

manage his benefit claims, he felt more under control and he was able to

focus on improving his health.

Case study

Success

through

partnership

• Moneyworks

• Webcam service

• Fuel Poverty partnership

• Bringing in investment from external

sources – British Gas Energy Trust, Big

Lottery

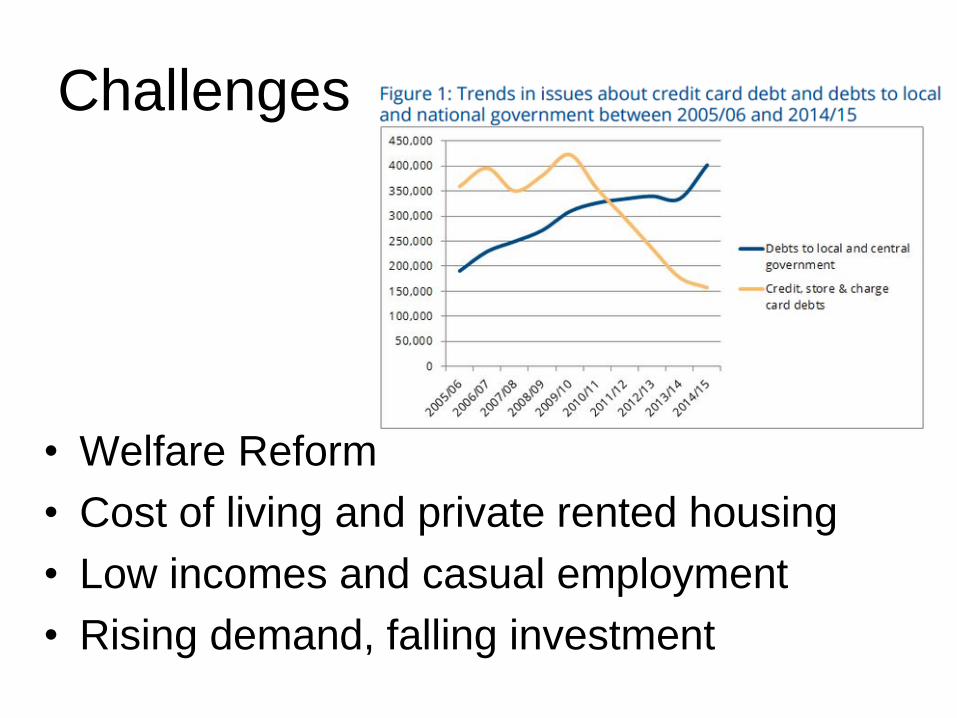

Challenges

• Welfare Reform

• Cost of living and private rented housing

• Low incomes and casual employment

• Rising demand, falling investment

ENVIRONMENT

• James Farrell

Environment Planning and Engagement Manager,

Environment Agency

• Vic Borrill

Director, Food Partnership

Biosphere Delivery Board Rep. and Vice-Chair

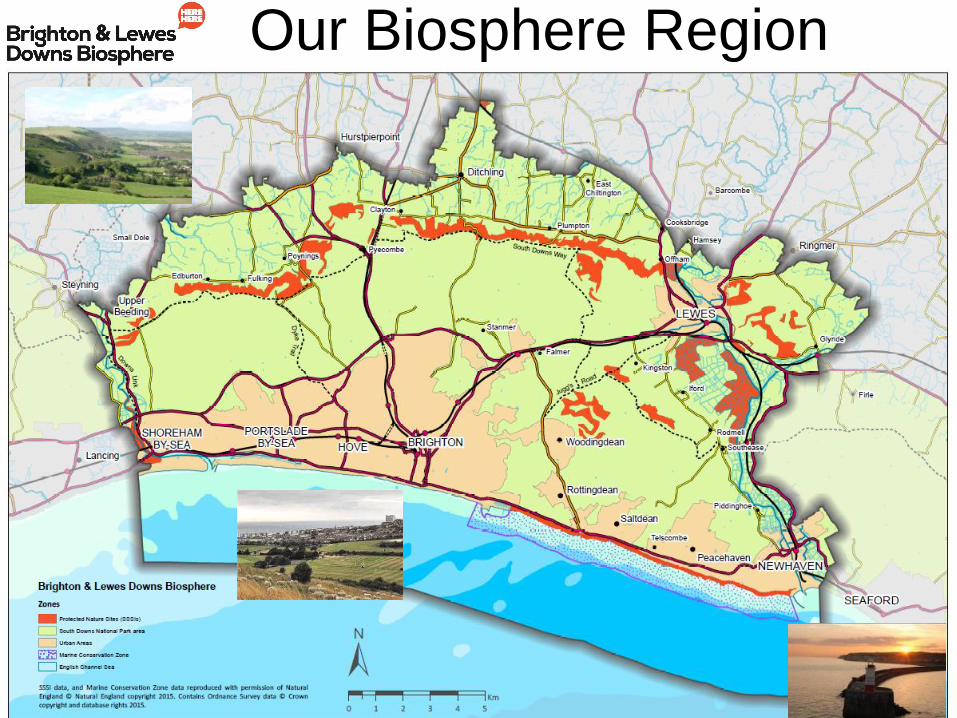

Our Biosphere Region

Our Biosphere Region

“Together we will create a

world-class environment, that

is economically successful and

enjoyed by all – forever”

Thematic partnership for Brighton & Hove Connected

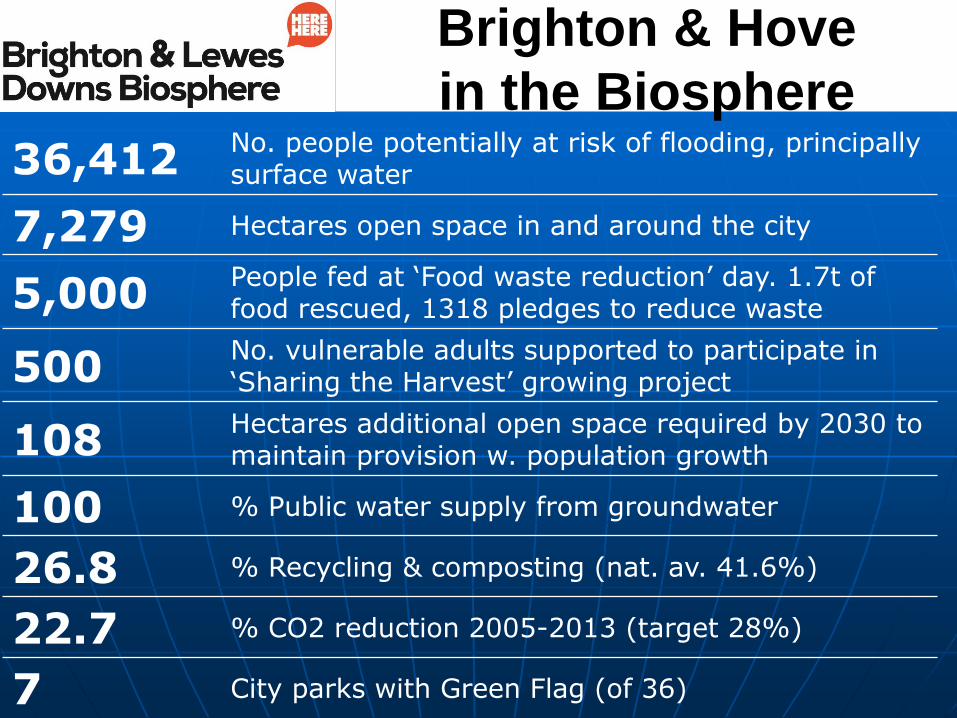

36,412 No. people potentially at risk of flooding, principally surface water

7,279 Hectares open space in and around the city

5,000 People fed at ‘Food waste reduction’ day. 1.7t of food rescued, 1318 pledges to reduce waste

500 No. vulnerable adults supported to participate in ‘Sharing the Harvest’ growing project

108 Hectares additional open space required by 2030 to maintain provision w. population growth

100 % Public water supply from groundwater

26.8 % Recycling & composting (nat. av. 41.6%)

22.7 % CO2 reduction 2005-2013 (target 28%)

7 City parks with Green Flag (of 36)

Brighton & Hove

in the Biosphere

Projects – Knowledge-

Learning-Awareness Recent Successes

• Creation of B&H’s first pilot ‘rain gardens’

• Delivery of innovative environmental education

Challenges for coming year

• Integrating environment in new policy & developments

• Develop ‘green infrastructure’ resilience & connections

• Growing eco-tourism in our Biosphere

• Connecting people with nature for health & wellbeing

Collaboration asks

• Closer working with Greater Brighton Economic Board

• Investment in the Biosphere delivery programme

TRAVEL

• Martin Harris

Managing Director, Brighton & Hove Bus Company

Transport Partnership Rep.

• Simon Newell

Head of Partnerships & External Relations, Brighton

& Hove Connected

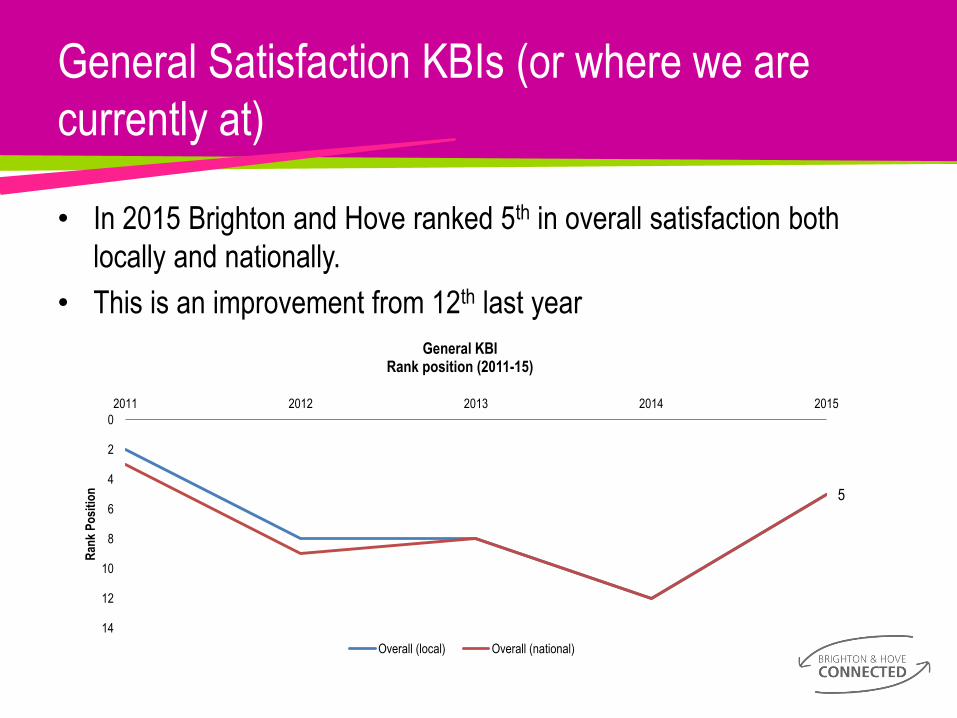

General Satisfaction KBIs (or where we are

currently at)

• In 2015 Brighton and Hove ranked 5th in overall satisfaction both

locally and nationally.

• This is an improvement from 12th last year

5

0

2

4

6

8

10

12

14

2011 2012 2013 2014 2015

Ran

k P

osi

tio

n

General KBI Rank position (2011-15)

Overall (local) Overall (national)

• Our overall satisfaction scores were also improved from last

year

59.2

58.9

59.2 59

57.1

56.8 56.6

56.4

57.6 57.4

55

55.5

56

56.5

57

57.5

58

58.5

59

59.5

Overall (local) Overall (national)

Sat

isfa

ctio

n S

core

KBI Performance Indicators

KBI Performance Overall

2011

2012

2013

2014

2015

57.6 57.4 55.2 55.3

0

10

20

30

40

50

60

Overall (local) Overall (national)

Sat

isfa

ctio

n S

core

KBI Performance Indicators

Satisfaction Scores

B&H satisfaction

Peer average

• Brighton and Hove satisfaction scores were also higher than

the peer average.

The Tackling Congestion KBI Satisfaction scores are as below.

43.77

48.23

58.46

45.22 45.25

56.37

43.3 46

53.7

40.6 47.5

54.2

40.9 47.4

55.9

0

10

20

30

40

50

60

70

Traffic levels & congestion Management of roadworks Traffic management

Sat

isfa

ctio

n S

core

KBI Performance Indicators

KBI Performance - Tackling Congestion

2011

2012

2013

2014

2015

Only one of the indicators has slipped slightly in satisfaction from

last year, however we must note that two of the indicators are still

below 50% satisfaction.

Road Safety KBIs

There are 3 KBIs for road safety.

Our national rankings are shown below.

10

24 25

0

5

10

15

20

25

30

35

40

45

50

2011 2012 2013 2014 2015

Ran

k P

osi

tio

n

Road Safety KBI Rank position (2011-15)

Road safety locally Road safety environment Road safety education

We have climbed significantly on all three since last year.

Compared to the peer group average we perform better across all

KBIs.

68.5

74.1

65.7

70.6

58.6 60 60.4

48.9

66.8

57.4

0

10

20

30

40

50

60

70

80

Local bus services Local bus services(BVPI 103)

Public TransportInfo (BVPI 103)

Taxi/mini cabservices

CommunityTransport

Sat

isfa

ctio

n S

core

KBI Performance Indicators

Public Transport KBI Satisfaction Scores

B&H Satsifaction

Peer Average

In particular we perform better on bus services and public transport

information.

Recent Successes

• The Transport Partnership itself

• Modal shift within the City

• Road Safety is improving

• Air quality is improving

• Accessibility

• Multi operator Smart Ticketing

• New bus links to the seafront

Current Challenges

• Coordination of Travel and traffic planning with

major capital investment programme

• Success of City as a whole leads to extra demand

on limited resources

• Congestion impacting journey times

• Brighton Station and Clocktower

Areas for Future Collaboration

Engagement from stakeholders in implementation of

LTP4 priorities…Transport should assist in • Grow the Economy

• Reduce Carbon Emissions

• Increase Safety & Security

• Provide Equality, Mobility & Accessibility

• Improve Health & Well-being

• Enhance the Public Realm

• Encourage Respect & Responsibility

More Areas for Future Collaboration

• Coach Strategy

• Freight/Delivery Strategy

• Interchange Strategy

• Information Strategy

• Corridor/Route Hierarchy

COMMUNITY SAFETY

• James Collis

Superintendent, Sussex Police

• Jayne Dando

Superintendent, Sussex Police

• Peter Castleton

Head of Community Safety, Brighton & Hove City

Council

Brighton and Hove Connected April 2016

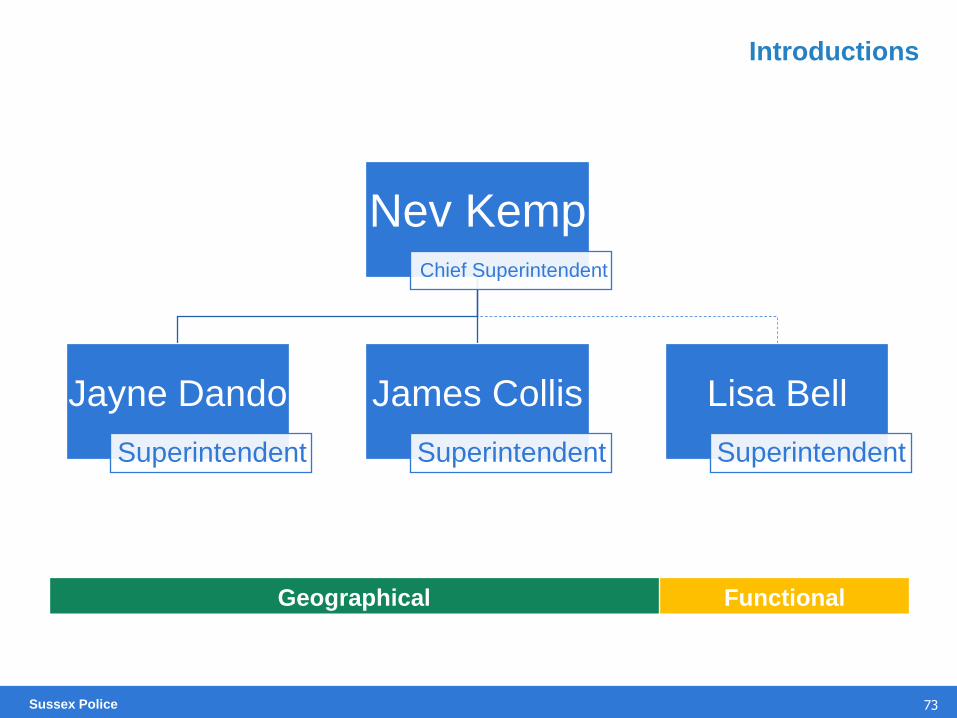

73 Sussex Police

Introductions

Nev Kemp Chief Superintendent

Jayne Dando

Superintendent

James Collis

Superintendent

Lisa Bell

Superintendent

Geographical Functional

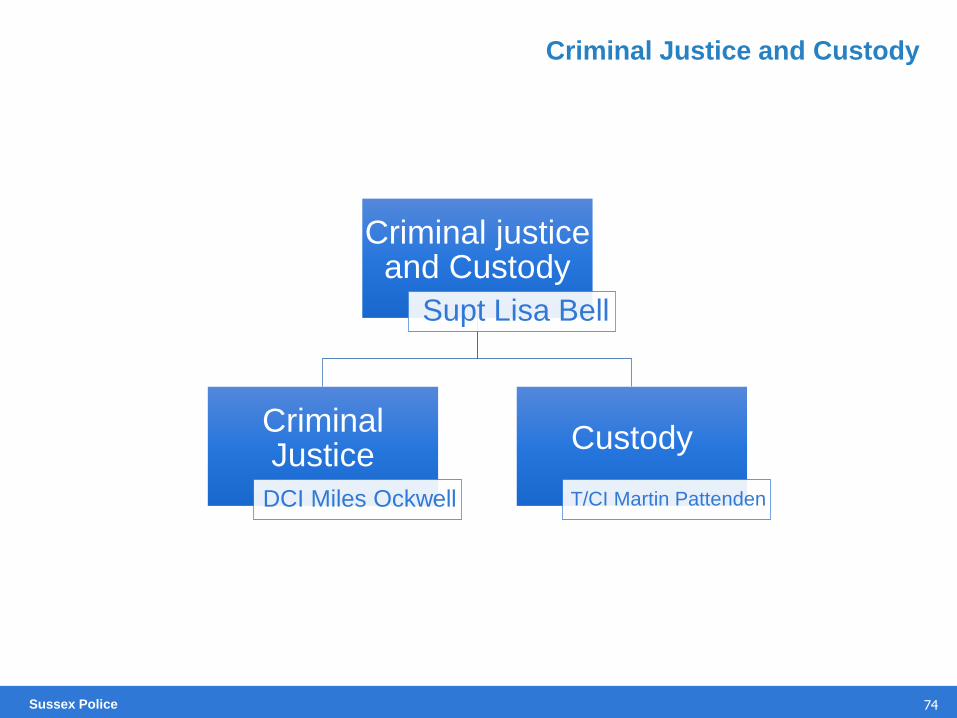

74 Sussex Police

Criminal Justice and Custody

Criminal justice and Custody

Supt Lisa Bell

Criminal Justice

DCI Miles Ockwell

Custody

T/CI Martin Pattenden

75 Sussex Police

Crime and Operations

Crime and Operations

Supt Jayne Dando

Operations

CI Chris Veale

Response

CI Katy Woolford

Investigations

DCI Steve Boniface

Public Protection

DCI Richard Bates

Licensing

Public Order

Events

Protests

Football

SAGs Chrysler

LST

Low level investigations

Mispers

1st Response Mental Health

RIT

CID

OCG

DA / DV

Drug Deaths

Coroners

SIU

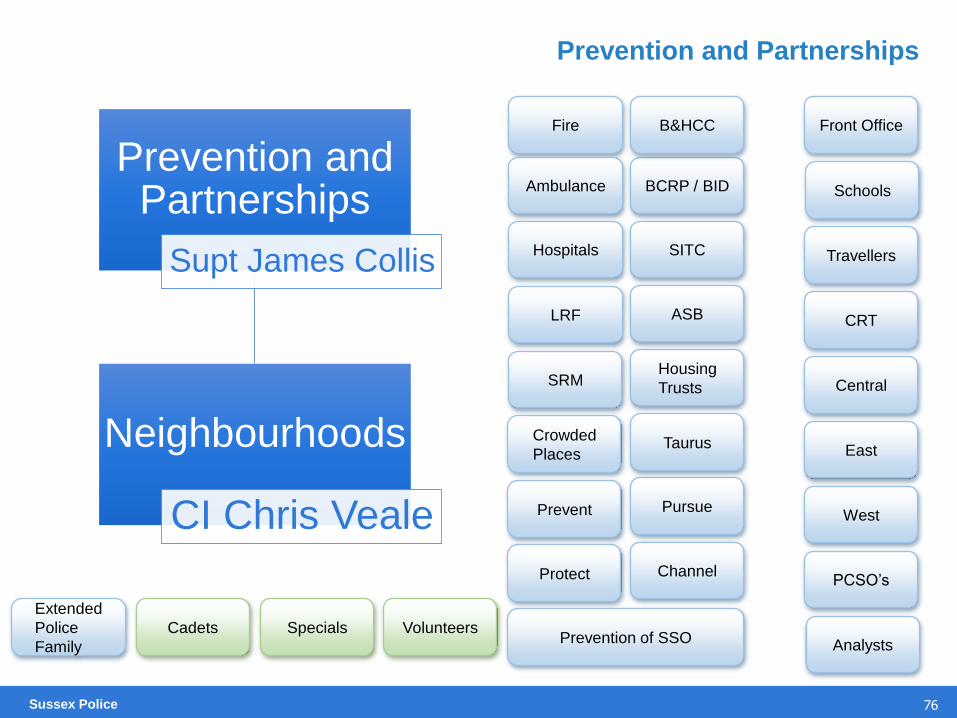

76 Sussex Police

Prevention and Partnerships

Prevention and Partnerships

Supt James Collis

Neighbourhoods

CI Chris Veale

Fire

BCRP / BID Ambulance

Hospitals

B&HCC

Housing

Trusts

LRF

Extended

Police

Family

Volunteers Specials Cadets

SRM

Prevent Pursue

Protect Channel

Taurus Crowded

Places

SITC

Front Office

ASB

Schools

CRT

Analysts

West

East

Central

Travellers

Prevention of SSO

PCSO’s

77 Sussex Police

Key priorities and challenges

Delivering an affordable resilient model of local

policing within a strong partnership framework

Providing an emergency service

Catching criminals

Protecting vulnerable people

Continuing to develop a policing response

aimed at minimising crime and disorder

Working in an environment of political uncertainty,

balancing right to peaceful protest against

disproportionate disruption to the city

A thriving nightime economy v Friday night disorder

78 Sussex Police

Key priorities and challenges

Development of sustainable multiagency

approaches to complex problems

Rough Sleeping and Street Community

ASB

Overt drug use in public places

Management of expectations and multiagency

approaches to:

Reducing of the statutory footprint in the communities

Promoting self-sufficiency through improving

communications throughout the whole system

Setting the tone for the city

79 Sussex Police

Questions

Any Questions ?