business interruption

DESCRIPTION

Business Interruption for InsuranceTRANSCRIPT

BUSINESS INTERRUPTION

Why purchasea Business Interruption Policy?

To protect _______ in the event of an Insured Loss

Business Interruption

?

Reference : Charles Taylor

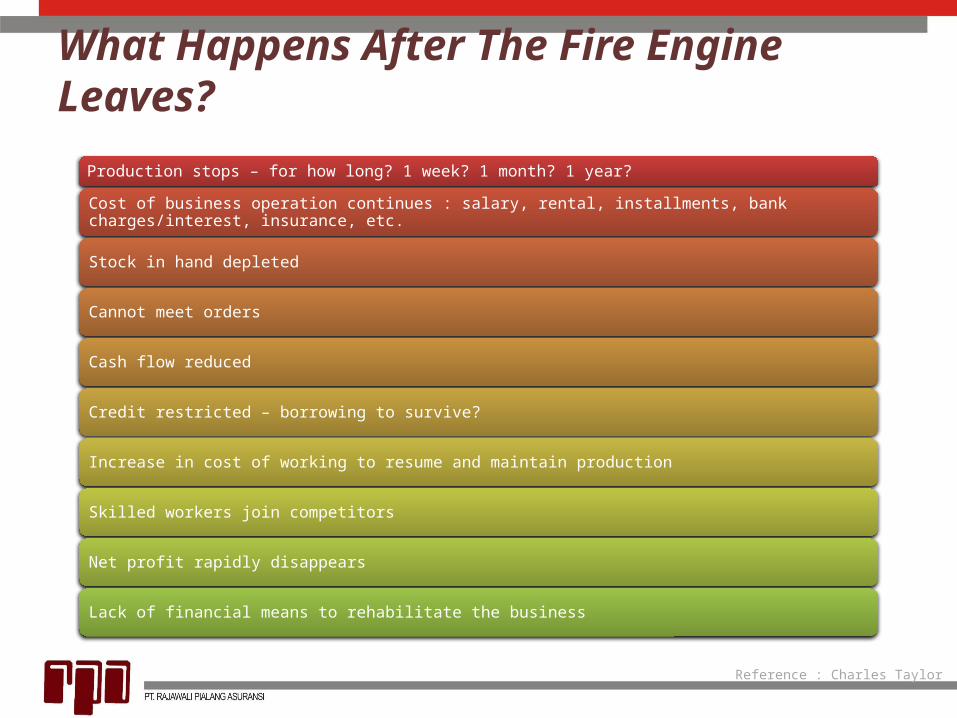

What Happens After The Fire Engine Leaves?

Reference : Charles Taylor

Production stops – for how long? 1 week? 1 month? 1 year?

Cost of business operation continues : salary, rental, installments, bank charges/interest, insurance, etc.

Stock in hand depleted

Cannot meet orders

Cash flow reduced

Credit restricted – borrowing to survive?

Increase in cost of working to resume and maintain production

Skilled workers join competitors

Net profit rapidly disappears

Lack of financial means to rehabilitate the business

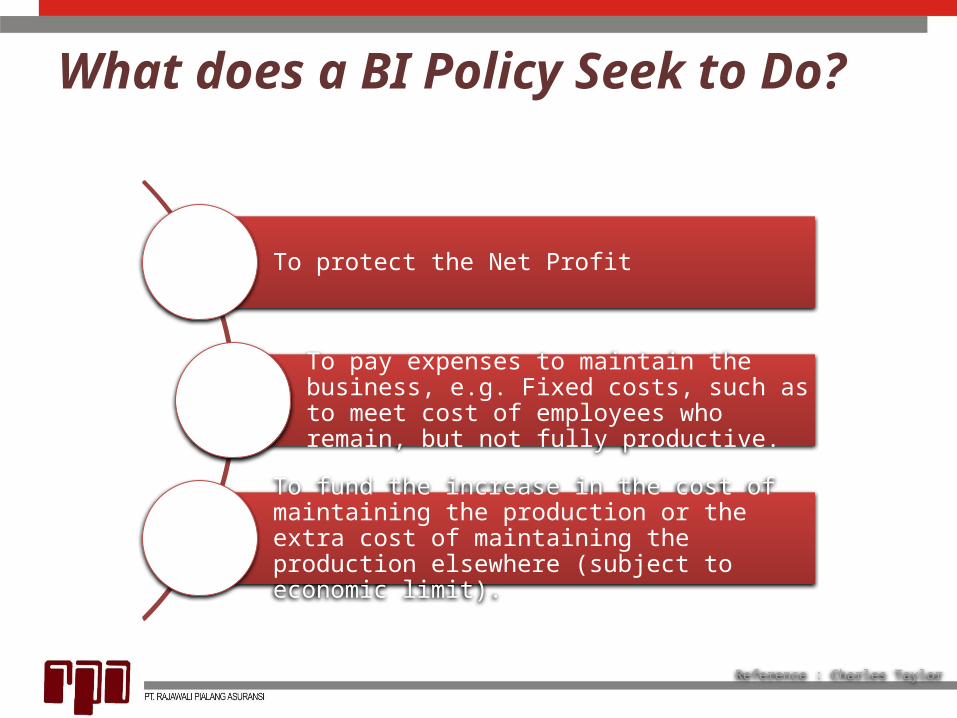

What does a BI Policy Seek to Do?

Reference : Charles Taylor

To protect the Net Profit

To pay expenses to maintain the business, e.g. Fixed costs, such as to meet cost of employees who remain, but not fully productive.

To fund the increase in the cost of maintaining the production or the extra cost of maintaining the production elsewhere (subject to economic limit).

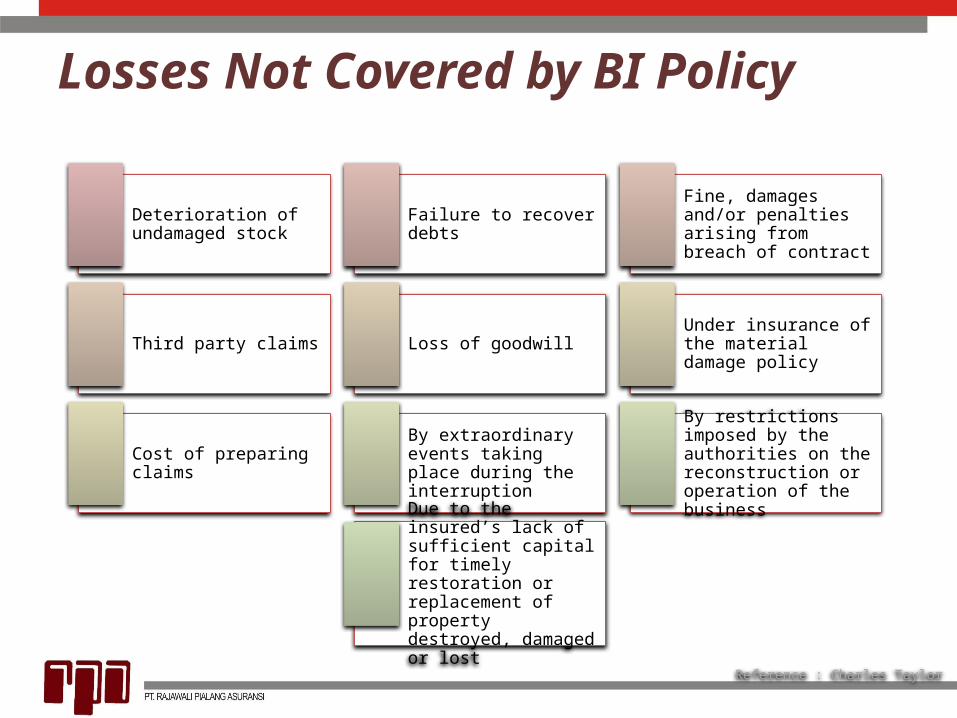

Losses Not Covered by BI Policy

Reference : Charles Taylor

Deterioration of undamaged stock

Failure to recover debts

Fine, damages and/or penalties arising from breach of contract

Third party claims Loss of goodwillUnder insurance of the material damage policy

Cost of preparing claims

By extraordinary events taking place during the interruption

By restrictions imposed by the authorities on the reconstruction or operation of the business

Due to the insured’s lack of sufficient capital for timely restoration or replacement of property destroyed, damaged or lost

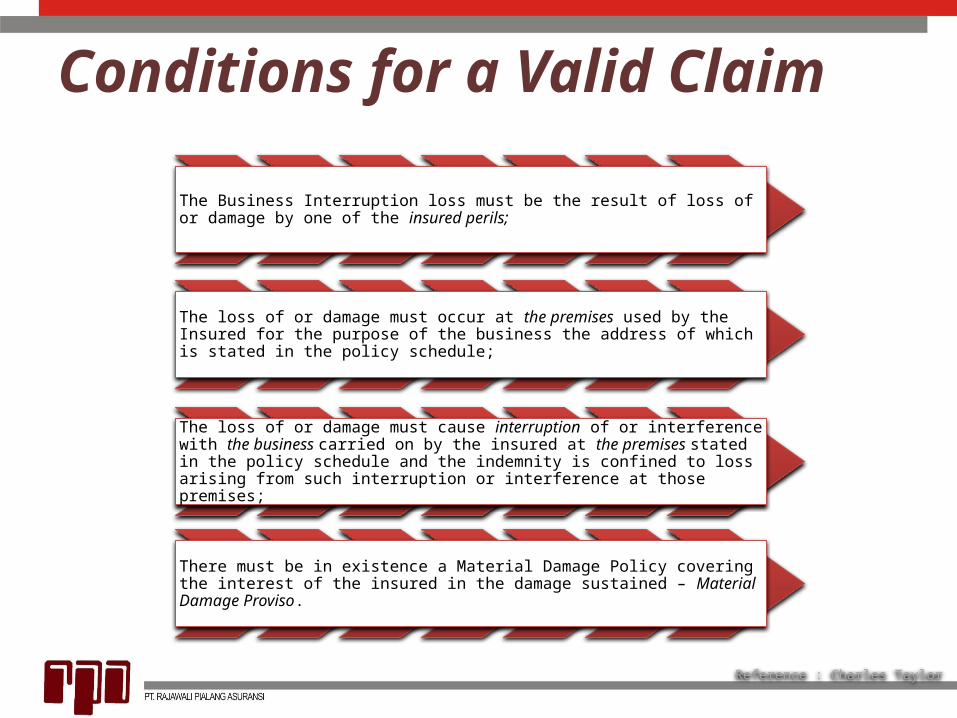

Conditions for a Valid Claim

Reference : Charles Taylor

The Business Interruption loss must be the result of loss of or damage by one of the insured perils;

The loss of or damage must occur at the premises used by the Insured for the purpose of the business the address of which is stated in the policy schedule;

The loss of or damage must cause interruption of or interference with the business carried on by the insured at the premises stated in the policy schedule and the indemnity is confined to loss arising from such interruption or interference at those premises;

There must be in existence a Material Damage Policy covering the interest of the insured in the damage sustained – Material Damage Proviso.

The money paid or payable to the Insured for goods sold and delivered and for services rendered in course of the Business at the Premises.Also known as : Sales Income Receipts takings Revenues Fees Royalties etc.

What is TURNOVER?

Reference : Charles Taylor

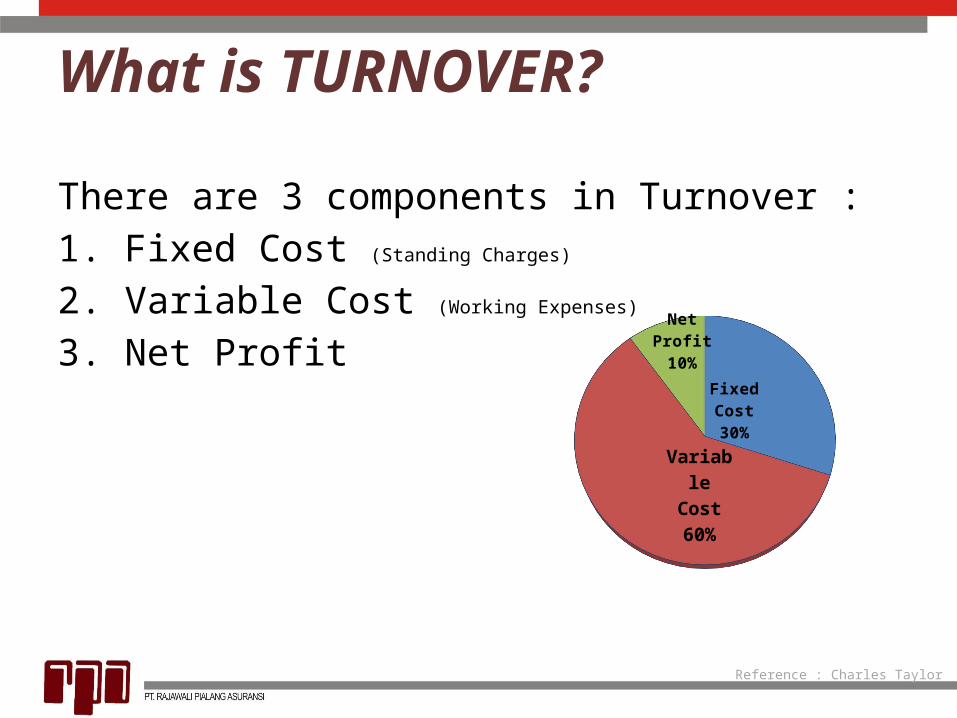

There are 3 components in Turnover :1. Fixed Cost (Standing Charges)

2. Variable Cost (Working Expenses)

3. Net Profit

What is TURNOVER?

Reference : Charles Taylor

Fixed Cost30%

Variable Cost60%

NetProfit10%

What is TURNOVER?

Reference : Charles Taylor

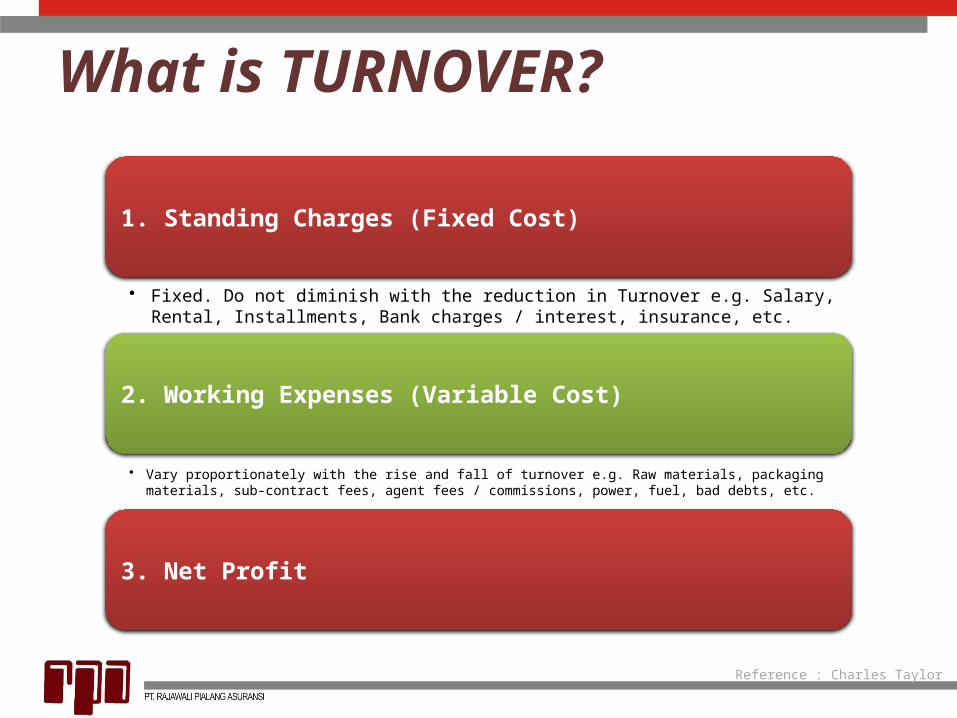

1. Standing Charges (Fixed Cost)

• Fixed. Do not diminish with the reduction in Turnover e.g. Salary, Rental, Installments, Bank charges / interest, insurance, etc.

2. Working Expenses (Variable Cost)

• Vary proportionately with the rise and fall of turnover e.g. Raw materials, packaging materials, sub-contract fees, agent fees / commissions, power, fuel, bad debts, etc.

3. Net Profit

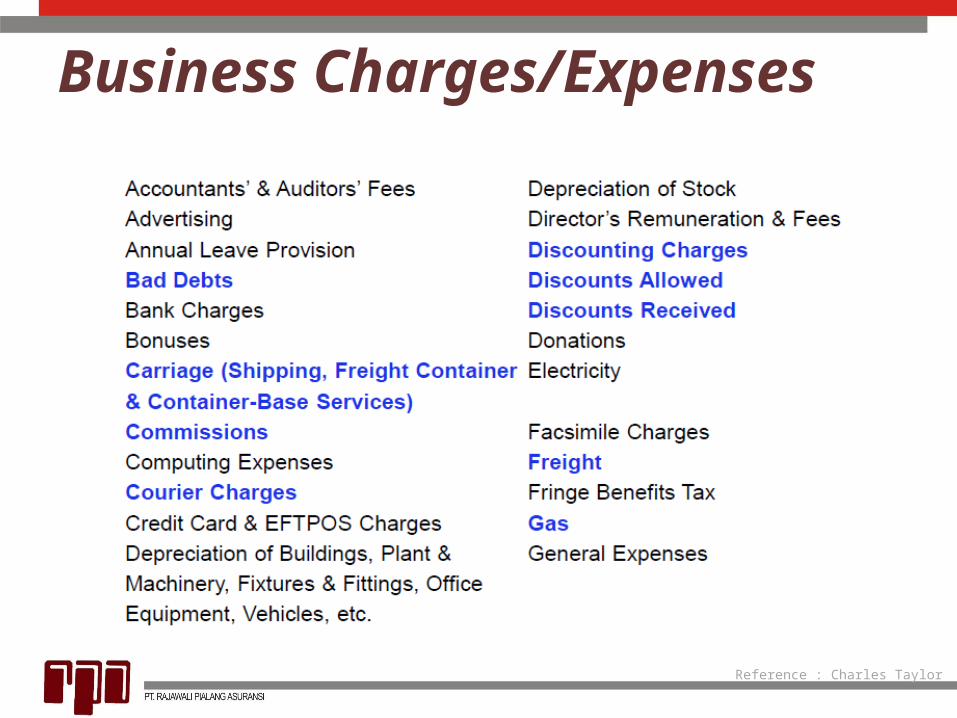

Business Charges/Expenses

Reference : Charles Taylor

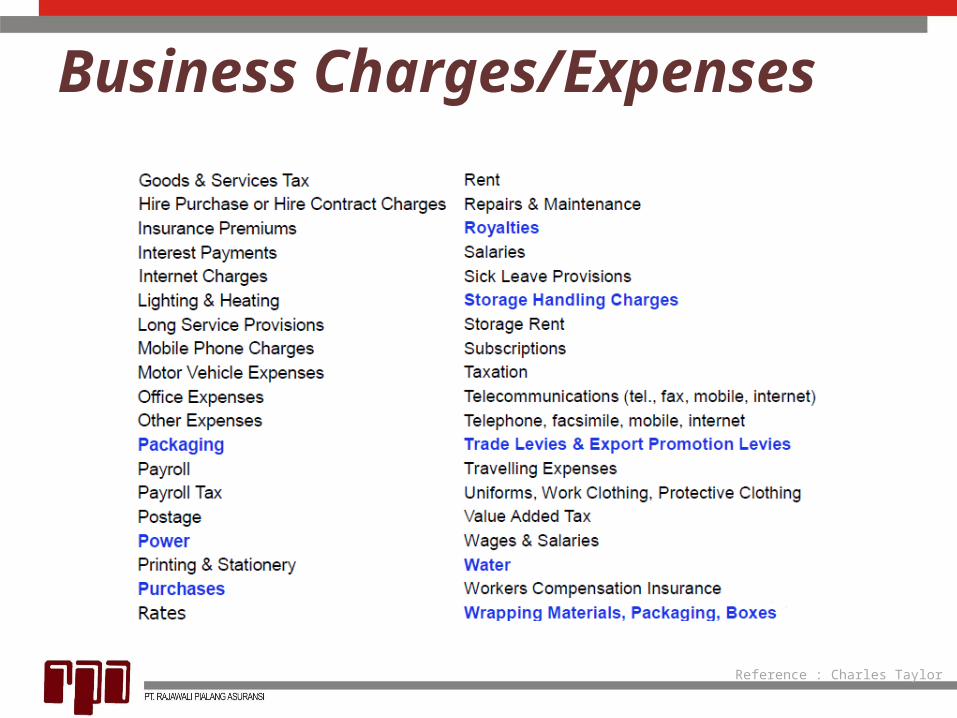

Business Charges/Expenses

Reference : Charles Taylor

The Period of Insurance

Reference : Charles Taylor

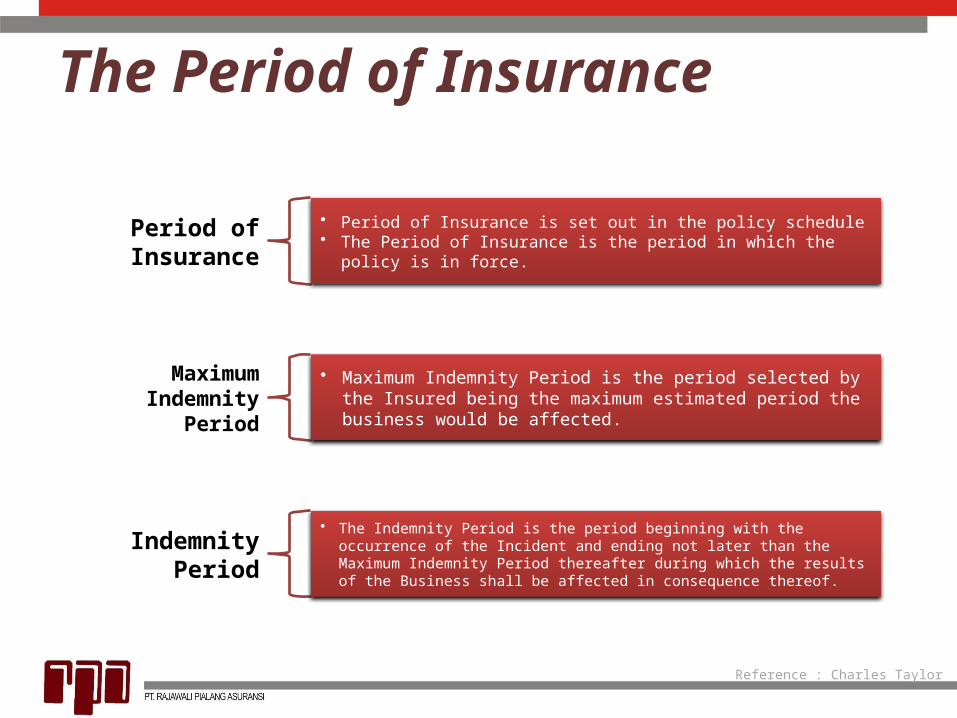

Period of Insurance

• Period of Insurance is set out in the policy schedule• The Period of Insurance is the period in which the

policy is in force.

Maximum Indemnity

Period

• Maximum Indemnity Period is the period selected by the Insured being the maximum estimated period the business would be affected.

Indemnity Period

• The Indemnity Period is the period beginning with the occurrence of the Incident and ending not later than the Maximum Indemnity Period thereafter during which the results of the Business shall be affected in consequence thereof.

Maximum Indemnity Period

Reference : Charles Taylor

Factors for consideration : Availability of alternative premises; The estimated period of repairs/reconstruction; The availability of raw materials; The lead time in the replacement of machinery; The availability of manufacturing the product by

sub-contractors; The estimated time required to ‘recover’

customers; Whether business is seasonal.

The Indemnity Period

Reference : Charles Taylor

Why it has to be adequate?

If the indemnity period chosen is insufficient, the Insured have to bear. All loss after the Maximum Indemnity Period. All ICW which achieved benefit after the

maximum indemnity period.

Maximum Indemnity Period

Reference : Charles Taylor

The maximum Indemnity Period should be sufficient to allow for : Clearance of site Preparation of plans and drawings Obtaining local authority permits and obtaining tenders Erection/construction Obtaining raw materials and installing machinery and

equipment (check lead time for special machines) Recruiting and training new staff, if necessary Regaining lost customers after full production is restored

Material Damage Proviso

Reference : Charles Taylor

“Provided that at the time of the happening of the damage there shall be in force an insurance covering the interest of the insured in the property at the premises against such damage and that payment shall have been made or liability admitted therefor under such insurance”

To have a valid claim, the Insured must :1. Have a material damage policy insuring the loss of property, and2. They must be a liability under that policy.

Objectives :3. The Insured is in the financial position to resume/rehabilitate the

business.4. No necessity to insert warranties & no necessity to investigate the

loss.

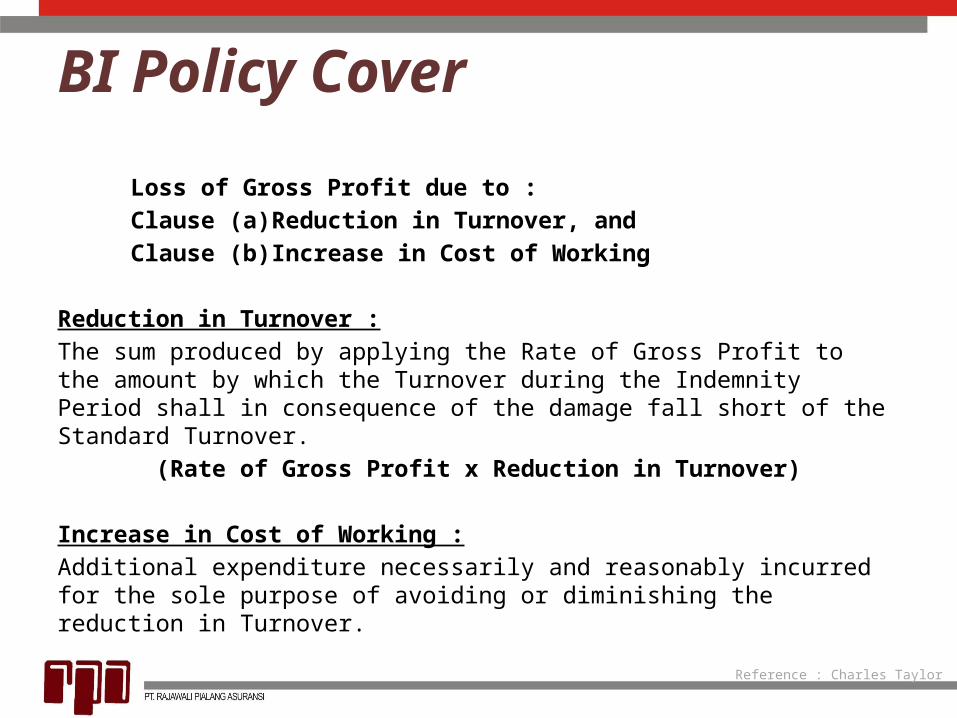

BI Policy Cover

Reference : Charles Taylor

Loss of Gross Profit due to :Clause (a) Reduction in Turnover, andClause (b) Increase in Cost of Working

Reduction in Turnover :The sum produced by applying the Rate of Gross Profit to the amount by which the Turnover during the Indemnity Period shall in consequence of the damage fall short of the Standard Turnover.

(Rate of Gross Profit x Reduction in Turnover)

Increase in Cost of Working :Additional expenditure necessarily and reasonably incurred for the sole purpose of avoiding or diminishing the reduction in Turnover.

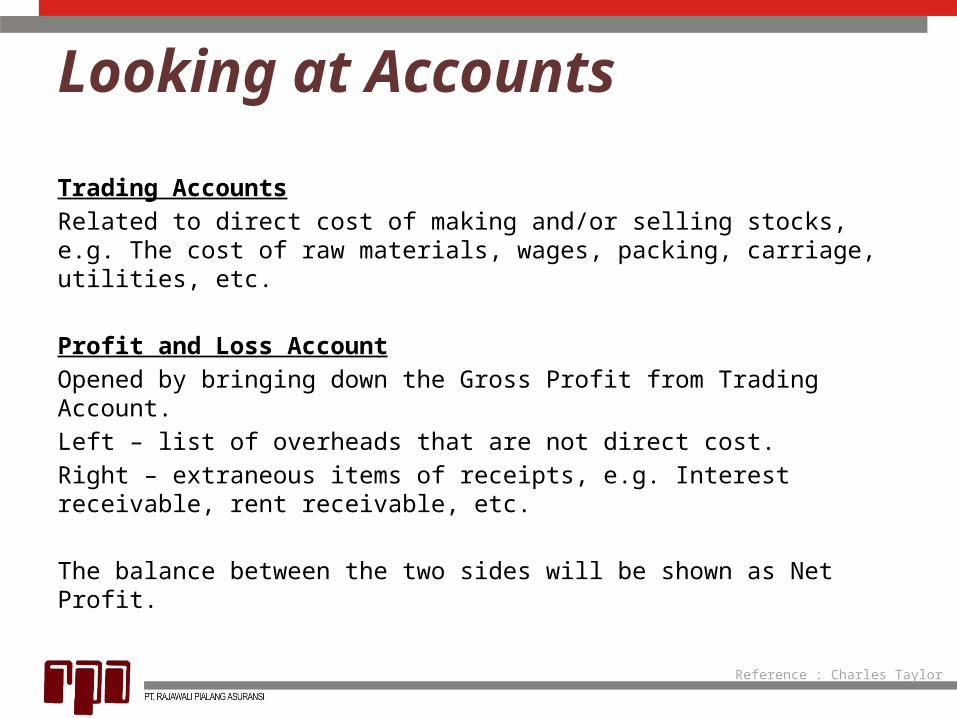

Looking at Accounts

Reference : Charles Taylor

Trading AccountsRelated to direct cost of making and/or selling stocks, e.g. The cost of raw materials, wages, packing, carriage, utilities, etc.

Profit and Loss AccountOpened by bringing down the Gross Profit from Trading Account.Left – list of overheads that are not direct cost.Right – extraneous items of receipts, e.g. Interest receivable, rent receivable, etc.

The balance between the two sides will be shown as Net Profit.

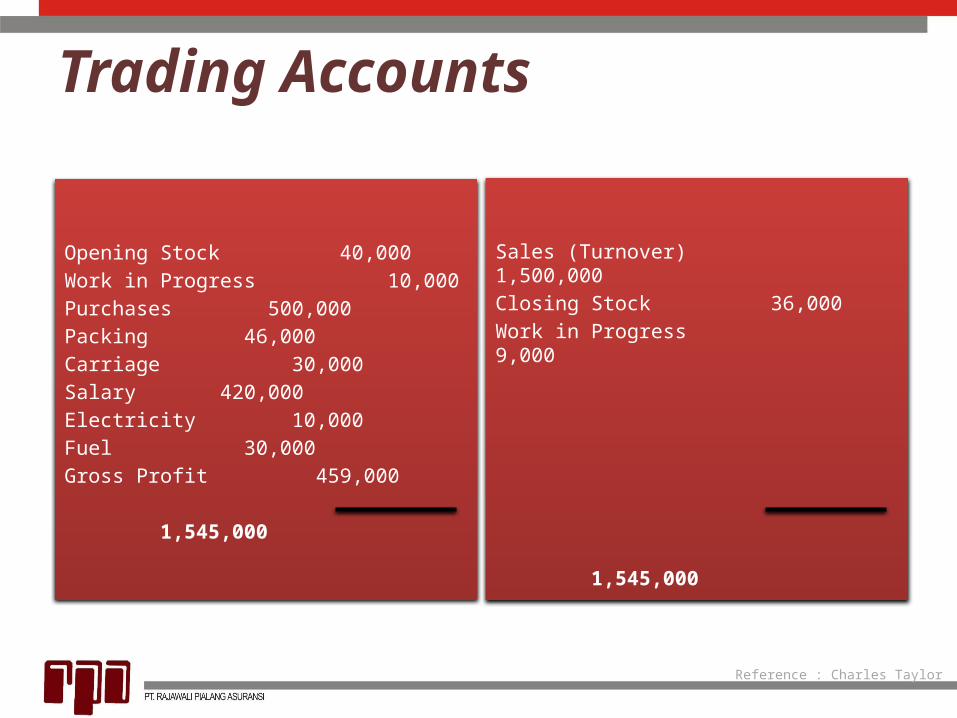

Opening Stock 40,000Work in Progress 10,000Purchases 500,000Packing 46,000Carriage 30,000Salary 420,000Electricity 10,000Fuel 30,000Gross Profit 459,000

1,545,000

Sales (Turnover) 1,500,000Closing Stock 36,000Work in Progress 9,000

1,545,000

Reference : Charles Taylor

Trading Accounts

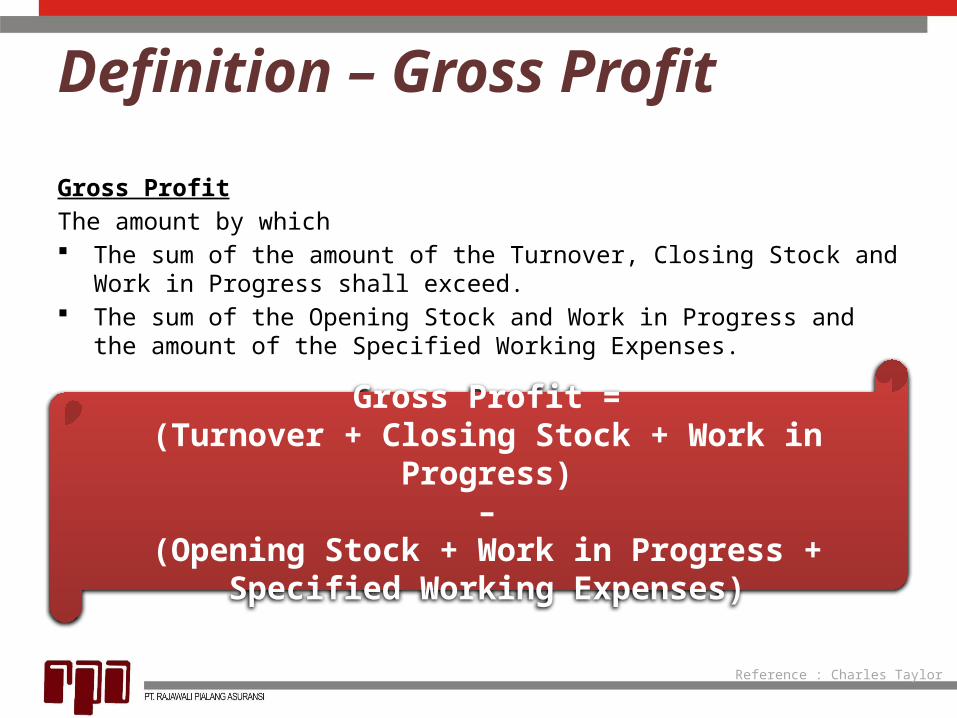

Definition – Gross Profit

Reference : Charles Taylor

Gross ProfitThe amount by which The sum of the amount of the Turnover, Closing Stock and Work in

Progress shall exceed. The sum of the Opening Stock and Work in Progress and the

amount of the Specified Working Expenses.

Gross Profit =(Turnover + Closing Stock + Work in

Progress)–

(Opening Stock + Work in Progress + Specified Working Expenses)

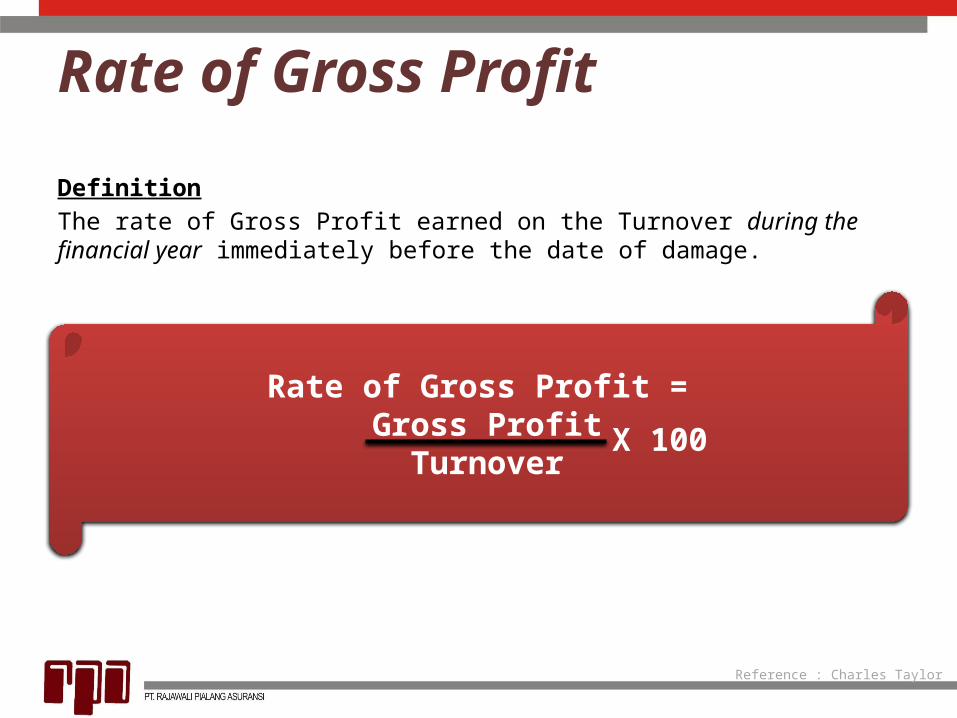

Rate of Gross Profit

Reference : Charles Taylor

DefinitionThe rate of Gross Profit earned on the Turnover during the financial year immediately before the date of damage.

Rate of Gross Profit = Gross Profit

TurnoverX

100

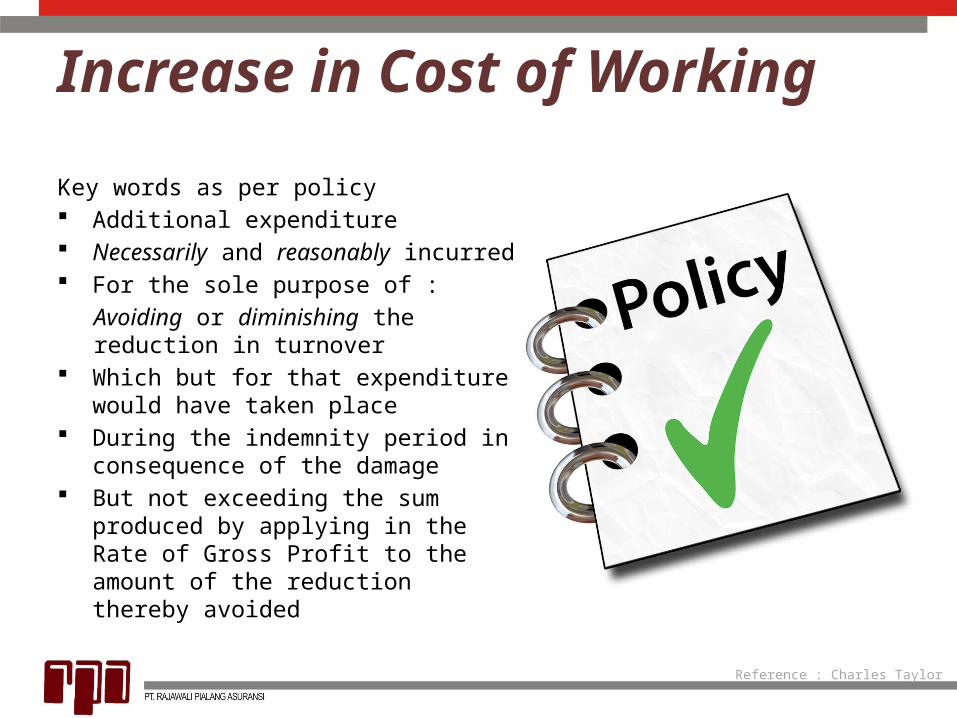

Increase in Cost of Working

Reference : Charles Taylor

Key words as per policy Additional expenditure Necessarily and reasonably

incurred For the sole purpose of :

Avoiding or diminishing the reduction in turnover

Which but for that expenditure would have taken place

During the indemnity period in consequence of the damage

But not exceeding the sum produced by applying in the Rate of Gross Profit to the amount of the reduction thereby avoided

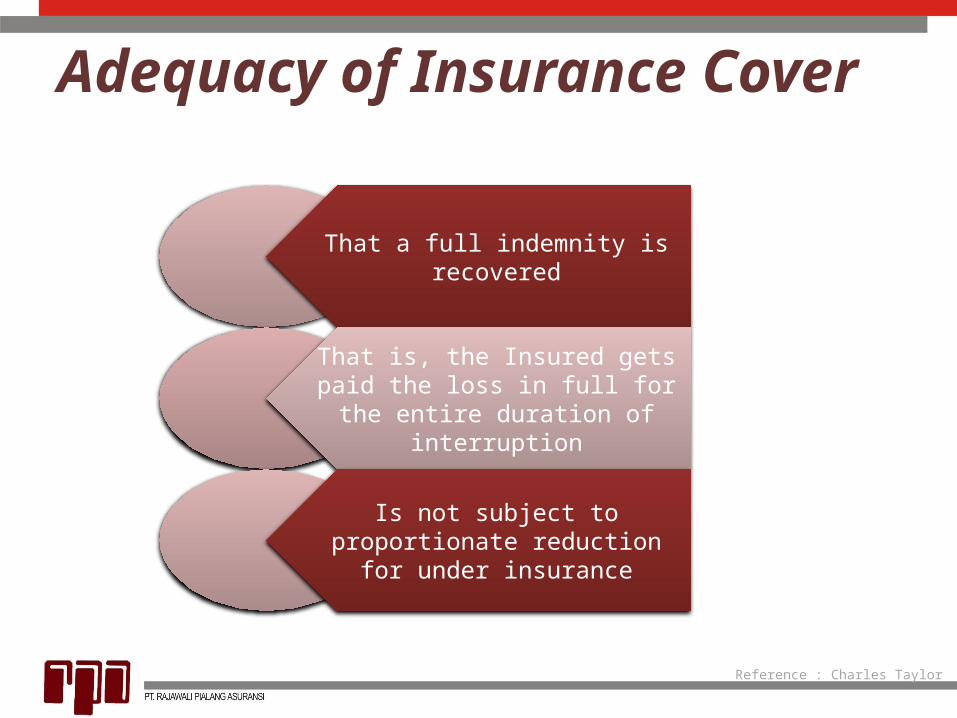

Adequacy of Insurance Cover

Reference : Charles Taylor

That a full indemnity is recovered

That is, the Insured gets paid the loss in full for the entire

duration of interruption

Is not subject to proportionate reduction for under insurance

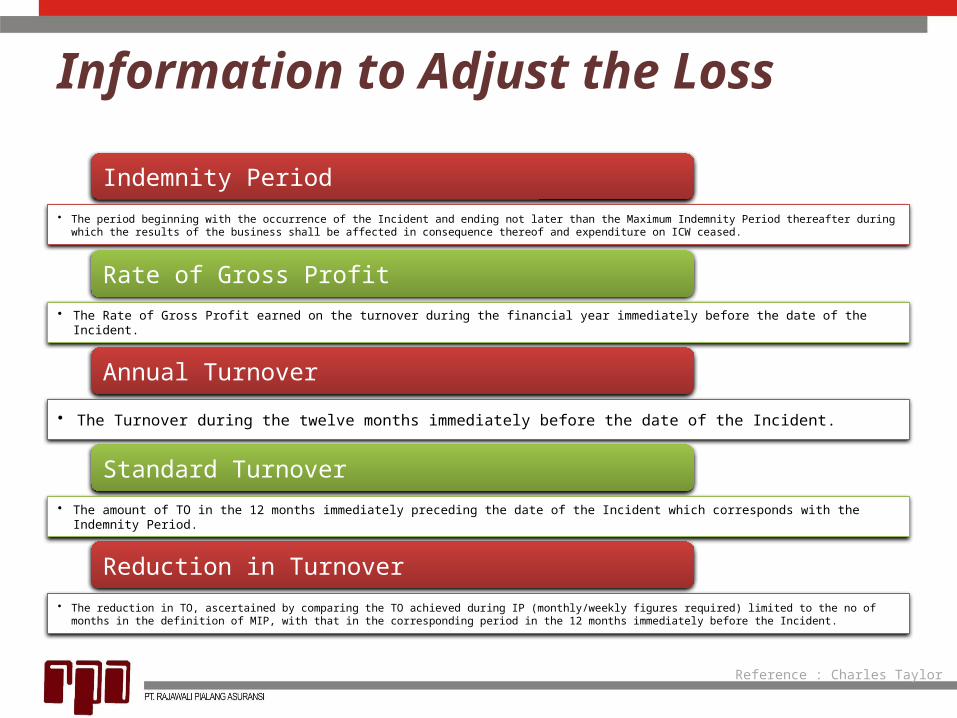

Information to Adjust the Loss

Reference : Charles Taylor

Indemnity Period• The period beginning with the occurrence of the Incident and ending not later than the Maximum Indemnity Period thereafter during

which the results of the business shall be affected in consequence thereof and expenditure on ICW ceased.

Rate of Gross Profit

• The Rate of Gross Profit earned on the turnover during the financial year immediately before the date of the Incident.

Annual Turnover

• The Turnover during the twelve months immediately before the date of the Incident.

Standard Turnover

• The amount of TO in the 12 months immediately preceding the date of the Incident which corresponds with the Indemnity Period.

Reduction in Turnover• The reduction in TO, ascertained by comparing the TO achieved during IP (monthly/weekly figures required) limited to the no of

months in the definition of MIP, with that in the corresponding period in the 12 months immediately before the Incident.

Information to Adjust the Loss

Reference : Charles Taylor

Increase Cost of Working

• Details of all additional/abnormal expenditure incurred to minimize the interference in the business.

Residual Value

• Residual value – Details of any property included in ICW above as additional expenditure which remains of some use after the end of IP and residual value of same.

Savings

• Any sum saved during the Indemnity Period in respect of such of the charges and expenses of the Business payable out of Gross Profit as may cease or be reduced in consequence of the Incident.

Other Circumstances

• Any grounds for adjustment as may be necessary to provide for the trend of the Business for variations in or other circumstances affecting the Business either before or after the Incident or which would have affected the Business had the Incident not occurred, so that the figures thus adjusted shall represent as nearly as may be reasonably practicable the results which but for the Incident would have been obtained during the period after the Incident.

1. Copies of the annual audited accounts for the preceding 3 years

2. Copies of detailed manufacturing, TPL accounts for the past 3 financial years

3. Monthly/weekly TO figures for the 24 months period prior the loss

4. Monthly/weekly TO figures during IP

5. Details of additional expenditure including supporting documents and explanation why the expense is considered to be an ICW expense and why the cost was incurred

6. Details of any savings in standing charges or expenses payable out of GP

7. Supporting documents, e.g. Income tax return, sales tax return, etc.

8. Details of major customers’ orders and an analysis of their orders.

9. Details of those customers’ orders during IP

10. Confirmation of the basis of valuation of stocks in the accounts has not changed.

11. Copies of Income Tax returns for the 24 months period before the fire and during IP (this will give official confirmation to the TO figures being used for the purpose of the claim)

Reference : Charles Taylor

Claim Documents