business systems - creating & maintaining order - jennifer lemcke, weed man usa

TRANSCRIPT

1

SYSTEMSGETTING BACK TO BASICS

THE BUSINESS

DEFINING YOUR BUSINESS

Where are you in the business cycle?

Infancy Stage

Adolescent Stage

Mature Business

THE BUSINESS

INFANCY STAGE

You are in the growth stage of thebusiness. Most companies that findthemselves in this stage are owneroperated and the owner is wearing allthe hats in the company!

2

THE BUSINESS

ADOLESCENT STAGE

You are still in the growth stage of thebusiness but the owner identifies the needfor help. Often occurs during crisis. Tomove beyond this stage you need to makesure you get the right people and developthe right environment for continued growth.

THE BUSINESS

MATURE BUSINESS

The third phase of a business cycle.Not all companies arrive at this stage,but the great ones that do have anowner that has vision, culture, benchstrength and passion.

THE BUSINESSHOW DO YOU TRANSITIONS FROM

INFANCY STAGE TO ADOLESCENT STAGE?

• Create Solid Business Plans• Build Procedural Type Systems• Develop Training Programs• Develop Measurement Tools• Create a Culture of Accountability• Develop Good Bench Strength• Manage Your Biggest Asset – Your People!• Lead With Passion!

3

SYSTEMS

SYSTEMIZING YOUR BUSINESS HAS THEPOWER TO DRAMATICALLY TRANSFORMANY BUSINESS FROM A CONDITION OFCHAOS TO A CONDITION OF ORDER.

WHY DO SOME PEOPLE FIGHT IT!

4

BENEFITS OF BUDGETING

• Better use of capital

• Efficient operations

• Spending control

• Identification of opportunities

• Measurement of progress

• Establishment of company goals

• Establishment of employee goals

• Many other benefits

BENEFITS OF ZERO BASEDBUDGETING

• More involved

• Managers start from a ‘clean slate’ or ‘from scratch’ each year

• Managers must justify the costs of creating and sustainingcarefully defined revenue streams

• Driven to root out waste and find cost-effective ways toimprove operations

• Combines planning and budgeting into a single process

• Expands management participation in ways that increaseresponsibility, communication and coordination

5

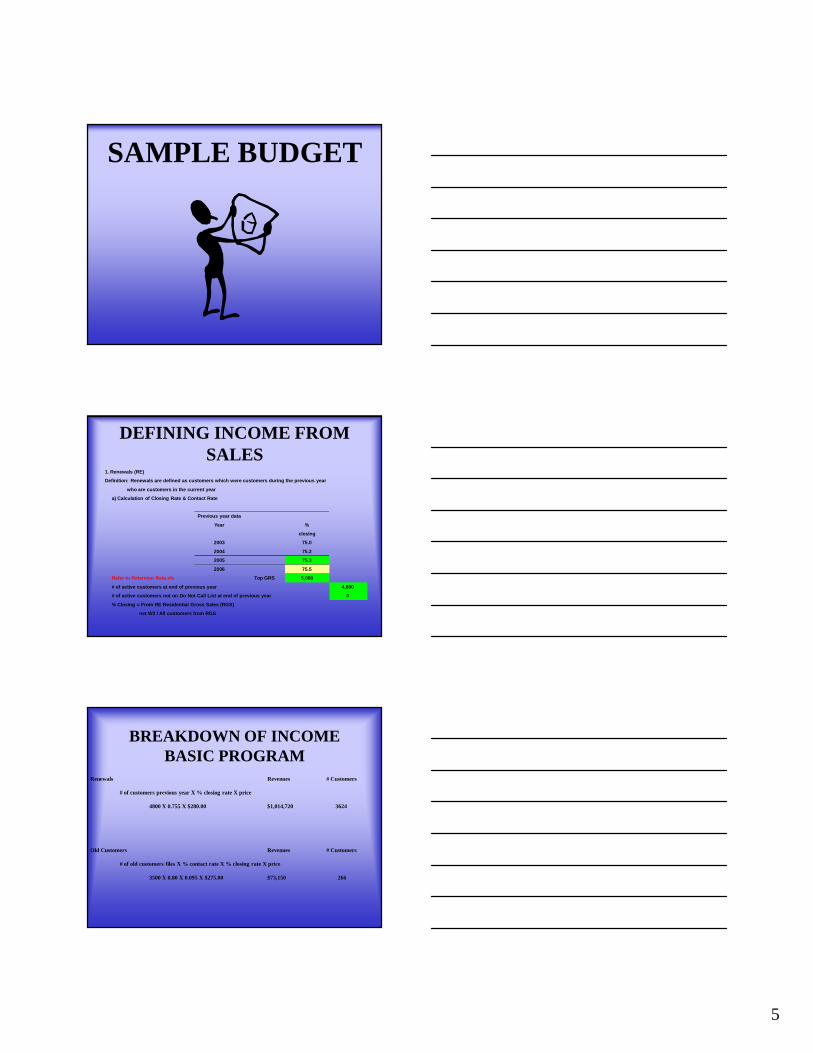

SAMPLE BUDGET

DEFINING INCOME FROMSALES

1. Renewals (RE)

Definition: Renewals are defined as customers which were customers during the previous year

who are customers in the current year

a) Calculation of Closing Rate & Contact Rate

Previous year data

Year %

closing

2003 75.0

2004 75.2

2005 75.3

2006 75.5

Refer to Retention Rate.xls Top GRS 5,000

# of active customers at end of previous year 4,800

# of active customers not on Do Not Call List at end of previous year 0

% Closing = From RE Residential Gross Sales (RGS)

net W2 / All customers from RGS

BREAKDOWN OF INCOMEBASIC PROGRAM

Renewals Revenues # Customers

# of customers previous year X % closing rate X price

4800 X 0.755 X $280.00 $1,014,720 3624

Old Customers Revenues # Customers

# of old customers files X % contact rate X % closing rate X price

3500 X 0.80 X 0.095 X $275.00 $73,150 266

6

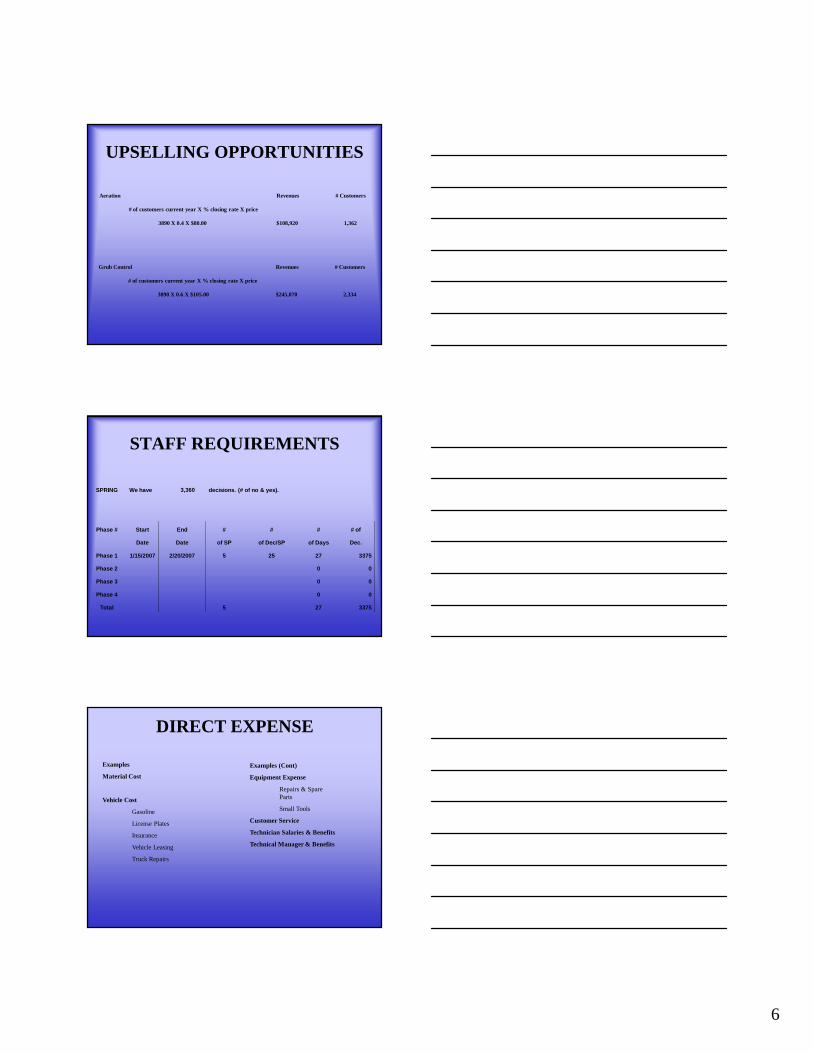

UPSELLING OPPORTUNITIES

Aeration Revenues # Customers

# of customers current year X % closing rate X price

3890 X 0.4 X $80.00 $108,920 1,362

Grub Control Revenues # Customers

# of customers current year X % closing rate X price

3890 X 0.6 X $105.00 $245,070 2,334

STAFF REQUIREMENTS

SPRING We have 3,360 decisions. (# of no & yes).

Phase # Start End # # # # of

Date Date of SP of Dec/SP of Days Dec.

Phase 1 1/15/2007 2/20/2007 5 25 27 3375

Phase 2 0 0

Phase 3 0 0

Phase 4 0 0

Total 5 27 3375

DIRECT EXPENSE

Examples

Material Cost

Vehicle Cost

Gasoline

License Plates

Insurance

Vehicle Leasing

Truck Repairs

Examples (Cont)

Equipment Expense

Repairs & SpareParts

Small Tools

Customer Service

Technician Salaries & Benefits

Technical Manager & Benefits

7

ADMINISTRATIVE EXPENSEExamples

Office supplies

Envelopes

Postage

Computer Paper

Ink Cartridge

Computer

Invoices

Office Maintenance

Office Equipment

Rentals

Repairs

Examples (Cont)

Office Rent

Rent

Utilities

Business Tax

Garbage & Others

Business Permits

Telephone

Installation

Monthly cost

Office Staff Salaries & Benefits

General Manager Salary & Benefits

SELLING EXPENSE

Examples

Promotion & Advertising

Radio & Television

Fact Sheets

Lawn Flags

Door Hangers

Yellow Pages

Promotional Gifts

Examples (Cont)

Direct Marketing

Salaries

Rent

Telephone

Sales Manager

BUSINESS PLANNINGDESCRIPTION TOTAL NOV DEC JAN FEB MAR

CASH INFLOW

COL. OF REC. PR. YR. 58,238 23,087 9,734 5,183 8,317 3,970

COL. OF REC. & PREPAIDS CUR. YR. 707,989 20,000 10,000 5,633 23,723 76,709

COL. OF PREPAIDS NEXT YR. 156,571

SERVICE CHARGES 8,317 700 700 1,138 220 826

INTEREST ON DEPOSIT - - - - - -

BANK LOAN - -

ADVANCE FROM PARENT (115,000) - - (40,000) -

TOTAL CASH INFLOW 816,115 43,787 20,434 (28,046) 32,260 81,505

CASH OUTFLOW

-

PMT OF LONG TERM DEBT 10,920 910 910 910 910 910

DIRECT EXPENSES 367,375 1,986 1,986 1,986 13,392 13,464

ADMINISTRATIVE EXPENSES 234,472 14,672 16,001 20,631 17,251 28,198

SELLING EXPENSES 149,750 3,167 2,140 5,458 13,899 26,569

FINANCIAL EXPENSES 3,096 258 258 258 258 258

CASH FLOWPROJECTIONS

8

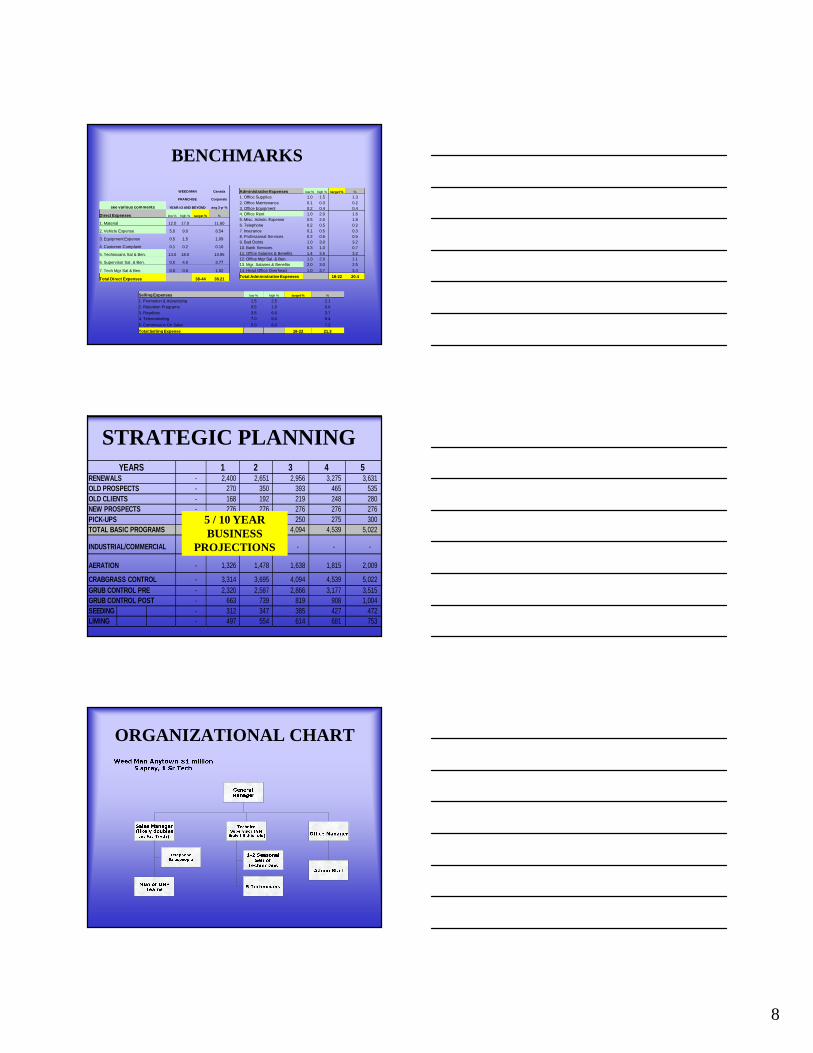

BENCHMARKS

WEED MAN Canada

FRANCHISE Corporate

see various comments YEAR #3 AND BEYOND avg 3 yr %

Direct Expenses low % high % target % %

1. Material 12.0 17.0 11.60

2. Vehicle Expense 5.0 9.0 8.54

3. Equipment Expense 0.5 1.5 1.09

4. Customer Complaint 0.1 0.2 0.10

5. Technicians Sal & Ben. 14.0 18.0 13.95

6. Supervisor Sal. & Ben. 0.0 4.0 3.77

7. Tech Mgr Sal & Ben. 0.0 0.0 1.92

Total Direct Expenses 38-44 38.21

AdministrativeExpenses low % high % target % %

1. Office Supplies 1.0 1.5 1.3

2. Office Maintenance 0.1 0.3 0.2

3. Office Equipment 0.2 0.4 0.4

4. Office Rent 1.0 2.0 1.6

5. Misc. Admin. Expense 0.5 2.0 1.8

6. Telephone 0.2 0.5 0.2

7. Insurance 0.1 0.5 0.3

8. Professional Services 0.2 0.6 0.5

9. Bad Debts 1.0 3.0 3.2

10. Bank Services 0.3 1.0 0.7

11. Office Salaries & Benefits 1.4 3.5 3.2

12. Office Mgr Sal. & Ben. 1.0 2.0 1.1

13. Mgr. Salaries & Benefits 2.0 3.0 2.5

14. Head Office Overhead 1.0 3.7 3.4

Total AdministrativeExpenses 18-22 20.4

Selling Expenses low % high % target % %

1. Promotion & Advertising 1.5 2.5 2.1

2. Retention Programs 0.5 1.0 0.0

3. Royalties 3.5 6.0 3.7

4. Telemarketing 7.0 9.0 8.4

5. Commission On Sales 5.0 8.0 7.2

Total Selling Expense 18-22 21.3

STRATEGIC PLANNINGYEARS 1 2 3 4 5

RENEWALS - 2,400 2,651 2,956 3,275 3,631

OLD PROSPECTS - 270 350 393 465 535

OLD CLIENTS - 168 192 219 248 280

NEW PROSPECTS - 276 276 276 276 276

PICK-UPS - 200 225 250 275 300

TOTAL BASIC PROGRAMS 3,000 3,314 3,695 4,094 4,539 5,022

INDUSTRIAL/COMMERCIAL - - - - - -

AERATION - 1,326 1,478 1,638 1,815 2,009

CRABGRASS CONTROL - 3,314 3,695 4,094 4,539 5,022

GRUB CONTROL PRE - 2,320 2,587 2,866 3,177 3,515

GRUB CONTROL POST - 663 739 819 908 1,004

SEEDING - 312 347 385 427 472

LIMING - 497 554 614 681 753

5 / 10 YEARBUSINESS

PROJECTIONS

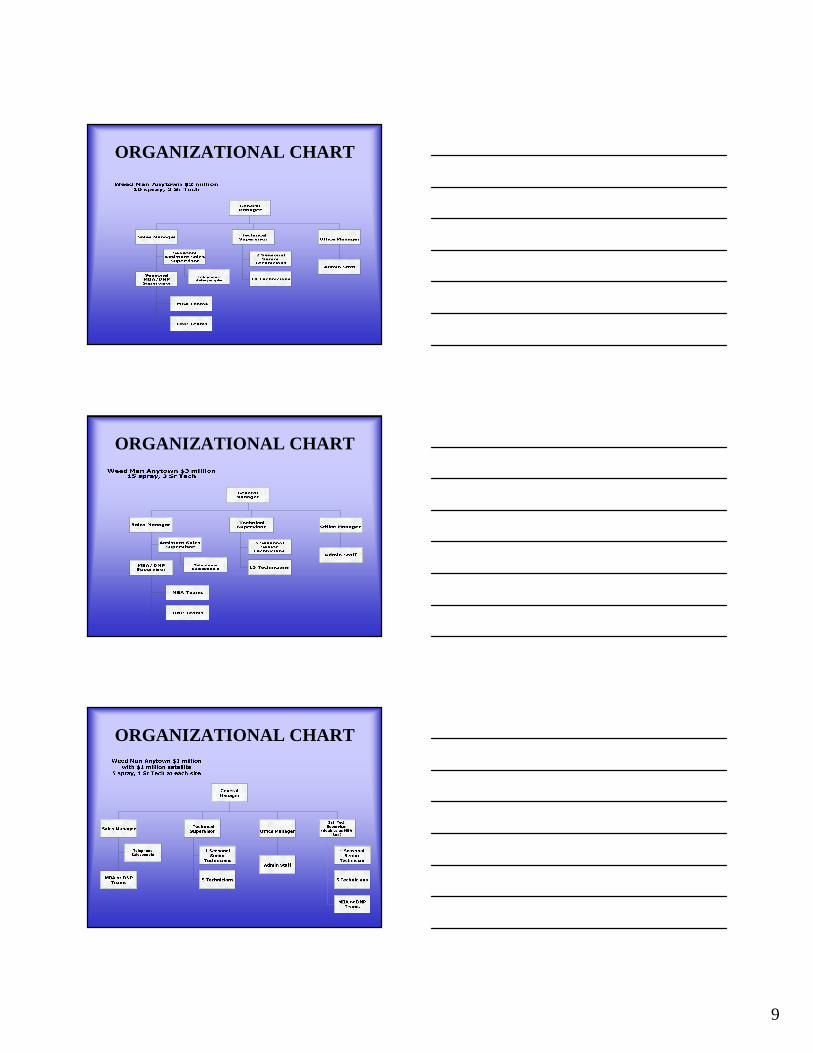

ORGANIZATIONAL CHART

9

ORGANIZATIONAL CHART

ORGANIZATIONAL CHART

ORGANIZATIONAL CHART

10

BUSINESS PLANNING

WHO SHOULD BE INVOLVED?

HOW LONG SHOULD IT TAKE?

WHERE SHOULD IT BE DONE?

HOW DO YOU EXECUTE THEBUSINESS PLAN!

11

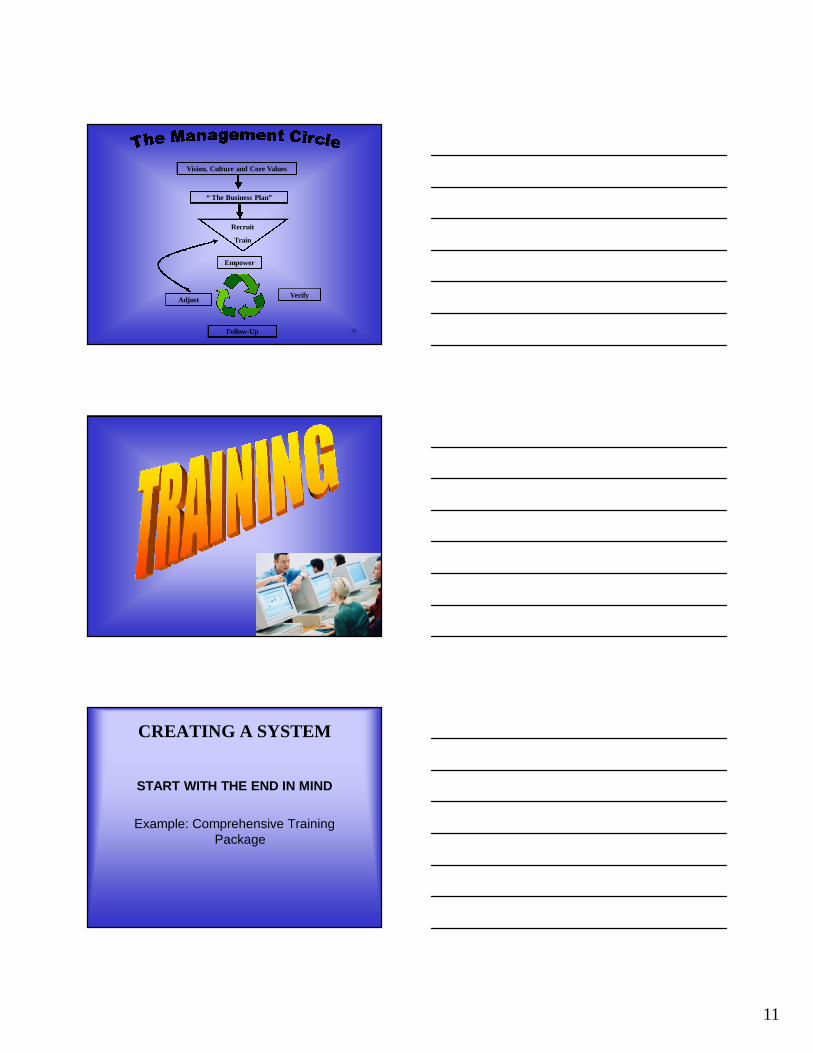

Vision, Culture and Core Values

“ The Business Plan”

Recruit

Train

Empower

Verify

Follow-Up

Adjust

31

CREATING A SYSTEM

START WITH THE END IN MIND

Example: Comprehensive TrainingPackage

12

CREATING A SYSTEM

Training Tools

Power Point Presentation

Manuals

Props (ie. Spreader)

Product Sample

Checklist for in field training

Videos

Outside Vendors

CREATING A SYSTEM

Training Content

Customer Service

Technical

Company Policies

Expectations/Benchmarks

Define Measurement Tools

Set Expectations for Follow Up

SALES POWER-POINT PRESENTATION

ATTI TUDES FOR SUCCESSTHE MAI N TYPES OF

CUSTOMERS

1)1) THE THINKERTHE THINKER

THE PRESENTATION

OBJECTI ONS

Why customersraiseobjections:

1. They donot like thesalesperson

2. They donot trust thesalesperson

3. They donot like theproduct

4. They do not want to be pressured into buyingand want to believe that they make all thebuying decisions and are in total control of thesituation

CLOSING THE SALE

THINGSTO REMEMBER WHENTHINGSTO REMEMBER WHENCLOSINGCLOSING

1) BE REALISITIC1) BE REALISITIC

2) CLOSE WITH CONFIDENCE2) CLOSE WITH CONFIDENCE

3) EMOTIONSWILL MAKE OR BREAK3) EMOTIONSWILL MAKE OR BREAKTHE SALETHE SALE

4) DON’T PAY ATTENTION TO THE4) DON’T PAY ATTENTION TO THEFIRST “NO”FIRST “NO”

5) COMPLETE PAPERWORK PROPERLY5) COMPLETE PAPERWORK PROPERLY

SALES MANAGERSEXPECTATIONS

ON TIMEON TIME

ATTENDANCEATTENDANCE

RESPECTRESPECTCUSTOM ERCUSTOM ER

IMPROVE INIMPROVE INSALESSALESTECHNI QUESANDTECHNI QUESANDKNOWLEDGEKNOWLEDGE

NOT DEGRADENOT DEGRADECOMPETITIONCOMPETITION

NO SCRIBBLINGNO SCRIBBLINGON TABLESON TABLES

PAY BASED ONPAY BASED ONSALARY SCALESALARY SCALE

RESPECT YOURESPECT YOU

CONTINUEDCONTINUEDCOACHING ANDCOACHING ANDSUPPORTSUPPORT

TRAINING SUPPORT SYSTEMS

13

CREATING A SYSTEM

START WITH THE END IN MIND

Example: Completed and BalancedFinancials by the 6th of every month

CREATING A SYSTEM

START WITH THE END IN MIND

Defined what you need

– Create chart of accounts that is inline withyour budget

– Chose accounting software that allowsbudget comparisons

– Create specific reporting capabilities

– Train employees on expectations

– Measure and follow up on expectations

14

ACCOUNTING

MEASURING

PROFIT & LOSSSTATEMENT WITHBUDGET OVERVIEW

FOLLOW UP

15

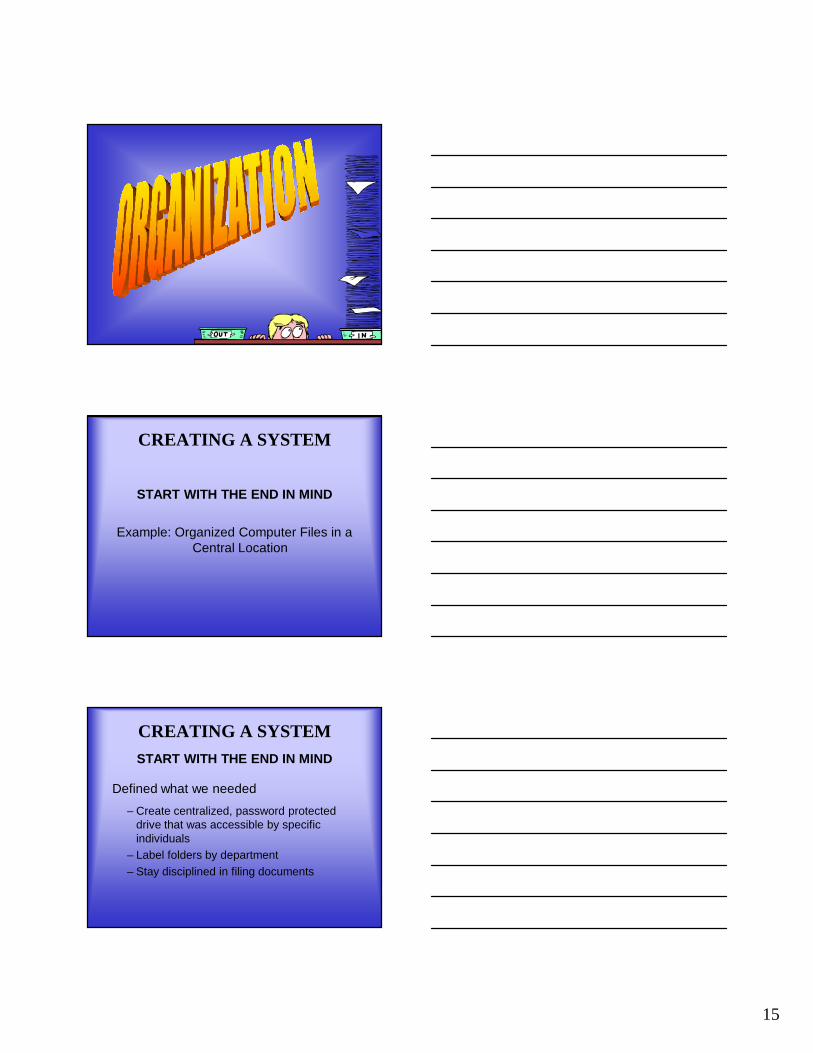

CREATING A SYSTEM

START WITH THE END IN MIND

Example: Organized Computer Files in aCentral Location

CREATING A SYSTEM

START WITH THE END IN MIND

Defined what we needed

– Create centralized, password protecteddrive that was accessible by specificindividuals

– Label folders by department

– Stay disciplined in filing documents

16

ADMINISTRATION

COMPUTER

My Documents

“Name of Company” Documents

Administration

Marketing

Technical

ADMINISTRATION

Drawer #1Accounts Payable

Drawer #2General Information

Drawer #3Employee Information

Hanging Folder - Administration

Manila Folder – Interviews

Manila Folder - Job Description

Manila Folder - Blank Evaluations

Hanging Folder - Marketing

Manila Folder - Salesperson Interviews

Manila Folder - Telemarketing Interviews

Manila Folder - Pay Rates

Hanging Folder - Technical

Manila Folder – Interviews

Manila Folder - Pay Rates

Hanging Folder – IRS

Manila Folder - General Information

Manila Folder - Blank W2

Manila Folder - Blank I9

Manila Folder - "Year" W3

Manila Folder - "Year" W4

Hanging Folder - Department of Labor

Manila Folder - General Information

Hanging Folder - Worker's Compensation

Manila Folder - General Information

Manila Folder – Rates

Manila Folder - Blank Forms

ADMINISTRATION

17

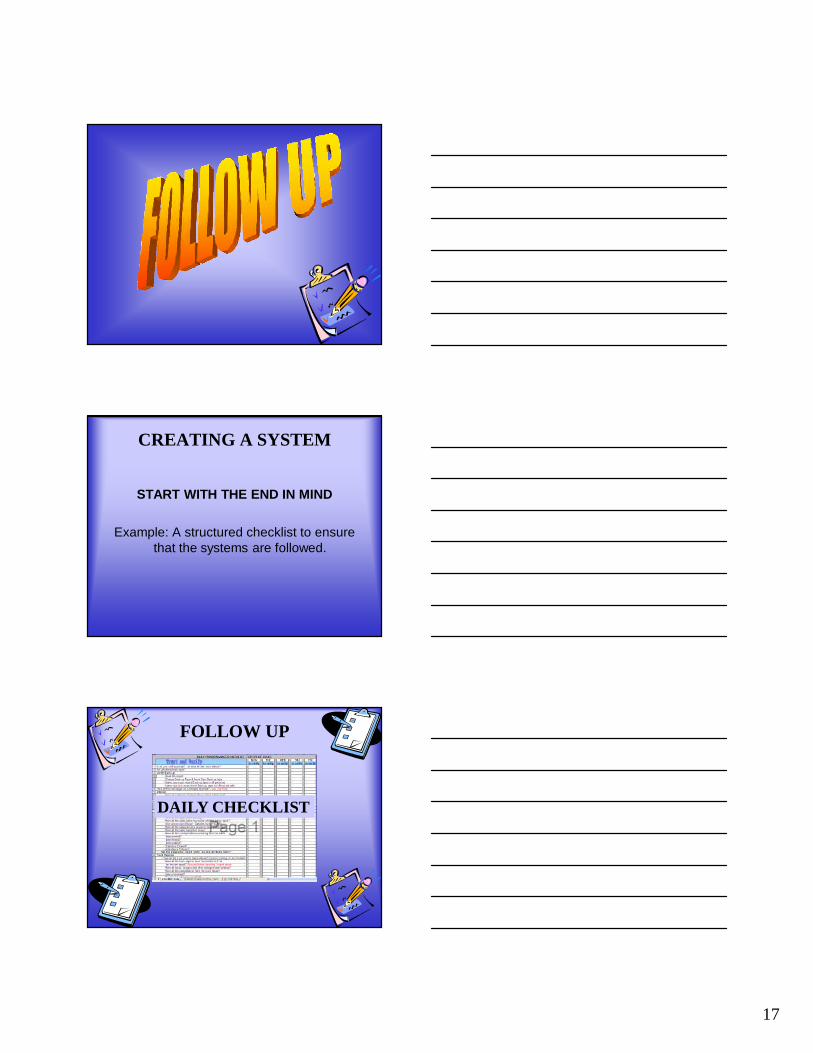

CREATING A SYSTEM

START WITH THE END IN MIND

Example: A structured checklist to ensurethat the systems are followed.

FOLLOW UP

DAILY CHECKLIST

18

FOLLOW UP

MONTHLY & YEARLYCHECKLIST

CREATING A SYSTEM

START WITH THE END IN MIND

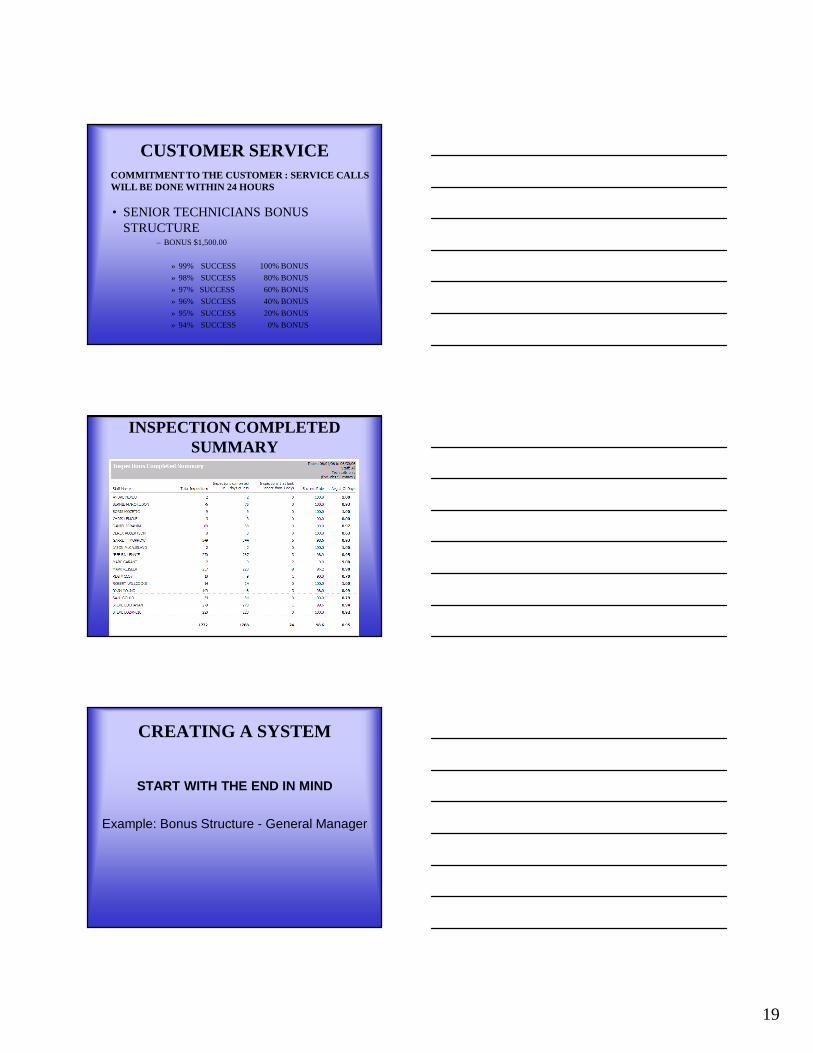

Example: Measuring Customer Serviceand rewarding for achieving our goal.

19

CUSTOMER SERVICE

• SENIOR TECHNICIANS BONUSSTRUCTURE

– BONUS $1,500.00

» 99% SUCCESS 100% BONUS

» 98% SUCCESS 80% BONUS

» 97% SUCCESS 60% BONUS

» 96% SUCCESS 40% BONUS

» 95% SUCCESS 20% BONUS

» 94% SUCCESS 0% BONUS

COMMITMENT TO THE CUSTOMER : SERVICE CALLSWILL BE DONE WITHIN 24 HOURS

INSPECTION COMPLETEDSUMMARY

CREATING A SYSTEM

START WITH THE END IN MIND

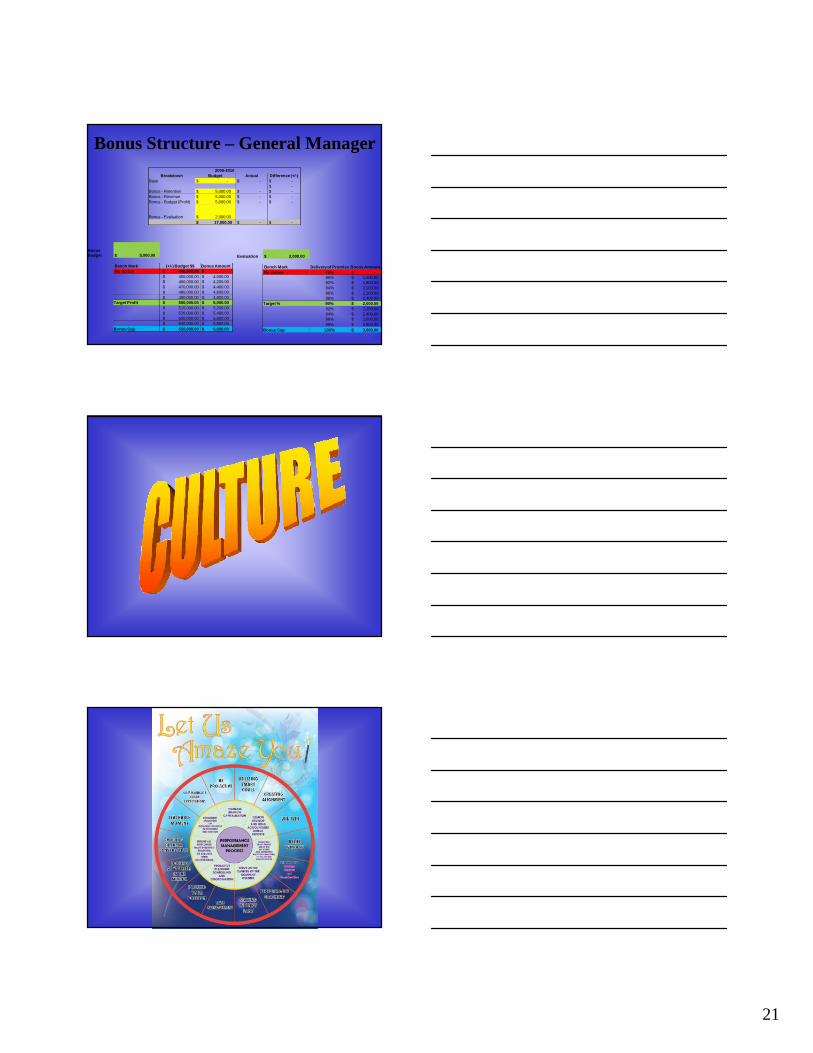

Example: Bonus Structure - General Manager

20

Bonus Structure – General Manager

• Currently many people rely on evaluations

Bonus Structure – General Manager

• Review Strategic Direction of Company

– Customer Service Oriented

– Growth

– Efficient Operations

– Cost Control

– Employee Personal Growth

Bonus Structure – General Manager2009-2010

Breakdown Budget Actual Difference (+/-)

Base $ - $ - $ -

$ -

Bonus - Retention $ 5,000.00 $ - $ -Bonus - Revenue $ 5,000.00 $ - $ -

Bonus - Budget (Profit) $ 5,000.00 $ - $ -

Bonus - Evaluation $ 2,000.00

$ 17,000.00 $ - $ -

BonusRetention $ 5,000.00

Bench Mark % Retention Bonus Amount

No Bonus 69% $ -70% $ 4,000.00

71% $ 4,200.00

72% $ 4,400.00

73% $ 4,600.0074% $ 4,800.00

Target % 75% $ 5,000.00

76% $ 5,200.0077% $ 5,400.00

78% $ 5,600.00

79% $ 5,800.00

Bonus Cap 80% $ 6,000.00

BonusRevenue $ 5,000.00

Bench Mark Budget $$ Bonus AmountNo Bonus $ 4,400,000.00 $ -

$ 4,500,000.00 $ 4,000.00

$ 4,600,000.00 $ 4,200.00

$ 4,700,000.00 $ 4,400.00$ 4,800,000.00 $ 4,600.00

$ 4,900,000.00 $ 4,800.00

Target Revenue $ 5,000,000.00 $ 5,000.00

$ 5,100,000.00 $ 5,200.00$ 5,200,000.00 $ 5,400.00

$ 5,300,000.00 $ 5,600.00

$ 5,400,000.00 $ 5,800.00

Bonus Cap $ 5,500,000.00 $ 6,000.00

Click HereFor

Spreadsheet

21

Bonus Structure – General Manager

2009-2010

Breakdown Budget Actual Difference (+/-)

Base $ - $ - $ -

$ -Bonus - Retention $ 5,000.00 $ - $ -

Bonus - Revenue $ 5,000.00 $ - $ -

Bonus - Budget (Profit) $ 5,000.00 $ - $ -

Bonus - Evaluation $ 2,000.00

$ 17,000.00 $ - $ -

BonusBudget $ 5,000.00

Bench Mark (+/-) Budget $$ Bonus Amount

No Bonus $ 440,000.00 $ -

$ 450,000.00 $ 4,000.00$ 460,000.00 $ 4,200.00

$ 470,000.00 $ 4,400.00

$ 480,000.00 $ 4,600.00

$ 490,000.00 $ 4,800.00Target Profit $ 500,000.00 $ 5,000.00

$ 510,000.00 $ 5,200.00

$ 520,000.00 $ 5,400.00

$ 530,000.00 $ 5,600.00$ 540,000.00 $ 5,800.00

Bonus Cap $ 550,000.00 $ 6,000.00

Evaluation $ 2,000.00

Bench Mark Deliveryof Promise Bonus Amount

No Bonus 79% $ -

80% $ 1,600.0082% $ 1,800.00

84% $ 2,000.00

86% $ 2,200.0088% $ 2,400.00

Target % 90% $ 2,000.00

92% $ 2,200.00

94% $ 2,400.0096% $ 2,600.00

98% $ 2,800.00

Bonus Cap 100% $ 3,000.00